CHAPTER 16leeds-courses.colorado.edu/.../FNCE4030-Fall-2014-ch16-handout.pdfCHAPTER 16 Managing Bond...

49

INVESTMENTS | BODIE, KANE, MARCUS Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin CHAPTER 16 Managing Bond Portfolios

-

Upload

hoangtuyen -

Category

Documents

-

view

230 -

download

1

Transcript of CHAPTER 16leeds-courses.colorado.edu/.../FNCE4030-Fall-2014-ch16-handout.pdfCHAPTER 16 Managing Bond...

INVESTMENTS | BODIE, KANE, MARCUS

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

CHAPTER 16

Managing Bond Portfolios

INVESTMENTS | BODIE, KANE, MARCUS

Bond Pricing Relationships

• Bond prices and yields are inversely related.

• An increase in a bond’s yield to maturity results in a smaller price change than a decrease of equal magnitude.

• Long-term bonds tend to be more price sensitive than short-term bonds, but price sensitivity increases at a decreasing rate.

• Interest rate risk is higher for lower bond’s coupon rates.

• Price sensitivity is inversely related to the bond’s yield to maturity.

16-2

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

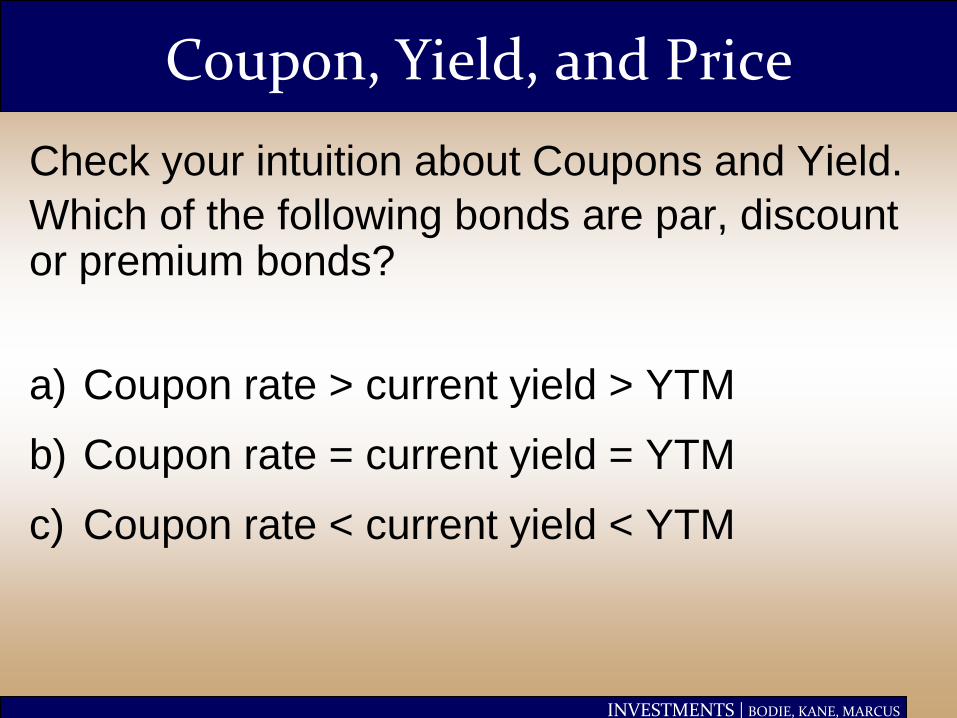

Coupon, Yield, and Price

Check your intuition about Coupons and Yield.

Which of the following bonds are par, discount or premium bonds?

a) Coupon rate > current yield > YTM

b) Coupon rate = current yield = YTM

c) Coupon rate < current yield < YTM

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

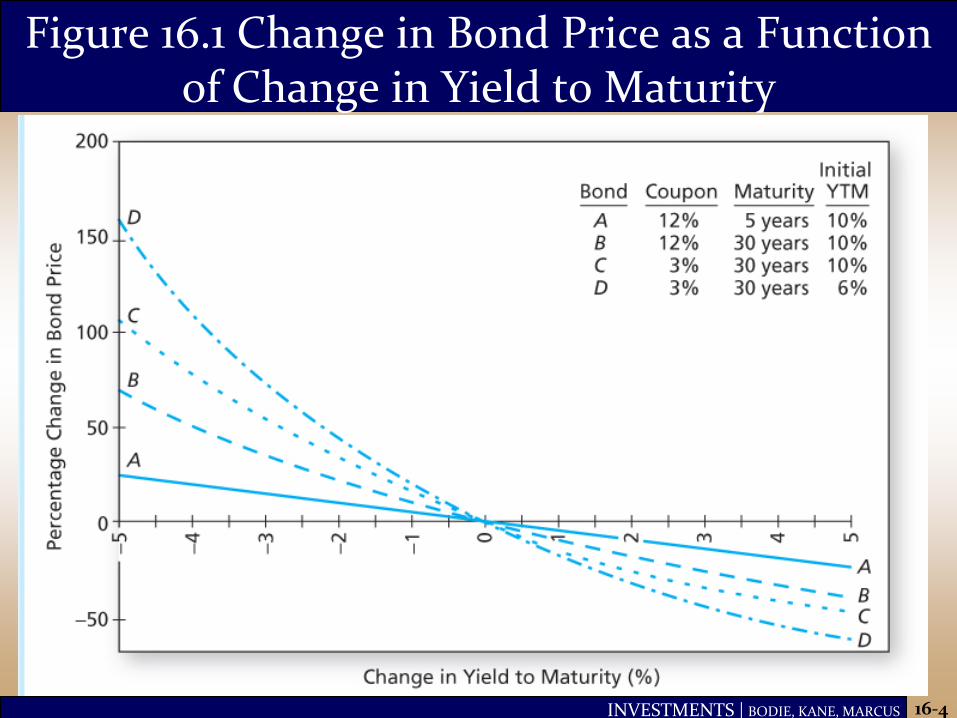

Figure 16.1 Change in Bond Price as a Function of Change in Yield to Maturity

16-4

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Table 16.1,2 Prices of 8% semiannual coupon bond, and a Zero Coupon Bond

16-5

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Duration and effective life

• A measure of the effective maturity of a bond

• The weighted average of the times until each payment is received; weights are proportional to the present value of the payment

• Duration is obviously equal to maturity for zero coupon bonds (one cash flow only!)

