CFA Institute Research Challenge - cfasociety.org IRC Documents/IRC 2018... · Pernod Ricard -...

30

CFA Institute Research Challenge Hosted by CFA Society France Team P 1

Transcript of CFA Institute Research Challenge - cfasociety.org IRC Documents/IRC 2018... · Pernod Ricard -...

CFA Institute Research Challenge Hosted by

CFA Society France Team P

1

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

2

Pernod Ricard is ranked number 2 in the wine and spirits market since 2005 and its

acquisition of Allied Domecq (Ballantine’s , Beefeater and Malibu among iconic brands). The

group produces and distributes a large range of spirits such as Vodka, Whiskey, Gin, Tequila

and Cognac but also wine. Given its geographic positioning, its wide range of brands and a

dynamic market in the spirits premium segment, we initiate coverage with a BUY rating on

Pernod Ricard supported by target price of €153.7 and a potential upside of 17% over a 1

year period.

The main drivers that bring us to stand with this recommendation are as follows:

A significant rebound in Asian markets: the group is market leader in China and

India, which are the two most significant spirits markets. Pernod Ricard will benefit

from the sharp improvement in these countries that mainly consume whiskey, boosted

by a notable increase in volume and a positive pricing/mix.

An upward perspective in the high margin Whiskey and Cognac markets:

underlying trends on these markets are strongly positive, fuelling growth for its

whiskey and cognac brands, whose exposure in the total group revenues has been

continuously growing since 2012. Whiskey and Cognac will contribute to improve the

EBITDA margin, especially in China, India and the US.

Targeted acquisitions of ultra-premium brands: the group achieved strategic local

spirits acquisitions over the past years in ultra-premium brands. These type of

alcohols (Mezcal, Gin, Bourbon) are forecasted to grow at a high CAGR. Hereby, we

expect the group to create value thanks to its recent acquisitions at sensible multiples.

December 20th 2017: Fitch Ratings decided to upgrade Pernod Ricard’s rating to

BBB. This decision reflects the strong efforts made by the company to deleverage over

the past two years as well as solid operating performances and improving profitability.

November 15th 2017: the UK Supreme court decided to implement a minimum price

for alcohol in Scotland. As of May, a 70cl Whiskey bottle will be sold at a min. GBP14.

June 7th 2017: Pernod announced the purchase of a majority stake of the Mexican Del

Maguey Single Village, which is ranked n°1 in Mezcal spirits production in the US. This

investment is consistent with its vision of selling ultra-premium spirits.

January 31th 2017: NBV Investment, a subsidiary of Pernod, acquired American

spirits producer Smooth Ambler. The portfolio embraces Contradiction Bourbon and

Old Scout Single Barrel Bourbons in addition to Gins and Vodkas.

Figure 1: Company data

STUDENT RESEARCH – TEAM P Agro-Food Industry

Euronext Paris

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Summary

Recent news:

Figure 2: Share price 3y

70

80

90

100

110

120

130

140

150

j-1

5

a-1

5

j-1

5

o-1

5

j-1

6

a-1

6

j-1

6

o-1

6

j-1

7

a-1

7

j-1

7

o-1

7

Pernod Ricard CAC 40 Base 100

Figure 3: Share price data

Ticker Bloomberg RI.FP

Ticker Reuters PERP.PA

Ticker S&P Capital IQ ENXTPA:RI

Shares O/S (m) 265.42

Float % 45.8%

Closing Price 130.95

Avg 3M Dly Vlm (mm) 0.41

52-wk High / Low 133.60 / 103.85

Gap (% Low) 128.6%

Market Cap (bn€) 34 578

Net debt 2017 (m€) 7 853

Price Earning Ratio 25.05

Price to Book Ratio 2.55

Earnings Per Share 5.28

Dividend yield 2016 % 1.53%

Market Data (12/01/2018)

Source: S&P Capital IQ

Source: S&P Capital IQ

Source: S&P Capital IQ

Valuation date January 12th 2018 Current Price €130.95 Target Price €153.7

Sector Beverages Upside 17% Recommandation BUY

Pernod Ricard

% change 1m 3m 1y 3y

Pernod Ricard 1.1% 7.6% 25.7% 35.3%

Eurostoxx 50 0.3% 0.2% 9.9% 17.1%

CAC 40 1.7% 2.9% 13.4% 30.5%

Diageo -0.3% 2.8% 21.3% 44.1%

Share price data

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023

Revenue (in m€) 8 558.0 8 682.0 9 010.0 9 195.9 9 530.0 9 873.4 10 202.1 10 518.3 10 833.9Revenue growth 7.7% 1.4% 3.8% 2.1% 3.6% 3.6% 3.3% 3.1% 3.0%

EBITDA (in m€) 2 433.0 2 481.0 2 599.0 2 644.4 2 792.4 2 955.5 3 133.9 3 309.4 3 433.2EBITDA margin (in %) 28.4% 28.6% 28.8% 28.8% 29.3% 29.9% 30.7% 31.5% 31.7%

Net income (in m€) 880.0 1 255.0 1 421.0 1 492.7 1 600.5 1 757.8 1 890.5 2 021.2 2 111.8Net margin (in %) 10.28% 14.5% 15.8% 16.2% 16.8% 17.8% 18.5% 19.2% 19.5%

Free Cash Flow (in m€) 1 475.0 1 826.0 1 786.0 1 797.4 1 788.3 1 898.4 2 053.2 2 185.5 2 216.9FCF yield (in %) 4.3% 5.3% 5.1% 5.2% 5.2% 5.5% 5.9% 6.3% 6.4%

Net debt (in m€) 9 086.0 8 793.0 7 870.0 7 709.5 7 082.1 6 515.2 5 749.6 5 013.2 4 290.0Net debt / EBITDA 3.7x 3.5x 3.0x 2.9x 2.5x 2.2x 1.8x 1.5x 1.2xEV / EBITDA 13.5x 14.8x 14.9x 17.7x 16.8x 15.9x 15.0x 14.2x 13.7xDividend yield 1.3% 1.4% 1.4% 1.6% 1.7% 1.8% 2.0% 2.1% 2.2%

Key financialsHistorical Projected

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

The group was created in 1975 following the merger of two French anise-based spirits

producers Pernod and Ricard. Pernod Ricard, world’s second largest producer of wines and

spirits after Diageo, enjoyed a turnover of €9.01bn as of June 2017 (+3.8% YoY). Specialized

in spirits, the group is present in a large range of alcohols from white alcohols, whiskeys,

cognac and other liqueurs to champagne and wines (although minor as of today).

The following three well-timed acquisitions performed in the first decade of the 2000’s led

the group to become the second market leader in wine and spirits:

• In 2001, it acquired, jointly with Diageo, in a complex deal, the wine and spirits division

of Canadian group “Seagram”, with mostly whiskeys and cognacs, for €3.7bn.

• In 2005, the group purchased the British “Allied Domecq” which produced premium

international spirits brands and premium wines for €10.7bn.

• In 2008, the group made its latest large acquisition by purchasing “Vin&Spirits”, owner

of the Absolut Vodka brand, for €5.6bn.

An international and decentralized group:

• Pernod Ricard is well implanted internationally with a presence in three major

geographical regions (Europe, Americas and Asia). However, its main markets remain

Asia and the United States. The group owns more than 85 affiliates, 18,000 employees

and 100 production plants worldwide.

• The group has adopted a decentralized organization. All subsidiaries respond to one

holding, each of them being specialized in a given brand (eg. development, specific

strategy and the production of each brand of alcohol) or in a specific market (eg. handle

the development and distribution of the products at a local level).

The group has split its products and strategies into four main poles:

• Strategic International Brands: gathers the 14 most prestigious and internationally

renowned brands of the group (12 spirits and 2 champagnes). This division is the main

contributor to the group’s growth for last fiscal year (+4%), mostly driven by whiskey

brands such as Jameson, the Martell cognac and the Perrier-Jouët champagne.

• Strategic Local Brands: embraces the 15 local brands, mainly exploited to penetrate

emerging markets. This segment is strongly decelerating with a 1% growth in 2016/17

compared to 5% last year. This slowdown is mainly due to the negative impact of

regulations in India.

• Premium Wines: an expanding pole composed of 4 premium wines. Last year was the

second consecutive year of solid performance for the segment (+4% and +5%

respectively).

• Other: this diversified segment gathers all products innovation (from innovative

products to the by-products of Strategic International Brands) but also accounts for the

resulting growth from new acquisitions, synergies and the premiumization strategy.

The group’s business model:

Pernod Ricard is continuously focusing its portfolio on strategic local and international

brands by withdrawing from non-key assets. Last divestitures included non-strategic local

assets such as the Vodka Frïs or Distillery Glenallachie. Alongside with the development of

its premium wines, Pernod Ricard is also surfing on the strong growth of Whiskey

consumption worldwide (especially in the US and India) with 50% of its strategic portfolio

being Whiskeys. Additionally, the group is specialized in premium brands which account for

76% of SIB (Strategic International Brands) volume sales.

