Chapter 3 Income Sources ©2007 South-Western Kevin Murphy Mark Higgins Kevin Murphy Mark Higgins.

Upload

roxanne-tuckerCategory

view

230download

2

Chapter 10Chapter 10

Cost Recovery on Property: Depreciation, Depletion, and

Amortization

Cost Recovery on Property: Depreciation, Depletion, and

Amortization

©2008 South-Western©2008 South-Western©2008 South-Western©2008 South-Western

Kevin MurphyKevin MurphyMark HigginsMark Higgins

Kevin MurphyKevin MurphyMark HigginsMark Higgins

Transparency 10-2Transparency 10-2© 2008 South-Western © 2008 South-Western

Concept ReviewConcept Review

The capital recovery concept allows a taxpayer to recover all invested capital before income is taxedAn asset’s basis is the maximum

investment that qualifies as capital for recovery

Legislative grace allows the capital to be recovered systematically over the life of the asset

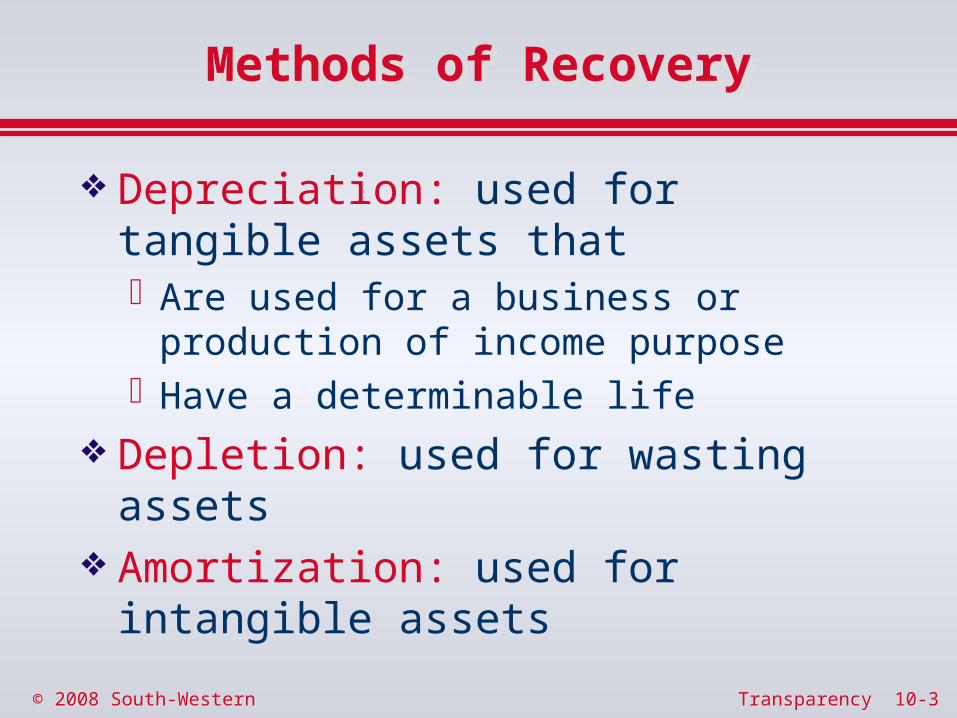

Transparency 10-3Transparency 10-3© 2008 South-Western © 2008 South-Western

Methods of RecoveryMethods of Recovery

Depreciation: used for tangible assets that Are used for a business or production of

income purposeHave a determinable life

Depletion: used for wasting assets Amortization: used for intangible assets

Transparency 10-4Transparency 10-4© 2008 South-Western © 2008 South-Western

History of DepreciationHistory of Depreciation

Based on facts and circumstances related to asset life and taxpayer’s

situation

ACRSBased on method and life

prescribed by law

MACRSBased on method and life

prescribed by law; less accelerated than ACRS

1981 1987

Section 179 Electionto Expense Assets

Transparency 10-5Transparency 10-5© 2008 South-Western © 2008 South-Western

Section 179 ElectionSection 179 Election

Promotes administrative convenience Treated as a depreciation deduction

A taxpayer may elect to expense rather than capitalize qualifying property placed in service during the year.

