Chapter 4 Analysis of Datashodhganga.inflibnet.ac.in/bitstream/10603/15088/8/09... · ·...

88

110 Chapter 4 Analysis of Data The chapter is covered as follows: 4.1 Analysis through Primary Data 4.1.1 Analysis of Questionnaire I for Regulators 4.1.2 Analysis of Questionnaire II for from professionals in banking and finance area 4.1.3 Analysis of Questionnaire III from Derivative traders 4.2 Analysis through Secondary Data 4.2.1 Comparison of NSE Nifty volatility- Pre and Post introduction of derivatives. 4.2.2 Price Discovery and volatility comparison 4.2.2.1 Data and Sample 4.2.2.2 Methodology of Analysis 4.2.2.3 Descriptive Statistics 4.2.2.4 Mates of the Index and Futures Returns 4.2.3 Comparison of impact cost at NSE This chapter is divided into analysis of information collected through Primary and Secondary Data. The first section analyzes data collected from Thomson Reuters and the National Stock Exchange. And the second section analyses information gathered through primary collection of data by administering questionnaire to various respondents in the Equity Derivative market. Derivative markets as discussed in chapter one functions for: • Risk Management • Price Discovery • Transactional Efficiency • Lower Volatility The use of financial derivatives help or aid in the price discovery process. It could facilitate reduction in transactional cost.

Transcript of Chapter 4 Analysis of Datashodhganga.inflibnet.ac.in/bitstream/10603/15088/8/09... · ·...

110

Chapter 4

Analysis of Data

The chapter is covered as follows:

4.1 Analysis through Primary Data

4.1.1 Analysis of Questionnaire I for Regulators

4.1.2 Analysis of Questionnaire II for from professionals in banking and finance area 4.1.3 Analysis of Questionnaire III from Derivative traders

4.2 Analysis through Secondary Data

4.2.1 Comparison of NSE Nifty volatility- Pre and Post introduction of

derivatives.

4.2.2 Price Discovery and volatility comparison

4.2.2.1 Data and Sample

4.2.2.2 Methodology of Analysis

4.2.2.3 Descriptive Statistics

4.2.2.4 Mates of the Index and Futures Returns

4.2.3 Comparison of impact cost at NSE

This chapter is divided into analysis of information collected through Primary and

Secondary Data. The first section analyzes data collected from Thomson Reuters and the

National Stock Exchange. And the second section analyses information gathered through

primary collection of data by administering questionnaire to various respondents in the

Equity Derivative market. Derivative markets as discussed in chapter one functions for:

• Risk Management

• Price Discovery

• Transactional Efficiency

• Lower Volatility

The use of financial derivatives help or aid in the price discovery process. It could

facilitate reduction in transactional cost.

111

4.1 Analysis through primary data.

4.1.1 Analysis of Questionnaire I for Regulators:

1. On query of whether the institutions monitor derivative trading, the institutions

replied:

SEBI: The SEBI has separate surveillance department Market Intermediaries

Regulation and Supervision Department comprising of around 30 to 40 personnel,

which monitors derivatives trading.

MCX: MCX monitors derivatives trading in Commodity Futures. NSE: NSE monitors derivative trading.

2. On query on the list of instruments allowed to trade in derivatives market,

SEBI responded:

SEBI: Stock option, stock future, index option, index future, currency future,

currency options and interest rates futures.

NSE: It has products like S&P CNX Nifty, Mini Derivative Contracts, CNXIT, Bank

Nifty, Nifty Midcap 50 and Individual securities.

3. How many audits do you perform in a year?

SEBI: All exchanges are inspected on a yearly basis.

MCX: MCX perform annual audits.

4. Do you train market participants in derivatives trading?

SEBI: No, training for the market participants in derivatives trading is carried out by

exchanges. However SEBI conducts periodic investors’ awareness programs and

programs for common people periodically.

112

MCX: Yes

NSE: Yes

5. How do you train derivative traders?

MCX: They are engaged in training market participants in derivative trading through

classroom training and literature/ pamphlet distribution.

NSE: NSE trains market participants and has large number of modules to offer. They

have classroom training methodology along with online examination system, which is

an ongoing activity.

6. How frequently? MCX: The periodicity of the training is monthly. NSE: Its an ongoing activity.

7. How do you enforce regulation compliance? SEBI: Market Intermediaries Regulation and Supervision Department enforces

compliance to regulations.

MCX: MCX enforce regulation compliance through periodic audits and collection of

compliance reports.

8. How many times do you carry out periodic audits?

MCX: MCX conduct the audit annually.

9. How many times in a year does a trader have to present a compliance report?

MCX: A trader at MCX has to submit a compliance report on an annual basis.

NSE: As an example the following Compliance Calendar has to be followed by the

members of the derivative segment.

113

Table 23: List of compliance calendar

What to Report When to Report Whom to Contact Circulars Dated

Activation / Deactivation of

Proprietary trading facility

Prior Approval required

Capital Market Trade

25th November 2008

23rd March 2010 Block Deal Execution

On the same day of trade

Capital Market Trade 25th November 2008

Bulk Deal Reporting

Single bulk deal immediately upon

the execution of the order. Cumulative

trades resulting in a bulk deal, within one

hour of closure of trading hours.

Capital Market Trade 25th November 2008

Application for providing IBT

Prior Approval required CTCL

12th May 2000 10th Nov 2006 6th Jun 2008

Submission of SSL certificate for IBT

Services By 31 July yearly CTCL 28th June 2006

System Audit Report By 31 July yearly CTCL 30th June 2009

Activation for CTCL /IBT for

ENIT

Prior Approval Required CTCL 25th Aug 2006

Advertisements (Rule (5) (h) of

Chapter IV of the Rules of the Exchange)

Advertisement to be submitted seven days in advance

before its publication. Written

permission to be obtained before

publication

Compliance 5th October 2009

Annual Returns Within 6 months from the end of accounting year

Compliance 7th Jun 2010

114

Appointment and change of

Compliance Officer

Intimation to Exchange Compliance 14th June 2002

Client wise Funding Report

Within seven days form the end

of the month Compliance

31st January 2007 19th December 2005

13th July 2005 19th December 2005

Internal Audit Report

Half yearly basis -Within 3 months from half year

ended March and September

Compliance

23rd April 2010

9th December 2009

Net worth certificate

Half yearly basis – within 3 months

from half year ending

Compliance 14th October 2009

Networth certificate in

Margin Trading for CM Segment

Within one month from the end of

half year Compliance

7th April 2004

7th April 2004

Proof of Insurance cover By July 31 yearly Compliance 10th May 2010

Client details for Margin Trading

facility

Before 9:00pm on the trade day Compliance

21st September 2006 11th March 2005 10th March 2005

9th September 2004 7th April 2004 7th April 2004 7th April 2004

Members trading through other

members

Intimation / Prior Approval required Compliance 22nd January 2004

Appointment of Authorized

personal in F&O segment

Prior Approval required. Membership 3rd December 2009

115

Change in address of member

Intimation to Exchange Membership

8th July 2004 4th October 2002

Change in designated directors

Prior Approval required Membership 13th August 2007

Change in non-designated directors

Fee Clearance from the

Exchange Membership 22nd January 2010

Change in name of member

Intimation to Exchange Membership 28th February 2008

Change in shareholding

Fee Clearance from the

Exchange Membership 22nd January 2010

Change in status and constitution

Prior Approval required Membership 25th July 2003

Increase in share capital

Fee Clearance from the

Exchange Membership 22nd January 2010

Upload of DMA IDs

Prior Approval required Membership 21st July 2008

Upload of CTCL IDs Activation / Deactivation /

Shifting of CTCL IDs

Prior Approval required Membership 25th September 2006

Pay in of Funds (CM)

On T+2 day by stipulated pay-in

time NSCCL – Funds 10th September 2009

Pay in of Funds (F&O)

On a T+1 day basis by

stipulated pay-in time

NSCCL – Funds 10th September 2009

Pay in of Funds (CDS)

Daily mark to market settlement

by 8:30 am on T+1 day

Final settlement by 8:30 am on

T+2 day

NSCCL – Funds 20th November 2008

Pay in of Funds (SLB)

On T+1 day by 9:30 am NSCCL – Funds 12th December 2008

Pay in of Funds (MFSS)

On the T+1 day by 8:30 a.m. NSCCL – Funds 24th November 2009

Client Margin Reporting

Within two days from trade date NSCCL - Risk 10th September 2009

116

Client Code Modification File

(CLD)*

Penalty Structure for Cld

modification

NSCCL - Securities 10th September 2009

On T day by 4.45 pm

NSCCL - Securities 10th September 2009

Client Direct Payout File (CPD)*

On T+2 day by 9.30 am

NSCCL - Securities 10th September 2009

Contraction of custodial Trades

file

DVP trades penalty , margins & exceptions for

same

NSCCL - Securities 10th September 2009

10. How many surprise checks do you carry out in a year?

MCX: MCX do not conduct any surprise checks/audits.

11. How many periodic meeting do you conduct with the traders and institutional

investors in a year?

SEBI: Meetings with the traders and institution investors are conducted whenever its

required and when they approach with issues which require SEBI intervention.

MCX: MCX meet traders and institutional investors once in a year.

12. What does the compliance report consist of?

SEBI: The compliance report mentions the volume of trading activity date and the

current positions.

MCX: The compliance report submitted by the trader includes compliance to

instructions and bye-laws as well as compliance to FMC circulars.

13. Does a trader have to be qualified for derivatives trading?

SEBI: A derivatives trader has to be qualified as per the exchanges compliance

exams. For example – NCFM exams being conducted by National Stock Exchange.

117

MCX: At MCX a trader need not be qualified for derivatives trading by may lose

permission to trade if his/her compliance is found not satisfactory.

14. How do you ensure compliance?

SEBI: Inputs are sort by different stake holders by way of suggestion, reviews. The

same if required to incorporated as regulation gets reviewed by the departmental head,

General Manager, Executive Director, Whole Time Member and then Chairman. Once

formulated the regulation is sent as a circular via letters and through website

information dissemination system.

15. How do you incorporate new regulations?

SEBI: Information is disseminated through the organizational official website. A

section disseminates all circulars which are to be made public

MCX: MCX incorporates new regulations through changes in the Bye-laws of the

exchange.

16. How do you ensure compliance on information dissemination?

MCX: Information dissemination is a voluntary activity by traders and is not

compelled.

17. How do you make investors aware of the risk involved in derivatives trading?

SEBI: Investors are provided with adequate literature on trading in various

instruments on the Stock Exchanges through pamphlets distribution, List of dos and

don’ts like signing on blank forms and applications and handing them to brokers

giving power of attorney to brokers etc.

MCX: MCX undertakes investor education and the KYC (Know Your Customer)

norms facilitate investors to understand the risk of investment and trading.

NSE: Professional Clearing Member (PCM)

118

The following persons are eligible to become PCMs of NSCCL for Futures & Options

and/or Capital Market Segment provided they fulfill the prescribed criteria:

• SEBI Registered Custodians; or

• Banks recognised by NSEIL/NSCCL for issuance of bank guarantees

Other Eligibility Criteria

At any point of time the applicant has to ensure that either the proprietor/one

designated director/partner or the Compliance Officer of the applicant entity should be

successfully certified either in Securities Market (Basic) Module or Compliance

Officers (Brokers) Module or the relevant module pertaining to the segments wherein

membership of the Exchange has been sought .i.e.

• Capital Market (Dealers) Module

• Derivatives Market (Dealers) Module

• National Institute of Derivatives Certification Examination

• Securities Markets (NISM) Series I – Currency

The above norm is a continued admittance norm for membership of the Exchange.

An applicant must be in a position to pay the membership and other fees, deposits etc,

as applicable at the time of admission within three months of intimation to him of

admission as a Trading Member or as per the time schedule specified by the

Exchange.

The Exchange may specify such standards for investor service and infrastructure with

regard to any category of applicants as it may deem necessary, from time to time.

18. How many companies approach SEBI for derivative trading?

SEBI: Companies approach exchanges for derivatives trading. All though final

approval is given by SEBI. Currently 202 companies are registered on NSE and 102

on BSE for trading in stock future and options.

119

19. How many listed companies (%) of the applied meet SEBI criteria in participating in

derivatives trading?

20. Do you collaborate with SEC?

SEBI: The SEBI collaborates with SEC and other international exchanges and other

security commissions through an association of regulators called as International

Organization of Securities Commissions (IOSCO).

MCX: The exchange does not collaborate with SEC or CFTC, but do track their

developments.

21. How much international exposure do you allow in derivatives trading?

SEBI: SEBI does not control international exposure of any trader in the international

markets. The same gets covered under FERA and FEMA which are governed by RBI.

There is no programmed interaction with RBI on these issues.

MCX: There is no exposure allowed in the derivative trades in the international

markets.

22. How is the red alert signaled?

MCX: The exchange ensures trading in stopped when a trader/investors approach

his/her position limit or prices start becoming volatile.

23. How do you monitor mark to market investors’ positions?

MCX: Positions of all traders are marked to market on a daily basis and accounts are

credited / debited accordingly.

24. How does SEBI monitor day to day trading pattern?

SEBI: Day to day trading patterns is monitored by the respective exchanges. SEBI

gets the report on the next day. There is a day’s lag in the same

120

MCX: The Forwards Market Commission (FMC) has the power to monitor daily

trading patterns and take preventive / penal action if unusual volatility is noted in the

prices.

25. How do you penalize non- compliance?

SEBI: If after analysis SEBI finds and non compliance and unusual pattern in trading,

it ceases the demat accounts and terminals of the default traders also results into

blocking of trading and barring the person on entering the market. Along with

imposing monitory penalties if required.

MCX: Any non-compliance by the traders is penalized by issuing warnings or

cancelling the licenses to trade.

26. Do you think a separate exchange for derivative trading should be established?

SEBI: As far as the functioning of exchanges are proving to be satisfactory, a need to

open a separate exchange may not be desired.

MCX: MCX is not of the opinion to establish a separate derivative exchange.

27. If yes, why do you think so?

SEBI: The desire to open new derivative exchange would not arise if the functioning

between the cash market and derivatives market are realistic and efforts being

coordinated for creation of an efficient market system.

28. How frequently do you introduce new products in the Derivatives Market?

SEBI: Whenever there is a mandate to introduce a new derivative product SEBI

considers it and introduces it after due diligence. SEBI follows the conservative

approach regarding introducing new products.

121

MCX: There is no fixed pattern of introduction of new products in the derivatives

market. It depends on the market demand.

29. Do you think Indian Financial System is matured enough to adapt to exotic products

in Derivatives?

SEBI: The Indian financial system is not matured enough to absorb exotic and

advance products in derivatives. The investors are not aware of the usage and

advantages of trading in these products. For example – An interest rate future product

was introduced last year but finds no takers, there is no liquidity in the market and the

market is unable to understand its complexities. Derivatives trading in stocks are not

allowed to be traded in OTC but only in exchanges. Only interest rate and currency

rate derivatives trading is allowed under OTC which is governed by RBI. The trading

in same is very small in exchanges.

MCX: Though it’s of the opinion that Indian Financial System is matured enough to

adapt to exotic products in Derivatives under the guidance and strict monitoring by

the regulator.

30. Why?

SEBI: As stated question no. 29.

31. Has any trader/broker defaulted?

SEBI: There has been no default in the equity derivative segment.

MCX: There have been default cases by traders in MCX against whom action has

been taken.

32. Have you taken any action on the defaulted trader/ broker?

NSE: Yes

33. If yes, then how many?

122

MCX: The number of defaulters is not revealed due to non-disclosure norms of the

exchange.

