Chapter 2: The Conceptual Framework 上海金融学院会计学院. 1.Describe the usefulness of a...

19

Chapter 2: Chapter 2: The Conceptual Framework The Conceptual Framework 上上上上上上上上上上

-

Upload

emily-foster -

Category

Documents

-

view

332 -

download

1

Transcript of Chapter 2: The Conceptual Framework 上海金融学院会计学院. 1.Describe the usefulness of a...

Chapter 2: Chapter 2: The Conceptual FrameworkThe Conceptual Framework

上海金融学院会计学院

1. Describe the usefulness of a conceptual framework.

2. Describe the FASB's efforts to construct a conceptual framework.

3. Understand the objectives of financial reporting.

4. Identify the qualitative characteristics of accounting information.

After studying this chapter, you should be able to:

Chapter 2: The Chapter 2: The Conceptual FrameworkConceptual Framework

5. Define the basic elements of financial statements.

6. Describe the basic assumptions of accounting.

7. Explain the application of the basic principles of accounting.

8. Describe the impact that constraints have on reporting accounting information.

Chapter 2: The Chapter 2: The Conceptual FrameworkConceptual Framework

• The Framework was to be the foundation for building a set of coherent accounting standards and rules.

• The Framework is to be a reference of basic accounting theory for solving emerging practical problems of reporting.

Objectives of the Objectives of the Conceptual FrameworkConceptual Framework

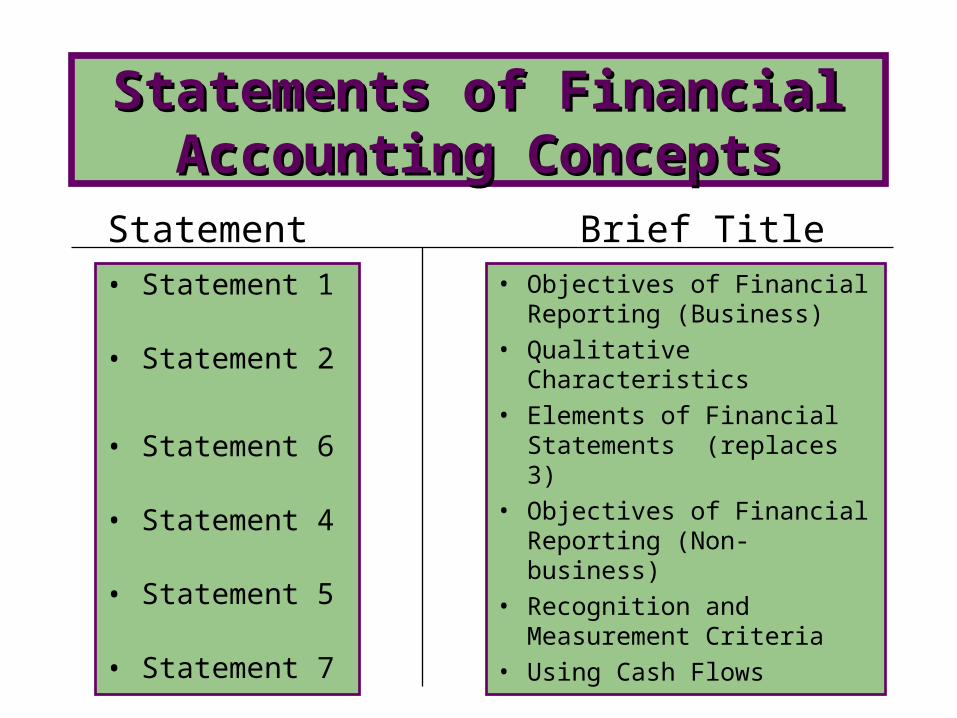

• The FASB has issued seven Statements of Financial Accounting Concepts (SFACs) to date (Statements 1 through 7.)

• These statements set forth major recognition and reporting issues.

• Statement 4 pertains to reporting by non-business entities.

• The other six statements pertain to reporting by business enterprises.