Transparency 10-6Transparency 10-6© 2008 South-Western © 2008 South-Western

Section 179 ElectionQualifying PropertySection 179 ElectionQualifying Property

Tangible, personal propertyReal estate does not qualify

Used in a trade or businessInvestment property does not qualify

Transparency 10-7Transparency 10-7© 2008 South-Western © 2008 South-Western

Section 179 ElectionDeduction LimitationsSection 179 Election

Deduction Limitations

Limitations apply to each entity Cannot exceed $112,000 Cannot exceed taxable income from the

businessExcess may be carried forward

Transparency 10-8Transparency 10-8© 2008 South-Western © 2008 South-Western

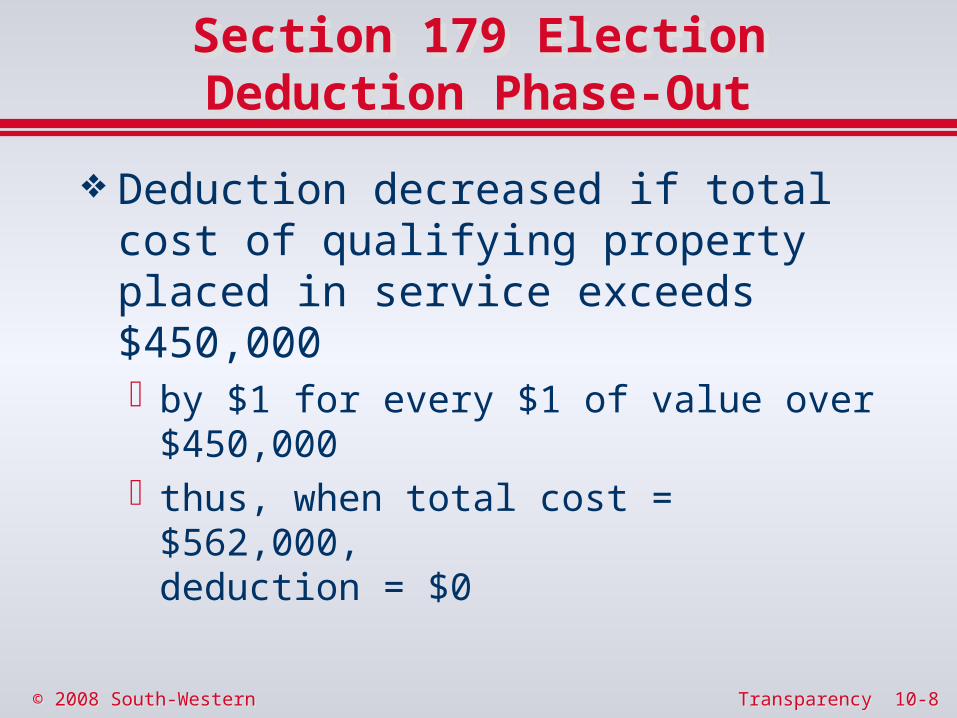

Section 179 ElectionDeduction Phase-OutSection 179 ElectionDeduction Phase-Out

Deduction decreased if total cost of qualifying property placed in service exceeds $450,000by $1 for every $1 of value over $450,000thus, when total cost = $562,000,

deduction = $0

Transparency 10-9Transparency 10-9© 2008 South-Western © 2008 South-Western

MACRSQualifying Property

MACRSQualifying Property

MACRS applies to New and used tangible, depreciable

propertyUsed in a trade or business or for the

production of income

Transparency 10-10Transparency 10-10© 2008 South-Western © 2008 South-Western

MACRSBasis

MACRSBasis

Depreciable basis is The asset’s original basis for depreciation

(discussed in Chapter 9)Reduced by any § 179 deduction

Adjusted basis is The remaining unrecovered capital of an

asset = asset basis minus accumulated depreciation

Transparency 10-11Transparency 10-11© 2008 South-Western © 2008 South-Western

MACRSRecovery Period

MACRSRecovery Period

Each asset must be placed in a MACRS class according to its class lifeMost personal property is in a 3, 5, or 7

year classMost land improvements and specialized

property are in a 10, 15, or 20 year class Real estate is in a 27.5, 31.5, or 39 year

class

Transparency 10-12Transparency 10-12© 2008 South-Western © 2008 South-Western

MACRSConventions

MACRSConventions

For administrative convenience, three assumptions are made about the time property was placed in service during the yearMid-year convention applies to all property

except real estateMid-month convention applies to real estate

onlyMid-quarter convention applies to some

personal property

Transparency 10-13Transparency 10-13© 2008 South-Western © 2008 South-Western

Mid-Year ConventionMid-Year Convention

Assumes property is placed in service and will be disposed of at the mid-point of the yearOne-half year depreciation allowed in the

first year of serviceOne-half year depreciation allowed in the

last year of service

IRS tables reflect the mid-year adjustment only for the first year

Transparency 10-14Transparency 10-14© 2008 South-Western © 2008 South-Western

Mid-Month ConventionMid-Month Convention

Assumes property is placed in service and will be disposed of at the mid-point of a monthOne-half month allowed at the beginningOne-half month allowed at disposition

