Chapter 15 Investing in Bonds McGraw-Hill/Irwin Copyright © 2007 by The McGraw-Hill Companies, Inc....

22

Chapter 15 Investing in Bonds McGraw-Hill/Irwin Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

-

Upload

ambrose-jordan -

Category

Documents

-

view

216 -

download

1

Transcript of Chapter 15 Investing in Bonds McGraw-Hill/Irwin Copyright © 2007 by The McGraw-Hill Companies, Inc....

Chapter 15

Investing in BondsInvesting in Bonds

McGraw-Hill/Irwin Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

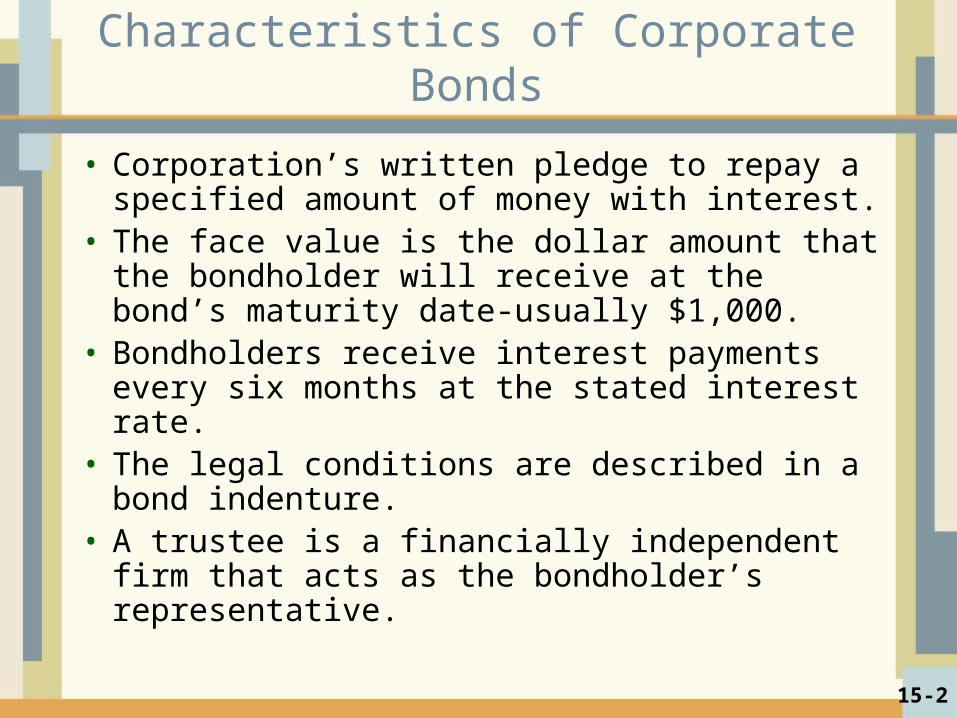

Characteristics of Corporate Bonds

• Corporation’s written pledge to repay a specified amount of money with interest.

• The face value is the dollar amount that the bondholder will receive at the bond’s maturity date-usually $1,000.

• Bondholders receive interest payments every six months at the stated interest rate.

• The legal conditions are described in a bond indenture.

• A trustee is a financially independent firm that acts as the bondholder’s representative.

15-2

Why Corporations Sell Bonds

• To get funds for major purchases.

• To fund ongoing business activities.

• When it is difficult or impossible to sell stock.

• To improve financial leverage.

• Interest paid to bondholders is a tax deductible business expense that can be used to reduce the federal and state taxes corporations must pay.

15-3

Four Types of Corporate Bonds

Debenture bond. Most corporate bonds are debenture bonds. Unsecured - Backed only by the reputation of

the issuing company.

Mortgage bond. A corporate bond that is secured by various

assets of the issuing firm, usually real estate. Interest rate is lower because it is secured.

15-4

Types of Corporate Bonds

Subordinated debenture bond. An unsecured bond that gives bondholders a

claim secondary to that of other designated bond holders with respect to interest payments and claim on assets.

Convertible bond. A special kind of corporate bond that can be

exchanged, at the owner’s option, for a specified number of shares of the corporation’s common stock.

(continued)

15-5

Call Feature of Corporate Bonds

• Corporation can call in or buy back outstanding bonds from current bondholders before the maturity date.

• Most agree not to call bonds for the first 5 to 10 years after they are issued.

• Bonds called if their interest rate is much higher than the going rate.

• Most corporate bonds are callable.

15-6

Provisions For Repayment of Bonds

• Sinking fund. Corporations deposit money in this fund

annually or semiannually and use the money to pay off the bondholders when the bond issue comes due.

