ch15

47

Price Levels and the Exchange Rate in the Long Run Price Levels and the Exchange Rate in the Long Run Chapter 15 Chapter 15 Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy International Economics: Theory and Policy , Sixth Edition by Paul R. Krugman and Maurice Obsteld

-

Upload

madalina-racea -

Category

Documents

-

view

4 -

download

0

description

chapter 15

Transcript of ch15

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 1/47

Price Levels and the Exchange Rate in the Long RunPrice Levels and the Exchange Rate in the Long Run

Chapter 15Chapter 15

Prepared by Iordanis Petsas

To Accompany

International Economics: Theory and PolicyInternational Economics: Theory and Policy, Sixth Edition

by Paul R. Krugman and Maurice Obsteld

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 2/47

&ntroduction

The La( o) *ne Price

Purchasing Po(er Parity

A LongRun Exchange Rate +odel ,ased on PPP

Empirical Evidence on PPP and the La( o) *ne Price

Explaining the Problems (ith PPP

Chapter *rgani-ation

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 3/47

,eyond Purchasing Po(er Parity. A /eneral +odelo) LongRun Exchange Rates

&nternational &nterest Rate 0i))erences and the Real

Exchange Rate Real &nterest Parity

Summary

Appendix. The isher E))ect% the &nterest Rate% andthe Exchange Rate 2nder the lexiblePrice+onetary Approach

Chapter *rgani-ation

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 4/47

&ntroduction

The model o) longrun exchange rate behavior provides the )rame(or4 that actors in asset mar4etsuse to )orecast )uture exchange rates'

Predictions about longrun movements in exchangerates are important even in the short run'

&n the long run% national price levels play a 4ey role indetermining both interest rates and the relative prices

at (hich countries products are traded'6 The theory o) !urchasing !o"er !arity #PPP$

explains movements in the exchange rate bet(een t(ocountries currencies by changes in the countries price

levels'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 5/47

The La( o) *ne Price

%a" o one !rice

6 &dentical goods sold in di))erent countries must sell )or

the same price (hen their prices are expressed in terms

o) the same currency' 7 This la( applies only in competitive mar4ets )ree o)

transport costs and o))icial barriers to trade'

7 Example. &) the dollar8pound exchange rate is 91'5# per

pound% a s(eater that sells )or 935 in :e( ;or4 must sell )or<$# in London'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 6/47

7 &t implies that the dollar price o) good i is the same(herever it is sold.

P i2S > ? E 98@ x ? P iE

(here.

P i2S is the dollar price o) good i (hen sold in the 2'S'

P iE is the corresponding euro price in Europe

E 98@ is the dollar8euro exchange rate

The La( o) *ne Price

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 7/47

Purchasing Po(er Parity

Theory o) Purchasing Po(er Parity ?PPP

6 The exchange rate bet(een t(o counties currencieseuals the ratio o) the counties price levels'

6 &t compares average prices across countries'6 &t predicts a dollar8euro exchange rate o).

E 98@ > P 2S8 P E ?151

(here.

P 2S is the dollar price o) a re)erence commodity bas4et sold in the 2nited States

P E is the euro price o) the same bas4et in Europe

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 8/47

Purchasing Po(er Parity

,y rearranging Euation ?151% one can obtain.

P 2S > ? E 98@ x ? P E

PPP asserts that all countries price levels are eual

(hen measured in terms o) the same currency'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 9/47

The Relationship ,et(een PPP and the La( o) *ne

Price

6 The la( o) one price applies to individual

commodities% (hile PPP applies to the general pricelevel'

6 &) the la( o) one price holds true )or every commodity%

PPP must hold automatically )or the same re)erence

bas4ets across countries'

6 Proponents o) the PPP theory argue that its validity

does not reuire the la( o) one price to hold exactly'

Purchasing Po(er Parity

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 10/47

Absolute PPP and Relative PPP

6 &bsolute PPP

7 &t states that exchange rates eual relative price levels'

6 Relati'e PPP 7 &t states that the percentage change in the exchange rate

bet(een t(o currencies over any period euals thedi))erence bet(een the percentage changes in national

price levels'

7 Relative PPP bet(een the 2nited States and Europe(ould be.

? E 98@%t - E 98@% t 718 E 98@% t 71 > π2S% t - πE% t ?15!

(here.

πt > in)lation rate

Purchasing Po(er Parity

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 11/47

Monetary a!!roach to the exchange rate

6 A theory o) ho( exchange rates and monetary )actors

interact in the long run'

The undamental Euation o) the +onetaryApproach

6 Price levels can be expressed in terms o) domestic

money demand and supplies.

