Chap 002 slides

40

Consolidation Consolidation of Financial of Financial Information Information McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc !ll rights reser"e#

-

Upload

alaaeqahwajii -

Category

Documents

-

view

234 -

download

0

Transcript of Chap 002 slides

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 1/40

ConsolidationConsolidation

of Financialof Financial

InformationInformation

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc !llrights reser"e#

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 2/40

A business combination occurs when

two or more separate businesses joininto a single accounting entity.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 3/40

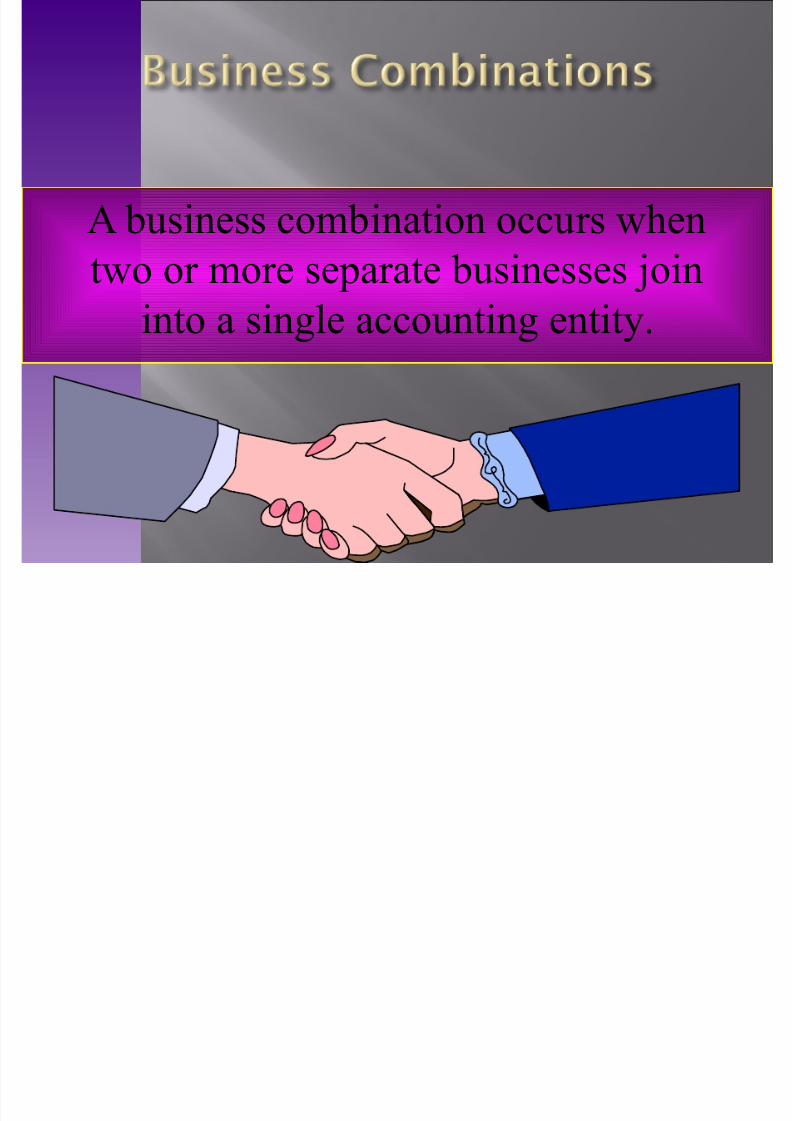

Cost advantage Finding New Facilities Human resources Side-

Research evelopment .

!ower ris" # purchase new products and mar"ets less ris"y $han trying to

develops new mar"et %new products. $his help Company to Reduce ris"

by diversi&y their investment in di&&erent products

Fewer operating delays- '(isting )usiness reduce delays operation#

)ecause *overnment regulation inspection % many things you have to do

+n order to start your business. $his will ,inimie operation delays.

Avoidance o& ta"eovers. #small companies a&raid big Com. aggressive in )uying other small business# to de&end their companies against

ta"eover )y bid Companies

Acuisition o& intangible assets # )usiness combinations bring both

$angible and intangible resources /atent% management '(pertise researchcustomer data base 0ther reason ta( Advanta es savin

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 4/40

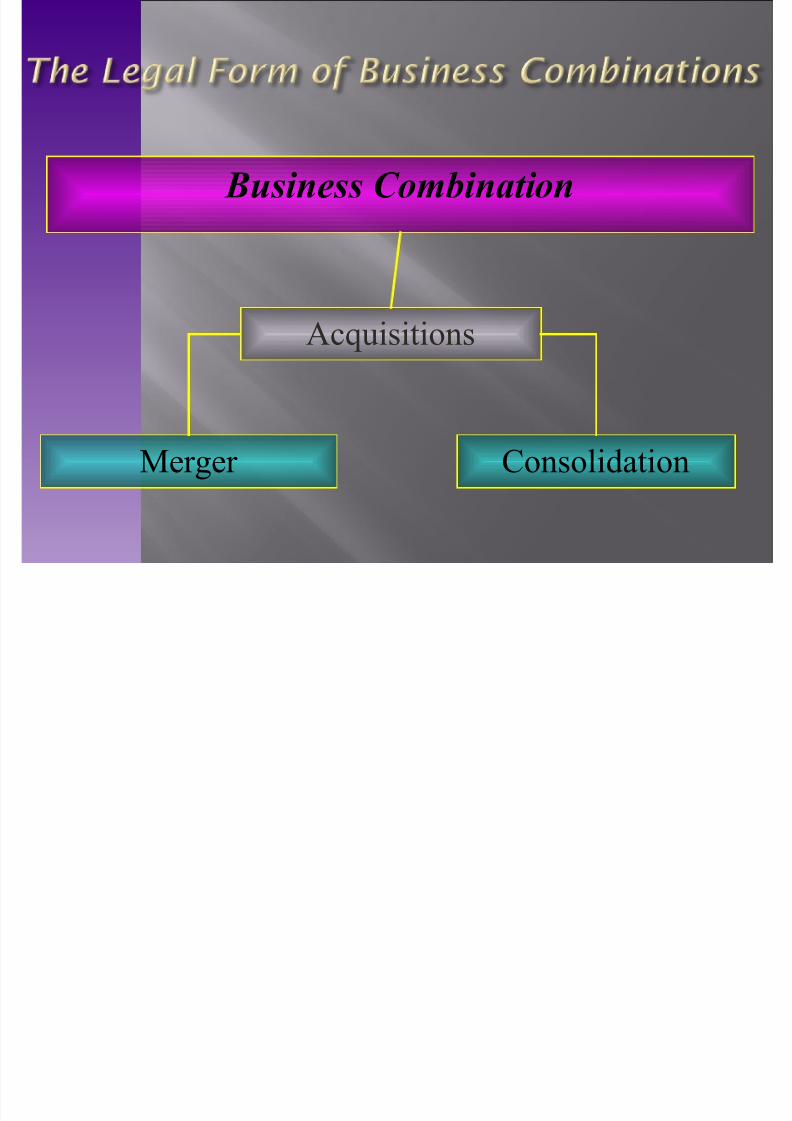

Business Combination

,erger

Acuisitions

Consolidation

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 5/40

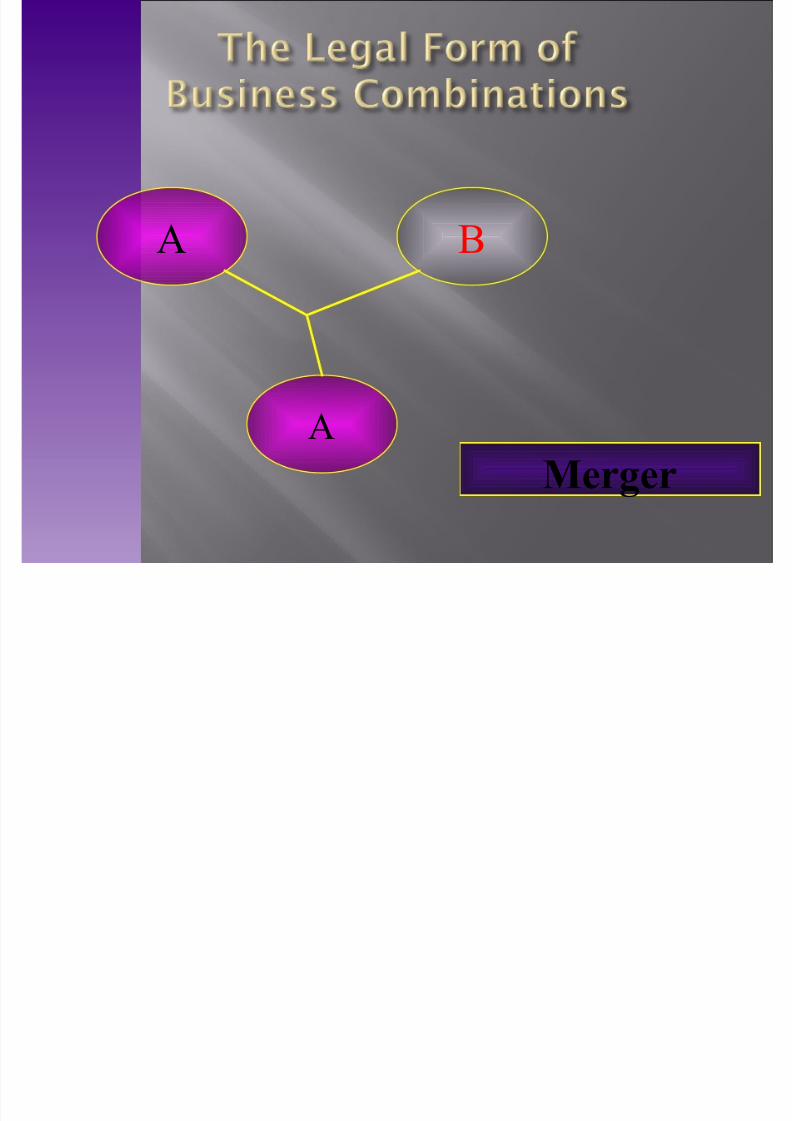

A )

A

Merger

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 6/40

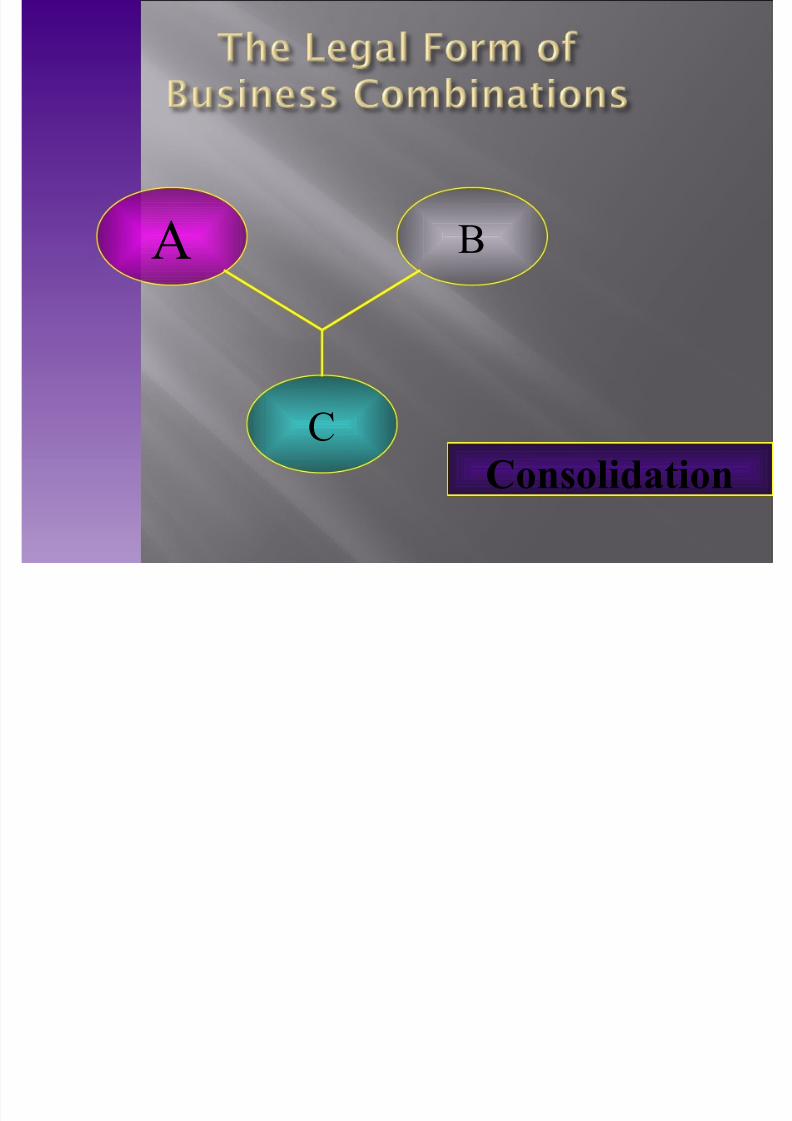

A)

