Change Relearn - Corporate Professionals

118

4/11/2014 Unlearn Change Relearn Companies Act, 2013

Transcript of Change Relearn - Corporate Professionals

4/11/2014

Unlearn Change Relearn

Companies Act, 2013

4/11/2014

Companies Act – Evolution & BackgroundCompanies Act, 2013 – Cynosure of all eyesKey Changes in Select ed Chapters

Chapter I - PreliminaryChapter II - Incorporation & Incidental MattersChapter III – Prospectus & Allotment of SecuritiesChapter IV – Share Capital & DebenturesChapter V – Acceptance of DepositsChapter VII – Management & AdministrationChapter VIII – Declaration and Payment of DividendChapter IX– Accounts of CompanyChapter X – Audit and AuditorsChapter XI – Appointment and Qualification of DirectorsChapter XII – Meetings of Board and its PowersChapter XIII – Appointment and Remuneration of Managerial PersonnelChapter XIV – Inspection, Inquiry and InvestigationChapter XXIX – Miscellaneous

Outline

4/11/2014

Basic Approaches to Companies Act

Modern

4/11/2014

10 Major Contours of Companies Act, 2013

Making corporate sector more accountable and responsible

Protection of Investors including minority shareholders

CSR

Enhancing disclosure to stakeholders

SFIO

Facilitating raising of capital by companies

e-Governance

Holding professionals accountable

Gender equality

4/11/2014

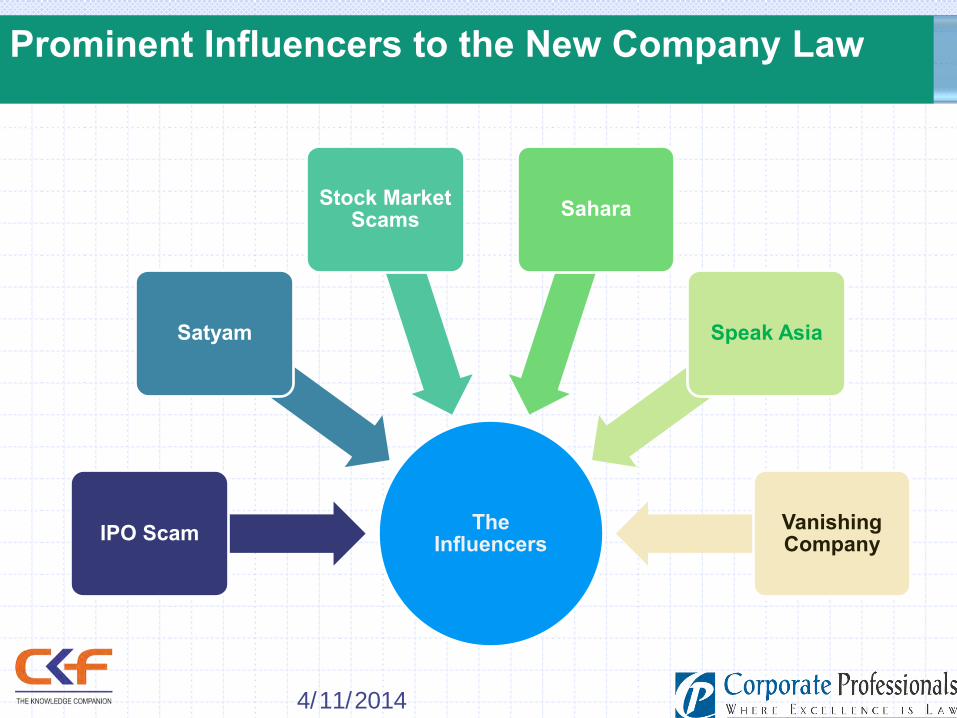

Prominent Influencers to the New Company Law

The InfluencersIPO Scam

Satyam

Stock Market Scams Sahara

Speak Asia

Vanishing Company

4/11/2014

Companies Act, 2013 - cynosure of all eyes

4/11/2014

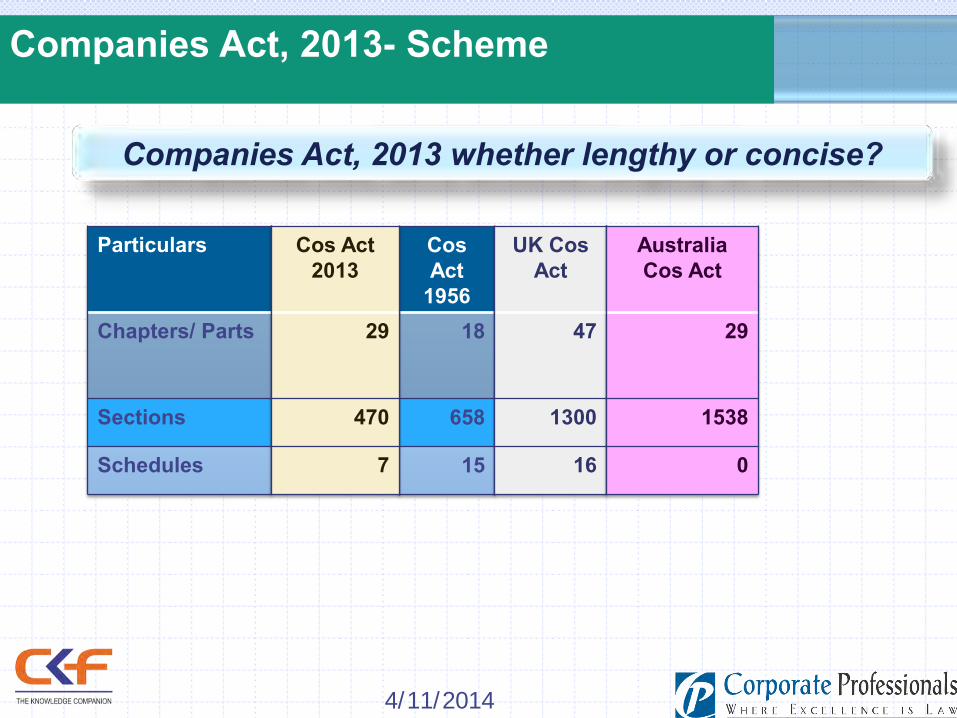

Companies Act, 2013 whether lengthy or concise?