• Duration is shorter than maturity for all bonds, except zero coupon bonds

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

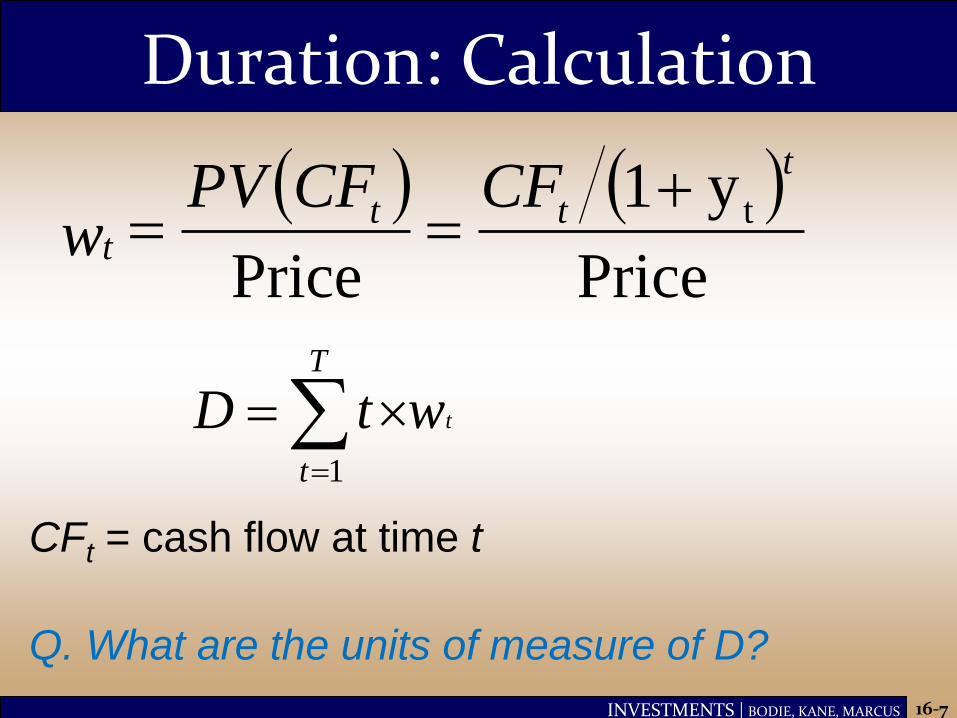

Duration: Calculation

CFt = cash flow at time t

Q. What are the units of measure of D?

16-7

twtDT

t

1

Price

y1

Price

t

t

ttt

CFCFPVw

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

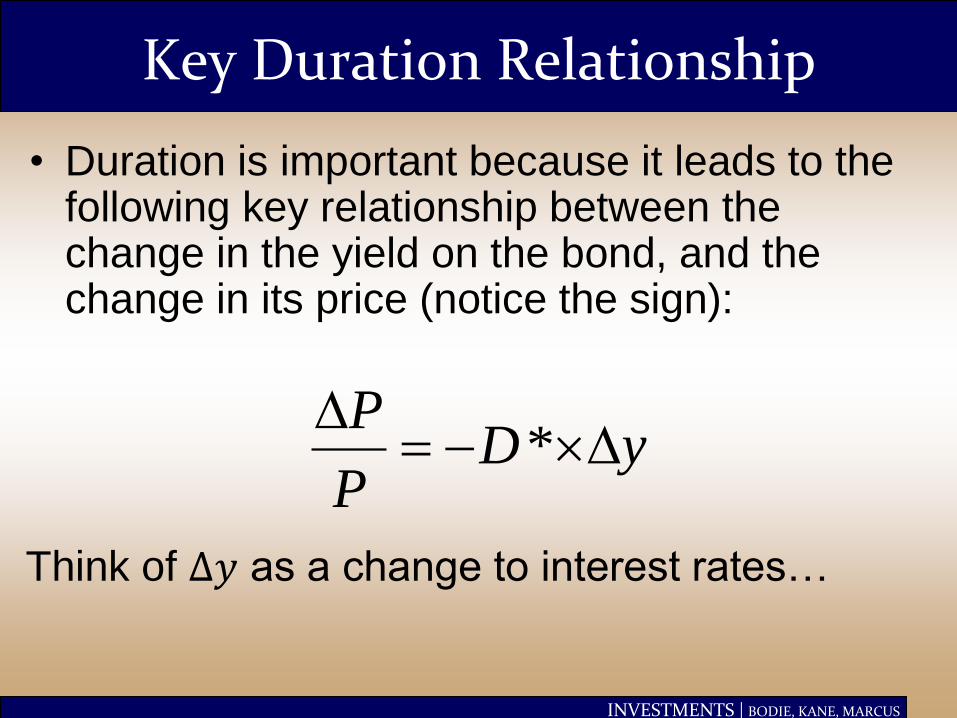

Key Duration Relationship

• Duration is important because it leads to the following key relationship between the change in the yield on the bond, and the change in its price (notice the sign):

yDP

P

*

Think of Δ𝑦 as a change to interest rates…

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Duration/Price Relationship - Derivation

Compute price sensitivity w.r.t. yield y:

1

𝑃 𝜕𝑃

𝜕𝑦=1

𝑃 𝜕

𝜕𝑦

𝐶𝑡1 + 𝑦 𝑡𝑡

=1

𝑃

−𝑡 × 𝐶𝑡1 + 𝑦 𝑡+1𝑡

= −1

𝑃 𝑡 × 𝐶𝑡1 + 𝑦 𝑡𝑡

×1

1 + 𝑦

= − 𝐷 ×1

1 + 𝑦

16-9

= −𝐷∗

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Duration/Price Relationship

Price change is proportional to duration (not to maturity). Notice the sign.

