Atmospheric Histories (1765-2015) for CFC-11, CFC-12, CFC ...

CFC Reform Seminar

KPMGKPMG andand HMT/HMRCHMT/HMRC

12 January 2012

IntroductionIntroduction

Jane McCormick

Seminar agenda

9:00am Introduction

9:05am HMT/HMRC presentation on the latest CFC proposals

9 40 9:40am Q&AQ&A

10:00am KPMG comments on the proposed treatment of business and non-trading finance profits

10:55am10:55am Wrap up and conclusions Wrap-up and conclusions

11:00am Close

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

2

Presentation onPresentation on the latest CFC proposalsproposals

HMT/HMRCHMT/HMRC

CFC Reform

12 January 201212 January 2012

Ai d bj ti Aims and objectives

A CFC regime that reflects the way businesses operate in a more globalised globalised economyeconomy moving towards a more territorial corporate tax system

Strike Strike the right balance the right between delivering a balance between delivering more competitive more tax a competitive tax system and protecting the UK tax base

system

Targeting artificially diverted UK profits - proportionate Keeping the compliance burden to a minimum

Key features Targeted “all tTargeted o – “all out unless nless in” in” Reduced rate for overseas intra-group financing Flexibility to self assess using the entity level exemptions or the

Gatewayy

5

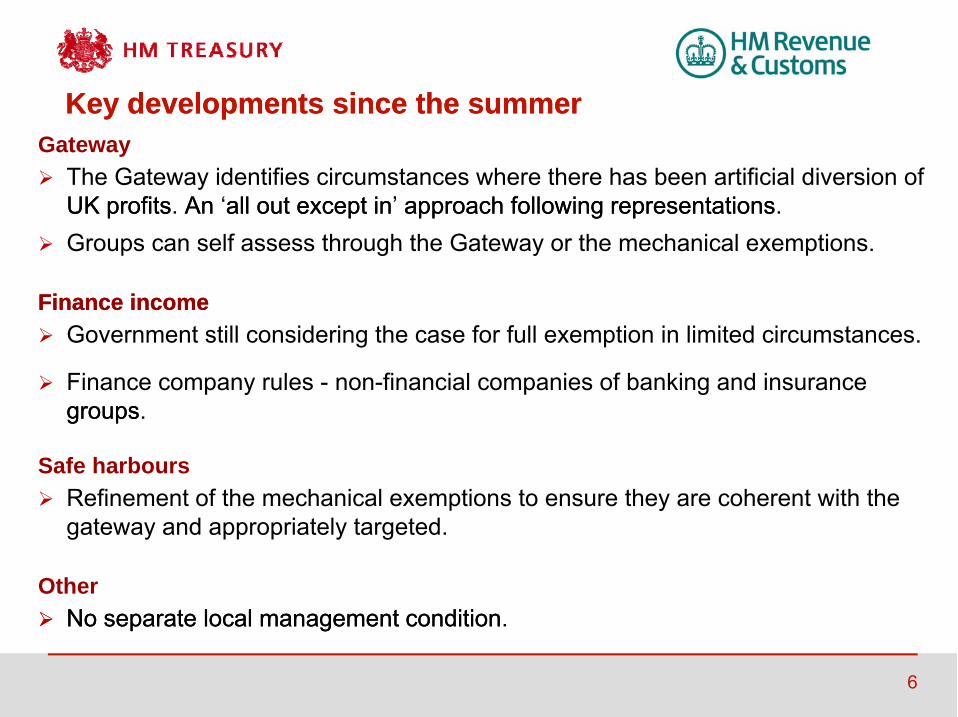

Key developments since the summerKey developments since the summer Gateway The Gateway identifies circumstances where there has been artificial diversion of

UK profits UK profits. A n An ‘all out out except inin ’ approach following representations all except approach following representations. Groups can self assess through the Gateway or the mechanical exemptions.

Finance incomeFinance income Government still considering the case for full exemption in limited circumstances.

Finance company rules - non-financial companies of banking and insurance groupsgroups.

Safe harbours Refinement of the mechanical exemptions to ensure they are coherent with the

gateway and appropriately targeted.

Other No separate local management condition No separate local management condition.

6

Feedback Feedback since t he publication of draft legislationsince the publication of draft legislation

Update document and guide to the draft legislation well received.

Many important changes have been made since June.

However, feedback that the legislation does not achieve what is set out in the uppdate document.

Focus on compliance burdens and we’re committed to working with you to minimise these.

Specific issues have been raised about the Gateway and the excluded territories exemption.

7

Th GThe Gatteway

Defines profits within the scope of the regime– “all out unless in”.