Particulars

Chapters/ Parts

Sections

Schedules

Cos Act

195618

658

15

UK CosAct

47

1300

16

Australia Cos Act

29

1538

0

Cos Act 2013

29

470

7

Companies Act, 2013- Scheme

The Companies Act, 2013Facts about the Act

Rules for 19 Chapters have been Notified

470 Sections –282Sections

Notified

7 Schedules –All Notified

Substantial Part of the Act has been effective form 01st April 2014

• 10 Circulars• 9 Notifications

• 3 Orders for removal of difficulties

have been issued so far

4/11/2014

Classes of Companies Covered in Companies Act, 2013

Entity Structure Recognized under the law

Access to Capital

Listed

Unlisted

Members

OPC

Private company

Public company

Control

Holding Company

Subsidiary Company

Associate Company

Liability

Limited

Shares

Guarantee

Unlimited

Others

Govt. Company

Banking Company

Foreign Company

Size

Small Company

Activity

Dormant Company

Nidhi Company

Producer Company

Body Corporate

4/11/2014

Novelties

One Person Company

Small company

Secretarial & Auditing

standards

Related party

KMP

Control

Dormant Company

Conciliation Panel

SecretarialAudit

Code for ID’s

Corporate SocialResponsibility

Securities Listed Company

Subsidiary and Holding

Company

Subsidiary and Holding

Company

Vigil Mechanism Fraud

4/11/2014

Chapter 1 - Preliminary

4/11/2014

Definitions

Officer in Default (OD) – Section 2(60)Whole time DirectorKMPs &

If no KMPs

All Directors if no one appointedDirectors appointed as OD Or

Any Person Authorized by Board or KMPs

Any Person who advices, directs or instructs BoD

Every Director who is aware of Contravention

For Issue or transfer of Shares

Share Transfer Agent Registrar to Issue Merchant Banker

Rationalization of directors role as liability arises on awareness of contravention through board proceedings or non opposition

4/11/2014

Definitions

Expert - Section 2 (38)

Engineer Valuer

Chartered Accountant

Company Secretary

Cost Accountant Any person who

issues certificate

4/11/2014

Definitions

Foreign Company – Section 2 (42)Means

Any Company or Body Corporate incorporated outside India

Has a Place of business in India whether by Itself or through an agent, physically or

through electronic mode; and

Conducts any business activity In India in any other manner

Electronic mode has been defined which primarily shall include carrying anybusiness electronically whether main server is installed in India or not

4/11/2014

Definitions

Private Company – Section 2(68)

Private Company

Paid Up Capital ≥ Rs. 1 lakh

Transfer of Shares Restricted

Maximum 200 members

4/11/2014

Definitions

Promoter – Section 2(69)

Named in Prospectus

Identified in Annual Return

Control over affairs of the

CompanyAdvices, directs or

instructs BoD

4/11/2014

Small Company – Section 2(85)Private Company

Paid Up Cap < Rs. 50 Lakhs Turnover < Rs. 2 Crores

Excludes

Holding co Subsidiary Co Not for Profit Co.

Paid up capital upto Rs. 25 Crores Net Tangible Assets of Rs. 1

Crores Networth of Rs. 3 Crores

SME in SEBI Law

Particulars Manuf (Inv in P&M)

Services (Inv in Equipments

Micro ≤ Rs. 25 Lakhs ≤ Rs. 10 Lakhs

Small > Rs. 25 Lakhs≤ Rs. 5 Crores

> Rs. 10 Lakhs ≤ Rs. 2 Crores

Medium > Rs. 5 Crores ≤ Rs. 10 Crores

> Rs. 2 Crores ≤ Rs. 5 Crores

SME in MSME Act

Definitions

4/11/2014

Chapter II – Incorporation & Incidental Matters

4/11/2014

Incorporation and Incidental Matters - New

Affidavit from Subscriber onIncorporation – Sec 7(1)(c )

Declaration of Commencement(+ Verification of RO) andSectoral Regulator ApprovalSec 11(1)a & 12(1)

Provision of Entrenchment –Sec 5(3)

Members liability extended to include unpaid share premium – Section 4 (1)(d)(i)

4/11/2014

Incorporation and Incidental Matters - New

*Company defaulted in filling of Annual Return/Financial Statement/Deposits/DebenturesOr interest shall not be allowed to change their name

* Change in object not reflected in thename now calls for change ofname also .

Object clause to state the main objects only, not required to divideinto main, ancillary and other objects

4/11/2014

Companies with Charitable Objects - Sec 8

New activities such as Sports, Education, Research, Protection of

Environment and Social Welfare included

Upon revocation of license, CG in public interest, may wind up the company

or amalgamate it with another similar company

A charitable company can only be amalgamated with a company registered

vide this section and having similar objects

Any amendment to MOA or AOA requires prior CG approval

* For license an estimate of the future annual income and expenditure of

the company for next 3 years is required to be submitted.

4/11/2014

One Person Company

• * Only a natural person who is an Indiancitizen and resident in India can be amember. Or nominee of the sole member ofOne Person Company.

• * Resident in India" means a person whohas stayed in India for a period of not lessthan 182 days during the immediatelypreceding 1 calender year.

• * A person can not form more than oneOPC or become a nominee of OPC.

• * Prohibited to carry out Non-BankingFinancial Investment activities includinginvestment in securities of any bodycorporates.

• * In case if the paid-up capital exceeds 50lakh or average annual turnover exceeds 2crores, the company ceases the status ofOPC.

• * OPC may convert itself into Public orPrivate Company on the other side onlyPrivate Company can convert itself intoOPC.

Only One Shareholder

Minimum One Director

Private Limited

Perpetual Succession

through Nomination

4/11/2014

Chapter III – Prospectus & Allotment of Securities

4/11/2014

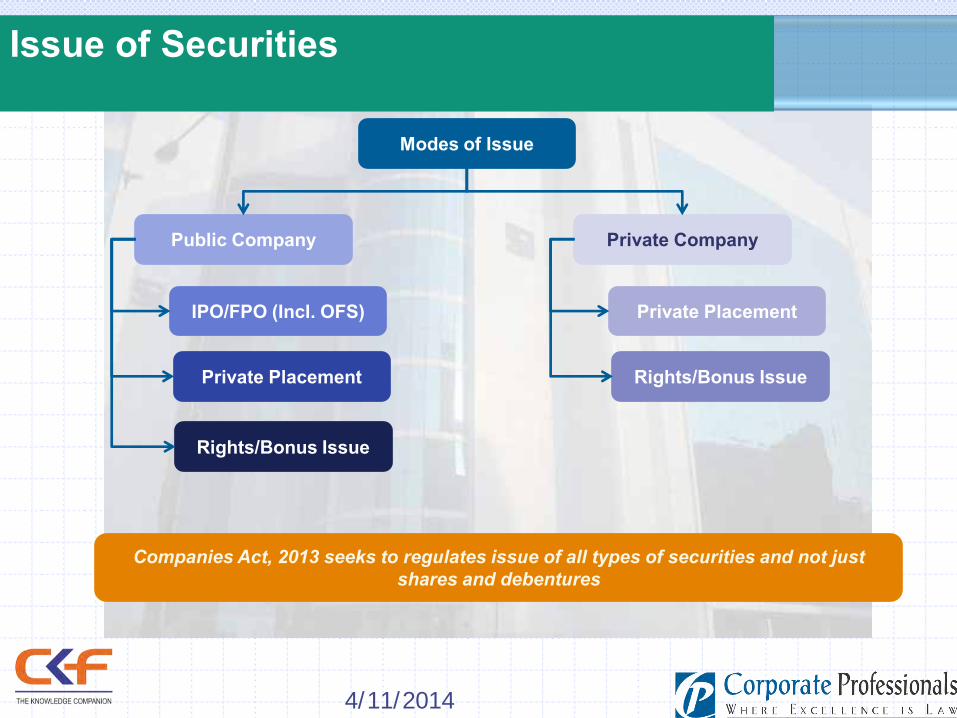

Issue of Securities

Companies Act, 2013 seeks to regulates issue of all types of securities and not just shares and debentures

Modes of Issue

Public Company Private Company

IPO/FPO (Incl. OFS)

Private Placement

Rights/Bonus Issue

Private Placement

Rights/Bonus Issue

4/11/2014

Public Issues (1 of 5)