The group leans on a premiumization strategy that is evidenced by:

(1) Organic Growth through innovation and development of new premium products

(2) External Growth through acquisitions of premium trendy alcohols

(3) A strong presence with a top-quality image worldwide through heavy R&D investments

3 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

1 Business description

62%19%

6%

13%

Sales breakdown by strategic poles

Strategic International Brands

Strategic Local Brands

Premium Wines

Others

Figure 4 : Sales breakdown by strategic poles (2017)

Figure 6: Spirits brands portfolio

Strategic

International

Brands

Strategic

Local Brands

Vodka AbsolutPolish

Wyborowa

Cognac Martell

Jameson Blenders Pride

Chivas JP Whisers

The Glenlivet Royal Stag

Ballantine's Imperial Blue

Royal Salute 100 Pipers

Imperial

Passport Scotch

Clan Campbell

Anisee Ricard Pastis 51

Gin Beefeater Seagream's Gin

Rum Havana Club

Ready-to-drink Malibu

Perrier-Jouet

Mumm

Armenian

Ararat

Koffee Liqueur

Kahlua

Amaro

Ramazzoti

Tequila Olmeca

Local alcohols

Champagne

Wiskeys

Source: Annual report

Source: Annual report

Source: Annual report

Figure 5 : Geographic breakdown (2017)

39.6%

29.5%

30.9%

Asia/ROW

Americas

Europe

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

4 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

2 Industry overview and competitive positioning

Industry overview:

From a macroeconomic point of view, the main demand drivers in the alcoholic beverages

industry are: 1/ an increasing GDP, which often translates into higher consumption

expenditures; 2/ income class redistribution, leading to rising purchasing power of

consumers; and 3/ global population growth (predominantly in emerging countries),

ultimately meaning an increasing consumer base.

Regional growth dynamics for Pernod Ricard are therefore obviously specific for each of its

geographical groups: Americas, Europe and Asia/Rest of the World.

GDP growth:

We notice positive trends for the overall economic health of Pernod Ricard key strategic markets. China remains one of the fastest growing economies around the world, having its GDP growth at a still remarkable 6.5%/7% in 2016 and 2017e. India’s economy is also confidently growing at attractive rates of ca. 7%. The US. is expanding gradually with the latest figures for Q2-Q3 2017 reaching 3.2%, the fastest pace over the last couple of years. Michigan consumer sentiment index (MCSI), as a result, is very high, hitting a 95.9 estimate. Thus, people are expecting favorable economic conditions, leading to an increase in real personal consumption expenditures, which certainly stimulates demand for the group’s products.

Income class redistribution:

The key driving force of future growth for Pernod Ricard is an emerging middle class in China and an increasing high income class in group largest market - US In China, the upper middle class, i.e. people earning $15,000 to $35,000 per year, is projected to expand from 20% in 2012 to 33% of total population in 2021. Those are the people who can now afford a bottle priced between €15 and €20. Thus, due to emerging middle class, Pernod Ricard has now an opportunity to expand its premium route to market in the region. In the US we observe an increasing number of high income population, that is people earning more than $100,000 and comprising the upper middle and affluent classes. If in 2012, these two income classes combined represented 38.3% of population, Bloomberg projections suggest that by 2021 this figure will increase to 42.5% of total population. Thus, group ultra-premiumization across whiskey, tequila and cognac categories is a sensible strategy in the region in our eyes.

Population growth:

Emerging markets are characterized by rapid population growths that ultimately will lead to an expanding consumer base target and an expansion of future demand for Pernod Ricard. Asia/Rest of the World is therefore a leading region as far as population growth indicators are concerned, with India and Africa being at the forefront. Each year the population of drinking age in India increases by 15 to 20 million people. In Africa, on the other hand, according to United Nations estimates, the change in population from 2015 to 2050 will be 112%, which is strongly exceeding growth indicators in any other region.

Competitive positioning:

The wine and spirits market is characterized by a moderate competition (Herfindahl

index of 451), represented by large multinational groups. We have determined the four

Pernod Ricard’s main competitors in accordance with several criteria:

• Diageo plc [D]: the market leader in the wine and spirits market; Diversified brands.

• Brown-Forman [BF]: corporation manufactures; Specialized in whiskey.

• Constellation Brands [CB]: specifically focused on the American market, a wine and spirits segment.

• Rémy Cointreau [RC]: specialized in cognac; international presence.

-2,0%

0,0%

2,0%

4,0%

6,0%

8,0%

2011 2012 2013 2014 2015 2016

India USA China Eurozone

Figure 7: GDP per year (%)

Figure 8: Income class distribution in China (%)

Figure 9: Income class distribution in the US (%)

Source: OECD

Source: Bloomberg

Source: Bloomberg

4432

25

30

30

28

20

2933

5 9 13

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2017 2021

Poor Mass middle class

Upper middle class Affluent

23.7 21.8 20.7

38 37.6 36.9

25 25.8 26.4

13.3 14.9 16

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2017 2021

Poor Middle class Upper middle class Affluent

Figure 10: estimated change in population (2015 – 2050)

19%

112%

-3%

23%

-20%

0%

20%

40%

60%

80%

100%

120%

Asia & Oceania

Africa Europe Americas

Source: The United Nations, Department of Economics and Social Affairs: The 2017 revision

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

5 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

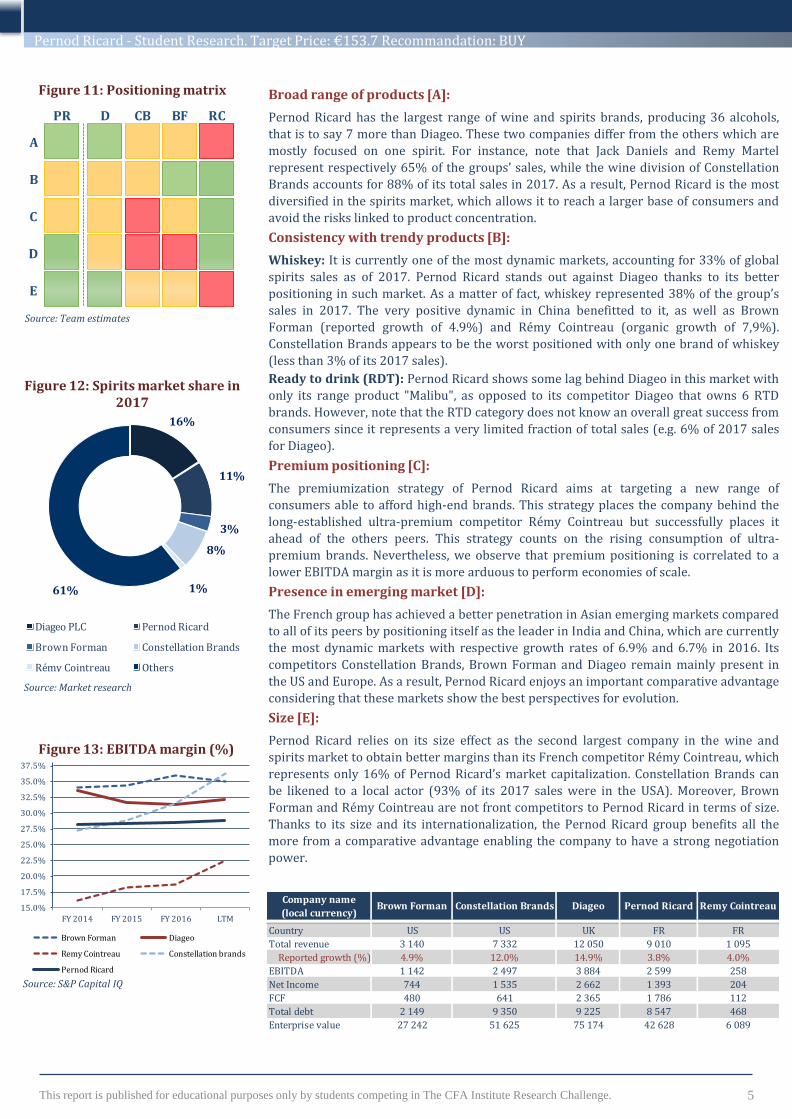

Figure 11: Positioning matrix

Figure 12: Spirits market share in 2017

Broad range of products [A]:

Pernod Ricard has the largest range of wine and spirits brands, producing 36 alcohols,

that is to say 7 more than Diageo. These two companies differ from the others which are

mostly focused on one spirit. For instance, note that Jack Daniels and Remy Martel

represent respectively 65% of the groups’ sales, while the wine division of Constellation

Brands accounts for 88% of its total sales in 2017. As a result, Pernod Ricard is the most

diversified in the spirits market, which allows it to reach a larger base of consumers and

avoid the risks linked to product concentration.

Consistency with trendy products [B]:

Whiskey: It is currently one of the most dynamic markets, accounting for 33% of global

spirits sales as of 2017. Pernod Ricard stands out against Diageo thanks to its better

positioning in such market. As a matter of fact, whiskey represented 38% of the group’s

sales in 2017. The very positive dynamic in China benefitted to it, as well as Brown

Forman (reported growth of 4.9%) and Rémy Cointreau (organic growth of 7,9%).

Constellation Brands appears to be the worst positioned with only one brand of whiskey

(less than 3% of its 2017 sales).

Ready to drink (RDT): Pernod Ricard shows some lag behind Diageo in this market with

only its range product "Malibu", as opposed to its competitor Diageo that owns 6 RTD

brands. However, note that the RTD category does not know an overall great success from

consumers since it represents a very limited fraction of total sales (e.g. 6% of 2017 sales

for Diageo).

