CENTURY 21 ACCOUNTING © Thomson/South-Western LESSON 9-2 Prepaid Expenses.

8

CENTURY 21 ACCOUNTING © Thomson/South-Western LESSON 9-2 LESSON 9-2 Prepaid Expenses

-

Upload

oswin-obrien -

Category

Documents

-

view

219 -

download

1

Transcript of CENTURY 21 ACCOUNTING © Thomson/South-Western LESSON 9-2 Prepaid Expenses.

CENTURY 21 ACCOUNTING © Thomson/South-Western

LESSON 9-2LESSON 9-2

Prepaid Expenses

CENTURY 21 ACCOUNTING © Thomson/South-Western

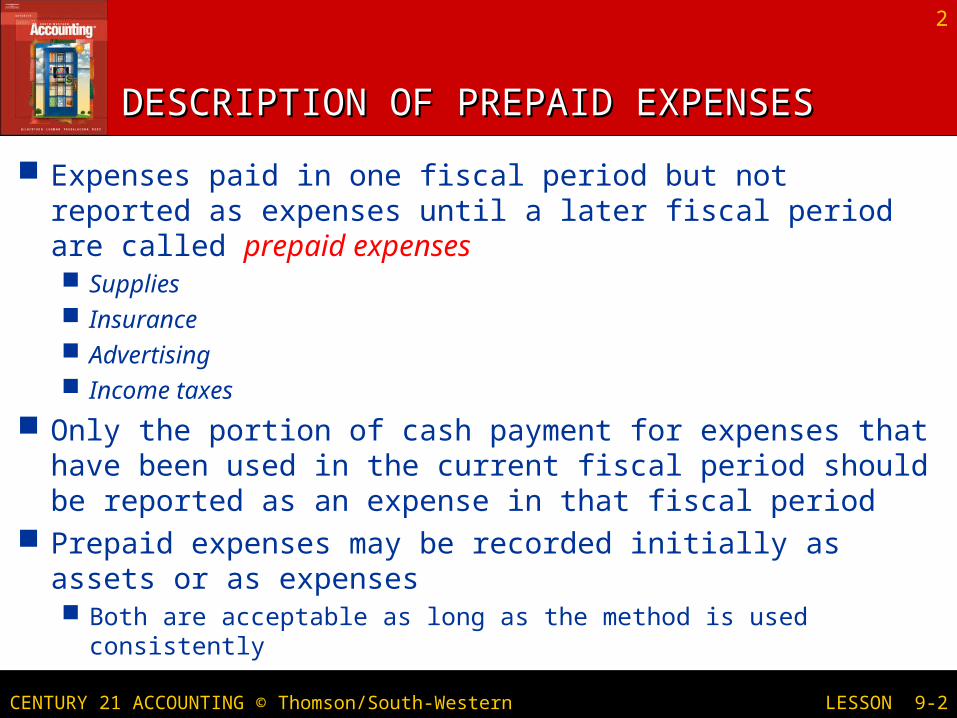

DESCRIPTION OF PREPAID EXPENSESDESCRIPTION OF PREPAID EXPENSES

Expenses paid in one fiscal period but not reported as expenses until a later fiscal period are called prepaid expenses Supplies Insurance Advertising Income taxes

Only the portion of cash payment for expenses that have been used in the current fiscal period should be reported as an expense in that fiscal period

Prepaid expenses may be recorded initially as assets or as expenses Both are acceptable as long as the method is used consistently

2

LESSON 9-2

CENTURY 21 ACCOUNTING © Thomson/South-Western

3

LESSON 9-2

1. Debit the expense account.

2. Credit the asset account.

SUPPLIES INITIALLY SUPPLIES INITIALLY RECORDED AS AN ASSETRECORDED AS AN ASSET page 267

11

22

When a company buys office supplies, the asset Supplies is debited & Cash is credited.

