Chap - std setting in Malaysia - updated - apr 13.doc

15

Standard Setting In Malaysia Learning Objectives i. Un de rstand th e devel op me nt of accoun ti ng st an da rds in Mal ay sia. ii . De scr ibe the str ucture an d object ives of Mal ay sian Ac counti ng Standards Board. iii. Desc ribe the structure and objec tives of the Int ernationa l Acc oun ting Sta nda rds Board. iv. E pl ai n th e issues r ela ted to convergence of accounti ng sta ndards . v. E pl ain the relationship be t!ee n Ma la ysian Ac counti ng St an da rds Bo ard to International Accounting Standards Board in relation to convergence of accounting standards. 1.0 Introduction Accounting standards refer to a set of standards stating how particular types of transactions and other events should be reflected in financial statements. These standards are issued by accounting standard setters. The application of accounting standards in the preparation and presentation of financial statements is generally govern by regulatory bodies and/or professional accounting bodies in a particular country. The emergence and development of multinational concerns and the growth of international financial markets, among other factors, are influencing the preparation of financial statements beyond national borders. Many countries around the world that are using their national Genera lly Accep ted Accou nting Principl es GAAP! are adopt ing the "ntern ational #inan cial $eporting %tandards "#$%! in the preparation and presentation of their financial statements. The "#$%s are issued by "nternational Accounting %tandards &oard "A%&! and the adoption of "#$%s is having a growing influence on national accounting re'uirements and practices. This chapter di scu sses the adoption of "#$%s and other asp ects of standar d( set ti ng environment in Malaysia. 2.0 Development of inancial !eporting in Malaysia The demand for corporate information by capital providers and other stakeholders, such as empl oyees, suppli er s, custo mers and ot he r agents has shaped the fi nancial reporti ng env ironme nt in Mal ays ia. The se par tie s re'uir e corporate inf ormati on in mak ing the ir econo mic decisions. The prov ision of corpo rate informatio n to these users has been initi ated by the )inth %chedule of the *ompanies Act +- re'uiring companies to disclose minimum information. #inancial reporting environment has evolved since then and currently companies are disclosing more comprehensive information as a result of considerable efforts by various bodies. #igure + depicts the timing of significant events related to the development of financial reporting in Malaysia. Roshayani Arshad/Accounting Theory Page 1

-

Upload

practikaltranninnng -

Category

Documents

-

view

222 -

download

0

Transcript of Chap - std setting in Malaysia - updated - apr 13.doc

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 1/15

Standard Setting In Malaysia

Learning Objectives

i. Understand the development of accounting standards in Malaysia.

ii. Describe the structure and objectives of Malaysian Accounting Standards Board.

iii. Describe the structure and objectives of the International Accounting Standards

Board.

iv. Eplain the issues related to convergence of accounting standards.

v. Eplain the relationship bet!een Malaysian Accounting Standards Board to

International Accounting Standards Board in relation to convergence of accounting

standards.

1.0 Introduction

Accounting standards refer to a set of standards stating how particular types of transactions

and other events should be reflected in financial statements. These standards are issued by

accounting standard setters. The application of accounting standards in the preparation and

presentation of financial statements is generally govern by regulatory bodies and/or

professional accounting bodies in a particular country.

The emergence and development of multinational concerns and the growth of international

financial markets, among other factors, are influencing the preparation of financial statements

beyond national borders. Many countries around the world that are using their national

Generally Accepted Accounting Principles GAAP! are adopting the "nternational #inancial$eporting %tandards "#$%! in the preparation and presentation of their financial statements.

The "#$%s are issued by "nternational Accounting %tandards &oard "A%&! and the adoption

of "#$%s is having a growing influence on national accounting re'uirements and practices.

This chapter discusses the adoption of "#$%s and other aspects of standard(setting

environment in Malaysia.

2.0 Development of inancial !eporting in Malaysia

The demand for corporate information by capital providers and other stakeholders, such as

employees, suppliers, customers and other agents has shaped the financial reporting

environment in Malaysia. These parties re'uire corporate information in making their

economic decisions. The provision of corporate information to these users has been initiated

by the )inth %chedule of the *ompanies Act +- re'uiring companies to disclose minimum

information. #inancial reporting environment has evolved since then and currently companies

are disclosing more comprehensive information as a result of considerable efforts by various

bodies. #igure + depicts the timing of significant events related to the development of

financial reporting in Malaysia.

Roshayani Arshad/Accounting Theory Page 1

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 2/15

igure 1" #imeframe Depicting Significant $vents !elated to t%e Development of

inancial !eporting In Malaysia.

&eriod inancial !eporting Development

+- )inth %chedule of the *ompanies Act +-( Minimum disclosure of specific information

+ $epresentation on the "nternational Accounting %tandards *ommittee "A%*!