16-10

D* = modified duration = D/(1 + 𝑦)

[note: Δ(1 + 𝑦) = Δ𝑦]

Therefore:

)1(

)1(

y

yD

P

P

yDP

P

*

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Modified Duration

• When the yield y is expressed with compounding m times per year

my

yDPP

1

D

y m1

• The modified duration becomes:

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

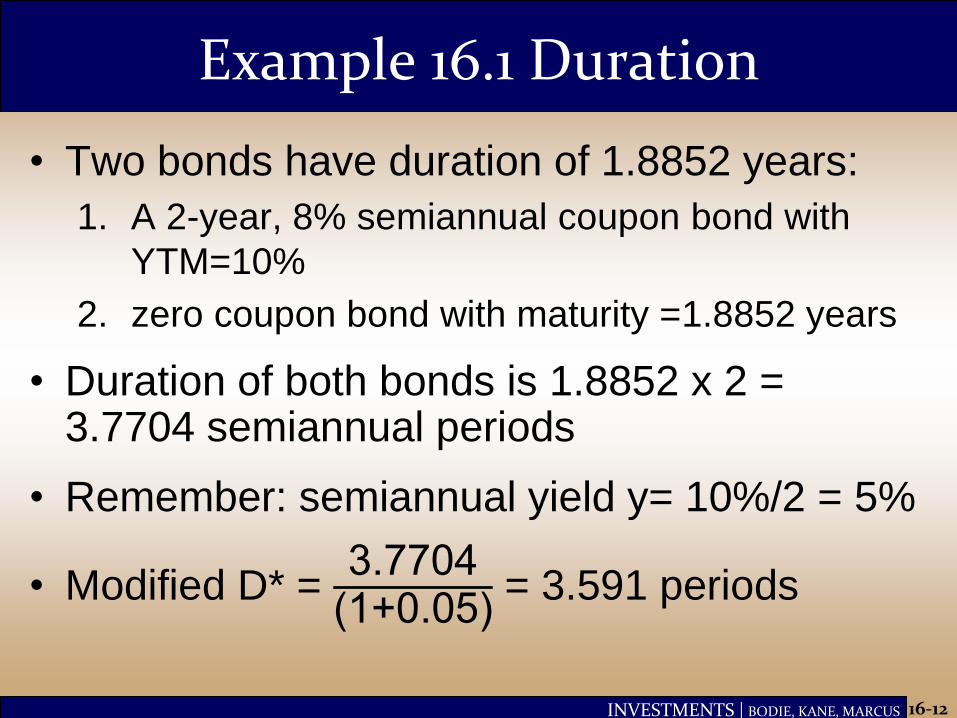

Example 16.1 Duration

• Two bonds have duration of 1.8852 years:

1. A 2-year, 8% semiannual coupon bond with

YTM=10%

2. zero coupon bond with maturity =1.8852 years

• Duration of both bonds is 1.8852 x 2 = 3.7704 semiannual periods

• Remember: semiannual yield y= 10%/2 = 5%

• Modified D* = 3.7704

(1+0.05) = 3.591 periods

16-12

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Example 16.1 Duration

• Suppose the semiannual interest rate increases by 0.01%. Bond prices fall by:

16-13

yDP

P

*

• Δ𝑃/𝑃 = -3.591 x 0.01% = -0.03591%

• Bonds with equal D have the same

interest rate sensitivity

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Example 16.1 Duration

Coupon Bond

• The coupon bond,

initially sells at

$964.540

• it falls to $964.1942

when its yield

increases to 5.01%

• Percentage decline is

0.0359%

Zero coupon bond

• The zero-coupon bond

initially sells for

$1,000/(1.05)3.7704 =

= $831.9704

• At higher yield, it sells

for $1,000/(1.05)3.7704 =

= $831.6717

• This price also falls by

0.0359%

16-14

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Duration of a Portfolio

• The duration for a portfolio is the weighted average duration of the instruments in the portfolio with weights proportional to PVs

• The key duration relationship for a portfolio describes the effect of small parallel shifts in the yield curve

• What exposures remain if the duration of the portfolio assets equals the duration of the portfolio liabilities?

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Duration – Check your intuition

How does each of these changes affect duration?

• Having no coupon payments

• Decreasing the coupon rate

• Increasing the time to maturity

• Decreasing the yield-to-maturity

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Pictorial look at duration

• Cash flows of a 7 year par 12% bond

• Shaded area of each box is PV of cash flow

• Duration, measured as time, is the position of the center of mass of the shaded areas

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Lower Coupon

• Duration is similar to the distance to the fulcrum

• Lower coupons shift the center of mass to the right. Higher coupons shift the center of mass to the left

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

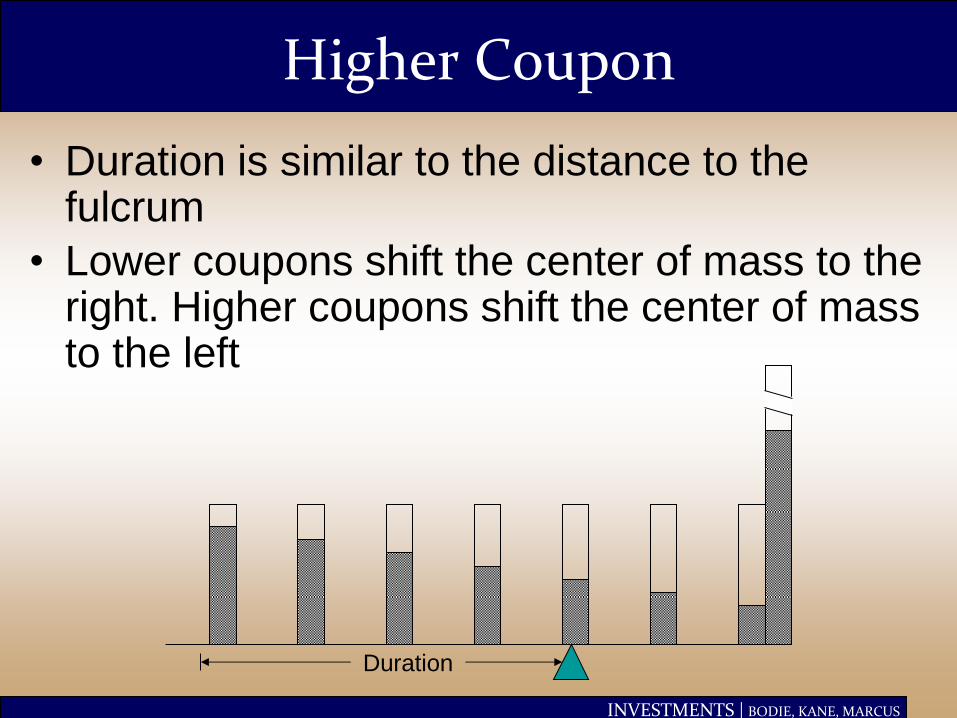

Higher Coupon

• Duration is similar to the distance to the fulcrum

• Lower coupons shift the center of mass to the right. Higher coupons shift the center of mass to the left