Statements of Financial Statements of Financial Accounting ConceptsAccounting Concepts

• Statement 1

• Statement 2

• Statement 6

• Statement 4

• Statement 5

• Statement 7

• Objectives of Financial Reporting (Business)

• Qualitative Characteristics

• Elements of Financial Statements (replaces 3)

• Objectives of Financial Reporting (Non-business)

• Recognition and Measurement Criteria

• Using Cash Flows

Brief TitleStatement

Statements of Financial Statements of Financial Accounting ConceptsAccounting Concepts

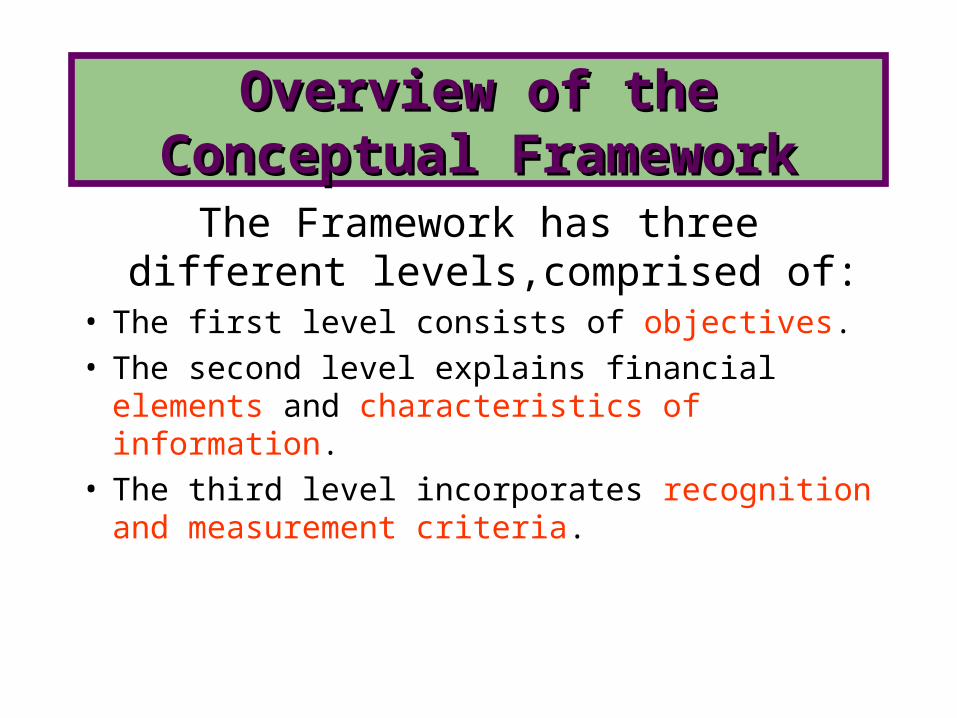

The Framework has three different levels,comprised of:

• The first level consists of objectives.• The second level explains financial

elements and characteristics of information.

• The third level incorporates recognition and measurement criteria.

Overview of the Overview of the Conceptual FrameworkConceptual Framework

Conceptual Framework Conceptual Framework for Financial Reportingfor Financial Reporting