34. On what grounds have the traders/ brokers defaulted?

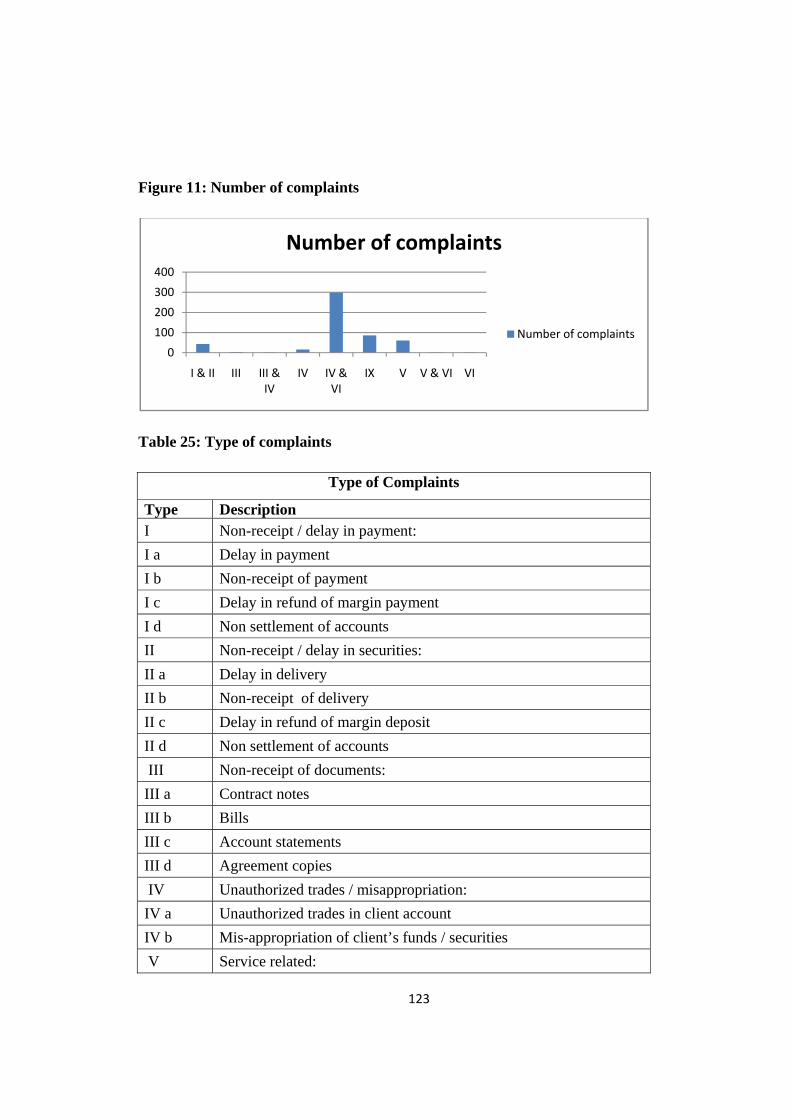

NSE: There were 1035 active members during January 2011 in the Futures and

Options (F & O) Segment. There were 1116 active members during January 2011 in

the Cash segment. Following is the complaint status against F & O trading members

as on 3rd December 2010.

• Non- Actionable: 13

• Opted for Arbitration: 67

• Resolved status: 428

• Under Process- 6

Interestingly the exchange received complaints against almost 50% of the members. The

above status does confirm the efficient grievance redress mechanism of NSE. 98 % is the

resolved rate.

Following are the type of complaints:

Table 24: Number of complaints

Type of complaints

Number of complaints %

I & II 43 8.37

III 3 0.58

III & IV 2 0.39

IV 16 3.11

IV & VI 299 58.17

IX 86 16.73

V 61 11.87

V & VI 2 0.39

VI 2 0.39

Total 514 100.00

123

Figure 11: Number of complaints

Table 25: Type of complaints

Type of Complaints

Type Description I Non-receipt / delay in payment: I a Delay in payment I b Non-receipt of payment I c Delay in refund of margin payment I d Non settlement of accounts II Non-receipt / delay in securities: II a Delay in delivery II b Non-receipt of delivery II c Delay in refund of margin deposit II d Non settlement of accounts III Non-receipt of documents: III a Contract notes III b Bills III c Account statements III d Agreement copies IV Unauthorized trades / misappropriation: IV a Unauthorized trades in client account IV b Mis-appropriation of client’s funds / securities V Service related:

0

100

200

300

400

I & II III III & IV

IV IV & VI

IX V V & VI VI

Number of complaints

Number of complaints

124

V a Excess brokerage V b Non-execution of order V c Wrong execution of order V d Connectivity / system related problem V e Non-receipt of corporate benefits V f Other service defaults VI Closing out / squaring up: VI a Closing off / squaring up position without consent VI b Dispute in Auction value / close out value VII Non implementation of arbitration award VIII IPO related IX Others

Table 26: Status of the complaints

Status

Type Description

I Non actionable

I a Complaint incomplete

I b Outside the scope of stock exchange

II Resolved

III Under Process

IV Referred to Arbitration

58% complaints are related to unauthorized trade and service related, of which 83% are

resolved, rest 1% is in process and 15% cases opt for arbitration. Which shows that the

exchange is quite efficient is handing disputes and has a control on the defaults by the

members.

MCX: The defaults are due to Business and Market malpractices and delivery

defaults.

35. What actions do you normally take on the default by the traders/ brokers?

SEBI: As per the gravity of the default.

125

36. Do you have a mechanism to monitor high performance individuals/ traders/ brokers?

MCX: MCX has mechanism to monitor high performance individual / traders /

brokers which are monitored by positions relative to the market and open positions.

37. If yes, then how do you monitor high performance individuals/ traders / brokers?

38. Are there any regulatory concerns to be addressed in the near future?

SEBI: Yes

MCX: Yes

39. If yes, then what?

SEBI: Investors and market maturity is a prime concern for SEBI. Introducing new

products in the market and finding takers also is a concern which has to be addressed.

Separate membership for separate class of product has to be taken by the trade

members. For example – separate membership for currency, equity and interest

derivatives trading has to be sought. The policy and regulations of SEBI are framed in

such a way that it ensures proper collection of margins and conservative approach in

introducing derivative products so that they are suitable for investors across the

sections included retail investors and they are introduced only if the markets are ready

to absorb them. SEBI also tries to ensure that their policies and regulations bring in an

overall efficiency in the market. Before launching a product adequate quantitative

analysis is done and theoretical simulations are conducted to ensure adequate

collection of margins and proposing desired margins and networth by the traders /

brokers / dealers.

SEBI does not have any control over exposure of Banks in foreign markets since they

come under the purview of RBI.

MCX: According to the exchange, there are regulatory concerns to be addressed in

126

the near future which are; that the market is governed by an archaic law which need to

be amended so that the regulator gets more power and autonomy, more products are

permitted in the market, more participants, such as financial institutions, which are

currently disallowed, are permitted in the market.

4.1.2 Analysis Questionnaire II for professionals in banking and finance area:

Analysis of the responses from professionals working in the banking and finance segment

has been summarized as below:

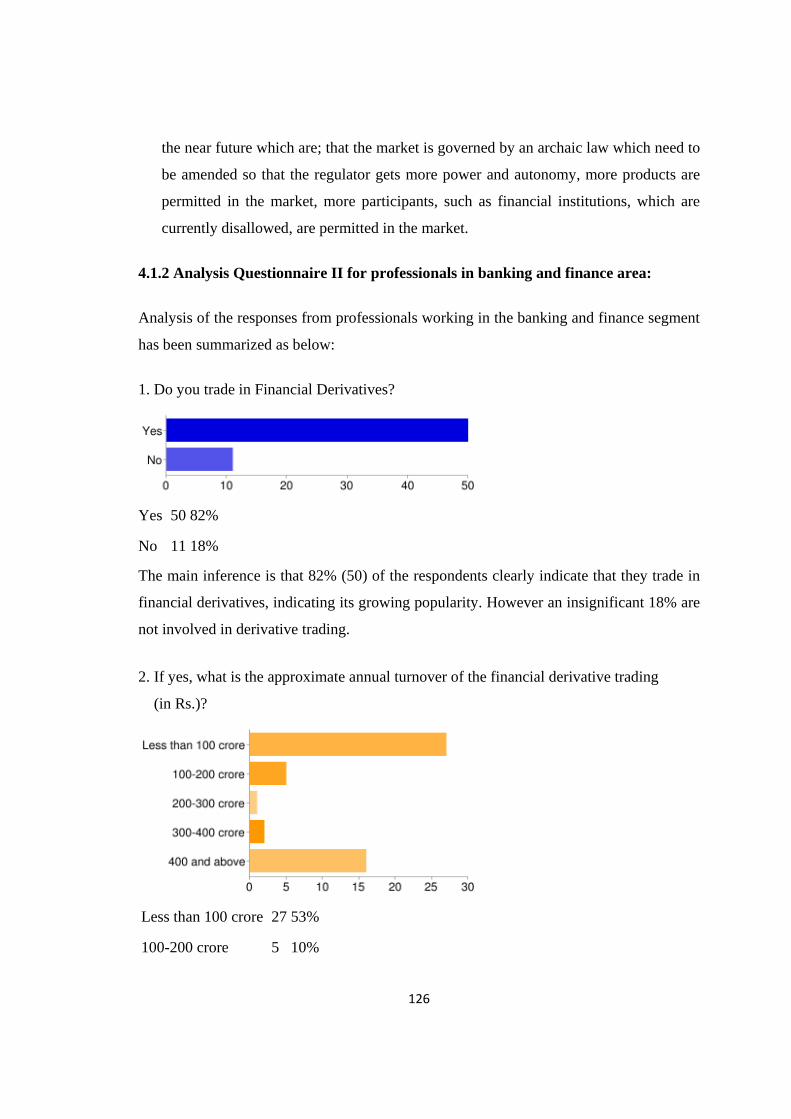

1. Do you trade in Financial Derivatives?

Yes 50 82%

No 11 18%

The main inference is that 82% (50) of the respondents clearly indicate that they trade in

financial derivatives, indicating its growing popularity. However an insignificant 18% are

not involved in derivative trading.

2. If yes, what is the approximate annual turnover of the financial derivative trading

(in Rs.)?

Less than 100 crore 27 53%

100-200 crore 5 10%

127

200-300 crore 1 2%

300-400 crore 2 4%

400 and above 16 31%

In connection with the above question, it has been noted that even though 53% (27) of the

respondents have shown an annual turnover of their financial derivative trading,

comprising less than Rs. 100 crore, it is still noteworthy to find that 31% (16) of the

respondents have indicated their annual turnover of Rs. 400 crore and more. Respondents

trading more than Rs. 400 crore comprise of large investment banks and asset

management companies. Respondents trading in less than Rs. 100 crores comprise of

traders and brokerage firms. Investment banks and other financial institutions trading in

high volumes are more likely to influence and get affected by the market movements.

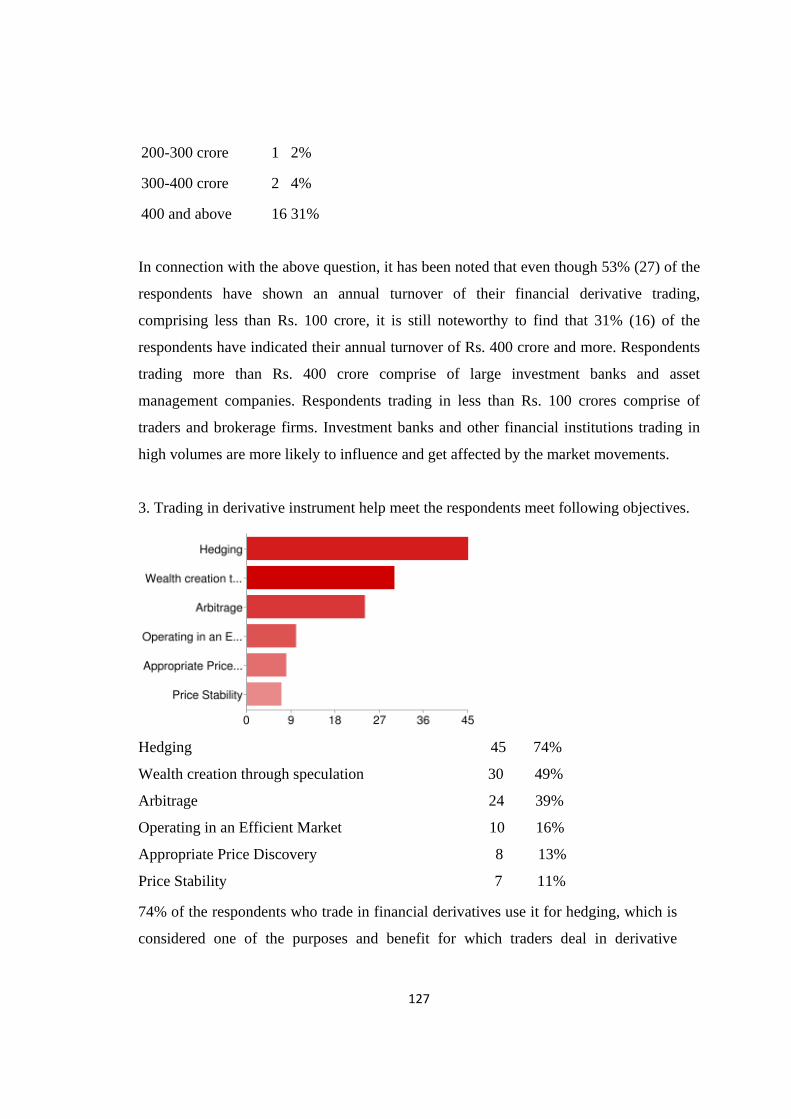

3. Trading in derivative instrument help meet the respondents meet following objectives.

Hedging 45 74%

Wealth creation through speculation 30 49%

Arbitrage 24 39%

Operating in an Efficient Market 10 16%

Appropriate Price Discovery 8 13%

Price Stability 7 11%

74% of the respondents who trade in financial derivatives use it for hedging, which is

considered one of the purposes and benefit for which traders deal in derivative

128

instrument. This also helps us in proving our hypothesis that the functioning of

derivative market is effective. The L C Gupta committee report also indicated that

majority (69.64%) of respondents prefer to enter the derivative market as hedgers.

49% of the respondents benefit in creating wealth through speculation, which also is a

positive sign since markets are made by speculators. 39% use the opportunity of

difference in the prices in the cash market and derivative market as an arbitrage

opportunity. 13% view derivative market as a price discovery opportunity. One of the

theories for an efficient derivative market is a price discovery process. Merely 11%

feel that they look up to derivative market for price stability benefits since the stock

market is a highly volatile and speculative market.

4. The Indian Financial System is efficient and robust.

1 0 0%

2 5 8%

3 22 36%

4 24 39%

5 9 15%

A substantial number of respondent (33) 54% feel that the Indian financial system is

efficient and robust. This inference is considered important since our hypothesis

states that the functioning of our derivative market is effective. Unless a country’s

financial system is efficient and effective, its financial bodies, systems, procedures

and markets may not be considered effective and efficient. This also indicates that

the stake holders have faith in the financial system of India. 36% (22) do not commit

towards commenting on the status of Indian financial system. Either they might

view full potential of Indian financial system emerging in near future or they might

129

feel that the current financial system could be over hauled to reach its full

potentiality. Only 8% (5) of the respondents do not show confidence in the Indian

financial system, which is very miniscule and could be ignored for data analysis.

5. Inefficient Derivative Markets would highly impact the Indian Financial System.

1 3 5%

2 3 5%

3 11 18%

4 19 31%

5 25 41%

72% (44) respondents feel that an inefficient derivative market would highly impact

the Indian financial system. 18% (11) took a neutral stand and would not like to

comment on its impact on the Indian financial system. This could be due to lack of

sufficient data in hand to comment. 8% (6) do not agree that an inefficient derivative

market would highly impact the Indian financial system.