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Example of the coupon effect

• Consider the durations of a 5-year and 20-year bond with varying coupon rates (semi-annual coupon payments):

5 year bond 20 year bond

Zero coupon 5 20

6% coupon 4.39 11.90

9% coupon 4.19 10.98

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Effect of maturity on duration

• Duration increases with increased maturity

• Example: add one period

Duration

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

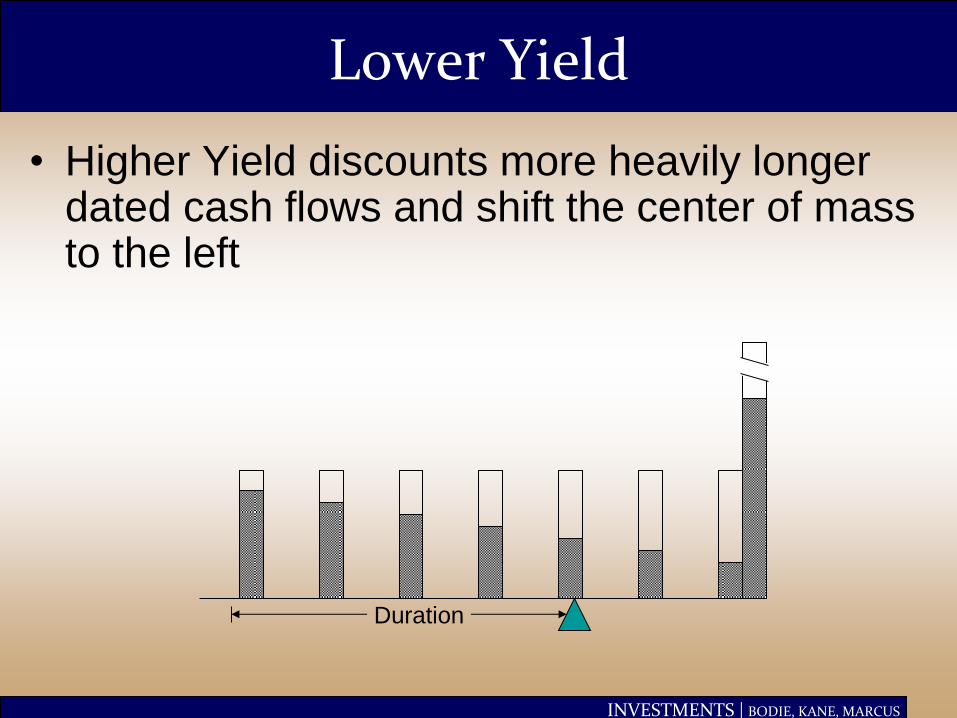

Lower Yield

• Higher Yield discounts more heavily longer dated cash flows and shift the center of mass to the left

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

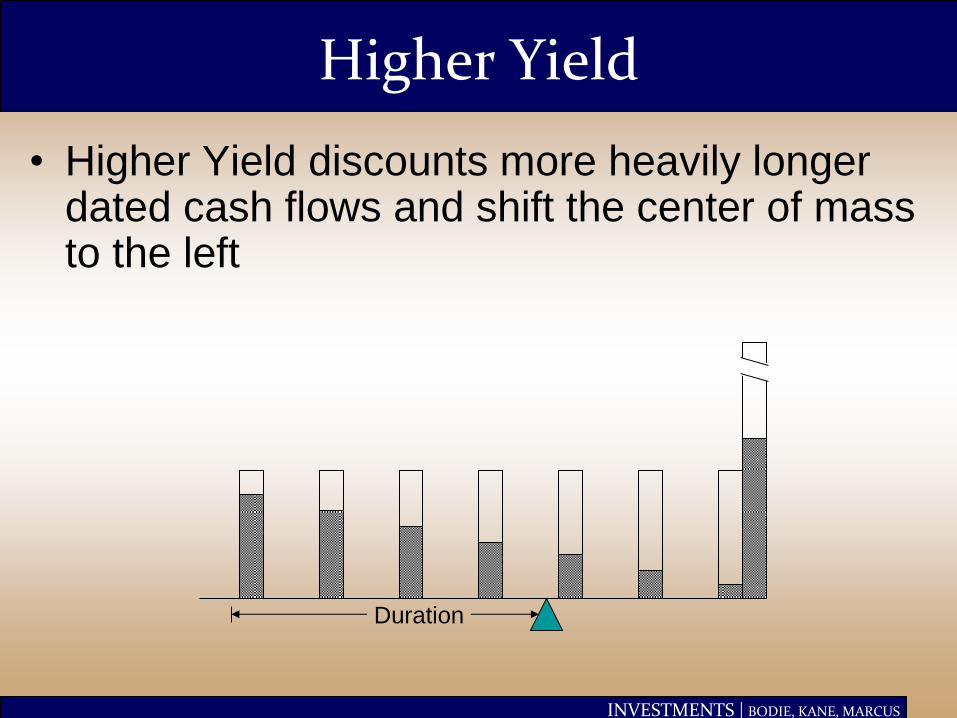

Higher Yield

• Higher Yield discounts more heavily longer dated cash flows and shift the center of mass to the left