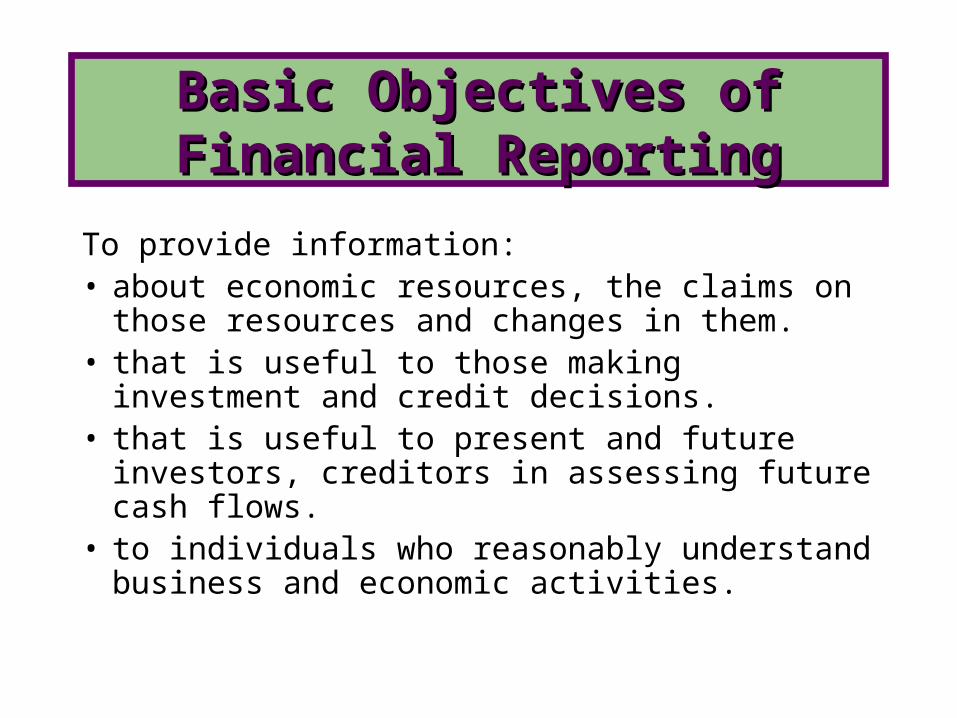

To provide information:• about economic resources, the claims on

those resources and changes in them.• that is useful to those making investment

and credit decisions.• that is useful to present and future

investors, creditors in assessing future cash flows.

• to individuals who reasonably understand business and economic activities.

