Challenges and opportunities for CCS

22

Challenges and opportunities for CCS Dr Andrew Minchener OBE General Manager IEA Clean Coal Centre ESI/IEA Coal Roundtable Thursday 31 October 2013

Transcript of Challenges and opportunities for CCS

Challenges and opportunities for CCS

Dr Andrew Minchener OBE General Manager

IEA Clean Coal Centre

ESI/IEA Coal Roundtable Thursday 31 October 2013

Scope of presentation

• Role of the IEA Clean Coal Centre • Overview of the CCS technology options • CCT HELE initiatives as precursors to CCS implementation • Broad comment on regional CCS programmes • Focus on China pilot programmes • Comment on SE Asia programmes via World Bank and ADB • Hurdles to be overcome • Final thoughts

Role of the IEA Clean Coal Centre

Italy Japan Republic of Korea

UK

Glencore Xstrata

BHEL

Anglo American Thermal Coal

USA

S Africa

Austria

Canada

Germany CEC

Beijing Research Institute of Coal Chemistry

Australia

Coal Association

NZ

Eletrobras

Suek Electric Power Planning & Engineering Institute of China

Banpu

Poland

The foremost centre of excellence for all aspects of clean coal knowledge

transfer

Some of the products and services offered by the Centre

WEBINARS

CO2 capture and storage

Boiler Air and coal Amine scrubbing

CO2 to storage

N2, excess O2, H2O, etc

De-NOx, FGD, ESP

Post combustion Flue gas scrubbing

Boiler Oxygen and coal

Moisture removal

CO2 to storage

Recycle combustion gases

Oxyfuel combustion

Contaminants removal

Gasification Shift reaction CO + H2

H2O

CO2 + H2 Separation

H2

CO2 to storage

Oxygen, steam and coal

Pre-combustion

First generation CO2 capture processes

Flue gas

Turbine

Mill Boiler

De-NOx EP De-S

Generator Condenser

Steam Water

Coal

CO2 Storage Pollutants to be reduced

•SO2, NOx, •Particulate matter

CO2

CO2 Capture

(2) Reducing non-GHG emissions

(3) Carbon Capture and Storage

(1) Reducing coal consumption

Technologies for cleaner coal generation

EP: Electrostatic Precipitator

HELE Technologies

Focus on technologies to reduce both GHG and non-GHG (NOx, SO2, PM) emissions.

N2, H2O

Decrease generation from subcritical Install CCS* on plants over supercritical

Increase generation from high-efficiency technology (SC or better)

Glo

bal c

oal-f

ired

elec

trici

ty

gene

ratio

n (T

Wh)

Supercritical

HELE Plants with CCS*

USC

Subcritical

*CCS (Post-combustion, Oxyfuel, Pre-combustion CO2 capture)

IGCC

Improve efficiency, then deploy CCS (IEA 2012)

* CCS fitted to SC (or better) units.

Three processes essential to achieve a low-carbon scenario

Data for hard coal-fired power plants from VGB 2007; data for lignite plants from C Henderson, IEA Clean Coal Centre; efficiencies are LHV,net

CO2 emissions reduction by key coal utilisation technologies

Energy Efficiency makes big change but deep cuts of CO2 emission can be done only by Carbon Capture and Storage (CCS)

>2030

but deep cuts only by CCS

Average worldwide hard coal

30.0% 1116 gCO2/kWh

38% 881 gCO2/kWh

EU av hard coal

45% 743 gCO2/kWh

State-of-the art PC/IGCC hard coal

50% 669 gCO2/kWh

Advanced R&D Hard coal

Latrobe Valley lignite (Australia)

28-29.0% 1400 gCO2/kWh EU state-of-

the-art lignite

43-44%

930 gCO2/kWh

55%

740 gCO2/kWh

Advanced lignite

Drax, UK’s most recent 6*660MWe

Torrevaldaliga Nord 3*660MWe

Shar

e of

CCS

(1=1

00%

)

Efficiency improvement

CO2 abatement by CCS

Aver

age

CO

2 in

tens

ity fa

ctor

in 2

DS

(g

CO

2/kW

h)

33% 34% 37% 42% 43%

Raising efficiency significantly reduces the CO2/kWh emitted (source: IEA HELE Roadmap, Dec 2012)

Efficiency in 2DS

Impact of efficiency improvement on CO2 abatement

CCS status worldwide

Extensive activities under way in Europe, USA, Australia, Japan and China

Some work beginning in Indonesia and elsewhere in SE Asia

Very large amount of R&D on all aspects of CO2 capture and CO2 storage characterisation

Several industrial scale pilot projects under way

Increasing focus on legal and regulatory issues

Many large scale integrated projects proposed (GCCSI) but, apart from some EOR based initiatives, little progress being made to establish commercial prototype demonstrations

Pulverised coal (PC) fired steam cycle power plant

Condencer

Ash handling

Steam turbine PC

Coal

FW Punp

RC Fan Mill FDF

Main steam HT Reheater

LT Reheater

Ash recovery

FGD

GGH ESP AH

SCR

IDF

Generator

Chinese energy efficiency programme for the coal power sector

• Over 200 GWe of advanced, high efficiency large capacity installed between 2006 and 2010 and over 72 GWe of old, small coal plants decommissioned

• Nationwide average coal consumption for power generation reduced from 370 grammes of coal equivalent (gce)/kWh in 2005 to 335 gce/kWh in 2010. Best new plants are achieving <280 gce/kWh

• Policy is being continued during 2011-2015, including closure of units up to 300 MWe in size

New emission limits for coal power plants in the priority regions of China

[GB13223-2011]

Towards 50% cycle efficiency with advanced USC technology

Metals used in boiler and turbine hot spots: • Steels well proven in USC at 600ºC • Nickel based alloys proving capable in

A-USC at 700ºC

In 2010, Huaneng installed a larger unit on the 2x660 MWe Shidongkou No. 2 Power Plant in Shanghai, which can capture 120,000 tonnes of CO2 each year.