Duration

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

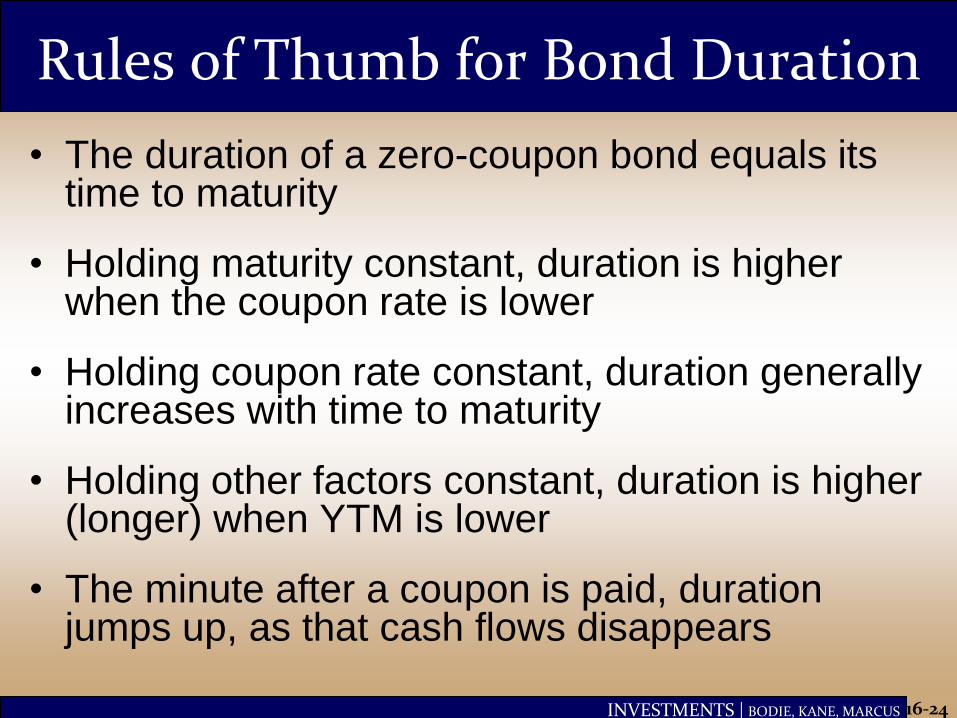

Rules of Thumb for Bond Duration

• The duration of a zero-coupon bond equals its time to maturity

• Holding maturity constant, duration is higher when the coupon rate is lower

• Holding coupon rate constant, duration generally increases with time to maturity

• Holding other factors constant, duration is higher (longer) when YTM is lower

• The minute after a coupon is paid, duration jumps up, as that cash flows disappears

16-24

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS 16-25

Figure 16.2 Bond Duration versus Bond Maturity

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

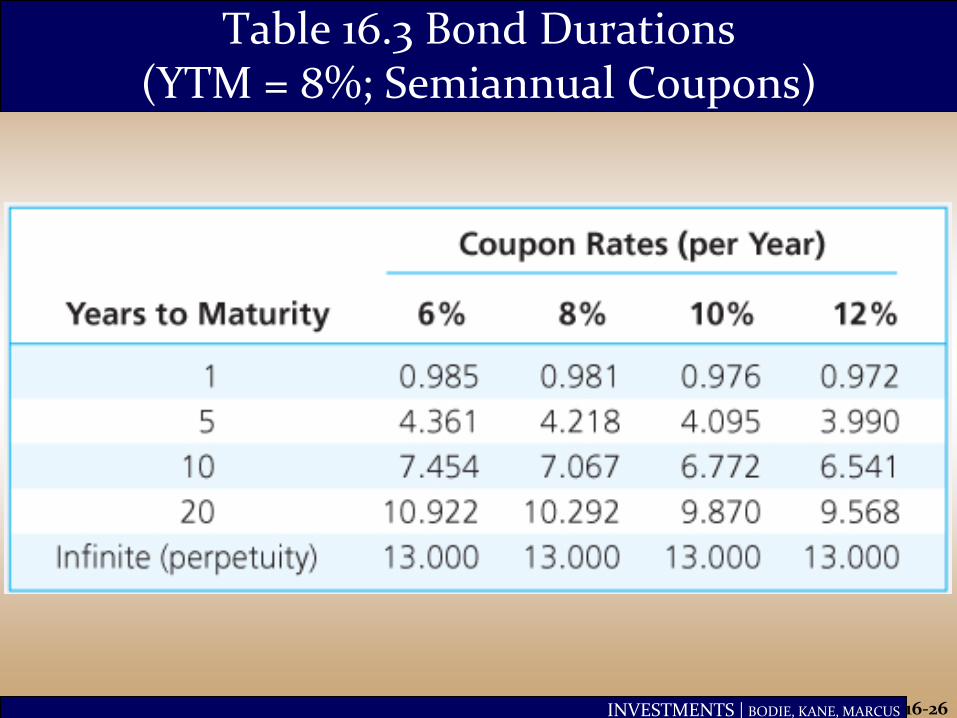

Table 16.3 Bond Durations (YTM = 8%; Semiannual Coupons)

16-26

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Industry calc. of Rate Sensitivity: dv01

• Traders in practice use dv01: dollar value of 1bp increase in rates

• Shock interest rates by +1bp and compute dollar impact dv01

• Also compute bucketed dv01 by shocking interest rates by 1bp at various tenor buckets, and then compute dollar impact