A considerable number of respondents (72%) do feel and are aware of the high risk

and high impact of trading in derivatives. Hence we find that there has been a

considerable caution adopted by Indian regulators to develop and grow derivative

markets in India. Cautious tendencies while introducing a new derivative product,

high margins systems, marked to market profit and losses and a strong exchange

level ombudsman to resolve complaints and disputes with respect to derivative

trading indicate regulator’s commitment to develop the market effectively and

efficiently. All though Indian derivative markets have developed exponentially over

130

the last decade since its introduction in 2000, we have observed that it has been well

regulated without any major crises or defaults in the market. A Chi-square test was

administered to validate the finding, with the Pearson Chi-Square value of 17.733a

which is more than the table value.

A Chi-square test was administered to validate the finding. Although a good

number of respondents (72%) feel that inefficient Derivative Markets would

highly impact the Indian Financial System, the same is also statistically validated

as Pearson Chi-Square value of 31.213b is more than the table value at 95%

confidence interval. It gives us an indication that the Indian financial markets may

have a strong faith in the Indian financial system and the size of the Indian

derivative markets currently witnessed, may affect the functioning of the same.

Test Statistics

4. The Indian Financial

System is efficient and

robust.

5. Inefficient Derivative Markets would highly impact the Indian

Financial System.

17.733a 31.213b

3 4

.000 .000

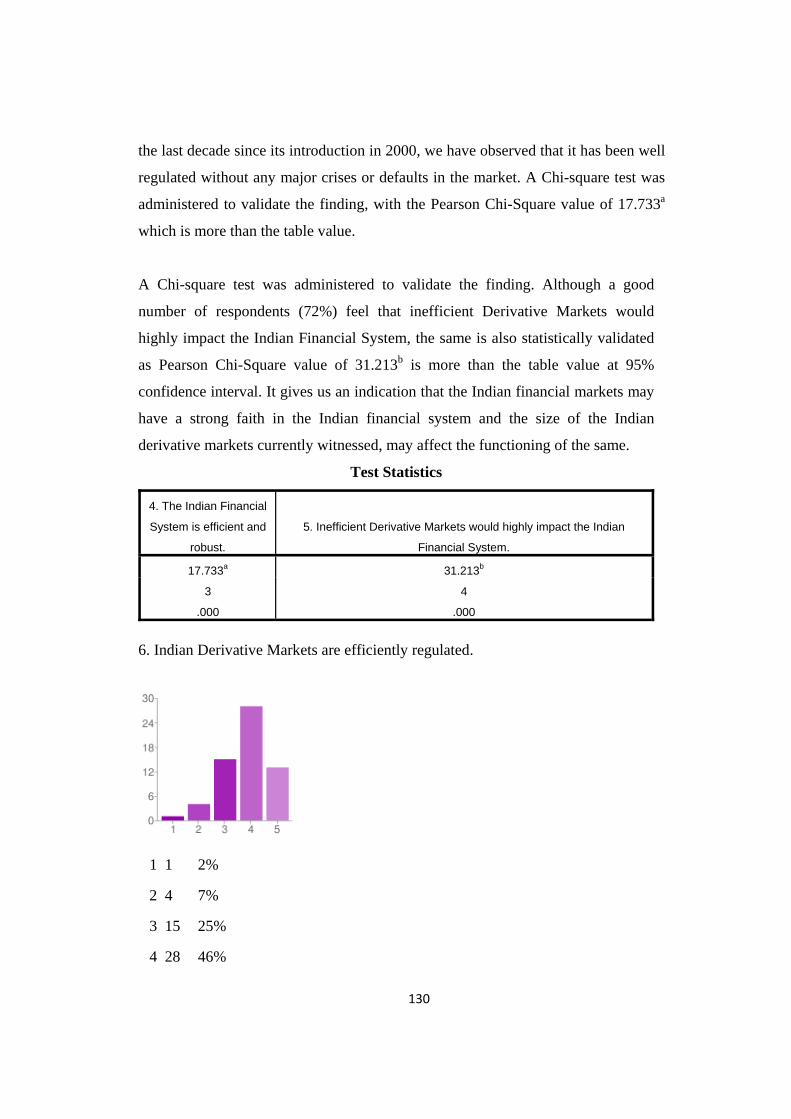

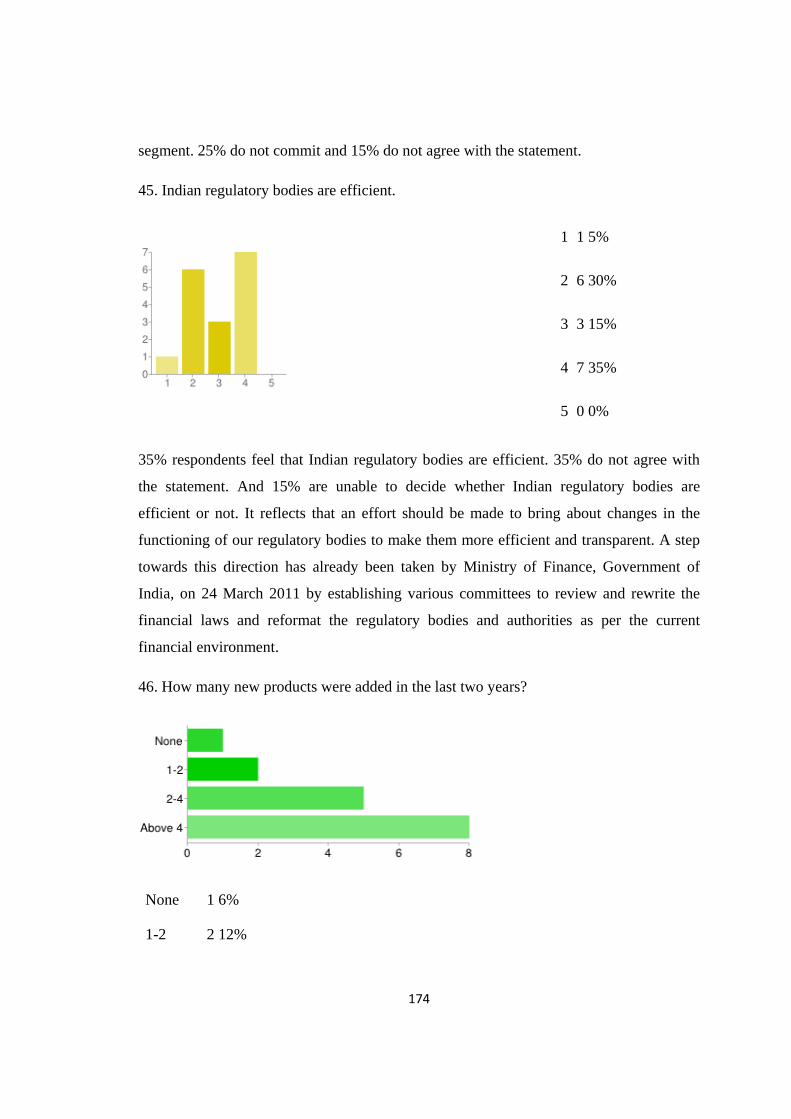

6. Indian Derivative Markets are efficiently regulated.

1 1 2%

2 4 7%

3 15 25%

4 28 46%

131

5 13 21%

67% (41) respondents feel that Indian derivative markets are efficiently regulated. 25%

(15) would not like to comment on the deficiency of the Indian regulators in regulating

our financial markets. A small percentage of 9% (5) respondents feel that Indian

derivative markets are not efficiently regulated. A comparatively high degree of non

committed respondents (25%) might have maintained their status / opinion due to few

financial crises in the Indian stock market which the Indian financial regulators might

have failed to prevent and control. But a lot of water has flown under the bridge since

then. Our financial regulators have evolved, matured and have developed some very

strong systems to curb unnatural tendencies in the market. The regulators also have been

swift in taking actions against the defaulters.

A Chi-square test was administered to validate the finding. A good number of respondents

(67%) feel that Indian Derivative Markets are efficiently regulated, the same is also

statistically validated as Pearson Chi-Square value of 36.951b which is more than the table

value at 95% confidence interval. Although the Chi- square value is high, an effort to

increase confidence and positive feedback by bringing in more efficiency in the market

could be undertaken. Descriptive Statistics

N Mean Std.

Deviation

Minimum Maximum

4. The Indian Financial

System is efficient and

robust.

60 3.62 .846 2 5

6. Indian Derivative

Markets are efficiently

regulated.

61 3.79 .915 1 5

132

Test Statistics

4. The Indian Financial

System is efficient and

robust.

6. Indian Derivative Markets are efficiently

regulated.

Chi-Square 17.733a 36.951b

df 3 4

Asymp. Sig. .000 .000

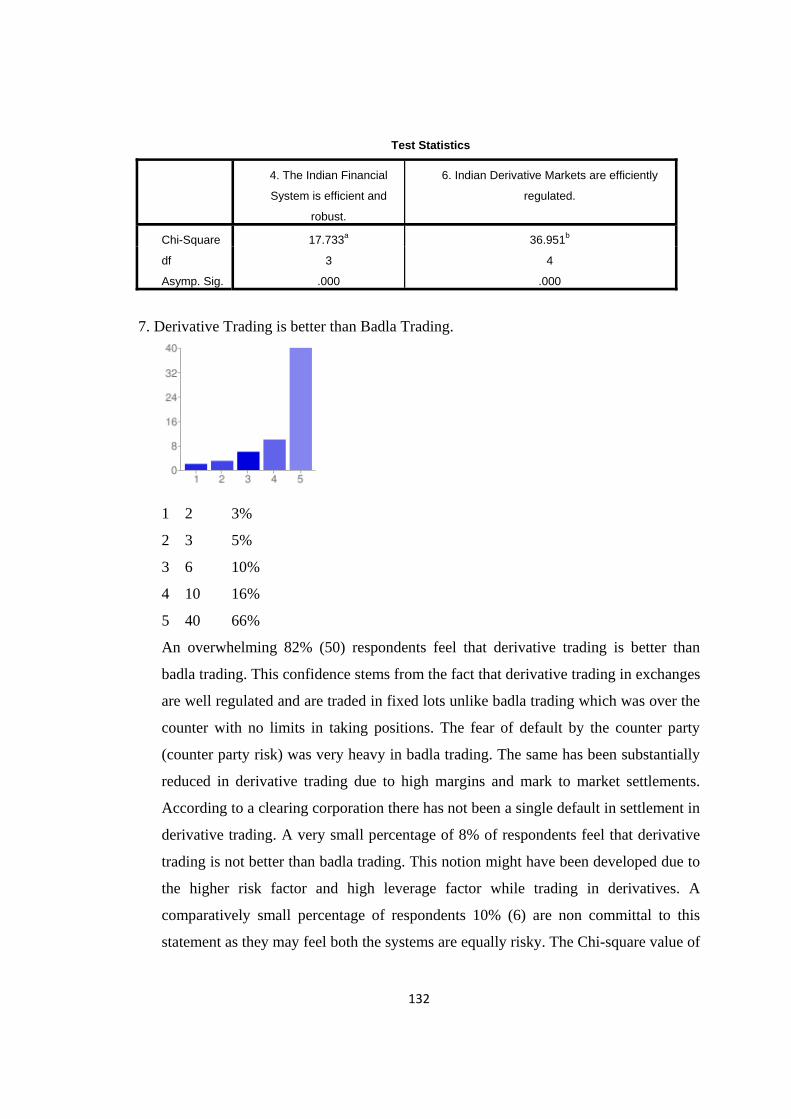

7. Derivative Trading is better than Badla Trading.

1 2 3%

2 3 5%

3 6 10%

4 10 16%

5 40 66%

An overwhelming 82% (50) respondents feel that derivative trading is better than

badla trading. This confidence stems from the fact that derivative trading in exchanges

are well regulated and are traded in fixed lots unlike badla trading which was over the

counter with no limits in taking positions. The fear of default by the counter party

(counter party risk) was very heavy in badla trading. The same has been substantially

reduced in derivative trading due to high margins and mark to market settlements.

According to a clearing corporation there has not been a single default in settlement in

derivative trading. A very small percentage of 8% of respondents feel that derivative

trading is not better than badla trading. This notion might have been developed due to

the higher risk factor and high leverage factor while trading in derivatives. A

comparatively small percentage of respondents 10% (6) are non committal to this

statement as they may feel both the systems are equally risky. The Chi-square value of

133

82.361b is considerably high than the table value, which shows that the Indian stock

markets has taken to derivative trading over badla trading positively.

Descriptive Statistics

N Mean Std.

Deviation

Minimum Maximum

4. The Indian Financial

System is efficient and

robust.

60 3.62 .846 2 5

7. Derivative Trading is

better than Badla

Trading.

61 4.36 1.065 1 5

7. Derivative Trading is better than Badla Trading.

Observed N Expected N Residual

1 2 12.2 -10.2

2 3 12.2 -9.2

3 6 12.2 -6.2

4 10 12.2 -2.2

5 40 12.2 27.8

Total 61

Test Statistics

4. The Indian Financial System is

efficient and robust.

7. Derivative Trading is better than

Badla Trading.

Chi-Square 17.733a 82.361b

df 3 4

Asymp. Sig. .000 .000

8. Derivative Trading has resulted in exposure to high risk.

134

1 2 3%

2 10 16%

3 16 26%

4 18 30%

5 15 25%

55% (33) respondents feel that trading in derivatives is a very risky proposition. This may

be due to volatility and booking of mark to market profit and losses. A downward market

forces a trader or an investor to deposit the deficit in cash or near cash instruments with

the clearing corporation on the same day. This requires a substantial financial holding

capacity in the futures market. Also derivative trading is a high leveraged form of trading

with no exchange or settlement in the shares in which the trader or the investor has

invested his money. The settlement is purely done in cash. Unlike the cash market where

the settlement takes place with an exchange of money with the underlying assets (shares).

19% (12) do not feel that derivative trading results into exposure to high risk. This could

be applicable to exchange regulated derivative trading as they are highly regulated with

strict entry and exist barriers. 26% (16) would not like to comment on its riskiness and

may would rather wait and watch the performance of derivative markets in the near future

to form an opinion whether they are risky or not.

