Centre for Disruptive Technologies Mobile Money & Payments Presentation

date post

22-Dec-2015Category

view

264download

8

Chapter 2 of Cecchetti

Money and the Payments System

MoneyMoney

Money is an asset that is generally accepted as payment for goods and services or repayment of debt.

1. A means of payment. Transferability Information

2. A unit of account Allocation of resources Relative prices

3. A store of value Liquidity

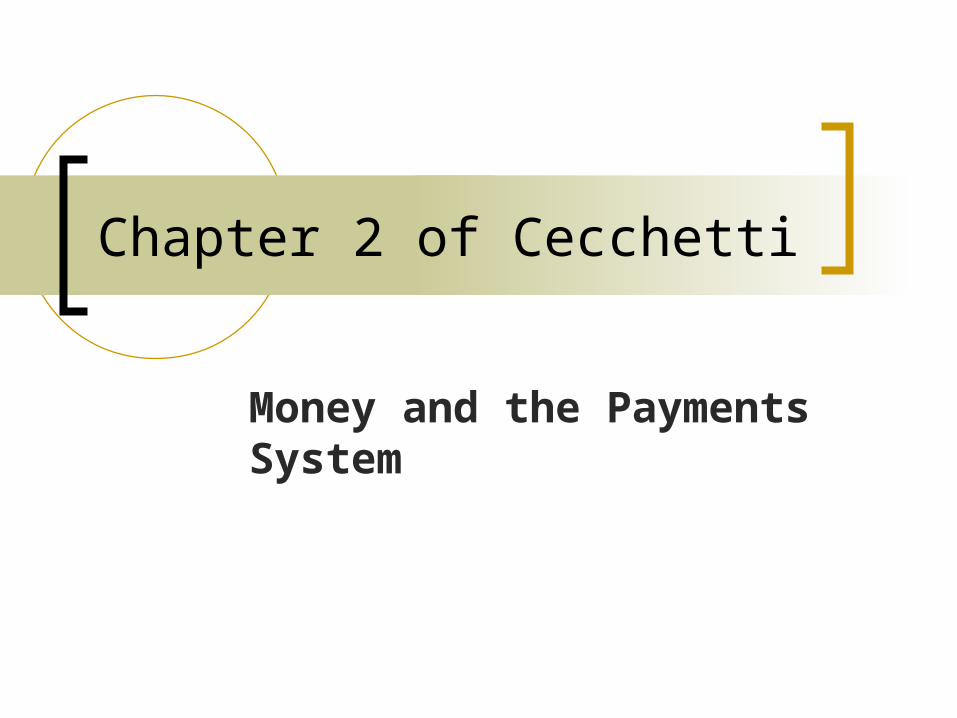

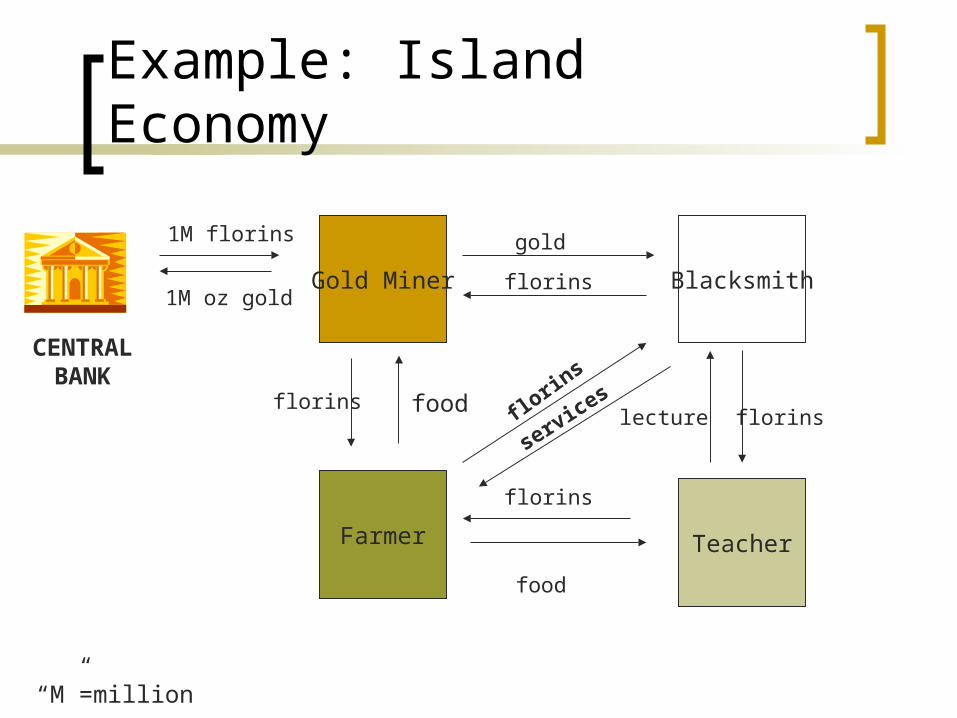

Example: Island Economy

Farmer

Gold Miner Blacksmith

Teacher

1M florins

1M oz gold

CENTRALBANK

“M”=million

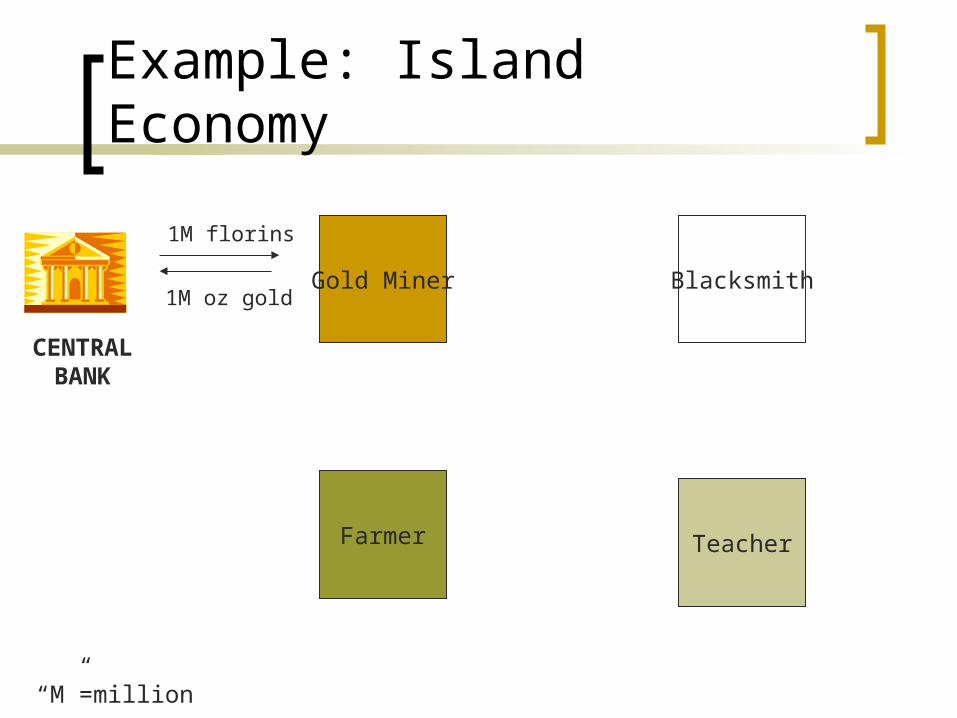

Example: Island Economy

Central bank declares it stands ready to redeem 1 florin for 1 ounce of gold from anyone at any time.