CConsolidation

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 7/40

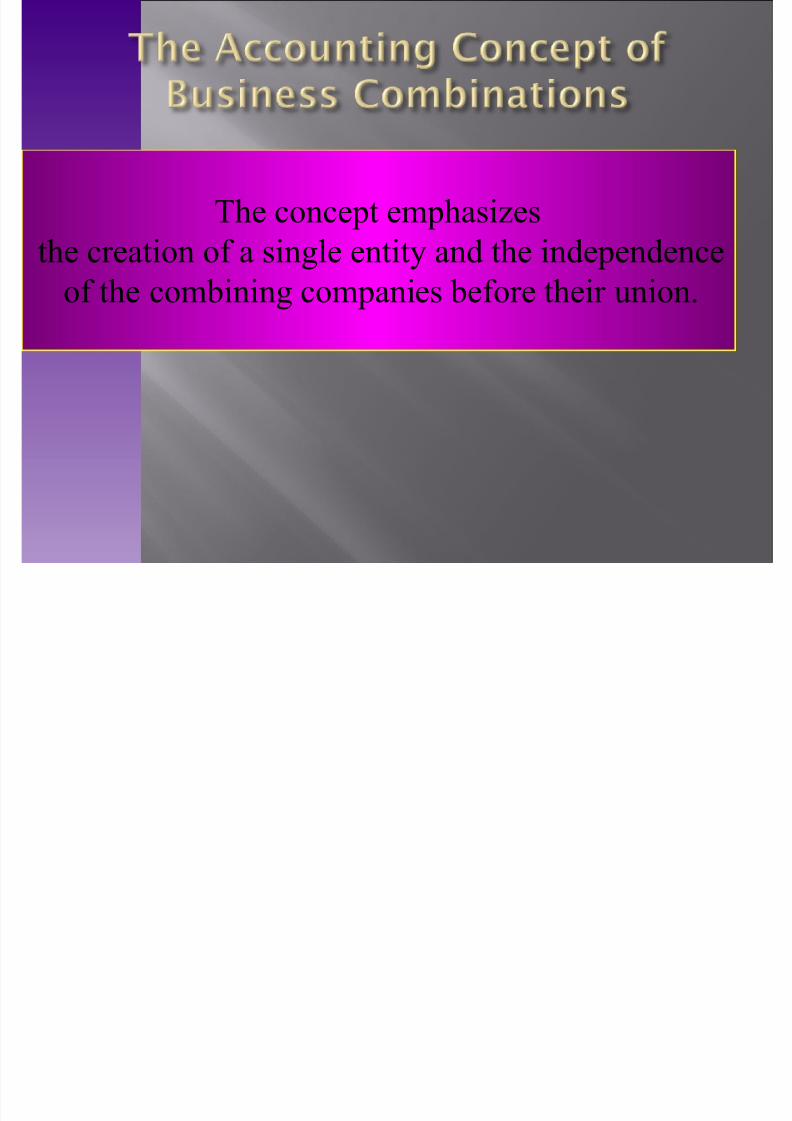

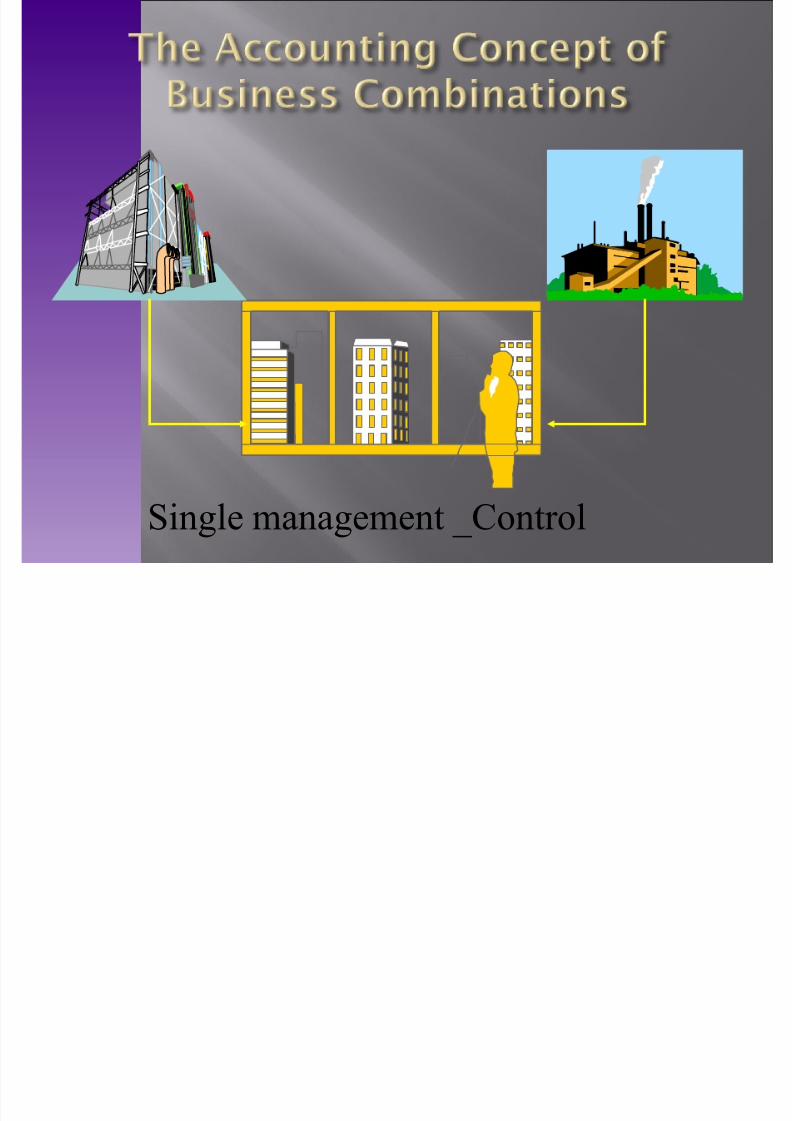

$he concept emphasies

the creation o& a single entity and the independence o& the combining companies be&ore their union.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 8/40Single management #Control

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 9/40

0ne or more corporations become subsidiaries.

0ne company trans&ers its net assets to another .

'ach company trans&ers its net assets to a newly &ormed corporation.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 10/40

Accounting &or )usiness Combination is one o& the most important and

interesting topic 0& accounting theory and practice and its comple( topic.Since 1234 /ooling o& interest been generally accepted. 5ntil 6441 accountin

reuirements &or business combination recognied )oth pooling 7 purchase

methods.

+n 1222 FAS) issued a report supporting its proposed decision to eliminate

/ooling o& interest &or the &ollowing Reasons8 /ooling provides less relevant

in&ormation to statement users 7 ignore economic value e(change in

the transaction. /ooling creates these problem because it uses Historical boo"

9alue rather than Fair value o& net assets at the transaction date.

*AA/ reuires recording asset Acuisitions at &air value. *aap 'liminated the pooling o& interest method o& accounting initiated a&ter :une ;4% 6441.

)usinesses must use the Acuisition ,ethod because the new standard

prohibited use pooling method. +FRS also consistent with *AA/ and reuires

to use the purchase methods. Accounting &or business combination was

a major joint project between FAS) 7 +AS).

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 11/40

FASB Statement No. 141 eliminated the pooling o& interest method

&or transactions initiated a&ter :une ;4% 6441. Combinations initiateda&ter this date must use the purchase method. /rior combinations will b

grand&athered.

/ooling uses historical boo" values to record combinations rather than

recogniing &air values o& net assets at the transaction date.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 12/40

Acuisitions ,ethod reuires the recording

o& assets acuired and liabilities assumed at

their &air values at the date o& combination.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 13/40

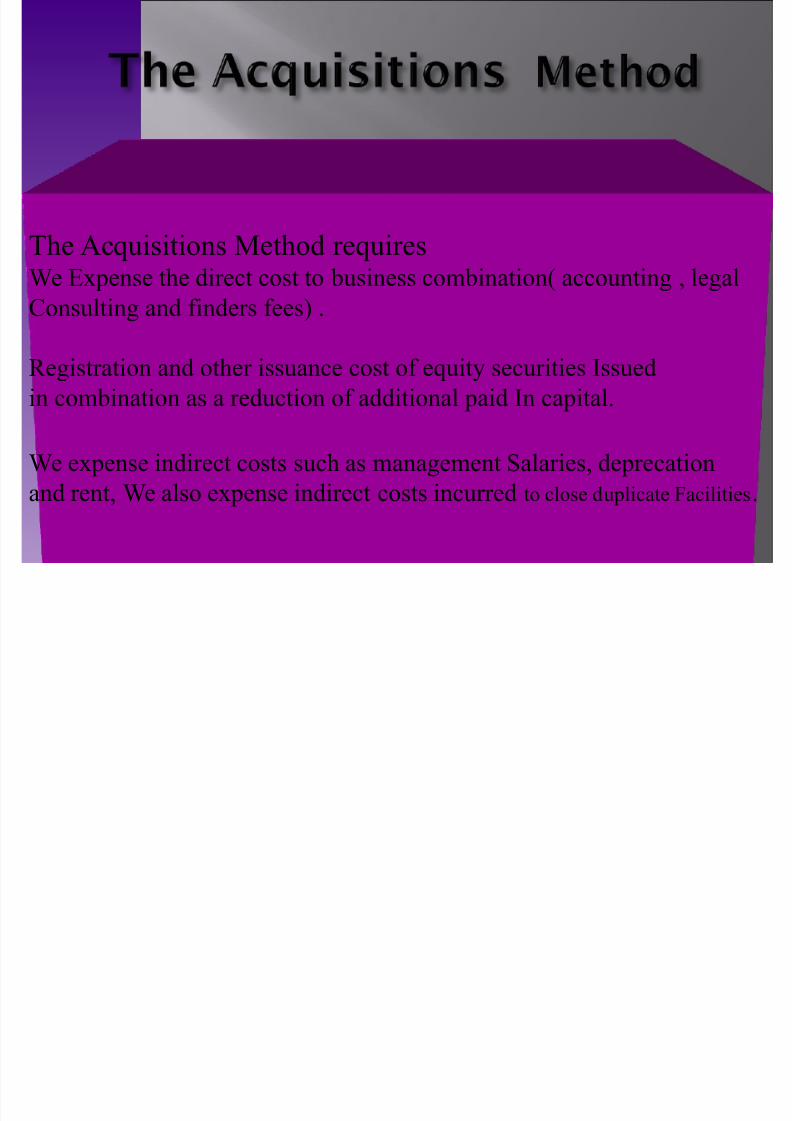

$he Acuisitions ,ethod reuires<e '(pense the direct cost to business combination= accounting % legal

Consulting and &inders &ees> .

Registration and other issuance cost o& euity securities +ssued

in combination as a reduction o& additional paid +n capital.

<e e(pense indirect costs such as management Salaries% deprecation

and rent% <e also e(pense indirect costs incurred to close duplicate Facilities.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 14/40

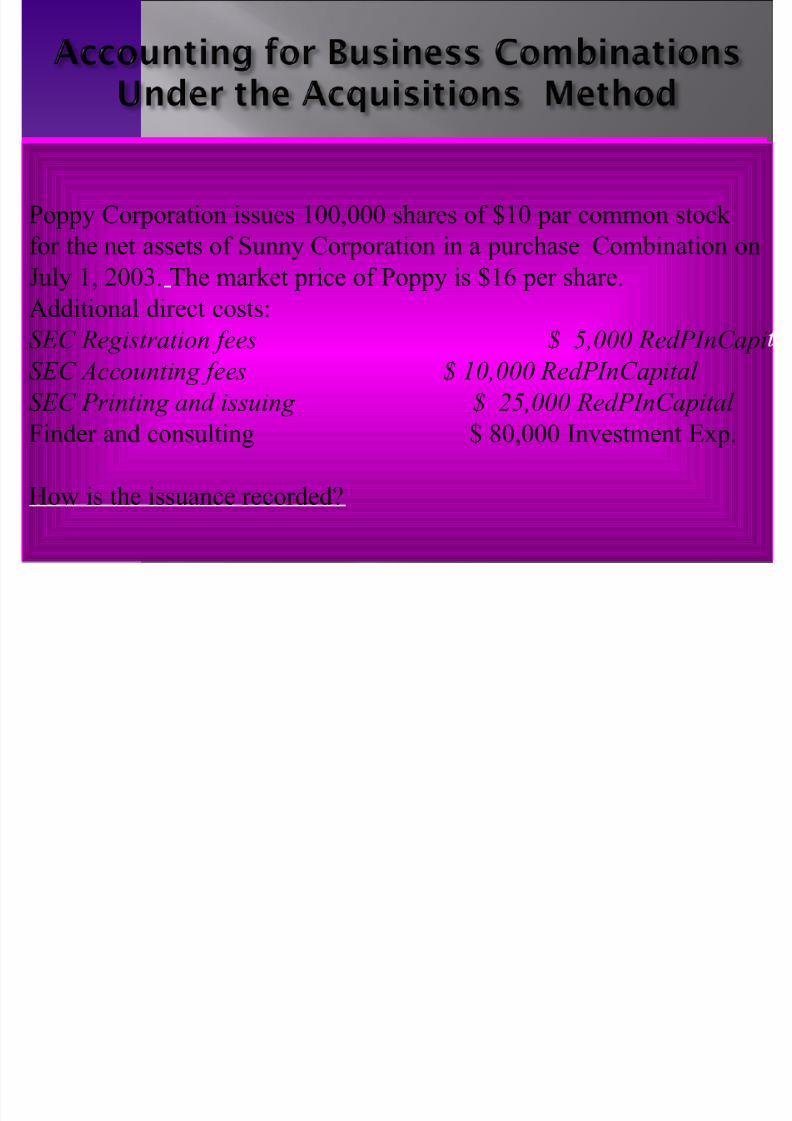

/oppy Corporation issues 144%444 shares o& ?14 par common stoc"

&or the net assets o& Sunny Corporation in a purchase Combination on

:uly 1% 644;. $he mar"et price o& /oppy is ?1@ per share.Additional direct costs8

SEC Registration fees $ 5,000 RedPInCapit

SEC A!!o"nting fees $ 10,000 RedPInCapita

SEC Printing and iss"ing $ #5,000 RedPInCapita Finder and consulting ? 4%444 +nvestment '(p.