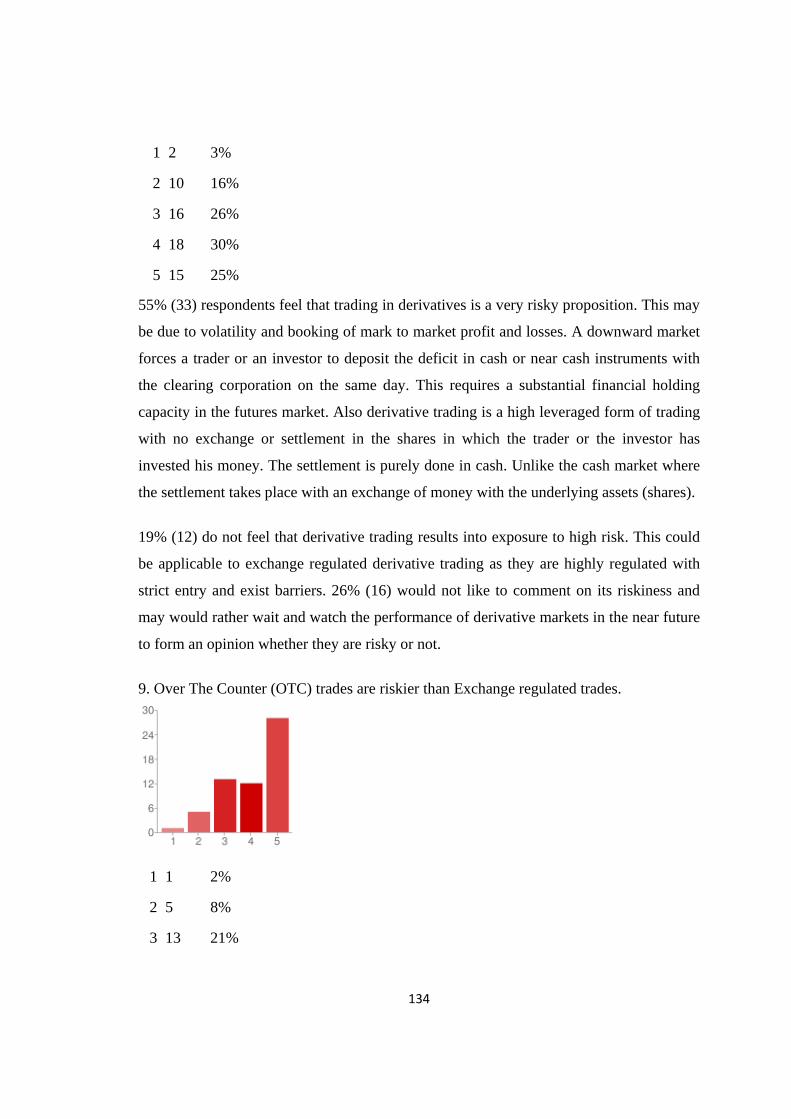

9. Over The Counter (OTC) trades are riskier than Exchange regulated trades.

1 1 2%

2 5 8%

3 13 21%

135

4 12 20%

5 28 46%

66% (40) respondents feel that over the counter trades are riskier than exchange regulated

trades. Hence we observe that in India the equity financial derivative products are quite

basic and are exchange regulated for e.g. index futures, stock futures, index options, stock

options etc. The Indian banking system is no hurry in introducing highly complicated and

complex products like the CDOs and the CDS which are primarily over the counter

derivative products. The Indian financial system / regulators are quite aware of the risk

and complexity involved in trading in such products. The recent sub-prime crises in US in

2007 have made financial regulators over the world more cautious in experimenting with

introduction of highly exotic derivatives products. There is a high degree of counter party

risk in over the counter trading unlike an exchange trading where the counter party risk is

considerably lower due to various measures adopted by the exchange and clearing

corporations to honor the commitments. However a small percentage of respondents

(10%), (6) do not feel that trading in OTC is riskier than exchanges. These respondents

are highly optimistic and may believe in a highly liberalized open market system. 21%

respondents do not wish to comment as they might not have experienced risk in OTC

trades, which is not allowed in India. Hence they may want to reserve their comments till

they experience any crises either in the OTC market or in the exchange regulatory market.

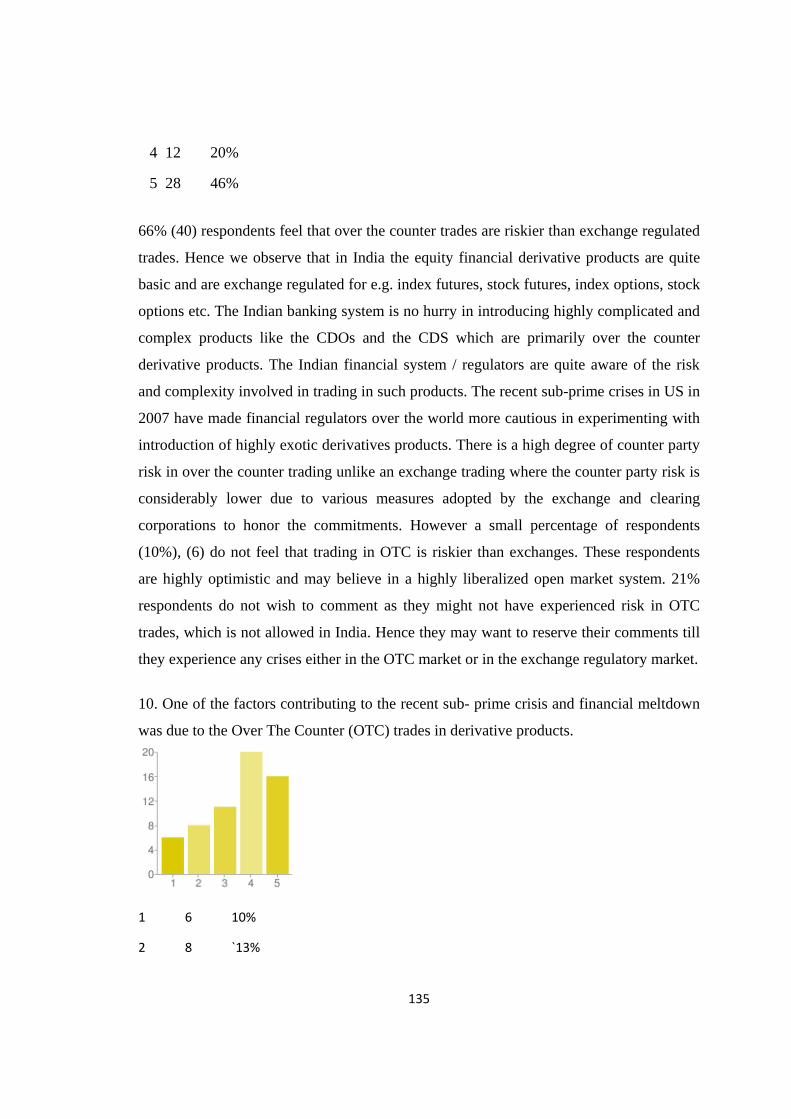

10. One of the factors contributing to the recent sub- prime crisis and financial meltdown

was due to the Over The Counter (OTC) trades in derivative products.

1 6 10%

2 8 `13%

136

3 11 18%

4 20 33%

5 16 26%

69% (36) of the respondents feel that one of the factors contributing to the recent sub-

prime crisis and financial meltdown was due to the Over The Counter (OTC) trades in

derivative products. CDOs and CDS which were highly unregulated over the counter

products triggered the crises due to default by counter parties to the contracts. 23% (14)

do not feel that the subprime crises were a result of the use of OTC derivative product. In

fact their observation is that the crises was due to the erosion of faith and trust in the

whole banking system of the United States of America. The normal practice of interbank

lending and borrowing collapsed due to lack of faith and trust amongst the big bankers.

About 18% (11) respondents are non committal due to the multiple factors which really

created the crises in 2007. Fall of real estate prices worsening, condition of US state

economy and factors like use of uncontrolled plastic money and subsequent defaults, high

trade deficits etc. had already bled the US banking / financial system.

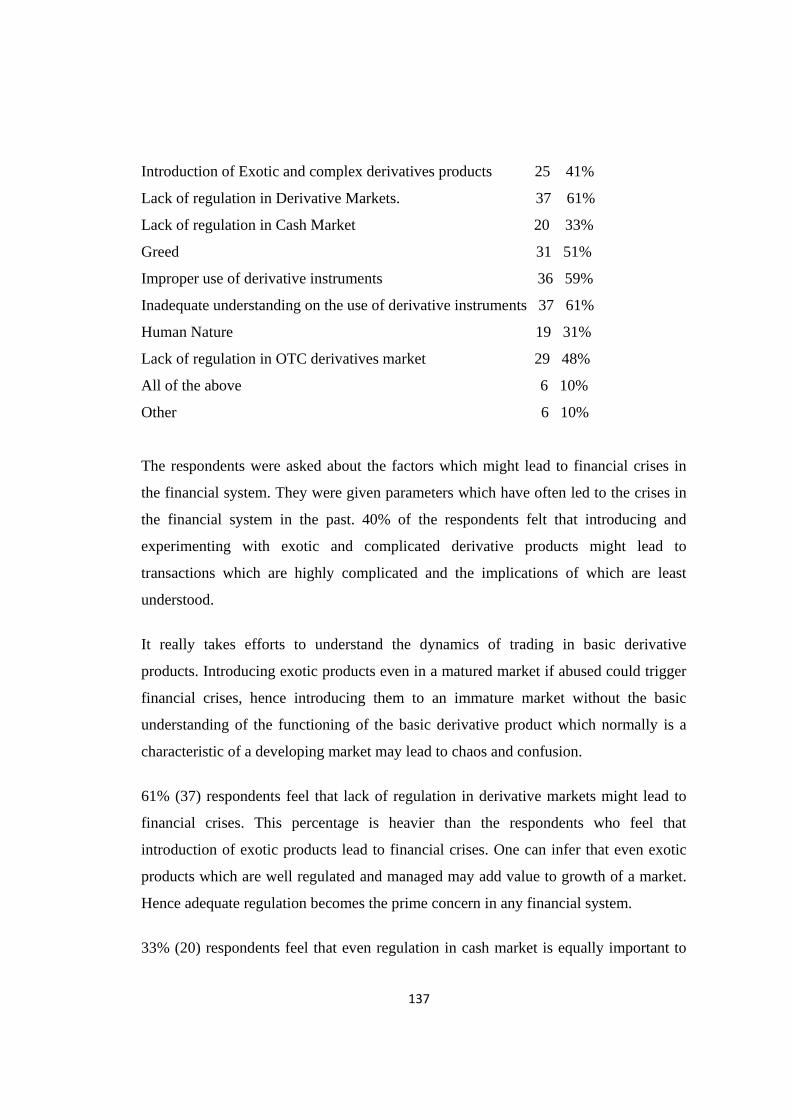

11. What could be the factors from the following which may lead to financial crisis?

137

Introduction of Exotic and complex derivatives products 25 41%

Lack of regulation in Derivative Markets. 37 61%

Lack of regulation in Cash Market 20 33%

Greed 31 51%

Improper use of derivative instruments 36 59%

Inadequate understanding on the use of derivative instruments 37 61%

Human Nature 19 31%

Lack of regulation in OTC derivatives market 29 48%

All of the above 6 10%

Other 6 10%

The respondents were asked about the factors which might lead to financial crises in

the financial system. They were given parameters which have often led to the crises in

the financial system in the past. 40% of the respondents felt that introducing and

experimenting with exotic and complicated derivative products might lead to

transactions which are highly complicated and the implications of which are least

understood.

It really takes efforts to understand the dynamics of trading in basic derivative

products. Introducing exotic products even in a matured market if abused could trigger

financial crises, hence introducing them to an immature market without the basic

understanding of the functioning of the basic derivative product which normally is a

characteristic of a developing market may lead to chaos and confusion.

61% (37) respondents feel that lack of regulation in derivative markets might lead to

financial crises. This percentage is heavier than the respondents who feel that

introduction of exotic products lead to financial crises. One can infer that even exotic

products which are well regulated and managed may add value to growth of a market.

Hence adequate regulation becomes the prime concern in any financial system.

33% (20) respondents feel that even regulation in cash market is equally important to

138

avoid any financial crises in the system. Few crises in the cash market which occurred

with Indian stock market could be a setting example for us to be highly vigilant in the

cash market as well.

50% of the respondents feel that human greed has a capacity to discount and debunk

even an adequately regulated market. Individual greed has played a considerable part in

demolishing the mightiest and wealthiest of the financial institutions around the world.

Many examples have been discussed in chapter no. 2 where human greed has managed

to beat the systems which have been functioning for decades in the past.

12. What could be the factors from the following which may have lead the financial crisis

due to derivatives trading in the past?

Introduction of Exotic and complex derivatives products 25 41%

Lack of regulation in Derivative Markets. 37 61%

Lack of regulation in Cash Market 16 26%

Greed 28 46%

Improper use of derivative instruments 39 64%

Inadequate understanding on the use of derivative instruments 39 64%

Human Nature 14 23%

139

Lack of regulation in OTC Derivatives Market 25 41%

All of the above 6 10%

64% (39) respondents strongly feel that financial crises in the past have been lead by

improper use of derivative instruments. Equal number of respondent feel that inadequate

understanding of derivative instruments have lead to financial crises.

A very recent example in India (news on CNBC TV18 on 26th April 2011,

http://www.moneycontrol.com/video/cnbc-tv18-comments/rbi-penalises-19-banks-for-

violating rulesderivatives_538495.html?utm_source=Article_Vid) has reported fining of

19 national and multinational banks from Rs. 5 lakhs to Rs. 15 lakhs for selling derivative

products to companies which they could not understand and suffered huge losses in 2007

financial crises. The products were banned by RBI hence.

61% (37) feel that lack of regulation in derivative markets have lead to financial crises in

the past. My study of the regulatory structure of Indian derivative (equity) market is based

on this apprehension. 46% (28) feel that greed too played a role in creating crises in the

past.

41% (25) respondents feel that introduction of exotic and complex products failed to be

understood by the markets and market participants lead to financial crises. Equal number

of respondents feel that lack of regulation in over the counter markets have lead to

financial crises. Since these transactions are not standardized, the signs of financial crises

approaching could be missed or misjudged. Hence we find that Indian regulator has taken

considerable lessons from the western countries and have always shown restraint while

introducing a new derivative product. Although over the counter transactions are allowed

in currency markets there has been an attempt by the regulator (RBI) to make them

exchange traded. The recent opening of currency exchange known as the United Stock

Exchange is a step towards this direction. Although only 5% of (Rs. 6000 crores) worth of

trades are conducted on the exchange, it might slowly grow as one of the well developed

currency exchange in the future. MCX and NSE also trade in currency futures. Human

nature (23% - 14) and lack of regulation in cash market (26%-16) comprise of the

140

remaining respondent choices which might have lead to financial crises in the past.

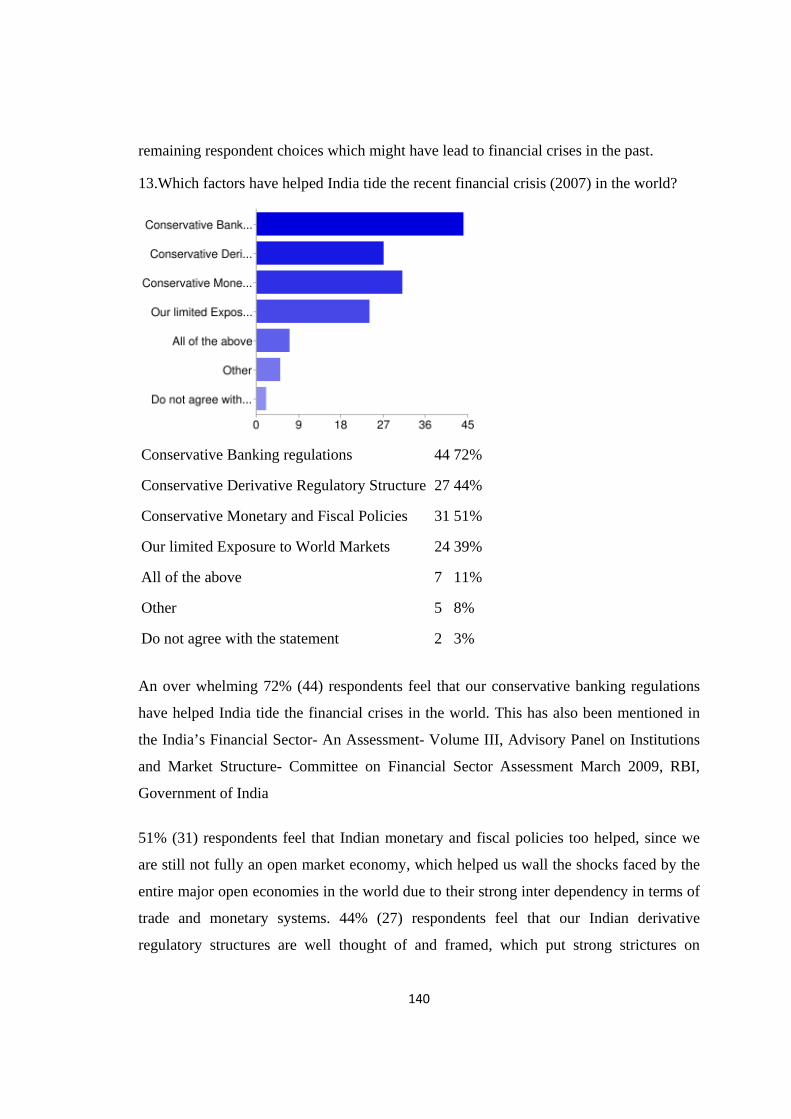

13.Which factors have helped India tide the recent financial crisis (2007) in the world?