Balance Sheet of

Central Bank

ASSETS LIABILITIES

Gold: 1M fl Currency: 1M fl

Example: Island Economy

Farmer

Gold Miner Blacksmith

Teacher

1M florins

1M oz gold

CENTRALBANK

“M”=million

florins food florin

s

florins

food

lecture florinsservices

florins

gold

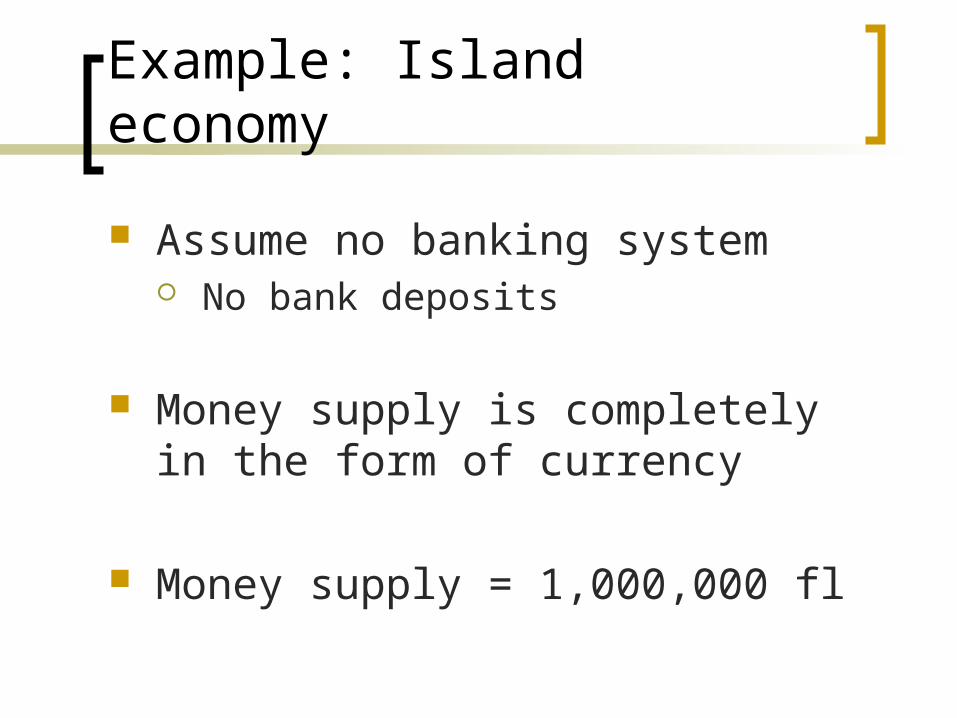

Example: Island economy

Assume no banking system No bank deposits

Money supply is completely in the form of currency

Money supply = 1,000,000 fl

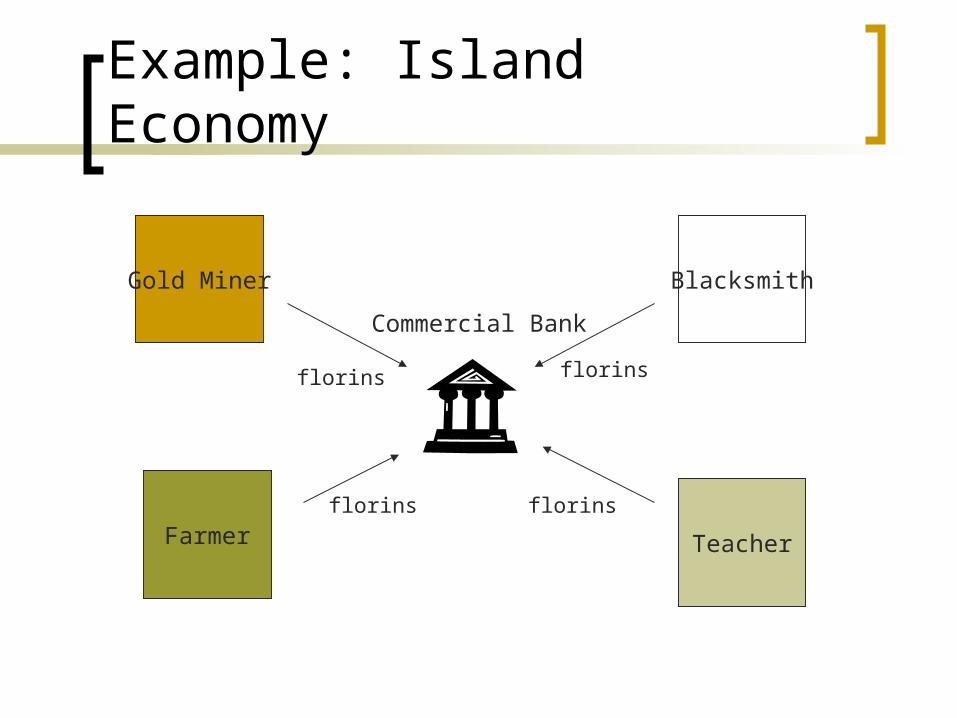

Example: Island Economy

Farmer

Gold Miner Blacksmith

Teacher

florins florins

florinsflorins

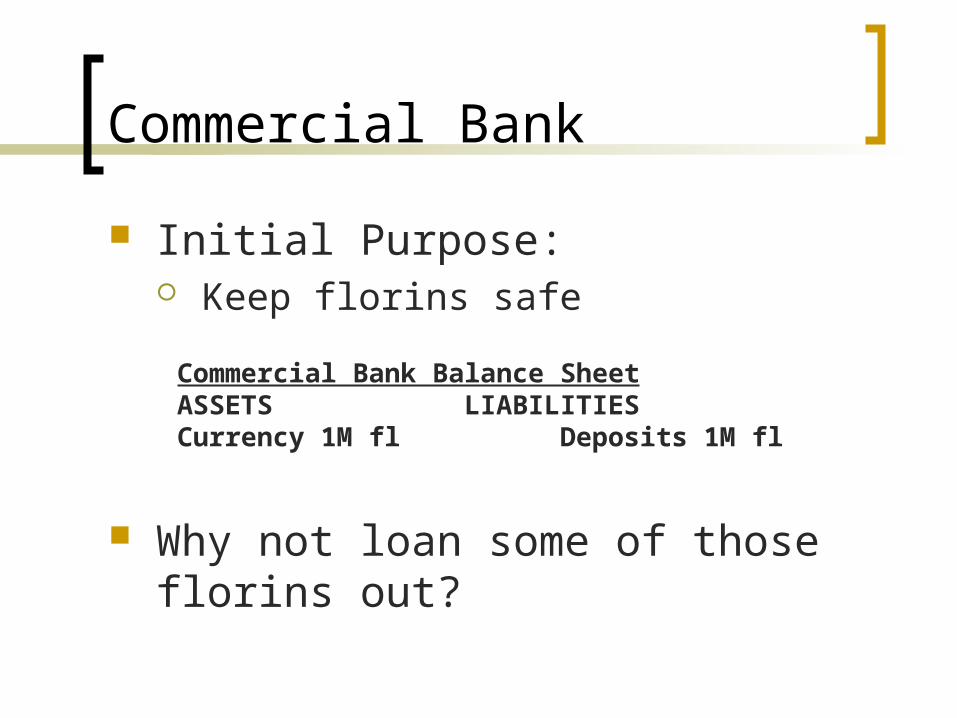

Commercial Bank

Commercial Bank

Initial Purpose: Keep florins safe

Why not loan some of those florins out?

Commercial Bank Balance SheetASSETS LIABILITIESCurrency 1M fl Deposits 1M fl

Example: Island Economy

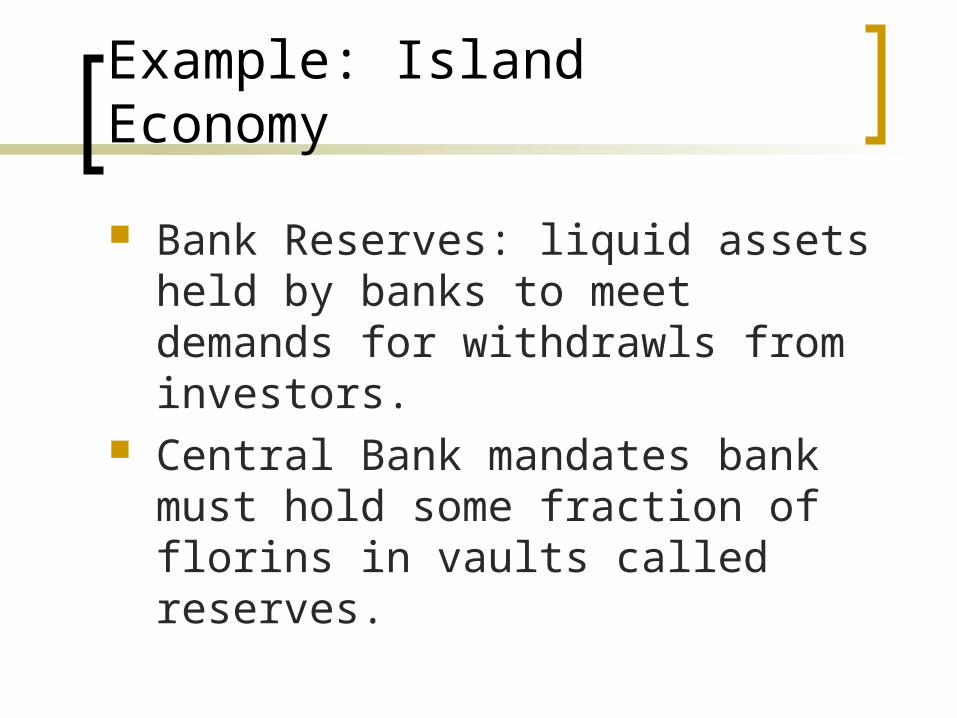

Bank Reserves: liquid assets held by banks to meet demands for withdrawls from investors.

Central Bank mandates bank must hold some fraction of florins in vaults called reserves.

Example: Island Economy

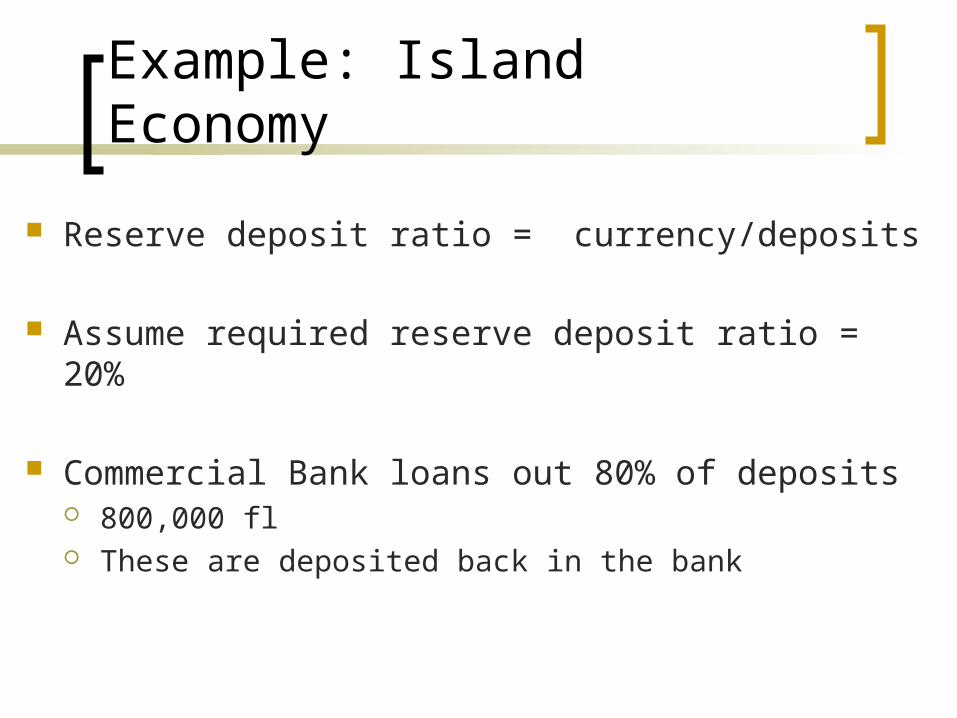

Reserve deposit ratio = currency/deposits

Assume required reserve deposit ratio = 20%

Commercial Bank loans out 80% of deposits 800,000 fl These are deposited back in the bank

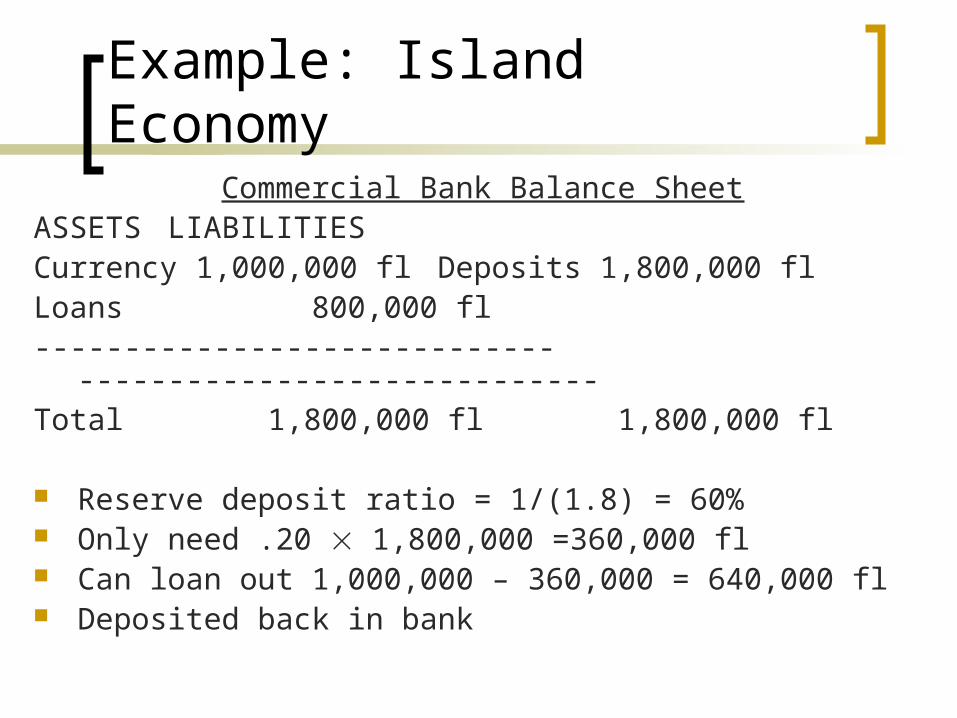

Example: Island EconomyCommercial Bank Balance Sheet

ASSETS LIABILITIESCurrency 1,000,000 fl Deposits 1,800,000 flLoans 800,000 fl----------------------------- -----------------------------Total 1,800,000 fl 1,800,000 fl

Reserve deposit ratio = 1/(1.8) = 60% Only need .20 1,800,000 =360,000 fl Can loan out 1,000,000 – 360,000 = 640,000 fl Deposited back in bank

Example: Island EconomyConsolidated Balance Sheet of Banks

ASSETS LIABILITIESCurrency 1,000,000 fl Deposits 2,440,000 flLoans 1,440,000 fl----------------------------- -----------------------------Total 2,440,000 fl 2,400,000 fl

Reserve deposit ratio = 1/(2.4) = 42% Only need .20 2,440,000 =488,000 fl Can loan out 1,000,000 – 488,000 = 512,000 fl Does this just go on forever . . . . . ?