Business profits will be in the scope of the regime only where profits derive from UK operations

Financial investment pprofits ggenerallydealt with se paratelyfrom business profits – either as income

y incidental

p y to an exempt

trade or property business or, through the finance company rules.

Some special rules for t rade finance profits (banking andSome special rules for trade finance profits (banking and insurance)

8

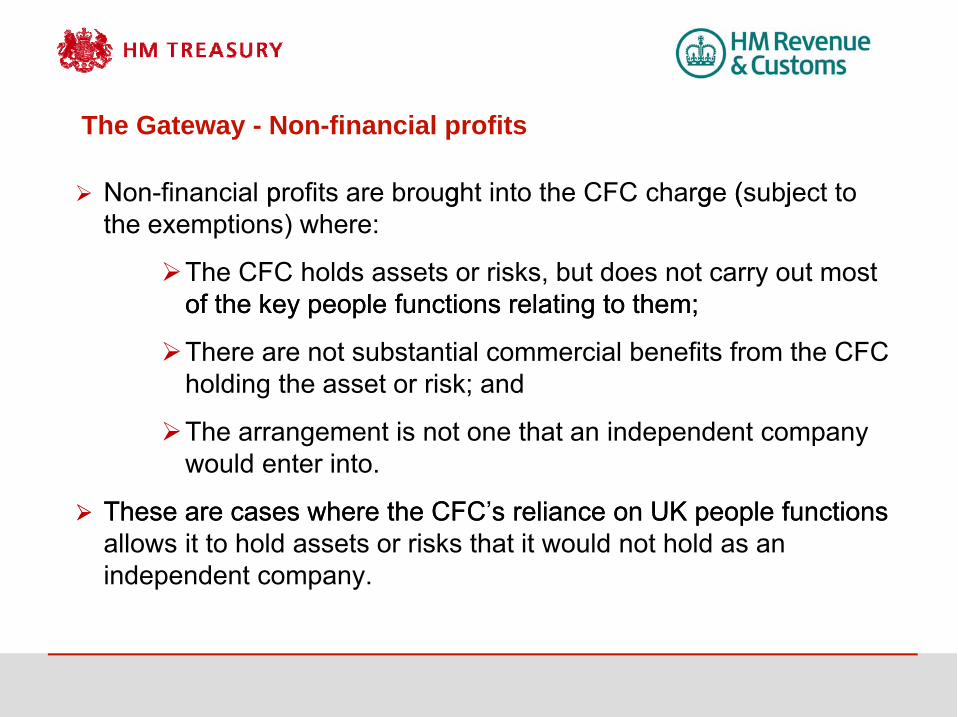

The Gateway - Non-financial profits

Non-financial pprofits are brought into the CFC charge (subject to the exemptions) where:

g g ( j

The CFC holds assets or risks, but does not carry out most of key of the the key people functions relating to them;people functions relating to them;

There are not substantial commercial benefits from the CFC holding the asset or risk; and

The arrangement is not one that an independent company would enter into.

These a re cases where the CFC’s reliance on UK people functions These are cases where the CFC s reliance on UK people functions allows it to hold assets or risks that it would not hold as an independent company.

UK tiUK perspective

Are here t people in the UK generating profits that are realised Are there people in the UK generating profits that are realised elsewhere?

Is UK reward modest – typically cost +?

But the group’s profit is much greater?

Does this profit attach to assets or risks under UK management?management?

Overall, is the UK’s reward commensurate with UK activity?

WhWhatt are th the SPFSPFs? ? They are the functions that lead to:

The assumption of risk

The ownership of assets

Th k The ongoiing managementt of fr iisks andd assetts

They are not:

