CHAMPAIGN COUNTY ADMINISTRATIVE SERVICES · In August, the Champaign County unemployment rate of...

43

CHAMPAIGN COUNTY ADMINISTRATIVE SERVICES 1776 East Washington Street, Urbana, Illinois 61802-4581 ADMINISTRATIVE, BUDGETING, PURCHASING, & HUMAN RESOURCE MANAGEMENT SERVICES Debra Busey, County Administrator November 10, 2015 To the Honorable Chair and Members of the Champaign County Board: In accordance with Resolution No. 9225 Establishing the Budget Process Fiscal Year 2016 approved by the County Board on May 21, 2015, and pursuant to 55 ILCS 5/6-1001, please accept the FY2016 budget for funding Champaign County government’s programs and services. This total budget is presented with $123,108,389 in revenue, and $124,914,480 in expenditure. ECONOMIC ENVIRONMENT The economy – at all levels – national, state and local, continues to display slow growth in the aftermath of the 2007-2009 recession. The Congressional Budget Office (CBO) predicts that although the economy’s growth was weak early in 2015, recent data indicates that the economy is now on firmer ground and CBO expects the pace of economic activity to pick up in the second half of this calendar year, and over the next few years. The CBO also estimates that the economy will have an impact on the elevated unemployment rate and relatively low rate of participation in the labor force with projections that the unemployment rate will fall from 5.7% at the beginning of 2015 to 5.2% in the fourth quarter, and to 5% by the 4 th quarter of 2017. The Illinois economy continues its latest expansion which began in March 2012. The University of Illinois Flash Index provides a quick reading on the state of the Illinois economy. The September Flash Index fell from 106.5 in August to 106.0 in September, and has fluctuated between 106 and 107.2 since May 2013. The Flash Index is a weighted average of Illinois growth rates in corporate earnings, consumer spending and personal income. Tax receipts from corporate income, personal income and retail sales are adjusted for inflation before growth rates are calculated. The growth rate for each component is then calculated for the preceding 12-month period. A reading of 100 or above indicates an expanding economy while a reading below 100 indicates an economy which is contracting. The unemployment rate in the State is at 5.6% as of August, which is 0.4% higher than the national rate of 5.2%. Compared to its neighboring states, Illinois has demonstrated slower job growth from the last quarter of 2014 to the first quarter of 2015 with Illinois job growth at 0.37%. The rates for neighboring states are: Michigan (1.11%), Wisconsin (0.84%), Indiana (0.75%), Missouri (0.64%), Iowa (0.64%), and Kentucky (0.54%). The current lack of a State budget contributes to a business climate that is not conducive to new job growth at the current time. In August, the Champaign County unemployment rate of 4.9% was better than the State of Illinois rate of 5.6% and the national rate of 5.2%, and represented a significant improvement over the August 2014 unemployment rate in Champaign County of 7.4%. Top employers in Champaign County include the University of Illinois at number 1 and Carle Clinic and Hospital as number 2. Typically these employers provide stability to the local employment statistics as the trend is that they (217) 384-3776 WWW.CO.CHAMPAIGN.IL.US (217) 384-3896 FAX

Transcript of CHAMPAIGN COUNTY ADMINISTRATIVE SERVICES · In August, the Champaign County unemployment rate of...

CHAMPAIGN COUNTY ADMINISTRATIVE SERVICES

1776 East Washington Street, Urbana, Illinois 61802-4581

ADMINISTRATIVE, BUDGETING, PURCHASING, & HUMAN RESOURCE MANAGEMENT SERVICES

Debra Busey, County Administrator

November 10, 2015 To the Honorable Chair and Members of the Champaign County Board: In accordance with Resolution No. 9225 Establishing the Budget Process Fiscal Year 2016 approved by the County Board on May 21, 2015, and pursuant to 55 ILCS 5/6-1001, please accept the FY2016 budget for funding Champaign County government’s programs and services. This total budget is presented with $123,108,389 in revenue, and $124,914,480 in expenditure. ECONOMIC ENVIRONMENT The economy – at all levels – national, state and local, continues to display slow growth in the aftermath of the 2007-2009 recession. The Congressional Budget Office (CBO) predicts that although the economy’s growth was weak early in 2015, recent data indicates that the economy is now on firmer ground and CBO expects the pace of economic activity to pick up in the second half of this calendar year, and over the next few years. The CBO also estimates that the economy will have an impact on the elevated unemployment rate and relatively low rate of participation in the labor force with projections that the unemployment rate will fall from 5.7% at the beginning of 2015 to 5.2% in the fourth quarter, and to 5% by the 4th quarter of 2017. The Illinois economy continues its latest expansion which began in March 2012. The University of Illinois Flash Index provides a quick reading on the state of the Illinois economy. The September Flash Index fell from 106.5 in August to 106.0 in September, and has fluctuated between 106 and 107.2 since May 2013. The Flash Index is a weighted average of Illinois growth rates in corporate earnings, consumer spending and personal income. Tax receipts from corporate income, personal income and retail sales are adjusted for inflation before growth rates are calculated. The growth rate for each component is then calculated for the preceding 12-month period. A reading of 100 or above indicates an expanding economy while a reading below 100 indicates an economy which is contracting. The unemployment rate in the State is at 5.6% as of August, which is 0.4% higher than the national rate of 5.2%. Compared to its neighboring states, Illinois has demonstrated slower job growth from the last quarter of 2014 to the first quarter of 2015 with Illinois job growth at 0.37%. The rates for neighboring states are: Michigan (1.11%), Wisconsin (0.84%), Indiana (0.75%), Missouri (0.64%), Iowa (0.64%), and Kentucky (0.54%). The current lack of a State budget contributes to a business climate that is not conducive to new job growth at the current time. In August, the Champaign County unemployment rate of 4.9% was better than the State of Illinois rate of 5.6% and the national rate of 5.2%, and represented a significant improvement over the August 2014 unemployment rate in Champaign County of 7.4%. Top employers in Champaign County include the University of Illinois at number 1 and Carle Clinic and Hospital as number 2. Typically these employers provide stability to the local employment statistics as the trend is that they

(217) 384-3776 WWW.CO.CHAMPAIGN.IL.US (217) 384-3896 FAX

are more insulated against economic volatility. However, the recession of 2007-2009 impacted these employers more so than in previous recessions, contributing to the County’s unemployment experience that more closely mirrored that at the state and national levels. The equalized assessed value of all parcels in Champaign County, including farm, industrial, commercial and residential, increased 1.53% with the 2014 real estate assessments, and is projected at a 1.9% increase in 2015. Median home sale prices in the Champaign-Urbana area rose from $142,800 in the 2nd quarter of 2014 to $145,200 in the 2nd quarter of 2015 – a 1.7% increase. From 2011 to 2013, the EAV had declined and median home prices had also declined. The fact that in 2014 and 2015 the trend of declining values has reversed and stabilized reflects positive indicators for slow but stable growth and recovery in the real estate market. Local retail sales receipts indicate sluggish growth so far in 2015. The general county-wide quarter cent sales tax is year-to-date 0.54% lower than 2014, and the Public Safety quarter cent sales tax which is collected on all retail sales with the exception of vehicles registered with the State of Illinois is 1.85% below 2014 year-to-date receipts. The 1% sales tax collected only in the unincorporated areas of the County reflects a more negative trend, performing at a 19% decrease year to date. This sales tax largely reflects the agricultural economy, and is believed to be down as a result of expired federal tax incentives resulting in producers holding off on making agricultural purchases. The net effect demonstrates a flat to slight decline in the local economy. The County financial outlook will continue to be impacted by the difficulty faced by the State of Illinois and the fact that it is currently four months into a fiscal year with no budget, and no immediate expectation that a budget will be adopted. At the end of the first quarter of the current State fiscal year, its revenues were down $1billion, and the Comptroller predicts the backlog of bills will reach $8.5 billion by December. Local social service agencies have already experienced funding cuts resulting in loss of services, particularly in the areas of mental health and substance abuse. The County will continue to watch the discussions and legislative resolutions at the State level, particularly in light of the potential negative impact some of those decisions could have on local governments and the local economy. LONG-TERM and STRATEGIC PLANNING The County Board updated its Strategic Plan in 2015 which is presented in the Introductory Section of this Budget document. The following table identifies the goals with specific County Board initiatives, current or planned activities, and ultimate outcomes to be achieved from the perspectives of both long term and short term planning.

ii

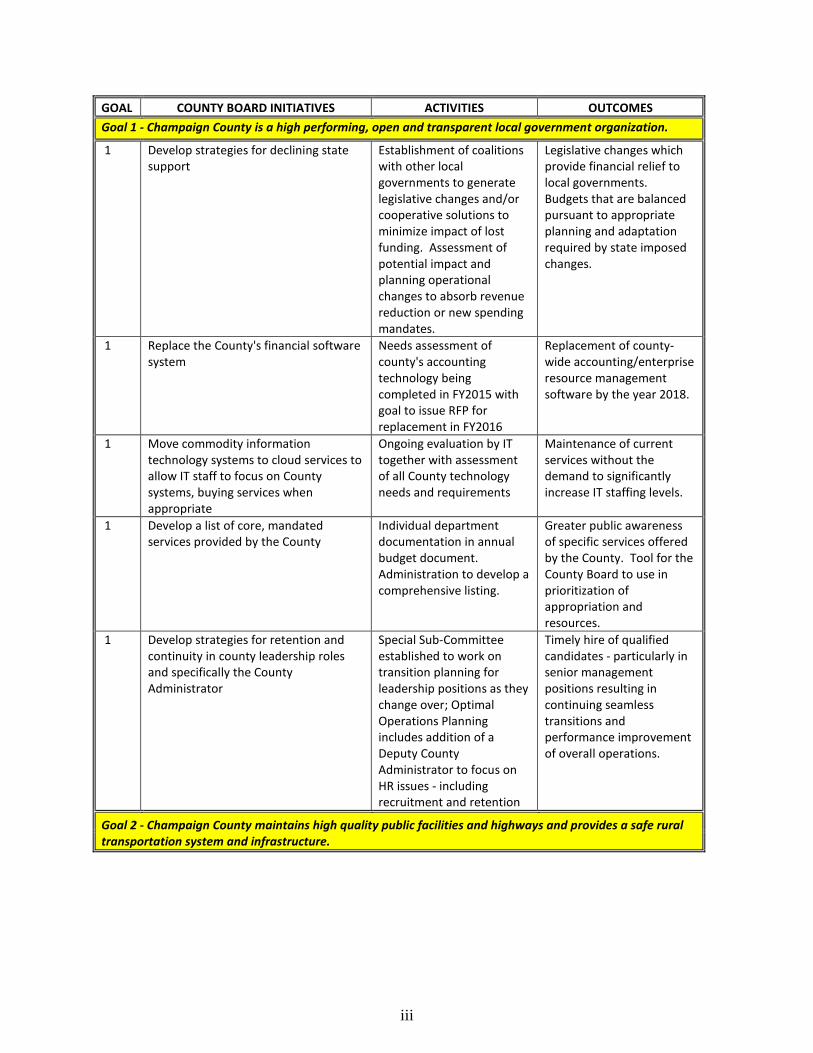

GOAL COUNTY BOARD INITIATIVES ACTIVITIES OUTCOMES Goal 1 - Champaign County is a high performing, open and transparent local government organization.