16-27

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

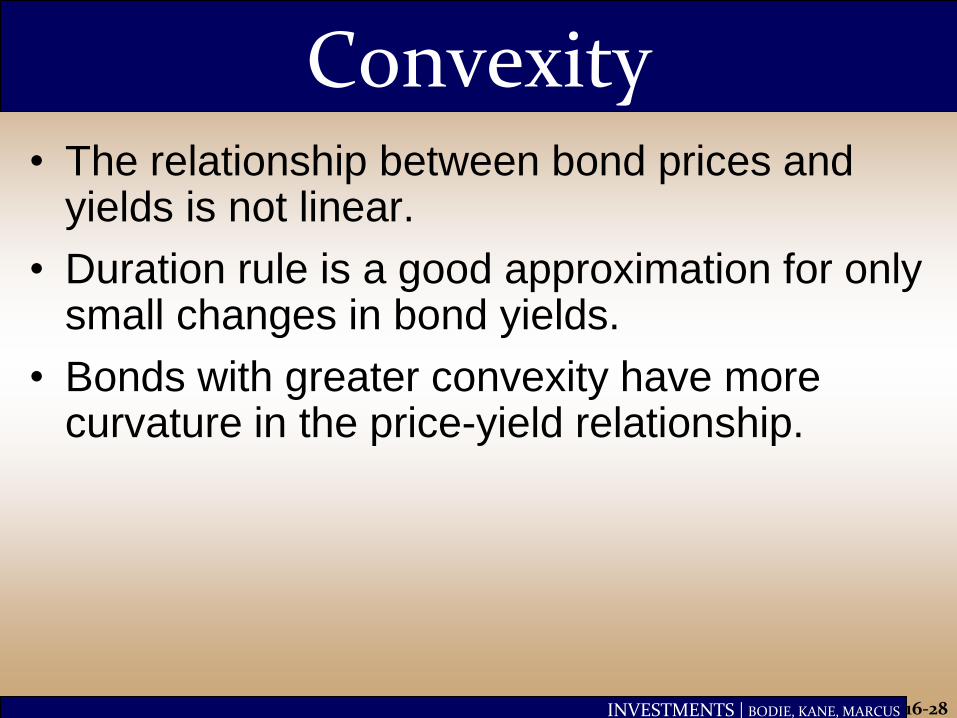

Convexity • The relationship between bond prices and

yields is not linear.

• Duration rule is a good approximation for only small changes in bond yields.

• Bonds with greater convexity have more curvature in the price-yield relationship.

16-28

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Figure 16.3 Bond Price Convexity: 30-Year Maturity, 8% Coupon; Initial YTM = 8%

16-29

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

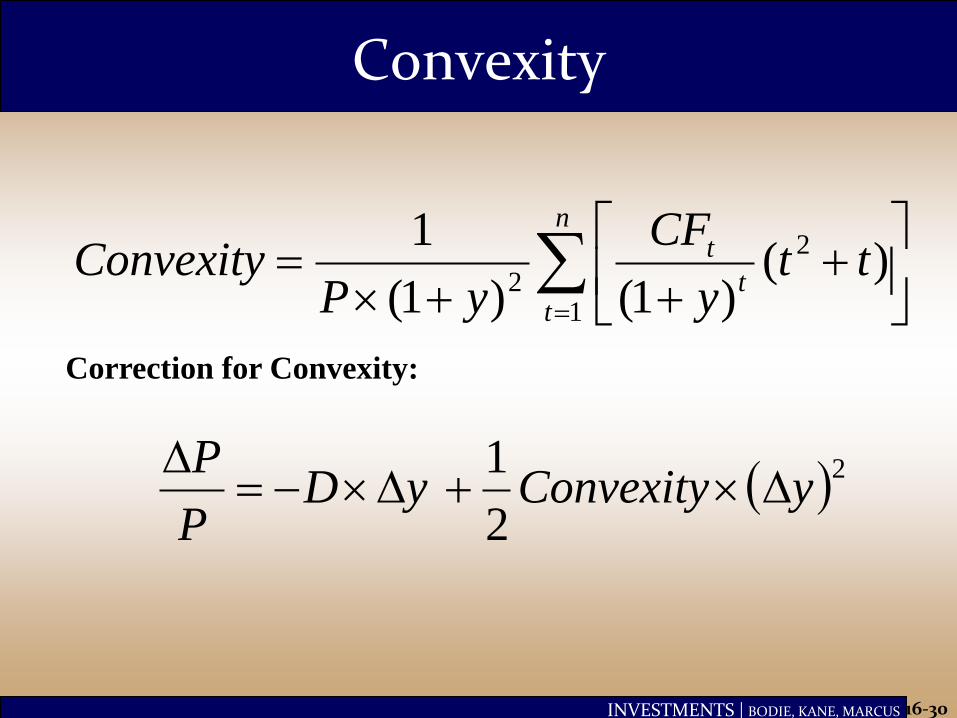

Convexity

16-30

n

tt

t tty

CF

yPConvexity

1

2

2)(

)1()1(

1

Correction for Convexity:

yDP

P

2

2

1yConvexity

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Figure 16.4 Convexity of Two Bonds

16-31

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

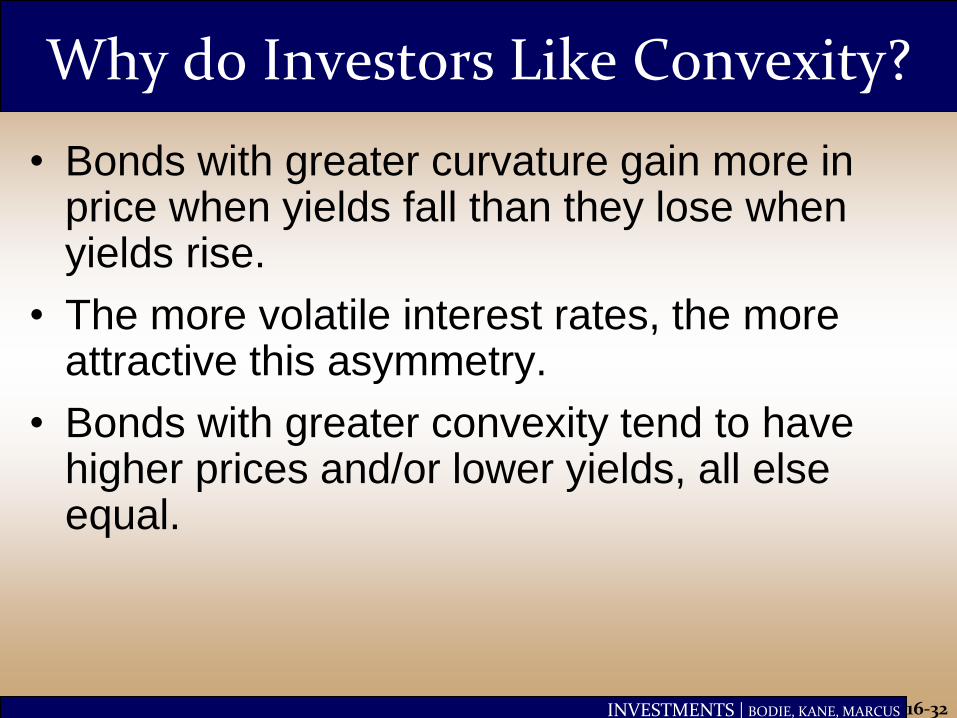

Why do Investors Like Convexity?

