CHAPTER 14 THE STATEMENT OF CASH FLOWS - GBS … 3 Using Cash Flow... · 1 CHAPTER 14 THE STATEMENT...

36

1 CHAPTER 14 THE STATEMENT OF CASH FLOWS E14–1 1. Investing activity 2. Financing activity 3. Operating activity 4. Financing activity 5. Investing activity 6. Investing activity (for the cash paid for the building) Financing activity (for the mortgage payable) 7. Financing activity (for the principal payment) Operating activity (for the interest payment) 8. Operating activity 9. Financing activity 10. Operating activity E14–2 1. Not included on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be: Allowance for Doubtful Accounts (+A) .......................... XX Accounts Receivable (–A) ...................................... XX Wrote off uncollectible accounts. 2. Investing activity 3. Financing activity 4. Any gain or loss would be adjusted out of operating activities. The exchange of notes for the building would have no net impact on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be: Notes Receivable (+A) .................................................. XX Accumulated Depreciation: Building (+A) ..................... XX Building (–A) ........................................................... XX Sold a building in exchange for a five year note. 5. Not included on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be: Dividend (–SE) .............................................................. XX Dividend Payable (+L) ............................................ XX Declared a dividend. 6. Not included on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be:

Transcript of CHAPTER 14 THE STATEMENT OF CASH FLOWS - GBS … 3 Using Cash Flow... · 1 CHAPTER 14 THE STATEMENT...

1

CHAPTER 14

THE STATEMENT OF CASH FLOWS

E14–1

1. Investing activity 2. Financing activity 3. Operating activity 4. Financing activity 5. Investing activity 6. Investing activity (for the cash paid for the building) Financing activity (for the mortgage payable) 7. Financing activity (for the principal payment) Operating activity (for the interest payment) 8. Operating activity 9. Financing activity 10. Operating activity

E14–2

1. Not included on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be:

Allowance for Doubtful Accounts (+A) .......................... XX Accounts Receivable (–A) ...................................... XX Wrote off uncollectible accounts. 2. Investing activity 3. Financing activity 4. Any gain or loss would be adjusted out of operating activities. The exchange of notes for

the building would have no net impact on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be:

Notes Receivable (+A) .................................................. XX Accumulated Depreciation: Building (+A) ..................... XX Building (–A) ........................................................... XX Sold a building in exchange for a five year note. 5. Not included on the statement of cash flows because it does not affect cash. As proof, the

entry for this event would be: Dividend (–SE) .............................................................. XX Dividend Payable (+L) ............................................ XX Declared a dividend. 6. Not included on the statement of cash flows because it does not affect cash. As proof, the

entry for this event would be:

Bonds Payable (–L) ...................................................... XX Common Stock (+SE) ............................................. XX Retired bonds with common stock. 7. Investing activity 8. Not included on the statement of cash flows because it does not affect cash. As proof, the

entry for this event would be: Dividend (–SE) .............................................................. XX Common Stock (+SE) ............................................. XX Additional Paid-in Capital, Common Stock (+SE) .. XX Declared and issued a stock dividend. 9. Not included on the statement of cash flows because it does not affect cash. As proof, the

entry for this event would be: Depreciation Expense (E, –SE) .................................... XX Accumulated Depreciation (–A) .............................. XX Depreciated fixed assets. 10. Operating activity 11. Not included on the statement of cash flows because it does not affect cash. As proof, the

entry for this event would be: Inventory (+A)................................................................ XX Accounts Payable (+L) ........................................... XX Purchased inventory on account. 12. Operating activity 13. Any gain or loss would be included in operating activities only to adjust Net Income. The

balance of the transaction would not be included on the statement of cash flows because it does not affect cash. As proof, the entry for this event would be:

Land (+A) ...................................................................... XX Accumulated Depreciation: Building (+A) ..................... XX Building (–A) ........................................................... XX Exchanged a building for land. 14. Financing activity 15. Operating activity

E14–5

Assets = Liabilities + Owners’ Equity 1. Depreciation expense –170,000 = –170,000 2. Issue of common stock +180,000 = +180,000 3. Purchase IBM stock 375,000 (securities) –375,000 (cash) 4. Purchase insurance +27,000 (ppd insurance) –27,000 (cash) 5. Purchase of building +200,000 (building) – 40,000 (cash) = +160,000 (mortgage) 1. Under the direct method, depreciation expense is not included on the statement of cash flows

because it does not affect cash. However, under the indirect method, depreciation expense is included under operating activities as an adjustment to net income to arrive at net cash flows from operating activities.

2. Issuance of common stock, $180,000, increases cash. The $180,000 would be included in the

financing activities section. 3. Purchase of marketable securities, $375,000, decreases cash. Marketable securities are

nonoperating assets for most businesses. Consequently, the purchase of these securities for cash would be disclosed in the investing activities section.

4. Prepaid insurance, $27,000, decreases cash. The $27,000 would be included in the operating

activities section. 5. Down payment on building, $40,000, decreases cash. The $40,000 would be included under

investing activities. (The mortgage would be disclosed in the footnotes to the financial statements or in a supplemental schedule to the statement of cash flows.)

E14–8

a. 1. Cash (+A)............................................................................... 20,000 Contributed Capital (+SE) ............................................... 20,000 Owner contributed capital.

2. Cash (+A)............................................................................... 60,000 Notes Payable (+L) ......................................................... 60,000 Borrowed money from the bank. 3. Property, Plant, & Equipment (+A) ........................................ 25,000 Cash (–A) ........................................................................ 25,000 Purchased long-lived assets. 4. Inventory (+A) 40,000 Cash (–A) ........................................................................ 25,000 Accounts Payable (+L) .................................................... 15,000 Purchased inventory.

E14–8 Continued

5. Cash (+A)............................................................................... 20,000 Accounts Receivable (+A) ..................................................... 60,000 Sales (R, +SE) ................................................................. 80,000 Made sale.

Cost of Goods Sold (E, –SE) ................................................. 25,000 Inventory (–A) .................................................................. 25,000 Recognized cost of inventory sold.

6. Operating Expenses (E, –SE) ............................................... 18,000 Payable to Bank (–L) ............................................................. 5,000 Dividend (–SE)....................................................................... 2,000 Cash (–A) ........................................................................ 25,000 Made cash disbursements. 7. Operating Expenses (E, –SE) ............................................... 15,000 Operating Expenses Payable (+L) .................................. 15,000 Incurred, but did not pay, expenses.

b.

Tony’s Business Income Statement

For the Year Ended December 31, 2015

Sales ................................................................................................ $ 80,000 Cost of goods sold ........................................................................... (25,000) Operating expenses ......................................................................... (33,000) Net income ....................................................................................... $ 22,000

Tony's Business

Statement of Retained Earnings For the Year Ended December 31, 2015

Beginning retained earnings balance: January 1, 2015 .................. $ 0 Plus: Net income .............................................................................. 22,000 Less: Dividends ................................................................................ (2,000) Ending retained earnings, December 31, 2015 ............................... $ 20,000

E14–8 Continued

Tony's Business Balance Sheet

December 31, 2015 Assets Liabilities & Stockholders' Equity Cash................................................. $ 25,000 Accounts payable ................. $ 15,000 Accounts receivable ........................ 60,000 Operating expenses payable 15,000 Inventory .......................................... 15,000 Payable to bank ................... 55,000 Property, plant & equipment ............ 25,000 Contributed capital ............... 20,000 Retained earnings ................ 20,000 Total liabilities and Total assets ..................................... $ 125,000 stockholders' equity ............ $ 125,000 c. Cash

Beginning balance 0 Owner's contribution 20,000 Purchase of fixed assets 25,000 Proceeds from bank loan 60,000 Purchase of inventory 25,000 Proceeds from sale 20,000 Operating expenses 18,000 Principal payment 5,000 Dividend payment 2,000