Basic Objectives of Basic Objectives of Financial ReportingFinancial Reporting

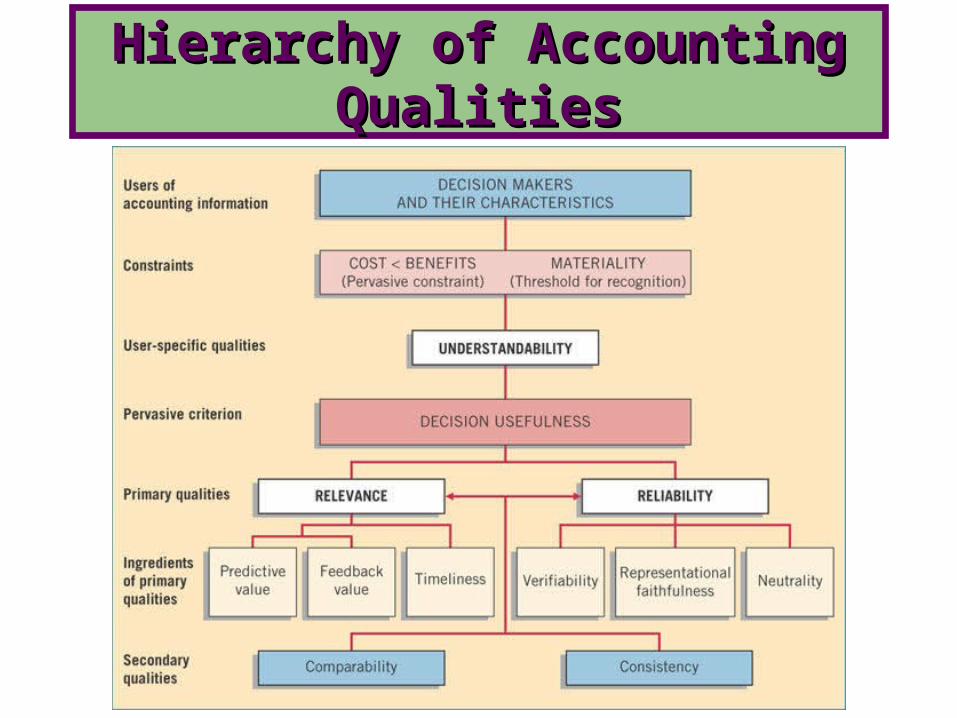

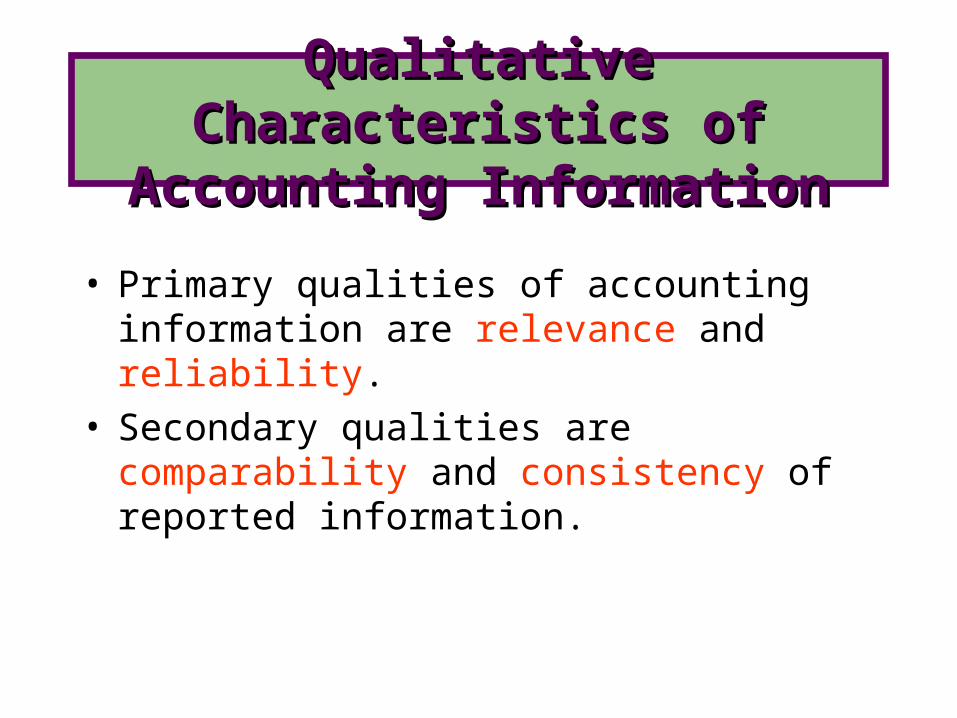

Hierarchy of Accounting Hierarchy of Accounting QualitiesQualities

• Primary qualities of accounting information are relevance and reliability.

• Secondary qualities are comparability and consistency of reported information.

Qualitative Qualitative Characteristics of Characteristics of

Accounting InformationAccounting Information

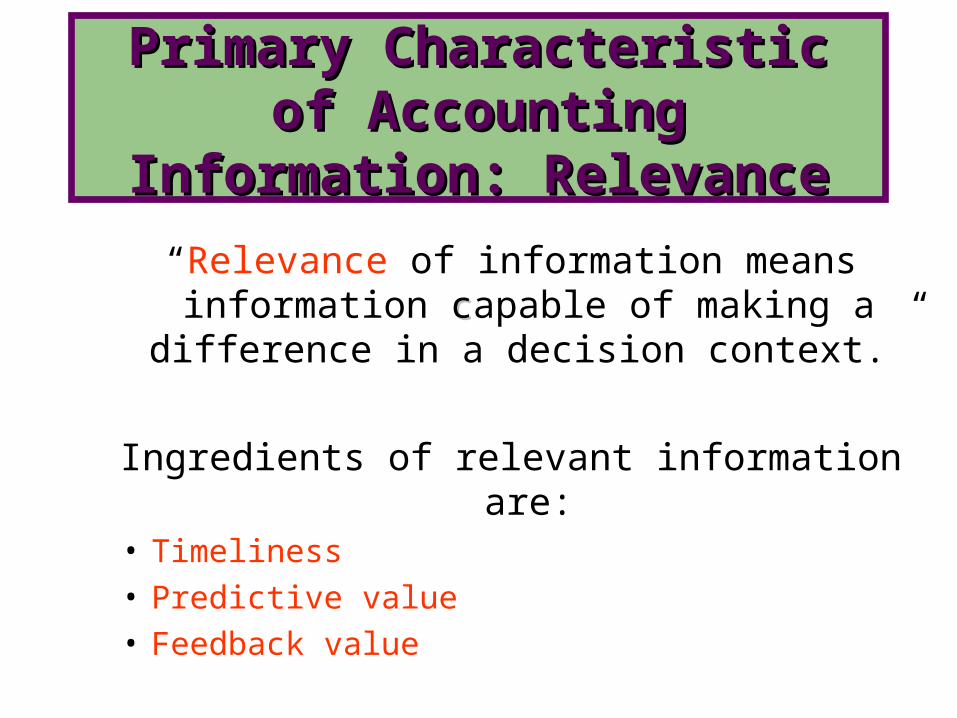

“Relevance of information means information ccapable of making a difference in a decision

context.”

Ingredients of relevant information are:• Timeliness• Predictive value• Feedback value

Primary Characteristic of Primary Characteristic of Accounting Information: Accounting Information:

RelevanceRelevance

Information is reliable when it can be relied on to represent the true,

underlying situation.