• Advertisement of prospectus to specify main objects, liability ofmembers, amount of share capital, details of subscribers to MOA andCapital Structure

Offer of Sale – Sec 28

• Offer for sale now specifically defined in the 2013 Act• A document for OFS shall be deemed to be prospectus• Persons desiring to make an OFS shall authorise company to

take necessary actions for OFS and reimburse all theexpenses

• No option to get physical allotment of shares in IPO• Shares to be compulsorily allotted in Demat form by a company

making an IPO and other prescribed classes of companies

• Source of Promoter’s contribution in prescribed manner• * Summary of Reservation or adverse remark of auditors and

the related party transaction since last five financial year• * Acts of material frauds committed against the company in

the last 5 years, if any,

Disclosure in Prospectus –

Sec 26

4/11/2014

Public Issues (2 of 5)

Liability for Mis-statements

Mis-statement

Untrue Statement

Misleading Statement

Liability

Civil - Sec 34 Criminal -Sec 35

Min 6 mthsMax 10 Yrs

Min Amt InvolvedMax 3x Amt Involved

Compensate those who have suffered loss or damage

Withdrawal of consent after issue but before allotment now not a defense

In case of a fraud every person involved personally liable without limitation of liability

Civil Liability for Mis-statements

4/11/2014

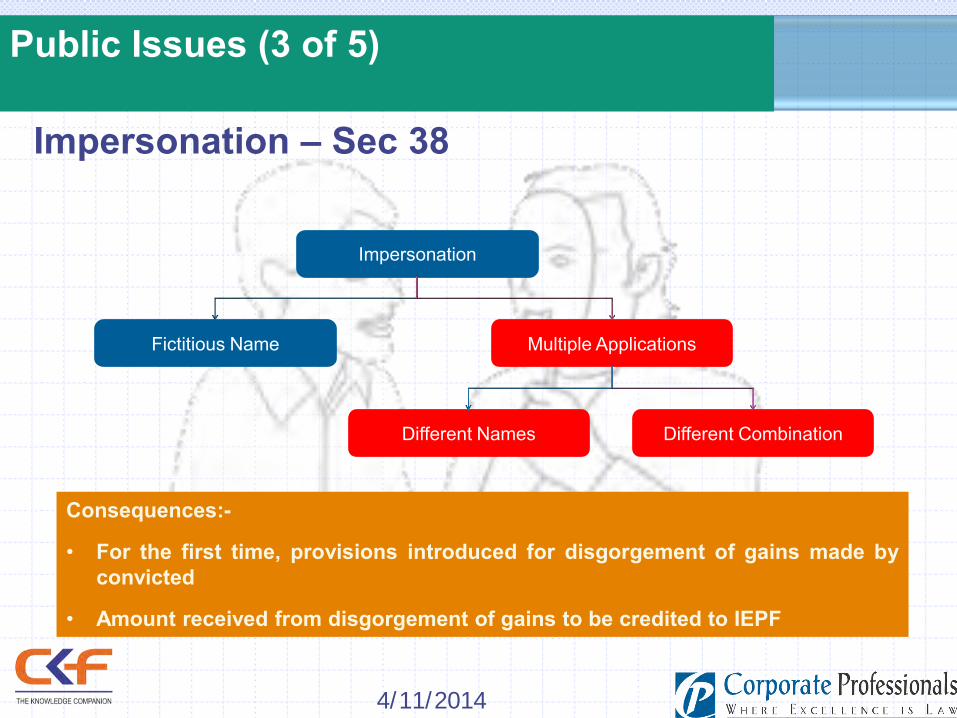

Public Issues (3 of 5)

Impersonation – Sec 38

Impersonation

Fictitious Name Multiple Applications

Different Names Different Combination

Consequences:-

• For the first time, provisions introduced for disgorgement of gains made byconvicted

• Amount received from disgorgement of gains to be credited to IEPF

4/11/2014

Public Issues (4 of 5)

Allotment of Securities – Sec 39

• Return of allotment to be filed for issue of any kind of security

• Power given to SEBI to modify the minimum amount to be paid

on application which shall not be less that 5% of the nominal

amount

• Minimum subscription to be received in 30 days as against

earlier 120 days. Power to SEBI to modify the same

Fraudulent Inducement for Investing money -Sec 36

• Scope of section extended to obtaining credit facilities

from banks or financial institutions

• The offence made non compoundable

• Stringent punishment prescribed under section 447

4/11/2014

Public Issues (5 of 5)

Variation in terms of Contracts or Objects – Sec 27I want to change the terms of

contracts referred to in prospectus or objects of the Issue ?

Its easy pass a ordinary resolution in

general meeting

Its no longer easy

Approval of members by

Special Resolution

Notice of GM to be published in

newspapers giving justification for

variation

Dissenting Shareholders to be given an exit offer

by promoters/ controlling

shareholders

Amount raised in IPO cannot be used for buying, trading or dealing in equity shares of another listed Company

Revised Process

4/11/2014

• 200 investors excluding QIB and ESOP

Max Allotment in One FY

• Allotment to be made within 60 days, else refund @ 12% interest p.a.

• Minimum gap between two offers to be not less than 60 days

• * Minimum investment size of Rs 20,000 per person

• Cash Receipt prohibited

• No fresh offer to be made unless previous offer is completed

• Share application money to be kept in Separate Account.

• * Transfer of shares is permitted

Conditions related to Allotment

Private Placement

In case of Unlisted companies, Issue price to be determined by a Registered Valuer

4/11/2014

Chapter IV – Share Capital & Debentures

4/11/2014

Share Capital & Debentures

Variation of Shareholder Rights – Sec 48

Class A shareholder Class B shareholders

Where variation in rights of any class of shareholders affects other class, then consent of affected class of shareholders also needs to be taken

4/11/2014

Share Capital & Debentures

Issue of Shares at Discount – Sec 53

Issue of Shares at discount isvoid. However Sweat EquityShares are permitted to be issuedat discount

Voting on Preference Shares – Sec 47

Different conditions for voting oncumulative or non cumulative preferenceshares when dividend are in arrearsdispensed with

Now, all preference shareholders areentitled to vote on every resolution onlywhen dividends are in arrears for 2 or moreyears

4/11/2014

Share Capital & Debentures

* Companies can issue pref. shares for

period > 30 years for infrastructure projects

subject to redemption of prescribed % of

shares on annual basis at the option of pref.

shareholders

Companies not in a position to redeem pref.

share or pay dividend can roll them over with

consent of 3/4th in value of pref.

shareholders and approval of Tribunal

Issue of Preference Shares – Sec 55

Consolidation and sub-division of share

capital now not easy

Consolidation and division which results

in changes in voting pattern shall require

prior approval of Tribunal (Minority

Squeeze-out through consolidation)

Alteration of Share capital – Sec 61

4/11/2014

Share Capital & Debentures

Validity of Instruments of transfer, presentation toauthority, for its endorsement etc. dispensed with

No Objection Certificate needs to be taken fromtransferee for transfer of partly paid shares