• Serial bonds. Bonds of a single issue that mature on different

dates.

15-7

Why Investors Buy Corporate Bonds

• For interest income. Investors know the interest rate. Interest will be paid to investors twice a year,

with the payment based on the interest rate and the face value of the bond.

• Appreciation of bond value. May be able to sell a bond with a fixed

interest rate to someone else at a higher price if overall interest rates fall.

• Bond face amount will be repaid at maturity.

15-8

Bond Registration

• Registered bond: Registered in your name by the company who issued it. Interest checks will be mailed directly to you.

• A bearer bond is not registered in your name. Also has detachable coupons. No longer issued by U.S. corporations.

• Zero coupon bonds: Sold for below face value; it pays no interest; redeem it for face value at maturity. Interest is taxed as you earn it.

15-9

Other Bond Information

• Can hold bond until maturity or sell it in the secondary market.

• Success or failure of the business and changes in market interest rates will affect the price of the bond.

• Interest and capital gains from selling bonds are both taxable.

15-10

Government Bonds and Debt Securities

• Sold to obtain money to finance the national debt, and the ongoing costs of government.

• Three levels of government issue bonds: Federal-no state income tax on the interest. State. Local municipalities.

15-11

U.S. Government Treasury Bills and Notes

Treasury Bills (T-Bills).• $1,000 minimum.• 4, 13, or 26 weeks to mature.• Sold at a discount.Treasury Notes (T-Notes).• $1,000 units.• 2, 3, 5, and 10 year terms.• Interest paid every six months, higher

rates than T-bills.15-12

Why Do Investors Buy Government Bonds?

• Pay a lower interest rate than corporate bond, but virtually risk free if chosen carefully.

• Often used by investors to diversify their investment holdings.

15-13

Federal Agency Debt Issues

• Fannie Mae (www.fanniemae.com). Federal National Mortgage Association.

• Ginnie Mae - pay interest once a month. Government National Mortgage Association.

• Freddie Mac. Federal Home Loan Mortgage Corporation.

• Slightly higher risk than Treasury securities, so slightly higher interest rates.

• Issued for 1-30 years, 12 year average.

• Minimum may be as high as $25,000.15-14

State and Local Government Securities

• Municipal bonds or munis.• Issued by a state or local government, such

as cities, counties, school districts.• Use funds for ongoing costs & to build major

projects such as schools, airports, and bridges.

• General obligation bonds are backed by the state or local government that issues them.

• Revenue bonds are repaid from money generated by the project the funds finance, such as a toll bridge.

15-15

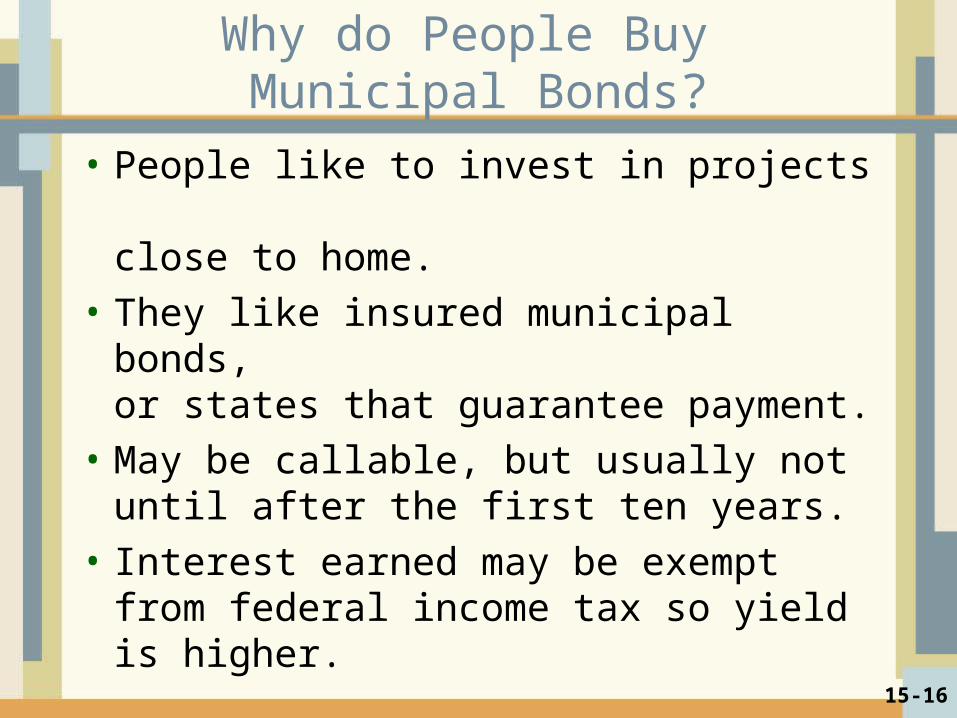

Why do People Buy Municipal Bonds?