Ending balance 25,000

Tony's Business Statement of Cash Flows

For the Year Ended December 31, 2015

Cash from operating activities: Cash collections from sales ............................................ $ 20,000 Cash paid for inventory ................................................... (25,000) Cash paid for expenses .................................................. (18,000) Net cash increase (decrease) due to operating activities .................................................................. $ (23,000) Cash from investing activities: Purchase of fixed assets ................................................. (25,000) Cash from financing activities: Proceeds from owner's contribution ............................... $ 20,000 Proceeds from bank loan ................................................ 60,000 Principal repayment on debt ........................................... (5,000) Payment of dividend ....................................................... (2,000) Net cash increase (decrease) due to financing activities .................................................................. 73,000 Net increase (decrease) in cash ......................................... $ 25,000 Beginning cash balance, January 1, 2015 .......................... 0 Ending cash balance, December 31, 2015 ......................... $ 25,000

E14–8 Concluded

d. Tony's Business

Statement of Cash Flows For the Year Ended December 31, 2015

Cash from operating activities: Net income .......................................................... $ 22,000 Adjustments: Increase in accounts receivable .................... $ (60,000) Increase in inventory ...................................... (15,000) Increase in accounts payable ........................ 15,000 Increase in operating expense payable ......... 15,000 Total adjustments ...................................... (45,000) Net cash increase (decrease) due to operating activities ....................... $ (23,000) Cash from investing activities: Purchase of fixed assets ..................................... (25,000) Cash from financing activities: Proceeds from owner's contribution ................... $ 20,000 Proceeds from bank loan .................................... 60,000 Principal repayment on debt ............................... (5,000) Payment of dividend ........................................... (2,000) Net cash increase (decrease) due to financing activities ........................................ 73,000 Net increase (decrease) in cash ............................. $ 25,000 Beginning cash balance, January 1, 2015 .............. 0 Ending cash balance, December 31, 2015 ............. $ 25,000

E14–9

a. 1. Cash (+A)............................................................................... 6,000 Common Stock (+SE) ..................................................... 6,000 Issued common stock.

2. Inventory (+A) ........................................................................ 6,000 Accounts Payable (+L) .................................................... 6,000 Purchased inventory on account. 3. Equipment (+A) ...................................................................... 5,000 Cash (–A) ........................................................................ 5,000 Purchased equipment. 4. Cash (+A)............................................................................... 10,000 Accounts Receivable (–A) ............................................... 10,000 Collected cash from customers.

E14–9 Continued

5. Accounts Payable (–L) .......................................................... 5,000 Cash (–A) ........................................................................ 5,000 Made payment to suppliers. 6. Dividend (–SE)....................................................................... 2,000 Cash (–A) ........................................................................ 2,000 Declared and paid cash dividend. 7. Rent Expense (E, –SE) ......................................................... 6,000 Prepaid Rent (+A) .................................................................. 6,000 Cash (–A) ........................................................................ 12,000 Disbursed cash for rent. 8. Cash (+A)............................................................................... 65,000 Accounts Receivable (+A) ..................................................... 35,000 Sales (R, +SE) ................................................................. 100,000 Made sales. 9. Miscellaneous Expenses (E, –SE) ........................................ 40,000 Cash (–A) ........................................................................ 40,000 Incurred and paid miscellaneous expenses. 10. Cash (+A)............................................................................... 25,000 Marketable Securities (–A) .............................................. 20,000 Gain on Sale of Marketable Securities (Ga, +SE) .......... 5,000 Sold marketable securities.

b. Cash

(B.B.) 25,000 (1) 6,000 (3) 5,000 (4) 10,000 (5) 5,000 (8) 65,000 (6) 2,000 (10) 25,000 (7) 12,000 (9) 40,000

(E.B.) 67,000

E14–9 Concluded

c. Driftwood Shipbuilders

Statement of Cash Flows For the Year Ended December 31, 2015

Cash flows from operating activities: Cash collections from customers ................................. $ 75,000 Cash payments for rent ............................................... (12,000) Cash payments for miscellaneous expenses .............. (40,000) Cash payments for inventory ....................................... (5,000) Net cash increase due to operating activities ......... $ 18,000 Cash flows from investing activities: Proceeds from sale of marketable securities .............. $ 25,000 Purchase of equipment ................................................ (5,000) Net cash increase due to investing activities .......... 20,000 Cash flows from financing activities: Proceeds from issue of common stock ....................... $ 6,000 Dividend payment ........................................................ (2,000) Net cash increase due to financing activities ......... 4,000 Net increase in cash ......................................................... $ 42,000 Beginning cash balance, January 1, 2015 ....................... 25,000 Ending cash balance, December 31, 2015 ...................... $ 67,000

E14–10

Insurance 2015 Ending prepaid insurance = 2015 Beginning prepaid insurance + Insurance purchases during 2015– 2015 Insurance expense $7,000 = $4,200 + Insurance purchases – $3,000 Insurance purchases = $5,800 Wages 2015 Ending wages payable = 2015 Beginning wages payable + 2015 Wage expense – Wages paid during 2015 $6,000 = $0 + $8,500 – Wages paid Wages paid = $2,500

E14–11

a. 2015 Ending machinery = 2015 Beginning machinery + Cost of machinery purchased during 2015 – Cost of machinery sold during 2015

$45,000 = $20,000 + Machinery purchased – $8,000 Machinery purchased = $33,000 b. When the machinery was sold during 2015, Dylan’s Toys, would prepare the appropriate entry

using the following format.

Cash (+A) ........................................................ XX Accumulated Depreciation (+A) ...................... XX Machinery (–A) .......................................... XX Gain on Sale of Machinery (Ga, +SE) ...... XX

We can find the cash collected for the sale of the machinery by first calculating the other three amounts. Machinery It is given in the exercise that the cost of the machinery sold was $8,000. Gain on Sale of Machinery It is given in the exercise that the gain on the sale was $2,000. Accumulated Depreciation 2015 Ending accumulated depreciation = 2015 Beginning accumulated depreciation + 2015 Depreciation expense – Accumulated depreciation on items sold $15,000 = $10,000 + $7,000 – Accumulated depreciation on items sold Accumulated depreciation on items sold = $2,000 From the entry given above, Cash = Cost of machinery sold + Gain on sale of machinery – Accumulated depreciation on machinery sold = $8,000 + $2,000 – $2,000 = $8,000

c. Cash (+A) ......................................................................................... 8,000 Accumulated Depreciation (+A) ....................................................... 2,000 Machinery (–A) ........................................................................... 8,000 Gain on Sale of Machinery (Ga, +SE) ....................................... 2,000 Sold machinery.