7 &n the 2nited States.

P 2S > M s2S8 L ? R9% Y 2S ?15$

7 &n Europe.

P E > M sE8 L ? R @% Y E ?153

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 12/47

6 The monetary approach ma4es a number o) speci)ic

predictions about the longrun e))ects on the exchange

rate o) changes in.

7 +oney supplies 7 An increase in the 2'S' ?European money supply causes a

proportional longrun depreciation ?appreciation o) the dollar

against the euro'

7 &nterest rates

7 A rise in the interest rate on dollar ?euro denominated assetscauses a depreciation ?appreciation o) the dollar against the euro'

7 *utput levels

7 A rise in 2'S' ?European output causes an appreciation

?depreciation o) the dollar against the euro'

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 13/47

*ngoing &n)lation% &nterest Parity% and PPP

6 +oney supply gro(th at a constant rate eventually

results in ongoing in)lation ?i'e'% continuing rise in the

price level at the same rate' 7 Changes in this longrun in)lation rate do not a))ect the

)ullemployment output level or the longrun relative

prices o) goods and services'

6 The interest rate is not independent o) the moneysupply gro(th rate in the long run'

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 14/47

6 The international interest rate di))erence is the

di))erence bet(een expected national in)lation

rates.

R9 - R @ > πe2S - πe ?155

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 15/47

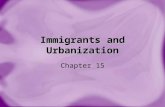

The isher E))ect

6 A rise ?)all in a countrys expected in)lation rate (ill

eventually cause an eual rise ?)all in the interest rate

that deposits o) its currency o))er' 7 igure 151 illustrates an example% (here at time t # the

ederal Reserve unexpectedly increases the gro(th rate

o) the 2'S' money supply to a higher level'

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 16/47

Slope = +

Slope = +

t 0

M US, t 0

Slope =

(a) U.S. money supply, M US

Time

Slope = Slope =

t 0

Slope = +

t 0

t 0

R $2 = R $

1 +

R $1

(igure )*+). LongRun Time Paths o) 2'S' Economic Fariables a)ter aPermanent &ncrease in the /ro(th Rate o) the 2'S' +oney

Supply

(d) Dollar/euro excan!e ra"e, E $/#

Time

() Dollar in"eres" ra"e, R $

Time(c) U.S. price le%el, P US

Time

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 17/47

6 &n this example% the dollar interest rate rises because

people expect more rapid )uture money supply gro(th

and dollar depreciation'

6 The interest rate increase is associated (ith higherexpected in)lation and an immediate currency

depreciation'

6 igure 15! con)irms the main longrun prediction o)

the isher e))ect'

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 18/47

(igure )*+. &n)lation and &nterest Rates in S(it-erland% the 2nitedStates% and &taly% 1B#!###

A LongRun Exchange Rate

+odel ,ased on PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 19/47

(igure )*+. Continued

A LongRun Exchange Rate

+odel ,ased on PPP

(igure )*+. Continued

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 20/47

A LongRun Exchange Rate

+odel ,ased on PPP

(igure )*+. Continued

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 21/47

The empirical support )or PPP and the la( o) one

price is (ea4 in recent data'

6 The prices o) identical commodity bas4ets% (hen

converted to a single currency% di))er substantiallyacross countries'

6 Relative PPP is sometimes a reasonable approximation

to the data% but it per)orms poorly'

Empirical Evidence on PPP

and the La( o) *ne Price

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 22/47

Empirical Evidence on PPP

and the La( o) *ne Price

(igure )*+-. The 0ollar80+ Exchange Rate and Relative 2'S'8/ermanPrice Levels% 1=3!###

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 23/47

The )ailure o) the empirical evidence to support the

PPP and the la( o) one price is related to.

6 Trade barriers and nontradables

6 0epartures )rom )ree competition

6 &nternational di))erences in price level measurement

Explaining the Problems (ith PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 24/47

Trade ,arriers and :ontradables

6 Transport costs and governmental trade restrictions

ma4e trade expensive and in some cases create

nontradable goods' 7 The greater the transport costs% the greater the range

over (hich the exchange rate can move'

Explaining the Problems (ith PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 25/47

0epartures )rom ree Competition

6 Ghen trade barriers and imper)ectly competitive

mar4et structures occur together% lin4ages bet(een

national price levels are (ea4ened )urther'6 Pricing to maret

7 Ghen a )irm sells the same product )or di))erent prices

in di))erent mar4ets'

7 &t re)lects di))erent demand conditions in di))erentcountries'