Example: Island Economy

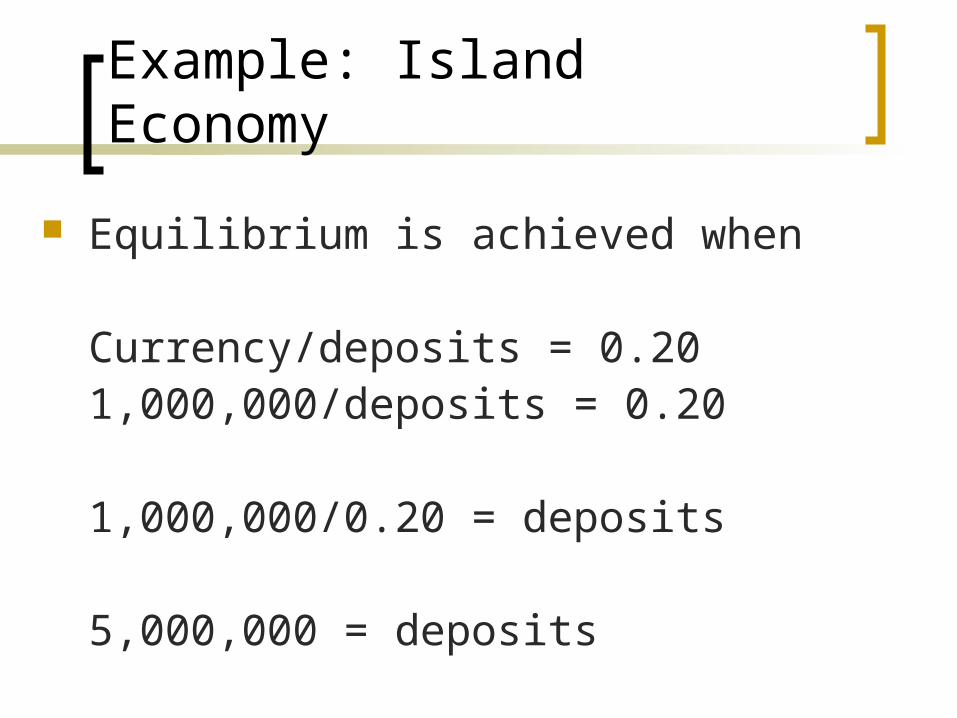

Equilibrium is achieved when

Currency/deposits = 0.201,000,000/deposits = 0.20

1,000,000/0.20 = deposits

5,000,000 = deposits

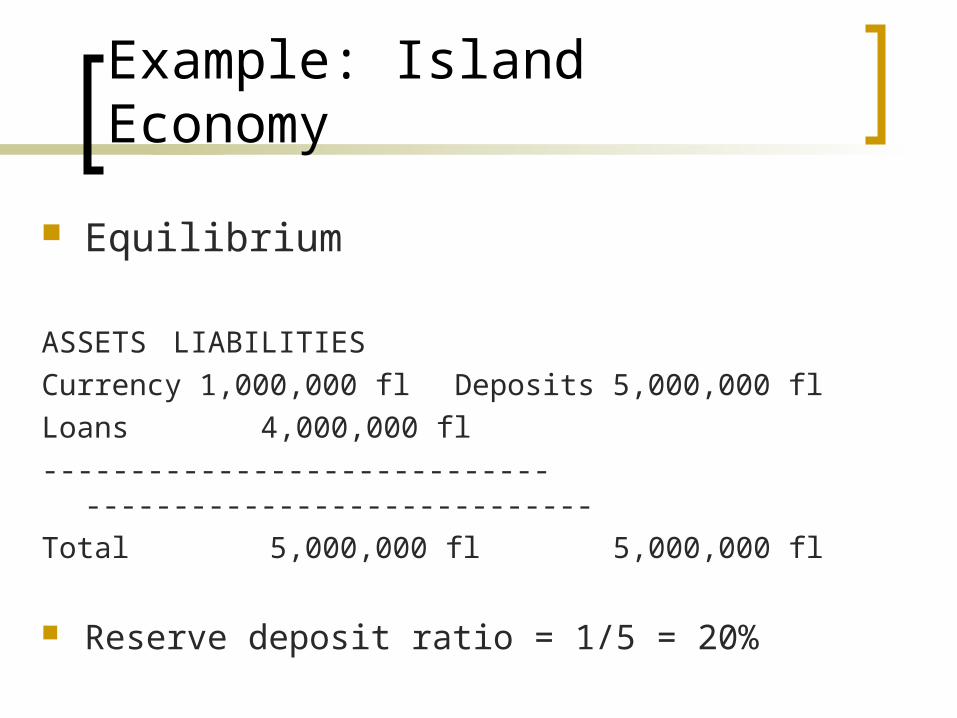

Example: Island Economy

Equilibrium

ASSETS LIABILITIES

Currency 1,000,000 fl Deposits 5,000,000 fl

Loans 4,000,000 fl

----------------------------- -----------------------------

Total 5,000,000 fl 5,000,000 fl

Reserve deposit ratio = 1/5 = 20%

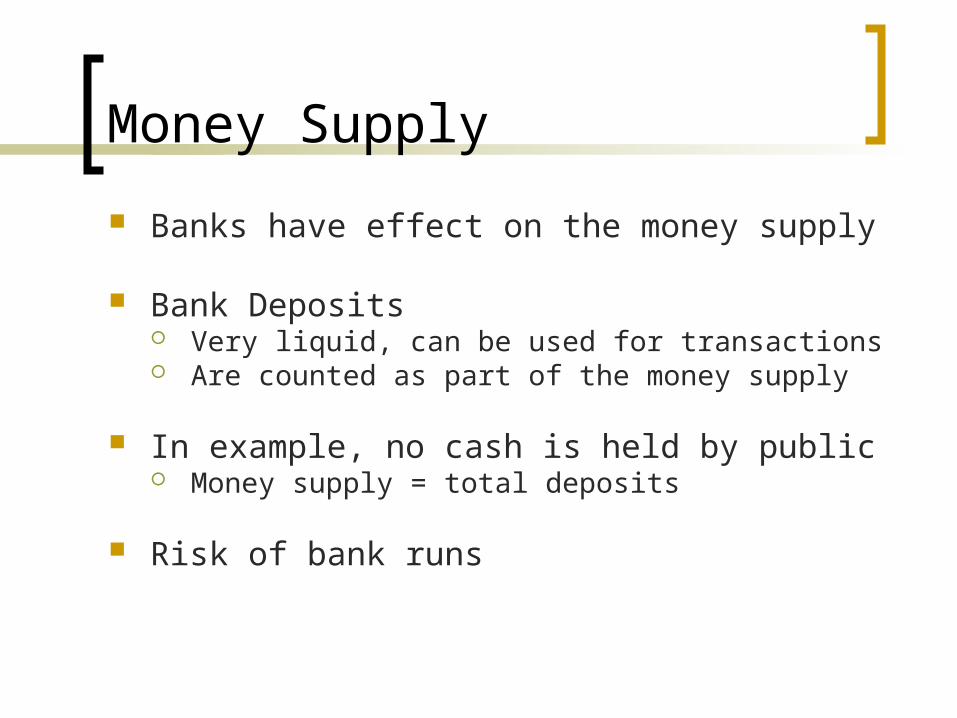

Money Supply

Banks have effect on the money supply

Bank Deposits Very liquid, can be used for transactions Are counted as part of the money supply

In example, no cash is held by public Money supply = total deposits

Risk of bank runs

Measuring Money

Different Definitions of money based upon degree of liquidity.