Advisory functionsAdvisory functions

Supervisory functions – e.g. saying yes or no to a proposal

Governance Governance arrangements arrangements

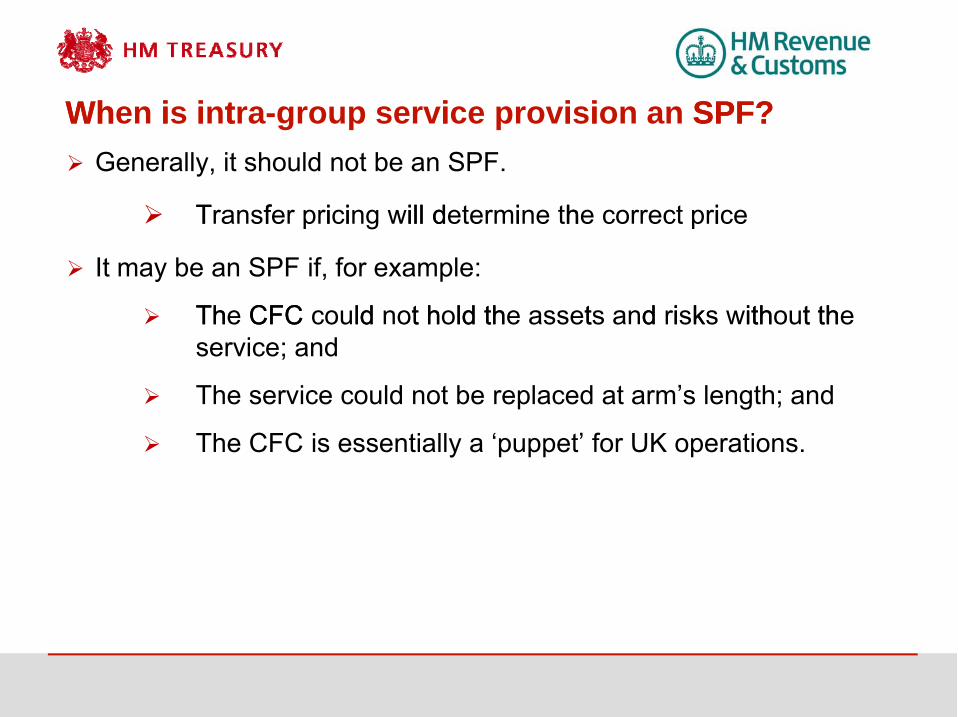

Wh i i t i i i SPF?When is intra-group service provision an SPF? Generally, it should not be an SPF.

TTransffer priiciing will dil etermiil d ne thhe correct priice

It may be an SPF if, for example:

Th e CFC could not h oldld th t d i k ith t th Th CFC t h ld the assets and risks without the service; and

The service could not be replaced at arm’s length; and

The CFC is essentially a ‘puppet’ for UK operations.

Th t di i l iThe trading income exclusion Replaced the proposed manufacturing and commercial activities

TBE and the leasingg exem pption.

An alternative to the consideration of SPFs, but is meant as a proxy and should exclude similar situations from the regime.

Conditions Business premises <50% expenditure on management per arrangement is in the

UK <20% UK income

IP transfers <20% i ncome i s from goods exported f rom th e UK 20% i i f d t d f th UK

The safe harbour includes a TAAR to prevent manipulation of commercial arrangements.

PPermanent E t Esttabli blishhmentt exemptiti on

PE anti PE exemption exemption legislation legislation will will be be updated so that the updated so that the anti -diversion rule matches the CFC rules

Exemptions apply as if the PE were a CFC

Gateway becomes 2 step process: Any chargeable profits? Are they attributed to the PE?

Non-trading finance income exempt if effectively connected to a trade or property investment business

raD f t egl si lati on o t b e publ s ei h d thi s month D ft l i l ti t b bli h d thi th

14

T t t f fi fit t t ti Treatment of finance profits – routes to exemption

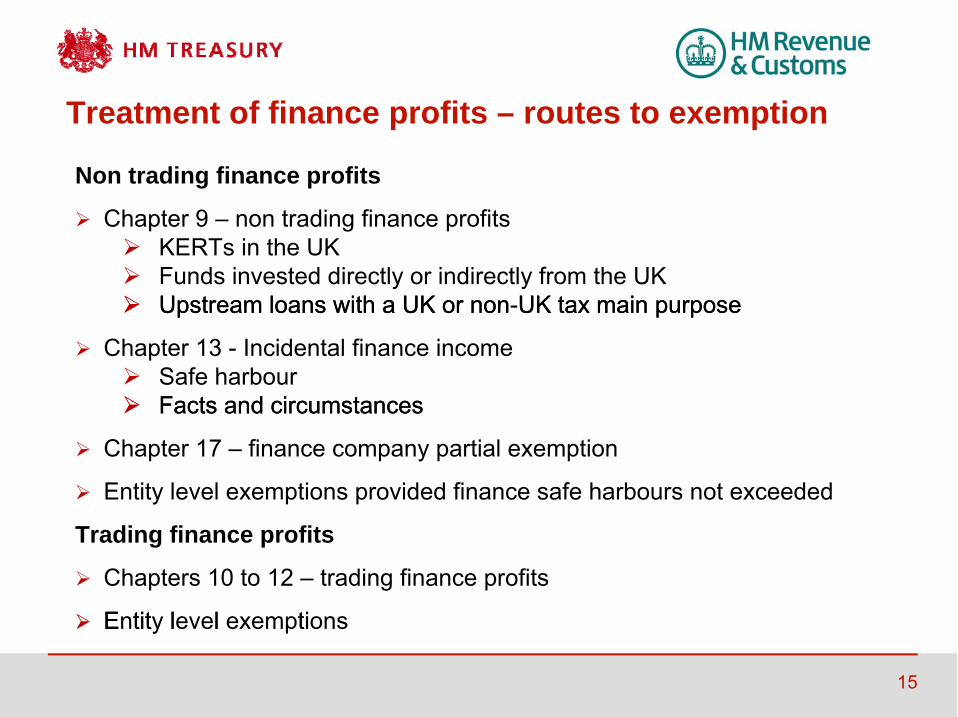

Non trading finance profits

Chapter 9 – non trading finance profits KERTs in the UK Funds invested directly or indirectly from the UK Upstream loans with a UK or non-UK tax main purpose Upstream loans with a UK or non - UK tax main purpose

