Chapter 3 Developing Financial Statements, Plans and Budgets Financial statements are assessments of...

37

Chapter 3 Developing Financial Statements, Plans and Budgets Financial statements are assessments of the current status of one’s personal financial position.

-

Upload

louisa-miller -

Category

Documents

-

view

221 -

download

2

Transcript of Chapter 3 Developing Financial Statements, Plans and Budgets Financial statements are assessments of...

Chapter 3Developing Financial Statements, Plans and Budgets

Financial statements are assessments of the current status of one’s personal financial position.

Chapter 3Developing Financial Statements, Plans and Budgets

TWO types of statements

1. Income statementTraces flow of income and expenses

2. Balance sheet Lists assets and liabilities

Also known as statement of net worth

Chapter 3Developing Financial Statements, Plans and Budgets

Financial statements provide:• an evaluation of financial well-being• information for loan applications• a starting point for estate planning• a basis for building future investments• a key to potential financial problems• information for divorce, prenuptial agreements

Chapter 3Developing Financial Statements, Plans and Budgets

• Mark and Susan’s Income Statement Mark and Susan earned $39,000 and $45,000

in salary respectively. Mark received a bonus of $2,500 and they

collected $1,500 in interest and dividends. They also received a federal tax refund of $500. Total income before taxes: $88,500.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Consider Taxes.Susan and Mark paid $17,000 in income and Social Security taxes during the year. Afterdeducting for taxes, they found they had a net income of $71,500.• Gross income $88,500.00

• Less taxes 17,000.00

• Net income 71,500.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Housing Expenses

– Mortgage payments totaled $12,000

– Utilities $3,600

– Property taxes of $1,800

– Maintenance expenses of $2,500

– Home-owners insurance cost $600

– Miscellaneous expenses $2,500

Chapter 3Developing Financial Statements, Plans and Budgets

Housing: Mortgage *$12,000.00 Utilities 3,600.00 Property Taxes *1,800.00 Maintenance 2,500.00 Insurance 600.00 Other 2,500.00

* Tax deductible

Chapter 3Developing Financial Statements, Plans and Budgets

• Transportation and Food ExpensesCar payments, gas and repairs, insurance, and

registration were estimated to be $5,500.Bus passes and bike maintenance cost another

$500.

Food cost were estimated to be $5,000.

Chapter 3Developing Financial Statements, Plans and Budgets

Transportation: Car payments $3,600.00 Gasoline & repairs 1,000.00 Insurance 700.00 Registration 200.00 Other 500.00

Food: Total Food $5,000.00

Chapter 3Developing Financial Statements, Plans and Budgets

Other ExpensesClothing $2,500.00Child care: $6,000.00Health insur. premiums 1,200.00Health care expenses 1,000.00Vacation, entertainment 2,000.00Gifts 2,000.00Life insurance 500.00Student loan payments 2,500.00Cash allowances 3,000.00Miscellaneous 2,500.00

Total Other Expenses $23,200.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Total Expenses

– Housing $23,000.00

– Food 5,000.00

– Transportation 6,000.00

– Other 23,200.00TOTAL EXPENSES $57,200.00

Chapter 3Developing Financial Statements, Plans and Budgets

•Savings & InvestmentMark and Susan earned a net income of $71,500 and had total expenses of $57,200. Therefore, they had $14,300 left for savings and investment.

Total net income $71,500.00(less) Total expenses 57,200.00*Available for savings, investment $14,300.00

** If this figure is negative, net worth declines

Chapter 3Developing Financial Statements, Plans and Budgets

•An income statement only shows how much money has been received and spent during a certain time period.

•A balance sheet is also needed to assess a person’s current financial position.

Chapter 3Developing Financial Statements, Plans and Budgets

• The Balance Sheet– Outlines what a person owns Assets

– Outlines what a person owes Liabilities

– Difference between the two = Net worth

A balance sheet provides a snapshot ofa person’s assets and liabilities at

any given point in time.

Chapter 3Developing Financial Statements, Plans and Budgets

• Current Financial Assets:Checking Account $1,500.00

Savings account 0.00

Money market 8,000.00

CD’s 0.00

Total Current Financial Assets $9,500.00

Chapter 3Developing Financial Statements, Plans and Budgets

•Financial Assets: Non-retirement, Retirement and Other Accounts

Susan and Mark valued their stocks and bonds not held in retirement accounts or special accounts.

Their retirement accounts and college fund total $24,000.

Chapter 3Developing Financial Statements, Plans and Budgets

• Financial Assets, cont.:– Non-retirement accts. $7,500.00– Retirement accts. 22,000.00– College fund

2,000.00

Subtotal $31,500.00

Total Financial Assets $41,000.00

Chapter 3Developing Financial Statements, Plans and Budgets

•Real Assets

We include houses, cars, furniture, and personal property in valuing fixed assets.