E14–12

Cash Receipts Cash Payments

12/31/11 accounts receivable $ 499 Change in payables (‘12-‘11) $ 79

2012 Sales 17,097 2012 cost of sales 14,803

12/31/12 accounts receivable (466) Change in inventory (‘11-’12) (54)

2012 cash receipts $17,130 2012 cash payments $ 14,828

E14–13

1. Direct method The first step in calculating the cash flows from operating activities is to calculate the cash inflows and outflows associated with each income statement account. These calculations are given below. Cash collections from customers: Cash collections from customers = Sales – Ending accounts receivable + Beginning accounts receivable + Ending deferred revenues – Beginning deferred revenues = $48,000 – $4,000 + $5,000 + $0 – $3,000 = $46,000 Cash paid for inventory: a. Inventory purchased

2015 Ending inventory = 2015 Beginning inventory + Net inventory purchased during 2015 – 2015 Cost of goods sold $9,000 = $11,000 + Net purchases – $30,000 Net purchases = $28,000

b. Disbursements for inventory

2015 Ending accounts payable = 2015 Beginning accounts payable + Net inventory purchased during 2015 – Payments for inventory during 2015 $3,000 = $4,000 + $28,000 – Payments Payments = $29,000

Cash paid for wages: 2015 Ending wages payable = 2015 Beginning wages payable + 2015 Wage Expense – Wages paid during 2015 $1,800 = $900 + $4,000 – Wages paid Wages paid = $3,100 Cash paid for advertising: 2015 Ending prepaid advertising = 2015 Beginning prepaid advertising + Advertising paid – 2015 Advertising expense $3,000 = $1,200 + Advertising paid – $1,000 Advertising paid = $2,800 Cash flows from operating activities:

Cash collections from customers ............................................... $ 46,000 Payments for inventory .............................................................. (29,000) Payments for wages .................................................................. (3,100) Payments for advertising ........................................................... (2,800) Net cash increase due to operating activities ............................ $ 11,100

E14–13 Concluded

2. Indirect method

Cash flows from operating activities: Net income .................................................................... $ 11,000 Adjustments: Depreciation .............................................................. $ 2,000 Decrease in accounts receivable ............................. 1,000 Decrease in inventory ............................................... 2,000 Increase in wages payable ....................................... 900 Increase in prepaid advertising ................................ (1,800) Decrease in deferred revenues ................................ (3,000) Decrease in accounts payable ................................. (1,000) Total adjustments ................................................ 100 Net cash increase due to operating activities ....................................................... $ 11,100

E14–14

Grimes Pools Statement of Cash Flows

For the Year Ended December 31, 2015

Cash from operating activities: Cash collections from sales ............................................ $ 35,000 Cash paid on operating liabilities .................................... (6,000) Cash paid for expenses .................................................. (34,000) Net cash increase (decrease) due to operating activities .................................................................. $ (5,000) Cash from investing activities:

Proceeds from sale of nonoperating assets ................... 8,000a Cash from financing activities:

Proceeds from issuing debt ............................................ $ 2,000b Payment of dividends ..................................................... (3,000)

Repurchase of contributed capital .................................. (4,000)c Net cash increase (decrease) due to financing activities .................................................................. (5,000) Net increase (decrease) in cash ......................................... $ (2,000) Beginning cash balance, January 1, 2015 .......................... 6,000 Ending cash balance, December 31, 2015 ......................... $ 4,000 a Proceeds from sale of nonoperating assets equals the decrease in nonoperating assets.

Since no gain on sale of assets or loss on sale of assets is reported, one must assume that the book value of the assets sold equaled the proceeds from the sale.

b Proceeds from issue of debt = Increase in nonoperating liabilities c Repurchase of contributed capital = Decrease in contributed capital

E14–15

Romora Supply House Statement of Cash Flows

For the Year Ended December 31, 2015

Cash from operating activities: Cash collections from sales ............................................ $ 64,000 Cash from decrease in noncash operating assets ......... 5,000 Cash from increase in operating liabilities ...................... 5,000 Cash paid for expenses .................................................. (61,000) Net cash increase (decrease) due to operating activities .................................................................. $ 13,000 Cash from investing activities:

Purchase of nonoperating assets ................................... (4,000)a Cash from financing activities:

Proceeds from contributed capital .................................. $ 3,000b

Payment on debt ............................................................. (2,000)c Payment of dividends ..................................................... (3,000) Net cash increase (decrease) due to financing activities .................................................................. (2,000) Net increase (decrease) in cash ......................................... $ 7,000 Beginning cash balance, January 1, 2015 .......................... 5,000 Ending cash balance, December 31, 2015 ......................... $ 12,000 a Purchase of nonoperating assets = Increase in nonoperating assets b Proceeds from contributed capital = Increase in contributed capital c Payment on nonoperating debt = Decrease in nonoperating liabilities

E14–17

L.L. Beeno Operating Section – Statement of Cash Flows (Direct Method)

For the Year Ended December 31, 2015

Cash from operating activities: Cash receipts from revenues .......................................... $ 45,900 Cash payments for inventory .......................................... (26,400) Cash payments for wages .............................................. (5,100) Cash payments for insurance ......................................... (3,900) Cash payments for interest ............................................. (1,600) Cash payments for taxes ................................................ _(1,200) Net cash increase (decrease) due to operating activities .................................................................. $ 7,700

E14–17 Concluded

L.L. Beeno Operating Section – Statement of Cash Flows (Indirect Method)

For the Year Ended December 31, 2015

Cash flows from operating activities:

Net income .................................................................... $ 5,500 Adjustments: Depreciation expense ............................................... $ 3,300 Increase in accounts receivable ............................... (1,100) Decrease in inventory ............................................... 300 Decrease in prepaid insurance ................................. 300 Decrease in accounts payable ................................. (1,700) Increase in wages payable ....................................... 1,100 Total adjustments ................................................ 2,200 Net cash increase due to operating activities ....................................................... $ 7,700

E14–18

Martland Stores

Operating Section – Statement of Cash Flows (Direct Method) For the Year Ended December 31, 2015

Cash from operating activities: Cash receipts from revenues .......................................... $ 97,500 Cash payments for inventory .......................................... (59,200) Cash payments for wages .............................................. (16,500) Cash payments for insurance ......................................... (8,900) Cash payments for interest ............................................. _(2,100) Net cash increase (decrease) due to operating activities .................................................................. $ 10,800

Martland Stores Operating Section – Statement of Cash Flows (Indirect Method)

For the Year Ended December 31, 2015

Cash flows from operating activities:

Net income .................................................................... $ (3,600) Adjustments: Depreciation expense ............................................... $ 5,700 Decrease in accounts receivable ............................. 1,500 Decrease in inventory ............................................... 5,300 Decrease in prepaid insurance ................................ 300 Decrease in accounts payable ................................. (500) Increase in wages payable ....................................... 2,100 Total adjustments ................................................ 14,400 Net cash increase due to operating activities ....................................................... $ 10,800

E14–19

Mako Retail Operating Section – Statement of Cash Flows (Direct Method)

For the Year Ended December 31, 2015

Cash from operating activities: Cash receipts from revenues .......................................... $ 108,700 Cash payments for inventory .......................................... (58,800) Cash payments for wages .............................................. (13,000) Cash payments for rent .................................................. (8,400) Cash payments for interest ............................................. (3,600) Cash payments for taxes ................................................ _ (4,400) Net cash increase (decrease) due to operating activities .................................................................. $ 20,500

Mako Retail

Operating Section – Statement of Cash Flows (Indirect Method) For the Year Ended December 31, 2015

Cash flows from operating activities:

Net income .................................................................... $ 11,200 Adjustments: Depreciation expense ............................................... $ 6,200 Loss on sale of equipment ....................................... 4,200 Increase in accounts receivable ............................... (2,200) Decrease in inventory ............................................... 600 Decrease in prepaid rent .......................................... 600 Decrease in accounts payable ................................. (3,400) Increase in wages payable ....................................... 2,200 Decrease in interest payable .................................... (700) Increase in unearned revenue .................................. _ 1,800 Total adjustments ................................................ 9,300 Net cash increase due to operating activities ....................................................... $ 20,500

P14–1

a., b., and c. Transaction Section Inflow Outflow Amount

1. Operating X $ 60,000 2. N/A 3. Operating X 40,000 4. Investing X 94,000 5. Operating X 15,000 Financing X 75,000 6. N/A 7. Financing X 150,000 8. N/A 9. Financing X 475,000 10. Investing X 100,000 11. N/A

P14–2

a., b., and c. Transaction Section Inflow Outflow Amount

1. Operating X $ 52,000 2. Investing X 12,000 3. Operating X 30,000 4. N/A 5. Operating X 10,000 Investing X 90,000 6. Operating X 45,000 7. Financing X 50,000 8. Financing X 40,000 9. Operating X 25,000 10. Financing X 300,000 11. N/A 12. N/A 13. N/A

P14–3

a. Transaction Cash Affected Type of Effect Dollar Amount

1. Yes Provided $ 1,200 2. Yes Used 13,000 3. Yes Used 9,000 4. Yes Provided 7,000 5. Yes Provided 2,500 6. Yes Provided 3,000 7. No 8. Yes Used 7,000 9. Yes Used 5,000 10. No 11. No 12. No 13. No

b. 1. Investing

2. Investing 3. Operating 4. Financing 5. Operating (for the interest) Investing or Operating (for the principal) depending on how the company acquired the

note. If it was accepted in a sales transaction, it could be argued that collecting the principal is an operating activity. If the company acquired the note in any other way, the collection of the principal would be considered an investing activity.