Chapter 13 - Incidental finance income Safe harbour Facts and circumstances Facts and circumstances

Chapter 17 – finance company partial exemption

Entity level exemptions provided finance safe harbours not exceeded

Trading finance profits

Chapters 10 to 12 – trading finance profits

E tit Entity llevell exempti tions

15

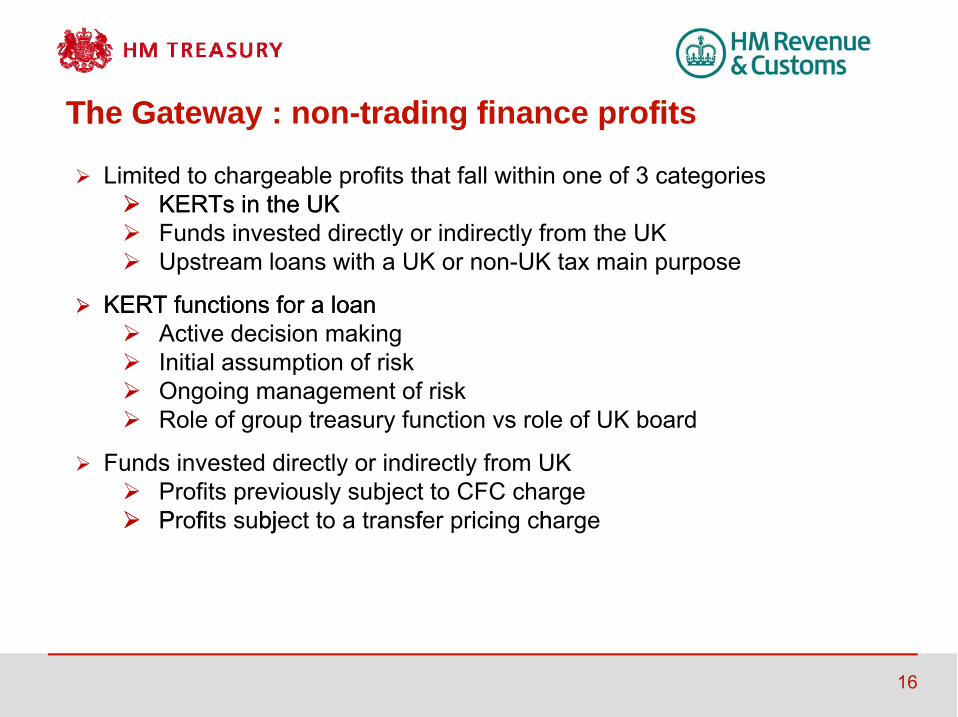

Th G t t di fi fit The Gateway : non-trading finance profits

Limited to chargeable profits that fall within one of 3 categories KERTs in the UK KERTs in the UK Funds invested directly or indirectly from the UK Upstream loans with a UK or non-UK tax main purpose

KERT functions for a a loan KERT functions for loan Active decision making Initial assumption of risk Ongoing management of risk Role of group treasury function vs role of UK board

Funds invested directly or indirectly from UK ro tP fi b t t t

Profits previously subject to CFC charge P fits subjec j t to a transfer priiciing chf harge

16

ThThe GGateway : ttrading fi finance profitfit st di

Finance profits of financial traders Investment of capital directly or indirectly indirectly from from UK Investment of capital directly or UK Capitalisation condition Safe harbours

Captive i nsurance companies Captive insurance companies Premiums paid by non UK companies and PEs exempt EEA – significant non-tax reasons for UK insurance contracts Non-EEA – UK premiums chargeable in full Capitalisation condition

17

FiFinance company rulles - overviiew

Introduction of FCPE is a pragmatic and competitive approach to allow groups to manage overseas finance operations while UK taxgroups to manage overseas finance protecting operations while protecting UK tax base

Recognises that multinationals prefer to manage overseas financing centrally , but centrally but also also removes ability to “swamp ” finance income removes ability to swamp finance income

Deliver an effective UK tax rate on overseas intra-group finance profits of 5.75% in the majority of circumstances

Applied to intra-group finance income with non-UK connected persons

Does not apply to monies held on deposit with third parties, loans to

t tinsurance companies or banks, or to finance income on most upstream lloans to hthe UK UK

