Ch. 32 - Financial Control PIFC in Iceland 2.2.2011.

35

Ch. 32 - Financial Control PIFC in Iceland 2.2.2011

-

Upload

tylor-gentle -

Category

Documents

-

view

216 -

download

1

Transcript of Ch. 32 - Financial Control PIFC in Iceland 2.2.2011.

Ch. 32 - Financial Control

PIFC in Iceland 2.2.2011

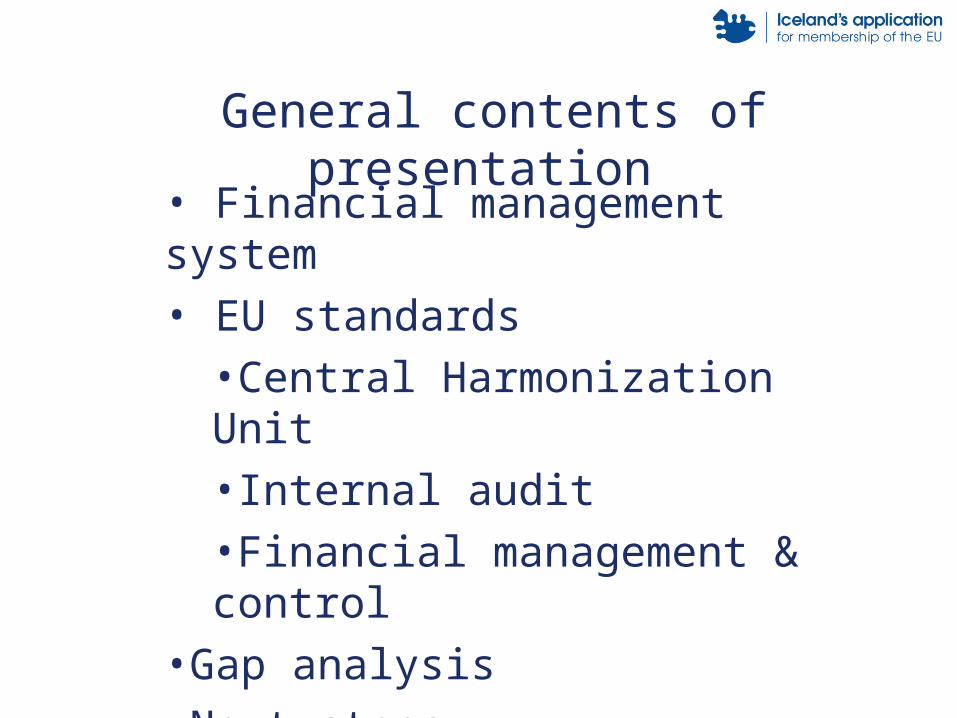

• Financial management system• EU standards

•Central Harmonization Unit•Internal audit•Financial management & control

•Gap analysis•Next steps

General contents of presentation

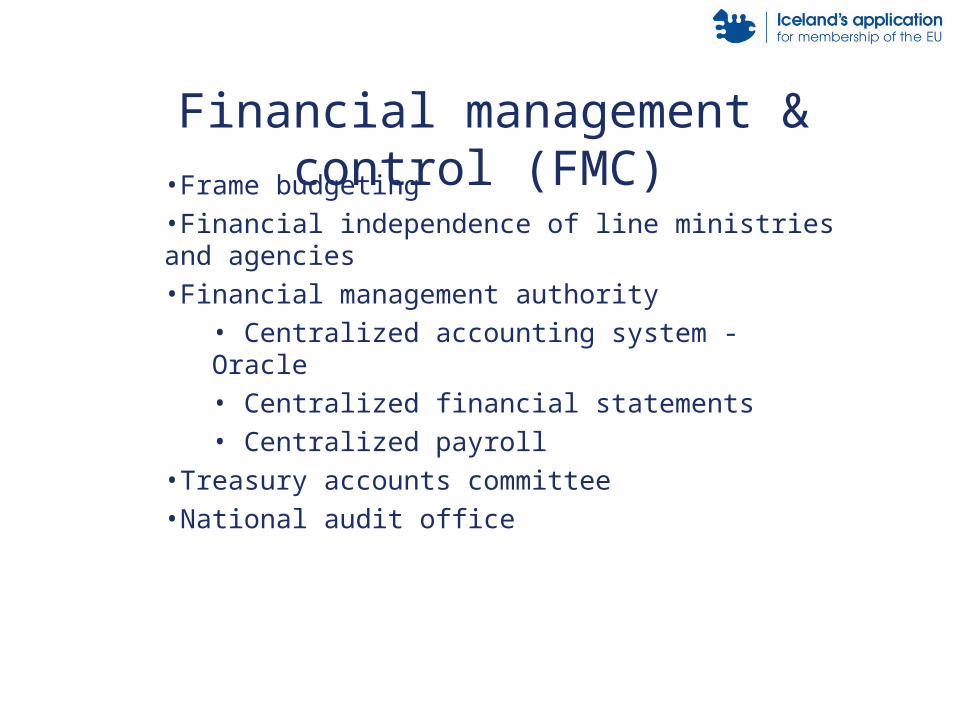

•Frame budgeting•Financial independence of line ministries and agencies•Financial management authority

• Centralized accounting system - Oracle• Centralized financial statements• Centralized payroll

•Treasury accounts committee•National audit office

Financial management & control (FMC)

• Authorized government expenditure and estimation of income

• Budget• Supplementary budget

• Execution of the budget• Based on regulation No. 1061/2004 for the implementation of the fiscal budget and the accountability for Treasury finances of the A-budget

Government financial management

•Preparation of Budget•Financial and operational yearly plans•Day to day financial control

•Monthly cash flow statements•Quarterly financial statement•Monthly review by ministries•State accounts - consolidated

•Other control•Performance management•Analysis by National Audit Office

Financial Management & Control

•Key players• Parliament • Ministry of Finance• Line ministries• Agencies• Financial Management Authority• National Audit Office• Treasury Accounts Committee

Financial management & control (FMC)

•Approves budget frames•Budget committee committee•Approves the split of the budget into items and between agencies•Passes the Fiscal budget act•Passes the supplementary budget act