Appeal to Tribunal on refusal can be made bytransferee only

Transfer and Transmission - Sec 56

Issue of Certificate Old New

On Allotment 3 months for sharesand debentures

6 month for debentures and

2 Months for otherOn Transfer 2month 1 month

4/11/2014

Put-Call Options in SHAs

Contracts having put-call options shall be enforceable

Articles of Association may contain provision for entrenchment

In Private company – agreed by all members

In Public company – Special resolution

SEBI vide notification LAD-NRO/GN/2013-14/26/6667 relaxed this provision & allowed Put/Call ,Tag along / drag along rights in SHA

Conflicting precedents special rights valid if incorporated in AOA

Earlier Position

SEBI Interpretation

4/11/2014

Share Capital & Debentures

All Companies shall issue further share capital after subscription to MOA under this section

Exemption for first 2 years of incorporation or 1 years from date of 1st allotment dispensed

Preferential Allotment shall be made at a price arrived based on the report of the Registered Valuer

Notice period of offer min 15 days and max 30 days

Optionally convertible debentures not to require CG approval

Further Issue of Share Capital – Sec 62

4/11/2014

Share Capital & Debentures

• No reduction of share capital allowed if the company is in arrears for payment of deposits

• Tribunal will give notice to CG, SEBI and Creditors about reduction of share capital

• Accounting Standard specified in Section 133 to be followed and auditor certificate to that effect required

• Publication for reason for reduction now mandatory

• Buy back offer cannot be made within a period of one year from the date of closure of preceding buy back offer

• No provision for Buy Back of shares from odd lots of shares • Compliance of provisions relating to declaration of dividends

necessary.

• Specific Provision relating to Issue of Bonus Shares• * Bonus once declared cannot be withdrawn• CRR can be used to issue bonus• Similar to SEBI ICDR Regulations

Sec 68 & 70

Sec 63 – Bonus Share

Sec 66 - Reduction of Share Capital (Not yet notified)

4/11/2014

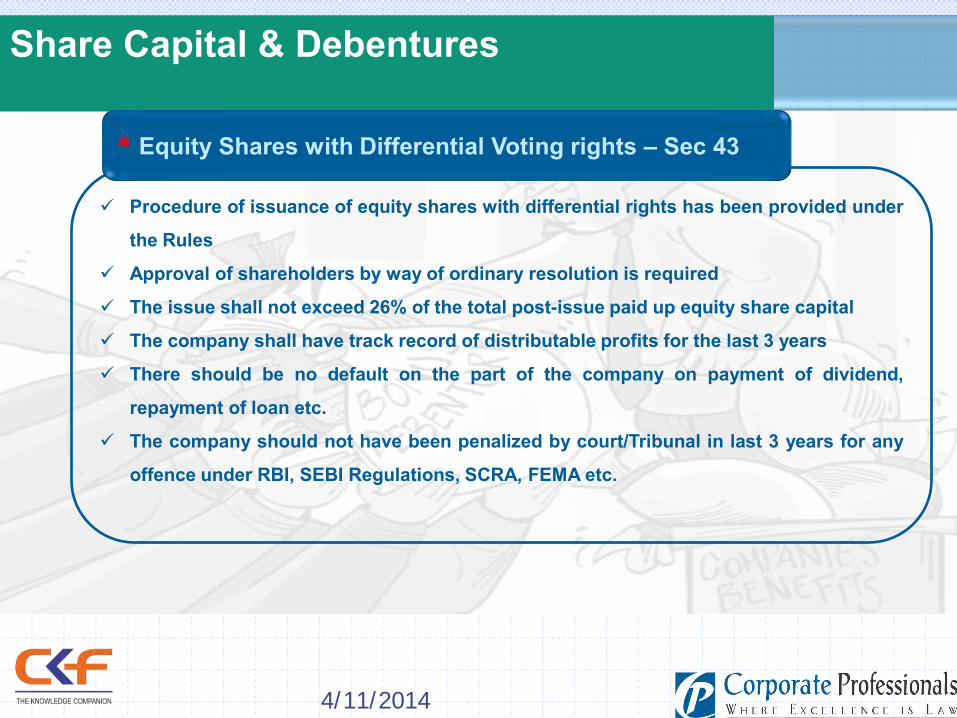

Share Capital & Debentures

Procedure of issuance of equity shares with differential rights has been provided under

the Rules

Approval of shareholders by way of ordinary resolution is required

The issue shall not exceed 26% of the total post-issue paid up equity share capital

The company shall have track record of distributable profits for the last 3 years

There should be no default on the part of the company on payment of dividend,

repayment of loan etc.

The company should not have been penalized by court/Tribunal in last 3 years for any

offence under RBI, SEBI Regulations, SCRA, FEMA etc.

* Equity Shares with Differential Voting rights – Sec 43

4/11/2014

Share Capital & Debentures

Employee shall include permanent employee, director and employee and director of

subsidiary and holding company

The company shall not issue sweat equity shares for more than 15% of the existing

paid up equity share capital in a year or shares of the issue value of five crore,

whichever is higher

The issue shall be valued by a registered valuer and the report of registered valuer

shall be circulated to the shareholders

The amount of sweat equity shares issued shall be treated as part of

managerial remuneration

* Issue of Sweat Equity Shares– Sec 54

4/11/2014

Chapter V – Acceptance of deposits

4/11/2014

Public Deposits – Tougher…

• All companies can accept deposits only

from members

• Any funds received from directors are

exempted from the definition.

• Prior approval of members required for

accepting deposits

• Deposit to be invited by issue of circular to

members

• Where deposits are unsecured it has to be

specifically quoted in every document

inviting deposit

• All the outstanding deposits oncommencement of the Act have to be repaidwithin 1 year from date of maturity or 1 yearfrom commencement if already maturedwhichever is earlier

Accepting Deposits Repayment

Accepting deposit from public no longer easy. Strict requirements to ensure protection of depositor’s interests

• Only prescribed classes of companies having

net worth of INR100 crore or turnover of INR

500 crore are allowed to raise deposits from

public

• Credit rating of deposits compulsory

• Obtaining Deposit Insurance

• Compulsory creation of charge on the assets

of the company within 30 days of acceptance,

if deposits are secured and appointment of

Deposit trustee

Conditions

4/11/2014

Chapter VII – Management & Administration

4/11/2014

Annual Return

Additional information required to be provided in Annual Return

Principal business activity with

particulars of holding, subsidiary and

associate company

Details about other securities issued by

company

Details of Promoters/KMP along

with changes since closure of last FY

Details of meetings of members/class

thereof/BOD/various committee along with

attendance details

Remuneration of Directors and KMP

Details of penalties/punishment

on Co/ directors/ officers/

compounding of offence/ appeals

Details related to certification of compliance,

disclosures, etc

Details of Foreign Institutional Investors if shares held by them

or on their behalf

Such other matters as may be prescribed

Info up to FY closure only

4/11/2014

Certification of Annual Return

* Annual Return of a listed company or

company having paid-up share capital

of R. 10 Crore or more or turnover of Rs.