Adjusting entries are recorded so that the supplies used during a fiscal period are reported as expenses & the supplies not used are reported as assets

CENTURY 21 ACCOUNTING © Thomson/South-Western

4

LESSON 9-2

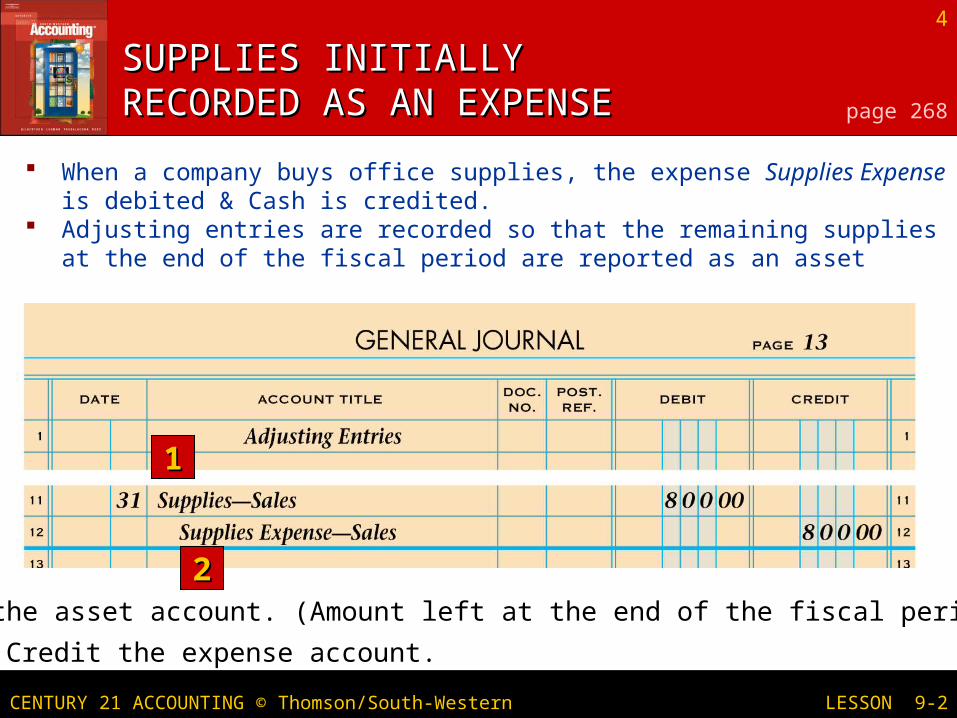

1. Debit the asset account. (Amount left at the end of the fiscal period.)

2. Credit the expense account.

SUPPLIES INITIALLY SUPPLIES INITIALLY RECORDED AS AN EXPENSERECORDED AS AN EXPENSE page 268

11

22

When a company buys office supplies, the expense Supplies Expense is debited & Cash is credited.

Adjusting entries are recorded so that the remaining supplies at the end of the fiscal period are reported as an asset

CENTURY 21 ACCOUNTING © Thomson/South-Western

5

LESSON 9-2

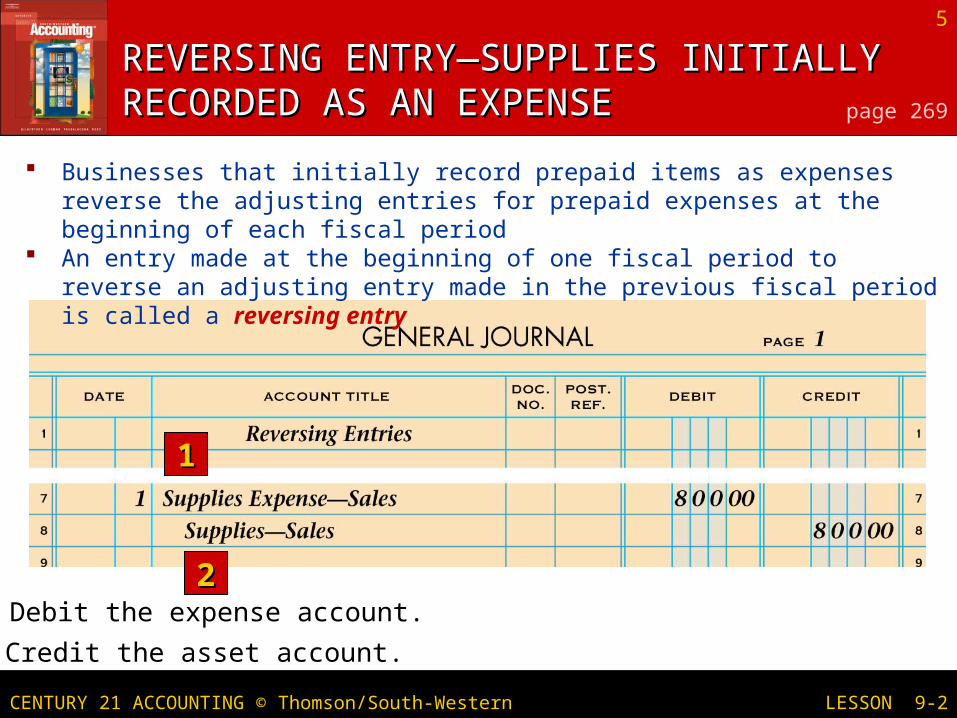

1. Debit the expense account.

2. Credit the asset account.

REVERSING ENTRY—SUPPLIES INITIALLY REVERSING ENTRY—SUPPLIES INITIALLY RECORDED AS AN EXPENSERECORDED AS AN EXPENSE page 269