How is the issuance recordedB

/oppy Corporation issues 144%444 shares o& ?14 par common stoc"

&or the net assets o& Sunny Corporation in a purchase Combination on

:uly 1% 644;. $he mar"et price o& /oppy is ?1@ per share.

Additional direct costs8

SEC Registration fees $ 5,000 RedPInCapi

SEC A!!o"nting fees $ 10,000 RedPInCapita

SEC Printing and iss"ing $ #5,000 RedPInCapita Finder and consulting ? 4%444 +nvestment '(p.

How is the issuance recordedB

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 15/40

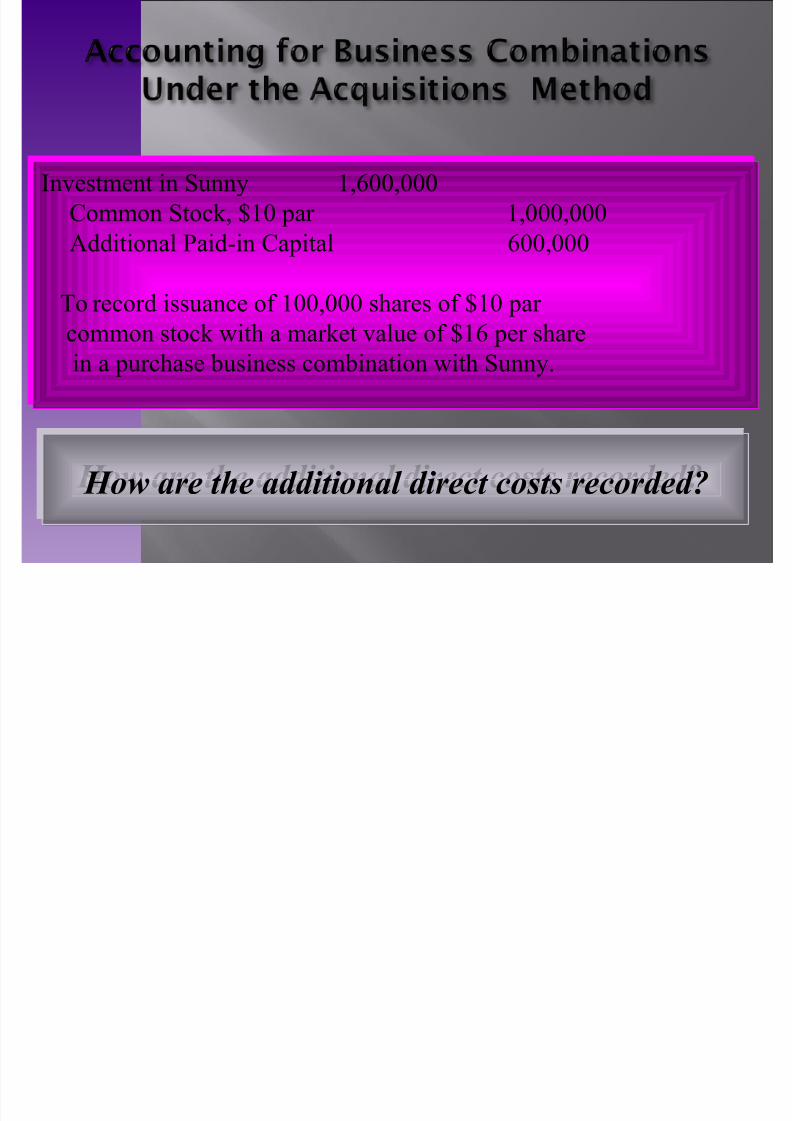

+nvestment in Sunny 1%@44%444

Common Stoc"% ?14 par 1%444%444

Additional /aid-in Capital @44%444

$o record issuance o& 144%444 shares o& ?14 par

common stoc" with a mar"et value o& ?1@ per share

in a purchase business combination with Sunny.

+nvestment in Sunny 1%@44%444

Common Stoc"% ?14 par 1%444%444

Additional /aid-in Capital @44%444

$o record issuance o& 144%444 shares o& ?14 par

common stoc" with a mar"et value o& ?1@ per share

in a purchase business combination with Sunny.

How are the additional direct costs recorded? How are the additional direct costs recorded?

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 16/40

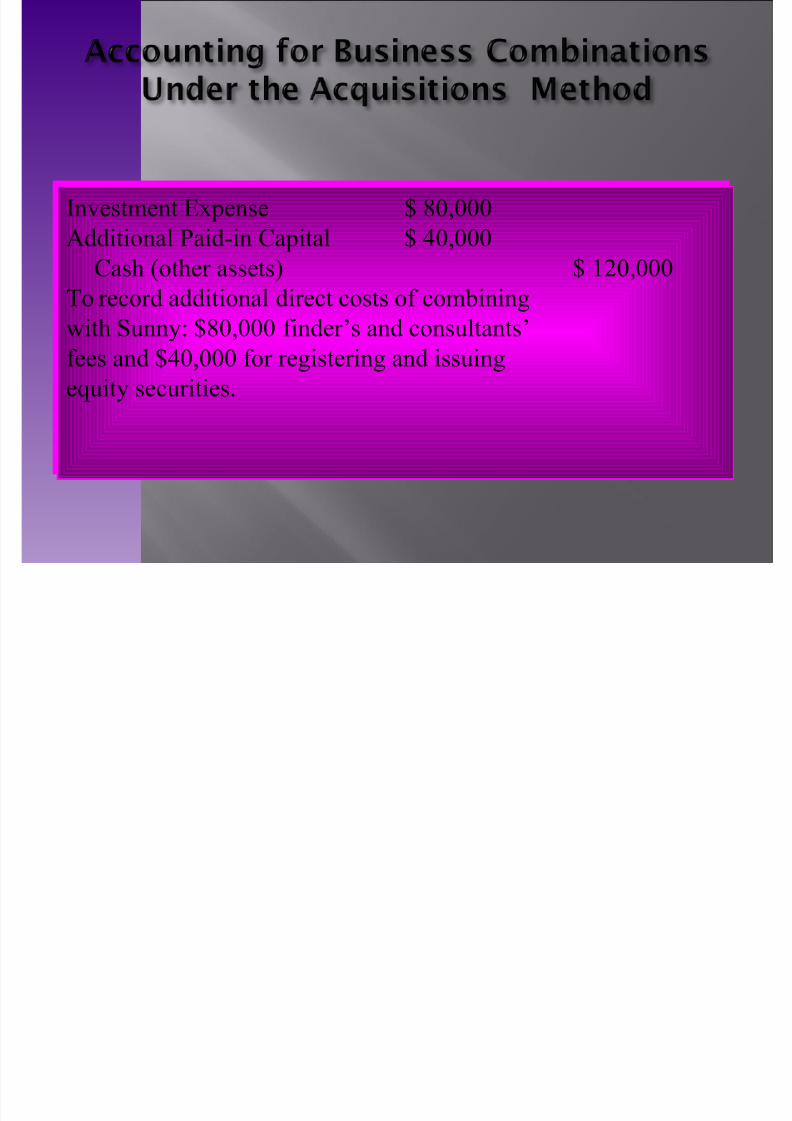

+nvestment '(pense ? 4%444

Additional /aid-in Capital ? 4%444

Cash =other assets> ? 164%444$o record additional direct costs o& combining

with Sunny8 ?4%444 &inderDs and consultantsD

&ees and ?4%444 &or registering and issuing

euity securities.

+nvestment '(pense ? 4%444

Additional /aid-in Capital ? 4%444

Cash =other assets> ? 164%444$o record additional direct costs o& combining

with Sunny8 ?4%444 &inderDs and consultantsD

&ees and ?4%444 &or registering and issuing

euity securities.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 17/40

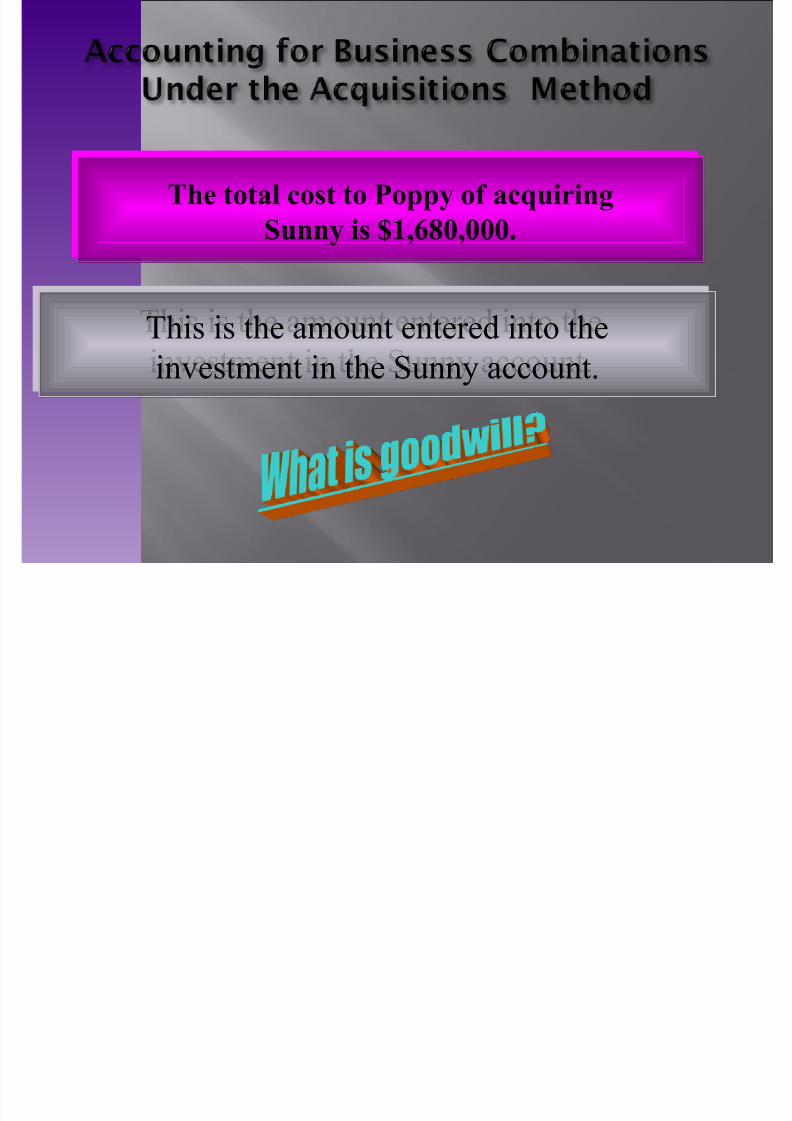

The total cost to Poppy of acquiring

Sunny is $1,680,000.The total cost to Poppy of acquiring

Sunny is $1,680,000.