Conservative Banking regulations 44 72%

Conservative Derivative Regulatory Structure 27 44%

Conservative Monetary and Fiscal Policies 31 51%

Our limited Exposure to World Markets 24 39%

All of the above 7 11%

Other 5 8%

Do not agree with the statement 2 3%

An over whelming 72% (44) respondents feel that our conservative banking regulations

have helped India tide the financial crises in the world. This has also been mentioned in

the India’s Financial Sector- An Assessment- Volume III, Advisory Panel on Institutions

and Market Structure- Committee on Financial Sector Assessment March 2009, RBI,

Government of India

51% (31) respondents feel that Indian monetary and fiscal policies too helped, since we

are still not fully an open market economy, which helped us wall the shocks faced by the

entire major open economies in the world due to their strong inter dependency in terms of

trade and monetary systems. 44% (27) respondents feel that our Indian derivative

regulatory structures are well thought of and framed, which put strong strictures on

141

market participants and products. Our derivative markets were comparatively less

exposed to crises in the world financial systems. 39% (24) respondents feel that we are

relatively less exposed to world financial markets to be impacted in any major way due to

the financial crises. This also raises a point on how much regulated or opened an economy

should be to protect its own interests. 11% (7) respondents feel that all the above

parameters played role in averting 2007 financial crises in India. 8% (5) respondents feel

that there are other factors which helped avert the crises. And 3% (2) respondents do not

agree with the statement at all. Either they feel that India was faced with the challenge of

financial crises in 2007 or that we failed to control and regulate our financial system as a

result of the crises.

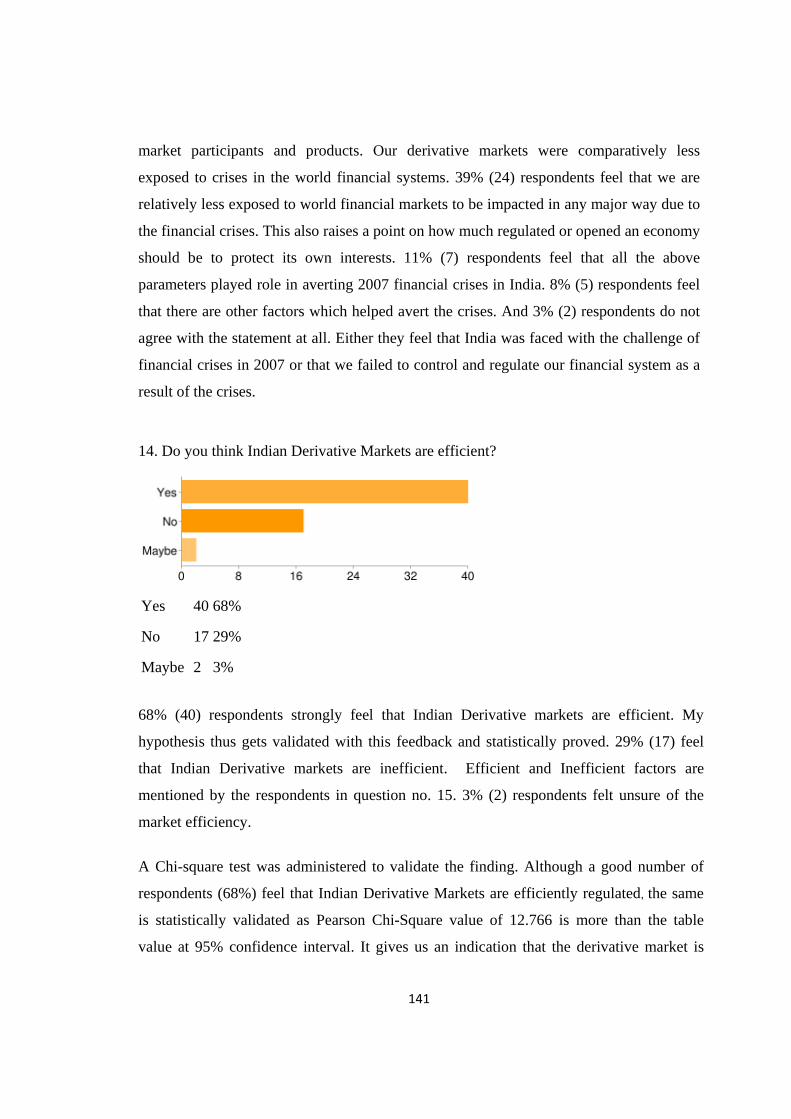

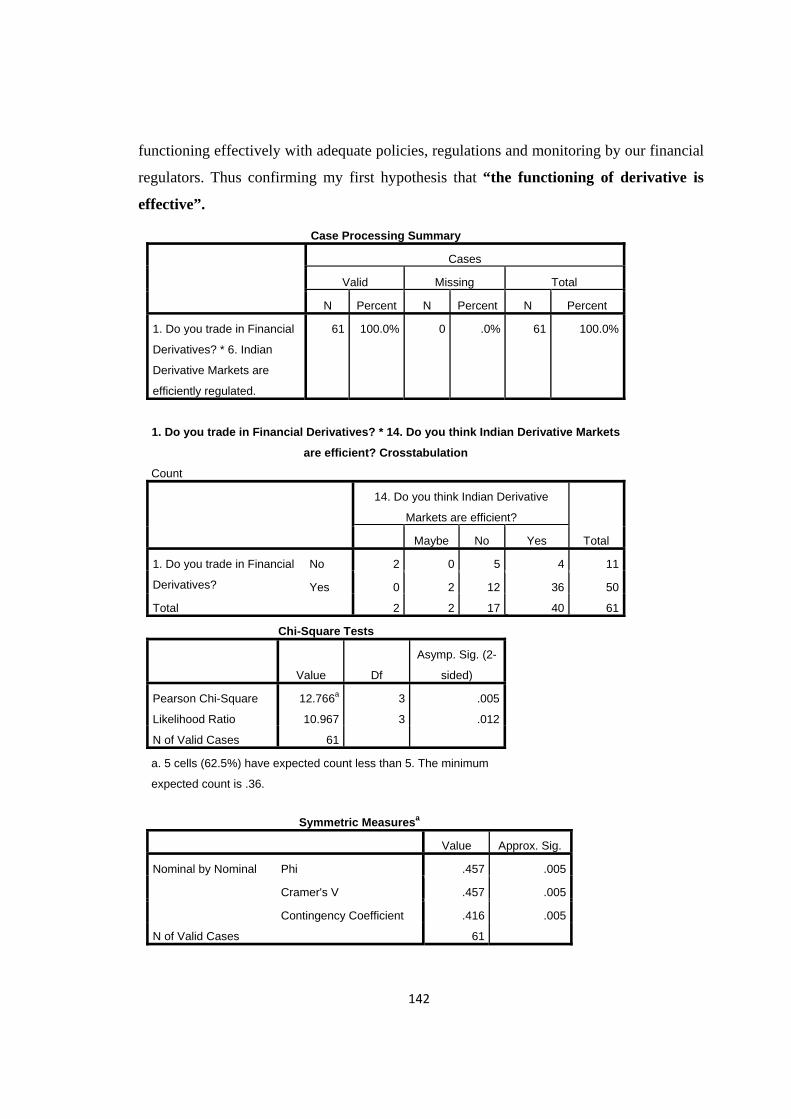

14. Do you think Indian Derivative Markets are efficient?

Yes 40 68%

No 17 29%

Maybe 2 3%

68% (40) respondents strongly feel that Indian Derivative markets are efficient. My

hypothesis thus gets validated with this feedback and statistically proved. 29% (17) feel

that Indian Derivative markets are inefficient. Efficient and Inefficient factors are

mentioned by the respondents in question no. 15. 3% (2) respondents felt unsure of the

market efficiency.

A Chi-square test was administered to validate the finding. Although a good number of

respondents (68%) feel that Indian Derivative Markets are efficiently regulated, the same

is statistically validated as Pearson Chi-Square value of 12.766 is more than the table

value at 95% confidence interval. It gives us an indication that the derivative market is

142

functioning effectively with adequate policies, regulations and monitoring by our financial

regulators. Thus confirming my first hypothesis that “the functioning of derivative is

effective”.

Case Processing Summary

Cases

Valid Missing Total

N Percent N Percent N Percent

1. Do you trade in Financial

Derivatives? * 6. Indian

Derivative Markets are

efficiently regulated.

61 100.0% 0 .0% 61 100.0%

1. Do you trade in Financial Derivatives? * 14. Do you think Indian Derivative Markets

are efficient? Crosstabulation

Count

14. Do you think Indian Derivative

Markets are efficient?

Total Maybe No Yes

1. Do you trade in Financial

Derivatives?

No 2 0 5 4 11

Yes 0 2 12 36 50

Total 2 2 17 40 61

Chi-Square Tests

Value Df

Asymp. Sig. (2-

sided)

Pearson Chi-Square 12.766a 3 .005

Likelihood Ratio 10.967 3 .012

N of Valid Cases 61

a. 5 cells (62.5%) have expected count less than 5. The minimum

expected count is .36.

Symmetric Measuresa

Value Approx. Sig.

Nominal by Nominal Phi .457 .005

Cramer's V .457 .005

Contingency Coefficient .416 .005

N of Valid Cases 61

143

15. Please state the factors in either case. Respondents gave the following qualitative

feedback.

The respondents gave two adverse views on the functioning of the derivative markets.

They are summarized as below:

Derivative Markets are efficient:

• Derivative Markets are not overtly aggressive and are progressing conservatively.

• Counter party risk and settlement mechanism is very strong.

• Strong interference and regulatory controls by SEBI.

• Healthy participation from foreign institutional investors (FII).

• Protection of investors by regulating exotic options and privately structured OTC

options by SEBI.

• RBI controlling Banks from designing complex options, which investors may not

fully understand.

• Derivative Markets witness very high volumes except in interest rate derivatives in

equity index, currency, and commodities derivatives which greatly reduces impact

costs and promotes high volumes of trading.

• Due to NIFTY futures trading in Singapore Stock Exchange and Chicago Mercantile

Exchange, where positions are taken in dollars, is greatly attracting foreign investors

to invest in NIFTY Futures.

• Liquidity is extremely good. Good derivative market regulation.

• Efficient risk management by exchanges. The transactions are faster, safer and

properly priced. Equity derivatives are efficient. Proper Margins are there. The

regulators keep revising it.

• The regulators are alert for the client's protection while trading in the derivative

market.

• So far the market has not heard of any fiasco.

• The derivative market functions quite smoothly.

• Price discovery for Options for every change in underlying is swift and promptly

reflected in price of options on screen.

144

• We have market participants playing different roles like arbitrageurs while some

acting as speculators and hedgers. Each of them indirectly serves the purpose of

others. Also margin money and MTM is required to be collected as per exchange

regulations. Compared to volume they are fairly regulated.

• The Indian Markets are online, transparent and relatively well-regulated to the extent

of being a bit over-regulated. The price-discovery is quite realistic given that the

Rupee is still not fully convertible.

Derivative Markets are inefficient:

• There are limited market participants, understanding and volumes are also quite weak,

and this needs to improve for efficient (liquid & deep) derivatives market.

• Need to focus on options for larger participation. Number of players are less, more

players needed.

• No appetite and no tools for pricing and managing derivative instruments.

• Derivatives are important to leverage capital and manage capital risks, in absence of

virtually zero exposure by Indian banks, funding the infrastructure would be a

challenge.

• Indian Markets are not efficient so derivative markets cannot be efficient. Still we

don't have t+ 1 settlement. Now its t+2. Real time gross settlement for bigger ticket

size is there; its not for the smaller ticket size.

• We need to create products which can be easily sold and marketed to the investors- we

only have maximum 3 months contracts in futures which is a pity....stock options are

mostly illiquid and the quantity of stocks in futures are very high and not all of them

are liquid and some of them are really pure speculative stocks.

• Extreme regulation.

• Very little exotic instruments.

• Still a developing market. Still not sufficient liquidity in the market.

• Lack of awareness of derivative products.

• Lack of sufficient strength in the home currency. Limited gold back up.

• Lack of awareness of derivative products, lack of sufficient strength in home currency

due to limited gold backup.

145

• Lack of understanding of the product and market mob flocking mentality.

• Derivatives trading is not broad based and penetration is limited.

• Derivatives are more used for speculation purpose rather than hedging and efficient

price discovery system.

• As an instrument of hedging, it has limited penetration in rural farmers etc.

• Use of vanilla products only.

• Restrictions/ Regulatory oversight.

• The markets do not have depth.

• Multiple regulators, multiple and different objectives among policy makers.

• Turnover velocity of shares in Indian Market is much lower than the other markets.

• Lack of depth was a major issue in Indian Market. However, we are witnessing great

improvements in liquidity in the recent years. Participation of larger number of

Institutional Investors would improve the overall liquidity.

16. Following factors help regulate the derivatives market efficiently.

High Margins 21 35%

Maintenance of High Net worth by brokers/ traders 21 35%

Periodic Audits and Reporting 39 65%

146

Adequate awareness generation of dynamics of derivative trading 38 63%

Monitoring of high volume/ value trades 38 63%

Monitoring Speculative tendencies 21 35%

Ensuring basic compliance for competent Market Participants 36 60%

Periodic Training to Market Participants 23 38%

All of the above 8 13%

Other 1 2%

65% (39) respondents feel that periodic audits and reporting are essential to control and

regulate the activities of traders in the derivative market. It can help the regulators to

detect and regulate any non compliance and omissions. The audits could be facilitated by

SEBI or a third party. Specialized trained audit teams could be built for the purpose. 63%

(38) respondents feel that an adequate awareness has to be generated amongst traders and

investors to understand the dynamics of derivative trading. It is very essential since a

derivative product is structured differently than any other investment options, which are

understood by a layman. Investing in a fixed deposit / postal deposit requires relatively

lesser education than may be investing in a derivative product to a person who is aware of

the dynamics of managing money.

63% (38) respondents feel that a very close scrutiny on abnormal trades in terms of high

value and volume has to be carried out since these are the indicators of either cornering

the market or taking a position which is against the dynamics of the market.

60% (36) respondents feel that ensuring basic compliance for competent Market

Participants. The regulator should ensure that the market participants’ like traders, brokers

etc. should fulfill some basic criteria to enable to trade in the derivative markets. This

might include ensuring high net worth, minimum education on the dynamics on the

derivative trading, background check and credibility etc.

38% (23) respondents feel that the players in the derivative markets need to be given

periodic training for better compliance. Education and awareness generation should be a

147

continual exercise which would motivate and guide market participants towards an

efficient process and system.

Not a very high degree of 35% (21) respondents feel that high margins and high net worth

may be effective measures for efficient markets. The percentage of respondents who feel

the same is not very high since they believe that efficiency can be brought by periodic

compliance and awareness generation.

13% (2) respondents feel that all the factors mentioned are important for a market to run

efficiently and 2% (1) feel that there could be other factors which may contribute towards

an efficient market.