6. Operating 7. N/A 8. Financing 9. Operating 10. N/A 11. N/A 12. N/A 13. N/A

P14–8

a. Case 1: Based on the $820,000 beginning balance in the Buildings account and the purchase during 2015 of a building for $60,000, one would expect the Buildings account to have a balance of $880,000 at the end of 2015. The fact that its balance is only $750,000 implies that Webb Industries must have sold a building that originally cost $130,000. Similarly, based on the beginning balance of $80,000 in the Accumulated Depreciation: Buildings account and the $40,000 of depreciation taken on the building during 2015, one would expect the Accumulated Depreciation: Buildings account to have a balance of $120,000 at the end of 2015. The fact that its balance is only $100,000 implies that the accumulated depreciation associated with the building that Webb Industries sold during 2015 must have been $20,000. This information is summarized in the following T accounts.

Buildings Accumulated Depreciation

B.B. 820,000 B.B. 80,000 Purchase 60,000 Sale X Sale Y Depr. Exp. 40,000 E.B. 750,000 E.B. 100,000

X = Cost of building sold = $130,000 Y = Accumulated depreciation on building sold = $20,000 Case 2: Based on the $380,000 beginning balance in the Equipment account and the sale during 2015 of equipment that originally cost $50,000, one would expect the Equipment account to have a balance at the end of 2015 of $330,000. The fact that its balance is $500,000 implies that Webb Industries must have purchased some equipment for $170,000. Similarly, based on the beginning balance of $85,000 in the Accumulated Depreciation: Equipment account and the $15,000 of depreciation taken on the equipment during 2015, one would expect the Accumulated Depreciation: Equipment account to have a balance at the end of 2015 of $100,000. The fact that its balance is only $75,000 implies that the accumulated depreciation associated with the equipment that Webb Industries sold during 2015 must have been $25,000. This information is summarized in the following T accounts.

Equipment Accumulated Depreciation

B.B. 380,000 B.B. 85,000 Purchase X Sale 50,000 Sale Y Depr. Exp. 15,000 E.B. 500,000 E.B. 75,000

X = Cost of equipment purchased = $170,000 Y = Accumulated depreciation on equipment sold = $25,000

Case 3: Based on the $250,000 beginning balance in the Land account and the sale of land during 2015, one would expect the balance in the Land account to decrease. The fact that its balance is still $250,000 at the end of 2015 implies that (1) Webb Industries must have purchased some land during 2015 and (2) the cost of the land purchased exactly equaled the original cost of the land that was sold. Since a gain on the sale of land equals the excess of the proceeds over the cost of the land, it can be inferred that the land that Webb Industries sold during 2015 originally cost $225,000 (i.e., proceeds of $300,000 less gain of $75,000). Thus, the cost of the land that Webb Industries purchased during 2015 was $225,000. This information is summarized in the following T account.

Land

B.B. 250,000 Purchase Y Sale X E.B. 250,000

Y = Cost of land purchased = $225,000 X = Cost of land sold = $225,000 Case 4: In exchange between two independent parties, one would expect the fair market value of the item given up by one of the parties to equal the fair market value of the item that party is to receive. Thus, it is probably safe to assume that the fair market value of the new building is $600,000. Based on the $820,000 beginning balance in the Buildings account and the acquisition during 2015 of a new building for $600,000, one would expect the Buildings account to have a balance of $1,420,000 at the end of 2015. The fact that its balance is only $750,000 implies that Webb Industries must have disposed of a building during 2015 that originally cost $670,000. Similarly, based on the beginning balance of $80,000 in the Accumulated Depreciation: Buildings account and the $40,000 of depreciation taken on buildings during 2015, one would expect the Accumulated Depreciation: Buildings account to have a balance at the end of 2015 of $120,000. The fact that its balance is only $100,000 implies that the accumulated depreciation associated with the building that Webb Industries sold during 2015 must have been $20,000. Further, based on the $250,000 beginning balance in the Land account and the disposal during 2015 of land that had a book value of $150,000, one would expect the Land account to have a balance of $100,000 at the end of 2015. The fact that its balance is $250,000 implies that Webb Industries must have acquired some land during 2015 that cost $150,000. This information is summarized in the following T accounts.

Buildings Accumulated Depreciation

B.B. 820,000 B.B. 80,000 Purchase 600,000 Sale X Sale Y Depr. Exp. 40,000 E.B. 750,000 E.B. 100,000

X = Cost of building sold = $670,000 Y = Accumulated depreciation on building sold = $20,000

Land

B.B. 250,000 Purchase Z Sale 150,000 E.B. 250,000

Z = Cost of land purchased = $150,000

b. Case 1: Proceeds from sale = Cost of building sold – Related accumulated depreciation = $130,000 – $20,000 = $110,000 Note: This solution assumes that there was no gain or loss on the sale of the building, since

no such information was given in the problem.

In the statement of cash flows for 2015, Webb Industries would report the following items under cash flows from investing activities. Proceeds from sale of building $ 110,000 Purchase of building (60,000)

Case 2: Proceeds from sale = Book value of equipment sold + Gain on sale = ($50,000 – $25,000) + $5,000 = $30,000

In the statement of cash flows for 2015, Webb Industries would report the following items under cash flows from investing activities. Proceeds from sale of equipment $ 30,000 Purchase of equipment (170,000)

Case 3: In the statement of cash flows for 2015, Webb Industries would report the following items under cash flows from investing activities. Proceeds from the sale of land $300,000 Purchase of land (225,000)

Case 4: Since Webb Industries exchanged land for a building, this transaction did not affect cash and would not be disclosed in the body of the statement of cash flows. However, Webb Industries did collect $650,000 from the building it sold ($670,000 cost of building sold – $20,000 accumulated depreciation on the building), which Webb Industries would report under cash flows from investing activities.

P14–9

Total number of shares issued during 2015 = Change in balance of common stock account ÷ Par value per share of common stock = ($128,000 – $100,000) ÷ $1 per share = 28,000 shares Number of shares issued for cash = Total number of shares issued – (Shares issued as stock dividend + Shares issued in exchange for land) = 28,000 shares – [(100,000 shares outstanding on

1/1/15 20%) + 6,000 shares exchanged for land] = 28,000 shares – (20,000 shares + 6,000 shares) = 2,000 shares Cash received = Change in common stock account due to issue of common stock for cash + Change in additional paid-in capital, common stock account due to issue of common stock for cash

= (2,000 shares $1 par value per share) + [($95,000 – $12,000) –

$40,000a + $12,000b] = $2,000 + $31,000 = $33,000

a $40,000 represents the additional paid-in capital from the 20% stock dividend. The company distributed 20,000 shares, and the fair market value at the time was $3 per share. One dollar was allocated to the Common Stock account, and the remaining $2 was allocated to the Additional Paid-in Capital, Common Stock account.

b $12,000 represents the additional paid-in capital from exchanging stock for land.