$his is the amount entered into the

investment in the Sunny account.$his is the amount entered into the

investment in the Sunny account.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 18/40

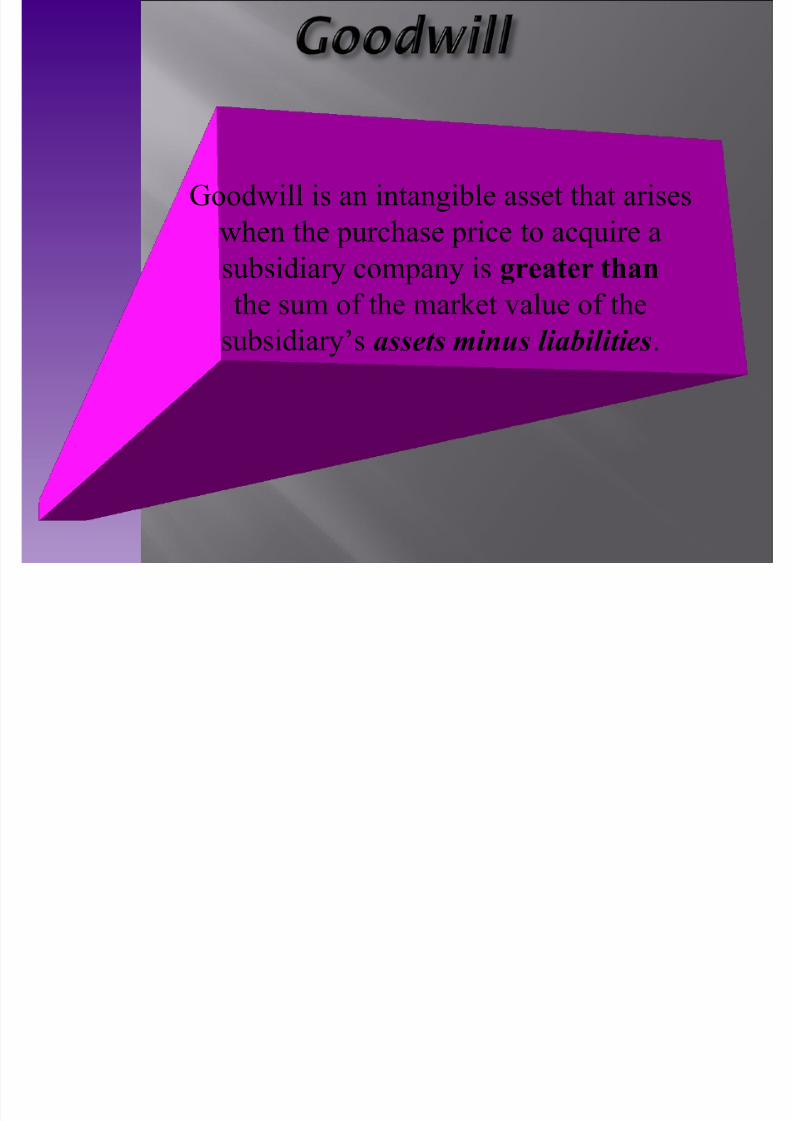

*oodwill is an intangible asset that arises

when the purchase price to acuire a

subsidiary company is greater thanthe sum o& the mar"et value o& the

subsidiaryDs assets minus liabilities.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 19/40

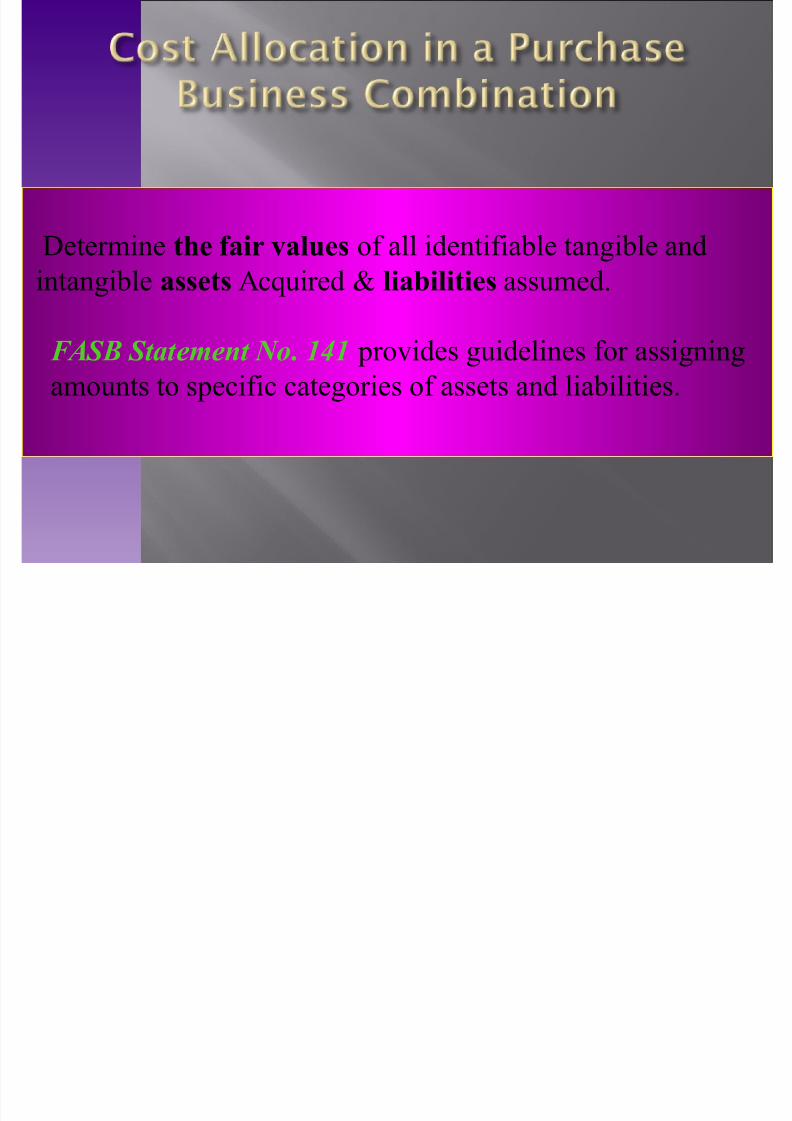

etermine the fair alues o& all identi&iable tangible and

intangible assets Acuired 7 lia!ilities assumed.

FASB Statement No. 141 provides guidelines &or assigning

amounts to speci&ic categories o& assets and liabilities.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 20/40

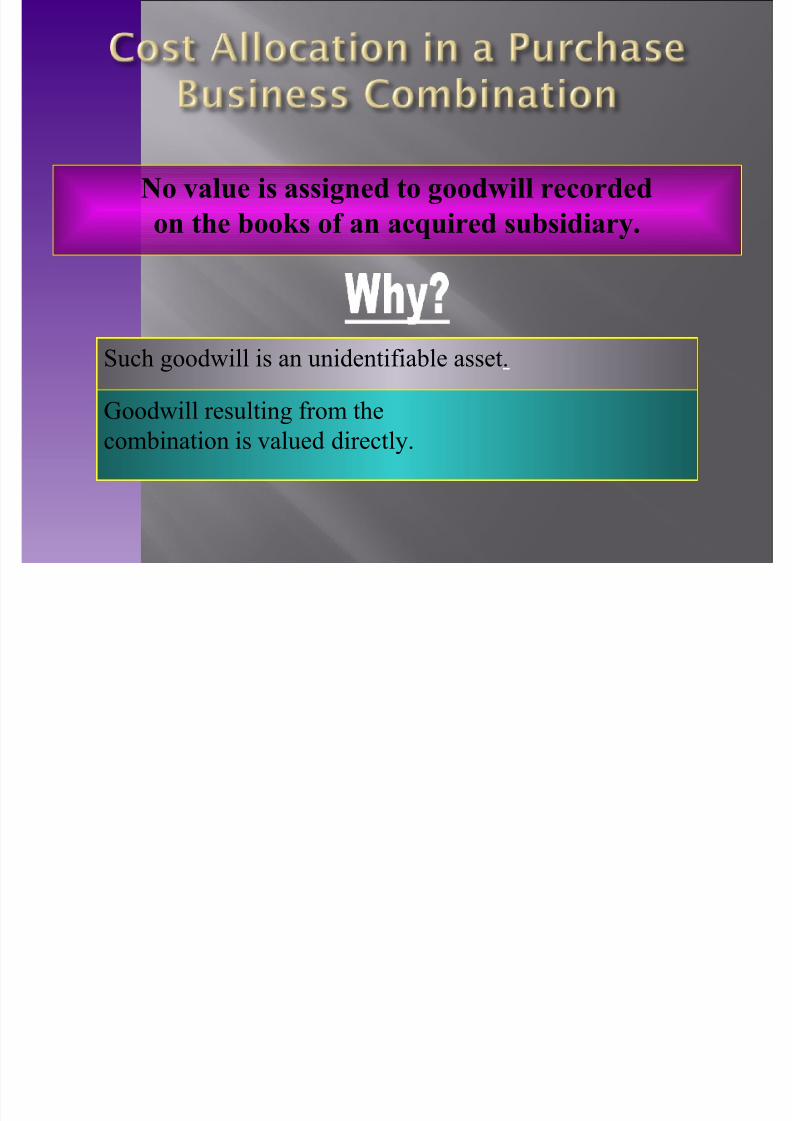

"o alue is assigned to good#ill recorded

on the !oos of an acquired su!sidiary.

Such goodwill is an unidenti&iable asset.

*oodwill resulting &rom the

combination is valued directly.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 21/40