1 Develop strategies for declining state support

Establishment of coalitions with other local governments to generate legislative changes and/or cooperative solutions to minimize impact of lost funding. Assessment of potential impact and planning operational changes to absorb revenue reduction or new spending mandates.

Legislative changes which provide financial relief to local governments. Budgets that are balanced pursuant to appropriate planning and adaptation required by state imposed changes.

1 Replace the County's financial software system

Needs assessment of county's accounting technology being completed in FY2015 with goal to issue RFP for replacement in FY2016

Replacement of county-wide accounting/enterprise resource management software by the year 2018.

1 Move commodity information technology systems to cloud services to allow IT staff to focus on County systems, buying services when appropriate

Ongoing evaluation by IT together with assessment of all County technology needs and requirements

Maintenance of current services without the demand to significantly increase IT staffing levels.

1 Develop a list of core, mandated services provided by the County

Individual department documentation in annual budget document. Administration to develop a comprehensive listing.

Greater public awareness of specific services offered by the County. Tool for the County Board to use in prioritization of appropriation and resources.

1 Develop strategies for retention and continuity in county leadership roles and specifically the County Administrator

Special Sub-Committee established to work on transition planning for leadership positions as they change over; Optimal Operations Planning includes addition of a Deputy County Administrator to focus on HR issues - including recruitment and retention

Timely hire of qualified candidates - particularly in senior management positions resulting in continuing seamless transitions and performance improvement of overall operations.

Goal 2 - Champaign County maintains high quality public facilities and highways and provides a safe rural transportation system and infrastructure.

iii

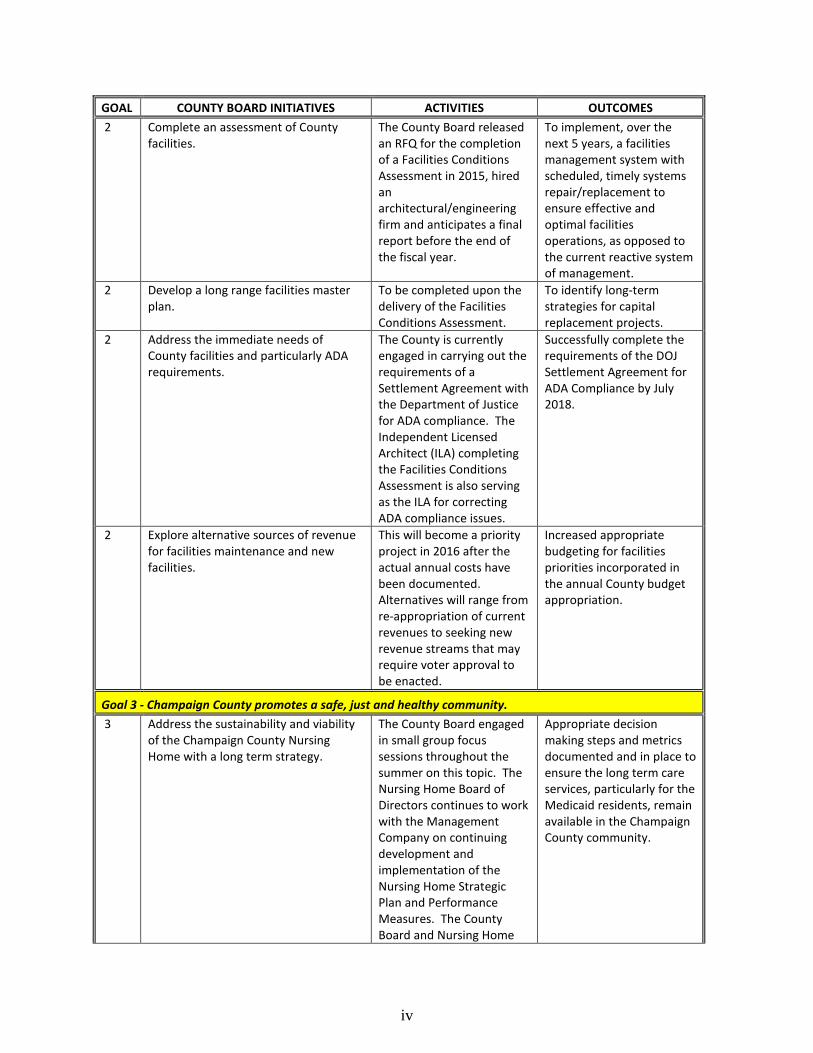

GOAL COUNTY BOARD INITIATIVES ACTIVITIES OUTCOMES 2 Complete an assessment of County

facilities. The County Board released an RFQ for the completion of a Facilities Conditions Assessment in 2015, hired an architectural/engineering firm and anticipates a final report before the end of the fiscal year.

To implement, over the next 5 years, a facilities management system with scheduled, timely systems repair/replacement to ensure effective and optimal facilities operations, as opposed to the current reactive system of management.

2 Develop a long range facilities master plan.

To be completed upon the delivery of the Facilities Conditions Assessment.

To identify long-term strategies for capital replacement projects.

2 Address the immediate needs of County facilities and particularly ADA requirements.

The County is currently engaged in carrying out the requirements of a Settlement Agreement with the Department of Justice for ADA compliance. The Independent Licensed Architect (ILA) completing the Facilities Conditions Assessment is also serving as the ILA for correcting ADA compliance issues.

Successfully complete the requirements of the DOJ Settlement Agreement for ADA Compliance by July 2018.

2 Explore alternative sources of revenue for facilities maintenance and new facilities.

This will become a priority project in 2016 after the actual annual costs have been documented. Alternatives will range from re-appropriation of current revenues to seeking new revenue streams that may require voter approval to be enacted.

Increased appropriate budgeting for facilities priorities incorporated in the annual County budget appropriation.

Goal 3 - Champaign County promotes a safe, just and healthy community. 3 Address the sustainability and viability

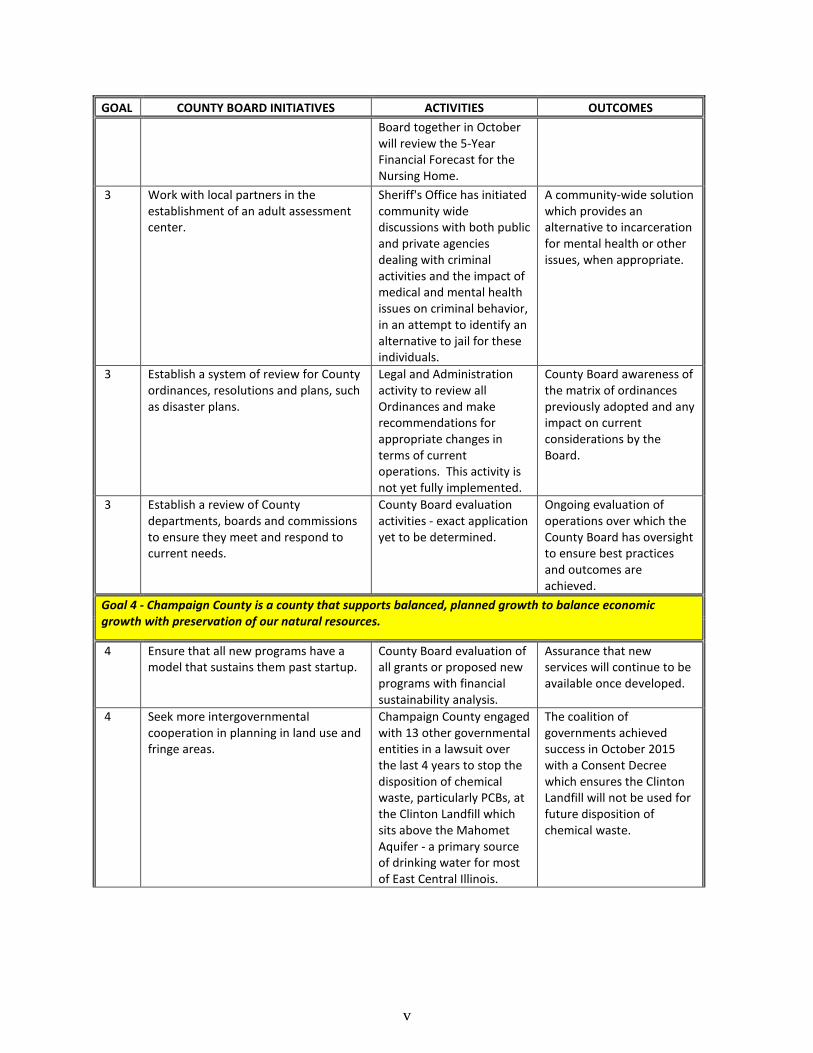

of the Champaign County Nursing Home with a long term strategy.

The County Board engaged in small group focus sessions throughout the summer on this topic. The Nursing Home Board of Directors continues to work with the Management Company on continuing development and implementation of the Nursing Home Strategic Plan and Performance Measures. The County Board and Nursing Home

Appropriate decision making steps and metrics documented and in place to ensure the long term care services, particularly for the Medicaid residents, remain available in the Champaign County community.

iv

GOAL COUNTY BOARD INITIATIVES ACTIVITIES OUTCOMES Board together in October will review the 5-Year Financial Forecast for the Nursing Home.

3 Work with local partners in the establishment of an adult assessment center.

Sheriff's Office has initiated community wide discussions with both public and private agencies dealing with criminal activities and the impact of medical and mental health issues on criminal behavior, in an attempt to identify an alternative to jail for these individuals.

A community-wide solution which provides an alternative to incarceration for mental health or other issues, when appropriate.

3 Establish a system of review for County ordinances, resolutions and plans, such as disaster plans.

Legal and Administration activity to review all Ordinances and make recommendations for appropriate changes in terms of current operations. This activity is not yet fully implemented.