Role of parliament

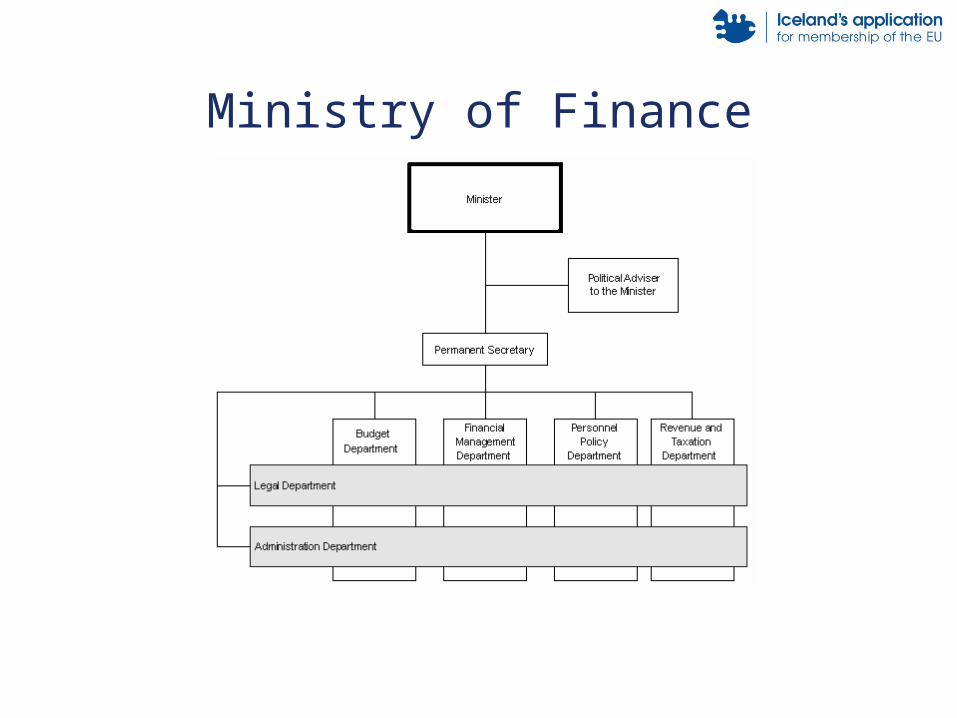

Ministry of Finance

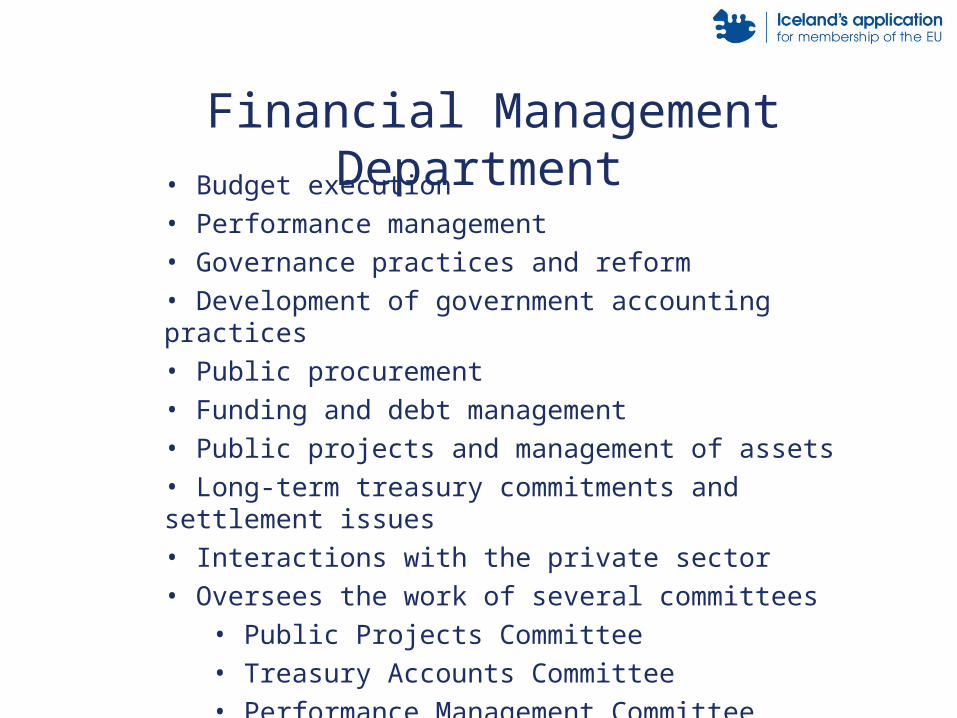

• Budget execution• Performance management• Governance practices and reform• Development of government accounting practices• Public procurement• Funding and debt management• Public projects and management of assets• Long-term treasury commitments and settlement issues• Interactions with the private sector• Oversees the work of several committees

• Public Projects Committee• Treasury Accounts Committee• Performance Management Committee

Financial Management Department

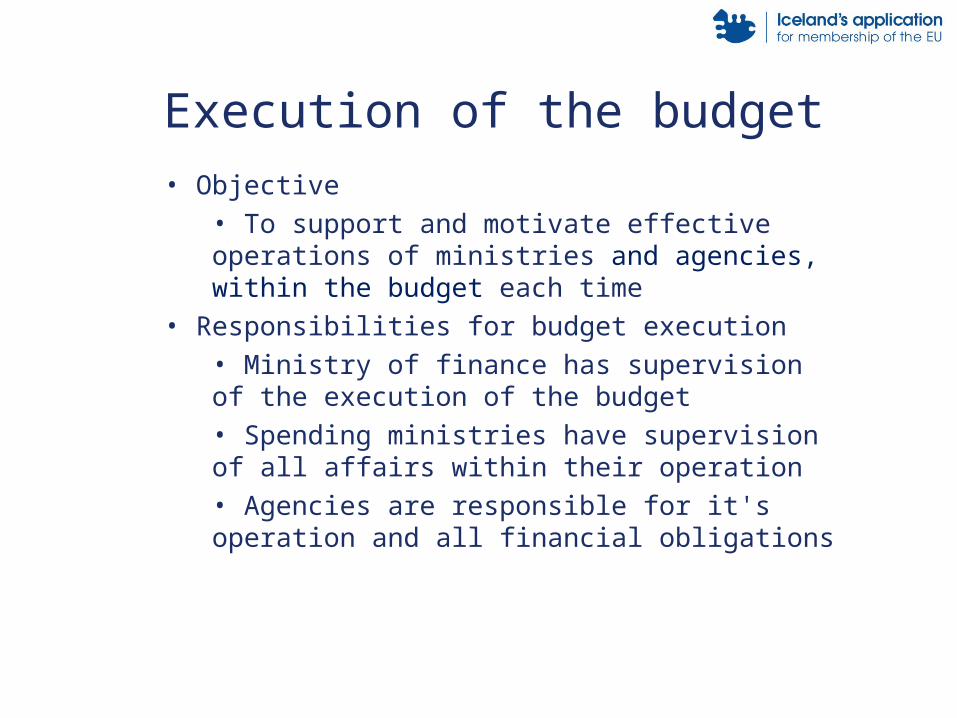

• Objective• To support and motivate effective operations of ministries and agencies, within the budget each time