As in Beijing, CO2 is sold

to the food and beverage industries

Huaneng post-combustion CO2 capture unit in Shanghai

Great potential of CO2-EOR and storage in China

•China has a proved OOIP in low-permeability reservoirs as 6.32 billion tonnes, which is 28.1% of the total proven OOIP.

•Gas or CO2 injection could improve the oil recovery of these oil fields.

•CO2 is a potentially valuable resource for oil recovery and 60% of CO2 injected could be stored in the reservoirs.

Main oil/gas fields in China

CCUS potential in the coal to chemicals sector of China

There is a growth in scale and extent of application in the coal to chemicals sector, with the opportunity to capture, at relatively low cost, concentrated streams of CO2. These developments suggest a valuable potential for some early CCS demonstrations and commercial prototypes, probably for EOR applications.

Presenter

Presentation Notes

While coal fired power generation dominates coal use in China, there is significant a growth both in scale and extent of application in the coal to chemicals sector, with the opportunity to capture, at relatively low cost, concentrated streams of CO2. These developments suggest a valuable potential for some early CCS demonstrations and commercial prototypes, probably for EOR applications. To put that in context, as part of China’s industrial and economic reforms, there has been a growing introduction of large, pressurised oxygen blown gasification units for chemicals production. Initially, these were built at various refineries to process petroleum residues to produce higher value products. However, this niche market has been rapidly superseded with the introduction of coal gasification for oil, gas and chemicals production. The driver for this change has been to establish a gasification based coal transformation industry as a possible means to limit the use of oil and natural gas for production of transport fuels and a wide range of secondary chemical products, including ammonia for fertilizer production and, more recently, methanol for the production of a wide range of secondary products, including olefins and DME.

CCS activities in SE Asia

• ADB: Enabling Carbon Capture and Storage in Southeast Asia's Coal Power Sector (Indonesia, Malaysia, Thailand, and Viet Nam)

• ADB: Gas processing and EOR pilot project in Indonesia

• World Bank: CCS-ready capacity building technical assistance in Indonesia

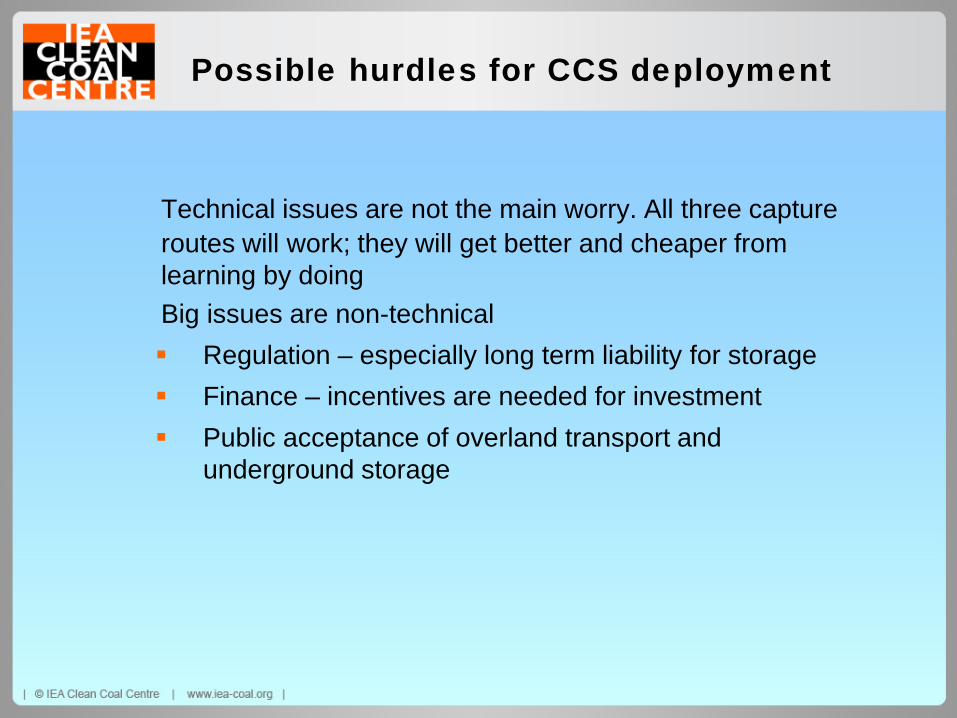

Possible hurdles for CCS deployment

Technical issues are not the main worry. All three capture routes will work; they will get better and cheaper from learning by doing

Big issues are non-technical Regulation – especially long term liability for storage Finance – incentives are needed for investment Public acceptance of overland transport and

underground storage

Comparative decarbonised power costs for Europe in the 2011-2016 period

(Alstom Power 2011)

The way forward

• Coal extraction and utilisation are set to continue to expand over the next 2 decades

• Coal has an important role in a secure and sustainable energy future but it will ultimately need to be a low carbon future

• Increasingly the focus for coal use will be China, India and the rest of Asia • While China is taking very significant steps to improve efficiency and limit

environmental impact, there is considerable scope to do better in many of the other Asian countries by creating conditions to enable the use of advanced, cleaner, more efficient technologies

• Need to incentivise best practice, high efficiency and low emissions, rather than just focus on CCS.

• Knowledge transfer will remain important and the Clean Coal Centre can fulfil a key role in disseminating technical, policy and regulatory information on a global basis