Full exemption

18

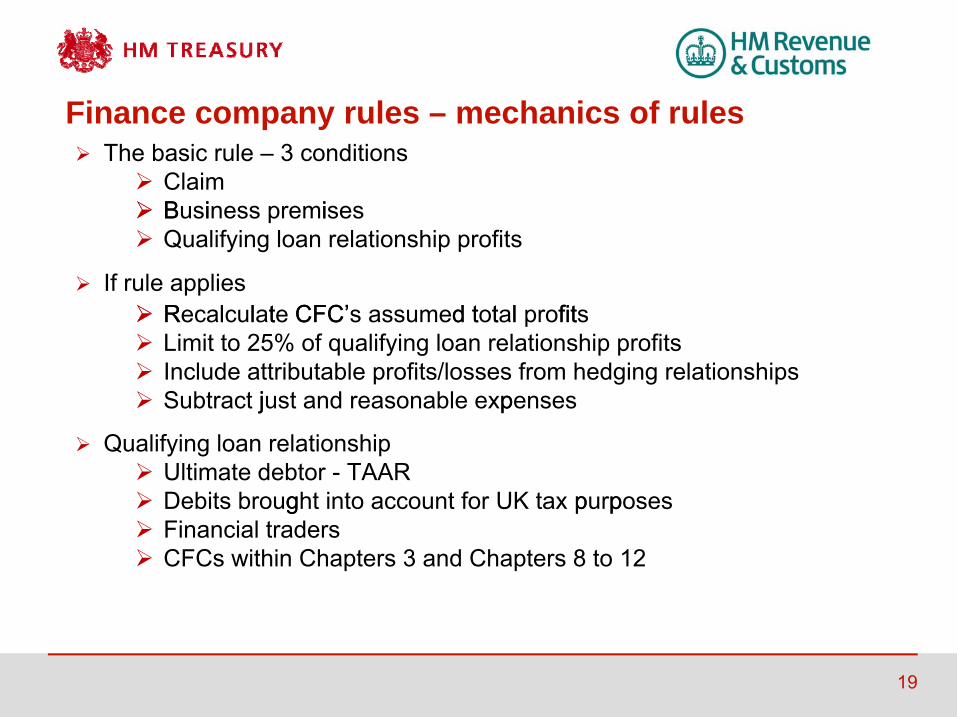

FiFinance company rulles – mechanics off rulesh i l The basic rule – 3 conditions

Claim B i i Business premises

Qualifying loan relationship profits

If rule applies R l l t Recalculate CFC’ d t t l fitCFC’s assumed total profits Limit to 25% of qualifying loan relationship profits Include attributable profits/losses from hedging relationships Subtract jjust and reasonable exppenses

Qualifying loan relationship Ultimate debtor - TAAR Debits brougght into account for UK tax ppurpposes Financial traders CFCs within Chapters 3 and Chapters 8 to 12

19

EntitE tity llevell exemptitionsLow profits exemption

SimpleSimple exemptionexemption forfor companiescompanies makingmaking aa ssmallmall profitprofit oror aa loss.loss.

<£500k trading income, <£50k investment income.

LowLow profitprofit marginmargin exemptionexemption

<10% profit above operating expenditure.

Accounts based exemption

Measure of expenditure excludes related party expenditure but include cost of goods for resale delivered into territory of residenceresidence.

The tax exemption

ReplacesReplaces thethe llowerower levellevel ooff taxtax testtest. NowNow anan exemptionexemption .

20

xcE l d d t it i ti E luded territories exemption CFCs are exempt if they are resident in a territory with a headline

tax rate of >75% of the UK main rate of Corpporation Tax and satisfy a number of conditions.