Federal Reserve System defines monetary aggregates: measures of money

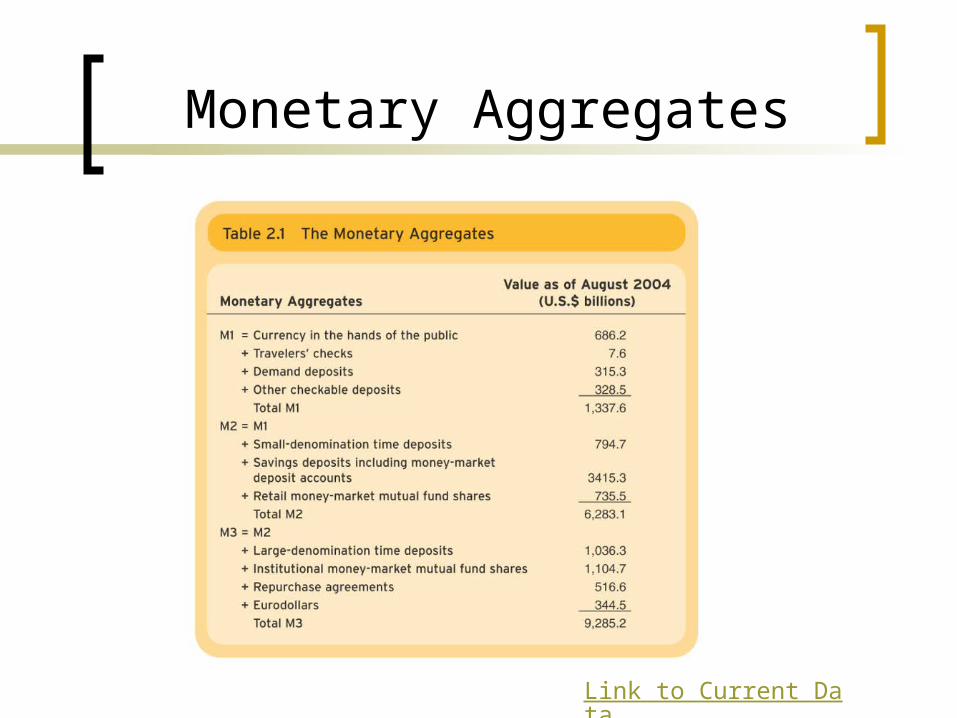

Monetary Aggregates

Link to Current Data

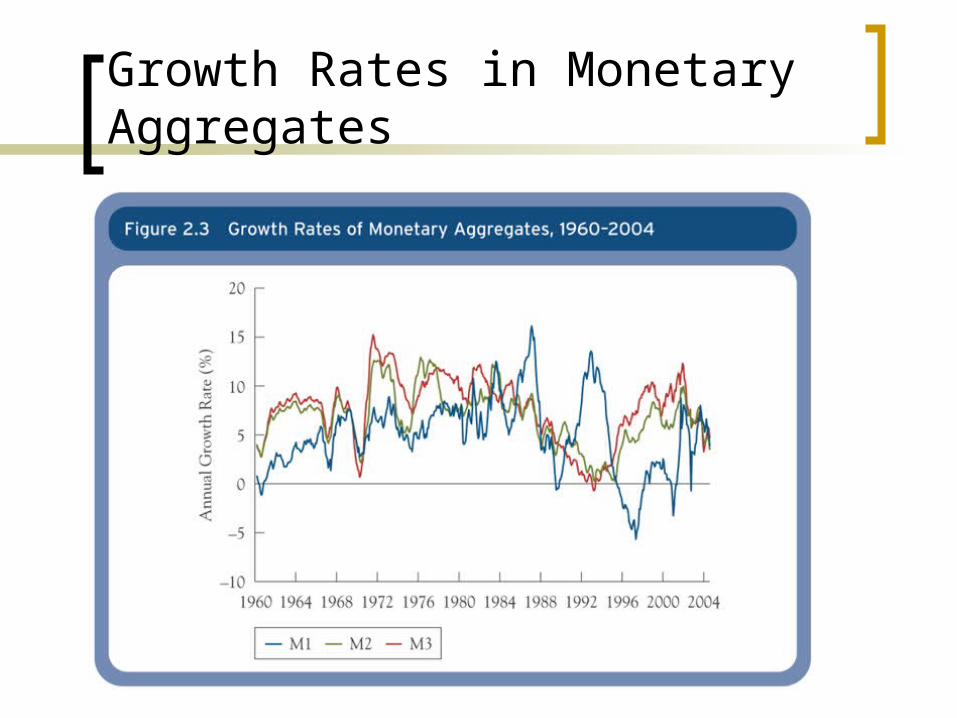

Growth Rates in Monetary Aggregates

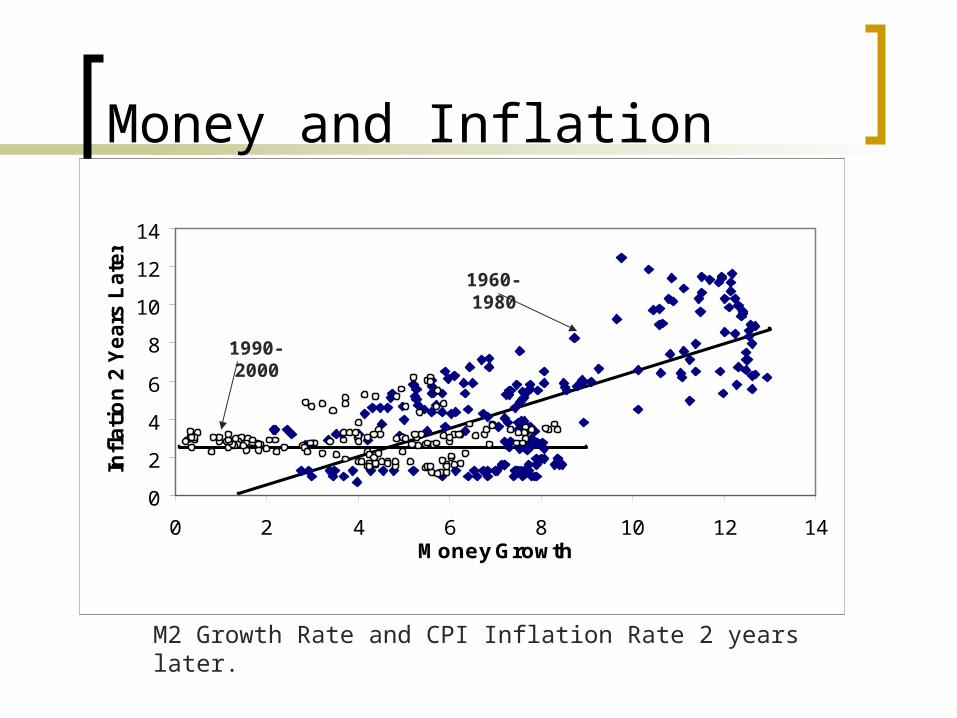

Money and Inflation

0

2

4

6

8

10

12

14

0 2 4 6 8 10 12 14Money Growth

Infl

ati

on

2 Y

ea

rs L

ate

r

1990-2000

1960-1980

M2 Growth Rate and CPI Inflation Rate 2 years later.

Changes in Rates

Chapter 6 of Cecchetti

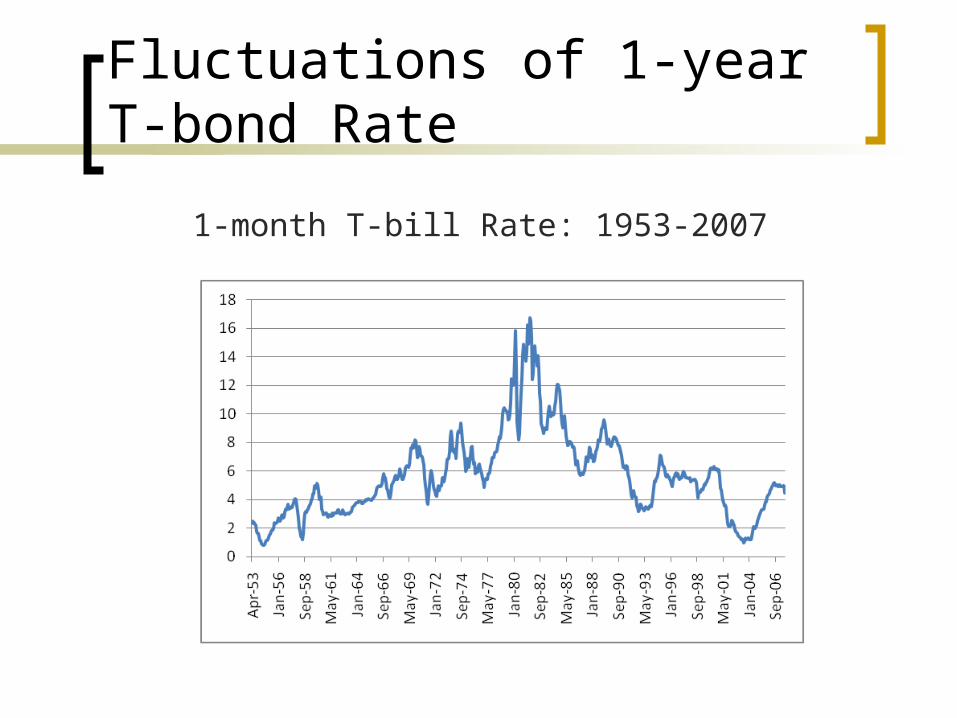

Fluctuations of 1-year T-bond Rate

1-month T-bill Rate: 1953-2007

Bond Demand and Supply

From perspective of primary market Market in which firms issue debt, sell to investors Suppliers: Firms and Government Demanders: Investors

Looking at secondary market, does not allow us to investigate firm behavior Market in which investors buy and sell bonds among

themselves

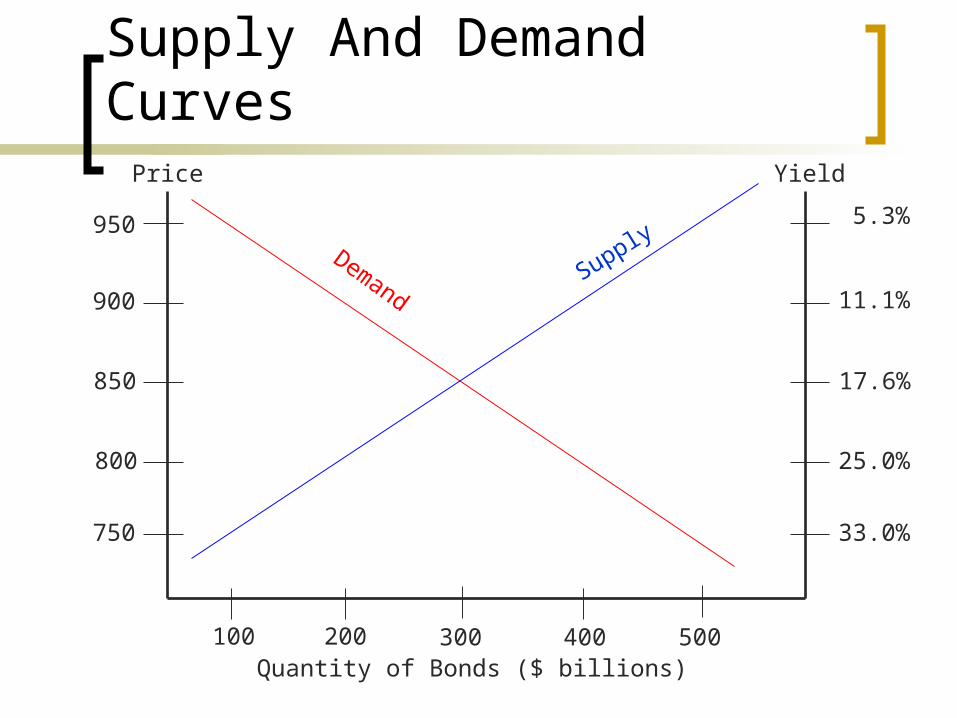

Supply And Demand Curves

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

SupplyDemand

Suppliers

We could actually have two supply curves Government Firms

Factors that impact one sector may not impact the other

Government and Corporate rates are connected.