• Responsibilities for budget execution• Ministry of finance has supervision of the execution of the budget• Spending ministries have supervision of all affairs within their operation• Agencies are responsible for it's operation and all financial obligations

Execution of the budget

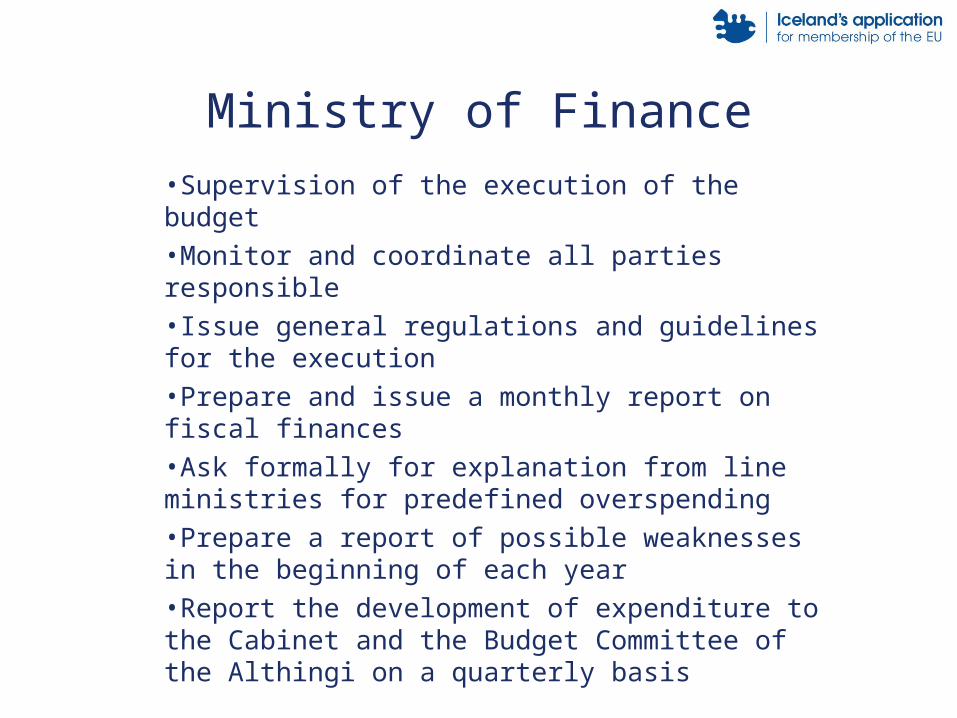

•Supervision of the execution of the budget•Monitor and coordinate all parties responsible•Issue general regulations and guidelines for the execution•Prepare and issue a monthly report on fiscal finances•Ask formally for explanation from line ministries for predefined overspending•Prepare a report of possible weaknesses in the beginning of each year•Report the development of expenditure to the Cabinet and the Budget Committee of the Althingi on a quarterly basis

Ministry of Finance

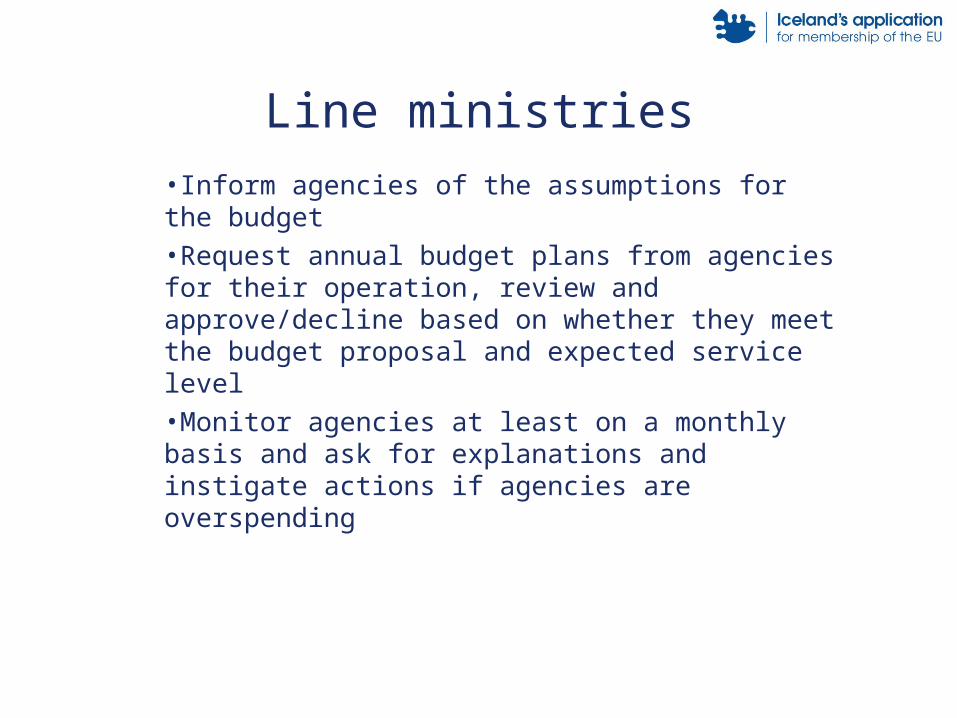

•Inform agencies of the assumptions for the budget•Request annual budget plans from agencies for their operation, review and approve/decline based on whether they meet the budget proposal and expected service level•Monitor agencies at least on a monthly basis and ask for explanations and instigate actions if agencies are overspending

Line ministries

•Agencies prepare and send to ministries an annual budget plan in line with budget and expected service level•Agencies are responsible for monitoring it's operation monthly compared to budget and plans•Managers are not authorized to initiate other financial obligations than those included in the budget limit