County Board awareness of the matrix of ordinances previously adopted and any impact on current considerations by the Board.

3 Establish a review of County departments, boards and commissions to ensure they meet and respond to current needs.

County Board evaluation activities - exact application yet to be determined.

Ongoing evaluation of operations over which the County Board has oversight to ensure best practices and outcomes are achieved.

Goal 4 - Champaign County is a county that supports balanced, planned growth to balance economic growth with preservation of our natural resources.

4 Ensure that all new programs have a model that sustains them past startup.

County Board evaluation of all grants or proposed new programs with financial sustainability analysis.

Assurance that new services will continue to be available once developed.

4 Seek more intergovernmental cooperation in planning in land use and fringe areas.

Champaign County engaged with 13 other governmental entities in a lawsuit over the last 4 years to stop the disposition of chemical waste, particularly PCBs, at the Clinton Landfill which sits above the Mahomet Aquifer - a primary source of drinking water for most of East Central Illinois.

The coalition of governments achieved success in October 2015 with a Consent Decree which ensures the Clinton Landfill will not be used for future disposition of chemical waste.

v

GOAL COUNTY BOARD INITIATIVES ACTIVITIES OUTCOMES 4 Develop energy reduction plans for

both conservation and cost savings. Brookens facility has undergone the Illinois Green Business Association study and implementation of green management practices.

The Brookens Administrative Center received its IGBA Certification in October 2015 following an eighteen month implementation of the IGBA recommendations for green management practices.

FY2016 BUDGET HIGHLIGHTS 5-Year Financial Forecast and Budget Impact The County Administrator presented the 5-Year Financial Forecast in April, which focused on the General Corporate Fund and Public Safety Sales Tax Fund – the funds covering the majority of general government services operations for the County. The forecast illustrated the following:

• FY2015 budgeted revenues not performing as budgeted and requiring a $637,424 decrease correction in the FY2016 budget preparation.

Major Required Decreased Revenue FY2015 FY2016 Decrease 1% Sales Tax (unincorporated) $1,519,211 $1,130,161 -$389,050 1/4% General Sales Tax $5,522,911 $5,519,290 -$3,621 Fees $4,358,156 $4,188,403 -$169,753 Interest-Delinquent Taxes $650,000 $575,000 -$75,000 TOTAL $12,050,278 $11,412,854 -$637,424

o The 1 cent sales tax identified at a decline reflecting a 19% decrease over FY2014

receipts. These sales directly correlate to the agricultural economy, and are believed to be decreasing due to federal tax code changes affecting the agricultural industry resulting in producers holding off on making agricultural-related purchases. The FY2016 budget would need to incorporate stabilizing at this decreased level.

o The ¼ cent general sales tax performance identified at a flat to slightly declining rate – current year-to-date at a decrease of 0.54%. While not a significant dollar amount, this performance is significant to FY2016 budget planning in that historically this revenue has performed at a stable 2% annual increase providing an opportunity for planned revenue growth to offset expenditure growth. The FY2016 budget is prepared anticipating this revenue as flat over FY2015 projected receipts.

o The court system fees were budgeted for FY2015 based on 5-year historical averages. It became clear at the point of the 5-Year Projection, that the budget did not reflect the continuing decline these fees have presented. Therefore, the

vi

FY2016 budget would have to be adjusted downward to appropriately reflect the drop in this revenue stream.

o The Penalties on Taxes had also been budgeted on best performance in the last

three years, and based upon FY2014 and projected FY2015 performance, required a downward adjustment.

• FY2016 documented mandates for spending level increases over FY2015 budget in the total amount of $817,206. Major Required Increased Expenditure FY2015 FY2016 Increase Negotiated Bargaining Unit Salary Increases $9,908,144 $10,211,935 $303,791 Juror Expense $139,500 $317,532 $178,032 Election Judges & Workers $80,000 $150,000 $70,000 METCAD $566,296 $656,903 $90,607 ADA Compliance $0 $174,776 $174,776 TOTAL $10,693,940 $11,511,146 $817,206

o Bargaining unit salary increases are required by previously negotiated contracts. o The Juror Expense increase is the result of an unfunded mandate wherein the

State of Illinois increased the amount of juror compensation to be paid by counties throughout the State, said increase effective 6/1/2015.

o Election Judges and Workers expenses are required to be increased in a presidential election year.

o METCAD – the County’s 911 dispatch agency has required 16% increases over a 3-year period that were built into the County’s budget. These increases were to accommodate loss of revenue from land-line phones which is the primary source of revenue in Illinois for these services; an increase to consolidate and bring the Village of Rantoul into the consortium of all public safety entities in Champaign

$0

$50,000

$100,000

$150,000

$200,000

$250,000 Court Costs

Sheriff

State's Attorney

Public Defender

vii

County who work with METCAD to provide 911 services; and the need to appropriately budget for the technology capital infrastructure replacement.

o ADA Compliance – the United States Department of Justice conducted an ADA Compliance Audit on the County of Champaign in September 2011. The DOJ delivered the results of that audit to the County in January 2015, and subsequent to negotiation, the County has entered into a Settlement Agreement with the DOJ in July of 2015 to implement a 3-year term in which the County will be required to adhere to all ADA non-compliance issues identified as a result of the Audit. The County is currently working with an Independent Licensed Architect to determine the actual cost of all required corrections – which is likely to be higher than the currently budgeted amount of $174,776 built into the FY2016 budget.

The projected revenue deficit and mandated increases for spending resulted in the County Board adopting a Budget Process Resolution in May 2015 requiring all General Corporate Fund Departments to prepare their FY2016 budgets with a goal of implementing an across the board 4% reduction. In reviewing budgets with the County Administrator, not all departments implemented the full 4% reduction. If the only way to implement a full 4% reduction was for the department to eliminate positions through layoffs, the additional reduction was not required. The General Corporate Fund Departments absorbed 10% reductions in staffing levels in FY2010 and FY2011, and those pre-recession staffing levels have not been restored, therefore creating hardship in the continuing delivery of services if additional staffing cuts were required for FY2016. Ultimately, these additional cuts were not required to balance the FY2016 budget. The highlights of the more significant expenditure cuts incorporated in the FY2016 budget include:

Department(s) Expenditure Category Total Cut Numerous Stationery & Printing -$37,567 Physical Plant Custodial Supplies -$12,050 Numerous Gasoline & Oil -$54,550 Numerous Equipment Less than $5,000 -$10,000 Sheriff Arsenal & Police Supplies -$45,300 County Clerk Election Supplies -$21,000 Sheriff Automobiles, Vehicles -$230,000 Administrative Services Salary Reductions through Attrition -$24,942

Recorder Move Salaries of 2 Regular Full Time Employees to Automation Fund -$56,637

IT Hold 1 position vacant in FY2016 -$61,328

Circuit Clerk Move Salary of 1 Regular Full Time Employees to Special Revenue Fund -$45,717

Public Defender Salary Reductions through Attrition -$31,042 State's Attorney Salary Reductions through Attrition -$35,552

General County

Transfer to Capital Asset Replacement Fund to fully Fund Future Reserve for technology & equipment -$352,362

viii

Department(s) Expenditure Category Total Cut

Sheriff Budgeting Corrections Salaries at 99% of Actual - possible because of turnover during the year -$43,257

TOTAL -$1,061,304 The total General Corporate Fund Expenditure Budget for FY2016 is $35,835,644 – which represents a 0.7% or $247,550 increase over the original FY2015 budget. The total General Corporate Fund Revenue Budget for FY2016 is $35,881,559 – which represents a 0.82% or $293,465 increase over the original FY2015 budget. With the early insight into the FY2016 budget identified by the County Board, and the cooperation of the elected officials and department heads, the FY2016 budget is presented as a balanced budget. Challenges facing the County Board with the FY2016 Budget and preparation of future budgets will result substantially from the identification of long term planning requirements the County Board has initiated in 2015. The Facilities Conditions Assessment of all county facilities will undoubtedly reveal the need for a significant increase over the current annual funding for facilities repair/maintenance/capital projects of $787,700. The initiation of the project to replace the County’s software systems – accounting, real estate tax cycle, and justice systems – will also reveal a significant increase over the current annual funding of approximately $897,000 for technology infrastructure. In spite of the fact that General Corporate Fund Departments were requested to reduce their budgets for FY2016, the County Board also requested the elected officials and department heads to present any recommendations they have for optimal operations planning in the future for their individual areas of responsibility and service delivery. The County Board did this to ensure that it has information regarding the overall optimal planning for the General Corporate Fund as it makes decisions moving forward that impact availability of funding for all requests. The summary of those optimal operations planning requests is documented in the General Corporate Fund Summary document within this budget. BUDGET CHANGE OVERVIEW: The overall change in expenditure for all funds from FY2015 to FY2016 is -0.05% - an overall decrease of $65,251. The overall change in revenue for all funds from FY2015 to FY2016 is +0.02% - an overall increase of $26,727. The total budget for FY2016 is then effectively a zero growth budget as compared to the original FY2015 budget –a reflection of the current economy which also exhibits minimal growth or expansion. Staffing Level Changes One of the clearest challenges with a flat budget is maintaining personnel budgets. The County has 13 different labor contracts which are typically negotiated for three year terms and historically include wage increases ranging from 1.5% to 3% annual increases. Health insurance