Threshold amount not to be exceeded

TAAR

Feedback re complexity

21

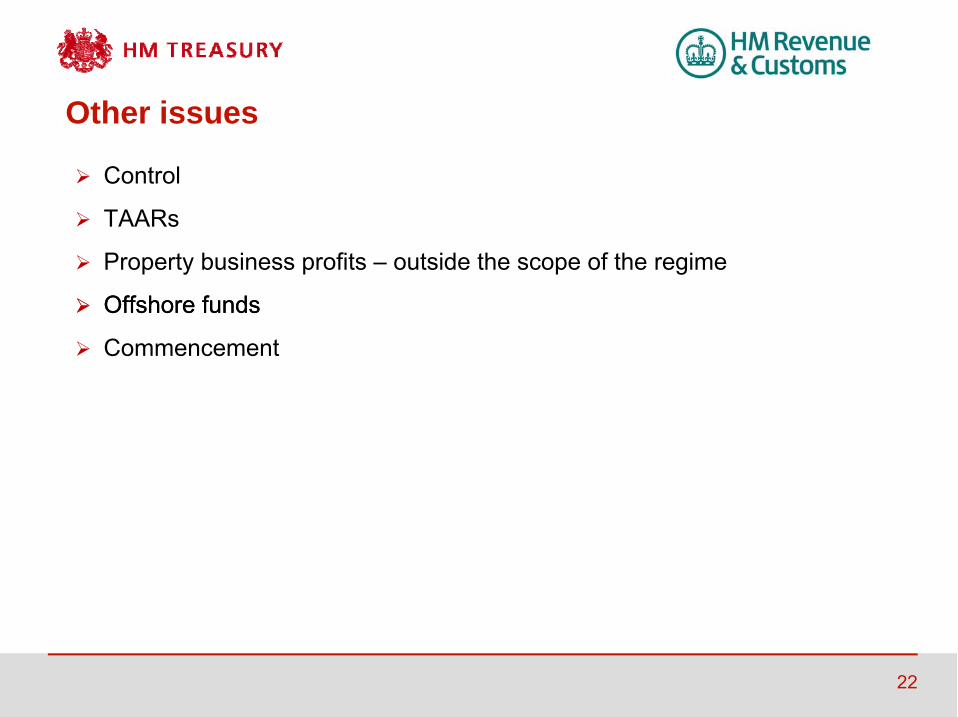

Oth iOther issues

Control

TAARs

Property business profits – outside the scope of the regime

Offshore f unds Offshore funds

Commencement

22

exN t tN t steps Businesses and advisors can and should continue to play a key role in

developin g p g the CFC reform p pinterested parties to engage

prop osals. The Government encouragges allto ensure a full range of views are heard.

Deadline for representations is 10 February 2012

Informal or staged responses welcome at earlier date Informal or staged responses welcome at earlier date

Working groups to continue

Further legislation, late January 2012. Final legislation, Finance Bill 2012

CFC team contacts

[email protected] 020 7270 6032

[email protected] @ .gov.ukh k 020 020 7147 7147 26732673

[email protected] 020 3300 9170

[email protected]@hmrc.gsi.gov.uk 020 7147 2668020 7147 2668

23

Any questions?

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

24

Comments onComments on proposed treatment oftreatment of business and nonnon-trading trading finance profits Jonathan Bridges, Debbie Green, Michael Bird and Robin Walduck

The Business Profits Gateway – basic principles

Actual fact pattern Deemed fact pattern

If:

1. The majority of profits from assets or risksrisks areare connectedconnected withith UKUK actiactivitity

by reference to SIGNIFICANT PEOPLE FUNCTIONS (SPFs)

(artificiality condition)

and

2. The separation of assets or risks from activity does not give rise to

substantialsubstantial nonnon taxtax vvaluealue (non tax value condition)

and

3. Identical arrangements meeting this separation would not be entered into

between independent companies (independent companies condition)

UK PLC

CFC

CFC

UK PLC

Attributed UK PE profits become

chargeable profits

of the CFC

SPF defined as ‘a significant people function OR a key entrepreneurial risk taking function’