( Adoption of "nternational Accounting %tandards "A%!

( "ssue of Malaysian Accounting %tandards MA%!

+ #inancial $eporting Act + established #inancial $eporting #oundation #$#!

and Malaysian Accounting %tandards &oard MA%&!

( #$#, a trustee body responsible for the oversight of MA%&0s operations

( MA%& is responsible for standard setting in Malaysia

( MA%& issue standards called MA%&, e.g. MA%& 1 Inventories 122 MA%& standards renamed as #$%, e.g. #$% +21 Inventories

12+1 *onvergence of #$%s MA%&! with "#$%s as issued by "A%&!

The provision of corporate information in Malaysia was first mandated by the *ompanies Act

+- re'uirements. %chedule of the *ompanies Act +- re'uires all registered companies

in Malaysia to disclose specific information in their financial statements. 3owever, the format

and content of financial statements are not prescribed by %chedule of the *ompanies Act

+-. As such, only minimum disclosure re'uirements are prescribed by the legislation.

The disclosure of corporate information beyond the minimum statutory disclosure

re'uirements in Malaysia began in + when Malaysia was represented on the "nternational

Accounting %tandards *ommittee "A%*!. The "A%* was set up in +4 and was responsible

for the setting of "nternational Accounting %tandards "A%!. The guidelines issued by the

"A%* were called %tanding "nterpretations *ommittee %"*!. %oon after its representation on

the "A%*, Malaysia began adopting the "A%s. 5hile the adoption of "A%s lead to more

comprehensive disclosure of corporate information, it was not able to meet some local

reporting re'uirements. Accounting and reporting re'uirements for transactions and events in

relation to specific industries such as a'uaculture and insurance were not addressed by the

"A%s. "n meeting the local reporting re'uirements, accounting standards known as Malaysian

Accounting %tandards MA%s! were issued 6ointly by two professional accounting bodies inthe +72s. These bodies were represented by Malaysian "nstitute of Accountants M"A!,

Malaysian Association of *ertified Public Accountants MA*PA!, now known as Malaysian

"nstitute of *ertified Public Accountants M"*PA!. 89amples of these standards are MA% +

Earnings "er Share, MA% - Accounting for #ood!ill and MA% 7 Accounting for "re$

%ropping %osts.

2.1 Malaysian 'ccounting Standards (oard )M'S(*

The standard setting role by M"A and MA*PA was superseded by Malaysian Accounting

%tandards &oard MA%&! in +. MA%& is established under the #inancial $eporting Act

+ #$A +!. The Act was ga:etted on - March +. "n addition to MA%&, the Act also

Roshayani Arshad/Accounting Theory Page 2

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 3/15

created #inancial $eporting #oundation #$#!. The overall responsibility of the #$# is to

oversee the operating activities of the MA%&.

The #$# comprises of nineteen +! members who are appointed by the Minister of #inance.

( seven members are e9(officio representing the Minister of #inance, the *entral &ank,

the %ecurities *ommission, the *ompanies *ommission of Malaysia, the &ursaMalaysia &erhad, the M"A and the MA%&, and

( twelve members representing a broad spectrum of interest groups ( principal officers

of public listed companies, senior partners of public accounting firms and persons with

other relevant e9perience and background.

The responsibilities of the #$# as provided under the #inancial $eporting Act + are as

follows;

i. To provide views to the MA%& on matters which the MA%& seeks to undertake or

implement with respect to the development and issue of accounting standards and

conceptual framework<ii. To review the performance of MA%&<

iii. To be responsible for the financing arrangements and operations of the MA%&<

iv. To approve the MA%& budget<

v. To engage or to employ persons and determine the conditions of such appointments as

are necessary to assist the #$# and MA%& perform their functions under the Act<

vi. To administer the fund established to finance the ongoing operations of #$# and

MA%& including management of funds not e9panded on operations during any period<

vii. To maintain proper accounts and prepare an annual statement of accounts of the #$#<

viii. To forward annual statement of accounts and audit report to the Minister of #inance,

and report on the activities of the #$# and MA%& at the end of each financial year,

and

i9. To perform such other functions as prescribe by the Minister of #inance prescribe.

The functions and powers of the MA%& as provided under the Act are to;

• issue new accounting standards as approved accounting standards and to review,

revise or adopt e9isting accounting standards as approved accounting standards<

• issue statements of principles for financial reporting<

• sponsor or undertake development of possible accounting standards<

• conduct public consultation as necessary<

•

develop a conceptual framework for the purpose of evaluating proposed accountingstandards<

• make such changes to proposed accounting standards as considered necessary<

• seek the view of the #$# in relation to new and e9isting standards, statement of

principles, and changes to proposed standards<

• determine scope and application of accounting standards< and

• to perform such other function as the Minister of #inance may prescribe.