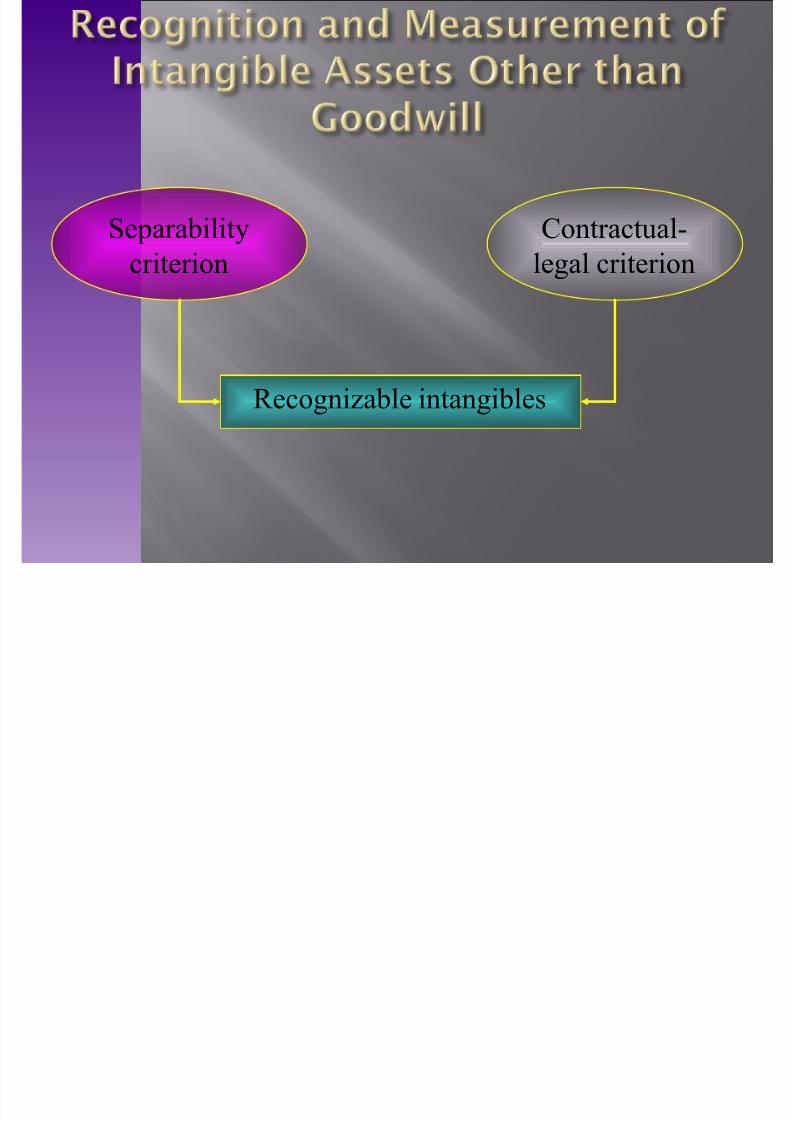

Recogniable intangibles

Separability

criterion

Contractual-

legal criterion

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 22/40

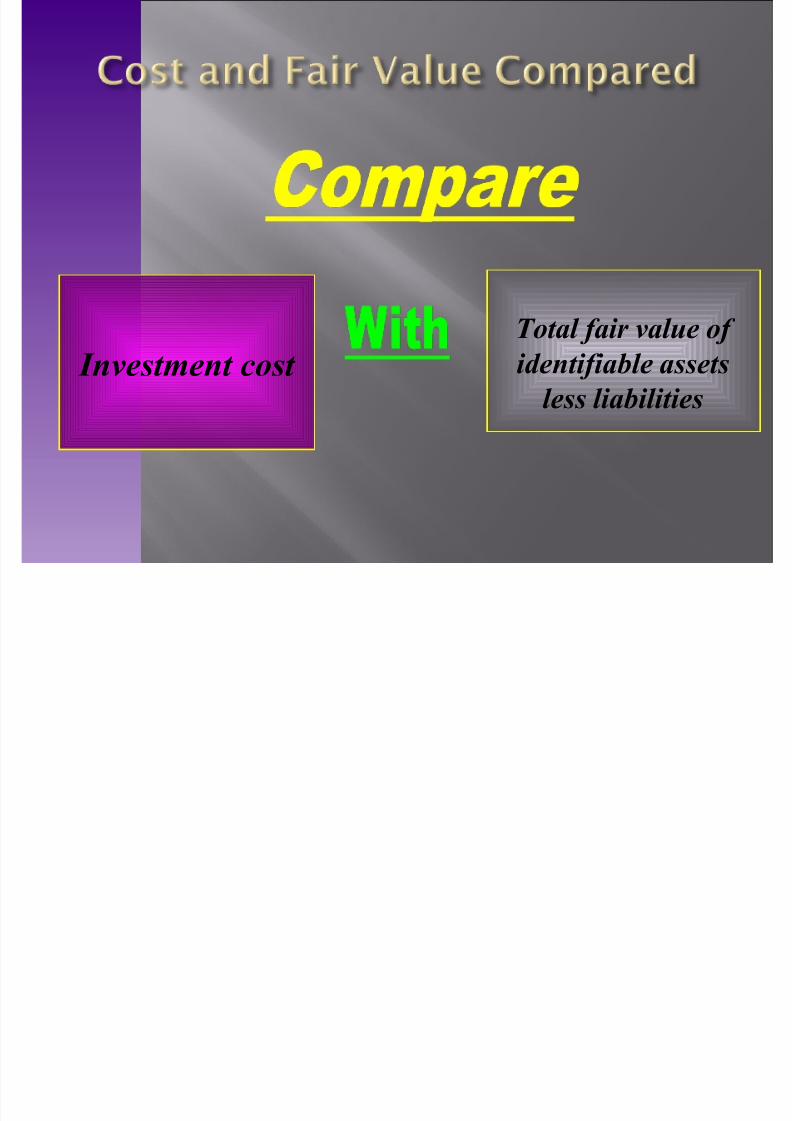

Investment cost

Total air value o

identiiable assets

less liabilities

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 23/40

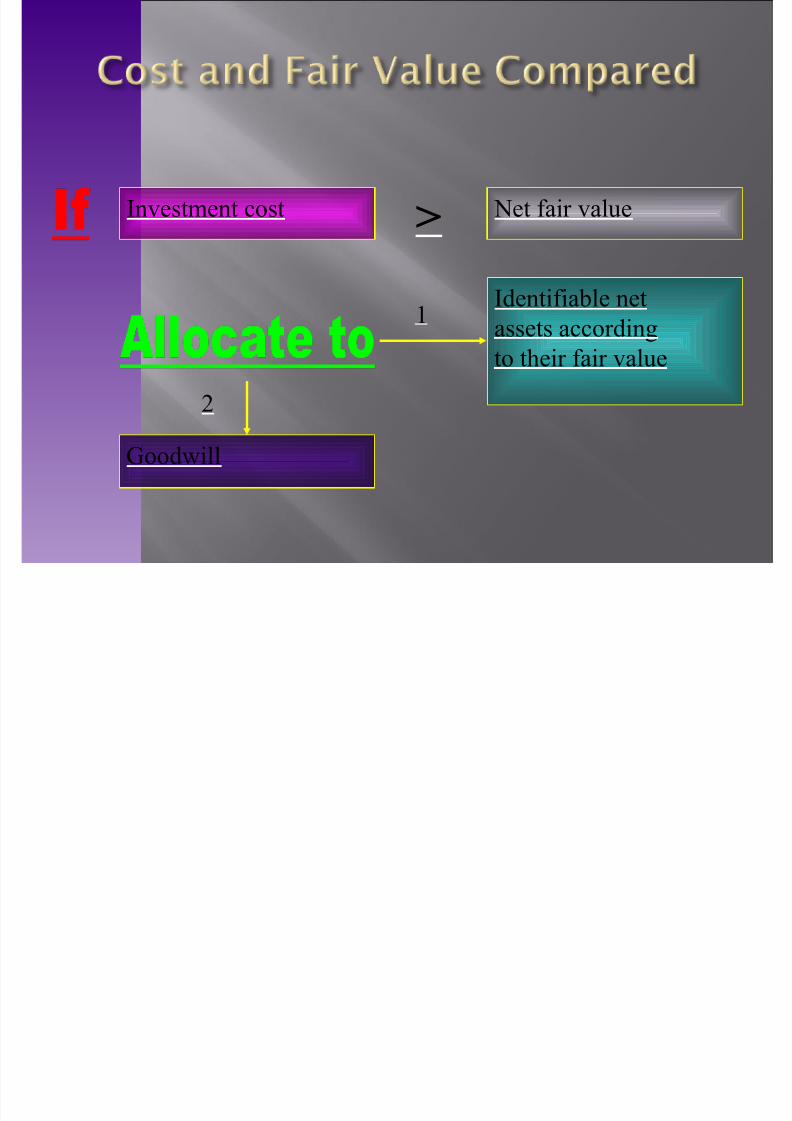

+nvestment cost Net &air value%

*oodwill

6

+denti&iable net

assets according

to their &air value

1

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 24/40

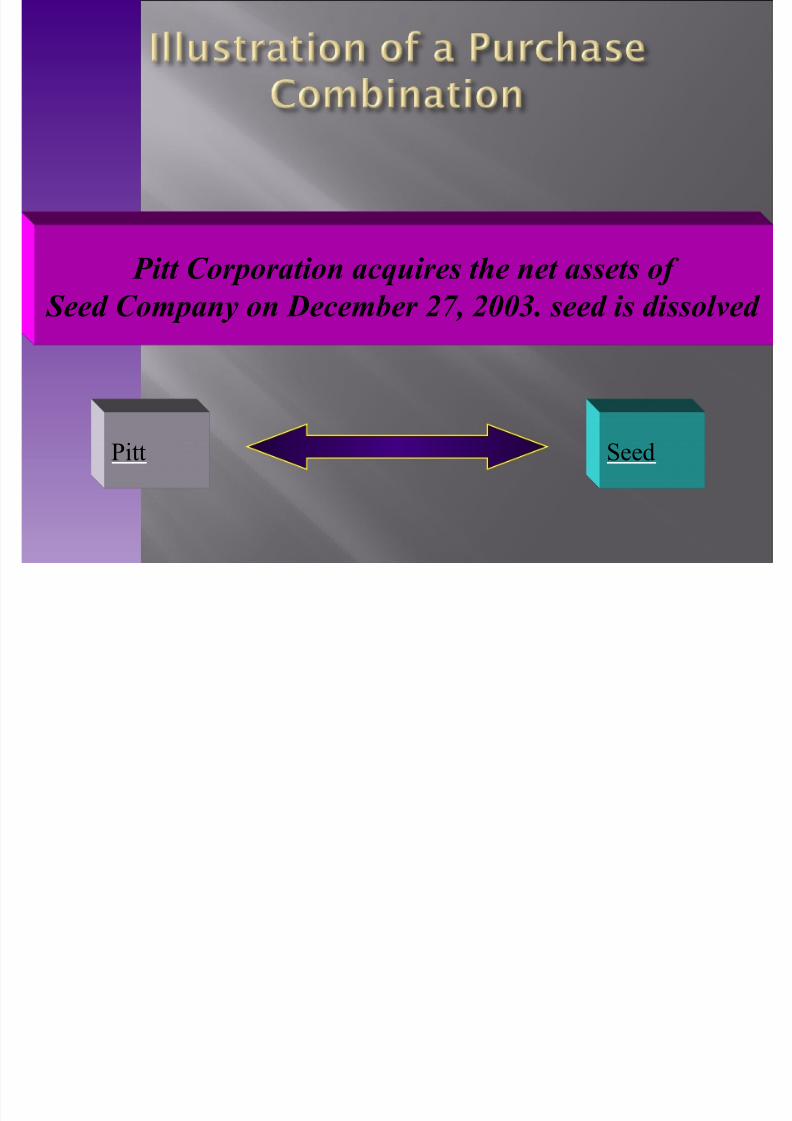

!itt Cor"oration ac#uires the net assets o Seed Com"an$ on %ecember &'( &))*. seed is dissolved

/itt Seed

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 25/40

)oo" 9alue

AssetsCash 34 ? 34

Net receivables 134 14+nventories 644 634!and 34 144

)uildings% net ;44 344'uipment% net 634 ;34

/atents 34$otal assets ?1%444 ?1%4

Fair 9alue

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 26/40

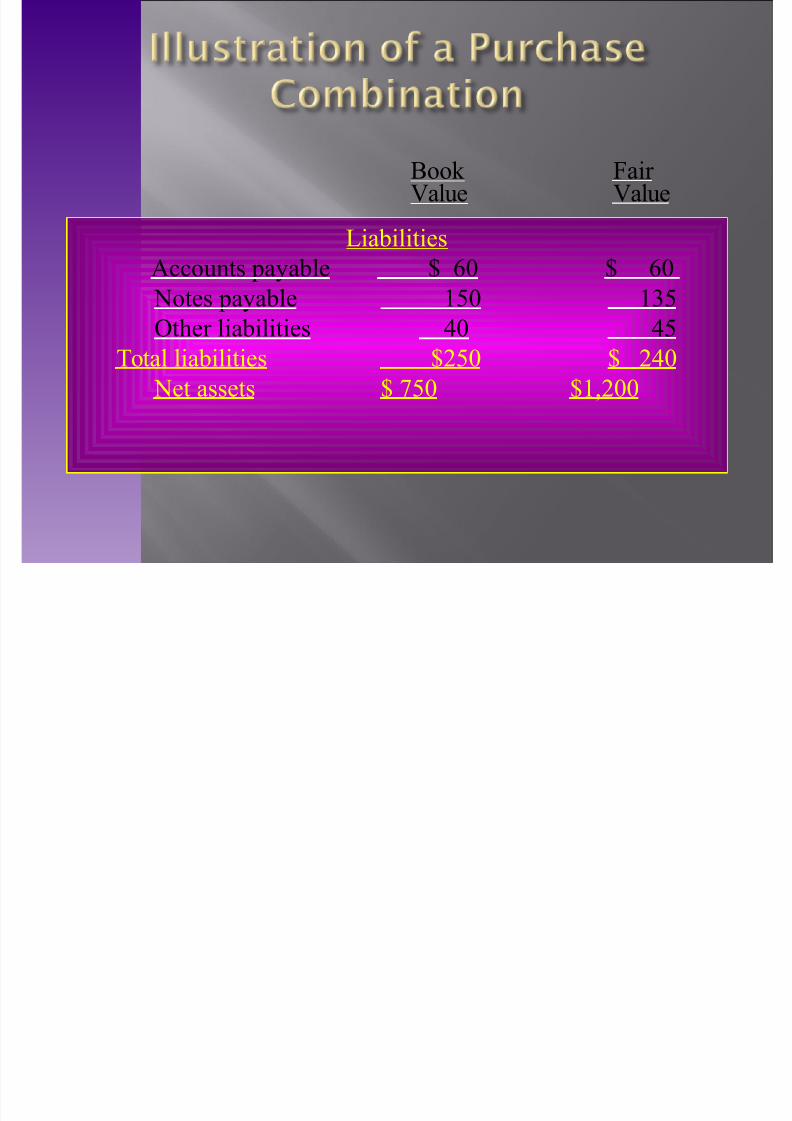

)oo" 9alue

!iabilities

Accounts payable ? @4 ? @4 Notes payable 134 1;3

0ther liabilities 4 3

$otal liabilities ?634 ? 64

Net assets ? E34 ?1%644

Fair 9alue

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 27/40

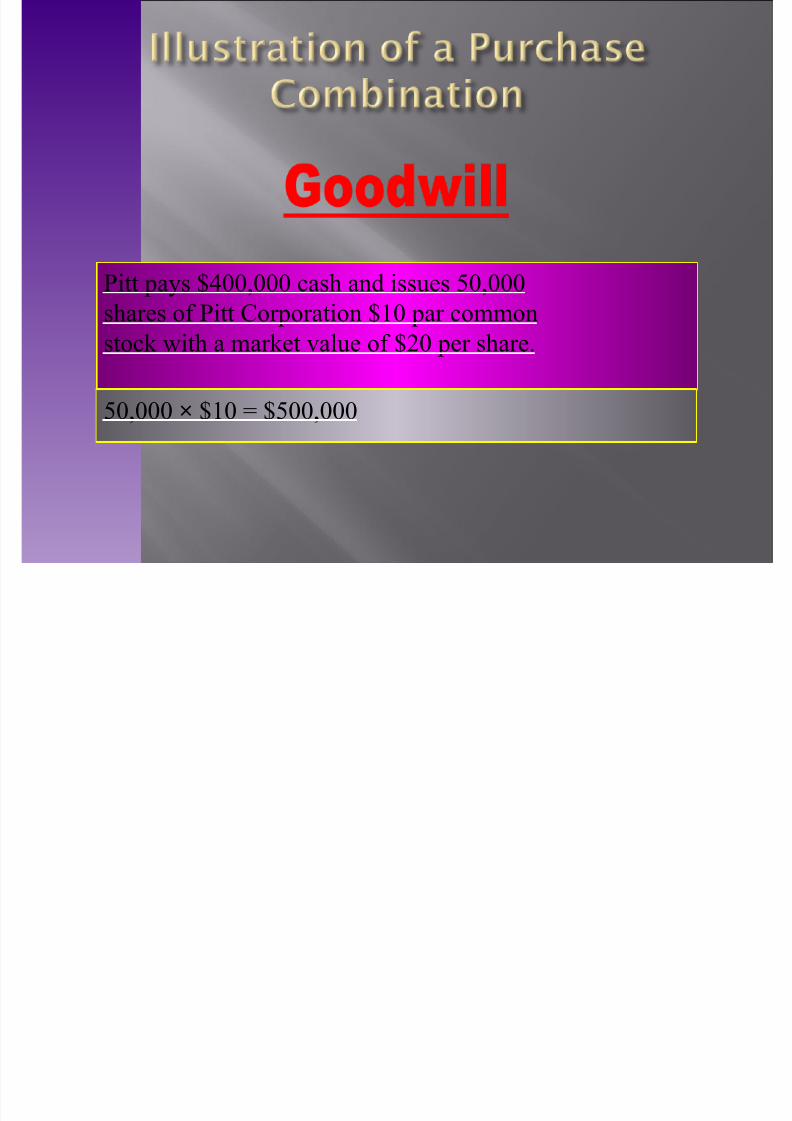

/itt pays ?44%444 cash and issues 34%444

shares o& /itt Corporation ?14 par common

stoc" with a mar"et value o& ?64 per share.