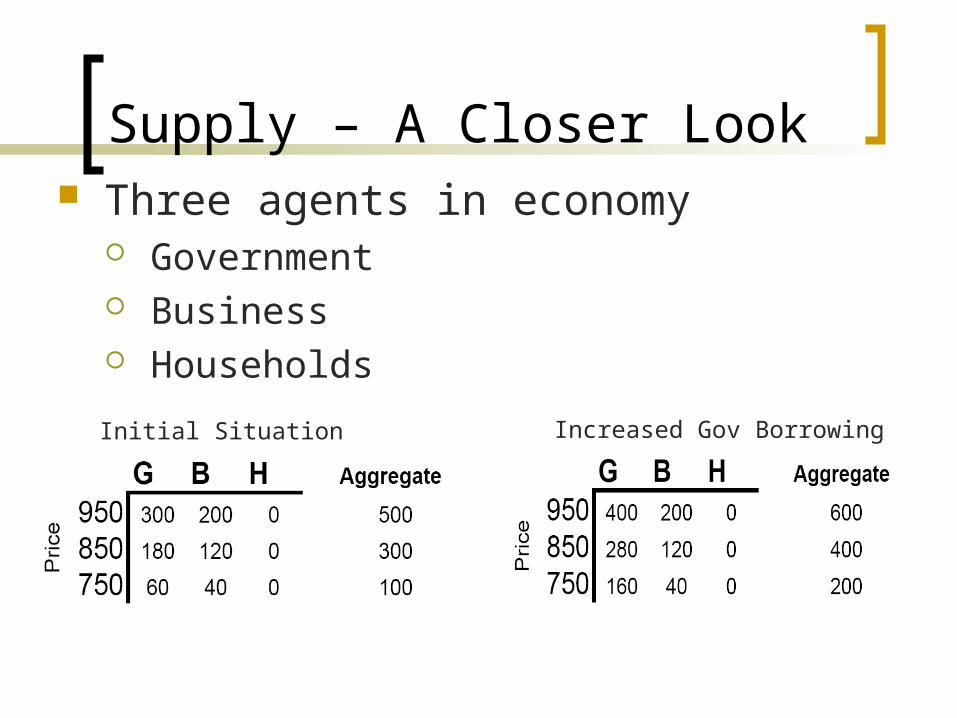

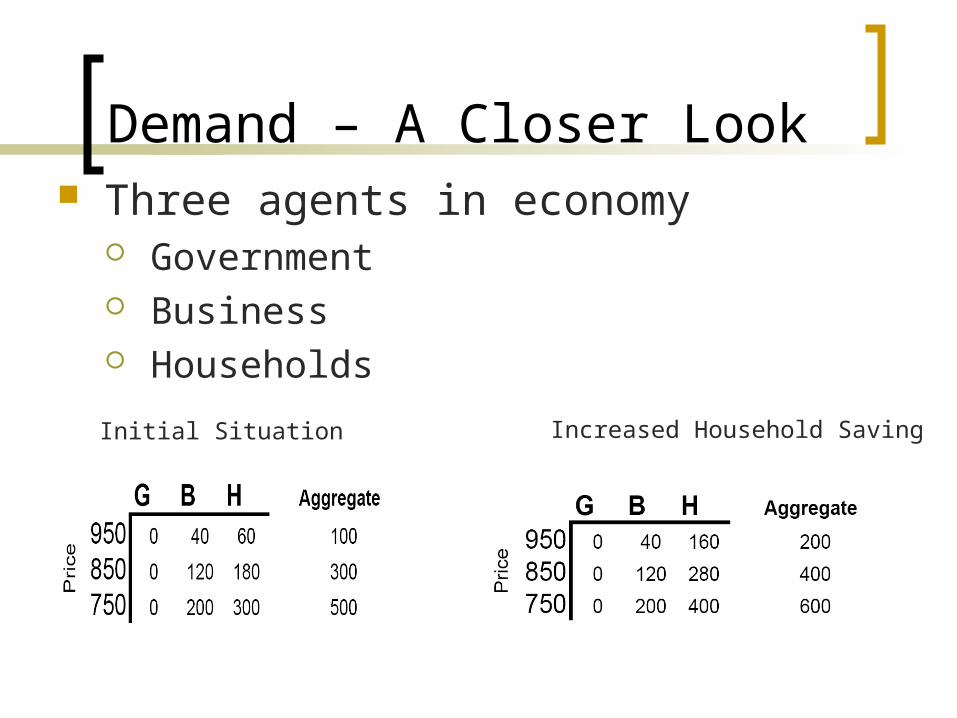

Supply – A Closer Look Three agents in economy

Government Business Households

Initial Situation Increased Gov Borrowing

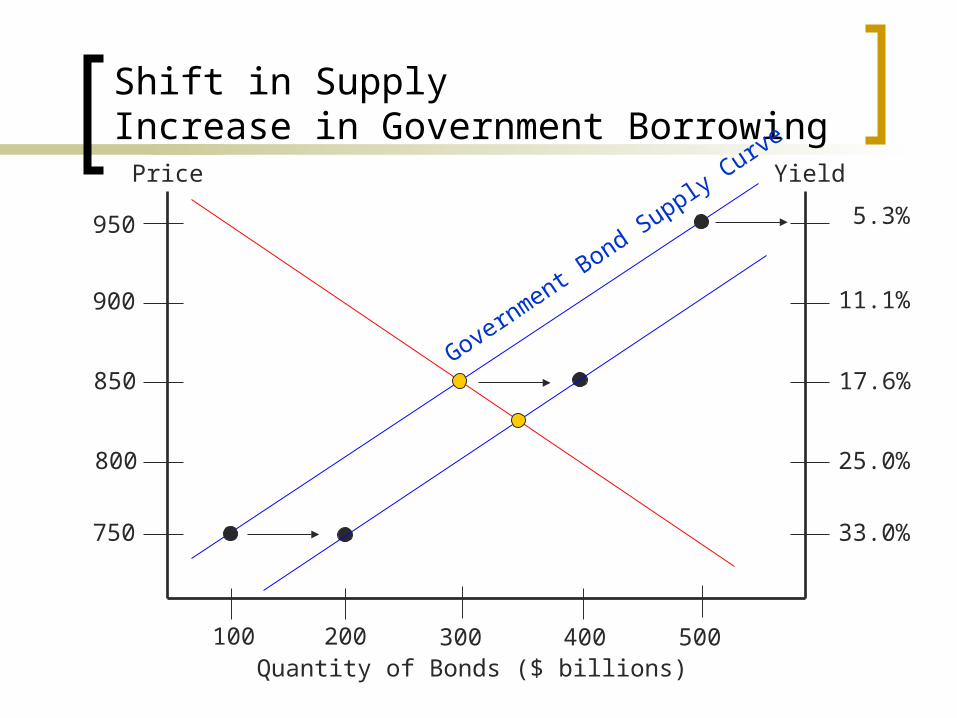

Shift in SupplyIncrease in Government Borrowing

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Government B

ond Supply Curve

Changes in Government Borrowing

An increase in Government borrowing The supply curve shifts to the right Prices to decrease Yields to increase

A decrease in Government borrowing The supply curve shifts to the left Prices to increase Yields to decrease

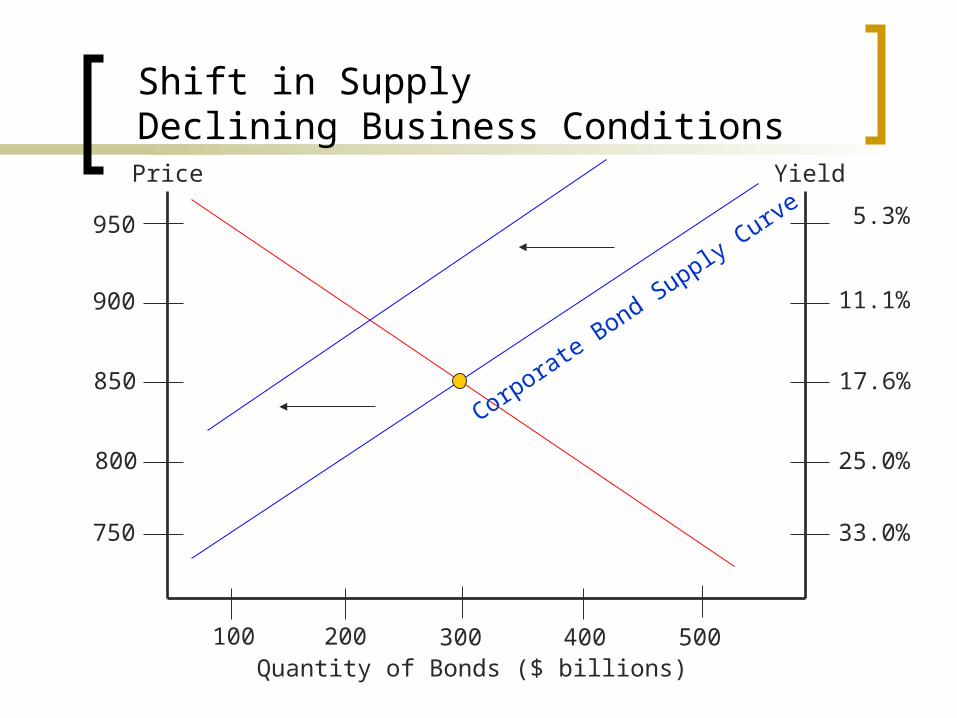

Shift in SupplyDeclining Business Conditions

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Corporate Bond Supply Curve

Changes in Business Conditions

An improvement in business conditions The supply curve to shift to the right Prices to decrease Yields to increase

A decline in business conditions The supply curve to shift to the left Prices to increase Yields to decrease

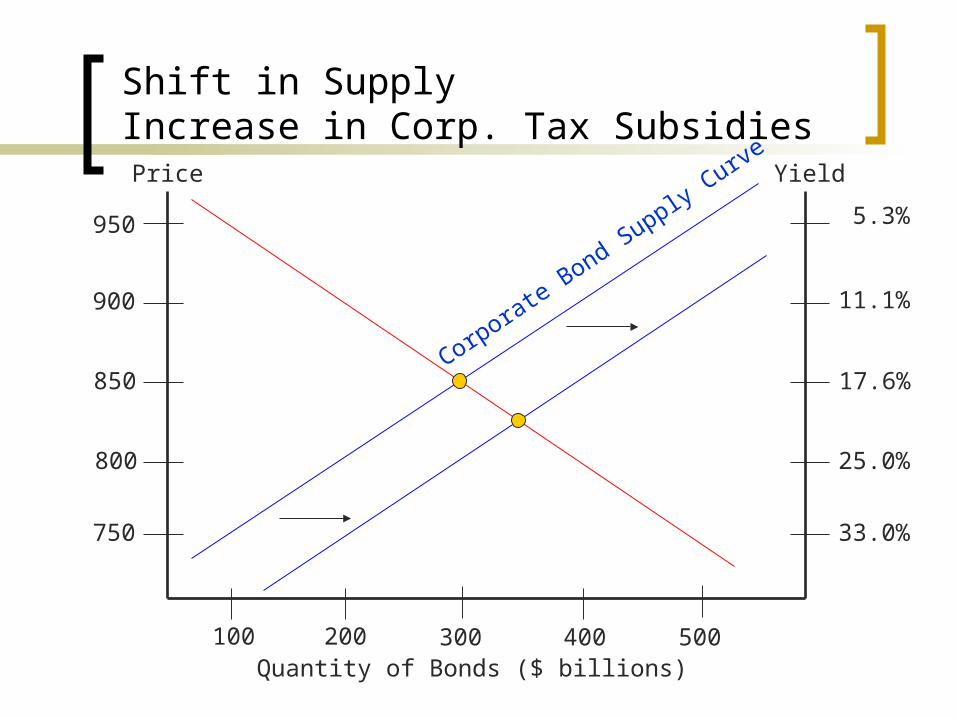

Shift in SupplyIncrease in Corp. Tax Subsidies

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Corporate Bond Supply Curve

Changes in Corp.Tax Subsidies

An increase in Corp. Tax Subsidies The supply curve to shift to the right Prices to decrease Yields to increase