ix

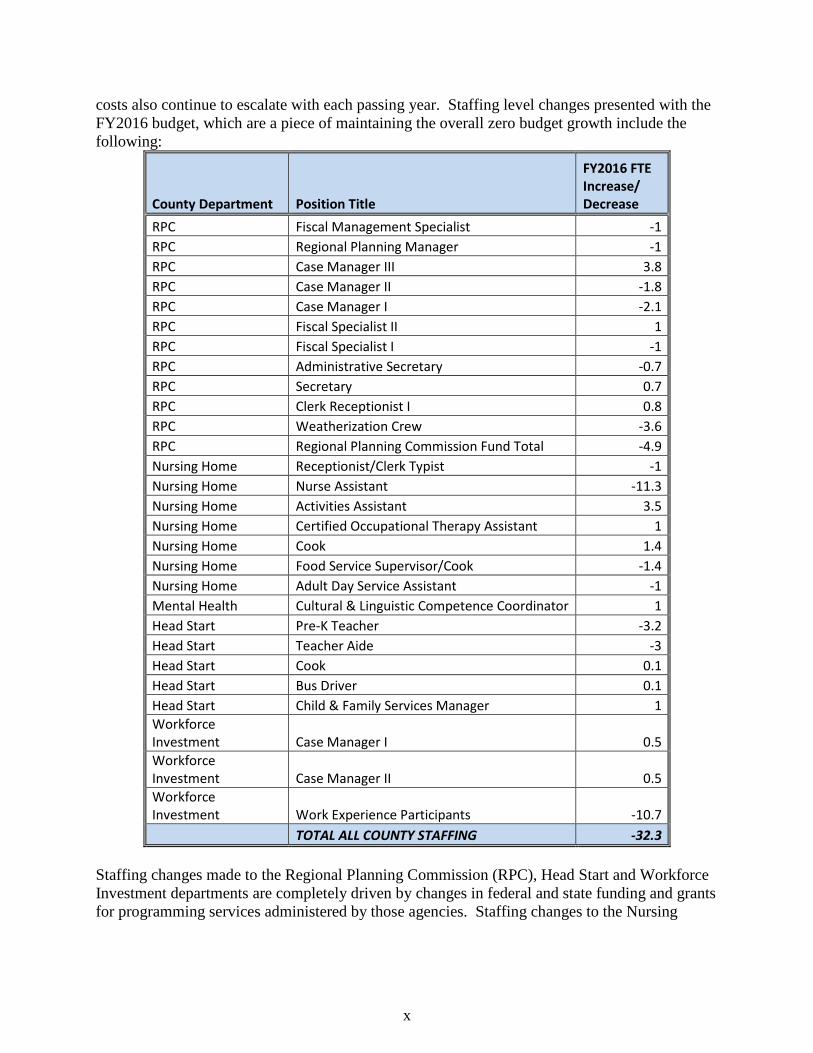

costs also continue to escalate with each passing year. Staffing level changes presented with the FY2016 budget, which are a piece of maintaining the overall zero budget growth include the following:

County Department Position Title

FY2016 FTE Increase/ Decrease

RPC Fiscal Management Specialist -1 RPC Regional Planning Manager -1 RPC Case Manager III 3.8 RPC Case Manager II -1.8 RPC Case Manager I -2.1 RPC Fiscal Specialist II 1 RPC Fiscal Specialist I -1 RPC Administrative Secretary -0.7 RPC Secretary 0.7 RPC Clerk Receptionist I 0.8 RPC Weatherization Crew -3.6 RPC Regional Planning Commission Fund Total -4.9 Nursing Home Receptionist/Clerk Typist -1 Nursing Home Nurse Assistant -11.3 Nursing Home Activities Assistant 3.5 Nursing Home Certified Occupational Therapy Assistant 1 Nursing Home Cook 1.4 Nursing Home Food Service Supervisor/Cook -1.4 Nursing Home Adult Day Service Assistant -1 Mental Health Cultural & Linguistic Competence Coordinator 1 Head Start Pre-K Teacher -3.2 Head Start Teacher Aide -3 Head Start Cook 0.1 Head Start Bus Driver 0.1 Head Start Child & Family Services Manager 1 Workforce Investment Case Manager I 0.5 Workforce Investment Case Manager II 0.5 Workforce Investment Work Experience Participants -10.7 TOTAL ALL COUNTY STAFFING -32.3

Staffing changes made to the Regional Planning Commission (RPC), Head Start and Workforce Investment departments are completely driven by changes in federal and state funding and grants for programming services administered by those agencies. Staffing changes to the Nursing

x

Home Fund are driven by the current business plan and anticipated changes in daily census and demand. AREAS of CONCERN Lack of a State Budget and Potential Implications to the County The lack of a state budget and the current state budget shortfalls present risks for many areas of the County’s operations and budgets. Proposed changes in local government distributions made by the State have been the subject of several different proposals at the state level – ranging from a 50% reduction in local income tax distribution (a potential $1.4 million annual loss to the County), to proposals for property tax freezes (potential $835,000 annual loss to the County), to changes in the Motor Fuel Tax distributions. At the time of this writing, it is known that at the end of its first quarter, the State is running out of cash which is reflected in the fact the County is no longer receiving its monthly distribution of gaming licenses revenue, Use Tax revenue, and salary reimbursements. It is difficult to plan for the ultimate impact on the County budget until the State resolves its own budget crisis and documents the impacts that will have on local governments. Nursing Home The Nursing Home operation is at risk if the State stops forwarding Medicaid payments, as is currently anticipated to occur in January. The Nursing Home’s fund balance is not adequate to absorb this monthly loss of revenue and continue operations. The County Board is scheduled to hold a Study Session on October 27th to focus on this issue and the decision points it will encounter in dealing with this loss of operating revenue in early 2016. LONG TERM CHALLENGES

• Development of Comprehensive Master Plan for County Facilities and Campuses • Identification and Appropriation of Funding for Capital Replacement and

Improvement Plans and any Impact that Requirement places on current operations • Replacement/Upgrade of Accounting Systems, Real Estate Tax Cycle and Justice

Systems Technology • Maintaining the General Corporate Fund Balance at a minimum 12.5% level with a

goal to increase the fund balance to 20% (recommended by rating agencies for improved rating)

• Developing Plan for Negotiation and Management of Personnel Costs within Available Revenues

• Establishment of a Fund Reserve for the Nursing Home Operation • Continuing development of intergovernmental cooperation to maximize the services

provided to citizens for the price of government throughout the community – roads, zoning, public health services, emergency management and preparedness

FINANCIAL SUMMARY The FY2016 Champaign County Budget – $123,108,389 in Revenue $124,914,480 in Expenditure

xi

The total budget presents a negative variance of $1,806,091. $1.52 million of the negative variance occurs in the County’s Motor Fuel Tax Fund, where funds reserved in previous years are scheduled to be spent on projects in FY2016. The remaining $0.35 million negative variance occurs throughout several of the County’s special revenue funds. Similar to the Motor Fuel Tax example, these funds also anticipate planned expenditures in FY2016 utilizing monies reserved in previous fiscal years for those expenditures. The FY2016 Budget is considered balanced in that it adheres to the County Board’s definition of Balanced Budget: A budget ordinance is balanced when the sum of estimated net revenues and appropriated fund balances is equal to appropriations. An overview of the total Champaign County Revenues, Expenditures and Combined Fund Balances for FY2014, FY2015 and FY2016 is:

ACKNOWLEDGMENTS The preparation of the FY2016 budget has been accomplished through the effort and cooperation of all county elected officials, department heads, and members of the County Board. We wish to thank all county officials for their continued cooperation over several months of budget preparation and review.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

FY2014 FY2015 FY2016

132.

87

115.

09

123.

11

138.

35

114.

30 124.

91

37.5

0

38.2

8

36.4

8

$ in

Mill

ions

Champaign County Total Budget

Revenues

Expenditures

Ending FundBalance

xii

In addition, special thanks and appreciation goes to Bill Simmering, Business Applications Developer; Andy Rhodes, IT Director; Evelyn Boatz, Budget & HR Specialist; Kathleen Oldrey, Planner II; and Kay Rhodes, Administrative Assistant for all of their efforts and assistance in the preparation of this document. Members of the Board, we are pleased to present to you the FY2016 Champaign County Budget. Respectfully submitted, Debra Busey Tami Ogden County Administrator Deputy County Administrator of Finance

xiii

1

HOW TO USE THIS DOCUMENT

The Champaign County FY2016 Budget Document is organized into nine sections.

These include: Introduction; Budget Summary; General Corporate Fund & Related

Special Revenue Funds; Special Revenue Funds; RPC Funds; Joint Venture Fund; Debt

Management & Capital Projects Funds; Proprietary Funds; and Supplemental

Information. Each section is described below, followed by a description of the

accounting and fund structure used to develop the budget document:

Section 1 - Introduction – This background section provides an overview including the

County Administrator’s Letter of Transmittal; this “How to Use” instructional document;

Champaign County economic and demographic information; and Champaign County

Board policy and process information.

Section 2 - Summary – This budget summary section provides a quick overview of

highlights of the FY2016 total Champaign County budget.

Section 3 - General Corporate Fund – A summary statement at the beginning of this

section provides complete revenue and expenditure detail for the General Corporate Fund

as a whole, including FY2014 actual revenues and expenditures, FY2015 budgeted and

projected revenues and expenditures, and FY2016 requested revenues and expenditures.

Following the summary statement are individual department budgets for each of the

General Corporate Fund departments. In addition to the financial section, each

department budget includes an organizational chart for that department; mission

statement; budget highlights; cost per capita for the operation of that department;

personnel summary information; alignment to the County Board Strategic Plan; and

objectives and performance indicators specific to that department’s operation. Any

Special Revenue Fund Budgets related specifically to the elected officials of the General

Corporate Fund are included immediately after the relevant elected official General

Corporate Fund Budget.

Section 4 - Special Revenue Funds – A summary statement and department budget

information within funds is provided for each of the County’s 18 remaining special

revenue funds. The fund and department budget document structure is substantially the

same as for the General Corporate Fund department budgets.

Section 5 - RPC Funds – A separate section for the five special revenue funds

(encompassing 100 individual department budgets) which are managed by the

Champaign County Regional Planning Commission.

Section 6 – Joint Venture Fund – Explanation of the GIS Consortium, Joint Venture

Fund, including fund/department budget information.

2

Section 7 - Debt Management and Capital Projects Funds – Explanation of each of the

County’s debt service and capital projects funds budgets, including financial detail,

source of revenues, debt structure, and project status updates.

Section 8 - Proprietary Funds – A summary statement and documentation is provided

for the Nursing Home enterprise fund, and the Self-Funded Insurance internal service

fund, together with documentation for each of the individual department budgets within

each fund.

Section 9 - Supplemental Information – This section includes additional information

including budget ordinances; property tax distribution; personnel staffing budgets and

salary schedules; and a glossary of terms used in this document.

The above description of the nine sections of the FY2016 budget document is further

enhanced for the reader with the following description of Champaign County’s

structure of funds.

Accounting Structure

A fund is the basic accounting unit: it is a self-balancing accounting entity with revenues

and expenditures which are segregated for the purpose of carrying out specific programs

in accordance with County policies and certain applicable State and Federal laws.

Each fund has at least one Department Budget, which is a group of expenditures that

provide for the accomplishment of a specific program or purpose.

Pursuant to GASB Statement 34, a major fund is a fund that meets the following criteria:

Total assets, liabilities, revenues, or expenditures/expenses of the individual

governmental or enterprise fund are at least 10 percent of the corresponding total

(assets, liabilities, and so forth) for all funds of that category (governmental

funds) or type (enterprise funds).