• People like to invest in projects close to home.

• They like insured municipal bonds, or states that guarantee payment.

• May be callable, but usually not until after the first ten years.

• Interest earned may be exempt from federal income tax so yield is higher.

15-16

Taxable Equivalent Yield

Tax-exempt yield

1.0 - Your tax rate

Example:

Taxable equivalent yield = 0.06

1.0 - 0.28

= 0.083 = 8.3%

15-17

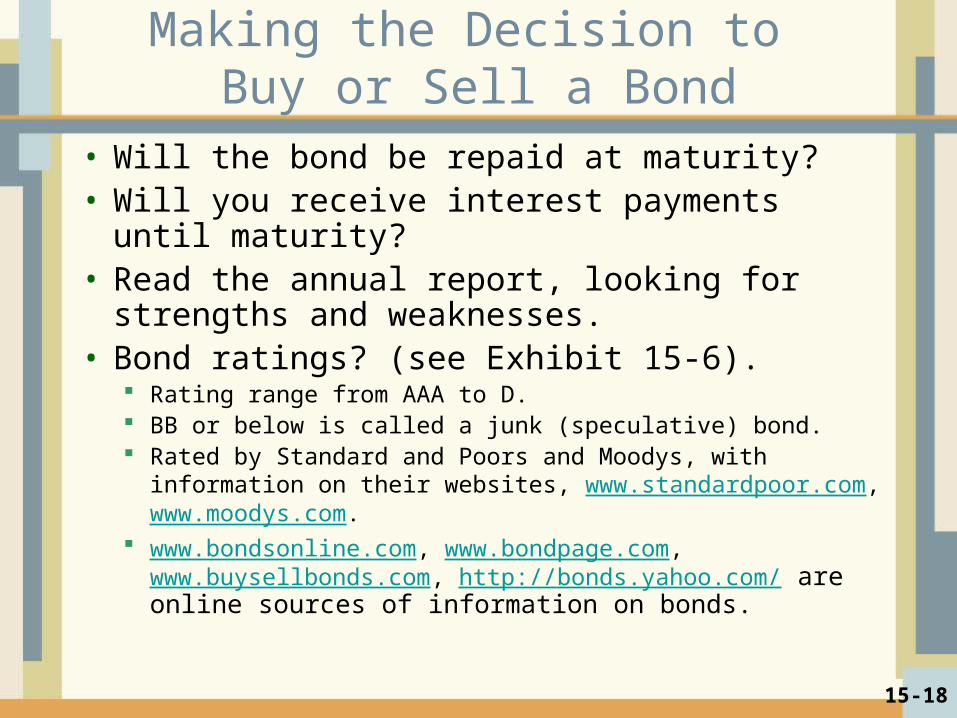

Making the Decision to Buy or Sell a Bond

• Will the bond be repaid at maturity?• Will you receive interest payments until

maturity?• Read the annual report, looking for strengths

and weaknesses.• Bond ratings? (see Exhibit 15-6).

Rating range from AAA to D. BB or below is called a junk (speculative) bond. Rated by Standard and Poors and Moodys, with information on

their websites, www.standardpoor.com, www.moodys.com. www.bondsonline.com, www.bondpage.com,

www.buysellbonds.com, http://bonds.yahoo.com/ are online sources of information on bonds.