• Bonds with greater curvature gain more in price when yields fall than they lose when yields rise.

• The more volatile interest rates, the more attractive this asymmetry.

• Bonds with greater convexity tend to have higher prices and/or lower yields, all else equal.

16-32

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

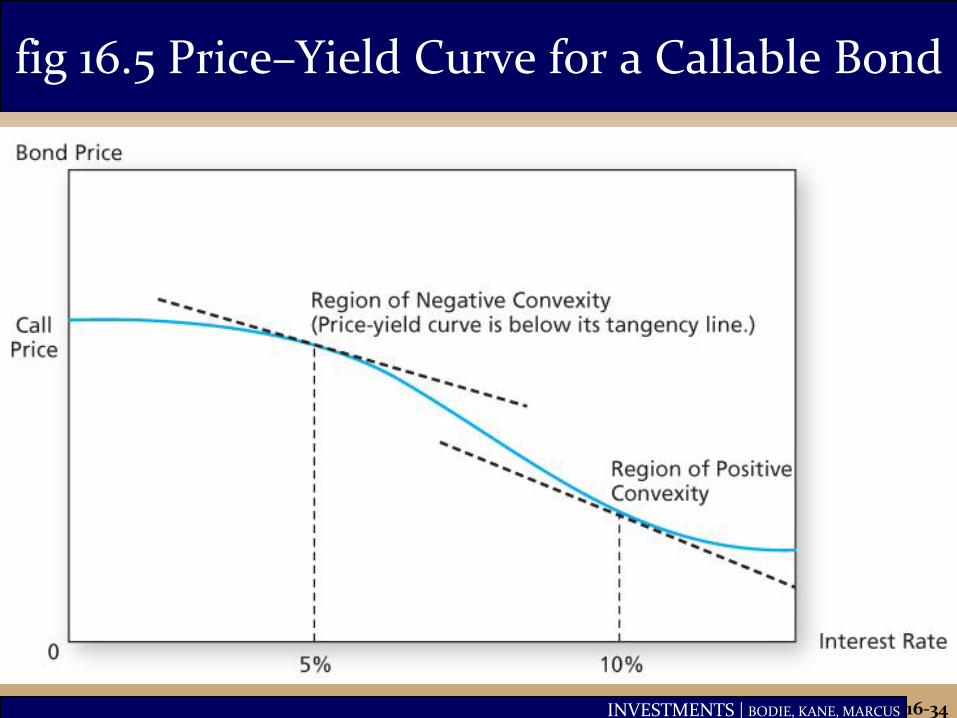

Callable Bonds

• As rates fall, there is a ceiling on the bond’s market price, which cannot rise above the call price.

• Negative convexity

• Use effective duration:

16-33

/Effective Duration =

P P

r

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS 16-34

fig 16.5 Price–Yield Curve for a Callable Bond

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

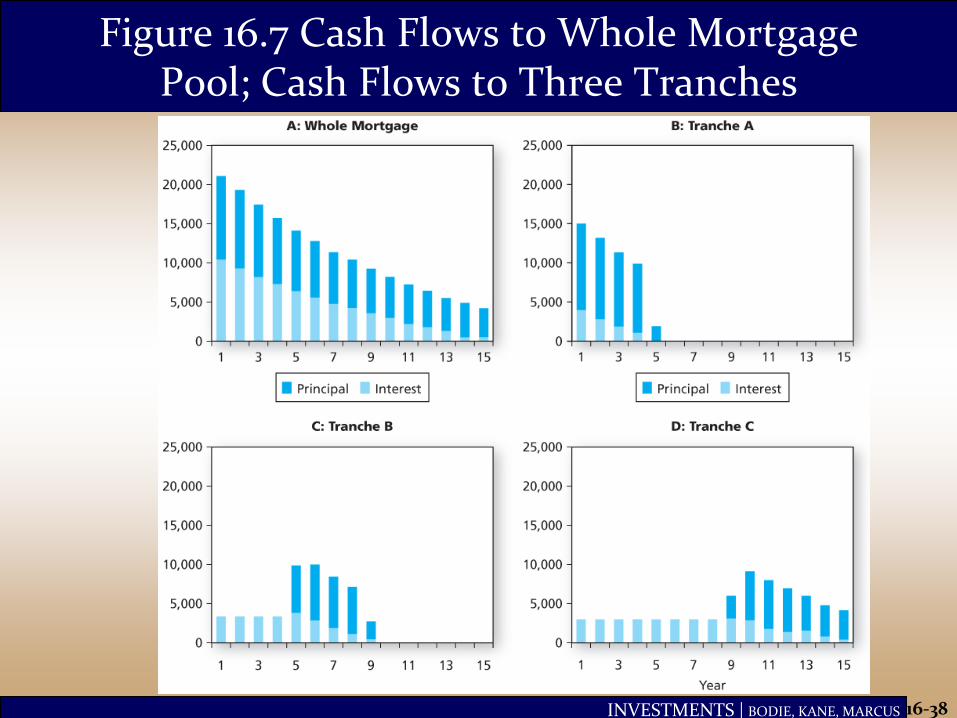

Mortgage-Backed Securities

• The number of outstanding callable corporate bonds has declined, but the MBS market has grown rapidly

• MBS are based on a portfolio of callable amortizing loans – Homeowners have the right to repay their loans

at any time

– MBS have negative convexity

16-35

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Mortgage-Backed Securities

• Often sell for more than their principal balance

• Homeowners do not refinance as soon as rates drop, so implicit call price is not quite a firm ceiling on MBS value

• Tranches – the underlying mortgage pool is divided into a set of derivative securities

16-36

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS 16-37

Figure 16.6 Price-Yield Curve for a Mortgage-Backed Security

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS 16-38

Figure 16.7 Cash Flows to Whole Mortgage Pool; Cash Flows to Three Tranches

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Passive Management

• Two passive bond portfolio strategies:

• Indexing

• Immunization

• Both strategies see market prices as being correct, but the strategies have very different risks.