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

26

Treatment of business profits

■ Intellectual property

■ Chain of command

■ Asset intensive business

■ Network business

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

27

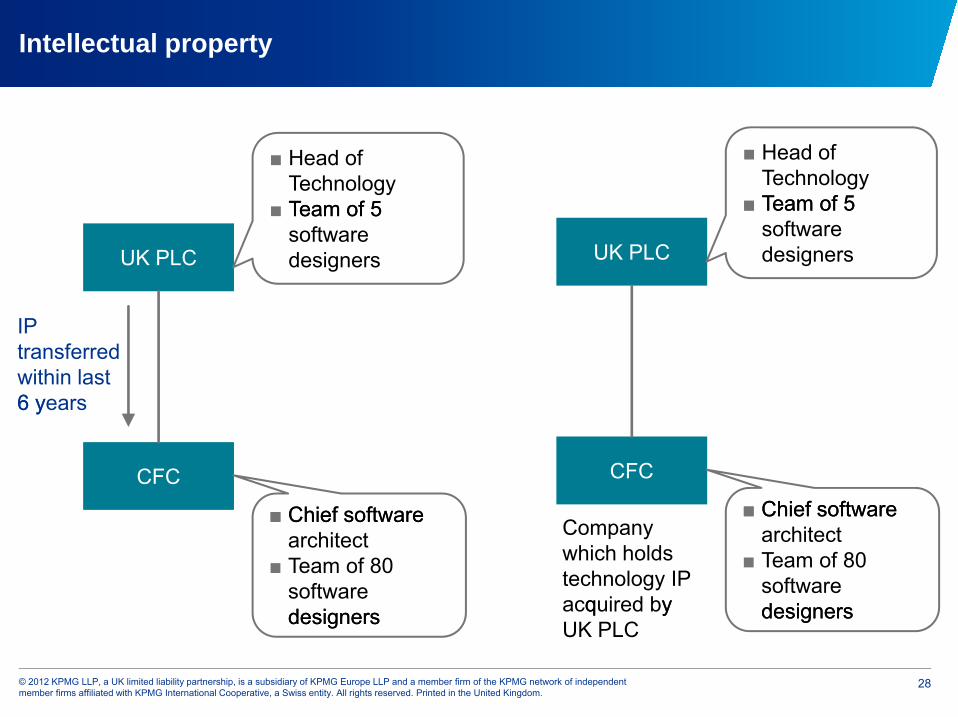

Intellectual property

IP transferred within last 6 e6 y ayearss

UK PLC

■ Head of Technology ■ Team of 5 Team of 5

software designers

CFC

■ Chief software ■ Chief software architect ■ Team of 80

software designers designers

UK PLC

■ Head of Technology ■ Team of 5 ■ Team of 5

software designers

CFC

■ Chief software ■ Chief software architect ■ Team of 80

software designers designers

Company which holds

technology IP acqq uired by y UK PLC

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

28

Intellectual property

UK PLC

■ Chief software architect ■ Team of 5 Team of 5

software designers

CFC

■ Head of ■ Head of Technology ■ Team of 80

software designersdesigners

UK PLC

■ Chief software architect ■ Head of

Technology

CFC

■ Team of 85 software designers

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

29

Chain of command – SPFs

Shareholders

BoardBoard ooff Directors

Operating Committee

CFO

Head of leggal

Head of Tax

Head of brand CFCCFC llocationocation

Decision-making and bearing of risks in relation to:

■■ OfOffshoringfshoring ofof aa brandbrand

■ Significant capital expenditure

■ Pricing strategyg gy

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

30

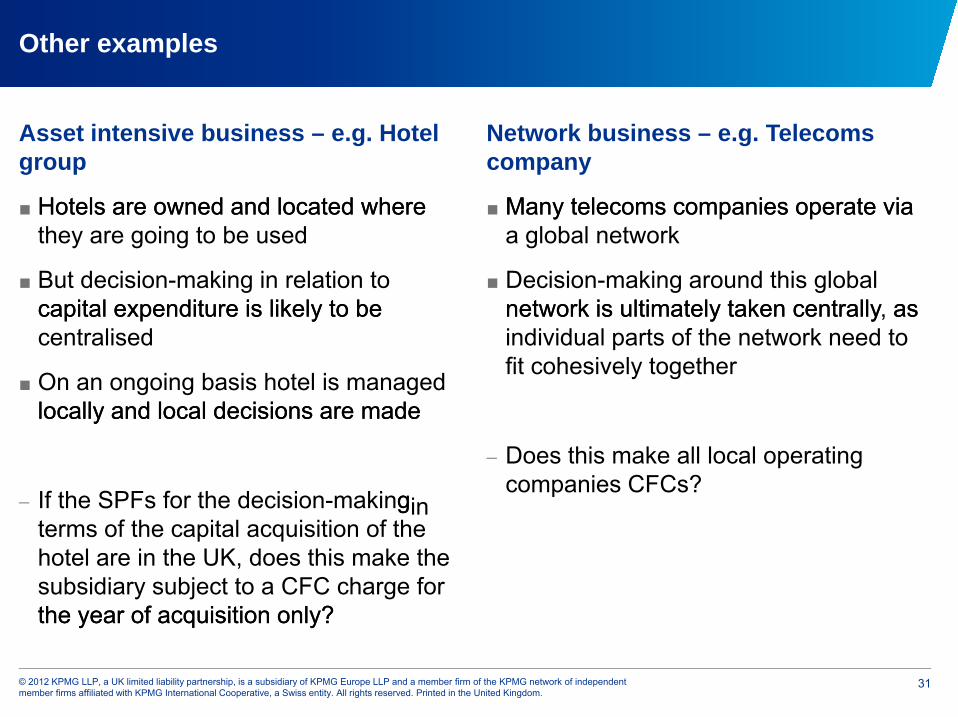

Other examples

Asset intensive business – e.g. Hotel group

■ Hotels are owned and located where Hotels are owned and located where they are going to be used

■ But decision-making in relation to capital expenditure is capital likely to be expenditure is likely to be

centralised

■ On an ongoing basis hotel is managed locally and local decisions locally are made and local decisions are made

If the SPFs for the decision-makingterms of

g in the capital acquisition of the

hotel are in the UK, does this make the subsidiary subject to a CFC charge for

the year of acquisition only? the year of acquisition only?