7 Example. Countries (here demand is more priceinelastic (ill

tend to be charged higher mar4ups over a monopolistic sellers

production cost'

Explaining the Problems (ith PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 26/47

&nternational 0i))erences in Price Level +easurement

6 /overnment measures o) the price level di))er )rom

country to country because people living in di))erent

counties spend their income in di))erent (ays' PPP in the Short Run and in the Long Run

6 0epartures )rom PPP may be even greater in the short

run than in the long run'

7 Example. An abrupt depreciation o) the dollar against

)oreign currencies causes the price o) )arm euipment in

the 2'S' to di))er )rom that o) )oreigns until mar4ets

adHust to the exchange rate change'

Explaining the Problems (ith PPP

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 27/47

Explaining the Problems (ith PPP

(igure )*+/. Price Levels and Real &ncomes% 1!

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 28/47

The Real Exchange Rate

6 &t is a broad summary measure o) the prices o) onecountrys goods and services relative to the otherIs'

6 &t is de)ined in terms o) nominal exchange rates and price levels'

6 The real dollar8euro exchange rate is the dollar price o)the European bas4et relative to that o) the American.

q98@ > ? E 98@ x P E8 P 2S ?15= 7 Example. &) the European re)erence commodity bas4etcosts @1##% the 2'S' bas4et costs 91!#% and the nominalexchange rate is 91'!# per euro% then the real dollar8euroexchange rate is 1 2'S' bas4et per European bas4et'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 29/47

6 Real de!reciation o) the dollar against the euro

7 A rise in the real dollar8euro exchange rate

7 That is% a )all in the purchasing po(er o) a dollar (ithin

Europes borders relative to its purchasing po(er (ithin the

2nited States

7 *r alternatively% a )all in the purchasing po(er o) Americas

products in general over Europes'

6 A real a!!reciation o) the dollar against the euro is

the opposite o) a real depreciation'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 30/47

0emand% Supply% and the LongRun Real Exchange

Rate

6 &n a (orld (here PPP does not hold% the longrun values

o) real exchange rates depend on demand and supplyconditions'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 31/47

6 There are t(o speci)ic causes that explain (hy the

longrun values o) real exchange rates can change.

7 A change in (orld relative demand )or American

products

7 An increase ?)all in (orld relative demand )or 2'S' output

causes a longrun real appreciation ?depreciation o) the dollar

against the euro'

7 A change in relative output supply

7 A relative expansion o) 2'S ?European output causes a longrun real depreciation ?appreciation o) the dollar against the

euro'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 32/47

:ominal and Real Exchange Rates in LongRun

Euilibrium

6 Changes in national money supplies and demands give

rise to the proportional longrun movements innominal exchange rates and international price level

ratios predicted by the relative PPP theory'

6 rom Euation ?15=% one can obtain the nominal

dollar8euro exchange rate% (hich is the real dollar8euroexchange rate times the 2'S'Europe price level ratio.

E 98@ > q98@ x ? P 2S8 P E ?15B

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

d h i i l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 33/47

6 Euation ?15B implies that )or a given real

dollar8euro exchange rate% changes in money demand

or supply in Europe or the 2'S' a))ect the longrun

nominal dollar8euro exchange rate as in the monetary

approach'

7 Changes in the longrun real exchange rate% ho(ever%

also a))ect the longrun nominal exchange rate'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

d h i i A / l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 34/47

The most important determinants o) longrun s(ings

in nominal exchange rates ?assuming that all variables

start out at their longrun levels.

6 A shi)t in relative money supply levels6 A shi)t in relative money supply gro(th rates

6 A change in relative output demand

6 A change in relative output supply

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

, d P h i P P i A / l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 35/47

Ghen all disturbances are monetary in nature%exchange rates obey relative PPP in the long run'

6 &n the long run% a monetary disturbance a))ects onlythe general purchasing po(er o) a currency'

7 This change in purchasing po(er changes eually thecurrencys value in terms o) domestic and )oreigngoods'

6 Ghen disturbances occur in output mar4ets% the

exchange rate is unli4ely to obey relative PPP% even inthe long run'

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

, d P h i P P i A / l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 36/47

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

Table )*+). E))ects o) +oney +ar4et and *utput +ar4et Changes on the

LongRun :ominal 0ollar8Euro Exchange Rate% E 98@

, d P h i P P i A / l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 37/47

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

(igure )*+*. The Real 0ollar8;en Exchange Rate% 15#!###

, d P h i P P it A / l

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 38/47

(igure )*+0. Sectoral Productivity /ro(th 0i))erences and the Change in

the Relative Price o) :ontraded /oods% 1B#1D5

,eyond Purchasing Po(er Parity. A /eneral

+odel o) LongRun Exchange Rates

&nternational &nterest Rate 0i))erences

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 39/47

&n general% interest rate di))erences bet(een countries

depend not only on di))erences in expected in)lation%

but also on expected changes in the real exchange

rate' Relationship bet(een the expected change in the real

exchange rate% the expected change in the nominal

rate% and expected in)lation.