A decrease in Corp. Tax Subsidies The supply curve to shift to the left Prices to increase Yields to decrease

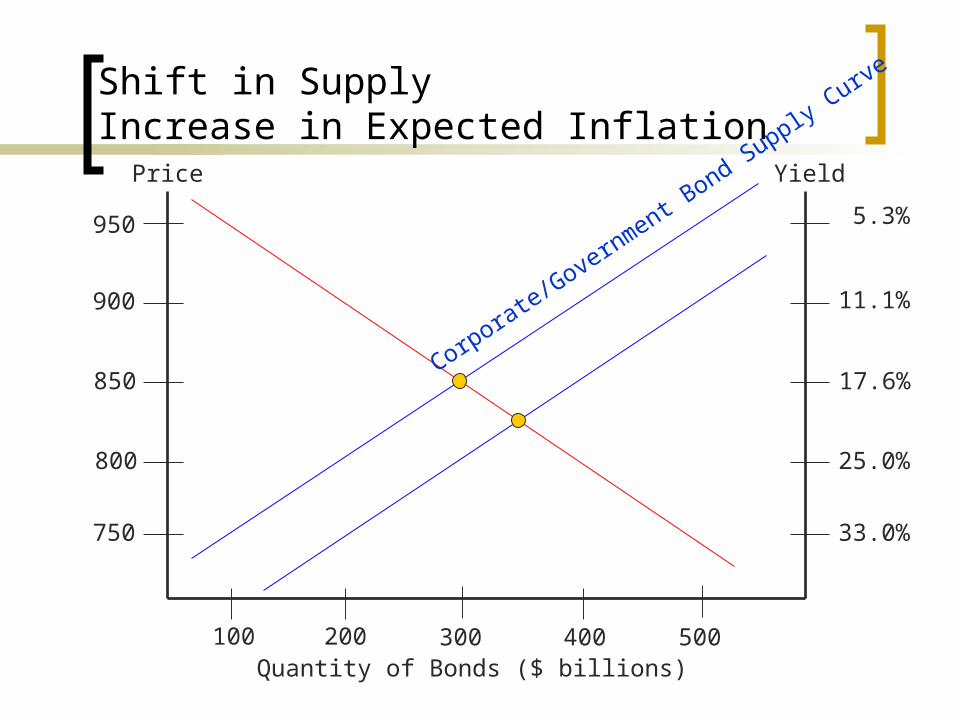

Shift in SupplyIncrease in Expected Inflation

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Corporate/Gove

rnment Bond Supply C

urve

Changes in Expected Inflation

An Increase in Expected Inflation The supply curve to shift to the right Prices to decrease Nominal Yields to increase

A decrease in Expected Inflation The supply curve to shift to the left Prices to increase Nominal Yields to decrease

Demand – A Closer Look Three agents in economy

Government Business Households

Initial Situation Increased Household Saving

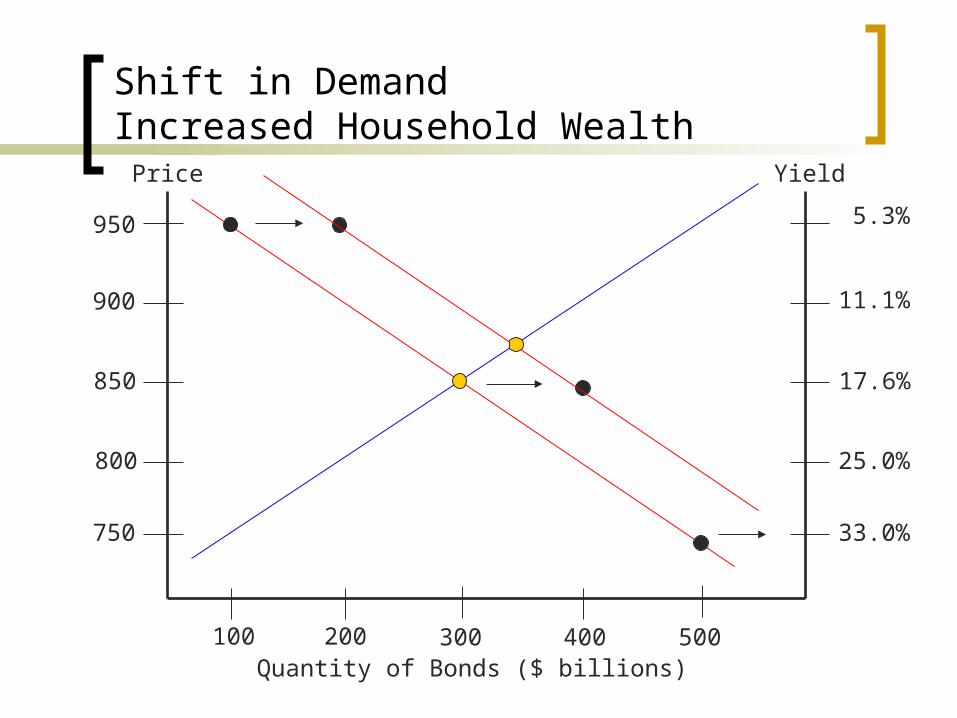

Shift in DemandIncreased Household Wealth

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

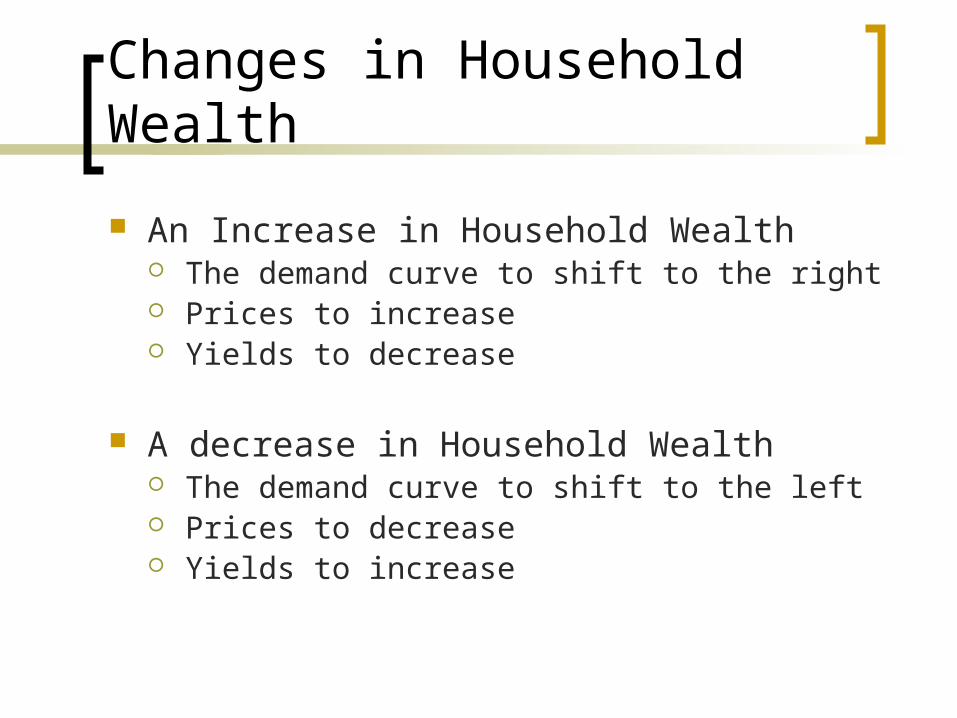

Changes in Household Wealth

An Increase in Household Wealth The demand curve to shift to the right Prices to increase Yields to decrease

A decrease in Household Wealth The demand curve to shift to the left Prices to decrease Yields to increase

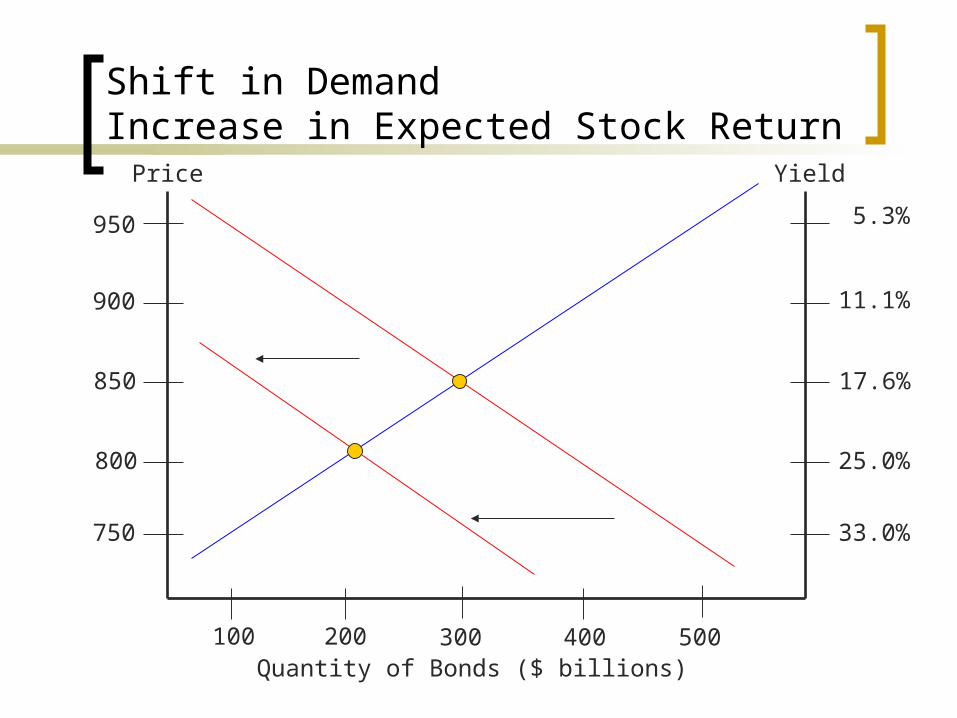

Shift in DemandIncrease in Expected Stock Return

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Changes in Expected Relative Bond Returns

An Increase in Bond Yield – Return Alt. The demand curve to shift to the right Prices to increase Yields to decrease

A decrease in Bond Yield – Return Alt. The demand curve to shift to the left Prices to decrease Yields to increase