11

22

Businesses that initially record prepaid items as expenses reverse the adjusting entries for prepaid expenses at the beginning of each fiscal period

An entry made at the beginning of one fiscal period to reverse an adjusting entry made in the previous fiscal period is called a reversing entry

CENTURY 21 ACCOUNTING © Thomson/South-Western

6

LESSON 9-2

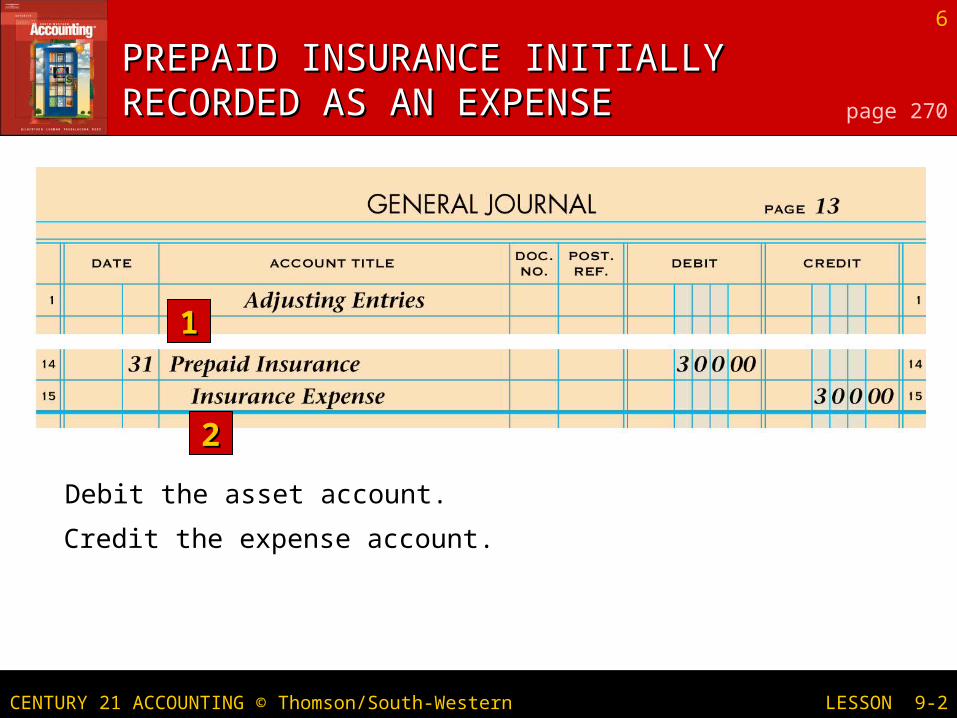

1. Debit the asset account.

2. Credit the expense account.

PREPAID INSURANCE INITIALLY PREPAID INSURANCE INITIALLY RECORDED AS AN EXPENSERECORDED AS AN EXPENSE page 270

11

22

CENTURY 21 ACCOUNTING © Thomson/South-Western

7

LESSON 9-2

1. Debit the expense account.

2. Credit the asset account.

REVERSING ENTRY FOR REVERSING ENTRY FOR PREPAID INSURANCEPREPAID INSURANCE page 270

11

22

CENTURY 21 ACCOUNTING © Thomson/South-Western

8

LESSON 9-2

TERMS REVIEWTERMS REVIEW

prepaid expenses reversing entry

page 271

![Farm expenses.pptx [Read-Only] - Iowa State University · 9/8/2015 3 Prepaid Farm Supplies • §464 limits the allowable deduction for pre‐paid expenses • If the prepaid farm](https://static.fdocuments.net/doc/165x107/5ae7f6357f8b9a6d4f8ed3ed/farm-read-only-iowa-state-university-3-prepaid-farm-supplies-464-limits.jpg)