16-39

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Bond Index Funds

• Bond indices contain thousands of issues, many of which are traded infrequently

• Bond indices turn over more than stock indices as the bonds mature

• Therefore, bond index funds hold only a representative sample of the bonds in the actual index

16-40

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

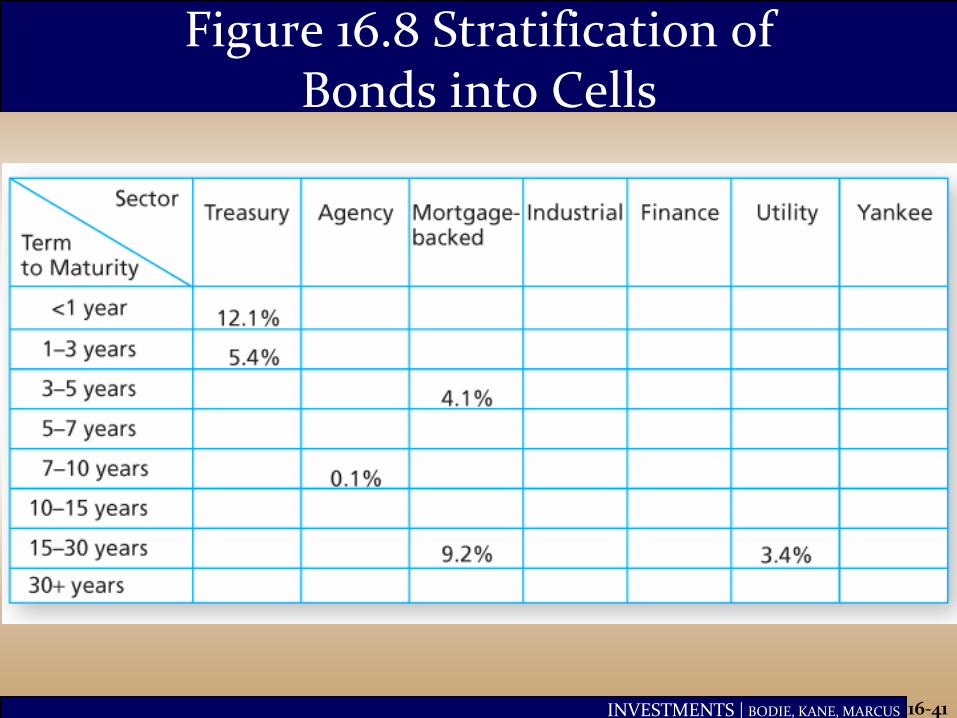

Figure 16.8 Stratification of Bonds into Cells

16-41

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Immunization

• Immunization is a way to mitigate interest rate risk

• Widely used by pension funds, insurance companies, and banks

• Requires deep understanding of duration and convexity of your portfolio

16-42

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Immunization

• Immunize a portfolio by matching the interest rate exposure of assets and liabilities – Match the duration of the assets and liabilities

– Price risk and reinvestment rate risk cancel out

for small interest rate movements

• Result: Value of assets will track the value of liabilities whether rates rise or fall (for small movements, need to rebalance)

16-43

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

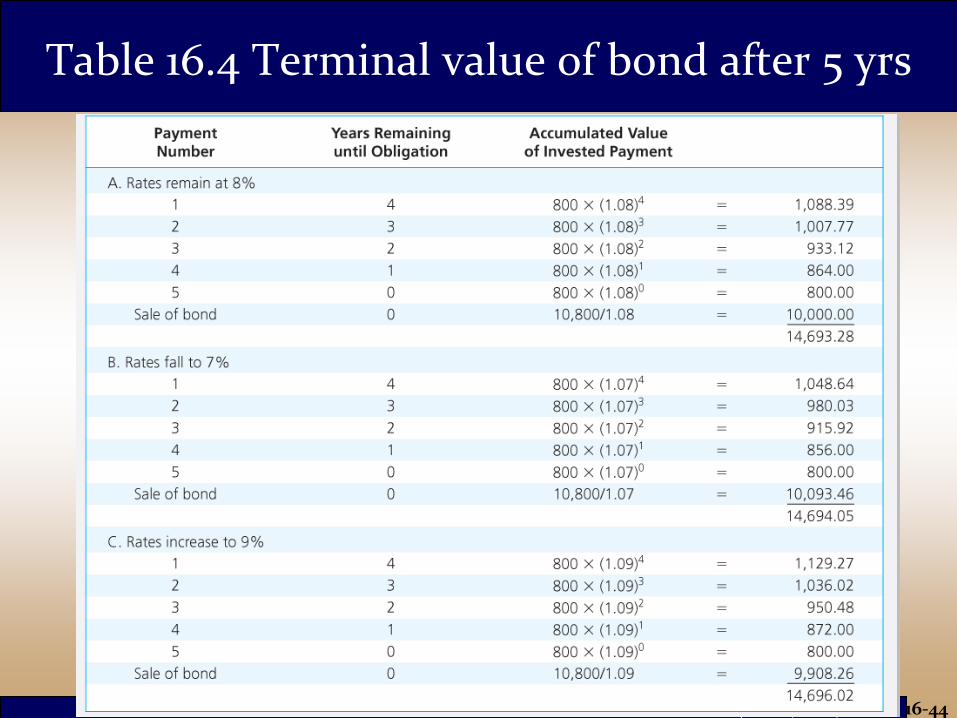

Table 16.4 Terminal value of bond after 5 yrs

16-44

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Table 16.5 Market Value Balance Sheet

16-45

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Figure 16.10 Immunization

16-46

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Cash Flow Matching and Dedication

• Cash flow matching = automatic immunization

• Cash flow matching is a dedication strategy

• Not widely used because of constraints associated with bond choices

16-47

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Active Management: Swapping Strategies

• Substitution swap

• Intermarket swap

• Rate anticipation swap

• Pure yield pickup

• Tax swap

16-48

RESET STYLE

INVESTMENTS | BODIE, KANE, MARCUS

Horizon Analysis

• Select a particular holding period and predict the yield curve at end of period

• Given a bond’s time to maturity at the end of the holding period, its yield can be read from the predicted yield curve and the end-of-period price can be calculated

16-49

RESET STYLE