P14–11

Accrual sales = Collections from customers + Increase in accounts receivable = $26,000 + $3,000 = $29,000 Accrual COGS = Payments to suppliers – Increase in inventory + Increase in accounts payable = $13,000 – $3,000 + $1,000 = $11,000 Accrual operating expenses = Payments for expenses – Decrease in accrued payables = $10,000 – $2,000 = $8,000

Battery Builders, Inc. Income Statement

Sales ...................................................................................................... $ 29,000 Cost of goods sold ................................................................................. (11,000) Depreciation expense ............................................................................ (3,000) Other operating expenses ...................................................................... (8,000) Gain on sale of equipment ..................................................................... 2,000 Net income ............................................................................................. $ 9,000

P14–13

Watson and Holmes Detective Agency Statement of Cash Flows – Direct Method For the Year Ended December 31, 2015

Cash flows from operating activities: Cash collections from customers .................................... $ 34,500* Cash paid for inventory ................................................... (23,000) Cash paid for interest ...................................................... (2,800) Cash paid for other expenses ......................................... (9,000) Net cash increase (decrease) due to operating activities .................................................................. $ (300) Cash flows from investing activities: Purchase of long-lived assets ......................................... $ (1,000) Net cash increase (decrease) due to investing activities .................................................................. (1,000) Cash flows from financing activities: Cash paid for dividends .................................................. $ (700) Proceeds from issuance of common stock ..................... 6,000 Net cash increase (decrease) due to financing activities .................................................................. 5,300 Net increase in cash ............................................................ $ 4,000 Beginning cash balance, January 1, 2015 .......................... 6,000 Ending cash balance, December 31, 2015 ......................... $ 10,000

* $35,500 = $42,000 revenues – $5,000 increase in accounts receivable + $500 increase in allowance for doubtful accounts – $2,000 bad debt expense – $1,000 decrease in deferred revenues

P14–13 Concluded

Watson and Holmes Detective Agency Statement of Cash Flows – Direct Method For the Year Ended December 31, 2015

Cash flows from operating activities: Net income .......................................................... $ 2,000 Adjustments: Depreciation ................................................... $ 2,000 Increase in allowance for doubtful accounts . 500 Decrease in accounts payable ....................... (1,000) Decrease in discount on note payable .......... 200 Increase in accounts receivable .................... (5,000) Decrease in inventory .................................... 2,000 Decrease in deferred revenues ..................... (1,000) Total adjustments ...................................... (2,300) Net cash increase (decrease) due to operating activities ......................... $ (300)

Cash flows from investing activities: Purchase of long-lived assets ............................. $ (1,000) Net cash increase (decrease) due to investing activities ....................................... (1,000)

Cash flows from financing activities: Cash paid for dividends ...................................... $ (700) Proceeds from issuance of common stock ......... 6,000 Net cash increase (decrease) due to financing activities ....................................... 5,300 Net increase in cash ................................................ $ 4,000

Beginning cash balance, January 1, 2015 .............. 6,000 Ending cash balance, December 31, 2015 ............. $ 10,000

P14–15

a. Marketing revenue 2015 Ending accounts receivable = 2015 Beginning accounts receivable + 2015 Marketing revenue – Cash collections during 2015 $150,000 = $105,000 + $1,000,000 – Cash collections Cash collections = $955,000

Salary expense Since no related balance sheet account exists as of December 31, 2014 or as of December 31, 2015, it is safe to assume that the entire balance in Salary Expense was paid in cash. Therefore, the cash paid for salaries equals $250,000. Supplies expense 2015 Ending office supply inventory = 2015 Beginning office supply inventory + Office supplies purchased during 2015 – 2015 Office supplies expense $75,000 = $85,000 + Supplies purchased – $175,000 Office supply purchases = $165,000

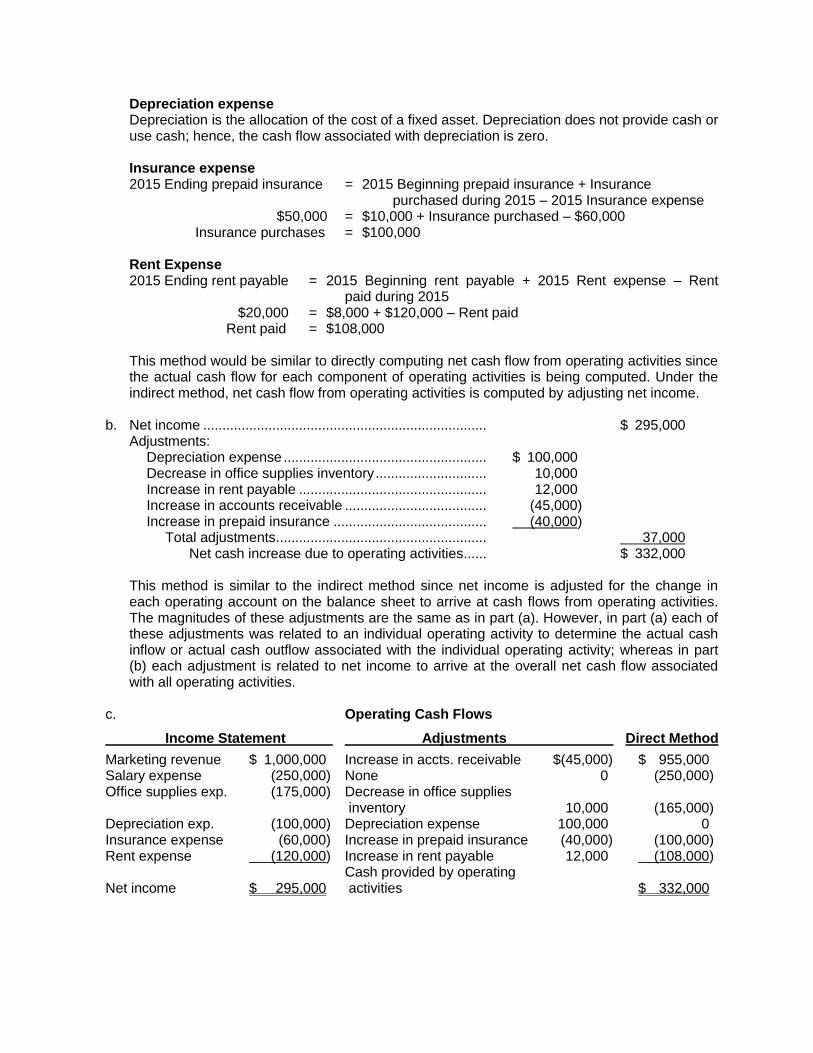

Depreciation expense Depreciation is the allocation of the cost of a fixed asset. Depreciation does not provide cash or use cash; hence, the cash flow associated with depreciation is zero. Insurance expense 2015 Ending prepaid insurance = 2015 Beginning prepaid insurance + Insurance purchased during 2015 – 2015 Insurance expense $50,000 = $10,000 + Insurance purchased – $60,000 Insurance purchases = $100,000 Rent Expense 2015 Ending rent payable = 2015 Beginning rent payable + 2015 Rent expense – Rent paid during 2015 $20,000 = $8,000 + $120,000 – Rent paid Rent paid = $108,000

This method would be similar to directly computing net cash flow from operating activities since the actual cash flow for each component of operating activities is being computed. Under the indirect method, net cash flow from operating activities is computed by adjusting net income.

b. Net income .......................................................................... $ 295,000

Adjustments: Depreciation expense ..................................................... $ 100,000 Decrease in office supplies inventory ............................. 10,000 Increase in rent payable ................................................. 12,000 Increase in accounts receivable ..................................... (45,000) Increase in prepaid insurance ........................................ (40,000) Total adjustments ....................................................... 37,000 Net cash increase due to operating activities ...... $ 332,000

This method is similar to the indirect method since net income is adjusted for the change in each operating account on the balance sheet to arrive at cash flows from operating activities. The magnitudes of these adjustments are the same as in part (a). However, in part (a) each of these adjustments was related to an individual operating activity to determine the actual cash inflow or actual cash outflow associated with the individual operating activity; whereas in part (b) each adjustment is related to net income to arrive at the overall net cash flow associated with all operating activities.