Premium positioning [C]:

The premiumization strategy of Pernod Ricard aims at targeting a new range of

consumers able to afford high-end brands. This strategy places the company behind the

long-established ultra-premium competitor Rémy Cointreau but successfully places it

ahead of the others peers. This strategy counts on the rising consumption of ultra-

premium brands. Nevertheless, we observe that premium positioning is correlated to a

lower EBITDA margin as it is more arduous to perform economies of scale.

Presence in emerging market [D]:

The French group has achieved a better penetration in Asian emerging markets compared

to all of its peers by positioning itself as the leader in India and China, which are currently

the most dynamic markets with respective growth rates of 6.9% and 6.7% in 2016. Its

competitors Constellation Brands, Brown Forman and Diageo remain mainly present in

the US and Europe. As a result, Pernod Ricard enjoys an important comparative advantage

considering that these markets show the best perspectives for evolution.

Size [E]:

Pernod Ricard relies on its size effect as the second largest company in the wine and

spirits market to obtain better margins than its French competitor Rémy Cointreau, which

represents only 16% of Pernod Ricard’s market capitalization. Constellation Brands can

be likened to a local actor (93% of its 2017 sales were in the USA). Moreover, Brown

Forman and Rémy Cointreau are not front competitors to Pernod Ricard in terms of size.

Thanks to its size and its internationalization, the Pernod Ricard group benefits all the

more from a comparative advantage enabling the company to have a strong negotiation

power.

D CB BFPR RC

A

B

C

D

E

Source: Team estimates

16%

11%

3%

8%

1%61%

Diageo PLC Pernod Ricard

Brown Forman Constellation Brands

Rémy Cointreau Others

Source: Market research

Figure 13: EBITDA margin (%)

Source: S&P Capital IQ

15.0%

17.5%

20.0%

22.5%

25.0%

27.5%

30.0%

32.5%

35.0%

37.5%

FY 2014 FY 2015 FY 2016 LTM

Brown Forman Diageo

Remy Cointreau Constellation brands

Pernod Ricard

Company name

(local currency)Brown Forman Constellation Brands Diageo Pernod Ricard Remy Cointreau

Country US US UK FR FR

Total revenue 3 140 7 332 12 050 9 010 1 095

Reported growth (%) 4.9% 12.0% 14.9% 3.8% 4.0%

EBITDA 1 142 2 497 3 884 2 599 258

Net Income 744 1 535 2 662 1 393 204

FCF 480 641 2 365 1 786 112

Total debt 2 149 9 350 9 225 8 547 468

Enterprise value 27 242 51 625 75 174 42 628 6 089

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

6 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

We issue a BUY recommendation on Pernod Ricard with a target price of €153.7 and a

potential upside of 17%. Our valuation is computed by using a combination of the

Discounted Cash-Flow model and relative multiple analysis. Our recommendation is

underpinned by the following key drivers:

Drivers of the investment case

Growing market in Asia (China/India): strong growth has made a come-back in the

region, with China gaining momentum in FY 2016/17 (+2% vs. -9% last year), as well

as overall in Asia in Q1 2017/18 (+7% in Asia/ROW). The Asian market accounts for

30% of group total revenues, China and India being the two most important division

markets. Strong growth in these markets will necessary support Pernod Ricard’s sales,

due to its premium positioning that will allow it to catch the emergence of a middle-

class and the increasing per capita consumption.

Strong upward perspective in the whiskey market: we expect Pernod Ricard to benefit

from the very positive dynamic of whiskey production, according to IWSR reports that

predict volumes should increase by 52.6m 9-litre cases over the next five years,

especially in India and China, where the group is the market leader, and in the US. Note

that Indian local whiskey is the most consumed alcoholic beverage in the country, fully

in line with the Pernod Ricard portfolio which includes three major ones. In addition,

we observe that the whiskey exposure of Pernod Ricard has substantially grown, from

35.2% in FY 2015 to 38.3% for FY 2017 and we expect such exposure to be at 40% at

the end of this year. Volume sales skyrocketed in FY 2017 by +15% for Jameson, +3%

for Ballantine’s and that the group is increasing its advertising costs in China for

Chivas Regal. As a result, we do think Pernod Ricard will remain able to outperform

the industry over the coming years.

Strategic acquisitions in Ultra-premium brands and innovation: we observe that

Pernod Ricard is slowly shifting its strategy upmarket by acquiring ultra-premium

local brands (42$ - 84$ for a 75cl bottle) with great potential, such as Del Maguey

(Mezcal, which is expected to grow at +17.8% CAGR 2017-2022 – Future Market

Insights), Smooth Ambler (Bourbon) and Ungava (Gin). Group’s growth is also driven

by Innovations brands, which accounted for 1/3 of the top line growth last year. These

strategies aim at targeting the rise of the upper-class in the US, whose income trends

an upward evolution allowing them to afford ultra-premium spirits. Such a strategic

positioning is corroborated by data on consumption evolution like the CAGR 2006-

2016, which stands at 9% for ultra-premium brands, as opposed to 3.4% for premium

brands.

Limits of the investment case

Low organic growth in Western Europe: Pernod Ricard is impacted by the slight

positive environment in Western Europe, with an average organic growth of 1.6% the

last three years in Europe, which includes the positive dynamic in Eastern Europe. For

instance, the group only achieved a 1% growth in France last year. The Western

Europe market is mature and pricing remains challenging in the region. Hereby, the

group will necessary have to increase its advertising and promotion expenses to

remain the market leader in Europe.

The vodka market is shrinking: Absolut is the most important brand of Pernod

Ricard , accounting for 23.1% of its international brands sales. Still, the brand is facing

difficulties as the vodka market shrank by 4.3% last year. The US is the Absolut’s most

important market, which is challenging (+0.4% LTM), partly due to the negative

pricing effect on the brand and changing consumer preferences.

3 Investment summary

Figure 14: Global spirits consumption (2017)

Figure 15: Price range in 2017 (growth %)

43%

33%

8%

7%

9%

White alcohols Whiskey Liqueur

Cognac Others

Source: Company data

Source: Company data

Figure 16: Whiskey vs. other SIB (growth %)

Source: Company data

PrestigeUltra-

premium

Super-

premiumPremium Standard

> $84 $42-84 $26-$42 $17-$26 $10-$17

4 Financial Analysis

We forecast total revenue of €9,196m in the course of 2018, with organic sales growth of 4.2% driven by the awakening of growth market in Asia and its strong market position. Furthermore, margins and earnings should continue in the years ahead thanks to costs containments efforts and a better control of non-recurring items.

5.3%

-1.3%

3.8% 4.3%3.5%

5.1%

2.6%

-1.3% -1.3%

1.0%

-6.8%

4.5%1.90%

2012 2013 2014 2015 2016 2017Whiskey sales

Other Strategic brands sales

7.40%

9%

6.80%

3.40%

1.20%

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

7

Analysis overview

Regarding many of Pernod Ricard’s operational and financial characteristics, we believe the group has the financial ability to both foster value creation in its existing operations and continue to grow through an acquisition strategy. The group benefits from a more than adequate liquidity and cash flows for future investments. The company should be able to reduce its leverage, and the capital structure is solid enough to support future strategic plans.

Performance measurement

We used the DuPont analysis to separate the components affecting the return on common equity, as it leads to assess the drivers of Pernod Ricard’s performance. Our projections highlight a progressive improvement in the ROE over the next three years through enhancements in the company’s profitability (driven by organic and external growth). The significance of the investment in associates is limited (associates’ contribution to ROE is weak).

Capital structure analysis

The Company has sought to secure its capital structure over the last three years. As of September 2017, Pernod’s total debt amounted to €8,547 million, representing 38.1% of the capital structure, as opposed to 42% in 2015, while the proportion of equity financing increased. Furthermore, we notice that the liquidity ratios improved more than modestly, providing a cushion to the cash generation that has been decreasing.

Cash flow relationships

Since Pernod Ricard has made a number of acquisitions, we analyzed the relationship between operating cash flow and its resource allocation over time. Cash flows cover reinvestment needs by a factor of 3.9x, and the trend should improve in the next years. The cash flow relationship with debt and interest indicates that the group should be able to handle more debt should profitable investment opportunities arise.

