© 2010 by Cengage Learning Chapter 8 ________________ Real Estate Sales Contracts.

Upload

madison-simmonsCategory

view

213download

0

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 10-1LESSON 10-1

Journalizing Sales on Account Using a Sales Journal

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

2

LESSON 10-1

SALES TAXSALES TAX page 270

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 10-1

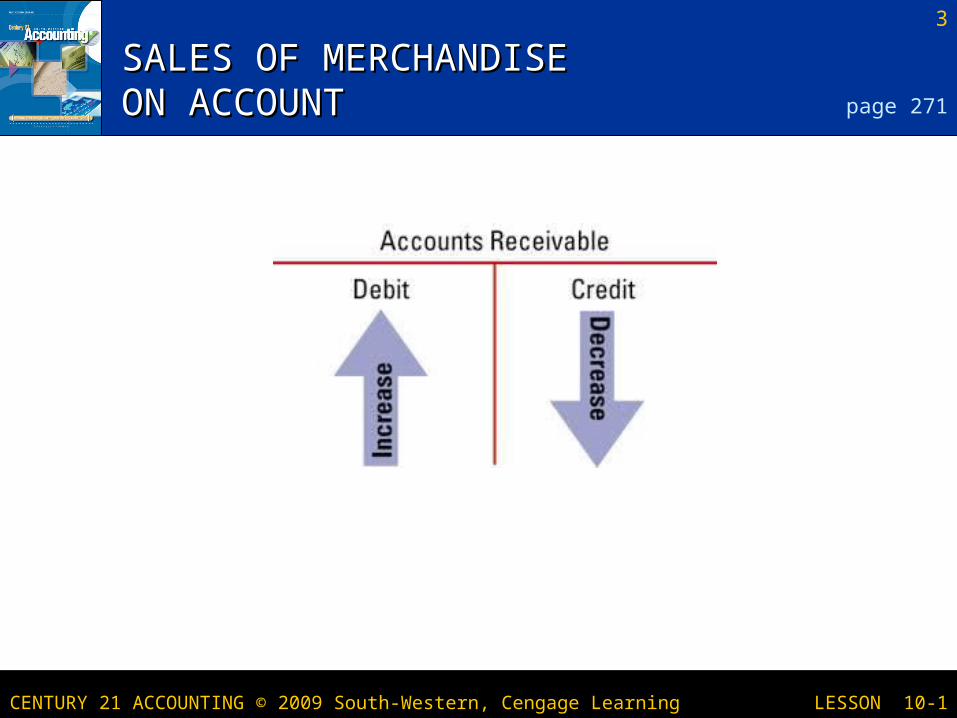

SALES OF MERCHANDISE SALES OF MERCHANDISE ON ACCOUNTON ACCOUNT page 271

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 10-1

SALES JOURNALSALES JOURNAL page 272

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

5

LESSON 10-1

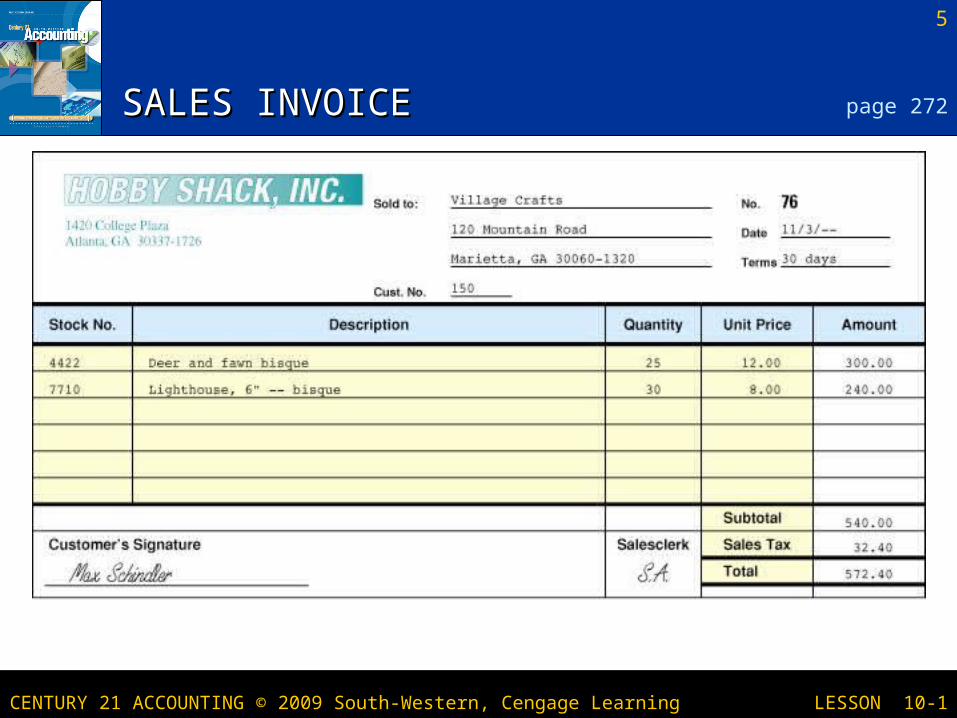

SALES INVOICESALES INVOICE page 272

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 10-1

SALE ON ACCOUNTSALE ON ACCOUNT

11 22 33 44 55 66

page 273

November 3. Sold merchandise on account to Village Crafts, $540.00, plus sales tax, $32.40; total, $572.40. Sales Invoice No. 76.