Total assets, liabilities, revenues, or expenditures/expenses of the individual

governmental fund or enterprise fund are at least 5 percent of the corresponding

total for all governmental and enterprise funds combined.

Fund Statements

A Fund Statement is presented for each fund, which summarizes past and projected

financial activity for the fund as follows:

Revenues – presented in line item detail within revenue categories;

Expenditures – presented in line item detail within major categories – e.g.,

personnel, commodities, services, etc.

Fund Balance – the actual or estimated funds remaining at the end of the fiscal

year.

3

Fund Types

All county funds are included in the Annual Budget Document except the fiduciary funds

which include two Private Purpose Trust Funds in which the County Engineer acts in a

trustee capacity on behalf of townships to use state funding to maintain township roads

and township bridges, which resources are not available to support the County’s own

programs; and Agency Funds whose purpose is to report resources, such as property taxes

and circuit court fees and fines, held in a custodial capacity for external individuals,

organizations and governments.

Governmental Funds – Governmental funds account for traditional governmental

operations that are financed through taxes and other fixed or restricted revenue sources.

A. General Fund: the General Corporate Fund is available for any authorized

purpose, and is used to account for all financial resources except those

required to be accounted for in another fund. A General Corporate Fund

summary is prepared which lists the amount of General Corporate Fund

appropriation for all affected departments. The General Corporate Fund is a

Major Fund.

B. Special Revenue Funds: Special Revenue Funds are used to account for the

proceeds of specific sources that are legally restricted to expenditures for a

specific purpose. Currently, the County has two major funds in Special

Revenue Funds – the Mental Health Fund and the Regional Planning

Commission Fund. Special Revenue Funds also include 42 non-major funds.

C. Debt Service Fund: Debt Service Funds are utilized to account for the

payment of interest, principal and related costs on the County’s general long-

term debt. The County has two debt services funds: one for the repayment of

bonds issued for the construction of the Nursing Home Facility; and one for

the repayment of bonds issued for the construction of the Highway Fleet

Maintenance Facility. (In addition to Debt Service Funds, the County also has

three debt service budgets included in other funds as appropriation based on

the purpose of the fund.)

D. Capital Projects Funds: Capital Project Funds are used to account for all

expenditures and revenues associated with the acquisition or construction of

major facilities that are not financed through proprietary funds or funds being

held for other governments. The County has one capital projects fund

budgeted in FY2016 – the Courts Complex Construction Fund. The County

closed out two Capital Projects Funds in FY2014 – the 202 Art Bartell

Construction Fund, and the Highway Facility Construction Fund.

Proprietary Funds – Proprietary Funds account for certain “business-type” activities of

governments that are operated so that costs incurred can be recovered by charging fees to

the specific users of these services.

4

A. Enterprise Fund: An enterprise fund is used to account for operations that

are financed primarily by User charges. The Nursing Home Fund is a Major

Fund, and is the only enterprise fund in Champaign County.

B. Internal Services Funds: An Internal Service Fund is established to account

for the financing of goods and services provided to the County and other

agencies on a cost reimbursement basis. The activities of the Self-Funded

Insurance Fund and Employee Health Insurance Fund are budgeted and

appropriated through the use of Internal Service Funds.

Joint Venture Fund – According to GASBS-14, a joint venture is defined as “a legal

entity or other organization that results from a contractual arrangement and that is owned,

operated, or governed by two or more participants as a separate and specific activity

subject to joint control in which the participants retain (a) an ongoing financial interest or

(b) an ongoing financial responsibility.” The Champaign County GIS Consortium is a

joint venture fund, created by an Intergovernmental Agreement shared by the County of

Champaign, City of Champaign, City of Urbana, Village of Mahomet, Village of

Rantoul, Village of Savoy and University of Illinois.

5

CHAMPAIGN COUNTY BOARD STRATEGIC PLAN

6

VALUES

Diversity

Teamwork

Responsibility to the Public

Justice

Quality of Life

VISION

Our vision is to be a recognized leader in local government where every official and

employee has a personal devotion to excellence in public service and embraces the

highest standards of ethics and integrity to serve the citizens of Champaign County.

MISSION

The Champaign County Board is committed to the citizens of Champaign County by

providing services in a cost-effective and responsible manner; which services are

required by state and federal mandates, and additional services as prioritized by the

County Board in response to local and community priorities.

DEFINING OUR VALUES

DIVERSITY

Appreciation of the diverse culture within our community

Strive for a workforce reflective of the community

Equal and inclusive access to services and programs

TEAMWORK

Intra-governmental cooperation

Inter-governmental cooperation

Legislative advocacy

Collaboration to achieve goals

Civility and cooperation among the County Board

RESPONSIBILITY TO THE PUBLIC

Fiscal solvency

Transparency

Efficient and friendly delivery of services

Ethical behavior

Adaptive thinking

Long-term planning

CHAMPAIGN COUNTY BOARD STRATEGIC PLAN

7

JUSTICE

Equal access to civil and criminal justice services

Place value on public safety and individuals’ rights

Encourage effective communication among public safety/criminal justice

system providers

Prevention of recidivism

Manage safe and secure detention facilities

QUALITY OF LIFE

Value broad range of quality education

Manage and encourage delivery of quality and effective health care services

Effectively manage real estate tax cycle

Support of local business community

Promote effective economic development

Management of natural resources

Provide transportation options and safe, long-lasting infrastructure

GOALS

GOAL 1 – Champaign County is committed to being a High Performing, Open, and

Transparent Local Government Organization

County Board Initiatives:

Develop strategies for declining state support

Replace the County's financial software system

Move commodity information technology systems to cloud services to allow IT

staff to focus on County systems, buying services when appropriate

Develop a the list of core, mandated services provided by the County

Develop strategies for retention and continuity in county leadership roles and

specifically the County Administrator

GOAL 2 – Champaign County Maintains High Quality Public Facilities and

Highways and Provides a Safe Rural Transportation System and Infrastructure

County Board Initiatives:

Complete an assessment of County facilities

Develop a long range facilities master plan

Address the immediate needs of County facilities and particularly ADA

requirements

Explore alternative sources of revenue for facilities maintenance and new

facilities

CHAMPAIGN COUNTY BOARD STRATEGIC PLAN

8

GOAL 3 – Champaign County Promotes a Safe, Just, and Healthy Community

County Board Initiatives:

Address the sustainability and viability of the Champaign County Nursing with a

long term strategy

Work with local partners in the establishment of an adult assessment center

Establish a system of review for County ordinances, resolutions, and plans, such

as disaster plans

Establish a review of County departments, boards, and commissions to ensure

they meet and respond to current needs

GOAL 4 – Champaign County is a County that Supports Balanced, Planned

Growth to Balance Economic Growth with Preservation of Our Natural Resources

County Board Initiatives:

Ensure that all new programs have a model that sustains them past startup

Seek more intergovernmental cooperation in planning in land use and fringe areas

Develop energy reduction plans for both conservation and cost savings

9

Dark blue: Administrative group

Light blue: Special revenue fund group

Gold: Justice system group

Green: Real estate tax cycle group

Citizens

Auditor Circuit Clerk

Jury Commission

Circuit Judges

Associate Judges

Court Administrator

Court Services

Public Defender

Coroner County Board

County Administrator

Administrative Services

Animal Control Director

County Engineer

Facilities Director

Information Technologies

Director

Planning and Zoning Director

Supervisor of Assessments

Boards, Commissions, and Joint Ventures

Board of Review

County Board of Health

Developmental Disabilities

Board

Geographic Information

System Consortium

Mental Health Board

Nursing Home Board of Directors

Regional Planning

Commission

Zoning Board of Appeals

County Clerk

Recorder Sheriff

Emergency Management

Agency

Merit Commission

State's Attorney

Children's

Advocacy

Center

Treasurer

10

Solid underline: Offices, officers, and/or employees created by the Illinois Counties Code (55 ILCS 5/).

Dashed underline: Boards created by referenda

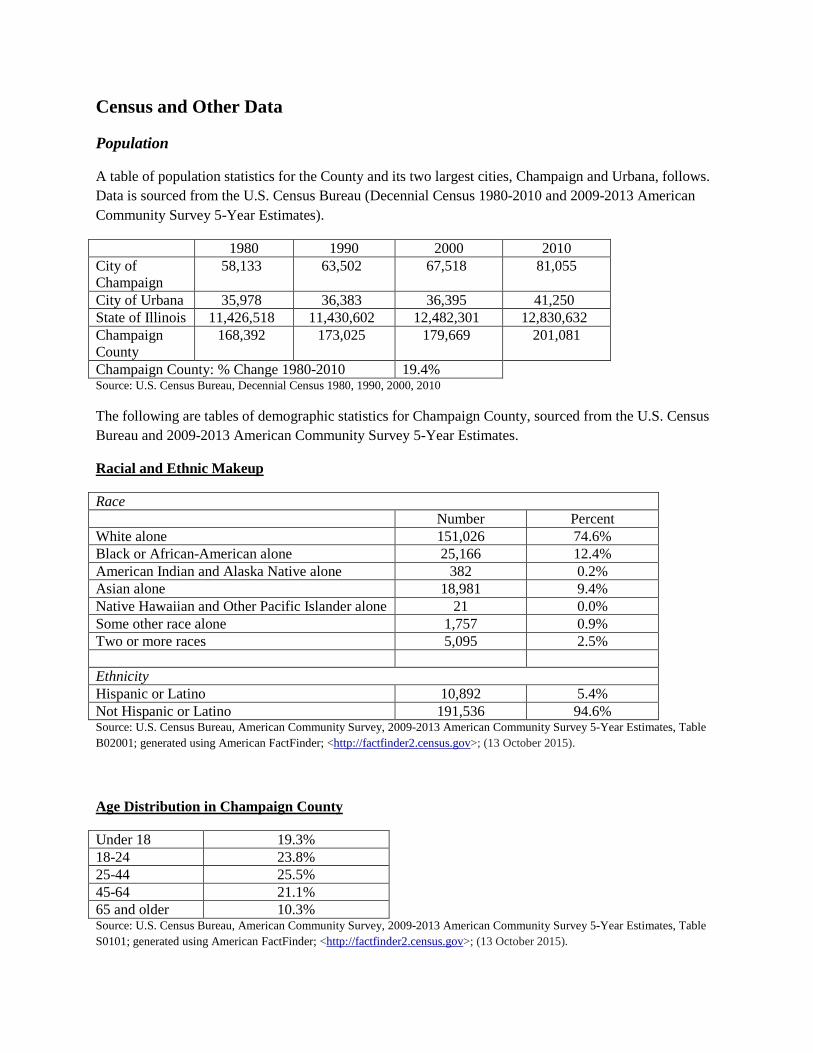

About Champaign County

Champaign County, Illinois is located in the heart of east-central Illinois, approximately 136 miles south of Chicago and 86 miles east northeast of Springfield, the state capital. The County is home to the University of Illinois, Parkland College, and two major regional hospitals. The County is comprised of 998 square miles, and 90.5% of its land area is utilized for agriculture.