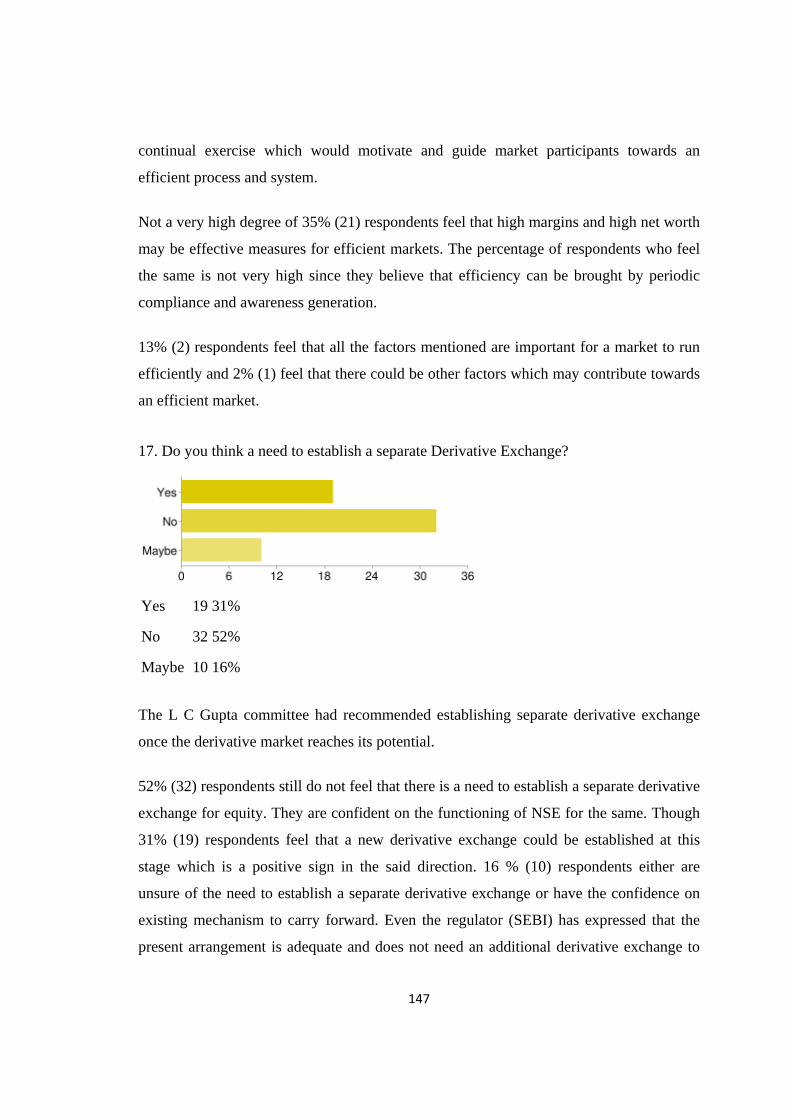

17. Do you think a need to establish a separate Derivative Exchange?

Yes 19 31%

No 32 52%

Maybe 10 16%

The L C Gupta committee had recommended establishing separate derivative exchange

once the derivative market reaches its potential.

52% (32) respondents still do not feel that there is a need to establish a separate derivative

exchange for equity. They are confident on the functioning of NSE for the same. Though

31% (19) respondents feel that a new derivative exchange could be established at this

stage which is a positive sign in the said direction. 16 % (10) respondents either are

unsure of the need to establish a separate derivative exchange or have the confidence on

existing mechanism to carry forward. Even the regulator (SEBI) has expressed that the

present arrangement is adequate and does not need an additional derivative exchange to

148

facilitate derivative trades.

A good number of respondents (52%) feel that there is no need to establish a separate

derivative exchange. It gives us an indication that the financial markets find the present

arrangement of the derivative exchange as adequate to meet the current requirement.

Hence as per the L C Gupta’s recommendation committee report for a separate derivative

exchange as and when the markets are ready, the feedback indicates that the market is not

ready for a separate derivative exchange.

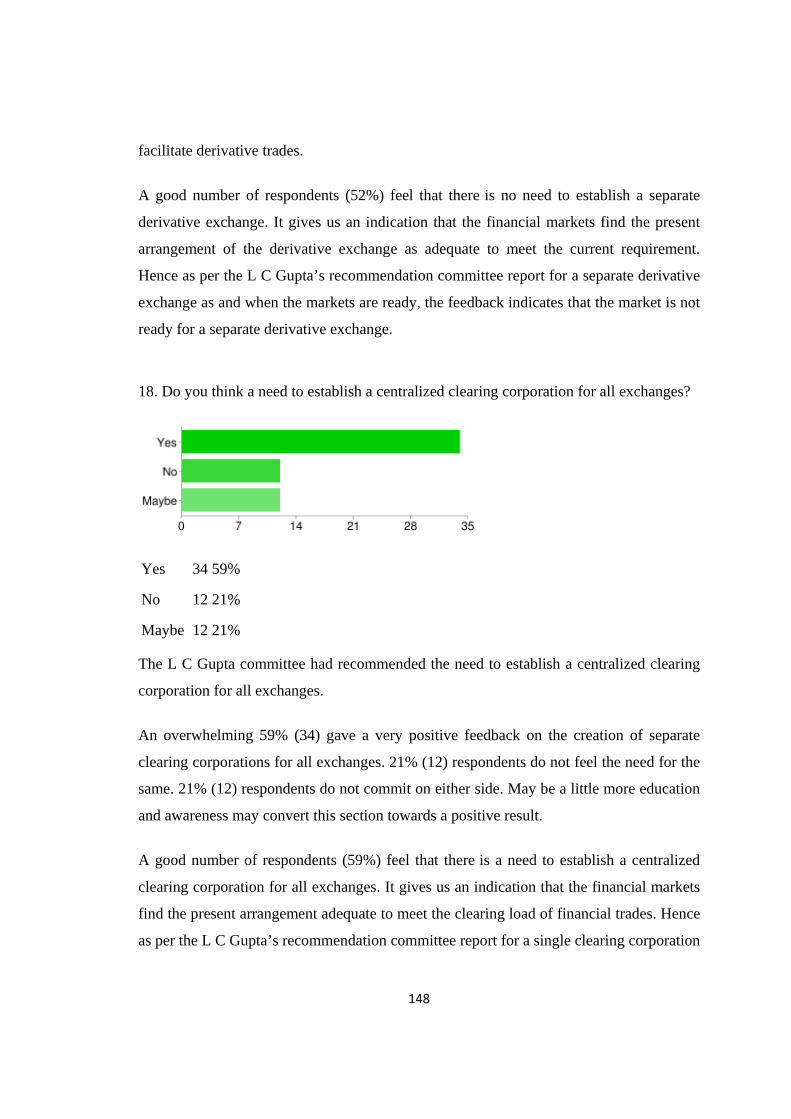

18. Do you think a need to establish a centralized clearing corporation for all exchanges?

Yes 34 59%

No 12 21%

Maybe 12 21%

The L C Gupta committee had recommended the need to establish a centralized clearing

corporation for all exchanges.

An overwhelming 59% (34) gave a very positive feedback on the creation of separate

clearing corporations for all exchanges. 21% (12) respondents do not feel the need for the

same. 21% (12) respondents do not commit on either side. May be a little more education

and awareness may convert this section towards a positive result.

A good number of respondents (59%) feel that there is a need to establish a centralized

clearing corporation for all exchanges. It gives us an indication that the financial markets

find the present arrangement adequate to meet the clearing load of financial trades. Hence

as per the L C Gupta’s recommendation committee report for a single clearing corporation

149

when the markets are ready, the feedback indicates that the market is still not ready / feel

the need for a single clearing corporation. It may also be due to the apprehension that it

could be a risky proposition to bring all financial trades under one roof. A small deviation

in the running of the corporation may risk the trades of the whole financial system.

19. Derivative Trades under exchanges are well regulated.

1 0 0 %

2 1 2%

3 16 26%

4 27 44%

5 16 26%

An overwhelming 70% (43) agree that derivatives trade under exchanges are better

regulated which is supporting my hypothesis that derivative markets are effective. 26%

(16) do not wish to commit on the effectiveness of the regulation under exchanges, only

2% (1) do not agree that derivative traders under exchange are well regulated. This

observation could be ignored in view of a very positive outlook of the respondents toward

exchange regulated trades.

A Chi-square test was administered to validate the finding. A good number of respondents

(70%) feel that Derivative Trades under exchanges are well regulated, the same is also

statistically validated as Pearson Chi-Square value of 22.800a which is more than the

table value at 95% confidence interval. It gives us a positive indication that the

functioning of the derivative markets are realistic thus confirming my first hypothesis that

“the functioning of derivative is effective”.

150

Descriptive Statistics

N Mean Std. Deviation Minimum Maximum

4. The Indian Financial

System is efficient and

robust.

60 3.62 .846 2 5

19. Derivative Trades under

exchanges are well

regulated.

60 3.97 .780 2 5

Test Statistics

4. The Indian

Financial

System is

efficient and

robust.

19. Derivative

Trades under

exchanges are

well regulated.

Chi-Square 17.733a 22.800a

df 3 3

Asymp. Sig. .000 .000

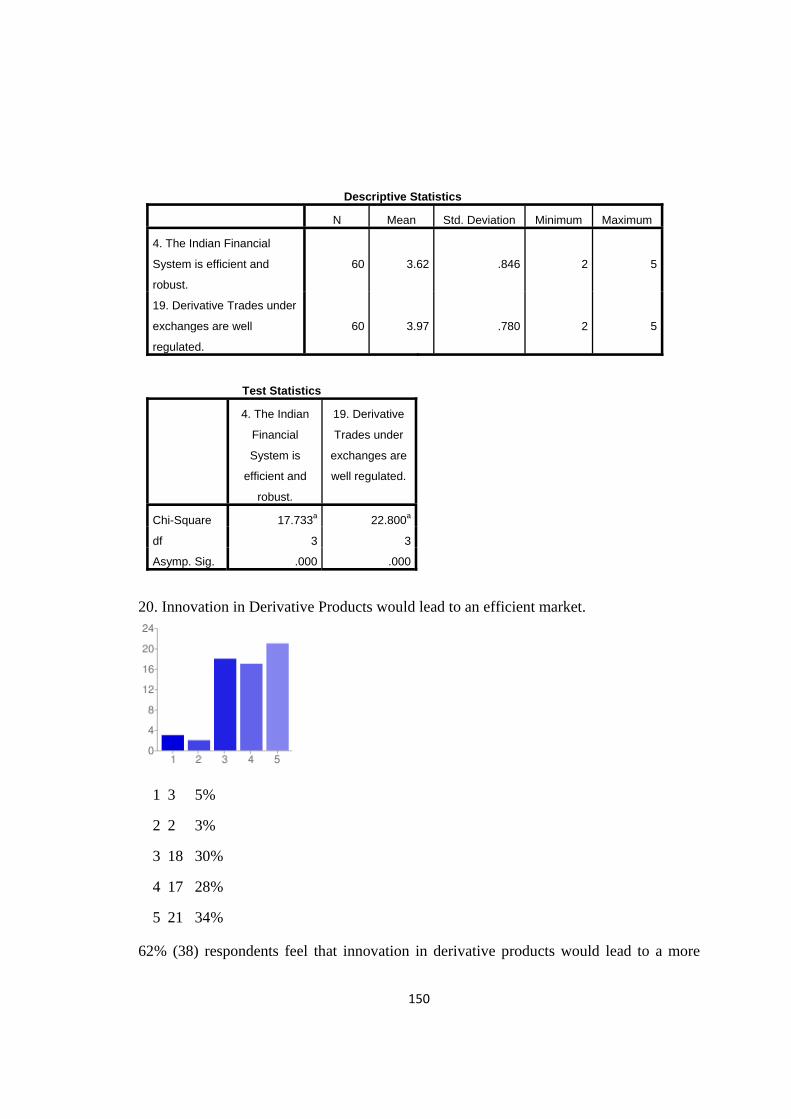

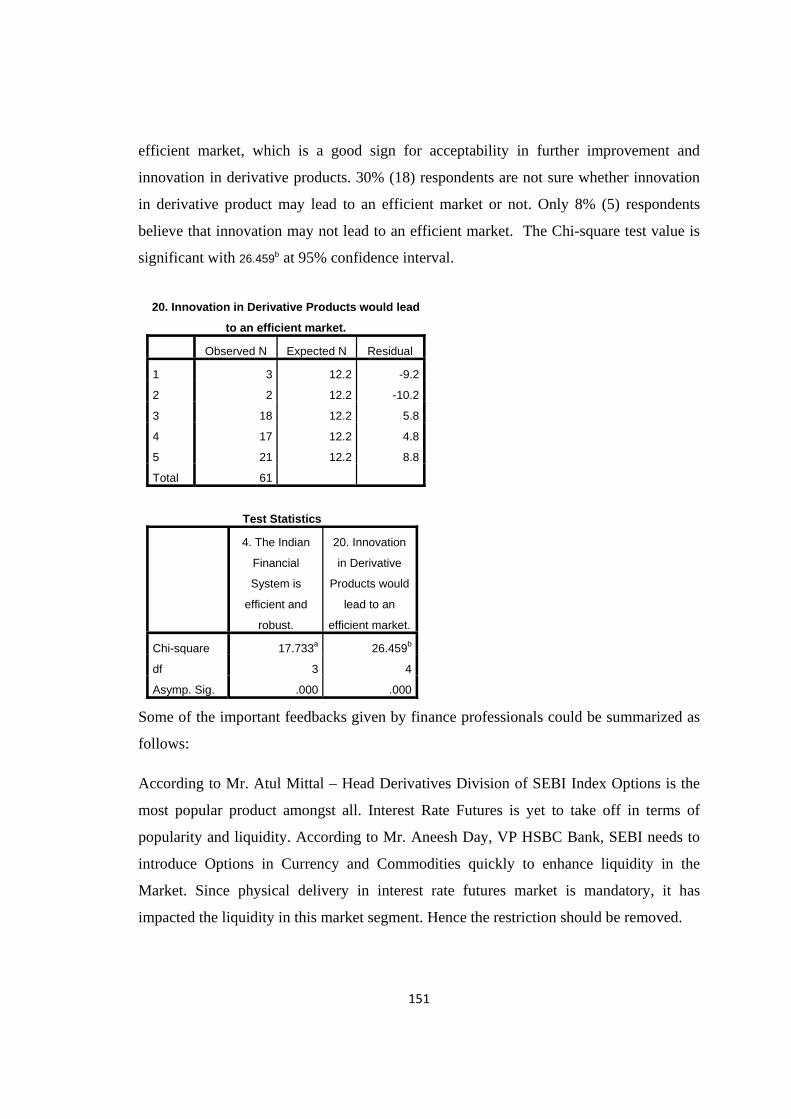

20. Innovation in Derivative Products would lead to an efficient market.

1 3 5%

2 2 3%

3 18 30%

4 17 28%

5 21 34%

62% (38) respondents feel that innovation in derivative products would lead to a more

151

efficient market, which is a good sign for acceptability in further improvement and

innovation in derivative products. 30% (18) respondents are not sure whether innovation

in derivative product may lead to an efficient market or not. Only 8% (5) respondents

believe that innovation may not lead to an efficient market. The Chi-square test value is

significant with 26.459b at 95% confidence interval.

20. Innovation in Derivative Products would lead

to an efficient market.

Observed N Expected N Residual

1 3 12.2 -9.2

2 2 12.2 -10.2

3 18 12.2 5.8

4 17 12.2 4.8

5 21 12.2 8.8

Total 61

Test Statistics

4. The Indian

Financial

System is

efficient and

robust.

20. Innovation

in Derivative

Products would

lead to an

efficient market.

Chi-square 17.733a 26.459b

df 3 4

Asymp. Sig. .000 .000

Some of the important feedbacks given by finance professionals could be summarized as

follows:

According to Mr. Atul Mittal – Head Derivatives Division of SEBI Index Options is the

most popular product amongst all. Interest Rate Futures is yet to take off in terms of

popularity and liquidity. According to Mr. Aneesh Day, VP HSBC Bank, SEBI needs to

introduce Options in Currency and Commodities quickly to enhance liquidity in the

Market. Since physical delivery in interest rate futures market is mandatory, it has

impacted the liquidity in this market segment. Hence the restriction should be removed.

152

Other feedbacks include that the Indian derivatives market is relatively small compared to

global markets. It is primarily exchange driven (OTC portions is smaller) and therefore

may be considered efficient on a standalone basis (i.e. without comparison with other

global markets). Derivative market is more speculative and is used more for speculative

gains rather than hedging. RBI persuades bankers and participants to go cautiously in

derivatives in view of bad experiences of many corporate losing money without proper

understanding of product and market.