c. Operating Cash Flows

Income Statement Adjustments Direct Method Marketing revenue $ 1,000,000 Increase in accts. receivable $(45,000) $ 955,000 Salary expense (250,000) None 0 (250,000) Office supplies exp. (175,000) Decrease in office supplies inventory 10,000 (165,000) Depreciation exp. (100,000) Depreciation expense 100,000 0 Insurance expense (60,000) Increase in prepaid insurance (40,000) (100,000) Rent expense (120,000) Increase in rent payable 12,000 (108,000) Cash provided by operating Net income $ 295,000 activities $ 332,000

P14–16

Direct method

Bower Manufacturing Industries Statement of Cash Flows

For the Year Ended December 31, 2015

Cash flows from operating activities: Cash collections from sales and accounts receivable .... $ 90,000a Cash paid to suppliers for inventory ............................... (90,000) Cash paid for wages ....................................................... (12,000) Cash paid for supplies .................................................... (5,000) Cash paid for interest ...................................................... (5,000) Net cash decrease due to operating activities ........... $ (22,000) Cash flows from investing activities: Proceeds from sale of fixed assets................................. $ 125,000b Proceeds from sale of marketable securities ................. 51,000c Net cash increase due to investing activities ............. 176,000 Net cash flow from financing activities ................................ 0 Net increase in cash ............................................................ $ 154,000 Beginning cash balance, January 1, 2015 .......................... 593,000 Ending cash balance, December 31, 2015 ......................... $ 747,000 a Cash collections include changes in both Accounts and Notes Receivable. b Proceeds from sale of fixed assets is computed as follows:

Cost of machinery and equipment sold ....................................... $ 150,000 Less: Related accumulated depreciation .................................... 15,000 Book value of machinery and equipment sold ............................ $ 135,000 Less: Loss on sale of fixed assets (per income statement) ........ 10,000 Proceeds from sale of fixed assets.............................................. $ 125,000

c Proceeds from sale of marketable securities is computed as follows:

Decrease in marketable securities .............................................. $ 55,000 Less: Loss on sale of marketable securities (per income statement) ................................................................................. 4,000 Proceeds from sale of marketable securities .............................. $ 51,000

P14–16 Concluded

Indirect method

Bower Manufacturing Industries Statement of Cash Flows

For the Year Ended December 31, 2015 Cash flows from operating activities: Net income .............................................................. $ 37,000 Adjustments: Decrease in inventory ....................................... $ 25,000 Depreciation ...................................................... 30,000 Decrease in discount on bonds payable ........... 5,000 Decrease in supplies inventory ......................... 2,000 Loss on sale of fixed assets .............................. 10,000 Loss on sale of marketable securities............... 4,000 Increase in accounts receivable ....................... (50,000) Increase in notes receivable ............................. (50,000) Decrease in accounts payable .......................... (35,000) Total adjustments ....................................... (59,000) Net cash decrease due to operating activities .............................................. $ (22,000) Cash flows from investing activities: Proceeds from sale of fixed assets ......................... $ 125,000 Proceeds from sale of marketable securities .......... 51,000 Net cash increase due to investing activities .... 176,000 Net cash flow from financing activities .......................... 0 Net increase in cash ...................................................... $ 154,000 Beginning cash balance, January 1, 2015 .................... 593,000 Ending cash balance, December 31, 2015 ................... $ 747,000

P14–17

Direct method

Price Restaurant Supply Company Statement of Cash Flows

For the Year Ended December 31, 2015

Cash flows from operating activities: Cash collections from customers .................................... $ 165,000 Cash paid to suppliers for inventory ............................... (199,000) Cash paid for interest ...................................................... (13,000) Net cash decrease due to operating activities ........... $ (47,000) Cash flows from investing activities:

Proceeds from sale of plant equipment .......................... $ 90,000a

Purchase of plant equipment .......................................... (25,000)a Net cash increase due to investing activities ............. 65,000 Cash flows from financing activities:

Proceeds from common stock issue............................... $ 65,000b

Payment of dividends ..................................................... (30,000)c Net cash increase due to financing activities ............ 35,000 Net increase in cash ............................................................ $ 53,000 Beginning cash balance, January 1, 2015 .......................... 120,000 Ending cash balance, December 31, 2015 ......................... $ 173,000 a Explanation of activity involving plant equipment:

Ending plant equipment = Beginning plant equipment + Equipment purchased – Equipment sold $275,000 = $350,000 + Equipment purchased – $100,000 Equipment purchased = $25,000

Proceeds from sale of equipment = Book value of assets sold + Gain on the sale = [(Asset cost – Accumulated depreciation on asset sold) + Gain on the sale] = [($100,000 – $20,000) + $10,000] = $90,000

b Proceeds from issue of common stock = Increase in common stock + Increase in

additional paid-in capital (common stock) = $35,000 + $30,000 = $65,000 c Dividends = Beginning retained earnings + Net income – Ending retained earnings = $204,000 + $37,000 – $211,000 = $30,000

P14–17 Concluded

Indirect method

Price Restaurant Supply Company Statement of Cash Flows

For the Year Ended December 31, 2015

Cash flows from operating activities: Net income ..................................................... $ 37,000 Adjustments: Depreciation .............................................. $ 12,000 Decrease in accounts receivable .............. 5,000 Decrease in prepaid insurance ................. 10,000 Increase in accounts payable ................... 1,000 Increase in inventory ................................. (100,000) Decrease in premium on bonds payable .. (2,000) Gain on sale of plant equipment ............... (10,000) Total adjustments ................................. (84,000) Net cash decrease due to operating activities ...................... $ (47,000) Cash flows from investing activities: Proceeds from sale of plant equipment ......... $ 90,000 Purchase of plant equipment ......................... (25,000) Net cash increase due to investing activities .................................. 65,000 Cash flows from financing activities: Proceeds from common stock issue.............. $ 65,000 Payment of dividends .................................... (30,000) Net cash increase due to financing activities ................................................. 35,000 Net increase in cash ........................................... $ 53,000 Beginning cash balance, January 1, 2015 ......... 120,000 Ending cash balance, December 31, 2015 ........ $ 173,000

P14–19

a. Original entries 1a. Cash (+A) ............................................................................. 1,500,000 Common Stock (+SE) .................................................... 750,000 Additional Paid-In Capital, Common Stock (+SE) ......... 750,000 Issued common stock. 1b. Cash (+A) ............................................................................. 102,000 Preferred Stock (+SE) ................................................... 100,000 Additional Paid-In Capital, Preferred Stock (+SE) ........ 2,000 Issued preferred stock. 2. Fixed Assets (+A) ................................................................ 750,000 Cash (–A) ....................................................................... 750,000 Purchased fixed assets.

3. Cash (+A) ............................................................................. 29,200a

Bonds Payable (+L) ....................................................... 20,000b Premium on Bonds Payable (+L) .................................. 9,200 Issued bonds.

a $29,200 = 20 bonds $1,000 face value per bond 146% b $20,000 = 20 bonds $1,000 face value per bond 4. Land (+A) ............................................................................. 40,000 Common Stock (+SE) .................................................... 15,000 Additional Paid-In Capital, Common Stock (+SE) ......... 25,000 Purchased land in exchange for common stock. 5a. Inventory (+A) ...................................................................... 2,000,000 Accounts Payable (+L) .................................................. 2,000,000 Purchased inventory on account.

5b. Accounts Payable (–L) ......................................................... 1,075,000 Cash (–A) ....................................................................... 1,075,000 Made payment to suppliers. 6a. Cash (+A) ............................................................................. 2,050,000 Sales (R, +SE) ............................................................... 2,050,000 Made sales. 6b. Cost of Goods Sold (E, –SE) ............................................... 875,000 Inventory (–A) ................................................................ 875,000 Recognized cost of inventory sold. 7. Prepaid Insurance (+A) ........................................................ 80,000 Cash (–A) ....................................................................... 80,000 Purchased two-year insurance policy. 8. Marketable Securities (+A) .................................................. 250,000 Cash (–A) ....................................................................... 250,000 Purchased marketable securities.