Agencies

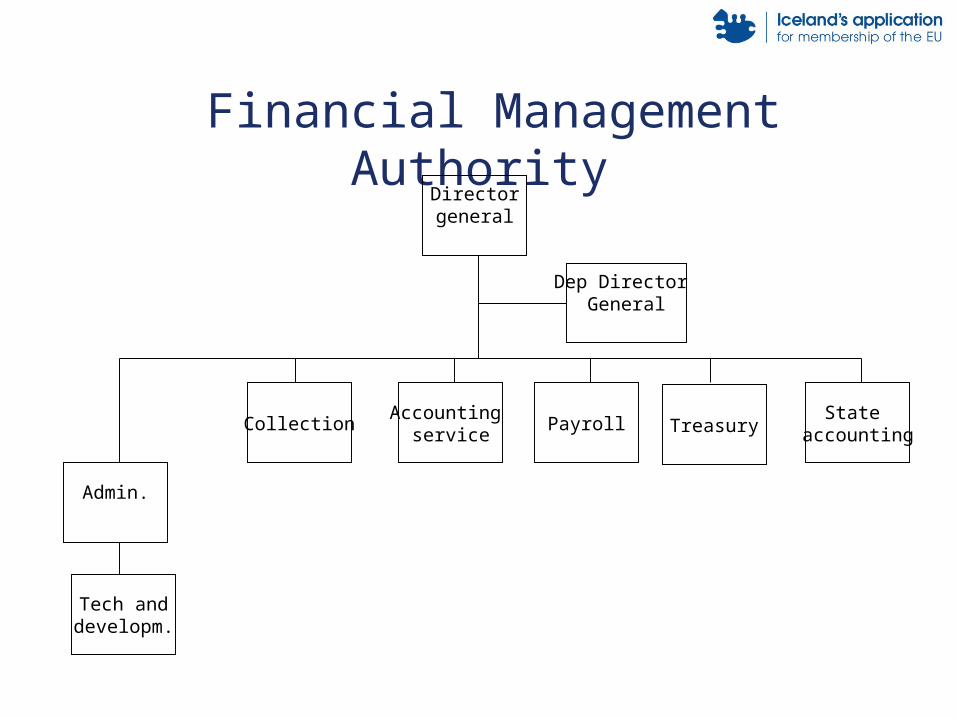

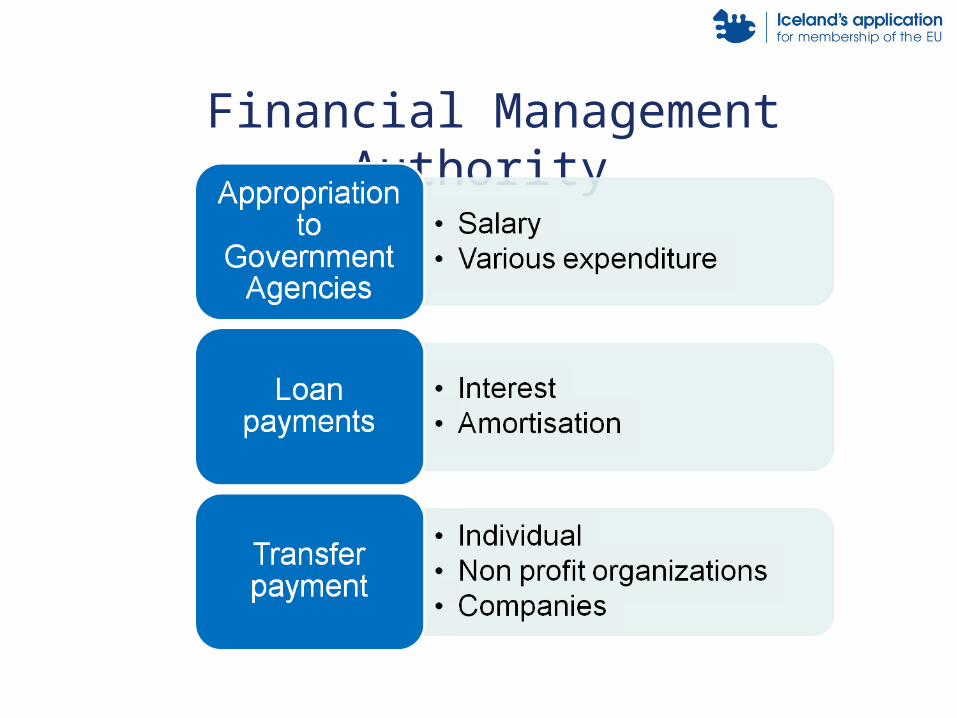

Financial Management Authority

Accounting service

State accounting

Collection Payroll Treasury

Tech anddevelopm.

Dep Director General

Directorgeneral

Admin.

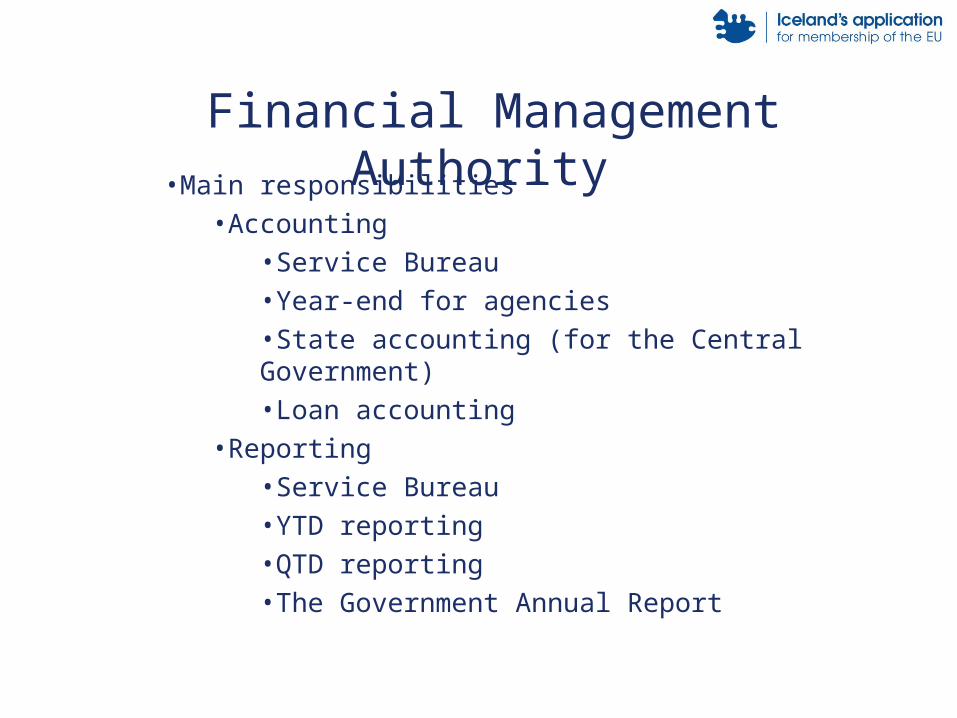

•Main responsibilities•Accounting

•Service Bureau•Year-end for agencies•State accounting (for the Central Government)•Loan accounting