50 Crore or more shall be certified by a

Company Secretary in practice

4/11/2014

Return to be filed with Registrar in case Promoter’s stake changes – Sec 93

Listed company to file Return in prescribed form with RoC within 15 days in case of change

of * 2% or more in either volume or value of shares held by the Promoters or top 10

shareholders

shareholders

4/11/2014

General Meeting – Sec 100

OPC not required to hold AGM

First AGM to be held within 9 months from

closure of first FY

AGM to be held on between business

hours i.e. 9 AM to 6 PM

Notice of GM may be sent through electronic mode

To be sent to all Directors

21 clear days notice to be given

In case of AGM Shorter notice can be given byconsent of 95% of members who are entitled tovote (like for EGM)

Secretarial Standards mandated

Report of AGM, prepared in prescribed manner,to be filed with RoC

4/11/2014

Statement to be annexed with Notice – Sec 102

Explanatory Statement in case of special business to specify

Nature of interest/ concern

RelativesKMPDirector

and Manager

Other Interest

Financial Interest

Liability in case of non-disclosure or insufficient disclosure in Explanatory Statement

Non-disclosure /insufficient disclosure

Promoter KMPDirector

and Manager

ProfitBenefit

Liable to compensate to Company to the extent of such profit/benefit

Explanatory statement to specify shareholding % ofPromoters/directors/manager/KMP whose shareholding is notless than 2% of paid up capital, incase the special businesstransacted is to affect other Company

Default in sending or providing disclosure in explanatorystatement shall attract fine extending up to Rs. 50000 or 5times of profit or benefit, whichever is more

4/11/2014

Quorum of General Meeting – Sec 103

Quorum (Members to be personally present)

in pub co

No. of members on the day of meeting

5 ≤ 1000

15> 1000 ≤ 5000

30 > 5000

3 days notice (either individually or innewspaper), in case of adjournment ofGM due to lack of quorum or change inday, time or place of adjourned meeting

Single person not to be proxy for more than 50 members

Proxy cannot vote by show of hands

Member of Private Limited company cannot appoint more than 1 proxy

to attend on same occasion

4/11/2014

Others

Postal Ballot – Sect 110 Postal ballot applicable to all companies whether

listed or unlisted. OPC and other companies having upto 200

members are not required to transact any businessthrough postal ballot.

Postal Ballot resolutions to be prescribed by CG.(Other than any businesses in whichdirectors/auditors have the right to be heard at themeeting and ordinary business)

To maintain minutes Not less than 1% of voting power or Member holding min Rs. 5,00,000 paid up share

capital can move Special Notice

Closure of RoM –Sec 88

Listed Company / Company which intends to get listed togive notice of atleast 7 days (or such lesser days asspecified by SEBI) before closure of Register of securityholders

4/11/2014

Others

Maintenance of documents in electronic form – Sect 120Mandatory for Listed Companies or company having not less than 1000

shareholders, debenture holders or other security holders. In case of existing companies data from physical mode to electronic

mode shall be converted within 6 months.

4/11/2014

Chapter VIII – Declaration and Payment of Dividend

4/11/2014

Declaration of Dividends Sec 123

Transfer to reserves before declaring dividends is

now optional

Interim dividend capped at avg. of dividends

declared during last 3 years, if company incurs

loss in preceding quarter

Where company has failed to comply with the

provision of Acceptance of deposits and

repayments it cannot declare dividends until the

non compliance continues

4/11/2014

Unpaid Dividends - Sec 124

Information relating to unclaimed dividends to be uploaded on the website of the company

and CG within 90 days of transfer to unpaid dividend account

Along with the unclaimed amounts, the shares in respect to which they relate are to

transferred to IEPF

The claimants can now apply to IEPF for claiming unpaid amounts/share due/belonging to

them

4/11/2014

Chapter IX– Accounts of Company

4/11/2014

Definitions

Subsidiary – Section 2(87)

Control through one half of the total share capital either at its own or together

with one or more of its subsidiary

Holding Co

Subsidiary Subsidiary

Subsidiary 20%

51%

20%20%

51%

However Layers of

subsidiaries also restricted

Total Share Capital has been defined in the

rules for the definition of subsidiaries

Companies as aggregate of the paid-upequity share capital and convertiblepreference share capital.

4/11/2014

Definitions

Company A Company BAssociate of

Significant Influence

Control of ≥ 20% Share Capital

Control of Business Decisions Under AgreementOR

Associate Company is not a subsidiary, but includes a jointventure company

• Associate Companies to be disclosed in annual report• Definition exists under AS – 18, now brought under

Companies Act• RPT dealings extended to Associate Companies

Associate Company – Section (6)

through

Total Share Capital has been defined in

the rules for the definition of associate

Companies as aggregate of the paid-upequity share capital and convertiblepreference share capital.

4/11/2014

Consolidation of Accounts – Sec 129

Subsidiary to include associates and joint ventures

Mandatory consolidation of accounts in case of subsidiary

The Balance Sheet, the Profit & Loss Account and the cash flow statementhave been collectively defined as the financial statements

Preparation, adoption and audit of the financial statements shall apply mutatismutandis to CFS

Non compliance of this provision shall attract penalty

Statement of subsidiaries shall be in Form AOC-1

Requirement of attaching BS, P&L, BOD and Auditors Report of subsidiarycompanies not stated

No relaxation to accounts of overseas subs - Every company to place separateaudited accounts for each subsidiary on its website, if any

4/11/2014

Directors’ Report

Directors Report, except incase of OPC, to contain:

Extract of Annual Return

Declaration by Independent

Director

Directors’ Responsibility

Statement

Comments/explanation by BOD on Secretarial Audit Report

Particulars of loan/guarantee/

investment

Material changes from end of FY

to date of Report

Statement on risk

management policy

Details of CSR policy developed

and implemented

BOD/Committees performance

evaluation

Other such matters

Statement for evaluation of Board Performance in case of prescribed class of companies

4/11/2014

Chapter X – Audit and Auditors

4/11/2014

Definitions

Financial Statement – Section 2(40)

Balance Sheet

Includes

explanatory notes

Profit & Loss Account

CashflowStatement

Statement of changes in Equity

4/11/2014

Definitions

Financial Year – Section 2(41)Incorporated before 1st Jan

31st March of Current Year 31st March of next Year Yes No

• Transition period of 2 years for existing Cos• Cos having foreign holding or subsidiary cos can follow different year with prior approval of

Tribunal

Audit and Auditors

Every Company to appoint auditor for a term of5 years provided the same shall be ratified bymembers at every AGM

Rotation of audit partner & team at suchintervals as may be prescribed

Cooling period for re-appointment as auditor is5 years

Transition period of 3 years provided fromcommencement of the Act.

The incoming auditor or audit firm shall not beeligible if the outgoing auditor or audit firmunder the same network of audit firms.

* Same network includes the firms operating orfunctioning hitherto or in future, under the samebrand name , trade name or common control .

Special resolution required for appointingauditor other than the retiring auditor or not re-appointing auditor

Appointment of Auditor – Sec 139

Rotation of auditors including audit firmsis being considered for introduction inEU, US, UK and Malaysia.

4/11/2014

Audit and Auditors

Special resolution of members along with CG approvalrequired for removal of auditor before expiry of term.

* Application for removal to be made to the CG within 30days of passing of Board resolution.