15-18

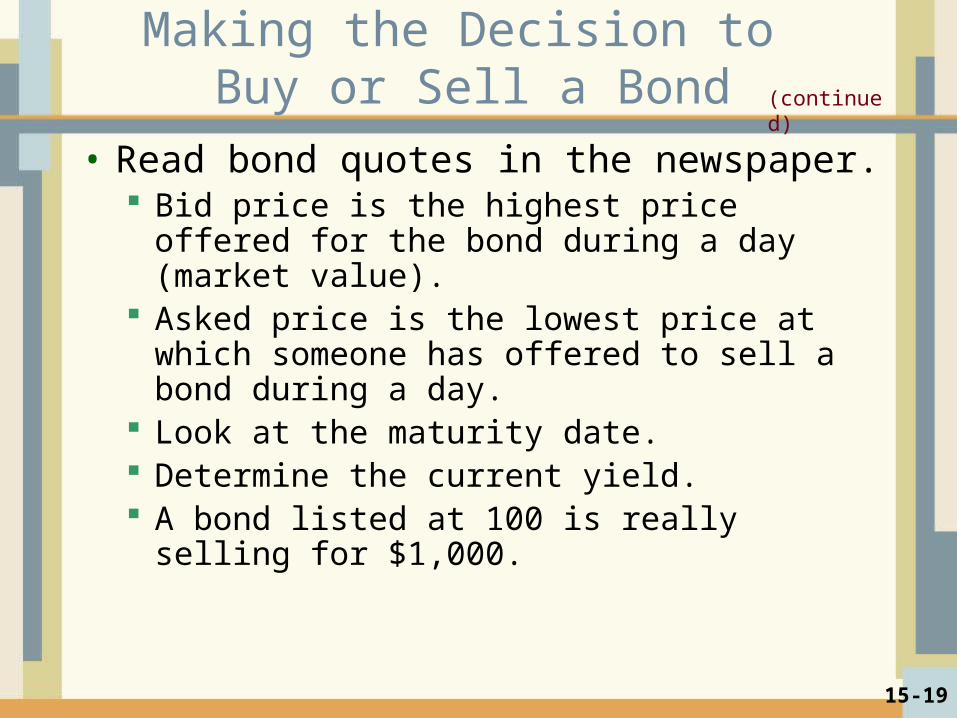

Making the Decision to Buy or Sell a Bond

• Read bond quotes in the newspaper. Bid price is the highest price offered for the

bond during a day (market value). Asked price is the lowest price at which

someone has offered to sell a bond during a day.

Look at the maturity date. Determine the current yield. A bond listed at 100 is really selling for $1,000.

15-19

(continued)

Current Yield of a Bond (%)

15-20

Example:Current yield = $75

$800 = 0.094 = 9.4%

The Investment’s Current Market value

Dollar Amount of Income Generated Yearly

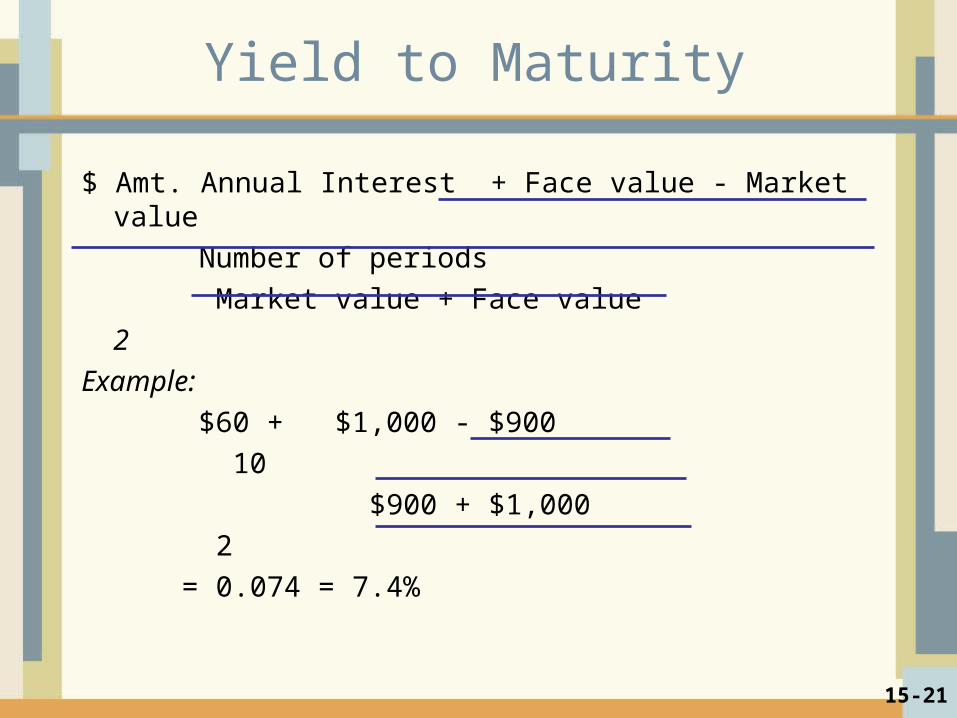

Yield to Maturity

$ Amt. Annual Interest + Face value - Market value

Number of periods

Market value + Face value

2

Example:

$60 + $1,000 - $900

10

$900 + $1,000

2

= 0.074 = 7.4%

15-21

Online Activity

• Go to one of these sites and look up information about municipal bonds in your area.

• www.emuni.com

• www.municipalbonds.com

• What do you think of the rates these bonds are paying?

15-22