34%444 & ?14 ?344%444

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 28/40

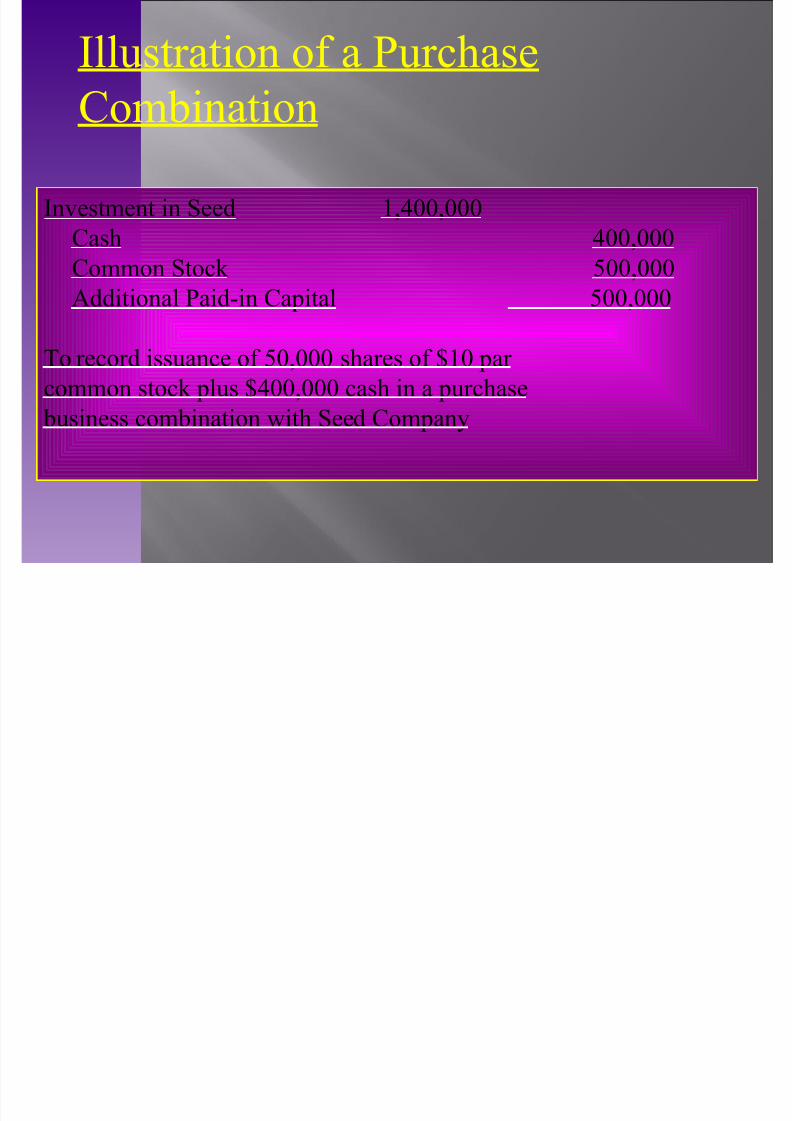

+nvestment in Seed 1%44%444

Cash 44%444

Common Stoc" 344%444Additional /aid-in Capital 344%444

$o record issuance o& 34%444 shares o& ?14 par

common stoc" plus ?44%444 cash in a purchase business combination with Seed Company

+llustration o& a /urchase

Combination

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 29/40

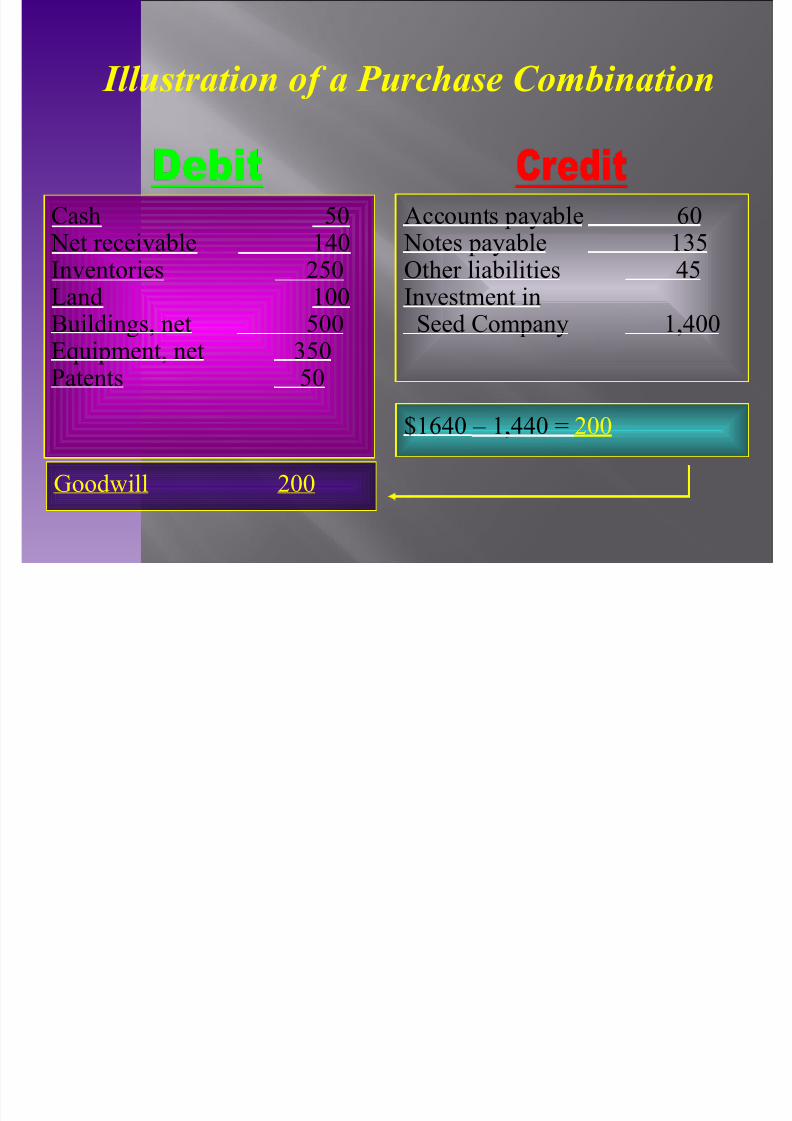

Illustration o a !urchase Combination

Cash 34 Net receivable 14

+nventories 634!and 144)uildings% net 344'uipment% net ;34/atents 34

Accounts payable @4 Notes payable 1;3

0ther liabilities 3+nvestment in Seed Company 1%44

?1@4 G 1%4 644

*oodwill 644

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 30/40

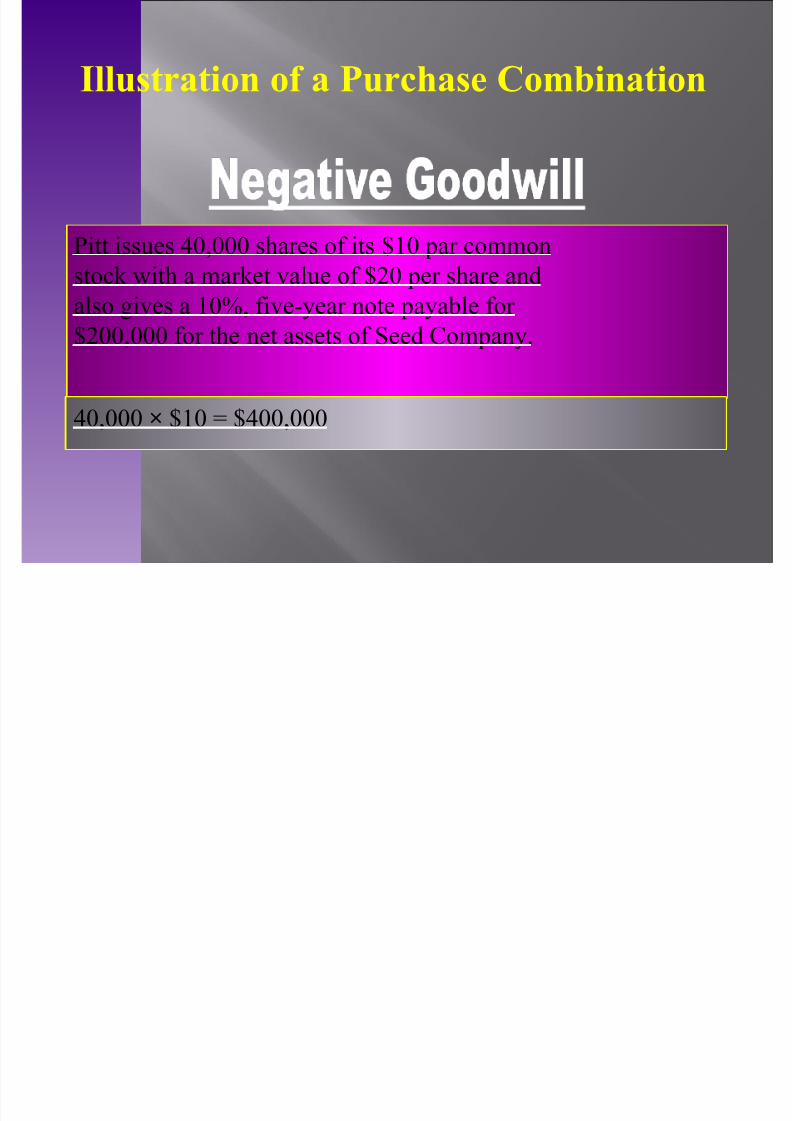

'llustration of a Purchase Co(!ination

/itt issues 4%444 shares o& its ?14 par common

stoc" with a mar"et value o& ?64 per share andalso gives a 14% &ive-year note payable &or

?644%444 &or the net assets o& Seed Company.

4%444 & ?14 ?44%444

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 31/40

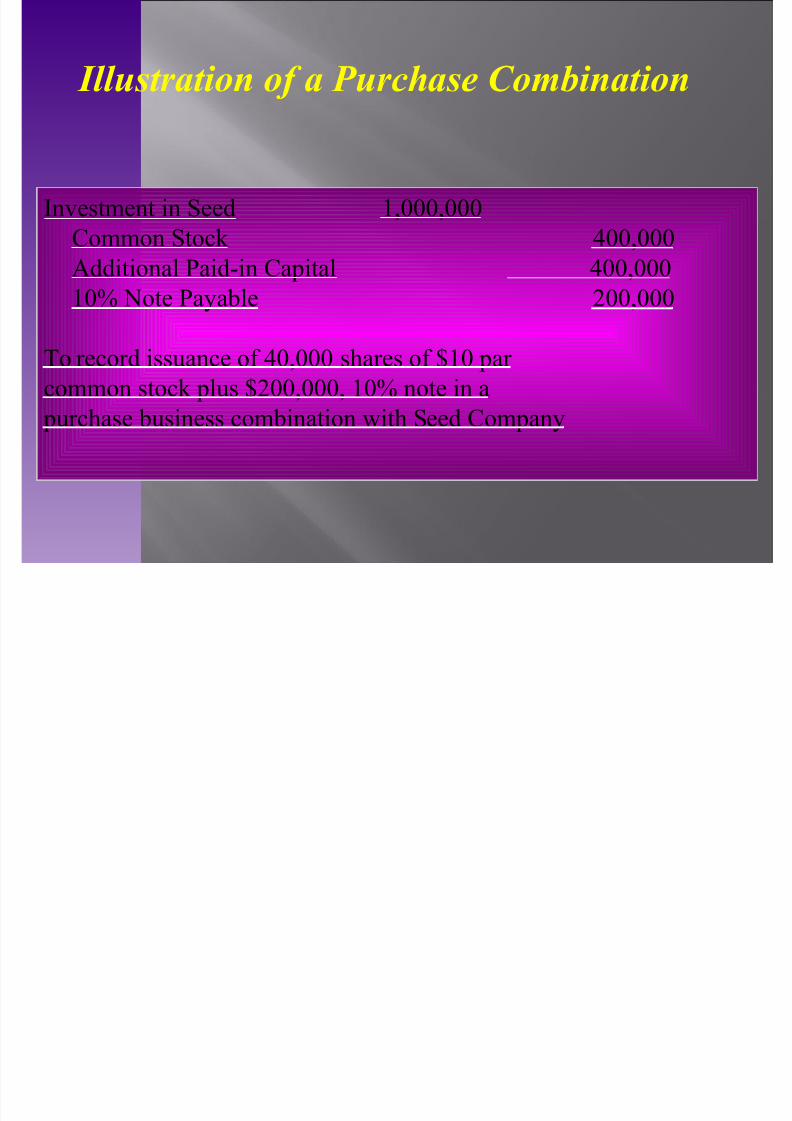

+nvestment in Seed 1%444%444

Common Stoc" 44%444

Additional /aid-in Capital 44%44414 Note /ayable 644%444

$o record issuance o& 4%444 shares o& ?14 par

common stoc" plus ?644%444% 14 note in a purchase business combination with Seed Company