Figure 17: ROE vs. ROCE forecasts

Source: Company data, Team estimates

Figure 18: Evolution of EPS

Source: Company data, Team estimates

Figure 19: Net debt forecasts

Source: Company data, Team estimates

6.5%

9.1%

10.0% 10.0% 10.1%

8.8% 8.8%

9.2% 9.2%

9.6%

5.5%

6.5%

7.5%

8.5%

9.5%

10.5%

2015 2016 2017 2018e 2019e

ROE ROCE

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

2015 2016 2017 2018e 2019e 2020e

Ne

t D

eb

t/E

BIT

DA

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Current Ratio 1.44 1.47 1.77 1.77 1.78 1.81

Quick Ratio 0.37 0.38 0.49 0.50 0.50 0.52

Defensive Interval Ratio 111.21 108.20 115.91 117.00 115.90 120.67

Days sales outstanding (DSO) 58.69 55.66 57.44 57.00 57.00 57.00

Days on hand of inventory (DOH) 598.75 583.60 568.34 560.00 560.00 560.00

Number of days payables 189.77 186.08 195.62 184.00 184.00 184.00

Cash conversion cycle 467.66 453.18 430.16 433.00 433.00 433.00

Working Capital Accounts and RatiosHistorical Projected

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Tax Burden 78.2% 74.3% 74.9% 76.0% 76.1% 76.3%

Interest Burden 49.6% 73.5% 78.1% 79.8% 80.9% 83.7%

EBIT Margin 25.9% 26.1% 26.4% 26.3% 26.8% 27.4%

Net Profit Margin 10.1% 14.2% 15.5% 15.9% 16.5% 17.5%

Total asset turnover 29.5% 28.5% 29.7% 30.4% 31.1% 31.6%

Leverage 2.31 2.28 2.22 2.12 2.03 1.95

Return on equity (ROE) 6.9% 9.2% 10.2% 10.3% 10.4% 10.8%

Expanded Dupont AnalysisHistorical Projected

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

4.68

5.27 5.545.95

6.55

0%

2%

4%

6%

8%

10%

12%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2015 2016 2017 2018e 2019e

EP

S gr

ow

th (

%)

EP

S

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Revenue Growth 7.7% 1.4% 3.8% 2.1% 3.6% 3.6%

EBITDA Margin 28.4% 28.6% 28.8% 28.8% 29.3% 29.9%

EBIT Margin 25.9% 26.1% 26.4% 26.3% 26.8% 27.4%

ROCE 8.8% 8.8% 9.2% 9.2% 9.2% 9.6%

ROE 6.5% 9.1% 10.0% 10.0% 10.1% 10.5%

ROA 3.0% 4.0% 4.6% 4.8% 5.1% 5.5%

Net Debt / Equity 94.3% 93.9% 92.1% 91.0% 90.5% 88.5%

EPS 3.26 4.68 5.27 5.54 5.95 6.55

DPS 1.80 1.88 2.02 2.05 2.20 2.42

Historical ProjectedKey Metrics

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

8 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

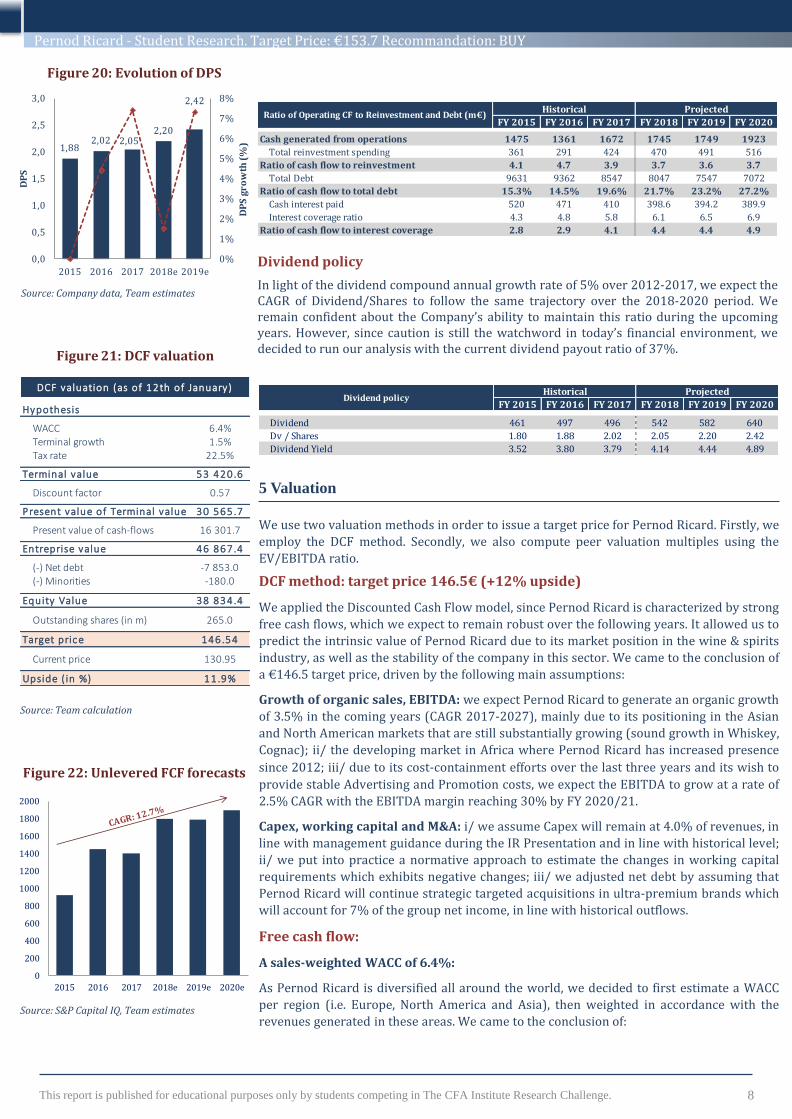

Dividend policy

In light of the dividend compound annual growth rate of 5% over 2012-2017, we expect the CAGR of Dividend/Shares to follow the same trajectory over the 2018-2020 period. We remain confident about the Company’s ability to maintain this ratio during the upcoming years. However, since caution is still the watchword in today’s financial environment, we decided to run our analysis with the current dividend payout ratio of 37%.

Figure 20: Evolution of DPS

1,882,02 2,05

2,20

2,42

0%

1%

2%

3%

4%

5%

6%

7%

8%

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2015 2016 2017 2018e 2019e

DP

S g

ro

wth

(%

)

DP

S

Source: Company data, Team estimates

We use two valuation methods in order to issue a target price for Pernod Ricard. Firstly, we

employ the DCF method. Secondly, we also compute peer valuation multiples using the

EV/EBITDA ratio.

DCF method: target price 146.5€ (+12% upside)

We applied the Discounted Cash Flow model, since Pernod Ricard is characterized by strong

free cash flows, which we expect to remain robust over the following years. It allowed us to

predict the intrinsic value of Pernod Ricard due to its market position in the wine & spirits

industry, as well as the stability of the company in this sector. We came to the conclusion of

a €146.5 target price, driven by the following main assumptions:

Growth of organic sales, EBITDA: we expect Pernod Ricard to generate an organic growth

of 3.5% in the coming years (CAGR 2017-2027), mainly due to its positioning in the Asian

and North American markets that are still substantially growing (sound growth in Whiskey,

Cognac); ii/ the developing market in Africa where Pernod Ricard has increased presence

since 2012; iii/ due to its cost-containment efforts over the last three years and its wish to

provide stable Advertising and Promotion costs, we expect the EBITDA to grow at a rate of

2.5% CAGR with the EBITDA margin reaching 30% by FY 2020/21.

Capex, working capital and M&A: i/ we assume Capex will remain at 4.0% of revenues, in

line with management guidance during the IR Presentation and in line with historical level;

ii/ we put into practice a normative approach to estimate the changes in working capital

requirements which exhibits negative changes; iii/ we adjusted net debt by assuming that

Pernod Ricard will continue strategic targeted acquisitions in ultra-premium brands which

will account for 7% of the group net income, in line with historical outflows.

Free cash flow:

A sales-weighted WACC of 6.4%:

As Pernod Ricard is diversified all around the world, we decided to first estimate a WACC

per region (i.e. Europe, North America and Asia), then weighted in accordance with the

revenues generated in these areas. We came to the conclusion of:

5 Valuation

Figure 21: DCF valuation

Source: Team calculation

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2015 2016 2017 2018e 2019e 2020e

Source: S&P Capital IQ, Team estimates

Figure 22: Unlevered FCF forecasts

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020Ratio of Operating CF to Reinvestment and Debt

Cash generated from operations 1475 1361 1672 1745 1749 1923

Total reinvestment spending 361 291 424 470 491 516

Ratio of cash flow to reinvestment 4.1 4.7 3.9 3.7 3.6 3.7

Total Debt 9631 9362 8547 8047 7547 7072

Ratio of cash flow to total debt 15.3% 14.5% 19.6% 21.7% 23.2% 27.2%

Cash interest paid 520 471 410 398.6 394.2 389.9

Interest coverage ratio 4.3 4.8 5.8 6.1 6.5 6.9

Ratio of cash flow to interest coverage 2.8 2.9 4.1 4.4 4.4 4.9

Ratio of Operating CF to Reinvestment and Debt (m€)Historical Projected

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020Dividend policy

Dividend 461 497 496 542 582 640

Dv / Shares 1.80 1.88 2.02 2.05 2.20 2.42

Dividend Yield 3.52 3.80 3.79 4.14 4.44 4.89

Dividend policyHistorical Projected

Hypothesis

WACC 6.4%Terminal growth 1.5%Tax rate 22.5%

Terminal value 53 420.6

Discount factor 0.57

Present value of Terminal value 30 565.7

Present value of cash-flows 16 301.7

Entreprise value 46 867.4

(-) Net debt -7 853.0(-) Minorities -180.0

Equity Value 38 834.4

Outstanding shares (in m) 265.0

Target pric e 146.54

Current price 130.95

Upside ( in %) 11.9%

DCF valuation (as of 12th of January)

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

9 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Figure 23: Sensitivity analysis

Figure 24: Monte-Carlo simulation

Beta: a weighted average beta of 0.8. We used a one-year regression between the firm’s

stock return and a European market index, which is the most consistent market index.

Damodaran public data have been used to determine betas in Asia/RoW and Americas.

Risk free rate: for Europe, we decided to adopt the Euro area yield curves delivered by the

ECB, that indicate a 10 years risk free rate of 1.10%. North American risk free rate has been

implemented by using the 10 years US Bill (2.5%) and we decided to equally weigh the 10

years free rate of China and India for RoW, which gave a rate of 5.5%.