The functions of the MA%& as formulated in its mission statement are as follows;

i. to develop and promote high 'uality accounting and reporting standards that are

consistent with international best practices for the benefit of users, preparers, auditorsand the public in Malaysia, and

Roshayani Arshad/Accounting Theory Page 3

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 4/15

ii. to contribute directly to the international development of financial reporting for the

benefit of users, preparers and auditors of financial reports.

"n fulfilling the above functions, MA%& sets out the following ob6ectives;

• to develop high 'uality, clear and enforceable national accounting standards for

financial reporting that benefit users<• to bring about harmonisation of national accounting standards with international

accounting standards<

• to promote the use and application of those standards by way of communication with

and education of users, preparers, auditors and the public<

• to actively contribute to the development of accounting standards internationally,

including, "slamic(based accounting standards< and

• to promote and support research in the area of financial reporting, in particular, for

emerging markets and "slamic markets.

The members of MA%& are appointed by the Minister of #inance and comprises of the

following members;

( a chairman,

( the Accountant General,

( advisors representing the %ecurities *ommission, *ompanies *ommission of Malaysia

and M"A, and

( si9 other members with e9pertise in accountancy, law, business and finance. "t should

be noted that the #$A + specifies that at least five of these members are members

of M"A.

%ection 1 of the #$A + re'uires all companies incorporated under the *ompanies Act to

comply with accounting standards issued and adopted by the MA%&. Accounting standards

are defined by #$# as statements of standard accounting practices used for the preparation of

financial statements. The MA%& established a committee called "ssues *ommittee and

5orking Groups in dealing with standard(setting related matters.

2.1.1 Issues +ommittee

"ssues *ommittee was established in May 1221, replacing its predecessor, the "nterpretation

*ommittee. The change of name reflects the e9panded scope of the committee which goes

beyond interpretations of approved accounting standards. "n addition to reviewing accounting

issues that have received or are likely to receive divergent views in interpretation, "ssues*ommittee also deals with other accounting related issues where there is no e9isting

accounting standard.

The committee comprises representatives from the accounting profession, commerce, the

academia as well as an analyst and a solicitor. =bserver representatives from M"A, %ecurities

*ommission, &ank )egara Malaysia and *ompanies *ommission of Malaysia also form part

of the committee.

2.1.2 ,or-ing roup

The MA%& has established numerous 5orking Groups which are assigned with different pro6ects. 8ach working group is responsible for reviewing and undertaking detailed studies of

Roshayani Arshad/Accounting Theory Page 4

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 5/15

the assigned pro6ect, taking into accounts any statutory and regulatory reporting re'uirements

as well as its practical implications. A 5orking Group must be chaired by a member of the

MA%&. =ther group members include a pro6ect manager and representatives from the

accounting profession, commerce, academia as well as regulatory authorities.

The works undertaken by 5orking Groups play an important role in the development of theMA%& standards. The MA%&0s due process for developing a standard is summarised in

#igure 1.

igure 2" M'S( Due &rocess

+. MA%& "dentifies "A% for review.

1. 5orking Group Prepares >iscussion Paper >P!.

4. MA%& $eview >P.

?. #$# $eview >P.

. MA%& #inalises >P into 89posure >raft 8>!.

-. Public Public e9posure of 8>.

. 5orking Group Prepare report on feedback received on 8>.

7. MA%& $eview feedback on 8>.

. #$# #inal review of feedback on 8>.

+2. MA%& Approval of MA%& standard followed by issue of MA%&standard.

Prior to the creation of MA%&, Malaysia has already adopted the "A%s issued by the "A%*

and MA%s issued by the *ouncil of M"A and M"*PA. @pon its creation, MA%& adopted

most of these standards which gave these standards the status of approved accounting

standards. These standards were referred to as MA%& standards. 5ith the e9ception of the

adopted MA%s, the MA%& standards were in substance similar to the "A%s.

"n April 122+, the international standard setting role of "A%* was superseded by the "A%&

and subse'uently the "A%& began issuing "nternational #inancial $eporting %tandards "#$%!.At this point in time, all "A%s issued by the "A%* remained in force until amended or

withdrawn by the new "#$% issued by "A%&. "n line with this development, MA%& standards

have been renamed to #inancial $eporting %tandards #$%! in 122. The numbering of the

#$%s corresponds to the "#$%s issued by the "A%&. #or e9ample, #$% + in Malaysia is

e'uivalent to "#$% +. #$% with a +22 prefi9 corresponds to its e'uivalent "A%s. Thus #$%

+2+ is e'uivalent to "A% +. #$% with a 122 prefi9 represents locally developed %tandard with

no e'uivalent "nternational %tandard.