•Reporting•Service Bureau•YTD reporting•QTD reporting•The Government Annual Report

Financial Management Authority

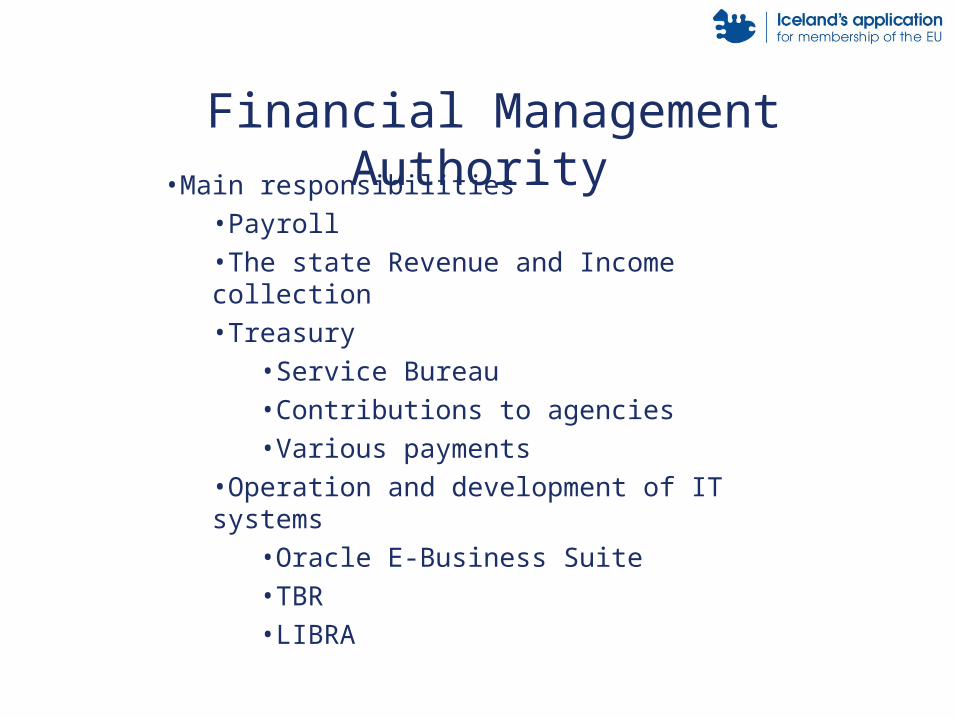

•Main responsibilities•Payroll•The state Revenue and Income collection•Treasury

•Service Bureau•Contributions to agencies•Various payments

•Operation and development of IT systems•Oracle E-Business Suite•TBR•LIBRA

Financial Management Authority

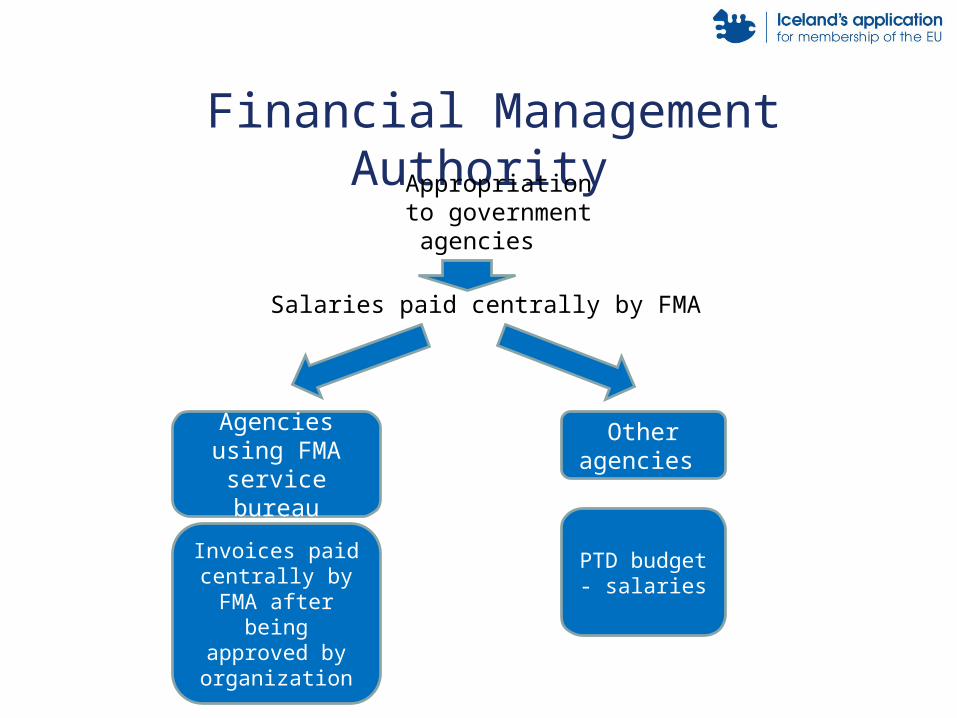

Financial Management Authority

Financial Management Authority

Salaries paid centrally by FMA

Agencies using FMA service

bureau

Invoices paid centrally by FMA

after being approved by organization

Other agencies

PTD budget - salaries

Appropriation to government agencies

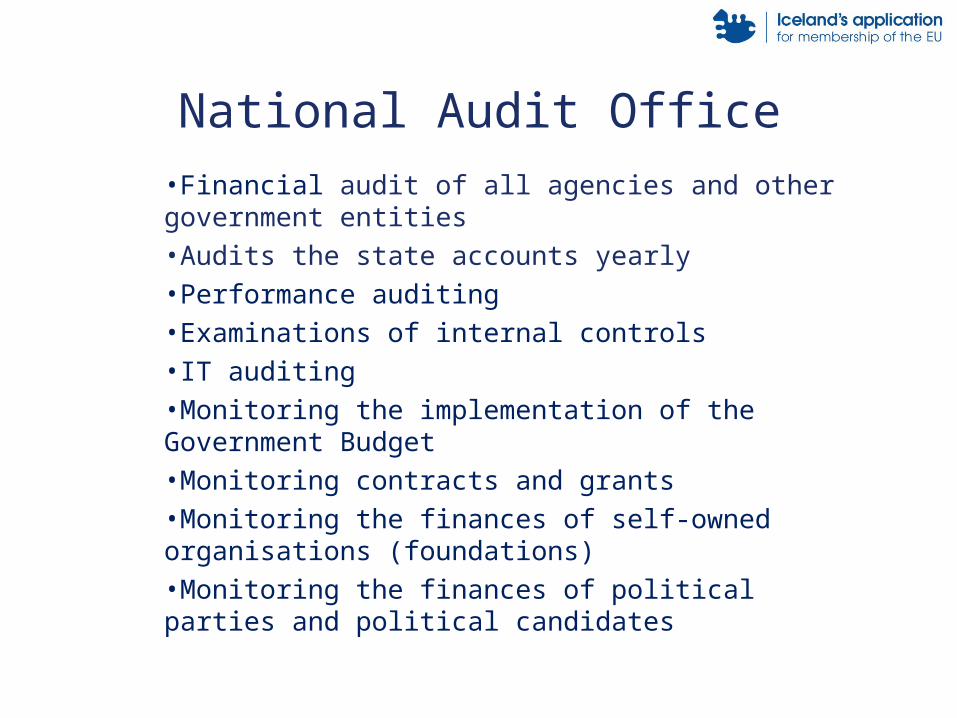

•Financial audit of all agencies and other government entities•Audits the state accounts yearly•Performance auditing •Examinations of internal controls•IT auditing•Monitoring the implementation of the Government Budget •Monitoring contracts and grants•Monitoring the finances of self-owned organisations (foundations)•Monitoring the finances of political parties and political candidates