IRS tables reflect the adjustment only for acquisition

Transparency 10-15Transparency 10-15© 2008 South-Western © 2008 South-Western

Mid-Quarter ConventionMid-Quarter Convention

If > 40% of the total depreciable basis of all personal property is placed in service during the 4th quarter of the year, mid-quarter:Assumes property is placed in service and

will be disposed of at the mid-point of a quarter rather than at mid-year

Determine the 40% after taking §179 expense

Transparency 10-16Transparency 10-16© 2008 South-Western © 2008 South-Western

Depreciation Method Alternatives

Depreciation Method Alternatives

Regular MACRS with Section 179

Straight-line MACRS

Straight-line Alternative Depreciation

System (ADS)

Transparency 10-17Transparency 10-17© 2008 South-Western © 2008 South-Western

Regular MACRSRegular MACRS

Method is double declining balanceIRS tables provide the depreciation rate

Designed to permit full recovery of depreciable basis

Incorporate the conventions

Maximizes acquisition year deduction using the Section 179 election

Transparency 10-18Transparency 10-18© 2008 South-Western © 2008 South-Western

Straight-Line MACRSStraight-Line MACRS

Taxpayers may elect to use the slower straight-line methodElection is made each yearMACRS recovery periods are usedMid-year convention applies

Transparency 10-19Transparency 10-19© 2008 South-Western © 2008 South-Western

Alternative Depreciation System

Alternative Depreciation System

Taxpayers may elect to use ADS Use is mandatory for Alternative

Minimum Taxable Income Uses a longer recovery period than

MACRS Election is made on a class-by-class,

year-by-year basis

Transparency 10-20Transparency 10-20© 2008 South-Western © 2008 South-Western

Limitations on Listed Property

Limitations on Listed Property

Most mixed-use property is considered listed property and subject to special limitationsExamples: automobiles, computers,

cellular phones, etc.

Transparency 10-21Transparency 10-21© 2008 South-Western © 2008 South-Western

Limitations on Listed Property

Limitations on Listed Property

Treatment depends on the percentage of business usageif >50% business use, treated like other

depreciable assetsif < 50% business use, deductions are

limited to ADS without Section 179 In either case, only the business portion of

the asset’s basis is depreciable

Transparency 10-22Transparency 10-22© 2008 South-Western © 2008 South-Western

Limitation on Passenger Autos

Limitation on Passenger Autos

The total amount of depreciation and Section 179 expense that can be deducted is limitedAnnual maximum limit set and linked to the year

the car was placed in serviceAnnual limit is further reduced by the business

use %

Transparency 10-23Transparency 10-23© 2008 South-Western © 2008 South-Western

Adequate Record KeepingAdequate Record Keeping

Listed property is subject to strict record keeping requirements

No deduction is allowed without proof ofWhy? The business purpose of the

useWhat? The amountWhen? The dates of useWhere? The reality of the use

Transparency 10-24Transparency 10-24© 2008 South-Western © 2008 South-Western

DepletionDepletion

The basis of natural resource assets subject to wasting away is recovered using depletion

Basis used is generally fees paid to acquire a lease and the costs of the lease, exploration, and drilling

Computed using two methods Figure both each year and use the largest

as deduction

Transparency 10-25Transparency 10-25© 2008 South-Western © 2008 South-Western

Cost Depletion MethodCost Depletion Method

Allocates unrecovered basis over the number of estimated units of resource

= Depletion per Unit Unrecovered Basis Estimated Recoverable Units

Cost Depletion = Depletion per Unit X # of Units Sold

Transparency 10-26Transparency 10-26© 2008 South-Western © 2008 South-Western

Percentage Depletion Method

Percentage Depletion Method

Depletion is the lesser of50% of taxable income before depletion, orGross income from the sale of the natural

resource times a statutory depletion rate Different statutory % for each type of resource

is given in IRS tables

Transparency 10-27Transparency 10-27© 2008 South-Western © 2008 South-Western

AmortizationAmortization

The basis of intangible assets is recovered using the straight-line method over the life of the asset

Intangible assets acquired through purchase generally use a 15 year life

Created assets and assets specifically excluded from use of the 15 year period are amortized over their legal life