Expected return: expected return has been computed by using: i/ the S&P 500 Beverages

10-year average return of 9.5% in North America; ii/ the CAC 40 5-year average return of

8.2% in Europe; iii/ the STOXX Asia/Pacific 600 Food & Beverage 3-year average return of

11% in Asia/RoW.

Cost of debt: we relied on the average cost of debt expected by Pernod Ricard (3.8%) for

this year and decided to apply it to all areas.

Source: Team calculation

Sensitivity analysis:

We took care to check that our result was not too sensitive to the growth rate at perpetuity and the WACC. We came to the conclusion that our DCF model was more sensitive to the WACC than the terminal growth for a 0.25% change. This result is consistent because mature companies are logically less sensitive to the terminal growth.

Monte Carlo Simulation:

We implemented a Monte Carlo simulation to see if our result is realistic with our DCF

valuation. We started a draw of 50,000 iterations to assure the relevancy of the results. The

Monte Carlo simulation supports our result, affirming there is more than a 50% probability

that the company achieve more than a 12% upside.

Relative valuation methods: Target price €160.9 (+22.9% upside)

We decided to focus on all listed sector companies that could be compared to Pernod

Ricard. But we didn’t equally weigh the companies because of strong differences with

Pernod Ricard portfolio, their geographical positioning and their size. Indeed, all these

characteristics have an impact on the EV/EBITDA multiple and led us to determine a

synthetic multiple.

We use an EV/EBITDA multiple, driven by the assumptions that EBITDA is less sensitive

than EBIT to accounting manipulations regarding the D&A, and that EBITDA is the most

reliable metric to compare companies’ operating income. The set of comparables chosen

drive us to an average synthetic EV/EBITDA of 19.5x that we applied to Pernod Ricard

without taking into account any drop in value that the group has been experiencing since

2014. We obtain an implied share price of €160.9 and a 22.9% upside.

Source: Team calculation

Diageo UK 65 449 75 174 17,7x 100%

Brown Forman US 25 250 27 242 20,3x 60%

Constellation Brands US 42 414 51 625 17,6x 50%

Remy Cointreau France 5 659 6 089 23,9x 50%

Davide Campari Italia 7 324 8 261 20,0x 40%

Average / Weighted average 19,9x 19,5x

EV / EBITDA

2017 LTM

Likeness to

Pernod Ricard

weighting

Company Country

Market cap.

local currency

(in m)

Enterprise value

local currency

(in m)

Source: Team calculation

Source: S&P Capital IQ, Team estimates

Figure 25: EV/EBITDA valuation

28,0%

28,5%

29,0%

29,5%

30,0%

30,5%

31,0%

1 000

1 500

2 000

2 500

3 000

3 500

EB

ITD

A M

argi

n (

%)

Figure 26: EBITDA forecasts

1.00% 1.25% 1.50% 1.75% 2.00%

5.90% 152.2 159.0 166.5 174.9 184.4

6.15% 143.4 149.4 156.0 163.4 171.6

6.40% 135.3 140.7 146.5 153.0 160.3

6.65% 128.0 132.8 138.0 143.8 150.2

6.90% 121.4 125.6 130.3 135.4 141.1

Sensivity analysis

Growth in perpetuity

WA

CC

Areas% of

total sales

E /

(E+D)

D /

(E+D)β Rf

Cost of

equity

Cost of

debt

Corporate

tax rate

Regional

WACC

Asia / ROW 39.6% 62.6% 37.4% 0.80 5.5% 9.9% 3.8% 22.0% 7.3%

Europe 30.9% 62.6% 37.4% 0.54 1.2% 5.0% 3.8% 23.0% 4.2%

Americas 29.5% 62.6% 37.4% 1.12 2.6% 10.3% 3.8% 22.5% 7.6%

Total 100.0% - - 0 .81 3.3% 8.5% 3.8% 22.9% 6.4%

WACC estimation break-down

Metrics 2599.0

Multiple applied 19.5x

Enterprise Value 50 755

(-) Net Debt -7853

(-) Minorities -180

(=) Equity Value 42 722

Average shares out. (m) 265

Implied share price (€) 160.93

Current Share price 130.95

Upside (in %) 22.9%

EBITDA 2017/18e

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

10

6 Management and Corporate Governance

Management Team:

The General Management of the group is carried out by Alexandre Ricard, CEO and

Chairman of the Group since the 29th of August 2012, following the passing of Patrick

Ricard, and Gilles Bogaert, Managing Director, Financial & Operations. Both have been

working for Pernod Ricard for a cumulative total of 37 years.

Executive Board:

The Executive Board prepares and approves all decisions related to the functioning of

Pernod Ricard and submits these decisions to the Board of Directors.

Board of directors:

The Pernod Ricard Board of Directors is composed of 14 members, whom half are

independent members and 42% are female directors, while the attendance rate is at 97%.

The governance consists of the following committees: the strategic committee directed by

Alexandre Ricard; the audit committee directed by Wolfgang Colberg; the nominations,

governance and CSR committee directed by Nicole Bouton; the compensation committee

also directed by Nicole Bouton. Each of these committees is at least composed of 50%

independent members and 100% attendance is required.

Shareholder rights:

We decided to split the shareholding structure into six blocks. The “Société Paul Ricard”

(family holding co) remains the main investor in the company with a total of 16%,

increasing by 7% in two years its holding in the group. The free-float is currently

accounting for around 46% of the company shares while it accounted for 41.5% two years

ago. Voting rights did not change very much in the recent years. “The Société Paul Ricard”

has a total of 22.4% of voting rights while the free-float is at 41.8%. Thus, the company is

becoming more sensitive to changes in financial markets while remaining stable over the

time, allowing to perfectly employ its strategy as decided by the board of directors.

Social responsibility:

The group has renownedly built a strong social responsibility in the past years. According

to an inquiry launched by independent survey company Towers Watson, 85% of its

employees declare that they are encouraged to act responsibly. The group committed in

2010 to following a roadmap to 2020 under which Pernod Ricard aims to reduce by 30% its

CO2 emissions by 2020. The group almost fulfilled this goal as it has already reduced its

carbon emissions by 27%.

Results: Target price €153.7 (+17.4% upside)

We equally weighted the DCF and relative valuation methods. The DCF method allowed us

to analyze the group’s capacity to create value through its brands portfolio shift and

geographic positioning. The relative valuation method helped us understand that Pernod

Ricard currently suffers from an undervaluation compared to its peers that should

disappear thanks to the significant EBITDA increase we predict in the coming years. As a

result, we set a BUY recommendation with a target price of €153.7 (+17.4% upside).

Figure 27: Final valuation

Figure 28: Shareholding structure (2017)

Valuation

conclusionDCF

Relative

multiple

Weighting (in %) 50% 50%

Target price 146,5 160,9

Weighted targ. price

Current share price

Upside

Equity value (in m€)

(+) Minorities (in m€)

(+) Net debt (in m€)

Entreprise value

7 853

48 773

153,7

131,0

17,4%

40 740

180

Societe Paul

Ricard + board16%

Floating46%

Groupe Bruxelles Lambert

7%

CGC10%

MFS IM10%

Inst. Inv.11%

Source: Registration document

Source: Team calculation

Societe Paul

Ricard + board16%

Floating42%

Groupe Bruxelles Lambert

11%

CGC9%

MFS IM7%

Inst. Inv.11%

Figure 29: Voting rights (2017)

Source: Registration document

7 Investment risks

Operational risks:

Digital (OR1): the group is trying to surf on the digital trend with, for example, the through

the « lesnouveauxcavistes.com » e-commerce website initiative. However, group is timid

compared to competitors like Diageo, that have partnerships with Amazon Prime to make

cocktails tutorials or Deliveroo that can home deliver Diageo’s alcohols at all times of the

day.

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

11 This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

How to mitigate: Develop partnerships, especially in China where e-commerce is booming.

Online sales only represent 8% of the group’s turnover.

Severe competition and absence from essential markets (OR2): entry barriers in the

beverage market are high but there is already unrelenting competition between the

international and local actors. Consumers can easily substitute brands, which forces the

group to anticipate the consumer’s future needs to remain among market leaders. For

example, Pernod Ricard is not present in the beer nor RTD segments, which are thriving

and may favor the penetration in emerging markets.

How to mitigate: acquire a local beer or baijiu brand in China, India or Africa but we do

think this is not consistent with the group’s premiumization strategy. Continue expanding

in the wine industry is also an option, more likely.

Raw material pricing (OR3): the group is threatened by several external matters

regarding the fluctuation of raw material prices, such as wheat, potatoes (used is the

production of Vodka), corn or rye (used in the production of whiskey), etc. Climate change

and pricing pressure could negatively impact the COGS so that the margin would

significantly affect EBITDA margin.

How to mitigate: by hedging (short term) or partnering with suppliers if necessary (long

term). If raw materials were to increase, the group would not be able to increase prices in

developed countries where pricing remains challenging due to suppliers control. However,

to compensate for the decreasing margin, it should increase prices in emerging countries

(supposed to generate organic growth).

Financial Risks

Exchange rate risk (FR1): as the group has an important international activity (70% of the

TO is not European) and produces 72% of its alcohols in Europe, it is strongly exposed to

exchange rates fluctuations (both transaction and conversion risk). For instance, a 5%

appreciation of the Euro vs. the Dollar would have a negative impact of ca. €130m on

turnover. A 5% appreciation of the Euro VS the Yuan would have a less negative, which

remains nonetheless significant (- €55m).