National Audit Office

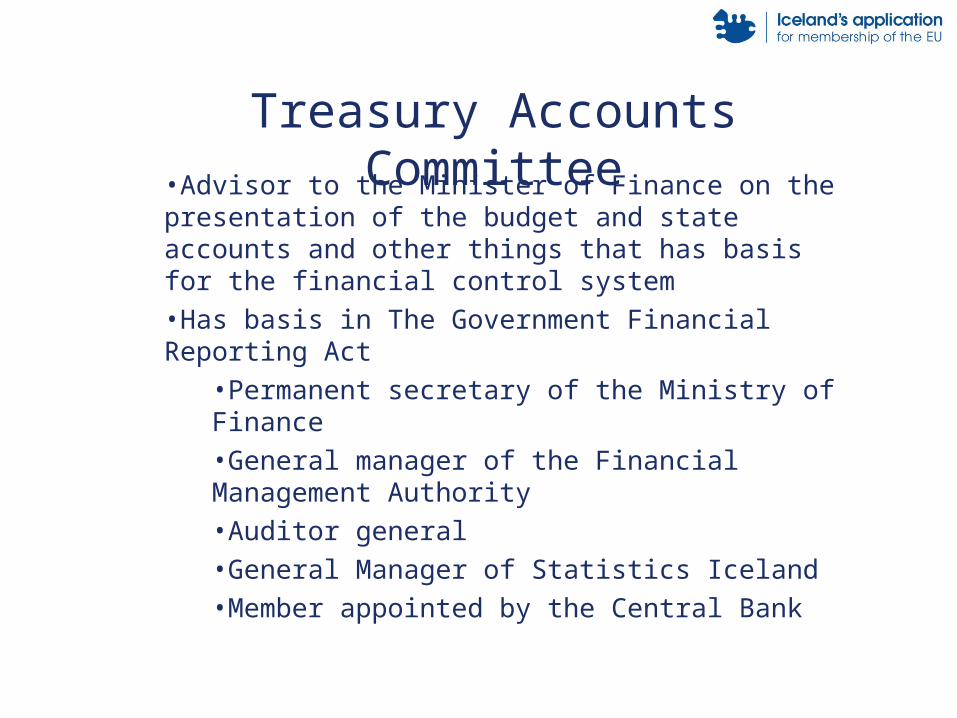

•Advisor to the Minister of Finance on the presentation of the budget and state accounts and other things that has basis for the financial control system•Has basis in The Government Financial Reporting Act

•Permanent secretary of the Ministry of Finance•General manager of the Financial Management Authority•Auditor general•General Manager of Statistics Iceland•Member appointed by the Central Bank

Treasury Accounts Committee

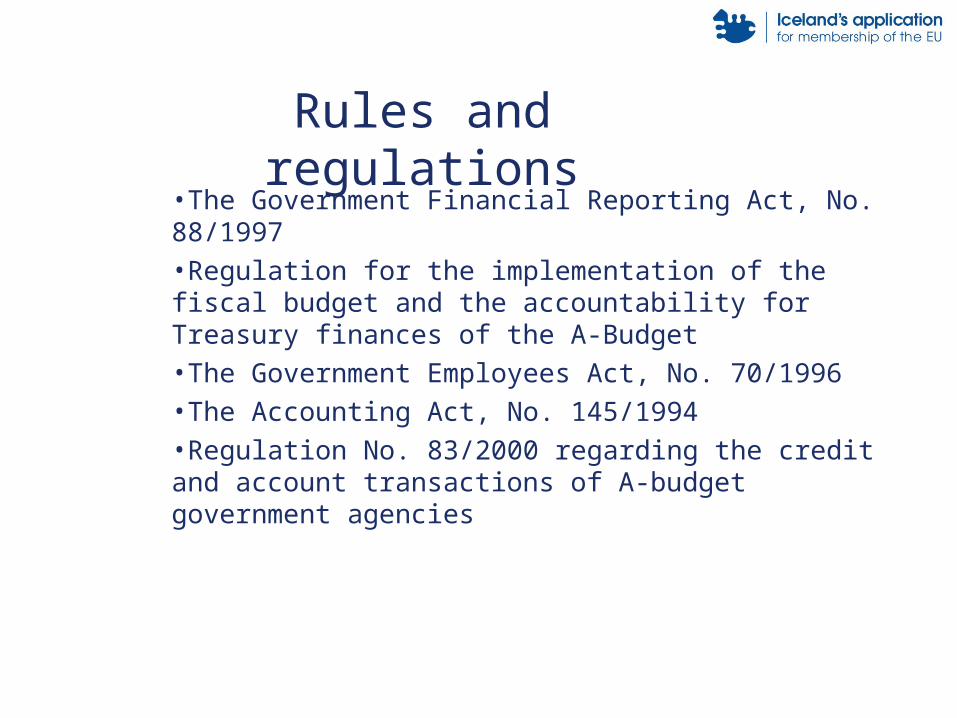

•The Government Financial Reporting Act, No. 88/1997•Regulation for the implementation of the fiscal budget and the accountability for Treasury finances of the A-Budget•The Government Employees Act, No. 70/1996•The Accounting Act, No. 145/1994•Regulation No. 83/2000 regarding the credit and account transactions of A-budget government agencies