Chapter 3Developing Financial Statements, Plans and Budgets

• Real Assets:Home $145,000.00

Auto 1 14,000.00

Auto 2 0.00

Home Furnishings 20,000.00

Personal property 15,000.00

Total Real Assets $194,000.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Total AssetsTotal financial assets: $41,000.00

Total real assets: 194,000.00

Total assets$235,000.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Liabilities--What You Owe

– Current liabilities• debts due within a short period of time (a month)

– Long-term liabilities• debts to be paid off over a longer period of time

(one year)

Chapter 3Developing Financial Statements, Plans and Budgets

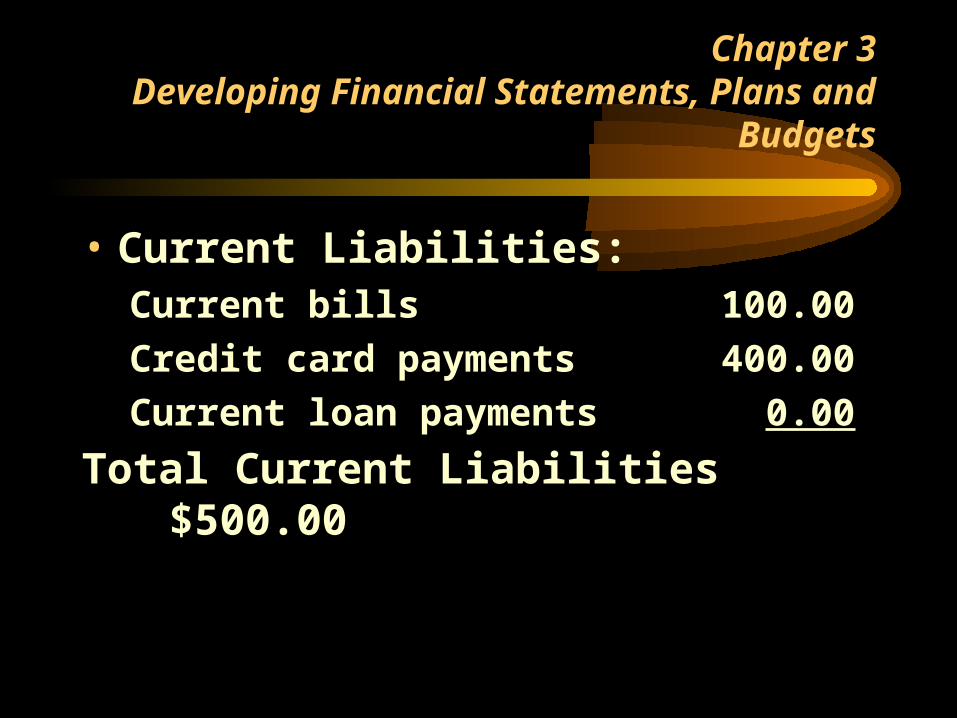

• Current Liabilities:Current bills 100.00

Credit card payments 400.00

Current loan payments 0.00

Total Current Liabilities $500.00

Chapter 3Developing Financial Statements, Plans and Budgets

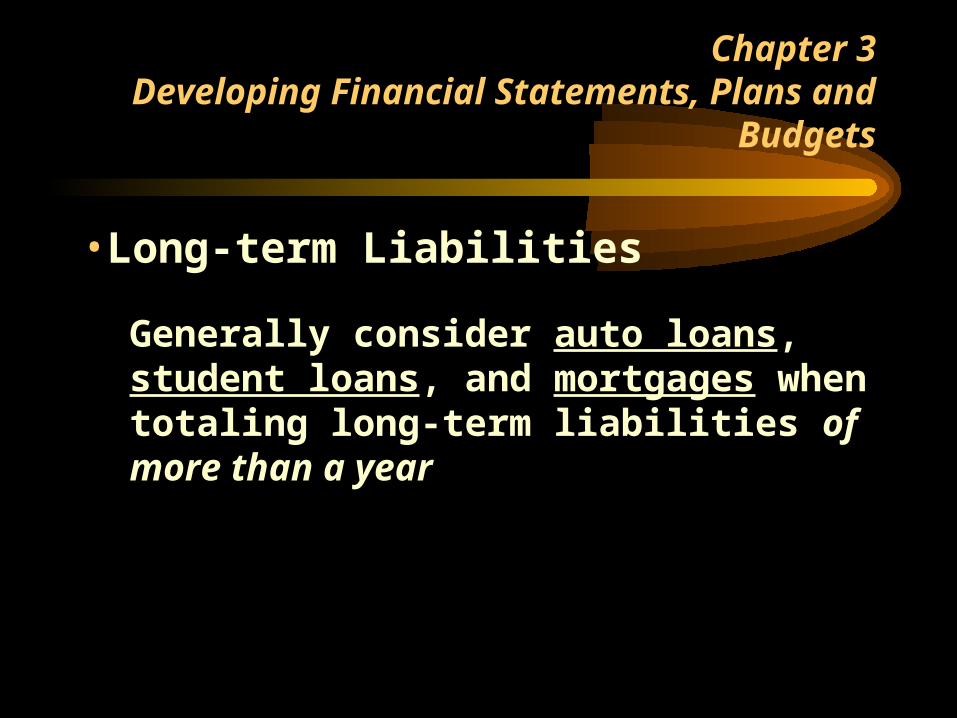

•Long-term Liabilities

Generally consider auto loans, student loans, and mortgages when totaling long-term liabilities of more than a year

Chapter 3Developing Financial Statements, Plans and Budgets

Long-term Liabilities:Auto loan $12,000.00

Student loan 8,000.00

Mortgage 115,000.00

Other 0.00

Total Long-term Liabilities $135,000.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Total LiabilitiesTotal current liabilities:

$500.00

Total long-term liabilities:135,000.00

Total liabilities$135,500.00

Chapter 3Developing Financial Statements, Plans and Budgets

• Net WorthTotal assets: $235,000.00

(Less) Total liabilities: 135,500.00*Net Worth $99,500.00

* Their net worth is more than twice their annual income, a good ratio.

Chapter 3Developing Financial Statements, Plans and Budgets

• Financial Ratios– Financial ratios are benchmarks of a

person’s current financial status.

– They can also be used to spot worrisome trends in someone’s financial well-being.

Chapter 3Developing Financial Statements, Plans and Budgets

• Four Common Ratios– Liquidity ratio– Debt/Total assets ratio– Debt service ratio– Financial assets/ Net worth

Chapter 3Developing Financial Statements, Plans and Budgets

•Liquidity RatioPurpose:Measures how many months someone can meet his or her expenses with no additional income.

Formula:Cash and near-cash financial assets /monthly living expenses (annual expenses divided by 12)

Chapter 3Developing Financial Statements, Plans and Budgets