9a. Accounts Receivable (+A) ................................................... 880,000 Sales (R, +SE) ............................................................... 880,000 Made sales on account.

9b. Cost of Goods Sold (E, –SE) ............................................... 490,000 Inventory (–A) ................................................................ 490,000 Recognized cost of inventory sold.

9c. Cash (+A) ............................................................................. 500,000 Accounts Receivable (–A) ............................................. 500,000 Collected cash from customers.

10. Miscellaneous Expenses (E, –SE) ...................................... 500,000 Cash (–A) ....................................................................... 500,000 Incurred and paid miscellaneous expenses.

11. Dividends (–SE) ................................................................... 100,000 Dividends Payable (+L) ................................................. 100,000 Declared dividends.

12. Interest Expense (E, –SE) ................................................... 1,460a Premium on Bonds Payable (–L) ......................................... 140

Cash (–A) ....................................................................... 1,600b Incurred and paid interest.

_____________________

a $1,460 = Book value of $29,200 Effective rate per six-month period of 5% b $1,600 = Face value of $20,000 Stated rate per six-month period of 8% Adjusting entries (a) Depreciation Expense (E, –SE) ........................................... 140,000* Accumulated Depreciation (–A) ..................................... 140,000 Depreciated fixed assets.

* $140,000 = ($750,000 Cost – $50,000 Salvage value) ÷ 5 year useful life (b) Insurance Expense (E, –SE) ............................................... 20,000 Prepaid Insurance (–A).................................................. 20,000 Expiration of a portion of insurance policy. (c) Unrealized Loss on Marketable Securities (Lo, –SE) .......... 25,000 Allowance for Unrealized Loss on Marketable Securities (–A) ............................................ 25,000 Adjusted short-term portfolio to LCM. (d) Miscellaneous Expenses (E, –SE) ...................................... 75,000 Miscellaneous Payables (+L) ........................................ 75,000 Incurred, but did not pay, miscellaneous expenses. (e) Bad Debt Expense (E, –SE) ................................................ 70,400* Allowance for Doubtful Accounts (–A) ........................... 70,400 Estimated bad debts.

* $70,400 = Credit sales of $880,000 Uncollectible percentage of 8% (f) Loss on Inventory Write-down (Lo, –SE) ............................. 5,000 Inventory (–A) ................................................................ 5,000 Adjusted inventory to LCM.

Cash Marketable Securities Allow. for Unr. Loss on M. S.

B.B. 0 B.B. 0 B.B. 0 (1a) 1,500,000 (2) 750,000 (8) 250,000 (c) 25,000 (1b) 102,000 (5b) 1,075,000 (3) 29,200 (7) 80,000 (6a) 2,050,000 (8) 250,000 (9c) 500,000 (10) 500,000 (12) 1,600

E.B. 1,524,600 E.B. 250,000 E.B. 25,000

Accounts Receivable Allowance for D. A. Inventory

B.B. 0 B.B. 0 B.B. 0 (9a) 880,000 (9c) 500,000 (e) 70,400 (5a) 2,000,000 (6b) 875,000 (9b) 490,000 (f) 5,000

E.B. 380,000 E.B. 70,400 E.B. 630,000

P14–19 Continued

Prepaid Insurance Land Fixed Assets

B.B. 0 B.B. 0 B.B. 0 (7) 80,000 (4) 40,000 (2) 750,000 (b) 20,000

E.B. 60,000 E.B. 40,000 E.B. 750,000

Accumulated Depreciation Accounts Payable Miscellaneous Payables

B.B. 0 B.B. 0 B.B. 0 (a) 140,000 (5b) 1,075,000 (5a) 2,000,000 (d) 75,000

E.B. 140,000 E.B. 925,000 E.B. 75,000

Dividends Payable Bonds Payable Premium on Bonds Pay.

B.B. 0 B.B. 0 B.B. 0 (11) 100,000 (3) 20,000 (12) 140 (3) 9,200

E.B. 100,000 E.B. 20,000 E.B. 9,060

Preferred Stock APIC: Preferred Stock Common Stock

B.B. 0 B.B. 0 B.B. 0 (1b) 100,000 (1b) 2,000 (1a) 750,000 (4) 15,000

E.B. 100,000 E.B. 2,000 E.B. 765,000

APIC: Common Stock Retained Earnings Dividends

B.B. 0 B.B. 0 B.B. 0 (1a) 750,000 (c4) 100,000 (c3) 728,140 (11) 100,000 (4) 25,000 (c4) 100,000

E.B. 775,000 E.B. 628,140 E.B. 0

Sales Cost of Goods Sold Miscellaneous Expenses

B.B. 0 B.B. 0 B.B. 0 (6a) 2,050,000 (6b) 875,000 (10) 500,000 (9a) 880,000 (9b) 490,000 (d) 75,000 (c1) 2,930,000 (c2) 1,365,000 (c2) 575,000

E.B. 0 E.B. 0 E.B. 0

Interest Expense Bad Debt Expense Insurance Expense

B.B. 0 B.B. 0 B.B. 0 (12) 1,460 (e) 70,400 (b) 20,000 (c2) 1,460 (c2) 70,400 (c2) 20,000

E.B. 0 E.B. 0 E.B. 0

Depreciation Expense Loss on Inv. Write-down Unrealized loss on Mkt. Sec.

B.B. 0 B.B. 0 B.B. 0 (a) 140,000 (f) 5,000 (c) 25,000 (c2) 140,000 (c2) 5,000 (c2) 25,000

E.B. 0 E.B. 0 E.B. 0

P14–19 Continued

b. Closing entries (c1) Sales .................................................................................... 2,930,000 Income Summary .......................................................... 2,930,000 Closed revenues into Income Summary. (c2) Income Summary ................................................................. 2,201,860 Miscellaneous Expenses ............................................... 575,000 Cost of Goods Sold ....................................................... 1,365,000 Interest Expense ............................................................ 1,460 Bad Debt Expense ......................................................... 70,400 Depreciation Expense ................................................... 140,000 Insurance Expense ........................................................ 20,000 Loss on Inventory Write-down ....................................... 5,000 Unrealized Loss on Marketable Securities .................... 25,000 Closed expenses into Income Summary. (c3) Income Summary ................................................................. 728,140 Retained Earnings ......................................................... 728,140 Closed Income Summary into Retained Earnings. (c4) Retained Earnings ............................................................... 100,000 Dividends ....................................................................... 100,000 Closed Dividends into Retained Earnings. c.