How to mitigate: the group hedges with currency swaps but not consequently enough

compared to the risk. Plus, as we mentioned, the group cannot easily increase the prices.

Indebtedness and interest rate (FR2): Pernod Ricard remains consequently indebted

even if it is quickly deleveraging. As indebted companies are more sensitive to interest rate

changes, the group is dependent to the changes in the interest rate when rolling its debt or

re-leveraging. In terms of target price, it increases the WACC and reduces the enterprise

value.

How to mitigate: increase the cash or improve the management of debt issuances to

decrease the net debt and increase debt average duration. Short term, group could also

hedge with an interest rate swap for the variable part of its leverage.

Context and External Risks

Decreasing global alcoholic consumption (ER1): the alcoholic global consumption is

declining at a faster rate this past years (e.g. -1.3% in 2016). This slowdown is mainly due

to the decreasing consumption in China, Russia and Brazil caused by economic or political

issues. Awareness campaigns also tend to lower the consumption in Western Europe.

How to mitigate: Pernod Ricard should concentrate in the economic and social

environments where consumption is booming and margins are more favorable.

Government or tax policy risk (ER2): a change in the government policy or a new law

against alcohol consumption would affect the group’s growth. For example, the “Highway

Ban” in India dragged the group growth in country to 1% vs. 12% in 2015/16. Another

example is the anti-extravaganza campaign in China.

How to mitigate: focus on neighbor’s countries and travel retail.

Figure 30: Risks matrix

Source: Team estimates

-15%

-10%

-5%

0%

5%

10%

15%

20%

2013 2014 2015 2016 2017 2018e2019e2020e

FX change External growth Organic growth

Figure 31: Growth breakdown (%)

Source: Company data, Team estimates

ER2

ER1 OR2

OR1

OR3

FR2

FR1

Impact

Pro

bab

ilit

y

Impact on net

sales (in €m)+1% +2% +3% +4% +5% +6%

EUR/USD -26.6 -53.2 -79.8 -106.4 -133.1 -159.7

EUR/CNY -11.3 -22.6 -33.9 -45.3 -56.6 -67.9

EUR/GBP -4.5 -8.6 -13.4 -17.9 -22.3 -26.8

Figure 32: Appreciation of € vs. other currencies (€m)

Source: Team estimates

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

APPENDIX

12

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

1993Creation of Havana Club International’s

joint-venture

2005Acquisition of Allied Domecq to become n°2

worldwide

2012Asia becomes the n°1 region for the

group

2008Acquisition of

Vin&Sprit

(Absolut)

2011Launch of the

Responsib’ALL day (for societal

responsability

2014Majority interest in

ultra-premium tequila « Avión »

1975Merger of

Pernod&Ricard

2001Acquisition of

the W&S division of Seagream

1988Acquisition

of Irish Distillers

1989Acquisition of

Orlando Wyndham

2015Alexandre Ricard

appointed CEO

2017Acquisition of

Del Maguey Single Village, n°1

Mezcal in the US

2016Majoritary interests in:

Premium Gin Monkey 47 and Smooth Ambler

2013The group fastens its position in

Africa

Source: Company data

Source: Company data

Appendix 1 Business description - History

Appendix 2 Brand positioning

For a 75cl bottle Standard ($10 - $17) Premium ($26 - $42) Super-premium ($26 - $42) Ultra-premium ($42 - 84) Prestige (> $84)

Absolut

Polish Wyborowa

100 pipers Jameson Chivas Chivas Chivas

Blenders Pride Ballantine's The Glenlivet The Glenlivet Royal Salute

Royal Stag JP Wiser"s Imperial

Imperial Blue Passport Scotch

Clan Campbell

Cognac Martell Martell Martell

Anisee Pastis 51 Ricard

Gin Seagram's Gin Beefeater

Rum Havana Club Havana Club

Ready-to-drink Malibu

Perrier-Jouet Perrier-Jouet

Mumm

Tequila Olmeca Mum

Kahlua Armenia

Amarro Ramazzotti Ararat

Strategic International Brands

Strategic Local Brands

Perrier-Jouet

Whiskey

Vodka

Champagne

Other spirits

Mumm

19.75% 19.66%20.24%

19.34% 18.98%

18.83%

18.30%

27.29% 27.59% 27.57%28.57% 28.98%

30.57% 30.56%

18.1% 18.6% 18.7% 18.5%19.0%

20.0% 20.6%

2011 2012 2013 2014 2015 2016 2017

Dis

trib

uti

on

of P

ern

od

Ric

ard

in

win

e a

nd

sp

irit

s (

%)

Vodka Whiskey Wine

Source: Annual reports

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge. 13

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

14

Main

markets

Market

type

Sales

growth

FY17

Main brands GDP

growth

rate

Population

growth

rate

Market

obstacles

General comments

USA Mature 5%

Jameson,

Malibu,

Martell,

Glenlivet,

Olmeca Altos,

Avion

1,8% 0,69%

Largest market both in Americas and globally

Continued strong performance of whiskey, tequila and cognac categories

Value growth mainly driven by mix and operational excellence initiatives

Growth drivers: a) Rising spending power of population, b) Spirits is the fastest growing alcohol beverage segment in U.S. and it continues to take share from other alcohol beverage categories.

France Mature 1%

Jameson,

Absolut,

Chivas,

Ballantine’s,

Ricard,

Havana Club,

Mumm,

Perrier-Jouet

0,8% 0,41%

Technical impact

of back-office

mutualisation

between Ricard

and Pernod on 1

July 2015

Pernod Ricard maintains its leadership position in France with 30% market share (Nielson).

UK Mature 7%

Absolut,

Jameson, The

Glenlivet,

Mumm,Chiva

s, Perrier-

Jouet,

Plymouth

Gin, Campo

Viejo

1,02% 0,78% -

Dynamic growth for strategic international brands as well as strategic wine portfolio

Concentration on prestige part of the market, particularly in London as the number of high-worth individuals is growing.

Germany Mature 4%

Lillet, Chivas,

Absolut,

Jameson,

Ballantine’s,

Malibu,

Monkey 47,

Havana Club,

Ramazzoti,

Aperitivo

Rosato

0,7% 1,19% -

Market leadership position of the Group

Increased focus on prestige categories as Germany is one of the markets with the largest number of high-net worth individuals

Key drivers of the growth are prestige portfolio (+19%) and innovation (+12%).

Growth of imported brands for international categories; decline of local brands for brandies, schnapps and Colon categories.

Success in the aperitif segment

Spain Mature 5%

Seagram’s

Gin and

Beefeater,

Chivas,

Ballantine’s,

The Glenlivet,

Campo Viejo

3,2% -0,008% -

Market leadership with 24% market share

Pernod Ricard is #1 in gin category with the most complete portfolio: Beefeater Dry, Seagram’s Gin, Beefeater 24, Plymouth Gin, Burrough’s Reserve,

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Appendix 3 Market analysis (1/2)

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

15

Appendix 3 Market analysis (2/2)

Poland Emerging 10%

Chivas,

Ballantine’s,

Jameson,

Absolut,

Wyborowa,

Ostoya, Pan

tadeusz.

2,8% -0,1% -

Quickly growing market in Eastern Europe

Price-sensitive consumer base, very competitive commercial environment

Russia Emerging 16%

Ararat,

Jameson,

Ballantine’s,

Chivas,

Absolut

-0,4% 0,18%

Difficult

environment

linked to

currency

volatility

Very dynamic and promising market

Penetration of imported Western style spirits is still low – 4-5%

China Emerging 2%

Martell,

Absolut,

Glenlivet,

Ballantine’s

6,7% 0,54%

Anti-

extravaganza

campaign, which

has seen a

crackdown on

conspicuous

spending and

gifting

Return to growth for the first time from FY13

From 2000 to 2010 the growth was driven by the Absolut Chinese consumer and Prestige portfolio. Due to emerging middle class, today Pernod Ricard in China has 2 different routes to market: premium and prestige

India Emerging 1%

Blender’s

Pride, Royal

Stag, Imperial

Blue

6,9% 1,15%

Demonetisation

(impact on Q1

and Q2);

Highway ban

(Impact on Q4

and Q1 FY18);

GST (margin

pressure on

FY18)

Market leadership with 45% value market share

Temporary deceleration of growth in FY17 due to regulatory changes

Leadership position in premium, local and international whiskey

South

Africa Emerging 15,7%

Jameson,

Martell,

Chivas,

Ballantine’s,

Absolut

-1,3% 1,62%

Economic

difficulties

across the

continent

related to petrol

and commodity

prices

#1 market in Africa At the group level, the region

is small, but it continues to grow double digits year by year.

Growth drivers: a) fast growing consumer base; b) emerging middle class; c) fast urbanization.