"n addition to the accounting standards, the "A%& has also issued the #ramework for the

Preparation and Presentation of #inancial %tatements. The MA%& adopted similar #ramework

known as the #$% #ramework. "n )ovember 12++, the MA%& issued a new approvedaccounting framework, the Malaysian #inancial $eporting %tandards M#$% #ramework!.

Roshayani Arshad/Accounting Theory Page 5

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 6/15

*ompliance with M#$% #ramework is effective on + anuary 12+1. The M#$% #ramework is

to be applied by all 8ntities =ther Than Private 8ntities, with the e9ception of entities that are

within the scope of M#$% +?+ Agriculture M#$% +?+! and "* "nterpretation + Agreements

for %onstruction of &eal Estate "* +!, including its parent, significant investor and venturer.

The accounting standards under the new framework is known as M#$% standards. The list of

M#$% standards effective on + anuary 12+1 are shown in #igure 4 below.

igure /" List of M!S Standards

#itle of M!Ss

M#$% + #irst(time Adoption of "nternational #inancial $eporting %tandards

M#$% 1 %hare(based Payment

M#$% 4 &usiness *ombinations

M#$% ? "nsurance *ontracts

M#$% )on(current Assets 3eld for %ale and >iscontinued =perations

M#$% - 89ploration for and 8valuation of Mineral $esources

M#$% #inancial "nstruments; >isclosures

M#$% 7 =perating %egments

M#$% #inancial "nstruments

M#$% +2+ Presentation of #inancial %tatements

M#$% +21 "nventories

M#$% +2 %tatement of *ash #lows

M#$% +27 Accounting Policies, *hanges in Accounting 8stimates and 8rrors

M#$% ++2 8vents After the $eporting Period

M#$% +++ *onstruction *ontracts

M#$% ++1 "ncome Ta9es

M#$% ++- Property, Plant and 8'uipment

M#$% ++ Beases

M#$% ++7 $evenue

M#$% ++ 8mployee &enefits

M#$% +12 Accounting for Government Grants and >isclosure of Government Assistance

M#$% +1+ The 8ffects of *hanges in #oreign 89change $ates

M#$% +14 &orrowing *osts

Roshayani Arshad/Accounting Theory Page 6

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 7/15

M#$% +1? $elated Party >isclosures

M#$% +1- Accounting and $eporting by $etirement &enefit Plans

M#$% +1 *onsolidated and %eparate #inancial %tatements

M#$% +17 "nvestments in Associates

M#$% +1 #inancial $eporting in 3yperinflationary 8conomies

M#$% +4+ "nterests in oint Centures

M#$% +41 #inancial "nstruments; Presentation

M#$% +44 8arnings per %hare

M#$% +4? "nterim #inancial $eporting

M#$% +4- "mpairment of AssetsM#$% +4 Provisions, *ontingent Biabilities and *ontingent Assets

M#$% +47 "ntangible Assets

M#$% +4 #inancial "nstruments; $ecognition and Measurement

M#$% +?2 "nvestment Property

M#$% +?+ Agriculture

"n addition to the above standards, the MA%& started a pro6ect on "slamic financial reportingin +. "n 122+, the board issued MA%& i(+ later re(numbered #$% i(+!, "resentation of

'inancial Statements of Islamic 'inancial Institutions. 3owever, this standard was

subse'uently withdrawn as the MA%& ceased its policies of issuing "slamic accounting

standards. The MA%& is of the opinion that such standards are largely similar to the current

standards in issue. "n line with this, the MA%& issued %tatement of Principles i(+ %=P i(+!,

#inancial $eporting from an "slamic Perspective on + %eptember 122. %=P i(+ affirm% that

MA%& approved accounting standards shall apply to %hariah compliant financial transactions

and events, unless there is a %hariah prohibition.

2.1./ #ec%nical &ronouncements

"n addition to issuing standards, the MA%& may also issue technical pronouncements such as

%tatement of Principles %=P!, Technical $eleases T$! and "nterpretation &ulletin. The

purpose of a technical pronouncement is to provide guidance on the application of generally

accepted accounting principles. "n some instances, the issue of a pronouncement represents an

interim measure prior to the issue of a particular standard. "t should be noted that the technical

pronouncements do not amend or overide MA%& %tandards or other statements issued by the

MA%&.