Champaign County was organized in 1833, having been previously a part of Vermilion County. The county and county seat were named for Champaign County, Ohio and Urbana, Ohio respectively, the home of the Illinois legislator who sponsored the bill to create the County. The County adopted township form of government on November 8, 1859. Currently, the County Board is comprised of 11 districts, with two members representing each District for a total of 22 County Board Members. The County Board elects a County Board Chair from among its members by a majority vote at the biennial organizational meeting on the first Monday of December of every even-numbered year.

The County’s population for the 2010 Census was 201,081, representing growth of 11.9% since the 2000 Census. This places Champaign County as the 10th largest county in the State of Illinois.

Census and Other Data

Population

A table of population statistics for the County and its two largest cities, Champaign and Urbana, follows. Data is sourced from the U.S. Census Bureau (Decennial Census 1980-2010 and 2009-2013 American Community Survey 5-Year Estimates).

1980 1990 2000 2010 City of Champaign

58,133 63,502 67,518 81,055

City of Urbana 35,978 36,383 36,395 41,250 State of Illinois 11,426,518 11,430,602 12,482,301 12,830,632 Champaign County

168,392 173,025 179,669 201,081

Champaign County: % Change 1980-2010 19.4% Source: U.S. Census Bureau, Decennial Census 1980, 1990, 2000, 2010

The following are tables of demographic statistics for Champaign County, sourced from the U.S. Census Bureau and 2009-2013 American Community Survey 5-Year Estimates.

Racial and Ethnic Makeup

Race Number Percent White alone 151,026 74.6% Black or African-American alone 25,166 12.4% American Indian and Alaska Native alone 382 0.2% Asian alone 18,981 9.4% Native Hawaiian and Other Pacific Islander alone 21 0.0% Some other race alone 1,757 0.9% Two or more races 5,095 2.5% Ethnicity Hispanic or Latino 10,892 5.4% Not Hispanic or Latino 191,536 94.6% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B02001; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Age Distribution in Champaign County

Under 18 19.3% 18-24 23.8% 25-44 25.5% 45-64 21.1% 65 and older 10.3% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table S0101; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Gender Distribution

Male 49.% Female 50.1% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table S0101; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Income

The following tables present the median household and family income and the distribution of household and family incomes in the County and the State according to the 2009-2013 American Community Survey 5-Year Estimates.

Median Household and Family Income

Champaign County State of Illinois Median Household Income $45,808 $56,797 Median Family Income $69,554 $70,344 Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Tables B19013 and B19113; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Household Income Distribution

Champaign County State of Illinois Number of

Households Percent Number of

Households Percent

Less than $10,000 9,954 12.6% 337,875 7.1% $10,000-$14,999 3,916 4.9% 219,468 4.6% $15,000-$24,999 9,685 12.2% 484,449 10.2% $25,000-$34,999 8,607 10.9% 462,771 9.7% $35,000-$49,999 9,904 12.5% 618,005 12.9% $50,000-$74,999 12,989 16.4% 856,630 17.9% $75,000-$99,999 8,987 11.4% 615,943 12.9% $100,000-$149,999 9,094 11.5% 667,146 14.0% $150,000-$199,999 3,070 3.9% 255,728 5.4% $200,000 or more 2,931 3.7% 254,708 5.3% Total 79,137 100.0% 4,772,723 100.0% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B19001; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Family Income Distribution

Champaign County State of Illinois Number of

Families Percent Number of

Families Percent

Less than $10,000 2,020 4.7% 137,093 4.4% $10,000-$14,999 911 2.1% 84,866 2.7% $15,000-$24,999 3,260 7.6% 225,548 7.2% $25,000-$34,999 3,625 8.5% 257,251 8.2% $35,000-$49,999 5,151 12.1% 381,248 12.2% $50,000-$74,999 8,391 19.7% 583,037 18.6% $75,000-$99,999 6,694 15.7% 470,717 15.0% $100,000-$149,999 7,421 17.4% 553,739 17.7% $150,000-$199,999 2,582 6.1% 222,115 7.1% $200,000 or more 2,615 6.1% 220,748 7.0% Total 42,670 100.0% 3,136,362 100.0% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B19101; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Housing

The following tables show the distribution of value of owner-occupied housing units with a mortgage and distribution of rent for renter-occupied housing units for the County and the State according to the 2009-2013 American Community Survey 5-Year Estimates, and the change in median home value over time in the County, the State, the City of Champaign, and the City of Urbana according to the Decennial Census of 1980, 1990, 2000, and 2010.

Housing Tenure

State of Illinois Champaign County City of Champaign City of Urbana Owner-Occupied 67.5% 54.9% 47.5% 36.0% Renter-Occupied 32.5% 45.1% 52.5% 64.0% Total Occupied Housing Units

100.0% 100.0% 100.0% 100.0%

Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B25003; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Value Distribution of Owner-Occupied Units

Champaign County State of Illinois Number of

Owner-Occupied Units

Percent Number of Owner-Occupied Units

Percent

Less than $50,000 3,538 8.1% 235,268 7.3% $50,000-$99,999 7,261 16.7% 493,044 15.3% $100,000-$149,999 11,030 25.4% 504,066 15.7% $150,000-$199,999 9,500 21.9% 538,003 16.7% $200,000-$299,999 8,080 18.6% 692,499 21.5% $300,000-$499,999 3,285 7.6% 513,968 16.0% $500,000-$999,999 655 1.5% 196,905 6.1% $1,000,000 or more 109 0.3% 46,285 1.4% Total Units 43,458 100.0% 3,220,038 100.0% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B25075; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

Rent Distribution of Renter-Occupied Units

Champaign County State of Illinois Number of Renter-

Occupied Units Percent Number of Renter-

Occupied Units Percent

No cash rent 874 2.4% 68,888 4.4% Less than $300 1,034 2.9% 76,827 4.9% $300-$499 2,624 7.4% 111,099 7.2% $500-$749 11,399 31.9% 310,637 20.0% $750-$999 9,828 27.5% 422,228 27.2% $1,000-$1,499 7,310 20.5% 376,381 24.2% $1,500-$1,999 1,766 4.9% 123,498 8.0% $2,000 or more 844 2.4% 63,127 4.1% Total Units 35,679 100.0% 1,552,685 100.0% Source: U.S. Census Bureau, American Community Survey, 2009-2013 American Community Survey 5-Year Estimates, Table B25063; generated using American FactFinder; <http://factfinder2.census.gov>; (13 October 2015).

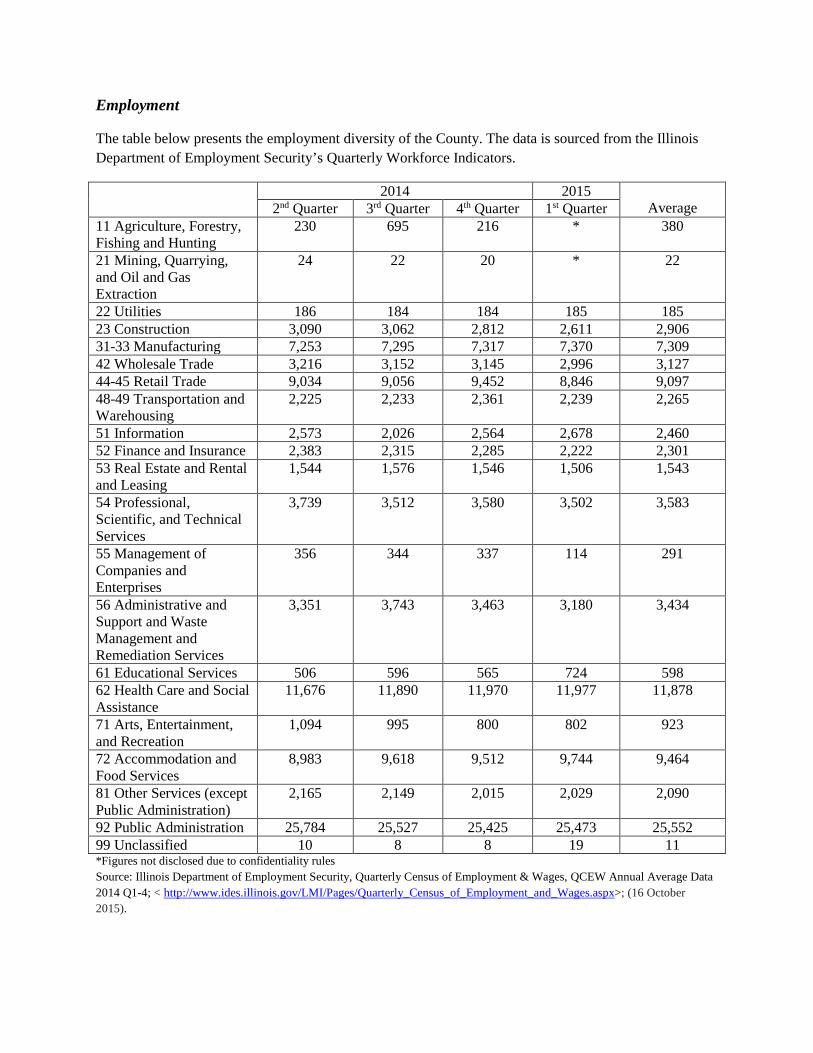

Employment

The table below presents the employment diversity of the County. The data is sourced from the Illinois Department of Employment Security’s Quarterly Workforce Indicators.