The ingredients of reliable information are:

• verifiability• representational faithfulness• neutrality (unbiased)

Primary Characteristic of Primary Characteristic of Accounting Information: Accounting Information:

RelevanceRelevance

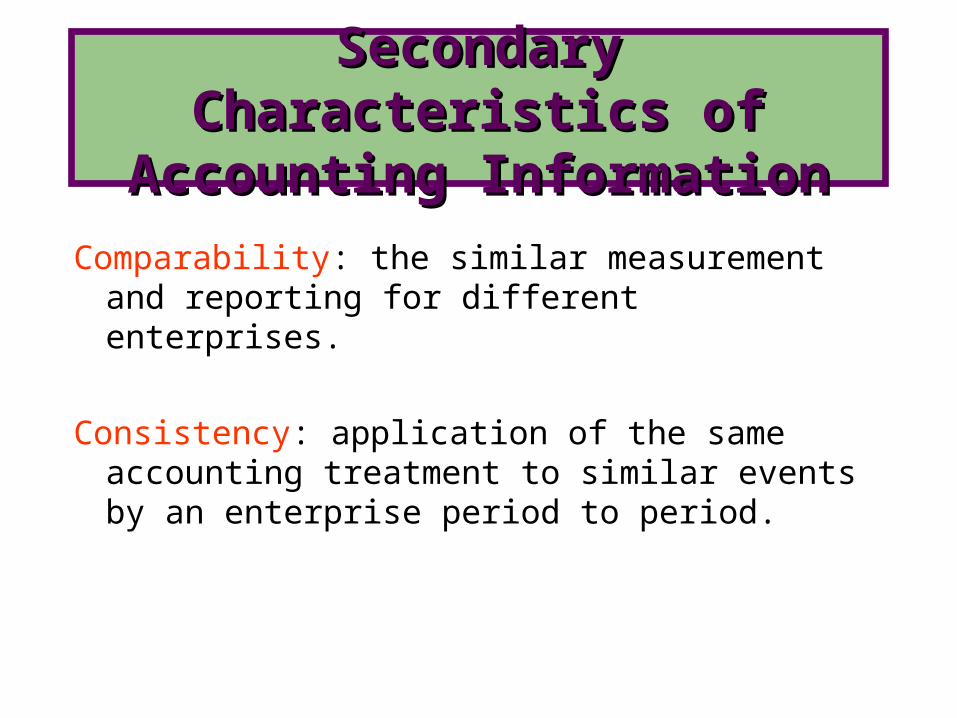

Comparability: the similar measurement and reporting for different enterprises.

Consistency: application of the same accounting treatment to similar events by an enterprise period to period.

Secondary Characteristics Secondary Characteristics of Accounting Informationof Accounting Information