89amples of technical pronouncements that have been issued are as follows;

#itle $ffective Date Summary

Roshayani Arshad/Accounting Theory Page 7

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 8/15

T$ 1 The Dear 1222 "ssue ; Accounting and >isclosure 4+ uly +7

T$ 4 Guidance on >isclosures of Transition to "#$%s 4+ >ecember 12+2

T$ i ( + Accounting for Eakat on &usiness + uly 122-

T$ i ( 1 "6arah + uly 122-

T$ i ( 4Presentation of #inancial %tatements of "slamic

#inancial "nstitutions+ an 12+2

T$ i ( ? %hariah *ompliant %ale *ontracts + an 12++

/.0 International 'ccounting Standards

=n + August 1227, MA%& issued a statement with regards to its plan for full convergence of

#$%s applicable in Malaysia with "#$%s issued by "A%& by the year 12+1 for all entitiesother than private entities. #ull convergence refers to full compliance with "#$% as a basis for

financial reporting system in Malaysia. "n moving towards full convergence, MA%&

participates actively in the "A%&0s due process at an early stage of standard development.

This is important in ensuring that the standards adopted are consistent with international best

practice as well as regulatory re'uirements in Malaysia. Active participation by MA%& started

since "A%& began its international due process in 122+.

/.1.1 #%e International 'ccounting Standards (oard )I'S(*

The "A%& is an independent and privately(funded accounting standard(setting body. The

standard setting responsibilities was assumed from its predecessor the "A%* in 122+,following the restructuring of the "A%*. The "A%* oversees the operations of the "A%& and

promotes adoption of "#$%s around the world. 3owever, the technical aspects related to the

"#$%s lies with the "A%&. The "A%& is responsible for the development and publication of

"#$%s, including the "#$% for %M8s and for approving "nterpretations of "#$%s as developed

by the "#$% "nterpretations *ommittee formerly called the "#$"*!. To bring about

convergence of national accounting standards and "#$%s, the "A%& engages closely with

stakeholders around the world. The various stakeholders include investors, analysts,

regulators, business leaders, accounting standard(setters and the accounting profession.

The ob6ectives of the "A%& as set out in its constitution;

• to develop, in the public interest, a single set of high 'uality, understandable and

enforceable global accounting standards that re'uire high 'uality, transparent and

comparable information in financial statements and other financial reporting to help

participants in the world0s capital markets and other users make economic decisions<

• to promote the use and rigorous application of those standards<

• in fulfilling the ob6ectives associated with a! and b!, to take account of, as

appropriate, the special needs of small and medium(si:ed entities and emerging

economies< and

• to bring about convergence of national accounting standards and "#$%s to high 'uality

solutions.

Roshayani Arshad/Accounting Theory Page 8

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 9/15

The main features of the "A%& structure are as follows;

i. The "A%* #oundation also known as "#$% #oundation! has two main bodies,

the Trustees and the "A%&. The overall ob6ective of the "A%* #oundation is to

develop a set of high 'uality, understandable, enforceable and globally

accepted financial reporting standards through its standard setting body, the"A%&.

ii. The "A%& is responsible for setting accounting standards.

iii. %tandards Advisory *ouncil and "#$% "nterpretations *ommittee are two other

bodies within the "A%& structure.

The structure of the "A%& is as shown in #igure ?.

igure " Structure of I'S(

#rustees

Members of the trustees must be selected from the Asia/=ceania region si9 members!,

8urope si9 members!, )orth America si9 members!, Africa one member!, %outh

America one member! and the remaining parts of the world two members!. The trustees

are accountable to the Monitoring &oard of public authorities and are entrusted with the

governance and oversight of the activities undertaken by the "A%* #oundation and "A%&.

The "A%& strategy will be reviewed and assessed annually by the trustees. The trustees are

also responsible for safeguarding the independence of the "A%&, ensuring the financing ofthe organisation and the appointment of the "A%& members. Members of the "A%&

Roshayani Arshad/Accounting Theory Page 9

IASC Foundation

IASB

Standard Advisoryounci! "nter#retation o$$ittee

%or&ing 'rou#

(eyA##oints

Re#orts toAdvises

Trustees o) "AS *oundation

+onitoring ,oardo) #u-!ic authorities

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 10/15

comprise of e9perts with an appropriate mi9 of recent practical e9perience of standard(

setting, or of the user, accounting, academic or preparer communities. At the same time, the

trustees promote the work of the "A%& and the application of "#$%s. 3owever, they are not

involved in the technical aspects of the matters relating to accounting standards as these

aspects are the responsibilities of the "A%&. =ther responsibilities of the trustees also

include amending the operating procedures, consultative arrangements and due process forthe "A%&, the "nterpretations *ommittee and the Advisory *ouncil<

#%e I!S Interpretations +ommittee

The "#$% "nterpretations *ommittee formerly called the "#$"*! is the interpretative body of

the "A%&. The members are appointed by the Trustees and drawn from a variety of countries

and professional backgrounds. The *ommittee provides timely guidance on accounting issues

that have arisen within the conte9t of current "#$%s and to provide authoritative

guidance )"#$"*s! on those issues.