Source: Company data, S&P Capital IQ, team analysis

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

22%

23%

23%

24%

24%

25%

25%

26%

6

7

8

9

10

11

12

2012 2013 2014 2015 2016 2017

Shar

e o

f to

tal

net

sal

es

In m

illi

on

of

9 li

ters

bo

x so

ld

Absolute

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

1

2

3

4

5

6

7

2012 2013 2014 2015 2016 2017

Shar

e o

f to

tal n

et s

ales

In m

illi

on

of

9 li

ters

bo

x so

ld

Jameson

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

8.8%

9.0%

0

1

2

3

4

5

2012 2013 2014 2015 2016 2017

Shar

e of

tot

al n

et s

ales

In m

illi

on o

f 9

lite

rs b

ox s

old

Havana Club

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2012 2013 2014 2015 2016 2017

Shar

e o

f to

tal n

et s

ales

In m

illi

on

of

9 li

ters

bo

x so

ld

Malibu

3.7%

3.8%

3.9%

4.0%

4.1%

4.2%

4.3%

4.4%

4.5%

4.6%

1.8

1.9

1.9

2.0

2.0

2.1

2.1

2.2

2012 2013 2014 2015 2016 2017

Shar

e of

tot

al n

et s

ales

In m

illi

on o

f 9

lite

rs b

ox s

old

Martell

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2012 2013 2014 2015 2016 2017

Shar

e o

f to

tal n

et s

ales

In m

illi

on

of

9 li

ters

bo

x so

ld

The Glenlivet

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

2012 2013 2014 2015 2016 2017

Shar

e of

tot

al n

et s

ales

In m

illi

on o

f 9

lite

rs b

ox s

old

Perrier-Jouet

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

201220132014201520162017

Shar

e o

f to

tal

net

sale

s

In m

illi

on

of

9 li

ters

bo

x so

ld

Ballantine's

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

201220132014201520162017

Shar

e of

tot

al n

et s

ales

In m

illi

on o

f 9

lite

rs b

ox s

old

Ricard

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Appendix 4 Evolution of Strategic International Brands

Source: Annual reports Source: Annual reports Source: Annual reports

Source: Annual reports Source: Annual reports Source: Annual reports

Source: Annual reports Source: Annual reports Source: Annual reports

16

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

0

1

2

3

4

5Total Strenghts

Total Weakenesses

Total Opportunities

Total Threats

Appendix 5 SWOT analysis

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Source: Team analysis

17

S W

O T

• Leading brands in each main category ofalcohol• Improving financials thanks to high-margin

brands• Suitable acquisitions at sensible multiples• Sales diversified by region and type ofalcohol• « Brand Builder »: the group is strongly

invested in the development of its newacquisitions

• Commitment to an environmental andsocially responsible chart• Strong advertising and branding of its

portfolio• « Drink less but drink better » trend

• Major international player inmature markets and in high-growth potential markets

• Robust distribution network andnegociation power due to its size

• Not present in the beer segment• Lack of presence in the market in the RTD(Malibu)

• Low digital presence despite efforts• Rising free-float, increasing the risk of

loosing control• Still important indebtedness -> sensitive toincreasing interest rates

• Negative price/mix effect (0% on the 4 firstbrands)

• Vodka and Aniseed are not trendy anymore• No customer loyalty

• North american market is growing durablyand steadily• GDP, Medium class and population growthin the emergeant regions (China, India,Africa, Eastern Europe)

• Premiumization policy: weak priceelasticity on the demand on top-of-the-rangeproducts• Increasing of the aerian international traficand so of the travel retail sales• Growth of the market for RTD and punchs• Low presence in digital that can only beimproved (latest to arrive = weakest)• Penetration in emergent markets is notsaturated yet

• Slowing growth rate of the industry due toa slightly decreasing global consumption• Counterfeiting of alcoholic beverages in

China• Competition, especially in india

• Stiffening regulations and taxation on theliqueur industry that can play on theconsumption and the margins

• Consumer health concerns andsensibilisation campaingns mostly in

Western countries lead to a maturization ofthe european liqueur market• Being perceived as sin stocks and non-ISRinvestments• Increasing price of raw materials

• Production centralized ineurope (transaction andconversion risks)

• International group dependent oneconomical and political fluctuation(FX risk)

• Strong lobby (alcoholic beverages)

•Diminishing custom taxes in India

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

Appendix 6 Porter’s five forces analysis

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge. 18

0 No threat

1 Insignificant threat

2 Low threat

3 Moderate

4 Significant threat

5 High threat

Legend

1 4

2

3

4

Threat of new entrants

Bargaining power of buyers

Bargaining power of suppliers

Industry rivalry

Threat of substitute products

Rivalry among competitors: Moderate

• The competitors are mostly specialized in a region, brands or price range.

• Margins in the sector are high, meaning that the competition is not severe (Herfindahl Hirschman index of 451).

• Nevertheless, there is a direct competition from leading groups on the wine and whiskey segments.

Threat of new entrants: Low

• The industry is composed by a significant share of local actors and a few main actors, holding most of the market

share.

• Highly profitable markets tend to attract new actors. However, the strong barriers at the entry make it roughly

likely.

• Note that local actors are continuously growing in emerging countries on specific products (Indian whiskey).

Bargaining power of buyers: Significant

• Buyers are the final consumer, restaurants/ bars/nightclubs or distributors.

• They are sensitive to price changes and reputation. Therefore, they might easily redirect themselves to

competition.

• However, as Pernod Ricard is focused on high income per capita consumers and offers premium products, the

power of buyers is not that significant.

Bargaining power of suppliers: Low

• The company produces all its alcohols. Hereby, it is sensitive to raw materials prices (corn, wheat, potatoes)

• To mitigate that risk, the company buys in high quantity and from several suppliers to generate economies of scale

Threat of substitute products: Significant

• Substitutes are an non negligible threat. Water can go from indirect substitution to direct substitution (Other

brands, RTD, supplier’s brands, local alcohols, other types of alcohols like beer…)

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

19

Appendix 7 PESTEL analysis

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

PPolitics

EEconomy

SSocio-

cultural

• Influence of the politics on the alcohol distribution and taxation policies (Highway ban, Anti-extravaganza campaign) • Actions from public Authorities to sensibilize to alcohol’s dangers (Sensibilization campaigns)• Political instability in countries where PR is implemented (Africa, Asia, South-America…)

• Inflationary environments can affect the mix-price of the group• Unexpected and strong appreciation of € vs. $ (Production in euro and sales mainly in dollars)• Increasing interest rates (US 10Y and tensions in european bonds) • General context of economic recovery worldwide • Increasing GDP and income per capita in emerging countries -> benefiting premium products • Increasing wine demand worldwide for the second consecutive year

• Trend to consume less but better, especially in spirits: « Drink less and drink better »• Youth’s alcoholic consumption increasing• Growing « home consumption », to savour the moment and less consumption in bars, especially among young people

(PR’s target)• Productssubstitution: shifting from vodka to wines, whiskeys and tequila• Booming population in emergings countries and especially youth -> increasing possible consumer base

TTechnology

EEnvironment

LLegal

• Innovation and new lauch of products are essentials in the industry to retain and attract the consumer, leading to significant R&D investments. Example: Fast-growing RTDs

• Rise of e-commerce, especially in China• Manufacturing techniques, reducing costs

• Increasing environmental responsability in Western countries• Obligation to comply with environmental laws and contraints (could increase costs)• Consumers tend to buy ethical brands and companies

• Publi-promotional restrictions (Evin Law for example)• Sales restrictions for under-age people• Quality control of wines in some countries. • Restrictions in terms of origins designation blocking actors of the liqueur industry to expend as they wish (Irish

wiskeys, champagne…)• Alcohol and alcohol production is banned from certain regions of the world (some indian regions for example)