Network business – e.g. Telecoms company

■ Many Many telecoms companies telecoms operate companies operate via via a global network

■ Decision-making around this global network is ultimately taken centrally , asnetwork is ultimately taken centrally as

individual parts of the network need to fit cohesively together

Does this make all local operating companies CFCs?

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

31

Any questions?

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

32

Treatment of non-trading finance profits – finance company partial exemption (FCPE)

■ Applies to mixed activity companies, as well as ‘standalone’ finance companies

■ Claim must be made by UK chargeable company to HMRC

■ Apportionment of 25% of CFC’s non-trading finance profits derived from qualifying loan relationships

■ Qualifying loan relationship where ‘ultimate debtor’ is a connected company subject to exceptions and anti-avoidanceexceptions and anti -avoidance

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

33

Treatment of non-trading finance profits – qualifying loan relationships

Ultimate debtor Qualifying loan relationship?

Overseas finance company

Loans

Foreign connected companies

Yes, unless: ■ Loan used for purposes of a banking or ■ Loan used for purposes of a banking or

insurance trade ■ Loan used for purposes of UK PE or property

business ■ Loan debits result in no/reduced CFC charge ■ Loan debits result in no/reduced CFC charge

under Low Profits Exemption/Gateway ■ There is a main purpose for ultimate debtor to

provide funding for loan to another person

UK connected companies

No, unless loan used for purposes of an exempt foreign PE

Unconnected persons

(e.(e gg . banks)banks)

No

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

34

Treatment of non-trading finance profits – ultimate debtor

Ultimate debtor

Overseas finance finance

company

£100m loan Foreign connected connected company 1

£100m loan Foreign connectedconnected

company 2

OverseasOverseas finance

company

£100£100 m ll oan UK UK connected connected company or

third party bank

£100£100 m lloan ForeignForeign connected company

ReducedReduced interest WHT?

Overseas finance

companycompany

£100m loan Foreign connected

company 1 company 1

£10m loan

£30£30m

UK connected company or

third party bank third party bank

Ultimatedebtor?

loan

£60m used in own exempt

business

Foreign connected company company 22

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

35

Treatment of non-trading finance profits – FCPE practical issues

■ Foreign tax:

– Only 25% creditable, so will need to be minimised as far as possible

■ Local substance:

– Business premises required, but otherwise no specific local management requirements

– But consider any local/treaty reqqy y uirements

■ FOREX differences on qualifying loans:

– Included, so position will require managing

– Although results of any hedging arrangements will also be included

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

36

Treatment of non-trading finance profits – dealing with FOREX

-

FX

UK Parent Hedge?

Equity Equity

FinCo (‘Lender’)

FX Hedge?

Loan

Non UK Sub Non UK Sub (‘Borrower’)

Base case ■ UK Parent would previously have lent to Borrower and hedged risk

at UK level ■ UK Parent and Borrower will have different currencies Post-FinCo? ■ Complications upon capitalising the FinCo:

– Where Where to hedge the currency exposure to hedge the currency exposure– Functional currency of FinCo (vs. group accounting constraints)

■ Single-currency loans (e.g. US$): – £ Functional currency at FinCo level; hedge at FinCo level – $ Functional currency; hedge/match at UK Parent level – Designated currency election (tax only; distributable reserves?)

■ Multiple-currency loans (e.g. US$ and ¥): £ F unctional currency individual – FX FX hedges at FinCo level£ Functional currency – individual hedges at FinCo level

– $ Functional currency – hedge ¥ to $; hedge $/£ at UK Parent level

– Designated currency election of limited use (one currency only)

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

37

Treatment of non-trading finance profits – trading/property companies

Overseas trading/property

company

Business pp rofits Non-trading finance profits finance profits

■ Non-trading finance profits excluded if:

– Entity-level exemption applies

Safe harbour Safe harbour applies: – applies:

profits do not exceed 5% of PBIT from exempt business; or

to the extent profits athe extent profits rise from arise from funds funds held to held for purpose of exempt business

– Gateway does not apply because profits:

are not attributable to UK SPFs; are not attributable to UK SPFs;

do not arise from capital invested from UK; and

do do not not arise on arise on upstream loans upstream loans

■ As alternative to Gateway, claim FCPE for qualifying profits so that partially exempt

■ An a are f Any remaining profits ithin Gate llremaining profits within Gateway are fullytaxable

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

38

Any questions?

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidia ry of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. Printed in the United Kingdom.

39

Wrap up andWrap-up and conclusions

Jane McCormick

Thank you

© 2012 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a SSwiiss entittity. AllAll riighthts reservedd. PPriinttedd iin ththe UUnititedd Kingdom.

The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks oof KPMGG Inteternatatioonaal CoopeCooperatativee ((KPMGG International).