•Liquidity RatioCash & near-cash assets / Monthly living expenses

($1,500 + $8,000) / ($57,200 / 12)$9,500 / $4,767

1.99 months

Their liquidity ratio covers only 1.99 months. Most financial advisors suggest having 3 - 6 months coverage. They need to increase their resources in this area.

Chapter 3Developing Financial Statements, Plans and Budgets

•Debt/Total Assets RatioPurpose:Measures ability to pay debts (solvency). Also shows what percentage of assets were acquired using borrowed funds.

Total Liabilities / Total assets$135,500 / $235,000

.58 or 58%

They have almost twice as many assets as liabilities, an excellent ratio.

Chapter 3Developing Financial Statements, Plans and Budgets

•Financial Planning– A financial plan is a guide to reaching

a targeted goal in the future.

Chapter 3Developing Financial Statements, Plans and Budgets

•Budget ComponentsA budget is a short-term monthly financial plan –Income or Cash Inflows

•Includes all money to come in during the month (pay, dividends, bonuses)

–Expenses or Cash OutflowsFixed expenses

Remains constant each month (mortgage payment

Variable expensesFluctuate from month to month (clothing)

Chapter 3Developing Financial Statements, Plans and Budgets

• Cash Inflows for July

Estimated Actual Variance

*Net salary $4,500 $4,500 $0

*Div & interest 100 125 $25

*Bonus 0 0 $0

TOTAL $4,600 $4,625 $25

Chapter 3Developing Financial Statements, Plans and Budgets

• Fixed Outflows for July Estimated Actual Variance Mortgage $800 $800 $0 Auto loan 250 250 0 Life insur. 50 50 0 Auto insur. 350 350 0 Savings 500 500 0 TOTAL $1950 $1950 $0

Chapter 3Developing Financial Statements, Plans and Budgets

• Selected Variable Outflows for JulyEstimated Actual Variance

Utilities $100 $125 ($25)Telephone 75 100 (25)Food 400 350 50Vacation 600 800 (200)Gifts 50 100 (50)Spending 400 375 25Totals $1,625 $1,850 ($225)

Estimated ActualVarianceUtilities $100 $125 ($25)Telephone 75 100 (25)Food 400 350 50Vacation 600 800 (200)Gifts 50 100 (50)Spending 400 375 25Totals $1,625 $1,850 ($225)

Chapter 3Developing Financial Statements, Plans and Budgets

• Record Keeping– Crucial to sound financial management– Should be kept on all financial assets– Where to keep records?

• File cards• Safe-deposit boxes• Home computers

– How long to keep records?• IRS cannot audit after three years except for fraud• If discarded, is it available elsewhere?