?qe98@ q98@8q98@ > J? E e98@ E 98@8 E 98@K 7 (πe

2S - πeE ?15D

&nternational &nterest Rate 0i))erences

and the Real Exchange Rate

&nternational &nterest Rate 0i))erences

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 40/47

Combining Euation ?15D (ith the interest paritycondition% the international interest gap is eual to.

R9 R @ > J?qe98@ q98@8q98@K (πe

2S - πeE ?15

6 Thus% the dollareuro interest di))erence is the sum o)t(o components.

7 The expected rate o) real dollar depreciation against theeuro

7 The expected in)lation di))erence bet(een the 2'S' andEurope

6 Ghen the mar4et expects relative PPP to prevail% thedollareuro interest di))erence is Hust the expectedin)lation di))erence bet(een 2'S' and Europe'

&nternational &nterest Rate 0i))erences

and the Real Exchange Rate

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 41/47

Real &nterest Parity

Economics ma4es an important distinction bet(een

t(o types o) interest rates.

6 1ominal interest rates

7 +easured in monetary terms6 Real interest rates

7 +easured in real terms ?in terms o) a countrys output

7 Re)erred to as expected real interest rates

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 42/47

Real &nterest Parity

The expected real interest rate ?r e is the nominal

interest rate ?r less the expected in)lation rate ?πe'

Thus% the di))erence in expected real interest rates

bet(een 2'S' and Europe is eual to.r e2S 7 r eE > ? R9 πe

2S ? R @ πeE

,y combining this euation (ith Euation ?15% one

can obtain the desired real interest parity condition.r e2S 7 r eE > ?qe

98@ q98@8q98@ ?151#

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 43/47

Real &nterest Parity

The real interest parity condition explains di))erences

in expected real interest rates bet(een t(o countries

by expected movements in the real exchange rates'

Expected real interest rates in di))erent countries neednot be eual% even in the long run% i) continuing

change in output mar4ets is expected'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 44/47

Summary

Absolute PPP states that the purchasing po(er o) any

currency is the same in any country and implies

relative PPP'

Relative PPP predicts that percentage changes inexchange rates eual di))erences in national in)lation

rates'

The la( o) one price is a building bloc4 o) the PPP

theory'

6 &t states that under )ree competition and in the absence

o) trade impediments% a good must sell )or a single

price regardless o) (here in the (orld it is sold'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 45/47

Summary

The monetary approach to the exchange rate uses PPPto explain longterm exchange rate behaviorexclusively in terms o) money supply and demand'

6The isher e))ect predicts that longrun internationalinterest di))erentials result )rom di))erent national rateso) ongoing in)lation'

The empirical support )or PPP and the la( o) one price is (ea4 in recent data'

6 The )ailure o) these propositions in the real (orld isrelated to trade barriers% departure )rom )reecompetition and international di))erences in price levelmeasurement'

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 46/47

Summary

0eviations )rom relative PPP can be vie(ed as

changes in a countrys real exchange rate'

A step(ise increase in a countrys money stoc4 leads

to a proportional increase in its price level and a proportional )all in its currencys )oreign exchange

value'

The ?real interest parity condition euates

international di))erences in nominal ?real interest

rates to the expected percentage change in the

nominal ?real exchange rate'

&!!endix: The (isher Eect, the Interest Rate,

7/17/2019 ch15

http://slidepdf.com/reader/full/ch15563db97d550346aa9a9dd5ac 47/47

2

R $2 = R $

1 +E 2$/#

!!

and the Exchange Rate 2nder

the (lexible+Price Monetary &!!roach

(igure )*&+). Mo( a Rise in 2'S' +onetary /ro(th A))ects Ghen/oods Prices are lexible

1

R $1

&oney demand,L(R $, Y US)

1'E 1$/#

* line

Dollar/euro excan!e ra"e, E $/#

a"es o re"urn(in dollar "erms)

U.S. real money oldin!s

Dollar/euroexcan!era"e, E

$/#

Initial expected return

on euro deposits

Expected return on euro

deposits after rise in

expected dollar depreciation

E 1$/#

M 1US

P 2US

E 2$/# 2'

M 1US

P 1US

--- rela"ion