2014 2015 Average 2nd Quarter 3rd Quarter 4th Quarter 1st Quarter

11 Agriculture, Forestry, Fishing and Hunting

230 695 216 * 380

21 Mining, Quarrying, and Oil and Gas Extraction

24 22 20 * 22

22 Utilities 186 184 184 185 185 23 Construction 3,090 3,062 2,812 2,611 2,906 31-33 Manufacturing 7,253 7,295 7,317 7,370 7,309 42 Wholesale Trade 3,216 3,152 3,145 2,996 3,127 44-45 Retail Trade 9,034 9,056 9,452 8,846 9,097 48-49 Transportation and Warehousing

2,225 2,233 2,361 2,239 2,265

51 Information 2,573 2,026 2,564 2,678 2,460 52 Finance and Insurance 2,383 2,315 2,285 2,222 2,301 53 Real Estate and Rental and Leasing

1,544 1,576 1,546 1,506 1,543

54 Professional, Scientific, and Technical Services

3,739 3,512 3,580 3,502 3,583

55 Management of Companies and Enterprises

356 344 337 114 291

56 Administrative and Support and Waste Management and Remediation Services

3,351 3,743 3,463 3,180 3,434

61 Educational Services 506 596 565 724 598 62 Health Care and Social Assistance

11,676 11,890 11,970 11,977 11,878

71 Arts, Entertainment, and Recreation

1,094 995 800 802 923

72 Accommodation and Food Services

8,983 9,618 9,512 9,744 9,464

81 Other Services (except Public Administration)

2,165 2,149 2,015 2,029 2,090

92 Public Administration 25,784 25,527 25,425 25,473 25,552 99 Unclassified 10 8 8 19 11 *Figures not disclosed due to confidentiality rules Source: Illinois Department of Employment Security, Quarterly Census of Employment & Wages, QCEW Annual Average Data 2014 Q1-4; < http://www.ides.illinois.gov/LMI/Pages/Quarterly_Census_of_Employment_and_Wages.aspx>; (16 October 2015).

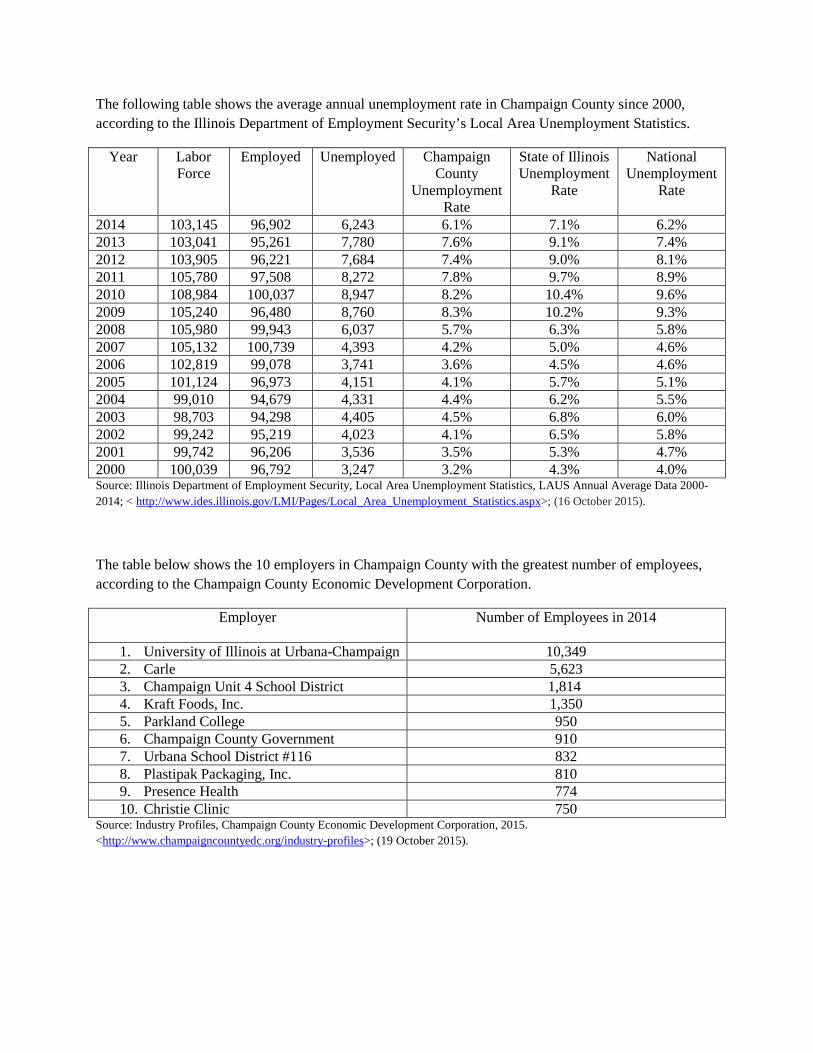

The following table shows the average annual unemployment rate in Champaign County since 2000, according to the Illinois Department of Employment Security’s Local Area Unemployment Statistics.

Year Labor Force

Employed Unemployed Champaign County

Unemployment Rate

State of Illinois Unemployment

Rate

National Unemployment

Rate

2014 103,145 96,902 6,243 6.1% 7.1% 6.2% 2013 103,041 95,261 7,780 7.6% 9.1% 7.4% 2012 103,905 96,221 7,684 7.4% 9.0% 8.1% 2011 105,780 97,508 8,272 7.8% 9.7% 8.9% 2010 108,984 100,037 8,947 8.2% 10.4% 9.6% 2009 105,240 96,480 8,760 8.3% 10.2% 9.3% 2008 105,980 99,943 6,037 5.7% 6.3% 5.8% 2007 105,132 100,739 4,393 4.2% 5.0% 4.6% 2006 102,819 99,078 3,741 3.6% 4.5% 4.6% 2005 101,124 96,973 4,151 4.1% 5.7% 5.1% 2004 99,010 94,679 4,331 4.4% 6.2% 5.5% 2003 98,703 94,298 4,405 4.5% 6.8% 6.0% 2002 99,242 95,219 4,023 4.1% 6.5% 5.8% 2001 99,742 96,206 3,536 3.5% 5.3% 4.7% 2000 100,039 96,792 3,247 3.2% 4.3% 4.0% Source: Illinois Department of Employment Security, Local Area Unemployment Statistics, LAUS Annual Average Data 2000-2014; < http://www.ides.illinois.gov/LMI/Pages/Local_Area_Unemployment_Statistics.aspx>; (16 October 2015).

The table below shows the 10 employers in Champaign County with the greatest number of employees, according to the Champaign County Economic Development Corporation.

Employer Number of Employees in 2014

1. University of Illinois at Urbana-Champaign 10,349 2. Carle 5,623 3. Champaign Unit 4 School District 1,814 4. Kraft Foods, Inc. 1,350 5. Parkland College 950 6. Champaign County Government 910 7. Urbana School District #116 832 8. Plastipak Packaging, Inc. 810 9. Presence Health 774 10. Christie Clinic 750

Source: Industry Profiles, Champaign County Economic Development Corporation, 2015. <http://www.champaigncountyedc.org/industry-profiles>; (19 October 2015).

18

BASIS OF ACCOUNTING/BASIS OF BUDGETING

Champaign County’s governmental accounting and financial reporting are managed in

accordance with “Generally Accepted Accounting Principles” (“GAAP”). Government

funds use a modified accrual basis of accounting. The modified accrual basis of

accounting and budgeting recognizes revenues when they become available and

measureable; and expenditures when the liability is incurred. Proprietary funds use an

accrual basis of accounting. The accrual basis of accounting recognizes revenue when

earned and expenses when incurred, regardless of when cash is received or disbursed.

The budgets for all governmental funds and proprietary funds are presented on a

modified accrual basis. The modified accrual basis of budgeting is reflected in the

County ordinance which provides that balances remaining in County appropriations shall

be available for sixty days after the close of the fiscal year to pay for goods or services

that were delivered prior to the close of the fiscal year. Because proprietary fund budgets

are not on a full accrual basis, the legally adopted budget is not on a basis strictly

consistent with generally accepted accounting principles (GAAP). The basis of

budgeting is different from the basis of accounting used in the audited financial

statements, where the actual results of operations are presented in accordance with

generally accepted accounting principles. Adjustments necessary to convert the results of

operations from the budgetary basis to the GAAP basis are mostly due to proprietary

funds having budgets on the modified accrual basis, while GAAP requires accounting for

those funds on the full accrual basis.

CHAMPAIGN COUNTY FINANCIAL POLICIES

OPERATING BUDGET POLICIES Amending the Budget After the adoption of the annual budget, the budget may be amended through a budget amendment or budget transfer. Budget Amendments -

Amendments to the budget require a 2/3rd majority vote (15) of the County Board.

Budget Transfers - The budget may be amended by transfers in two ways:

Department heads may authorize transfers between non-personnel budget line items in their department budget as long as they do not exceed the total combined appropriation for these categories; and department heads may transfer from one personnel line item to another personnel line item in their department budget as long as they do not exceed the total combined appropriation for the personnel line items.

All other transfers require a 2/3rd majority vote (15) of the County Board. Appropriation All County funds are appropriated in the “Official Budget”. Appropriations will be considered the maximum authorization to incur obligations and not a mandate to spend. Balanced Budget The County will make all current expenditures with current revenues, avoiding procedures that balance current budgets by postponing needed expenditures, realizing future revenues early, or rolling over short-term debt. A budget ordinance is balanced when the sum of estimated net revenues and appropriated fund balances is equal to appropriations.

Capital Asset Replacement Fund A Capital Asset Replacement Plan includes a multi-year plan for vehicles, computers and technology, and furnishings and office equipment will be updated and prepared for the General Corporate Fund departments in the annual budget process. These expenditures will be appropriately amortized and reserves for replacement will be appropriated to the Capital Asset Replacement Fund.

Champaign County Financial Policies Page 20

20

The Capital Asset Replacement Plan also includes a multi-year plan for the facilities owned and maintained by the County. The County will maintain all its assets at a level adequate to protect the County’s capital interest and to minimize future maintenance and replacement costs. The County will identify the estimated costs and potential funding sources for each capital project proposal before it is submitted and included in the Capital Asset Replacement Fund plan. The County Administrator is authorized to approve all expenditures from the Capital Asset Replacement Fund in compliance with the multi-year plan and policies established by the County Board. No more than 3% of the total of the General Corporate Fund Appropriation may be appropriated to the Capital Asset Replacement Fund. Contingency Fund A General Corporate Fund contingency appropriation will be designated for emergency purchases during the year. The contingency appropriation goal is 1% of the total anticipated expenditure for the General Corporate Fund. No more than 5% of the total General Corporate Fund Appropriation may be appropriated to the Contingency Fund. Money appropriated in the contingency fund may be used for contingent, incidental, miscellaneous, or general county purposes, but no part of the amounts so appropriated shall be used for purposes for which other appropriations are made in such budget unless a transfer of funds is made with the approval of 2/3 of the members (15) of the County Board. Form of the Budget The final Budget document must include the following, showing specific amounts:

Statement of financial information including prior year revenue and expenditure totals, and current year and ensuing year revenue and expenditure projections;

Statement of all moneys in the county treasury unexpended at the termination of the last fiscal year;

Statement of all outstanding obligations or liabilities of the county incurred in any preceding fiscal year;

Any additional information required by state law. Fund Structure Champaign County’s budgetary policies are in accordance with generally accepted accounting principles (GAAP). The County’s financial structure begins with funds. A fund is a self-balancing accounting entity with revenues and expenditures which are segregated for the purpose of carrying out specific programs in accordance with County policies and certain applicable State and Federal laws.