Mick’s Photographic Equipment Income Statement

For the Year Ended December 31, 2014

Sales revenue ................................................... $ 2,930,000 Cost of goods sold ............................................ 1,365,000 Gross profit ........................................................ $ 1,565,000 Operating expenses: Depreciation expense ................................. $ 140,000 Bad debt expense ....................................... 70,400 Insurance expense ..................................... 20,000 Miscellaneous expenses ............................ 575,000 Total operating expenses ..................... 805,400 Income from operations .................................... $ 759,600 Interest expense ............................................... (1,460) Loss on write-down of inventory ....................... (5,000) Unrealized loss on marketable securities ......... (25,000) Net income ........................................................ $ 728,140

P14–19 Continued

Mick’s Photographic Equipment Balance Sheet

December 31, 2014 Assets Current assets: Cash ..................................................................................... $ 1,524,600 Marketable securities (net of allowance for unrealized losses of $25,000) ....................................... 225,000 Accounts receivable (net of allowance for doubtful accounts of $70,400) ..................................................... 309,600 Inventory .............................................................................. 630,000 Prepaid insurance ................................................................ 60,000 Total current assets ....................................................... $ 2,749,200 Land…. ....................................................................................... 40,000 Fixed assets (net of accumulated depreciation of $140,000) .... 610,000 Total assets ................................................................................ $ 3,399,200 Liabilities and Stockholders' Equity Current liabilities: Accounts payable ................................................................ $ 925,000 Miscellaneous payables ....................................................... 75,000 Dividends payable ............................................................... 100,000 Total current liabilities .................................................... $ 1,100,000 Bonds payable (including associated premium of $9,060) ........ 29,060 Stockholders' equity: Preferred stock ..................................................................... $ 100,000 Common stock ..................................................................... 765,000 Additional paid-in capital: Preferred stock .............................................................. 2,000 Common stock ............................................................... 775,000 Retained earnings ................................................................ 628,140 Total stockholders' equity .............................................. 2,270,140 Total liabilities and stockholders' equity ..................................... $ 3,399,200

P14–19 Continued

d. Direct method

Mick’s Photographic Equipment Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities: Cash collections from customers ................................ $ 2,550,000 Cash paid for inventory ............................................... (1,075,000) Cash paid for insurance .............................................. (80,000) Cash paid for interest .................................................. (1,600) Cash paid for miscellaneous expenses ...................... (500,000) Net cash increase (decrease) due to operating activities ............................................................... $ 893,400 Cash flows from investing activities: Purchase of marketable securities .............................. $ (250,000) Purchase of fixed assets ............................................. (750,000) Net cash increase (decrease) due to investing activities ............................................... (1,000,000) Cash flows from financing activities: Proceeds from bond issue .......................................... $ 29,200 Proceeds from preferred stock issue .......................... 102,000 Proceeds from common stock issue ........................... 1,500,000 Net cash increase (decrease) due to financing activities ............................................................... 1,631,200 Net increase in cash ........................................................ $ 1,524,600 Beginning cash balance, January 1, 2014 ...................... 0 Ending cash balance, December 31, 2014 ..................... $ 1,524,600

P14–19 Concluded

Indirect method

Mick’s Photographic Equipment Statement of Cash Flows

For the Year Ended December 31, 2014 Cash flows from operating activities: Net income .............................................................. $ 728,140 Adjustments: Increase in accounts receivable ......................... $ (380,000) Increase in inventory .......................................... (630,000) Increase in prepaid insurance ............................ (60,000) Decrease in premium on bonds payable ........... (140) Increase in accounts payable............................. 925,000 Increase in miscellaneous payables .................. 75,000 Depreciation expense......................................... 140,000 Bad debt expense .............................................. 70,400 Unrealized loss on mkt. securities ..................... 25,000 Total adjustments .......................................... 165,260 Net cash increase (decrease) due to operating activities ............................... $ 893,400 Cash flows from investing activities: Purchase of marketable securities ......................... $ (250,000) Purchase of fixed assets ......................................... (750,000) Net cash increase (decrease) due to investing activities ........................................... (1,000,000) Cash flows from financing activities: Proceeds from bond issue ...................................... $ 29,200 Proceeds from preferred stock issue ...................... 102,000 Proceeds from common stock issue....................... 1,500,000 Net cash increase (decrease) due to financing activities ........................................... 1,631,200 Net increase in cash ..................................................... $ 1,524,600 Beginning cash balance, January 1, 2014 .................... 0 Ending cash balance, December 31, 2014 ................... $ 1,524,600

ID14–1

a. Quality of earnings and earnings persistence have to do with the sustainability of the earnings as well as nearness of the earnings to the cash generated by operating activities. The indirect method of preparing the statement of cash flows is especially helpful in spotting the noncash adjustments to net income. This information helps investors identify the companies that use aggressive accounting choices, since the magnitude of such adjustments, in general, would be higher in these cases.

b. In the case of Mattel, the changes in accounts receivable were certainly positive, which indicated

that the majority of the sales were on credit with no contributions to cash. The change in the inventory could have been attributed to either: 1. matching the old production and currents sales or 2. purchasing new inventory on credit. Similarly, an increase in deferred taxes and translation gains would indicate no related cash effect except an adjustment to earnings due to (i.e., changes in tax rates) and foreign currency exchange rates.

c. Wall Street firms employ various models to identify over- and under-valued stocks. The choice of

accounting policies by a firm is just one variable in the whole equation. Therefore, the choice of accounting policy may have some explanatory power, but alone it would not provide sufficient information to differentiate among the stocks.

ID14–3

a. The capitalization and matching process is not very useful for assessing the cash available to a company because disbursing cash and consuming an item are two very different concepts. In order to measure performance, it is necessary to match the costs that were incurred to generate benefits against the benefits. Under accrual accounting, costs should be capitalized if they are expected to provide benefits in the future. Thus, when a company disburses cash to acquire an item expected to provide a future benefit, the company should capitalize the cost of the item as an asset. As the company uses the item over time to help generate revenue, the item will be expensed and matched against the revenue it helped generate. Thus, through the process of capitalizing costs and then expensing them when the cost helps generate revenue, revenues and expenses are closely matched. In this manner, the capitalization and matching process make it difficult to assess a company’s cash performance.

b. Solvency refers to a company’s ability to pay its obligations as they come due, and earning

power refers to a company’s ability to generate net assets through operating activities. The two concepts are closely related in that a company will not remain solvent if it is unable to generate net assets through operations. That is, a company cannot stay in business indefinitely if its operations fail to generate sufficient net assets to allow the company to pay back debt or pay dividends. Similarly, a company will not have very good earning power if it is not solvent. If a company is having solvency problems, it will have to divert cash away from operations and toward paying creditors.

Information that is useful for assessing a company’s solvency can be found in both the balance sheet and statement of cash flows. The balance sheet lists the company’s obligations and the assets currently available to the company to use to pay off the liabilities. In addition, the balance sheet indicates which liabilities are expected to mature in the near future and which assets are more liquid. The statement of cash flows provides information about where the company is getting its cash and how it is using it. Of particular interest is the net cash generated or used by operating activities.

The income statement is the primary source to assess a company’s earning power. Net income represents the net assets the company generated during the year from operations. By comparing net income to certain balance sheet amounts, such as average stockholders’ equity

or average total assets, one can assess how effectively a company is using its assets to generate returns.

c. Bankruptcies usually imply that a company was unable to pay its debts. Because cash is the

most common medium of exchange in the United States, creditors expect to receive interest and principal payments in cash. Thus, a wave of bankruptcies implies that companies were having cash flow problems, which, in turn, increases interest in assessing nonbankrupt companies’ cash flows to avoid other problem loans.

ID14–9

a. Starbucks has been incredibly consistent in its generation of cash from operating activities over the time period. It has used this cash to open additional stores (cash from investing activities) and has still had excess balances allowing it to repay debt and return cash to shareholders.

b. The heavy use of cash for investing signals this profile as one of a growing company. Starbucks differs from many other growth companies in that it does not have to look to financing sources (debt and/or equity) to fund the investments; the operations are strong enough to provide the funding for the growth.

c. At this point the company is quite strong. Fast growth can often hurt companies, but Starbucks

is not leveraging up its balance sheet or diluting its existing owners to fund the growth. The consistent cash flow from operations given the economic climate of the Great Recession and the relatively soft economic recovery is quite impressive.

d. At some point, the company’s growth will slow, meaning that the use of cash for investing will

not be as much a drag for the company. If operations remain strong, the company might divert the cash (that in other years would have gone to new stores) to shareholders in the form of larger dividends or increased share repurchases. On the negative side, if the operations face increased competition (from competitors such as McDonald’s, from new coffee chains or from substitution products if the coffee fad fades), cash flow could decrease and limit the company’s ability to grow and return cash to its financiers.