Rules and regulations

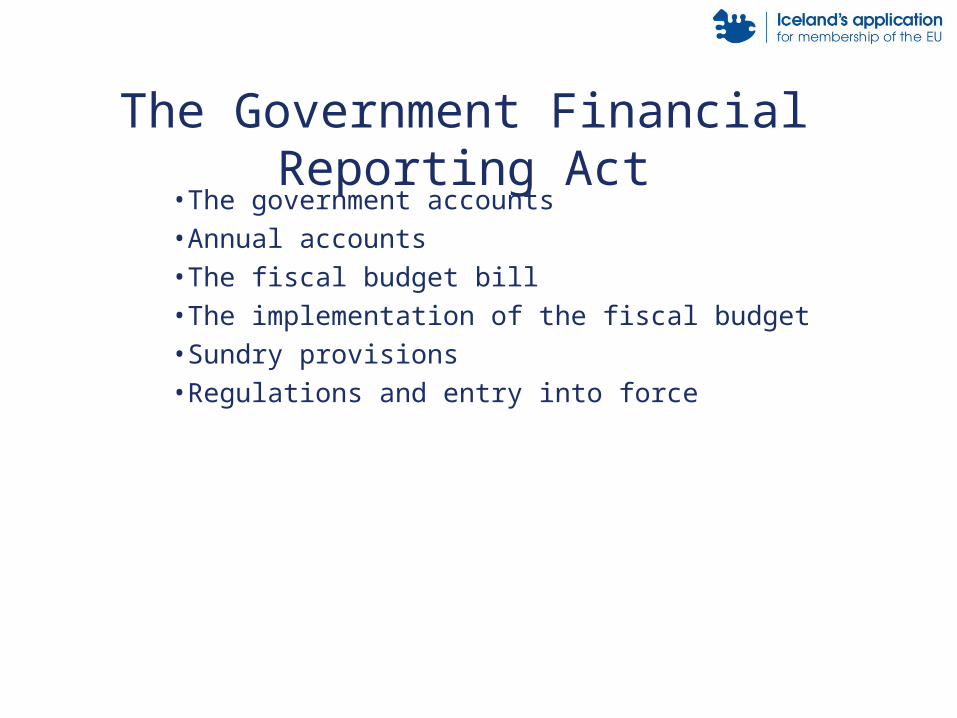

•The government accounts•Annual accounts•The fiscal budget bill•The implementation of the fiscal budget•Sundry provisions•Regulations and entry into force

The Government Financial Reporting Act

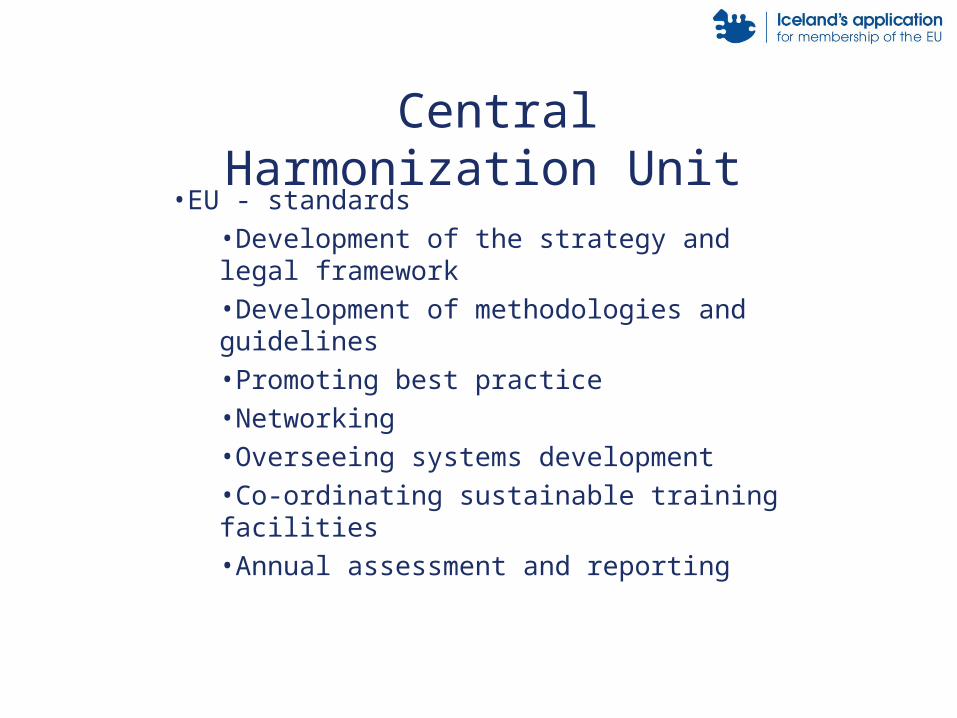

•EU - standards•Development of the strategy and legal framework•Development of methodologies and guidelines•Promoting best practice•Networking•Overseeing systems development•Co-ordinating sustainable training facilities•Annual assessment and reporting