On resignation, auditor to file with RoC and Company orCAG incase of Govt. company, a statement indicatingreasons for resignation within 30 days failing which he shallbe penalized

Special notice required for proposing a resolution forchange of auditor except in case of expiry of term of 5/10years

Copy of representation made by auditor who is proposed tobe removed if not sent to member shall be filed with RoC

Tribunal either suo moto or on application direct thecompany to change its auditor, if it is satisfied that he hascommitted fraud

Auditor against whom an order has been passed byTribunal shall be ineligible for appointment in any companyfor 5 years

Removal and Resignation of Auditor – Sec 140

Actuarial services

Investment advisory services

Management services

Internal Audit

Design and implementation of any financial

information system

Rendering of outsourced

financial services

Accounting and book keeping services

Investment banking services

Restriction for the auditors to undertake following specialized services by himself or his

subsidiary or associate company or any other form of entity

Whether following services may be undertaken ?o Tax consultancy and representationo Project financing assignmento Restructuring assignment

Restrictions for the Auditors

Audit Report to contain:

• Qualification, reservation or adverse

remark and reasons thereof

• Whether company has internal controls

and operating effectiveness of internal

financial control system

• Report on Cash Flow and such other

matters as prescribed

• Reasons for required matters not

included or included with qualification

• *Impact, if any, of pending litigations on

its financial position in its financial

statement;

Auditors Report

Audit Report to contain:

• * Any delay in transferring amounts,

required to be transferred, to the Investor

Education and Protection Fund by the

company

• * The Company has/has not made

provision , as required under any law or

accounting standards, for material

foreseeable losses, if any, on long term

contracts including derivative contracts;

Auditors Report

• Qualification, observation or comments on financial transactions or matters mentioned in

Audit Report, which have adverse effect on functioning of Company, shall be read in GM

• Any fraud detected immediately to report to CG

4/11/2014

Mandatory Internal Audit

Every Listed

Company

* Every public company

having paid-share capital

of Rs. 50 crores or more OR

turnover of Rs. 200 Crore or more

OR having borrowings from

banks/financial institutions/

exceeding Rs. 100 crores OR outstanding

Deposits of 25 crore or more

4/11/2014

Mandatory Internal Audit

* Every Private Company having

Turnover of 200 Crore or more

* Private Company having loans or

borrowings from

banks/financial institutions/

exceeding

Rs. 100 crores at any point of time

during the preceding FY

4/11/2014

Depreciation

No Separate depreciation rate including for extra shift

Depreciation of assets over its useful life

Depreciable Amount = Amount of an Asset or amount substituted for cost Less its

residual value

Useful life has been differently prescribed in Schedule II to Companies Act, 2013

and Schedule XIV of Companies Act, 1956

4/11/2014

Chapter XI – Appointment and Qualification of Directors

Audit and Auditors - Sec 143Audit and Auditors Sec 141Bird view to Provisions

At least one Women Director in prescribed class or classesof company

At least one Resident Director

Concept of Independent directorintroduced for the first time in Companies Act, 2013

Only Listed Companies may appointone director elected by small shareholder

Nomination of Director by memberhas been made Costlier

Candidate failed to be appointedas director by member shall not beappointed as Additional Director

Alternate Director shall be appointedonly if the original director is outof India for not less than 3 months

Resigning Director shall be liablefor the acts done by him duringhis tenure

Rubber Stamp Directors: Absence in meeting for a consecutivePeriod of 12 months shall made his Office vacant. They shall also beLiable to file Annual Statements orAnnual Returns, failing which for 3Years or failed to repay deposit,Interest.

Audit and Auditors - Sec 143

4/11/2014

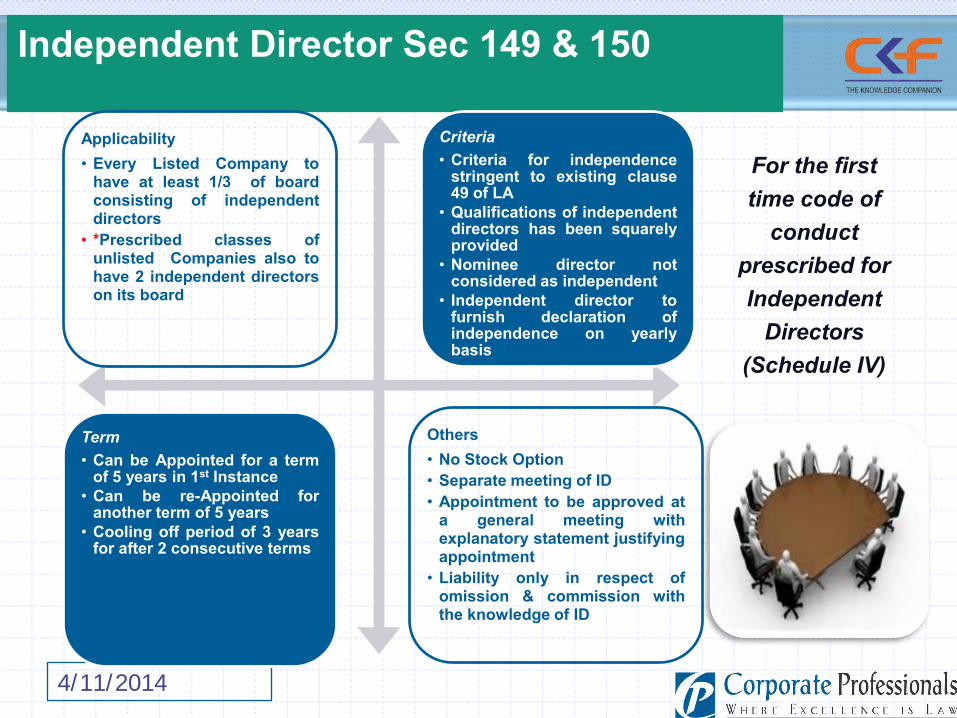

Audit and Auditors Sec 141Independent Director Sec 149 & 150

Applicability• Every Listed Company to

have at least 1/3 of boardconsisting of independentdirectors

• *Prescribed classes ofunlisted Companies also tohave 2 independent directorson its board

Criteria• Criteria for independence

stringent to existing clause49 of LA

• Qualifications of independentdirectors has been squarelyprovided

• Nominee director notconsidered as independent

• Independent director tofurnish declaration ofindependence on yearlybasis

Term• Can be Appointed for a term

of 5 years in 1st Instance• Can be re-Appointed for

another term of 5 years• Cooling off period of 3 years

for after 2 consecutive terms

Others• No Stock Option• Separate meeting of ID• Appointment to be approved at

a general meeting withexplanatory statement justifyingappointment

• Liability only in respect ofomission & commission withthe knowledge of ID

For the first time code of

conduct prescribed for Independent

Directors (Schedule IV)

Audit and Auditors - Sec 143

4/11/2014

Audit and Auditors Sec 141Final Rules

Particulars Class of Companies

Women Director* Listed Companies + Public Company having paid up

capital of 100 crore or more/ turnover of Rs. 300 Crore or more

1/3rd of BOD to be ID’s in case of listed companies and atleast 2 ID’S in Public Companies having

* Public Companies havingPaid up capital 10 crore or

Turnover of 100 CrOr

Companies having o/s loans/deposits /debentures exceeding Rs. 50 crore +

Vigil Mechanism * Companies accepting deposit for public + Companies borrowed money from Banks/PFIs in excess of 50 crore

Audit committee & Nomination and Remuneration committee

• Public Companies having Paid up capital of 10 crore +

OrTurnover of 100 crore +

OrO/s loan/deposit of 50 crore +

4/11/2014

Chapter XII – Board of Directors and its Meeting

Audit and Auditors - Sec 143

4/11/2014

Audit and Auditors Sec 141Board Composition

Women Director

Independent Director

Resident Director

Small Shareholder

Director

Number of directors

2Private

Company

3Public

Company

Maximum Number: 15 (earlier 12)

Directorship of directors

Director in maximum 20 companies including Alternate Directorship

Public Companies or Subsidiariesof Public Companies

Maximum 10

No. of Directorships can be reduced by passing special resolution by members

4/11/2014

Notice to be sent to all the directors,

through electronic means or others

Board of Directors may participate

through video conferencing

Presence of at least 1 ID required in the

meeting called at shorter notice.