1. Write the date.

6. Write the sales tax amount.

2. Write the customer name.

3. Write the sales invoice number.

4. Write the total amount owed by the customer.

5. Write the sales amount.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 10-1

TOTALING, PROVING, AND RULING TOTALING, PROVING, AND RULING A SALES JOURNALA SALES JOURNAL page 274

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 10-1

TERMS REVIEWTERMS REVIEW

customer sales tax sales journal

page 275

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 10-2LESSON 10-2

Journalizing Cash Receipts Using a Cash Receipts Journal

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 10-2

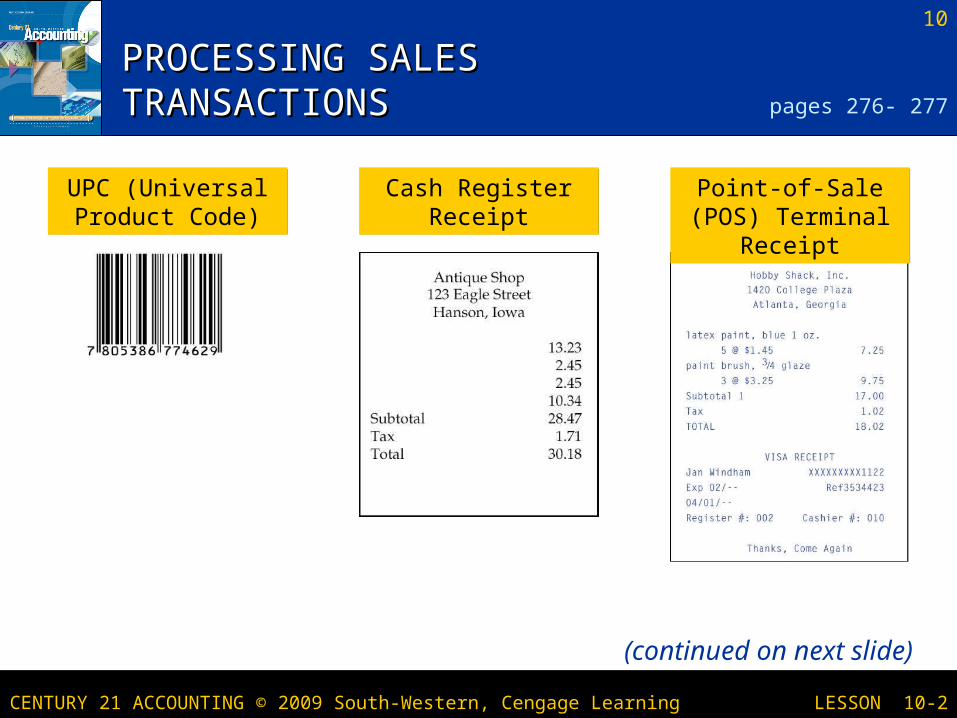

PROCESSING SALES PROCESSING SALES TRANSACTIONSTRANSACTIONS pages 276- 277

UPC (Universal Product Code)UPC (Universal Product Code)

Cash Register Receipt

Cash Register Receipt

Point-of-Sale (POS) Terminal Receipt

Point-of-Sale (POS) Terminal Receipt

(continued on next slide)