4.1.3 Analysis of Questionnaire III for derivative stock brokers

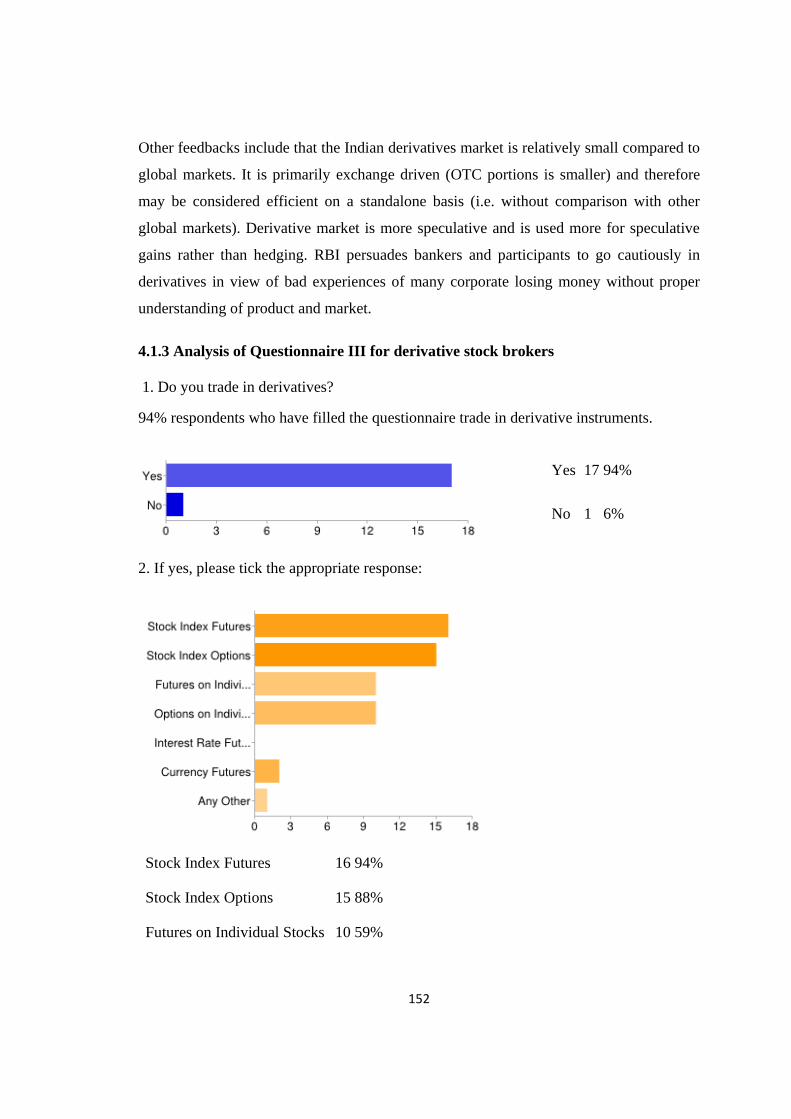

1. Do you trade in derivatives?

94% respondents who have filled the questionnaire trade in derivative instruments.

Yes 17 94%

No 1 6%

2. If yes, please tick the appropriate response:

Stock Index Futures 16 94%

Stock Index Options 15 88%

Futures on Individual Stocks 10 59%

153

Options on Individual Stocks 10 59%

Interest Rate Futures 0 0%

Currency Futures 2 12%

Any Other 1 6%

94% respondents trade in Stock index Futures and 88% respondents trade in Stock Index

Options. The least popular instrument is Interest Rate Futures (0%).

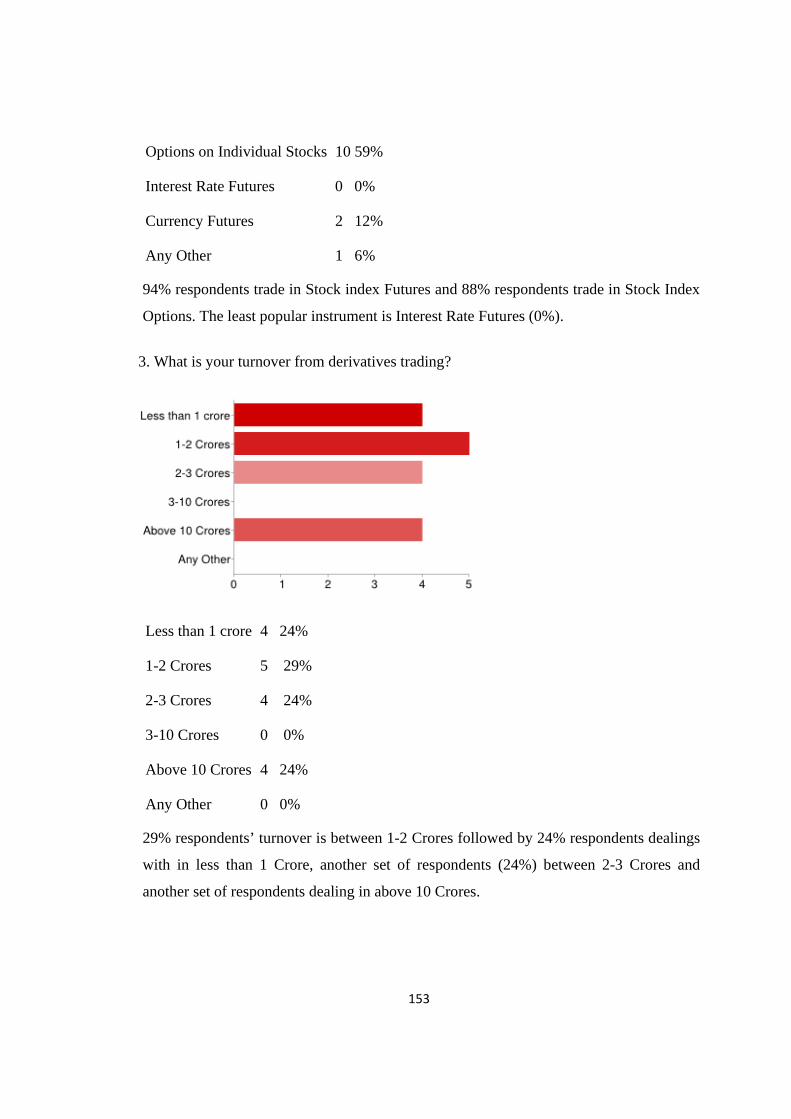

3. What is your turnover from derivatives trading?

Less than 1 crore 4 24%

1-2 Crores 5 29%

2-3 Crores 4 24%

3-10 Crores 0 0%

Above 10 Crores 4 24%

Any Other 0 0%

29% respondents’ turnover is between 1-2 Crores followed by 24% respondents dealings

with in less than 1 Crore, another set of respondents (24%) between 2-3 Crores and

another set of respondents dealing in above 10 Crores.

154

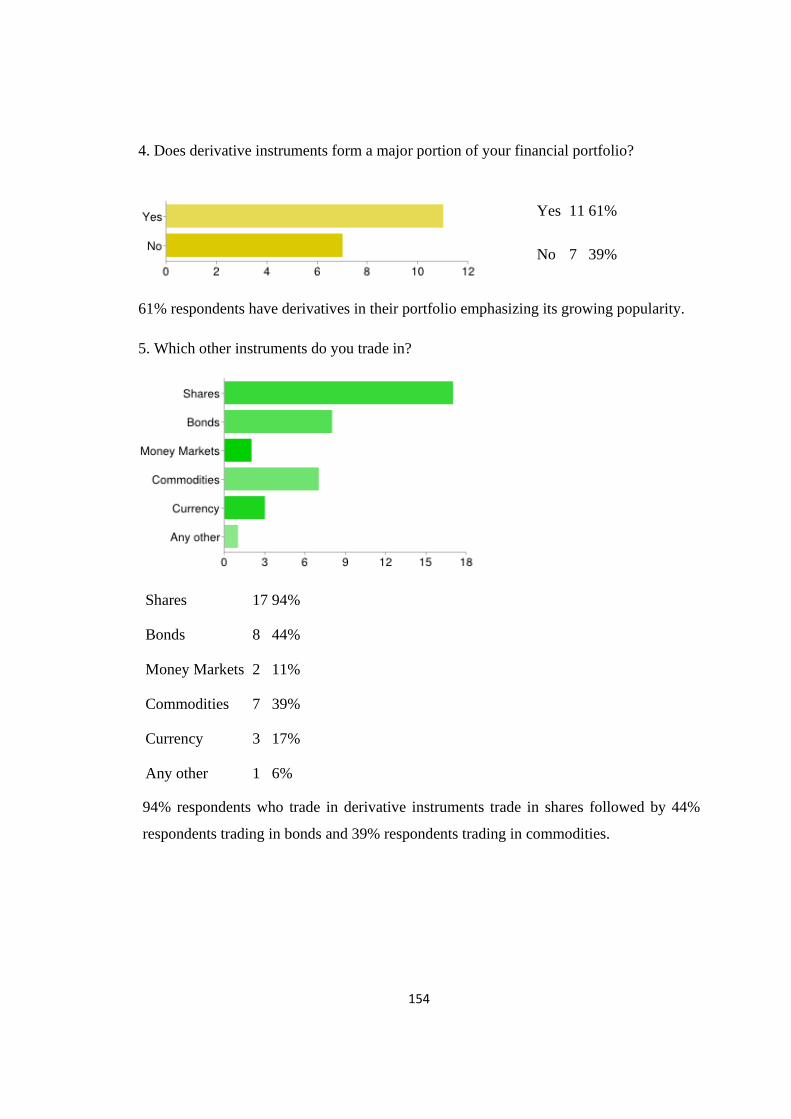

4. Does derivative instruments form a major portion of your financial portfolio?

Yes 11 61%

No 7 39%

61% respondents have derivatives in their portfolio emphasizing its growing popularity.

5. Which other instruments do you trade in?

Shares 17 94%

Bonds 8 44%

Money Markets 2 11%

Commodities 7 39%

Currency 3 17%

Any other 1 6%

94% respondents who trade in derivative instruments trade in shares followed by 44%

respondents trading in bonds and 39% respondents trading in commodities.

155

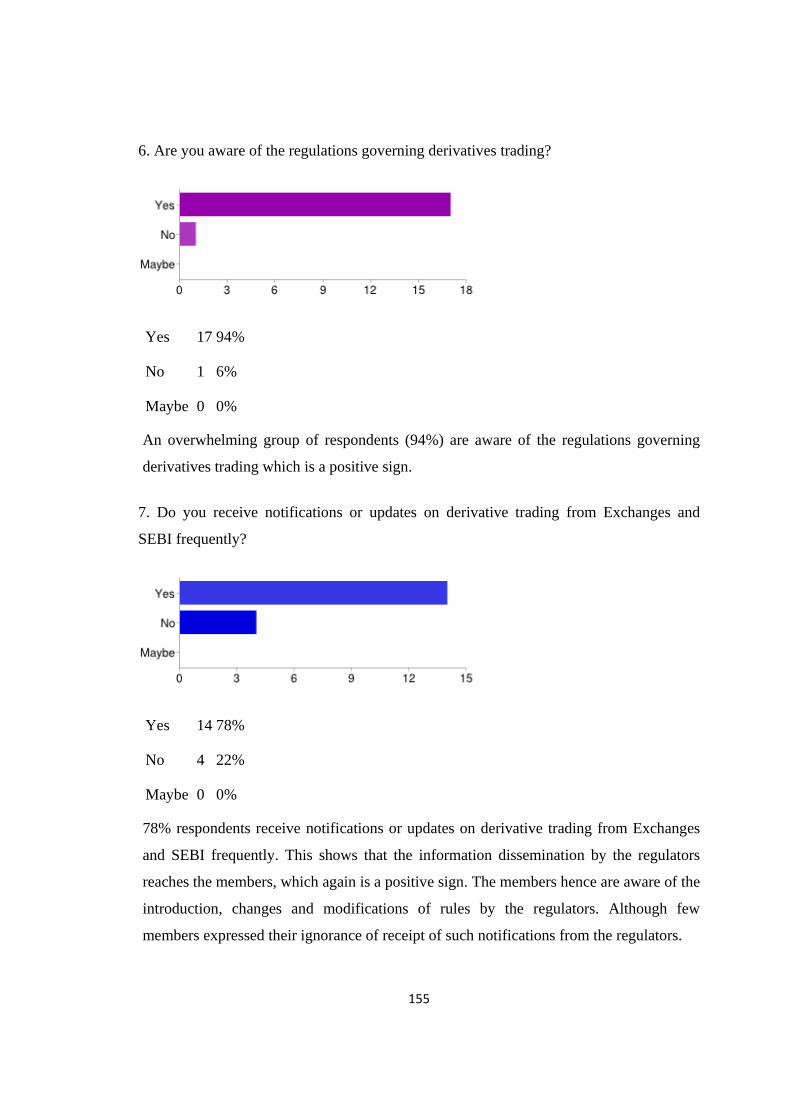

6. Are you aware of the regulations governing derivatives trading?

Yes 17 94%

No 1 6%

Maybe 0 0%

An overwhelming group of respondents (94%) are aware of the regulations governing

derivatives trading which is a positive sign.

7. Do you receive notifications or updates on derivative trading from Exchanges and

SEBI frequently?

Yes 14 78%

No 4 22%

Maybe 0 0%

78% respondents receive notifications or updates on derivative trading from Exchanges

and SEBI frequently. This shows that the information dissemination by the regulators

reaches the members, which again is a positive sign. The members hence are aware of the

introduction, changes and modifications of rules by the regulators. Although few

members expressed their ignorance of receipt of such notifications from the regulators.

156

8. Do you have to be qualified in trading in derivative instruments?

Yes 11 61%

No 7 39%

Maybe 0 0%

Although it’s mandatory to be a qualified derivatives trader, there are around 39%

respondents who are not aware of this requirement, which is a factor to look into and

amend. More awareness may need to be generated of this requirement and a strict

compliance needs to be imposed.

9. Were you trained in trading of derivative instruments?

Yes 11 61%

No 7 39%

Maybe 0 0%

Although it’s mandatory to be a qualified derivatives trader, there are around 39%

respondents who are not trained derivatives traders, which is a factor to look into and

amend. More awareness and training programmes may need to be conducted to capture

such audience.

157

10. Do you undergo training in derivatives trading from time to time?

Yes 9 50%

No 8 44%

Maybe 1 6%

Only 50% respondents undergo training periodically. 44% respondents do not undergo

training in derivatives trading periodically. A training schedule with training needs

should be published annually to benefit members of the same.

11. If yes, how frequently?

Quarterly 4 36%

Semi Annually 1 9%

Annually 4 36%

More than a year 2 18%

Two groups (36% respondents each) of respondents undergo training quarterly and

annually respectively. The periodicity of training should be increased and have a

continuous flow throughout the year.