Standards 'dvisory +ouncil

Members of the *ouncil comprise groups and individuals with diverse geographic andfunctional backgrounds. They advise the Trustees and "A%& on all ma6or pro6ects.

I'S( Due &rocess

The due process, which involves interested individuals and organisations from around the

world comprises of si9 stages. These stages are;

+. %etting the agenda. The main consideration of the "A%& in deciding whether a

particular item is to be included in its agenda is based on whether such item will add

value to the needs of the investors.

1. Planning the pro6ect. =nce a new agenda is established, the "A%& will consider

whether the pro6ect will be conducted alone or with other standard(setter. At this stage,

a working group will be established.

4. >eveloping and publishing the discussion paper . The development and publication of

the discussion paper can arise from an active agenda pro6ect of the "A%& or a research

pro6ect conducted by another standard setter. 8ven though the discussion paper is not

mandatory, it is usual for "A%& to publish it as its first publication with the ob6ective

of e9plaining the issue and solicit views from various constituents. "ssues in the

discussion paper are discussed in the "A%& meeting. %ubse'uently, any technical

issues in the discussion paper are discussed in the public session.

?. >eveloping and publishing the e9posure draft. "n contrast to discussion paper, the

development and publication of the e9posure draft is mandatory step in the due process of the "A%&. The development of a particular e9posure draft takes into

account various issues, comments and suggestions received from various parties. =nce

these matters are resolved at the "A%& meeting, an e9posure draft will be drafted. "t

sets out a proposed standard or amendment to an e9isting standard and this will be

issued for public comments.

. >eveloping and publishing the standard. =nce the "A%& received the views from the

public on a particular e9posure draft, a meeting will be held and the "A%& will

consider whether a re(e9posure is necessary. "f all the issues raised are concluded

satisfactorily, the "A%& will instruct its staff to draft the relevant "#$%.

-. After the standard is issued, the "A%& will hold regular meetings with various parties

in order to understand issues related to the practical implementation of the "#$% andany impact of the "#$%. 8ducational activities are also carried out by the "A%*

Roshayani Arshad/Accounting Theory Page 1.

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 11/15

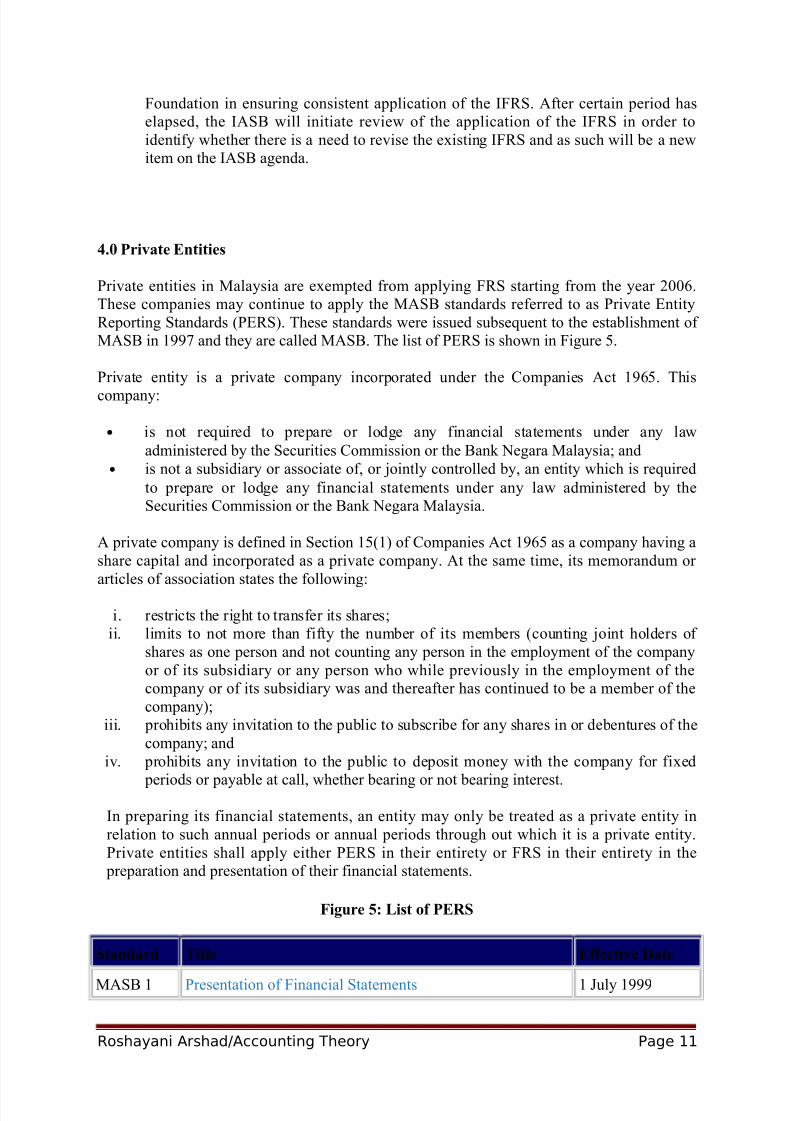

#oundation in ensuring consistent application of the "#$%. After certain period has