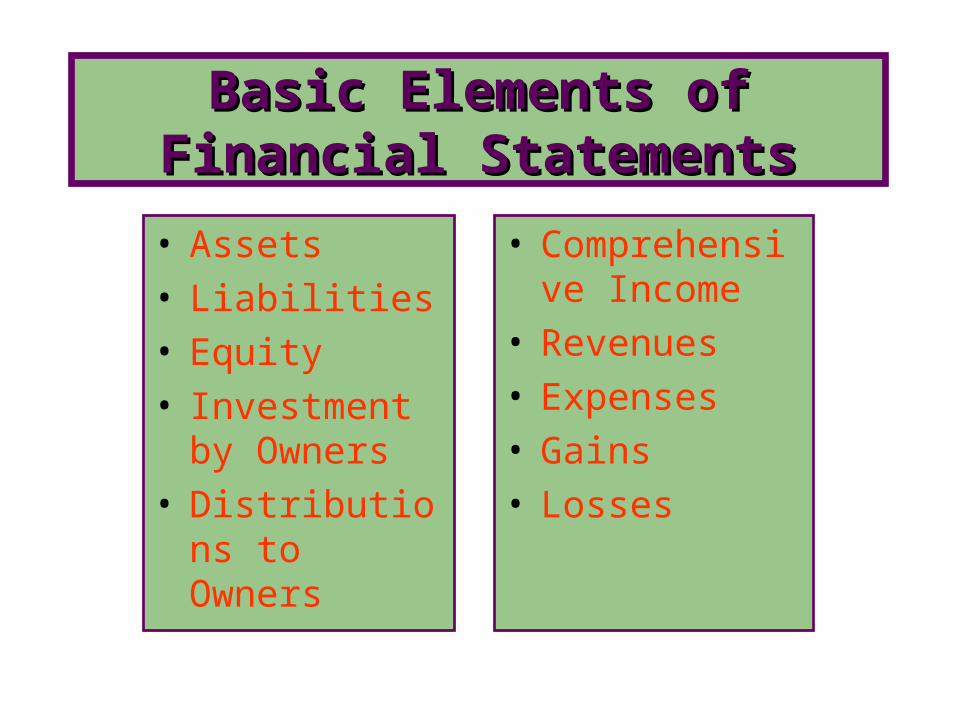

• Assets• Liabilities• Equity• Investment

by Owners• Distributions

to Owners

• Comprehensive Income

• Revenues• Expenses• Gains• Losses

Basic Elements of Basic Elements of Financial StatementsFinancial Statements

BasicAssumptions

1. Economic entity 2. Going concern 3. Monetary

unit4. Periodicity

Principles

1. Historical cost

2. Revenue recognition

3. Matching4. Full

disclosure

Constraints

1. Cost benefit2. Materiality3. Industry practices4. Conservatism

Recognition and Recognition and Measurement CriteriaMeasurement Criteria

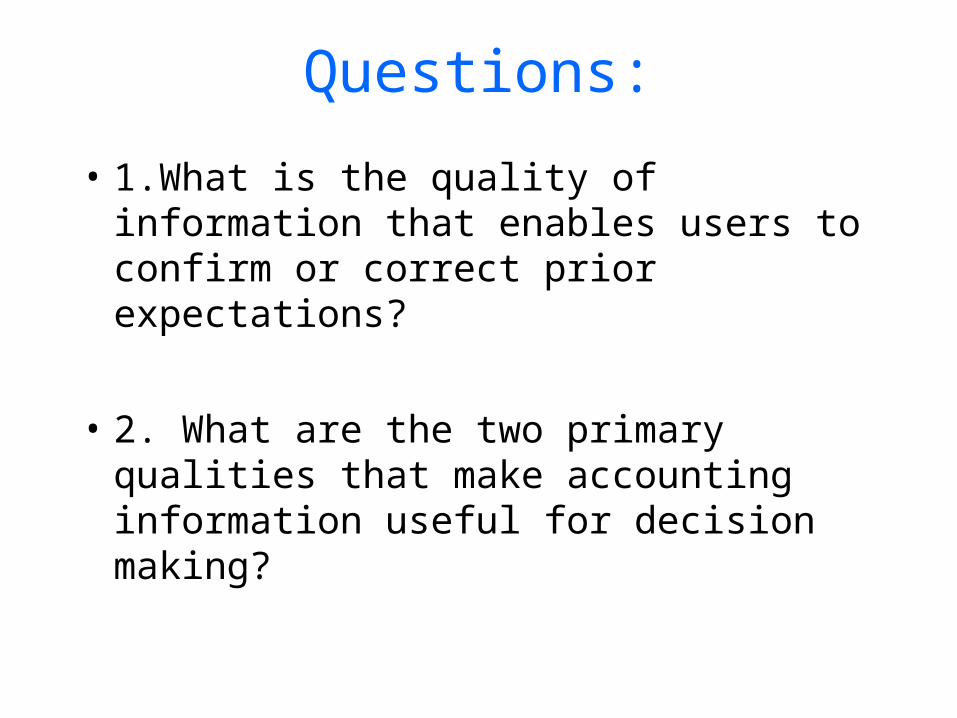

Questions:

• 1.What is the quality of information that enables users to confirm or correct prior expectations?

• 2. What are the two primary qualities that make accounting information useful for decision making?