Source: Team analysis

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

Profitability Analysis

Company FY 2014 FY 2015 FY 2016 LTM FY 2014 FY 2015 FY 2016 LTM

Brown Forman 34.1% 34.4% 35.9% 35.0% 22.0% 21.8% 34.5% 23.0%

Diageo 33.6% 31.7% 31.5% 32.2% 21.9% 22.0% 21.4% 22.1%

Remy Cointreau 16.2% 18.1% 18.8% 22.5% 6.0% 9.6% 9.7% 17.4%

Constellation brands 27.3% 28.8% 31.4% 36.3% 39.9% 13.9% 16.1% 23.6%

Davide Campari 21.6% 23.2% 22.8% 22.5% 8.3% 10.6% 9.6% 11.4%

Lanson-BCC 14.0% 12.6% 10.9% 10.1% 5.8% 4.6% 4.3% 4.0%

Pernod Ricard 28.2% 28.4% 28.6% 28.8% 12.8% 10.1% 14.2% 15.5%

Mean 25.0% 25.3% 25.7% 26.8% 16.7% 13.2% 15.7% 16.7%

Median 27.3% 28.4% 28.6% 28.8% 12.8% 10.6% 14.2% 17.4%

EBITDA Margin Net Income Margin

Solvency Analysis

Company 2014 2015 2016 LTM 2014 2015 2016 LTM

Brown Forman 44.30x 36.55x 22.47x 16.50x 0.47x 0.79x 1.14x 1.84x

Diageo 4.89x 4.17x 5.13x 6.82x 2.85x 3.52x 2.95x 2.09x

Remy Cointreau 5.76x 5.91x 8.34x 11.96x 2.51x 2.68x 2.32x 1.58x

Constellation brands 5.79x 5.62x 5.16x 6.66x 4.45x 4.32x 4.18x 3.20x

Davide Campari 4.92x 5.24x 5.07x 7.19x 3.01x 2.26x 3.19x 3.15x

Lanson-BCC 4.31x 4.21x 3.73x 4.00x 12.25x 14.80x 17.69x 20.46x

Pernod Ricard 4.09x 4.50x 4.89x 5.91x 3.77x 3.73x 3.54x 3.03x

Mean 10.58x 9.46x 7.83x 8.43x 4.19x 4.59x 5.00x 5.05x

Median 4.92x 5.24x 5.13x 6.82x 3.01x 3.52x 3.19x 3.03x

EBIT/Interest Exp Net Debt / EBITDA

EV multiples

Company 2014 2015 2016 LTM 2014 2015 2016 LTM

Brown Forman 17.69x 21.33x 19.89x 22.86x 6.04x 7.34x 7.14x 8.00x

Diageo 17.23x 20.64x 20.76x 18.64x 5.79x 6.54x 6.53x 6.01x

Remy Cointreau 21.40x 20.75x 20.20x 22.78x 3.48x 3.51x 3.79x 5.13x

Constellation brands 14.19x 18.40x 20.00x 18.15x 3.87x 5.30x 6.28x 6.59x

Davide Campari 14.14x 15.37x 17.77x 20.38x 3.06x 3.57x 4.06x 4.59x

Lanson-BCC 18.79x 21.23x 25.17x 29.80x 2.63x 2.68x 2.75x 3.01x

Pernod Ricard 14.58x 13.49x 14.81x 14.95x 4.11x 3.84x 4.23x 4.31x

Mean 16.86x 18.74x 19.80x 21.08x 4.14x 4.68x 4.97x 5.38x

Median 17.23x 20.64x 20.00x 20.38x 3.87x 3.84x 4.23x 5.13x

EV / EBITDA EV/Revenue

Per Share Analysis

Company 2014 2015 2016 LTM 2014 2015 2016 LTM

Brown Forman 10.34x 10.83x 12.66x 15.74x 27.08x 32.48x 19.55x 32.19x

Diageo 6.41x 5.82x 6.28x 5.99x 21.03x 24.03x 25.54x 23.13x

Remy Cointreau 3.21x 2.94x 3.17x 4.01x 52.94x 34.00x 34.35x 43.53x

Constellation brands 3.06x 4.04x 4.60x 5.23x 6.85x 29.83x 31.33x 23.92x

Davide Campari 2.38x 2.88x 3.02x 3.89x 29.45x 29.00x 35.43x 35.94x

Lanson-BCC 1.02x 0.85x 0.80x 0.90x 14.27x 17.73x 18.98x 23.76x

Pernod Ricard 2.07x 1.80x 2.08x 2.25x 23.88x 27.62x 22.60x 22.22x

Mean 4.07x 4.16x 4.66x 5.43x 25.07x 27.81x 26.83x 29.24x

Median 3.06x 2.94x 3.17x 4.01x 23.88x 29.00x 25.54x 23.92x

P/BV P/E (Diluted)

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

Appendix 8 Comparable companies analysis

20

Source: S&P Capital IQ

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

Appendix 9 Share price performance

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

70

80

90

100

110

120

130

140

150

jan

v.-

15

fév

r.-1

5

mar

s-1

5

avr.

-15

mai

-15

juin

-15

juil

.-1

5

aoû

t-1

5

sep

t.-1

5

oct

.-1

5

no

v.-

15

déc

.-1

5

jan

v.-

16

fév

r.-1

6

mar

s-1

6

avr.

-16

mai

-16

juin

-16

juil

.-1

6

aoû

t-1

6

sep

t.-1

6

oct

.-1

6

no

v.-

16

déc

.-1

6

jan

v.-

17

fév

r.-1

7

mar

s-1

7

avr.

-17

mai

-17

juin

-17

juil

.-1

7

aoû

t-1

7

sep

t.-1

7

oct

.-1

7

no

v.-

17

déc

.-1

7

Vo

ulm

e in

k t

ran

sact

ion

s (P

ern

od

Ric

ard

)

R²: 0.87

CAC 40

Pernod Ricard

Appendix 10 Performance positioning (Pernod Ricard vs. peers)

-8%

-3%

2%

7%

12%

17%

22%

10% 15% 20% 25% 30% 35% 40%

Re

po

rte

d g

row

th i

n 2

01

6/

17

(%)

Operating margin in 2016/17 (%)

Diageo

Rémy Cointreau

Pernod Ricard Constellation Brands

Brown Forman

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge. 21

Source: S&P Capital IQ, Bloomberg

Source: S&P Capital IQ,

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

Appendix 11 Key financials

Appendix 12 M-Score

This report is published for educational purposes only by students competing in The CFA Institute Research Challenge.

𝑀 − 𝑠𝑐𝑜𝑟𝑒 = −4.84 + 0.92 × 𝐷𝑆𝑅𝐼 + 0.528 × 𝐺𝑀𝐼 + 0.404 × 𝐴𝑄𝐼 + 0.892 × 𝑆𝐺𝐼 + 0.115 × 𝐷𝐸𝑃𝐼 − 0.172 × 𝑆𝐺𝐴𝐼 + 4.679 × 𝑇𝐴𝑇𝐴 − (0.327 ∗ 𝐿𝑉𝐺𝐼)

Inputs Variables 2013 2014 2015 2016 2017

Net Sales 8 575 7 945 8 558 8 682 9 010

Costs of Goods Sold 3 224 2 958 3 262 3 311 3 407

Net Receivables 1 257 1 147 1 307 1 258 1 347

Current Assets 6 507 6 648 7 420 7 288 7 531

Property Plant and Equiptment 1 940 2 012 2 194 2 360 2 298

Depreciation 185 203 214 219 219

Total Assets 27 537 27 616 30 398 30 598 30 088

Selling general and Administrative Expenses 3 146 2 948 3 077 3 109 3 223

Net Income 1 172 1 016 861 1 235 1 393

Cash Flow from Operations 1 085 940 1 035 1 336 1 642

Current Liabilities 4 418 3 905 5 138 4 956 4 256

Long-term Debt 7 712 7 674 7 458 7 335 7 380

Derivated Variables

Day's Sales Receivables Index (DSRI) 0.98 1.06 0.95 1.03

Gross Margin Index (GMI) 0.99 1.01 1.00 0.99

Asset Quality Index (AQI) 1.02 0.94 1.02 1.02

Sales Growth Index (SGI) 0.93 1.08 1.01 1.04

Depreciation Index (DEPI) 0.95 1.03 1.05 0.98

SG&A expenses Index (SGAI) 1.01 0.97 1.00 1.00

Leverage Index (LVGI) 0.95 0.99 0.97 0.96

Total Accuals to total assets (TATA) 0.00 -0.01 0.00 -0.01

M-score -2.5326 -2.3864 -2.5074 -2.4416

Result: We observe that the company is unlikely to manipulate its earnings as its M-score is always < -2.22

Source: S&P Capital IQ, Team estimates

Source: S&P Capital IQ, Team estimates

22

Key financial ratio 2015 2016 2017 2018e 2019e 2020e

Liquidity Ratio

Current Ratio 1.44x 1.47x 1.77x 1.77x 1.80x 1.83x

Quick Ratio 0.37x 0.38x 0.49x 0.42x 0.46x 0.48x

Cash Ratio 0.11x 0.11x 0.16x 0.07x 0.12x 0.13x

Efficiency Ratio

Total Asset Turnover 0.30x 0.28x 0.30x 0.30x 0.31x 0.32x

Fixed Asset Turnover 4.07x 3.81x 3.87x 3.80x 3.58x 3.37x

Acc Receivable Turnover 6.63x 6.43x 6.57x 6.33x 6.41x 6.52x

Inventory Turnover 1.68x 1.63x 1.70x 1.68x 1.68x 1.70x

Payables Period (days) 190 186 196 180 180 180

Operating Cycle (days) 273 281 270 275 275 271

Cash conversion Cycle (days) 468 453 430 469 457 457

Profitability Ratio

Gross Profit Margin 61.9% 61.9% 62.2% 62.0% 62.2% 62.5%

EBITDA Margin 28.4% 28.6% 28.8% 28.8% 29.3% 29.9%

EBIT Margin 25.9% 26.1% 26.4% 26.3% 26.8% 27.4%

Net Income Margin 10.1% 14.2% 15.5% 15.9% 16.5% 17.5%

ROA 3.0% 4.0% 4.6% 4.8% 5.1% 5.5%

ROE 6.5% 9.1% 10.0% 10.0% 10.1% 10.5%

ROCE 8.8% 8.8% 9.2% 9.2% 9.2% 9.6%

SG&A/Sale 36.0% 35.8% 35.8% 35.7% 35.4% 35.1%

Solvency Ratio

Debt Ratio 56% 56% 54% 52% 50% 48%

Debt to Equity Ratio 1.29x 1.27x 1.17x 1.07x 0.99x 0.91x

Equity Multiplier 2.29x 2.27x 2.17x 2.07x 1.99x 1.91x

Long Term Debt Ratio 94.8% 94.7% 94.7% 94.3% 94.0% 93.5%

Interest Coverage Ratio 4.50x 4.89x 5.91x 6.06x 6.48x 6.95x

Pernod Ricard - Student Research. Target Price: €153.7 Recommandation: BUY

2015 2016 2017 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e

Total Revenue 8 558 8 682 9 010 9 196 9 530 9 873 10 202 10 518 10 834 11 159 11 494 11 838 12 194

COGS 3 262 3 311 3 407 3 494 3 602 3 703 3 775 3 839 3 954 4 073 4 195 4 321 4 451