elapsed, the "A%& will initiate review of the application of the "#$% in order to

identify whether there is a need to revise the e9isting "#$% and as such will be a new

item on the "A%& agenda.

.0 &rivate $ntities

Private entities in Malaysia are e9empted from applying #$% starting from the year 122-.

These companies may continue to apply the MA%& standards referred to as Private 8ntity

$eporting %tandards P8$%!. These standards were issued subse'uent to the establishment of

MA%& in + and they are called MA%&. The list of P8$% is shown in #igure .

Private entity is a private company incorporated under the *ompanies Act +-. This

company;

• is not re'uired to prepare or lodge any financial statements under any law

administered by the %ecurities *ommission or the &ank )egara Malaysia< and

• is not a subsidiary or associate of, or 6ointly controlled by, an entity which is re'uired

to prepare or lodge any financial statements under any law administered by the

%ecurities *ommission or the &ank )egara Malaysia.

A private company is defined in %ection ++! of *ompanies Act +- as a company having a

share capital and incorporated as a private company. At the same time, its memorandum or

articles of association states the following;

i. restricts the right to transfer its shares<

ii. limits to not more than fifty the number of its members counting 6oint holders of

shares as one person and not counting any person in the employment of the company

or of its subsidiary or any person who while previously in the employment of the

company or of its subsidiary was and thereafter has continued to be a member of the

company!<

iii. prohibits any invitation to the public to subscribe for any shares in or debentures of the

company< and

iv. prohibits any invitation to the public to deposit money with the company for fi9ed

periods or payable at call, whether bearing or not bearing interest.

"n preparing its financial statements, an entity may only be treated as a private entity in

relation to such annual periods or annual periods through out which it is a private entity.

Private entities shall apply either P8$% in their entirety or #$% in their entirety in the

preparation and presentation of their financial statements.

igure " List of &$!S

Standard #itle $ffective Date

MA%& + Presentation of #inancial %tatements + uly +

Roshayani Arshad/Accounting Theory Page 11

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 12/15

MA%& 1 "nventories + uly +

MA%& 4 )et Profit or Boss for the Period, #undamental 8rrors and

*hanges in Accounting Policies+ uly +

MA%& ? $esearch and >evelopment *osts + uly +

MA%& *ash #low %tatements + uly +

MA%& - The 8ffects of *hanges in #oreign 89change $ates + uly +

MA%& *onstruction *ontracts + uly +

MA%& $evenue + an 1222

MA%& +2 Beases + an 1222

MA%& ++*onsolidated #inancial %tatements and "nvestments in

%ubsidiaries + an 1222

MA%& +1 "nvestments in Associates + an 1222

MA%& +? >epreciation Accounting + uly 1222

MA%& + Property, Plant F 8'uipment + uly 1222

MA%& +- #inancial $eporting of "nterests in oint Centure + uly 1222

MA%& + 8vents after the &alance %heet >ate + uly 122+

MA%& 12 Provisions, *ontingent Biabilities F *ontingent Assets + uly 122+

MA%& 14 "mpairment of Assets + an 1221

MA%& 1 "ncome Ta9es + uly 1221

MA%& 1 &orrowing *osts + uly 1221

MA%& 17 >iscontinuing =perations + an 1224

MA%& 1 8mployee &enefits + an 1224

MA%& 42 Accounting and $eporting by $etirement &enefit Plans + an 1224

MA%& 4+ Accounting for Government Grants and >isclosure ofGovernment Assistance

+ an 122?

MA%& 41 Property >evelopment Activities + an 122?

"A% 1 Accounting for "nvestments + %ept +7

"A% 1 #inancial $eporting in 3yperinflationary 8conomies + an 1224

MA% Accounting for A'uaculture + %ept +7

"&(+ Preliminary and Pre(operating 89penditure + an 122+

Roshayani Arshad/Accounting Theory Page 12

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 13/15

.0 +onvergence of 'ccounting Standards

*urrently, the top global capital markets that re'uire or permit the use of "#$% are;

a! @nited ingdom<

b! #rance<c! Germany<

d! 3ong ong<

e! %pain<

f! %wit:erland<

g! Australia.