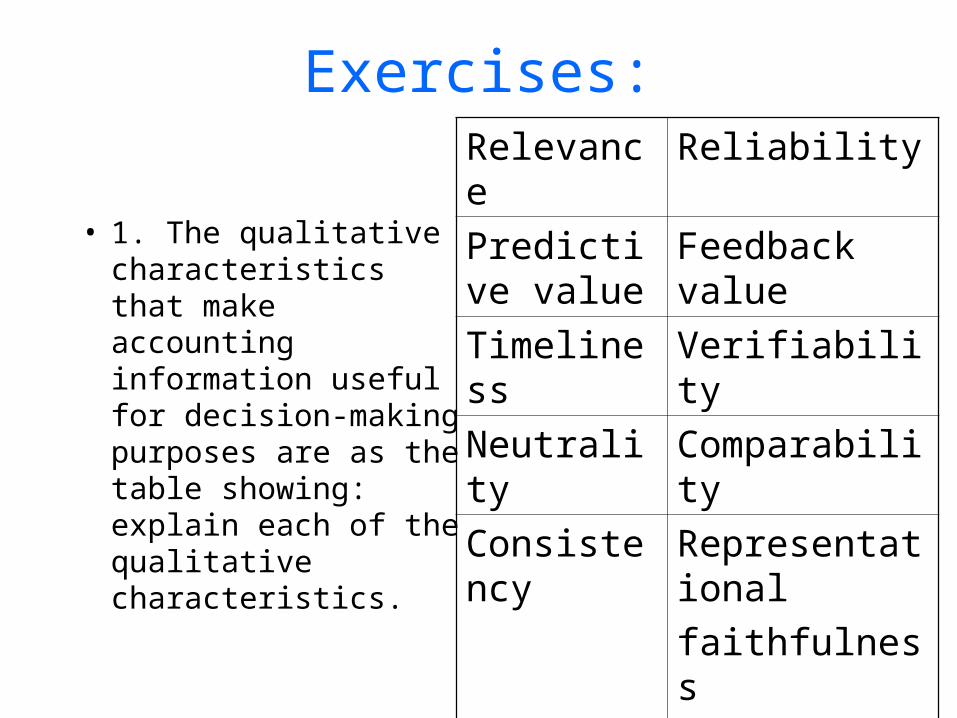

Exercises:

• 1. The qualitative characteristics that make accounting information useful for decision-making purposes are as the table showing: explain each of the qualitative characteristics.

Relevance Reliability

Predictive value

Feedback value

Timeliness Verifiability

Neutrality Comparability

Consistency Representational

faithfulness

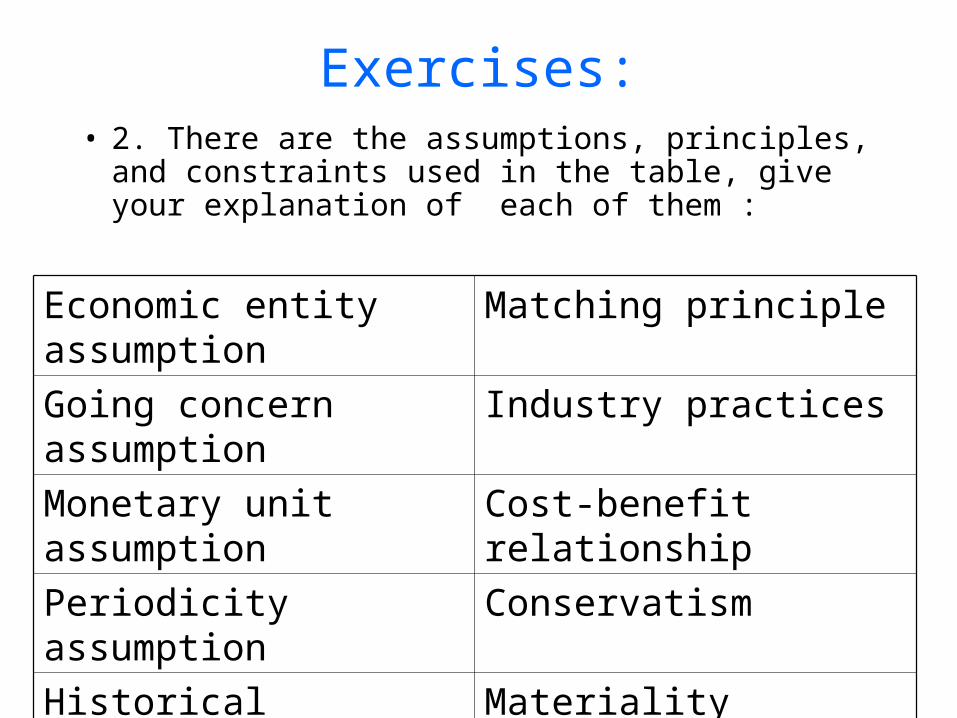

Exercises:• 2. There are the assumptions, principles, and

constraints used in the table, give your explanation of each of them :

Economic entity assumption

Matching principle

Going concern assumption Industry practices

Monetary unit assumption Cost-benefit relationship

Periodicity assumption Conservatism

Historical principle Materiality

Full disclosure principle