Champaign County Financial Policies Page 21

21

Each fund has at least one Department Budget, which is a group of expenditures that provide for the accomplishment of a specific program or purpose. A major fund is a budgeted fund whose revenues or expenditures represent more than 10% of the total appropriated revenues or expenditures. Fund Statements A Fund Statement is presented for each fund, which summarizes past and projected financial activity for the fund as follows:

Revenues – presented in line item detail within revenue categories;

Expenditures – presented in line item detail within major categories – e.g., personnel, commodities, services, etc.

Fund Balance – the actual or estimated funds remaining at the end of the fiscal year.

Fund Types All county funds are included in the Annual Budget Document except the fiduciary funds which include two Private Purpose Trust Funds in which the County Engineer acts in a trustee capacity on behalf of townships to use state funding to maintain township roads and township bridges, which resources are not available to support the County’s own programs; and Agency Funds whose purpose is to report resources, such as property taxes and circuit court fees and fines, held in a custodial capacity for external individuals, organizations and governments. Governmental Funds – Governmental funds account for traditional governmental operations that are financed through taxes and other fixed or restricted revenue sources.

A. General Fund: the General Corporate Fund is available for any authorized purpose, and is used to account for all financial resources except those required to be accounted for in another fund. A General Corporate Fund summary is prepared which lists the amount of General Corporate Fund appropriation for all affected departments. The General Corporate Fund is a Major Fund.

B. Special Revenue Funds: Special Revenue Funds are used to account for the proceeds of specific sources that are legally restricted to expenditures for a specific purpose. Currently, the County has four major funds in Special Revenue Funds: the Mental Health Fund; the Developmental Disability Fund; the Illinois Municipal Retirement Fund; and the Regional Planning Commission Fund. Special Revenue Funds also include 44 non-major funds. a. Debt Service Fund: Included in the Special Revenue Funds are Debt

Service Funds utilized to account for the payment of interest, principal and related costs on the County’s general long-term debt. The County has three debt services funds: one for the repayment of the bonds issued for the construction of the Satellite Jail and remodeling of the Downtown

Champaign County Financial Policies Page 22

22

Correctional Center; and one for the repayment of bonds issued for the construction of the Nursing Home Facility; and one for the repayment of bonds issued for the construction of the Highway Fleet Maintenance Facility. (In addition to Debt Service Funds, the County also has three debt service budgets included in other funds as appropriation based on the purpose of the fund.)

b. Capital Projects Funds: Also included in Special Revenue Funds are Capital Project Funds used to account for all expenditures and revenues associated with the acquisition, construction or maintenance of major facilities that are not financed through proprietary funds or funds being held for other governments. The County has one capital project fund budgeted in FY2015 – the Courts Complex Construction Fund.

Proprietary Funds – Proprietary Funds account for certain “business-type” activities of governments that are operated so that costs incurred can be recovered by charging fees to the specific users of these services.

A. Enterprise Fund: An enterprise fund is used to account for operations that are financed primarily by User charges. The Nursing Home Fund is a Major Fund, and is the only enterprise fund in Champaign County.

B. Internal Services Funds: An Internal Service Fund is established to account for the financing of goods and services provided to the County and other agencies on a cost reimbursement basis. The activities of the Self-Funded Insurance Fund and Employee Health Insurance Fund are budgeted and appropriated through the use of Internal Service Funds.

REVENUE POLICIES Sources of Revenue The County will try to maintain a diversified and stable revenue system to shelter it from unforeseeable short-run fluctuations in any one-revenue source. The County will estimate its annual revenues by an objective, analytical process, wherever practical. The County will project revenues for the next year and will update the projection annually. Each existing and potential revenue source will be re-examined annually. One-Time Revenues To the extent feasible, one-time revenues will be applied toward one-time expenditures; they will not be used to finance ongoing programs. Ongoing revenues should be equal to or exceed ongoing expenditures. Grants The Champaign County Board supports efforts to pursue grant revenues to provide or enhance County mandated and non-mandated services and capital needs. Activities

Champaign County Financial Policies Page 23

23

which are, or will be, recurring shall be initiated with grant funds only if one of the following conditions are met: (a) the activity or service can be terminated in the event the grant revenues are discontinued; or (b) the activity should, or could be, assumed by the County (or specific fund) general and recurring operating funds. Departments are encouraged to seek additional sources of revenue to support the services prior to expiration of grant funding. Grant approval shall be subject to the terms and conditions of Champaign County Ordinance Number 635. Financial Reserves and Surplus On an annual basis, the fund balance for each fund shall be reviewed, and projections of reserve requirements and a plan for the use of an excess surplus shall be documented. The minimum fund balance requirement for the General Corporate Fund is a 45-day or 12.5% of expenditure fund balance for cash flow purposes. Instances where an ending audited fund balance is below the 45-day minimum requirement, a plan will be developed to increase the fund balance. It is the intent of the County to use all surpluses generated to accomplish three goals: meeting reserve policies, avoidance of future debt and reduction of outstanding debt. Property Tax The property tax rates for each levy shall be calculated in accordance with the Property Tax Extension Limitation Law. User Fees The County charges user fees for items and services, which benefit a specific user more than the general public. State law or an indirect cost study determines the parameters for user fees. The County shall review all fees assessed in its annual budget preparation process to determine the appropriate level of fees for services and recommend any proposed changes to the fees collected to be implemented in the ensuing budget year. ACCOUNTING POLICIES Accounting/Auditing State statutes require an annual audit by independent certified public accountants. A comprehensive annual financial report shall be prepared to the standards set by the government finance Officers Association (GFOA). The County follows Generally Accepted Accounting Principles (GAAP). The County uses an accounts receivable system to accrue revenues when they are measurable for governmental fund types. Departments should bill appropriate parties for amounts owed to Champaign County, review aging reports, complete follow-up information about the account, and monitor all accounts receivables.

Champaign County Financial Policies Page 24

24

DEBT MANAGEMENT POLICIES When applicable, the County shall review its outstanding debt for the purpose of determining if the financial marketplace will afford the County the opportunity to refund an issue and lessen its debt service costs. In order to consider the possible refunding of an issue a Present Value savings of three percent over the life of the respective issue, at a minimum, must be attainable. The County will confine long-term borrowing to capital improvements or projects that cannot be financed from current revenues. When the county finances capital projects by issuing bonds, it will pay back the bonds within a period not to exceed the estimated useful life of the project. The County will strive to have the final maturity of general obligation bonds at, or below, thirty years. Whenever possible, the County will use special assessment, revenue, or other self-supporting bonds instead of general obligation bonds, so those benefiting from the improvements will bear all or part of the cost of the project financed. The County will not use long-term debt for current operations. The County will maintain good communications with bond rating agencies regarding its financial condition. The County will follow a policy of full disclosure on every financial report and borrowing prospectus. FIXED ASSETS The County maintains a fixed asset inventory of furniture, equipment, buildings, and improvements with a value of greater than $5,000 and a useful life of one year or more. ENCUMBRANCE An encumbrance system is maintained to account for commitments resulting from purchase orders and contracts. Every effort will be made to ensure that these commitments will not extend from one fiscal year to the next. Any emergency encumbrances, which do extend into the next fiscal year, shall be subject to appropriation in the next year’s budget. Encumbrances at year - end do not constitute expenditures or liabilities in the financial statements for budgeting purposes. FISCAL YEAR The County’s fiscal year is January 1st through December 31st.

Champaign County Financial Policies Page 25

25

INVESTMENT The County Treasurer is responsible for the investing of all Champaign County funds. With County Board approval, the Treasurer may make a short term loan of idle monies from one fund to another, subject to the following criteria:

a. Such loan does not conflict with any restrictions on use of the source fund;

b. Such loan is to be repaid to the source fund, with interest, within the current fiscal year.

PURCHASING All items with an expected value of $30,000 or more must be competitively bid with exceptions for professional services (other than engineering, architectural or land surveying services). Additional competitive bid requirements may apply by statute or as a condition of using funds from an outside source. All purchases over the respective limit of $30,000, which require the use of either formal bids or requests for proposals, must be approved by the full Champaign County Board. The Champaign County Purchasing Ordinance establishes the procedures to be followed in all purchasing activities. RISK MANAGEMENT The County established a self-funded insurance program for workers compensation and liability. To forecast expenditures, the county hires an actuarial consulting firm to review loss history and recommend funding taking into consideration claims, fixed costs, fund reserves, and national trends. The County strives to maintain the actuary recommended fund balance. SALARY ADMINISTRATION The County Administrator is responsible for computing salaries and fringe benefits costs for all departments. Increases for non-bargaining employees, as defined in the Personnel Policy, will be established by the Finance Committee at the beginning of the budget cycle and forwarded to the County Board for inclusion in the annual budget.

26

FY2016 BUDGET PROCESS

BUDGET DEVELOPMENT PROCESS

Phase 1 - Planning

The budget development process begins approximately nine months prior to the beginning of the

fiscal year. At that time, the County Administrator updates the Five-Year Forecast for the

General Corporate Fund, and conducts market surveys to review the mid-point valuation of jobs

in Champaign County. Based upon these analyses, the County Administrator recommends salary

range adjustments and a set of assumptions for planning purposes and direction on balancing the

next year’s General Corporate Fund budget, to be adopted by the Finance Committee in May.

Based upon the Finance Committee Recommendation, the County Board adopts the annual

Budget Process Resolution in May of each year.

Champaign County requires department budget requests to be performance-based and focused on

goals, objectives and performance indicators. Additionally, statutory budget requirements as

defined in 55 ILCS 5/6 require the following information be included in the annual budget

document:

Statement of financial information including prior year revenue and expenditure

totals, and current year and future year revenue and expenditure projections;

Statement of all monies in the county treasury unexpended at the termination of the

last fiscal year;

Statement of all outstanding obligations or liabilities of the county incurred in any

preceding fiscal year;

Statement showing any bonuses or increase in any salary, wage, stipend, or other