"n Malaysia, all entities that are re'uired to comply with approved accounting standards under

the #inancial $eporting Act + will be re'uired to prepare and present their financial

statements in accordance to the "#$%s, e9cept for private entities. #ull compliance begins on

or after anuary +, 12+1. "n moving towards this, the MA%& issued a new MA%& approved

accounting framework, the Malaysian #inancial $eporting %tandards M#$% #ramework! in )ovember 12++. The new famework is effective on + anuary 12+1 and it comprises

new/revised accounting standards issued by the "A%& that was effective after + anuary 12+1.

#inancial statements prepared in compliance with this framework is a fully "#$%(compliant

framework and e'uivalent to "#$%s.

.1 (enefits of +onvergence

The benefits of convergence based on the benefits to various users of financial statements can

be summarised as follows;

i. "nvestors

( "ncrease comparability of financial information across borders as well as among

companies nationally in making investment decisions.

( "ncrease transparency.

( Greater understandabiliy.

ii. Multinational companies

( &etter access to foreign capital markets.

( "ncrease credibility of domestic capital markets to foreign capital providers.

( #acilitate compliance with reporting re'uirements of foreign stock e9changes,

( #acilitate preparation and presentation of financial statements as companies are onlyre'uired to maintain one set of books prepared in compliance with "#$%s.

( Bower cost of capital to companies.

iii. $egulatory bodies

( 8ase of regulation of securities market as convergence increases regulatory

acceptability of financial information provided by market participants.

( $educed costs of national standard setters.

( #acilitate calculation of ta9 liability for companies receiving income from

international sources.

( Transfer of accounting staffs across borders as similar accounting practices e9isted

worldwide.( Promote economic growth within region practicing common accounting practices.

Roshayani Arshad/Accounting Theory Page 13

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 14/15

.2 +%allenges of +onvergence

The challenges of convergence include;

( Application of similar "#$%s may not be appropriate as the purpose of financial

reporting differs across countries. #or e9ample, in countries where the legal system is based on $oman Baw, the financial statements are prepared for ta9 assessment while

in other countries the information is for investor decision(making.

( >ifferent legal system can hinder development of certain accounting practices.

( >ifferent in culture may affect variations in ob6ectives of accounting systems.

( Back of professional e9pertise due to lack of strong accountancy bodies in certain

countries.

( >ifferent emphasis on user groups. #or instance, investors and creditors are important

in the @%A, employees are important in 8urope while in many 8ast Asian countries

where corporate ownerships are more concentrated, there are lower investor

protection.

( >evelopment of standards and principles in developing countries are not at par withthe developed countries. This could slower the rate of full convergence in some

countries.

( )ational standards in some countries are not based on a conceptual framework of

accounting while "#$%s are.

.0 Summary

$eliable and transparent financial reporting is paramount to support the decision(making by

investors, lenders and regulatory authorities. "n meeting the needs of various users, there is a

need to develop and issue accounting standards that are of high 'uality, transparent and

comparable in the preparation of financial statements. The current move is through the

adoption of "#$%s by countries around the world. The "A%& is responsible for setting and

issuing the "#$%s. "n ensuring the success of full convergence, the work of national standard

setters and the "A%& should be integrated. "n Malaysia, the MA%& actively participates in the

"A%&0s due process at an early stage of standard development. "n line with the MA%&0s

convergence effort in 12+1, the board issued a new MA%& approved accounting framework,

the Malaysian #inancial $eporting %tandards M#$% #ramework! in )ovember 12++. The

new famework is effective on + anuary 12+1 and it comprises new/revised accounting

standards issued by the "A%& that was effective after + anuary 12+1. *ompliance with this

framework facilitates companies in Malaysia to prepare their financial statements in

accordance to "#$%s as the new framework is a fully "#$%(compliant framework ande'uivalent to "#$%s.

3uestions

+. 89plain the development of accounting standards in Malaysia.

1. >escribe the structure and ob6ectives of Malaysian Accounting %tandards &oard.

4. 5hat is the difference between "nternational Accounting %tandards and "nternational

#inancial $eporting %tandardsH

?. Bist some of the benefits and challenges to convergence.

Roshayani Arshad/Accounting Theory Page 14

7/27/2019 Chap - std setting in Malaysia - updated - apr 13.doc

http://slidepdf.com/reader/full/chap-std-setting-in-malaysia-updated-apr-13doc 15/15

. "n some countries, income reported to investors differ from income prepared for ta9

calculations. >iscuss whether these income should be identically determined through the

application of "nternational #inancial $eporting %tandards.

-. %tandard setting approaches in countries may differ. >iscuss how these difference affect

the acceptance of compliance with "nternational #inancial $eporting %tandards.

Roshayani Arshad/Accounting Theory Page 15