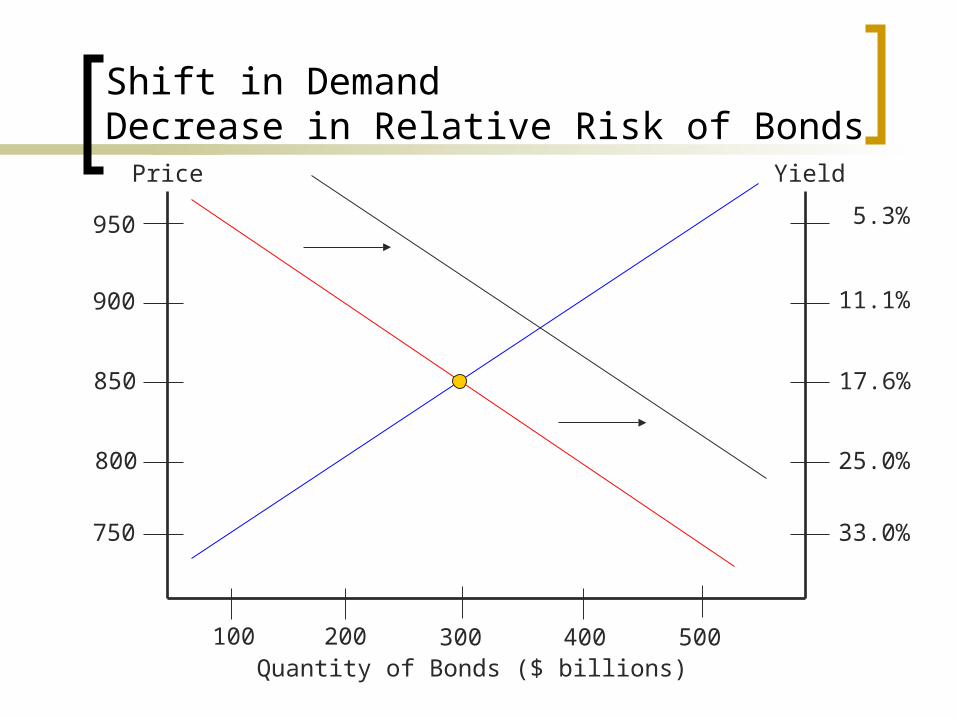

Shift in DemandDecrease in Relative Risk of Bonds

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Changes in Relative Bond Risk

A decrease in Bond Risk – Risk Alt. The demand curve to shift to the right Prices to increase Yields to decrease

An increase in Bond Risk – Risk Alt. The demand curve to shift to the left Prices to decrease Yields to increase

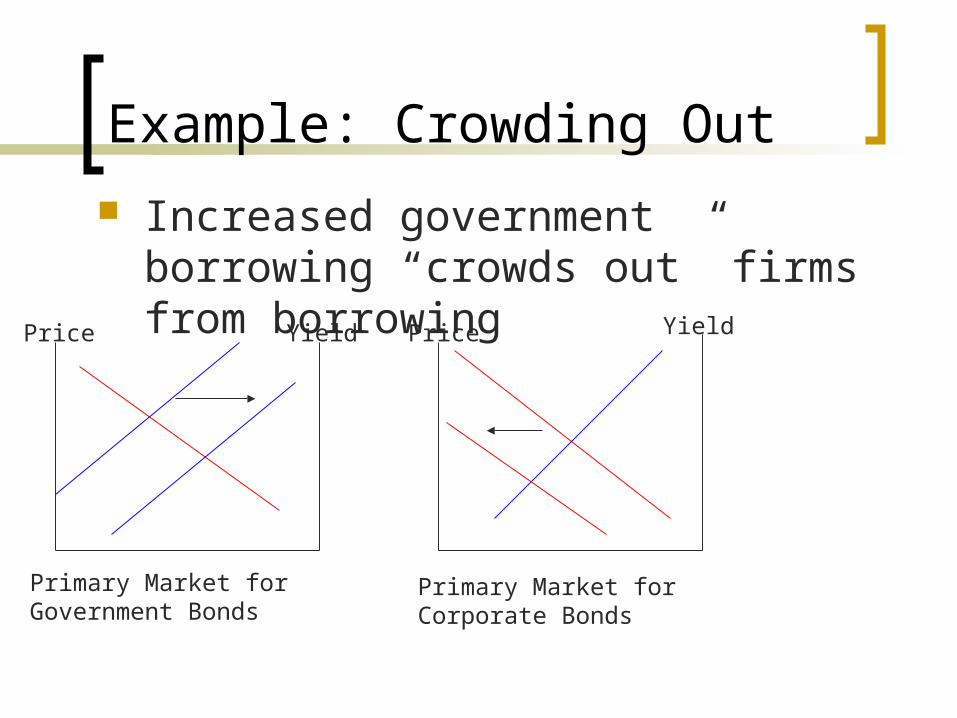

Example: Crowding Out

Increased government borrowing “crowds out” firms from borrowing

Price Yield

Primary Market forGovernment Bonds

Price Yield

Primary Market forCorporate Bonds

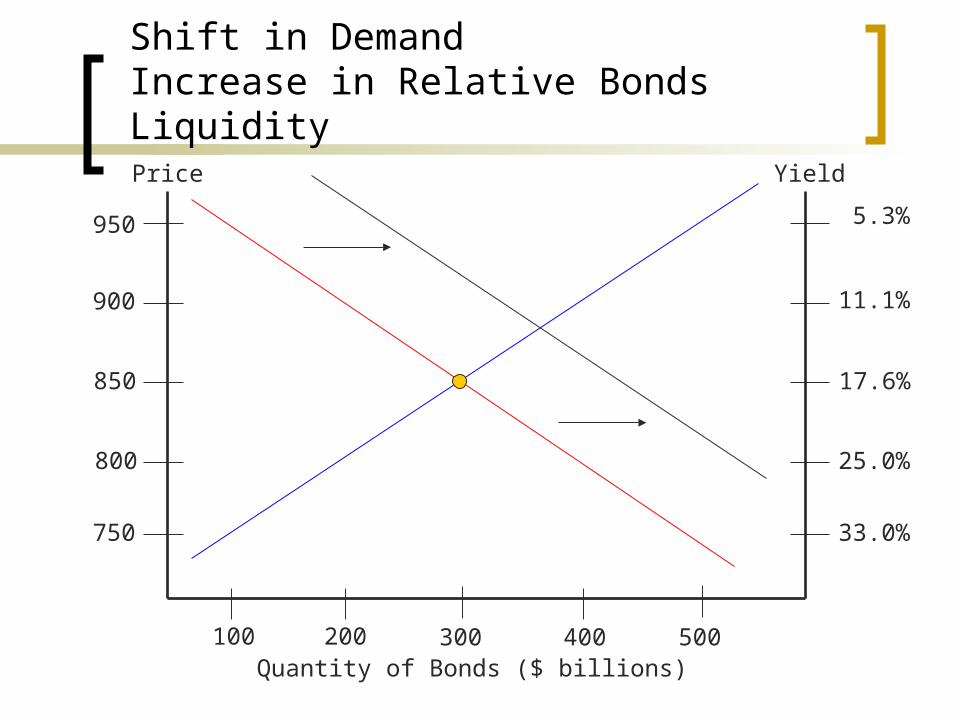

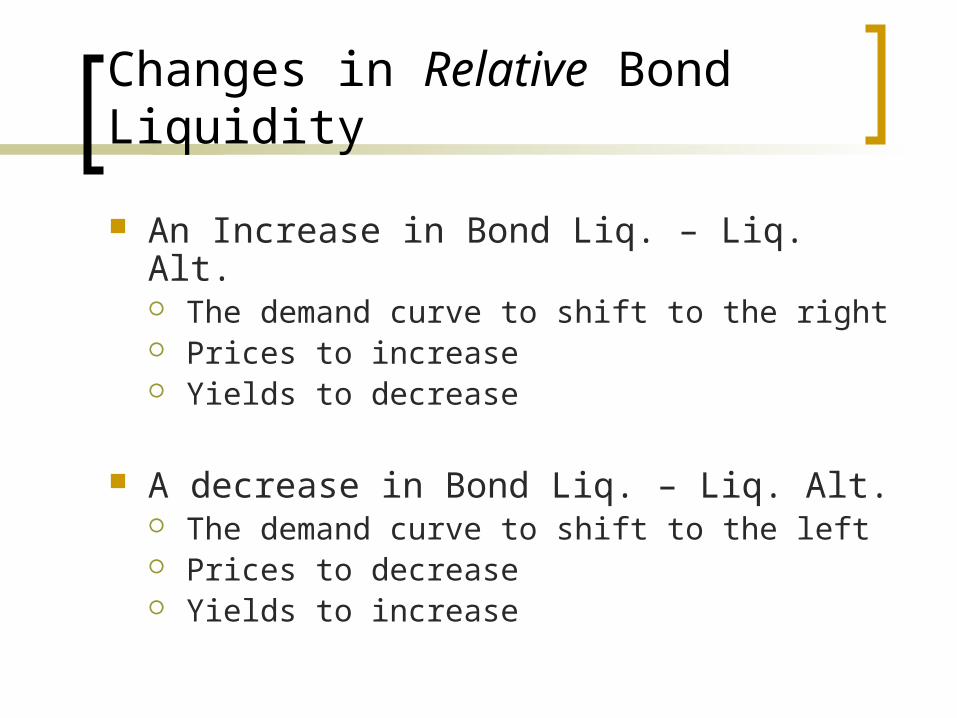

Shift in DemandIncrease in Relative Bonds Liquidity

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Changes in Relative Bond Liquidity

An Increase in Bond Liq. – Liq. Alt. The demand curve to shift to the right Prices to increase Yields to decrease

A decrease in Bond Liq. – Liq. Alt. The demand curve to shift to the left Prices to decrease Yields to increase