Illustration o a !urchase Combination

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 32/40

+llustration o& a /urchase

Combination

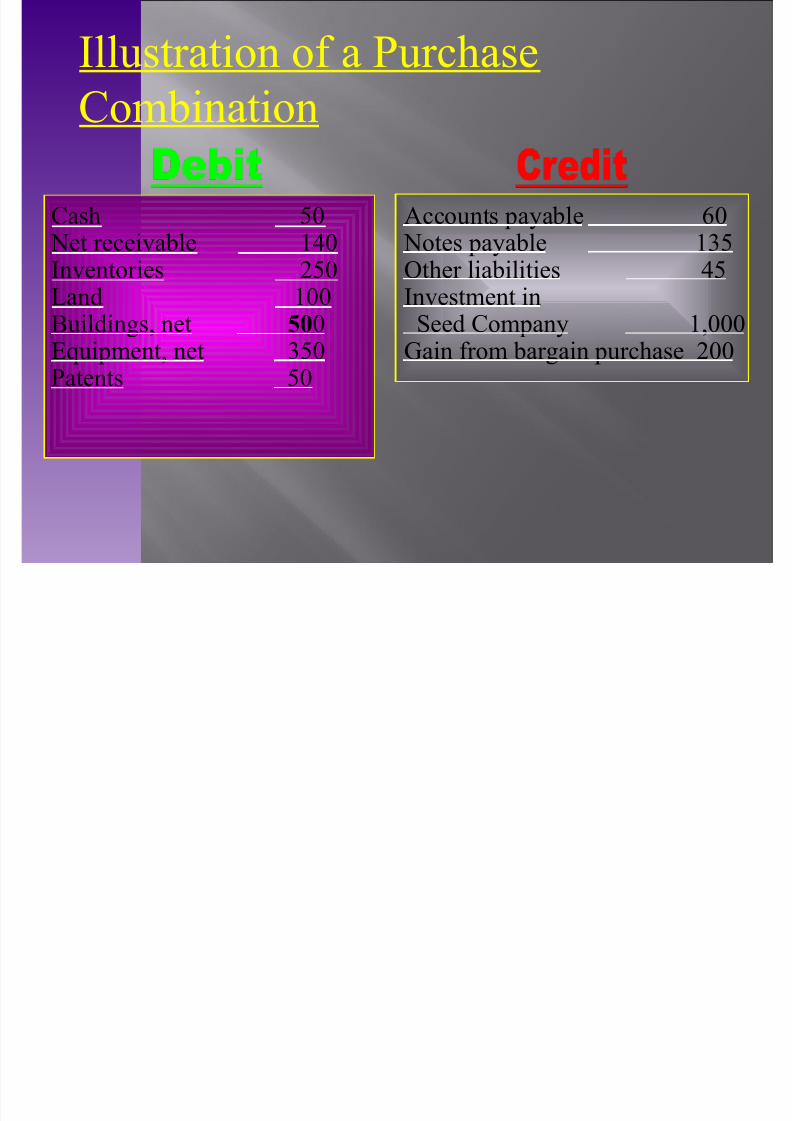

Cash 34 Net receivable 14

+nventories 634!and 144)uildings% net )04'uipment% net ;34/atents 34

Accounts payable @4 Notes payable 1;3

0ther liabilities 3+nvestment in Seed Company 1%444*ain &rom bargain purchase 644

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 33/40

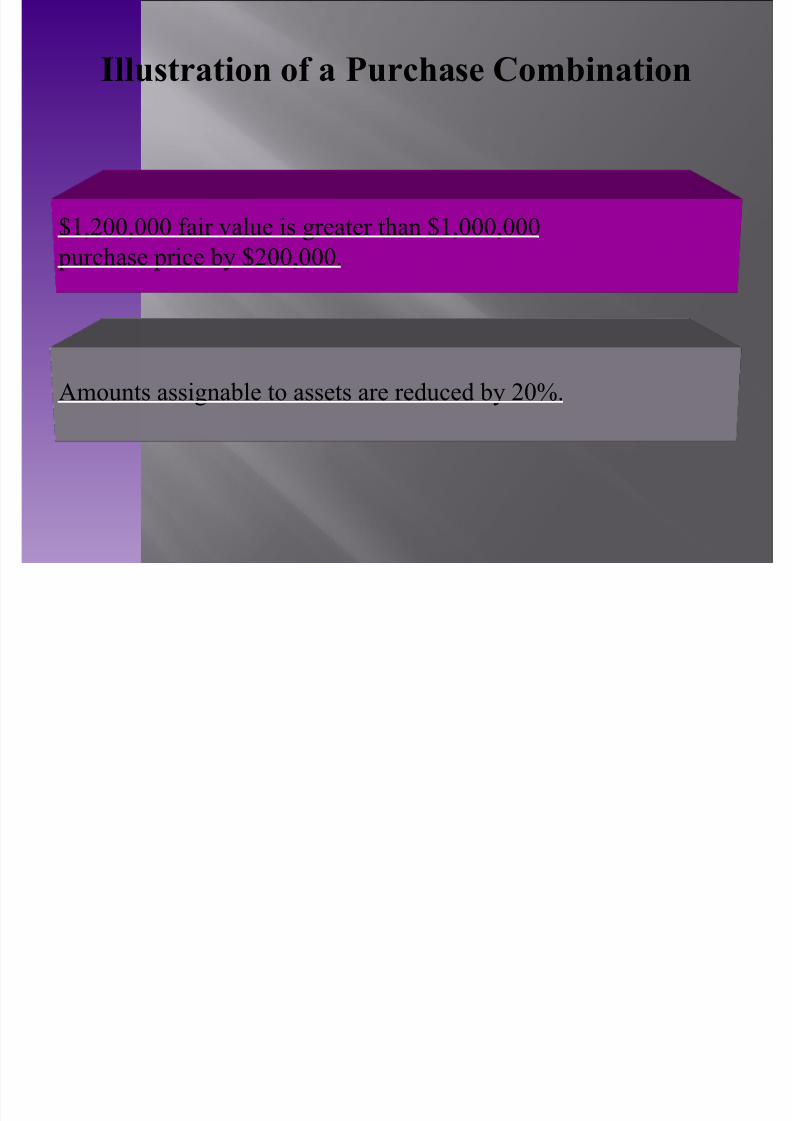

'llustration of a Purchase Co(!ination

?1%644%444 &air value is greater than ?1%444%444

purchase price by ?644%444.

Amounts assignable to assets are reduced by 64.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 34/40

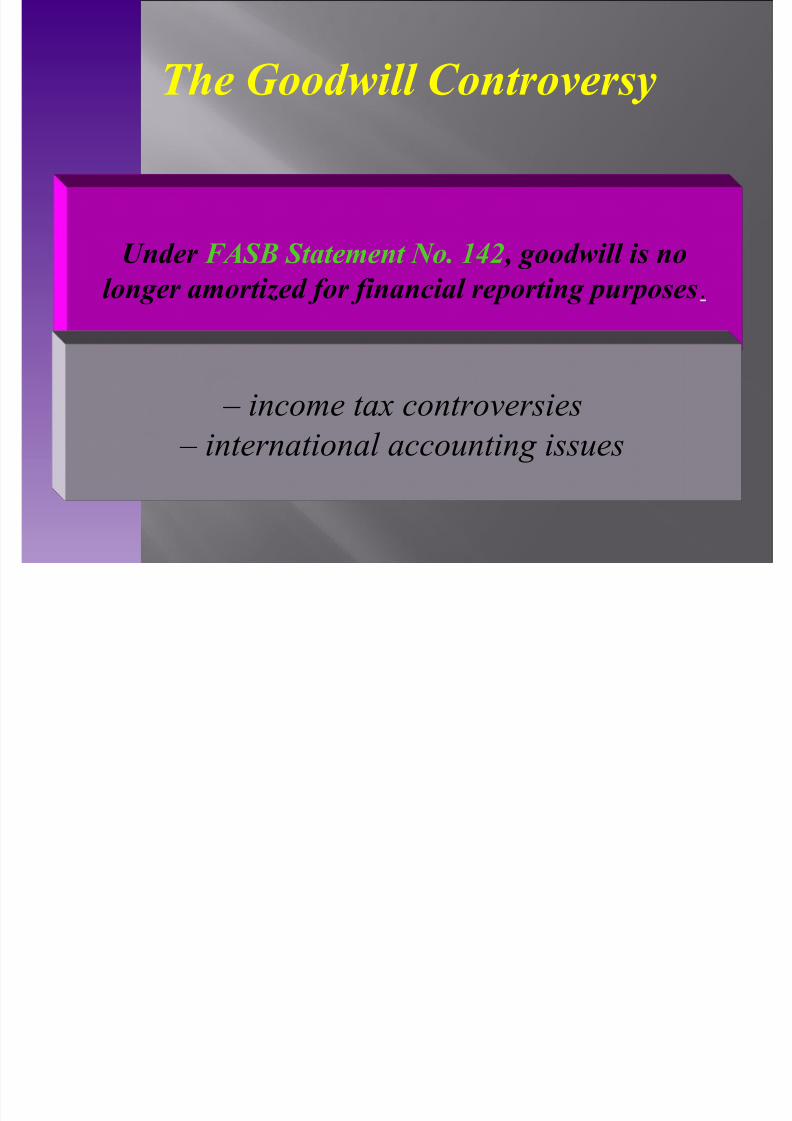

The +oodwill Controvers$

,nder FASB Statement No. 14& ( -oodwill is nolon-er amortied or inancial re"ortin- "ur"oses.

in!ome ta% !ontro&ersies internationa a!!o"nting iss"es

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 35/40

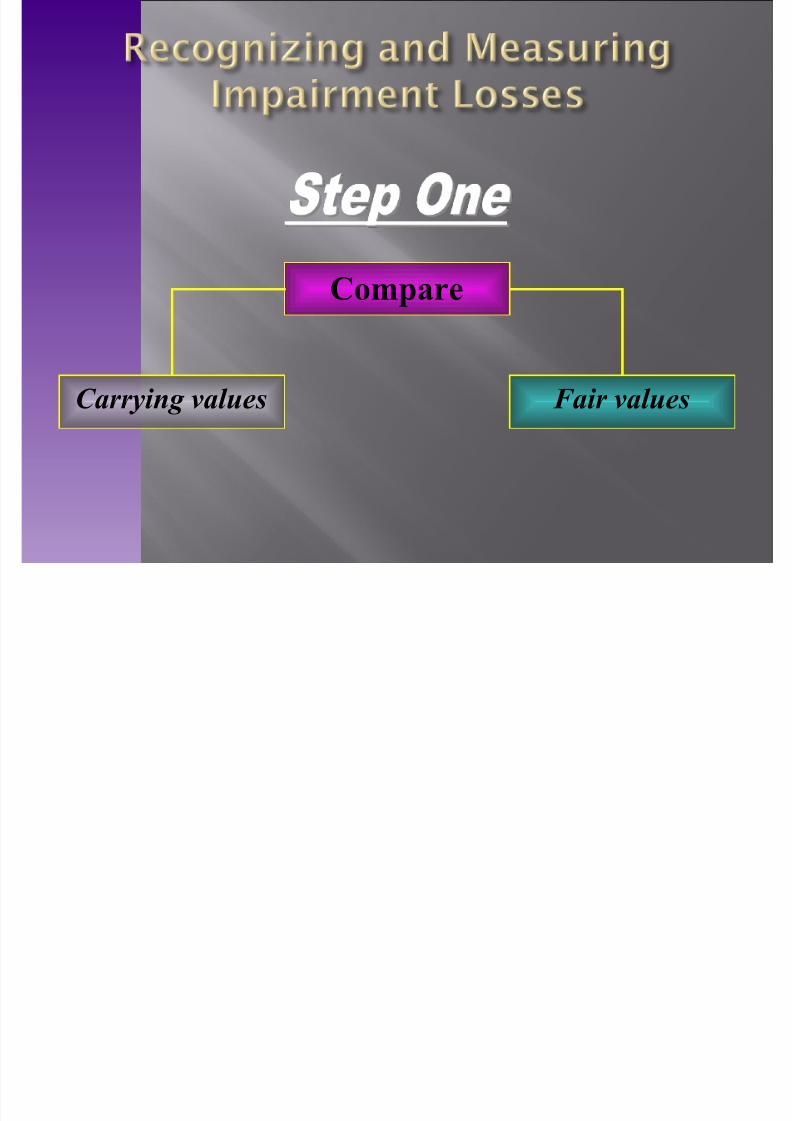

$he *oodwill Controversy

5nder FASB Statements No. 141 and No. 14#%

the FAS) reuires that &irms periodically assess

goodwill &or impairment o& its value.

An impairment occurs when the recorded value

o& goodwill is less than its &air value.