Else decision to be circulated to all the

directors and to be valid only after

ratification by at least one ID

One person company, dormant company

and small company are required to held

one meeting in each half a calendar year

and gap between 2 meetings not to be

less than 90 days.

Meeting of Board

4/11/2014

Participation in meeting through video

conferencing allowed

Confirmation of accuracy of draft minutes

by every directors who attended meeting

within 7 days of receipt of draft minutes

Matters not to be dealt in meeting through

video conferencing

To approve the annual financial

statements; and

To approve the board’s report

To approve prospectus

The audit committee meetings for

consideration of accounts

To approve merger , amalgamation,

demerger, acquisition and takeover

Meeting through Video Conferencing

4/11/2014

Insufficient quorum shall now be not

allowed as a defense for non

compliance with frequency of

Board meeting Provision of quorum for meetings of

board are not applicable on One person

company having only one director

Quorum for Board Meeting

4/11/2014

Notice to be sent to all directors

whether in India or outside India

Approval of majority of all Directors

required.

In case of decent of 1/3rd of the

BoDs, then the resolution shall be

decided at the meeting and not by

circulation

Draft Resolution may be circulated to

the directors along with necessary

papers by e-mail or fax

Circular Resolution

4/11/2014

New and Mandatory Committees

4/11/2014

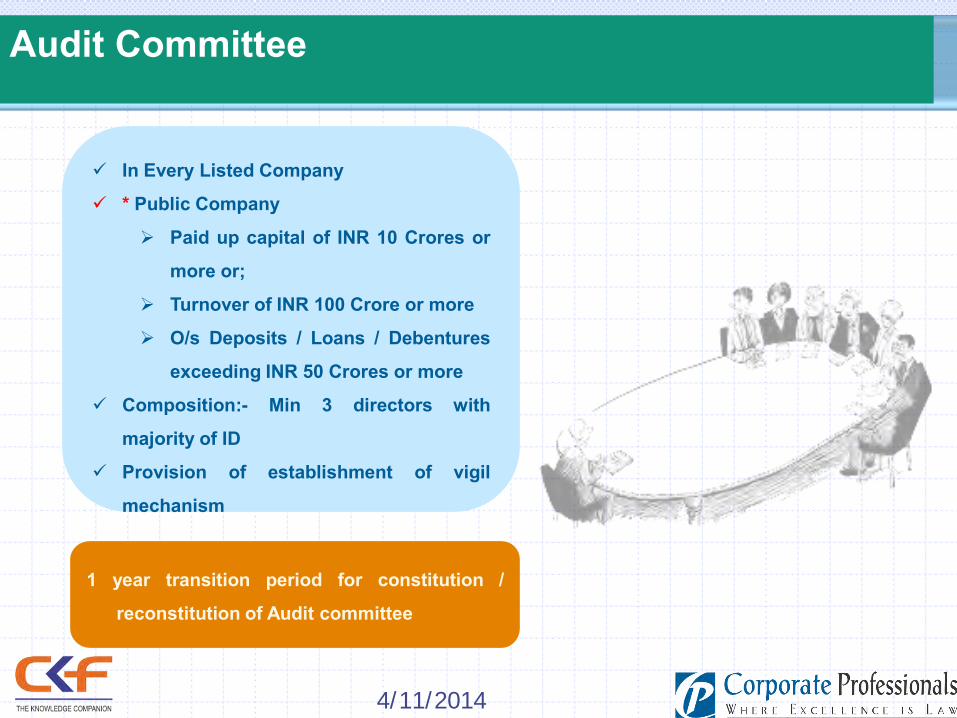

In Every Listed Company

* Public Company

Paid up capital of INR 10 Crores or

more or;

Turnover of INR 100 Crore or more

O/s Deposits / Loans / Debentures

exceeding INR 50 Crores or more

Composition:- Min 3 directors with

majority of ID

Provision of establishment of vigil

mechanism

Audit Committee

1 year transition period for constitution /

reconstitution of Audit committee

4/11/2014

In Every Listed Company

* Public Company

Paid up capital of INR 10 Crores or

more or;

Turnover of INR 100 Crore or more

O/s Deposits / Loans / Debentures

exceeding INR 200 Crores or more Composition:- Min 3 Non executive

directors. ≥ ½ comprising IDs.

Mandate of the Committee:-• Identification of qualified Directors

and senior management personnel

• Performance evaluation of directors

• Recommend to the Board policy forremuneration of Directors, KMPsand other employees

Nomination and Remuneration Committee

4/11/2014

In Every Company having more that1,000 debenture / deposit / securityholders.

Composition:- to be decided by BoD.Chairperson to be an NED.

Mandate of the Committee:-• Consider and resolve the grievances

of Securities holders.

Stakeholders Relationship Committee

4/11/2014

Remuneration to director

Type NE Director

Independent Director Executive Director

SalaryCommissionESOPSitting Fee

4/11/2014

Amount of sitting fees payable to be maximum of

Rs.1 lakh per meeting of the Board or committee

Board may decide different sitting fee

* Sitting fee for independent director and woman

directors not to be less than sitting fees payable

to other directors

Independent director shall not be entitled to any

stock options

Remuneration to director

• Listed Company to disclose in Board Report the ratio of

remuneration of each director to the median employee’s

remuneration

• Premium paid on Director’s & Officer’s insurance not to

be part of remuneration

• No CG approval required for making payment of salary to

the Non Executive Director’s by way of monthly payment

provided that its within the limits

Net Profit Approval from

> 11% Central Govt

Inadequate or no profit

Comply with Schedule V or Central Govt

approval

Overall max remuneration & max remunerationin case of absence/inadequate profit

WD / WTD Who receives Commission Company

Holding Company

Subsidiary Company

Can also receives Commission / Remuneration

4/11/2014

Enhanced Duties, Responsibilities

To act in accordance with the company’s Articles

To act in good faith in order to promote the objects of the company

Exercise his duties with due and reasonable care, skill and diligence.

Not to have a direct or indirect interest that conflicts, or possibly may conflict, with the interest of the company.

Director shall not achieve or attempt to achieve any undue gain or advantage either to himself or to his relatives, partners, or associates.