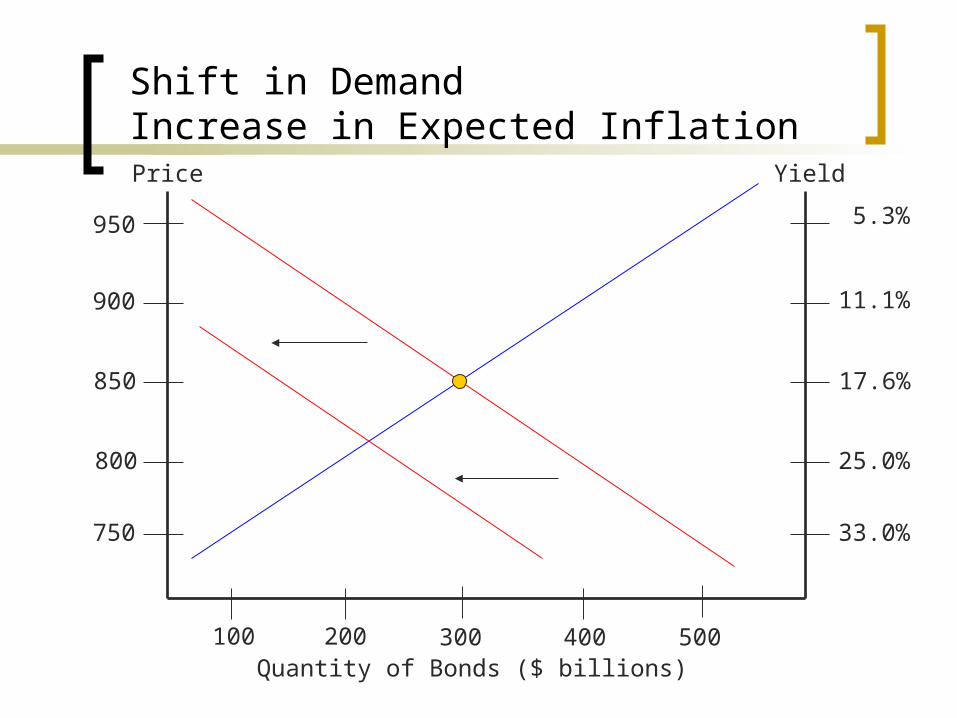

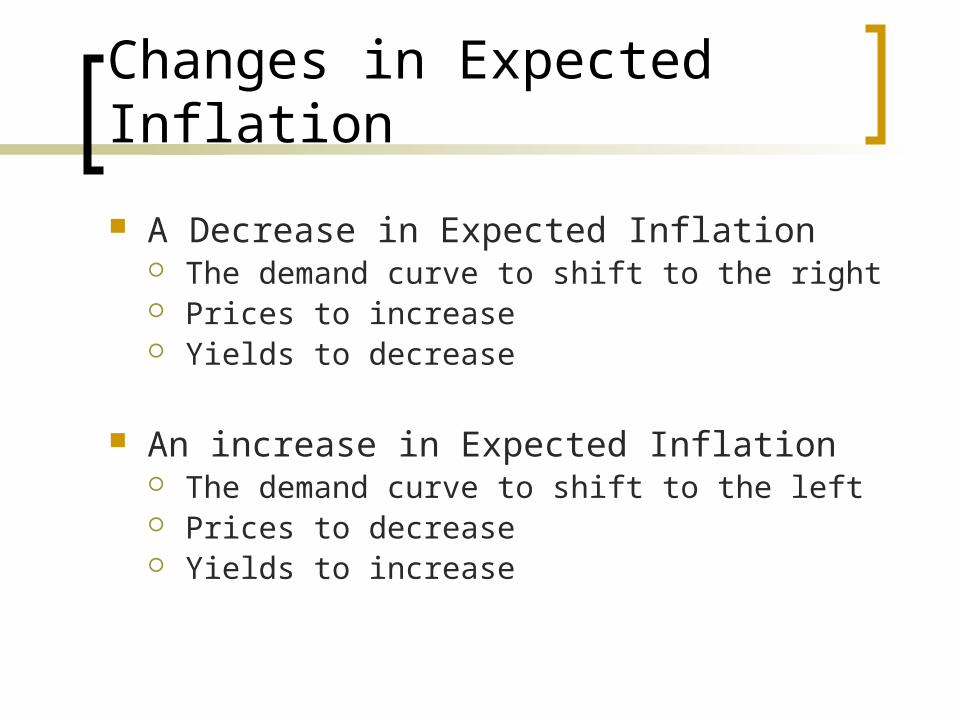

Shift in DemandIncrease in Expected Inflation

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Changes in Expected Inflation

A Decrease in Expected Inflation The demand curve to shift to the right Prices to increase Yields to decrease

An increase in Expected Inflation The demand curve to shift to the left Prices to decrease Yields to increase

Expected Inflation

Expected inflation shifts both curves

Consider a decrease in expected inflation

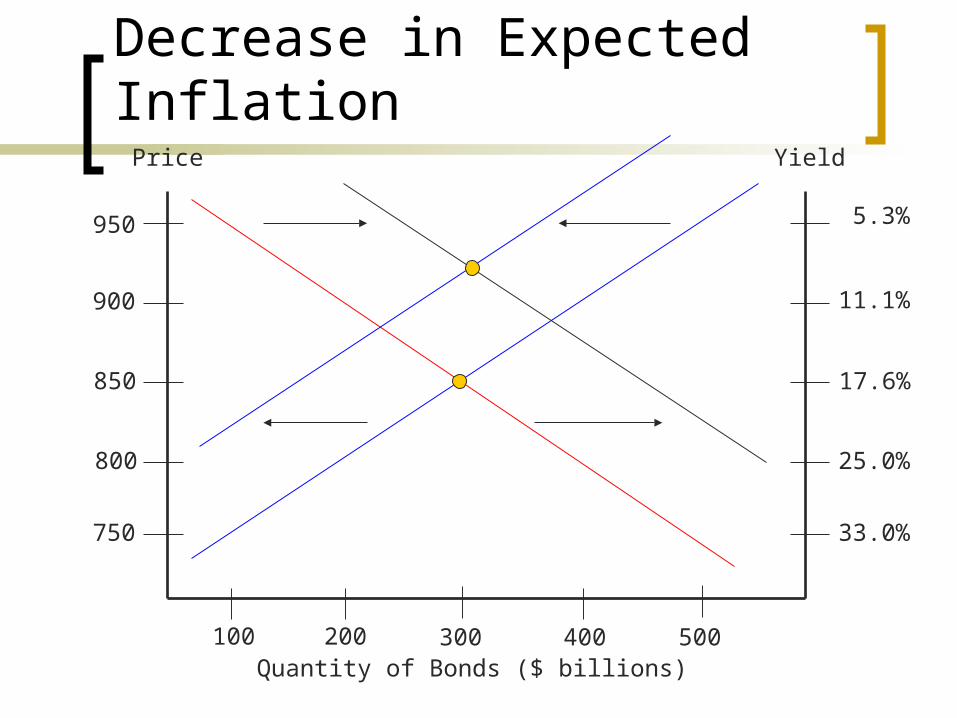

Decrease in Expected Inflation

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Decrease in Expected Inflation

A decrease in expected inflation unambiguously causes bond prices to rise and yields to fall.

Business Cycles

Business Cycles can shift both curves

Consider what happens when economy emerges from a recession.

Jobs are created, household wealth increases Business conditions improve

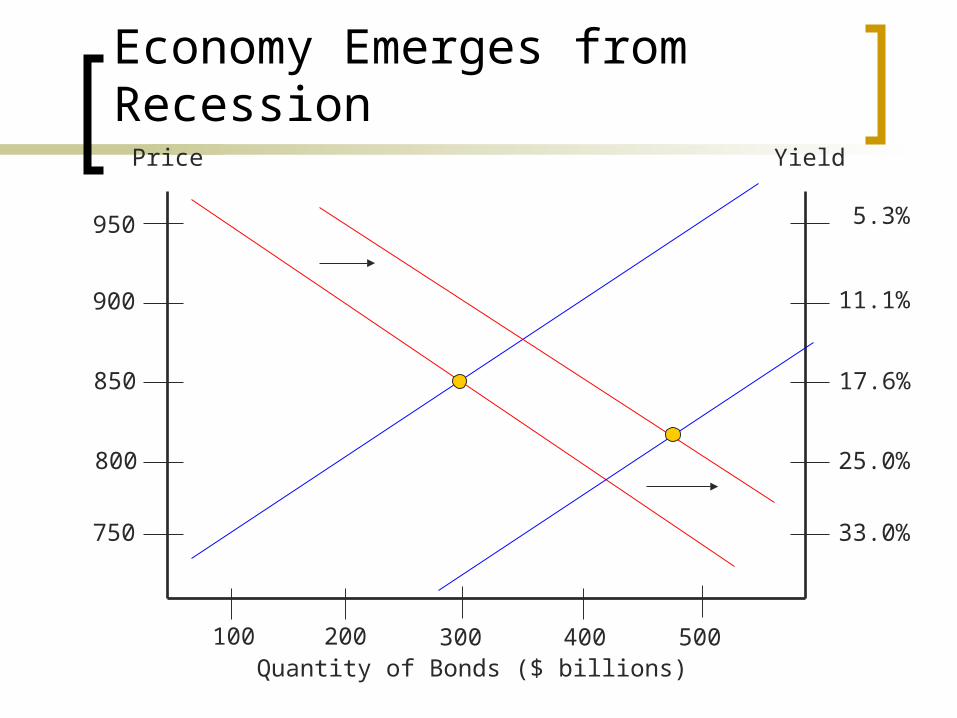

Economy Emerges from Recession

Quantity of Bonds ($ billions)

Price

950 5.3%

Yield

300

900

850

800

750

200100 400 500

11.1%

17.6%

25.0%

33.0%

Economy Emerges from Recession

During expansions Wealth increases (demand shifts right) Business Conditions improve (supply shifts

right)

Effect could be ambiguous Data shows during expansions

Bond prices decline, yields increase

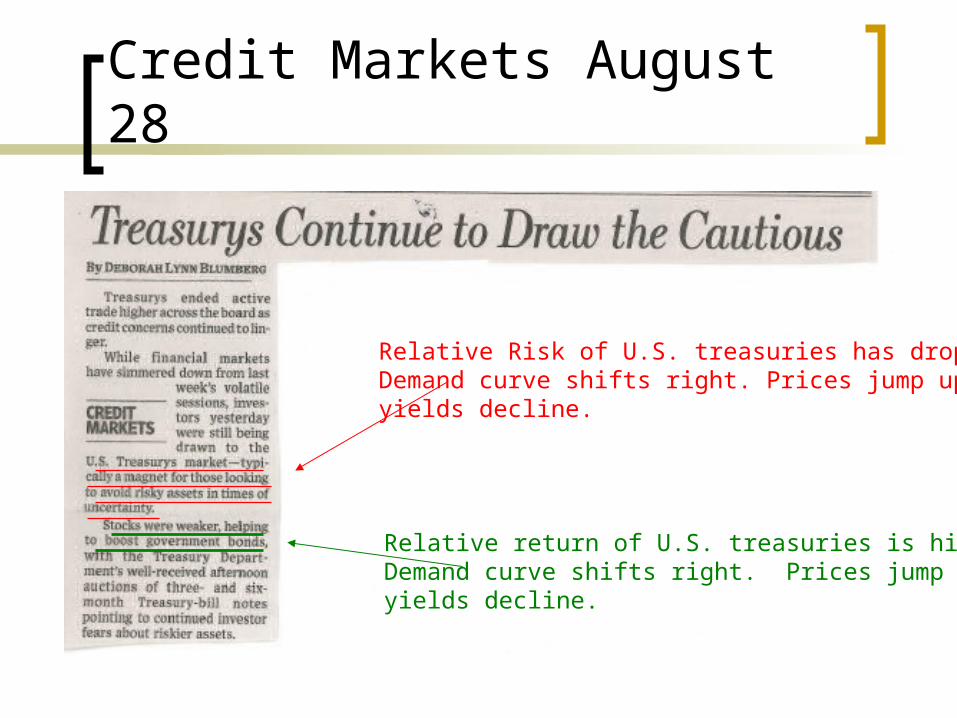

Credit Markets August 28

Relative Risk of U.S. treasuries has dropped.Demand curve shifts right. Prices jump up,yields decline.

Relative return of U.S. treasuries is higher.Demand curve shifts right. Prices jump up,yields decline.

Credit Markets July 2Softer inflation causes demand curve toshift right, supply curve to shift left. Botheffects cause prices to increase, yieldsto decrease.