Central Harmonization Unit

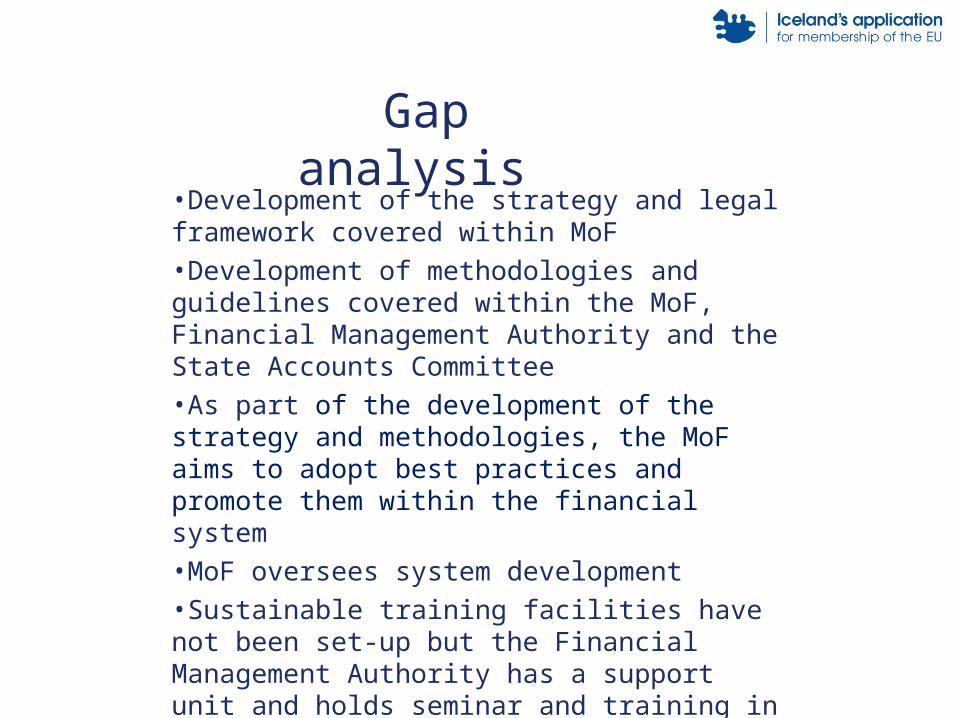

•Development of the strategy and legal framework covered within MoF•Development of methodologies and guidelines covered within the MoF, Financial Management Authority and the State Accounts Committee•As part of the development of the strategy and methodologies, the MoF aims to adopt best practices and promote them within the financial system•MoF oversees system development•Sustainable training facilities have not been set-up but the Financial Management Authority has a support unit and holds seminar and training in specific matters•Assessment and reporting is done by MoF over the year according to legislation and regulation

Gap analysis

•The formal task of a Centralized Harmonization Unit (CMU) will be the responsibility of the Financial management department of the MoF•The role of the CMU will be stated in The Government Financial Reporting Act•The State Accounts Committee will support the Financial management department and will give advise on development of rules, laws and regulation if needed

Our view and suggestions

The FMC system should cover:•Various commitments (budget allocations/appropriations, contracts)•All tendering and contracting•All kind of income, disbursements, management of assets and liabilities

Requirements:•Control environment•Managerial risk analysis and risk management•Control activities•Information and communication•Monitoring

Financial management & control (FMC)

Current system is up to standards in most areas:•Planning•Programming•Budgeting•Controlling•Accounting•Reporting•Archiving•Monitoring

Needs improving in:•Risk analysis and risk management

Gap analysis

•The Government Financial Reporting Act, No. 88/1997 will be reviewed: A review is currently being carried out•Update guidelines and rules: Ongoing project and the responsibility of MoF and the State Accounts Committee•Set guidelines and rules: Responsibility of MoF and the State Accounts Committee

Our view and suggestions

•EU - standards•Functionally independent and objective advice about the robustness of the FMC systems in terms of legality and 3E´s•Aims to add value and improve an organisation's operations•Helps an organisation to accomplish its objectives•Established by top manager•Is not responsible for design, implementation and running of FMC system•IA has access to all management meetings and their reports, to all staff, to all systems and documentation

Internal audit

• Formal internal audit is not performed in a centralized way in the current system•National Audit Office has issued guidelines for agencies in this field•Ministries have performed iternal audit informally for their agencies •Internal auditor is working within 6 agencies that work according to international guidelines•Coordinated rules or guidelines are not in place for the work of internal auditors•Part of the task is set in the performance management contracts between directors of agencies and line ministries•Individual line ministries have issued guidelines or rules for their agencies in this field•Current system needs improving in this field

Gap analysis

•Internal audit•Centralized internal audit function•Located within the Financial Management Authority

•The responsibility for specific tasks within agencies is just between this IA function and the manager of the agency

•Performs internal audit for all agencies that are to small to be able to have special IA functions•Coordinates IA for the state and supports internal auditors of the bigger agencies•Acts as a “community of internal auditors”

Our view and suggestions

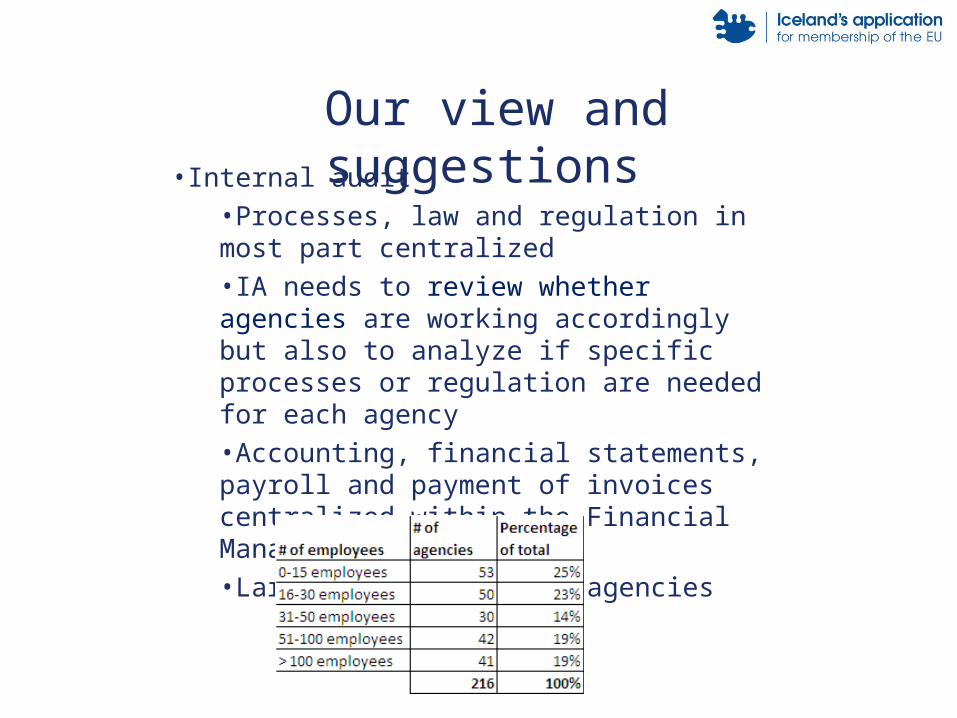

•Internal audit•Processes, law and regulation in most part centralized•IA needs to review whether agencies are working accordingly but also to analyze if specific processes or regulation are needed for each agency•Accounting, financial statements, payroll and payment of invoices centralized within the Financial Management Authority•Large number of small agencies

Our view and suggestions

• Review of law and regulation•The Government Financial Reporting Act – including CHU and IA•Government Act No. 73/1969

•Review of guidelines and processes for financial control

In process

•Further gap analysis needed•SIGMA assistance not possible•TAIEX assistance will be requested•Direct contact with DG Budget

•Public policy paper•Work has begun•Will be based on current system plus the changes already mentioned•Main lines have been discussed by the top management of MoF, Financial Management Authority, the National Audit Office and part of the government

Next steps

Thank you !