158

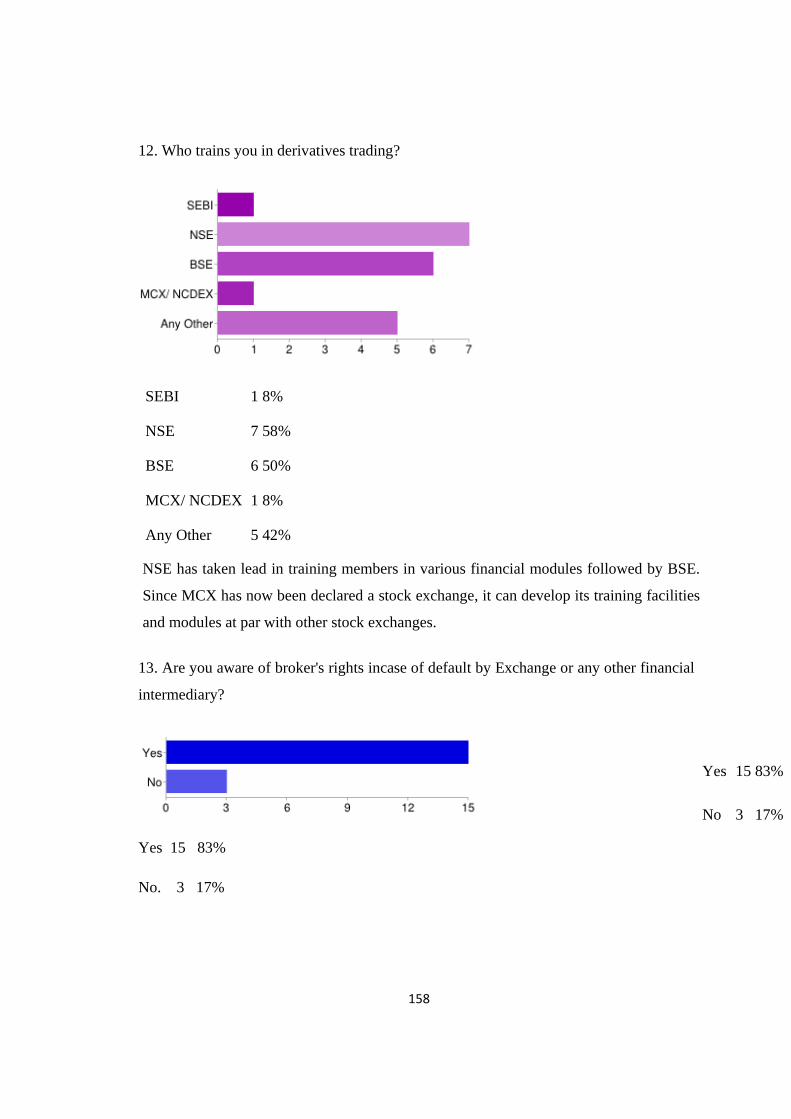

12. Who trains you in derivatives trading?

SEBI 1 8%

NSE 7 58%

BSE 6 50%

MCX/ NCDEX 1 8%

Any Other 5 42%

NSE has taken lead in training members in various financial modules followed by BSE.

Since MCX has now been declared a stock exchange, it can develop its training facilities

and modules at par with other stock exchanges.

13. Are you aware of broker's rights incase of default by Exchange or any other financial

intermediary?

Yes 15 83%

No. 3 17%

Yes 15 83%

No 3 17%

159

An overwhelming 83% respondents are aware of their legal rights in case of disputes

with financial intermediaries. This is a positive sign. But we also should not ignore the

17% population with less or no awareness. We should make an effort to convert them

into legally literate members.

14. Do you sensitize your investors on the risk of derivatives trading?

Yes 11 61%

No 7 39%

This factor is very important. Only 61% respondents follow sensitizing investors on the

risk of derivatives trading. The same should be 100% compliance from the members. An

initiative in the form an audit or inspection from the exchanges should be undertaken

exclusively to find out on the compliance of this regulation.

15. If yes, then how?

The respondents’ responses are summarized as below:

• Personalized approach to risk return profile analysis for all clients.

• Explaining the risks involved orally and through the risk document attached as

Know Your Customer (KYC) norm. Explaining the clients that their entire

principal amount could be whitewashed, if the trades are not done diligently.

• Risk Disclosure document is given to the client for reference. The Risk Disclosure

Document (RDD) is given to the client along with the account opening form.

16. Which are the statutory regulatory clauses are you concerned with closely and need to

comply with without exception?

• Margin Compliance to be complied without exception.

• Regular confirmation to clients about the trades undertaken.

160

• Account opening formalities and KYC (Know Your Client) Norms;

• Networth requirements; Maintenance of books and records; and Issue of Contract

Notes

17. What percentage of your customers/ clients of yours, trade in derivative instruments?

Less than 10% 5 28%

10%-20% 7 39%

20%-30% 3 17%

30%-40% 1 6%

Above 40% 2 11%

We find that around 10- 20% clients’ trade in derivative instruments followed by less

than 10% clients who wish to trade in derivative instruments. The percentages do not

seem to be very high may be due to lack of awareness of the dynamics of derivative

trading unlike share trading.

18. How would you categorize them in terms of investment capacities?

High Net Worth 11 61%

Medium 9 50%

Small 0 0%

161

Around 61% investors are high net worth individuals who deal in derivative instruments.

There are hardly any small investors who invest in these instruments. This may be due to

many reasons like investing in lots, awareness, risk, ignorance, complexity etc.

19. How much do you charge your investors?

Less than 10% 13 76%

10%-20% 4 24%

20%-30% 0 0%

30%-40% 2 12%

76% investors are charged less than 10% of the trade profit. Around 24% respondents

charged between 10-20%. And around 12% respondents charged between 30-40% which

could be for additional financial consultancy and advise.

20. How much margin do you extend to your investors?

Less than 1 Crore 8 53%

1-2 Crore 5 33%

More than 2 Crore 2 13%

The majority of investors (53%) are extended less than 1 crore as margin money

followed by 33% investors being extended 1 -2 crores as margin money. We find that the

majority of investors trade in moderation with less than 1 crore margin payment. We find

162

that they play safe with their investment.

21. What interest do you charge for the money lent?

Less than 1% 3 21%

1%-2% 7 50%

2%-4% 0 0%

Above 4% 1 7%

Risk Free 3 21%

LIBOR/ MIBOR 0 0%

Around the 50% of the investors are charged 1 -2% interest on the margin money lent.

22. The above interest charged is:

163

Per day 0 0%

Per week 1 8%

Per month 11 92%

Quarterly 0 0%

Semi- annually 0 0%

Annually 0 0%

92% investors are charged monthly interest. This comes between 12% - 24% per annum

as per the response in question number 21.

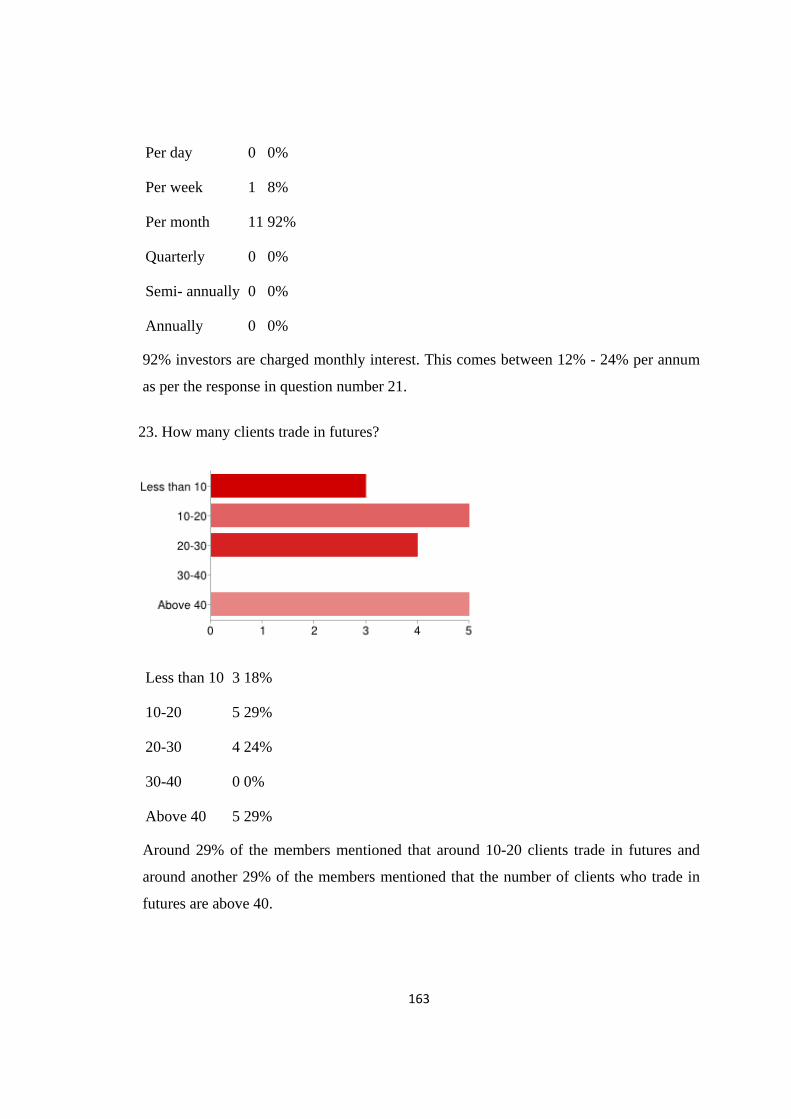

23. How many clients trade in futures?

Less than 10 3 18%

10-20 5 29%

20-30 4 24%

30-40 0 0%

Above 40 5 29%

Around 29% of the members mentioned that around 10-20 clients trade in futures and

around another 29% of the members mentioned that the number of clients who trade in

futures are above 40.

164

24. How many clients trade in options?

Less than 10 3 18%

10-20 3 18%

20-30 3 18%

30-40 3 18%

Above 40 5 29%

Around 18% of the members mentioned that around 10-20 clients trade in options and

around another 29% of the members mentioned that the number of clients who trade in

options are above 40

25. Derivative instruments are fully useful to hedge risks.

1 0 0%

2 3 15%

3 5 25%

4 3 15%

5 7 35%

35% of respondents feel that derivative instruments are useful to hedge risk. This

validates our hypothesis that derivative markets are realistic since one of the major

165

functions of a derivative market is to hedge risk. Its note worthy to find that no

respondents feel that derivative trading do not aid in hedging risk.

26. How are Derivative instruments useful/ not useful to hedge risks? Suggest changes, if

required.

Following is the summary of the responses:

Neutral view can always use derivatives to hedge our core portfolio risk. If we have a

portfolio, one could hedge the risk by index future and reduce the risk. By taking a

position in the futures market that is opposite to a position in Cash market, the risks

associated with price changes are limited or reduced. Derivatives help leverage and

arbitrage in the underlying equities. It can hedge the position to the fullest.

27. Derivative Instruments help in earning wealth.

1 1 5%

2 2 10%

3 10 50%

4 2 10%

5 1 5%

50% of respondents neither agree nor disagree to the statement that derivative instruments

help in wealth creation. Only 15% respondents feel that it helps in wealth creation. This

factor is important since it conveys that derivative instruments are helpful in hedging and

transferring risk rather than earning unlimited wealth.

28. How are Derivative Instruments useful/ not useful in earning wealth.

The responses are summarized as follows:

• Neutral view if used effectively and very useful otherwise could be disastrous.

• They help remove the systematic risk.

166

29. Do you have an international exposure in trading in derivative instruments?

Yes 1 6%

No 16 94%

An over whelming majority (94%) stated that they do not have an international exposure

in derivative trading. This reflects that our derivative markets are less integrated and

exposed to international derivative markets. In a way it helps us insulate from the

fluctuations and volatility in the international markets. But it also disadvantages our

markets to gain from the benefits, which exists (in terms of price, volume, technology etc)

in international markets.

30. If yes, please tick the appropriate choice:

Stock Index Futures 0 0%

Stock Index Options 1 100%

Futures on Individual Stocks 0 0%

Options on Individual Stocks 0 0%

Interest rate Futures 0 0%

Currency Futures 0 0%

167

Any other 0 0%

100% respondent (1) has an international exposure in stock index option which reflects

that Indian derivative trades are not internationally exposed.

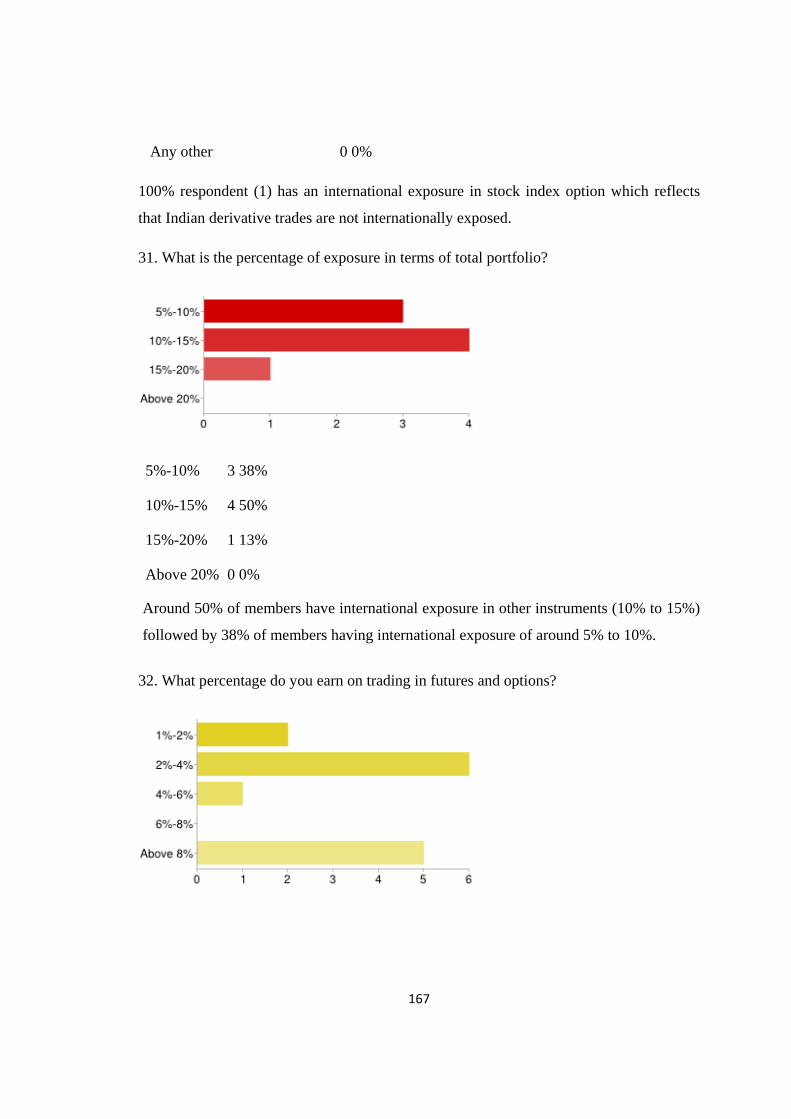

31. What is the percentage of exposure in terms of total portfolio?

5%-10% 3 38%

10%-15% 4 50%

15%-20% 1 13%

Above 20% 0 0%

Around 50% of members have international exposure in other instruments (10% to 15%)

followed by 38% of members having international exposure of around 5% to 10%.

32. What percentage do you earn on trading in futures and options?

168

1%-2% 2 14%

2%-4% 6 43%

4%-6% 1 7%

6%-8% 0 0%

Above 8% 5 36%

43% respondents earn around 2-4% from the derivative trades followed by 36%

respondents earning above 8% returns. 2-4% category is also a risk free interest earning

category. It shows that derivative trading does not aid in creating unlimited wealth but

plays a role in risk management for which the investors invest in these instruments. But

on the other side respondents also earn above 8% returns but with a cap as these

instruments do not allow a trader to earn unlimited wealth/ profits due to their intrinsic

characteristics.

33. What is the percentage of exposure in derivatives in terms of value (in Rs.)?

Less than 50 Crores 3 50%

50-100 Crores 2 33%

100-150 Crores 1 17%

150-200 Crores 0 0%

Above 200 Crores 0 0%

50% respondents have less than 50 crores of exposure in derivatives in terms of value.

Around 33% have exposure between 50-100 crores.

169

34. Do you finance your requirement from Banks and other Financial Institutions?

Yes 7 41%

No 10 59%

Around 59% of respondents do not finance their requirements from banks or other

financial institutions. This may be because banks are not allowed to extend money for

stock trading activities. Although 41% do finance their requirements from the financial

institutions. This may be in the form of pledge or loan against their securities.

35. If yes, what is the percentage of your borrowing vis-a vis your own contribution?

Less than 10% 3 30%

10%-20% 6 60%

20%-30% 1 10%

30%-40% 0 0%

Above 40% 0 0%

60% of respondent borrow only 10-20% of their financial requirements and contribute