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 36/40

Carr$in- values

Co(pare

Fair values

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 37/40

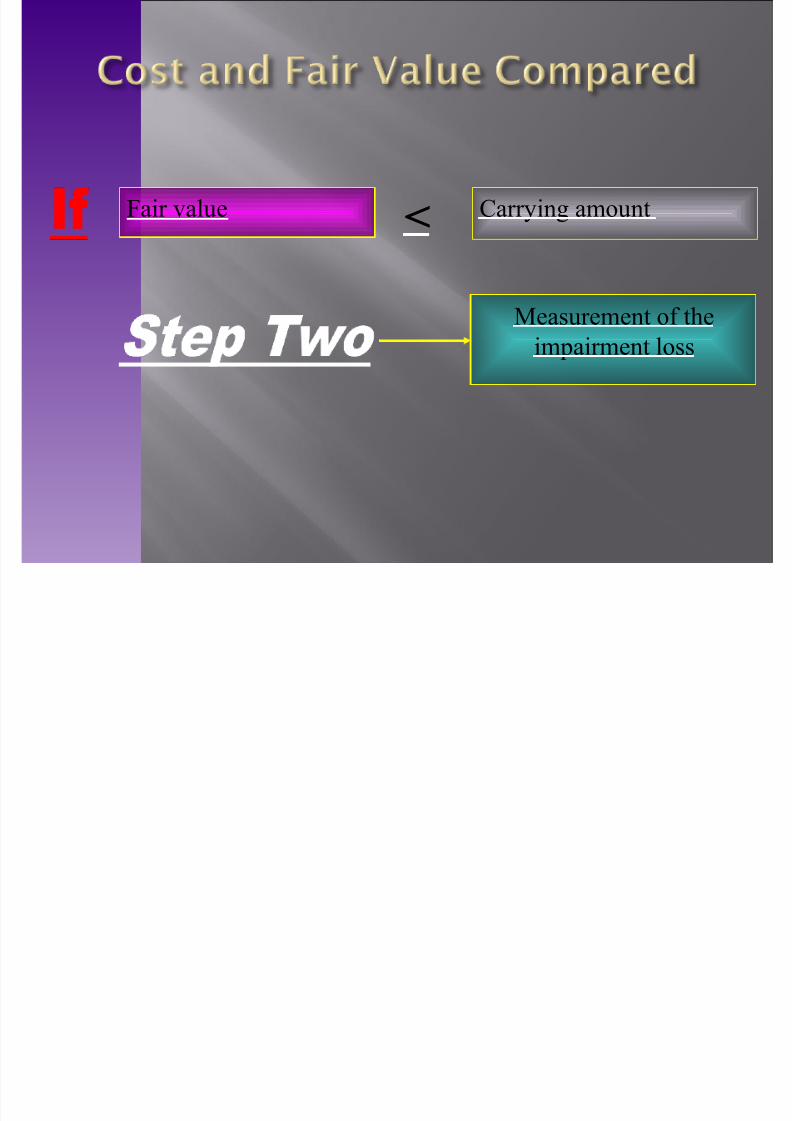

Fair value Carrying amount*

,easurement o& the

impairment loss

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 38/40

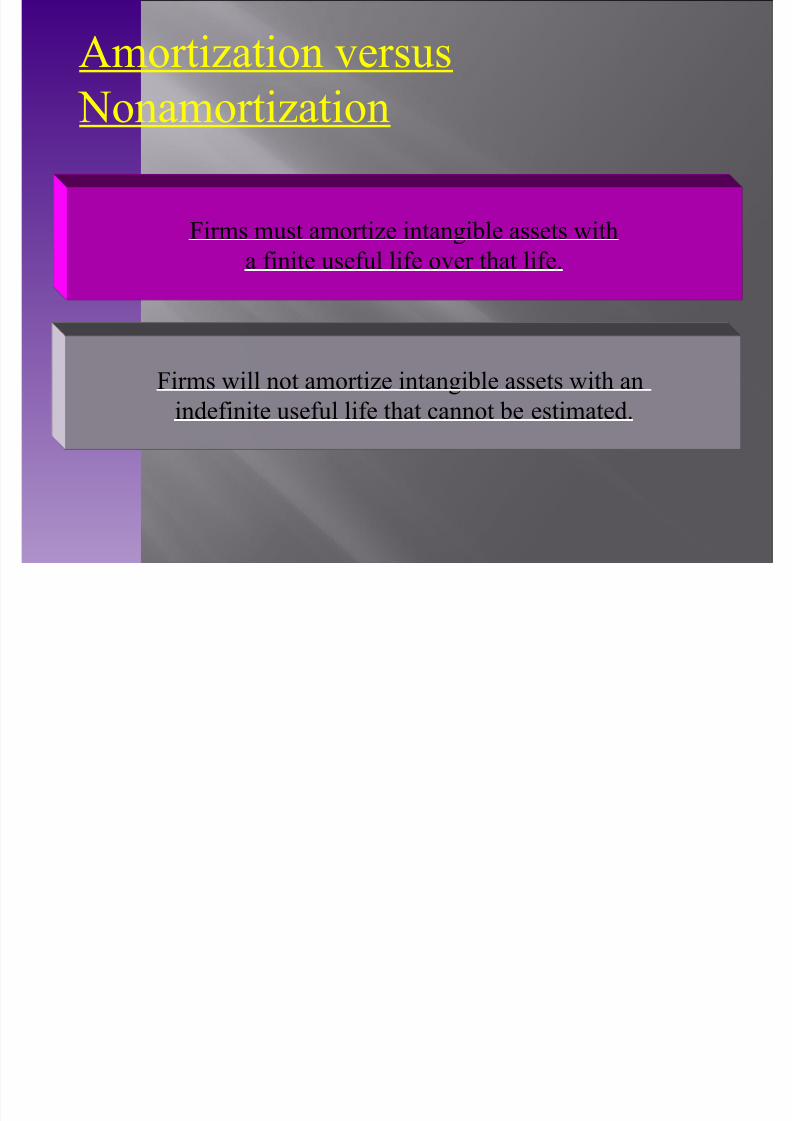

Amortiation versus

Nonamortiation

Firms must amortie intangible assets with

a &inite use&ul li&e over that li&e.

Firms will not amortie intangible assets with an

inde&inite use&ul li&e that cannot be estimated.

2-39

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 39/40

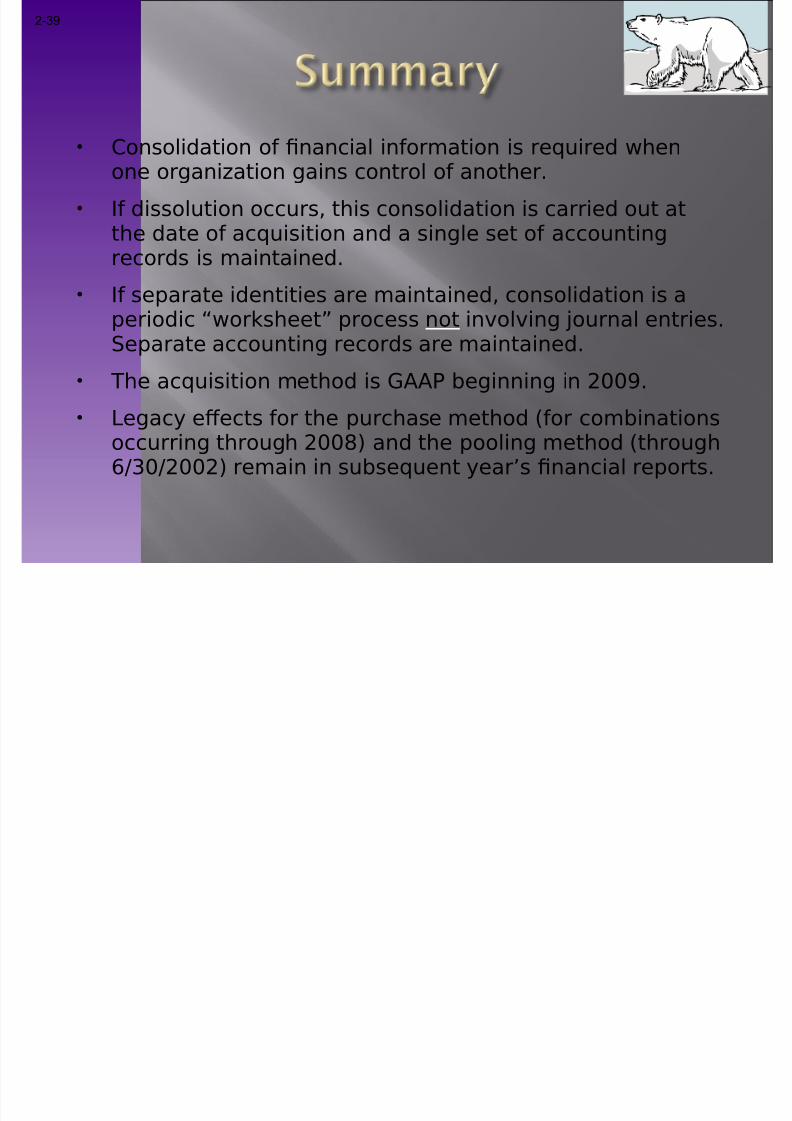

Consolidation of nancial information is required whenone organization gains control of another.

If dissolution occurs, this consolidation is carried out atthe date of acquisition and a single set of accountingrecords is maintained.

If separate identities are maintained, consolidation is aperiodic “worksheet” process not involving journal entries.eparate accounting records are maintained.

!he acquisition method is "##$ %eginning in &''(.

)egac* e+ects for the purchase method for com%inationsoccurring through &''- and the pooling method through/01'0&''& remain in su%sequent *ear2s nancial reports.

C # C 3

7/26/2019 Chap 002 slides

http://slidepdf.com/reader/full/chap-002-slides 40/40

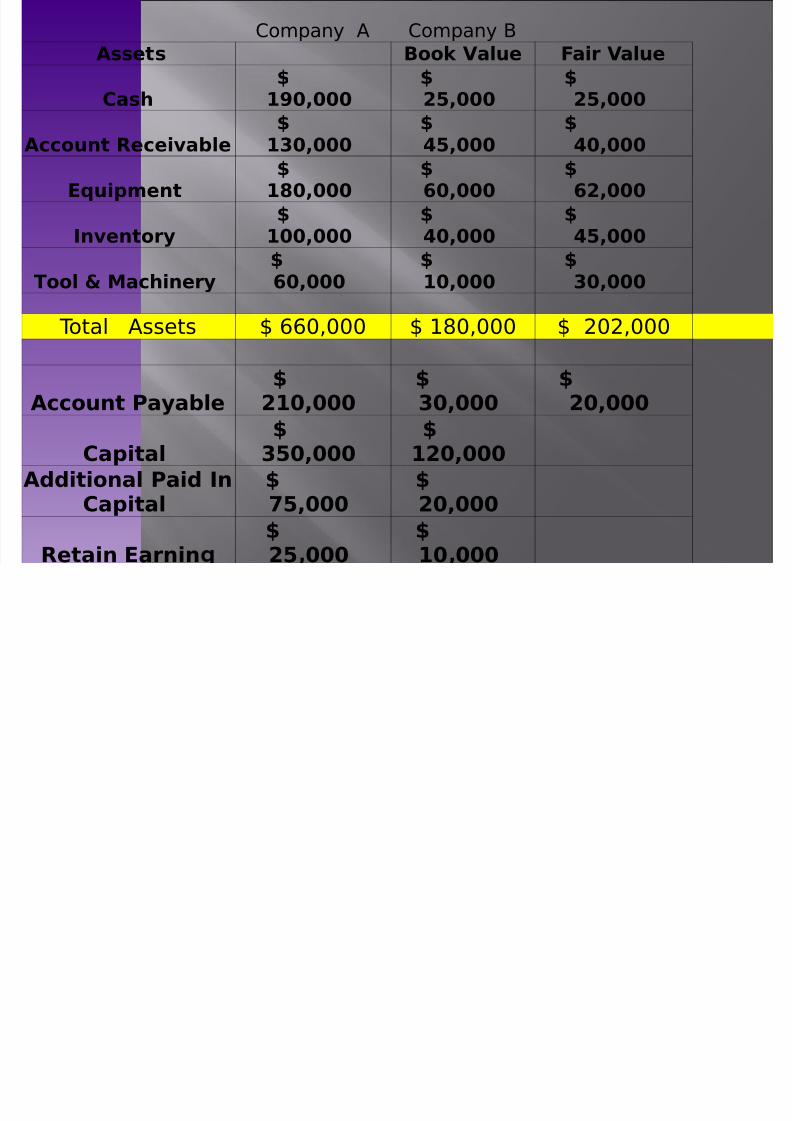

Compan* # Compan* 3

Assets Book Value Fair Value

Cash$

190,000$25,000

$25,000

Account Receivable $130,000

$5,000

$0,000

!"ui#ent$

1%0,000$&0,000

$&2,000

'nventor($

100,000$0,000

$5,000

)ool * +achiner( $&0,000 $10,000 $30,000

!otal #ssets 4 //',''' 4 5-',''' 4 &'&,'''

Account a(able

$

210,000

$

30,000

$

20,000

Ca#ital$

350,000$

120,000

A--itional ai- 'nCa#ital

$.5,000

$20,000

$ $