Shall not assign his office and any assignment so made shall be void

Duties of Director

4/11/2014

Powers of Board

4/11/2014

Following powers shall be exercised by

the Board only at their meeting:-

• Issue of Securities – Equity,

Preference, Debentures

• Give guarantee or provide security in

respect of loans

• Approve financial statements and

Director’s report

• To make political contribution

• To fill a casual vacancy in the board

• To commence a new business

• * To appoint internal & Secretarial

auditor

Matters to be considered only at meeting of the Board

4/11/2014

Following powers shall be exercised by

the Board only at their meeting:-

• * To appoint or remove key

managerial personnel (KMP)

• * To buy, sell investments held by the

company (other than trade

investments), constituting 5% or

more of the paid – up share capital

and free reserves of the investee

company;

• * To invite or accept or renew public

deposits and related matters;

• * Approval of financial statements or

financials

Matters to be considered only at meeting of the Board

4/11/2014

Restrictions on powers of Board

4/11/2014

Restrictions on powers of Board

Restriction for sale of undertaking

applicable to all classes of companies

Term “Undertaking” and “Substantial

Undertaking” has now been defined

Borrowing in excess of the paid –up

capital & free reserves

A special resolution is required to

be passed instead of Ordinary

resolution

4/11/2014

Related Party Transactions

4/11/2014

Definitions

Related Party – Section 2 (76)Company

Director or his Relative

KMP or his Relative

Partnership Firm in which

partner

Private Company in

which member or

director

Public Company in

which member or

director

Holding Company

Subsidiary & Associate

Fellow Subsidiaries

Body Corporate Advised

Directed or instructed

Person who Advises

Directs or instructs

Director, manager or his Relative

Related Parties under various legislations

4/11/2014

Definitions

Related Party – Section 2 (77)Relative

Father (including

Step father)

Mother (including

Step Mother)

Son (including Step Son

Son’s wife Daughter

14 persons have been excluded from the definition of Related Parties

Daughter Husband Brother

(including Step Brother)

Sister(including Step Sister

4/11/2014

Related Party Transactions

Prior approval of CG for any RPT or appointment to

any office or place or profit NOT required

Transaction related to any kind of property are also

covered

Exemption granted to transactions in ordinary

course of business made at arm’s length price

Member who is a related party shall not vote on the

resolution

4/11/2014

Related Party Transactions

Transactions to be Approval by Special Resolution :

RPTs for companies having paid up capital of 10

crore rupees; or

Appointment to any office or place of profit in

the company, its subsidiary company or

associate company at a monthly remuneration

exceeding Rs 2.5 lakhs

Remuneration for underwriting the subscription

of any securities or derivatives thereof of the

company exceeding 1% of the net worth

4/11/2014

Related Party Transactions

Transactions to be Approval by Special Resolution :

Sale, purchase or supply of any goods or

materials directly or through appointment of

agents exceeding 25% of the annual turnover

Selling or otherwise disposing of, or buying,

property of any kind directly or through

appointment of agents exceeding10% of net

worth

Leasing of property of any kind exceeding ten

percent. of the net worth or exceeding 10%

percent. of turnover

Availing or rendering of any services directly or

through appointment of agents exceeding 10%

of the net worth

4/11/2014

Disclosure in explanatory statement to be annexed

to the notice

name of the related party ;

name of the director or key managerial

personnel who is related, if any;

nature of relationship;

nature, material terms, monetary value and

particulars of the contract or arrangement;

any other information relevant or important

for the members to take a decision on the

proposed resolution.

Every RPT shall be reported in the Board’s Report

along with justification for entering into the same

Disclosures of related party transaction

4/11/2014

Restrictions on Non-Cash Transactions

Director of a company or of its holding/

subsidiary/Associate company or any

connected person can not acquire

assets for consideration other than cash

from the company & vice versa.

Approval at a general meeting is

required

If the Director or connected person is

director of holding company then

approval of holding company in general

meeting is also required

Valuation of the assets by registered

valuer

4/11/2014

Forward dealing in the shares and

debentures of a company, its holding,

subsidiary or associate by Directors

and KMPs is prohibited

Banned contracts include both forward

contracts and option contracts

Securities acquired in violation to be

surrendered to company

Restriction on Directors, KMP and any

order person for indulging in Insider

trading

Communication required in ordinary

course of business or under law

exempted

Prohibition on Forward Dealing / Insider Trading

4/11/2014

Chapter XIII – Appointment and Remuneration of Managerial Personnel

4/11/2014

Definitions

Key Managerial PersonnelCEO OR Managing Director

Company Secretary

Whole time Director

CFO

+

+

OR ManagerOR

4/11/2014

Appointment of MD/WTD/Manager/KMP

• Minimum age 21 years (as per old act 25 years)

and maximum 70 years

• Notice of BM/GM – T&C of appointment,

remuneration and other matters to be included

4/11/2014

• KMP not to hold office in > 1 Company

except in Subsidiary Company at the

same time

KMP can be director with

permission of BOD

• KMP vacancy to be filled up by BOD

within 6 months at BM

Appointment and Removal of KMP

When Director fails to attend all Board

Meetings for consecutive period of 12 months,

even when the leave of absence has been

granted

When Director is disqualified by an order of

court or Tribunal under any Act not only the

Companies Act.

When all directors have vacated the office:

the promoter shall appoint minimum

number of directors

Central Government may appoint

Directors till company makes

appointment in General Meeting

4/11/2014

Vacation of office of directors

4/11/2014

Chapter XIV – Inspection, Inquiry and Investigation

4/11/2014

Investigation into the affairs of the Company by SFIO

Receipt of Report from Registrar/

Inspector u/s 208

Special Resolution for

investigating the affairs of the

company

Public Interest

may order

Request from any department of Central Govt or State Govt

Central Govt

Serious Fraud Investigation

Office

Investigation Report

may direct SFIO to initiate

prosecution against the company &

officer

Investigation officer will

investigate the affairs of the

company

• SFIO commands authority over other Investigation Agencies of CG/State Govt• SIFO to provide copy of Investigation Report to other agencies who were carrying out

investigation

Search and Seizure

Power to Arrest

Powers

4/11/2014

Fraud and Penal Provisions

4/11/2014

Fraud – Section 447

Act

Fraud

Omission Concealment of fact

With intent to

Abuse of position

Deceive Gain undue advantage from Injure

Interests of

Company Shareholders Creditors Any other person

Whether or not there is

Wrongful gain Wrongful loss

4/11/2014

Fraud

“wrongful gain” means the gain by unlawful means of property to which the person gaining is

not legally entitled

“wrongful loss” means the loss by unlawful means of property to which the person losing is

legally entitled.

All offenses covered u/s 447 cognizable and non bailable unless excepted

Punishment

Min 6 mthsMax 10 Yrs

Min Amt InvolvedMax 3x AmtInvolved

4/11/2014

Chapter XXIX – Miscellaneous

4/11/2014

Dormant Company – Sec 455

Dormant Company

Inactive Company

For future Projects

To hold IPRs

To hold Assets

On Application to be made to ROC in MSC- 1 for the status of a dormant company and issue

certificate to that effect

Company to have minimum directors and file annual returns to retain status

Company can become active anytime by filing application with ROC

Having no Significant Accounting

Transactions

4/11/2014

Secretarial Audit – Sec 204

Secretarial Audit

Public Company Paid-up Capital < 50 Cr

Turnover < 250 CrListed Company &

• Audit to be conducted by a Practising Company Secretary

• Audit of secretarial and related records• Secretarial Audit Report to form a part of Board

Report• BOD to explain in full any qualification or

observation or other remarks made in the report

Same Powers & Duties as of Statutory Auditor

4/11/2014

We must Analyze the whole Structure and

Systems of our organization and take necessary

Actions to Align them with new Legal

Environment...

What we need to do