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 10-2

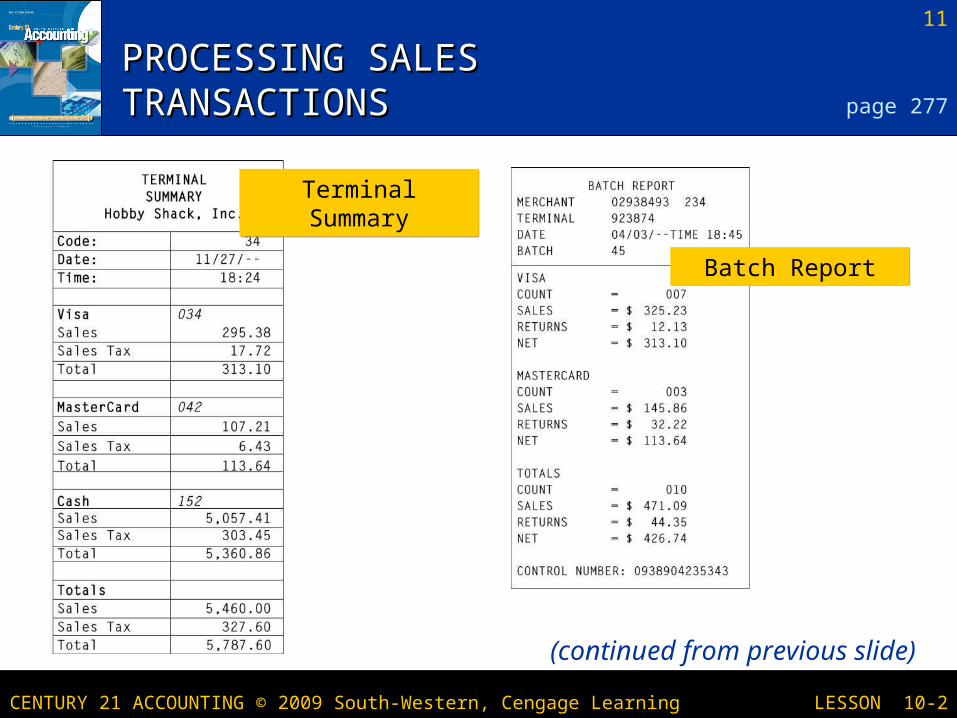

PROCESSING SALES PROCESSING SALES TRANSACTIONSTRANSACTIONS page 277

Terminal SummaryTerminal Summary

Batch ReportBatch Report

(continued from previous slide)

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 10-2

CASH RECEIPTS JOURNALCASH RECEIPTS JOURNAL page 278

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

13

LESSON 10-2

CASH AND CREDIT CARD SALESCASH AND CREDIT CARD SALES

1122

3344

55 66

page 279

November 4. Recorded cash and credit card sales, $5,460.00, plus sales tax, $327.60; total, $5,787.60. Terminal Summary 34.

1. Write the date.2. Place a check mark in the Account Title column.3. Write the terminal summary document number.4. Place a check mark in the Post. Ref. column.5. Write the sales amount.6. Write the sales tax amount.7. Write the cash amount.

77

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

14

LESSON 10-2

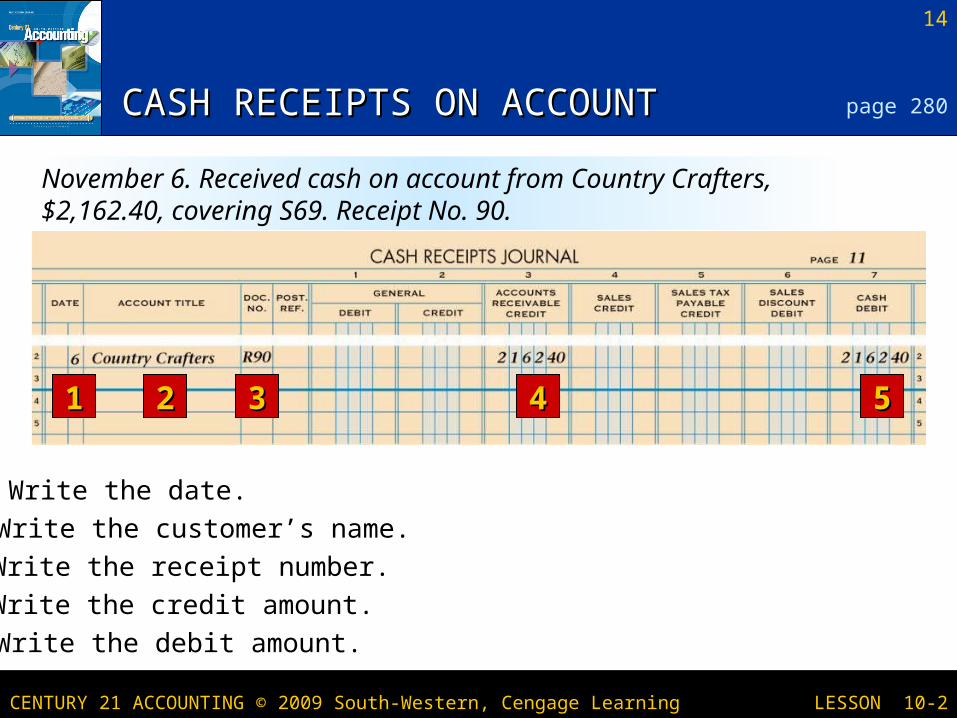

CASH RECEIPTS ON ACCOUNTCASH RECEIPTS ON ACCOUNT

11 22 33 44 55

page 280

November 6. Received cash on account from Country Crafters, $2,162.40, covering S69. Receipt No. 90.

1. Write the date.

2. Write the customer’s name.

3. Write the receipt number.

4. Write the credit amount.

5. Write the debit amount.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

15

LESSON 10-2

JOURNALIZING CASH RECEIPTS ON JOURNALIZING CASH RECEIPTS ON ACCOUNT WITH SALES DISCOUNTSACCOUNT WITH SALES DISCOUNTS

11 22 33 44 55 66

page 282

November 7. Received cash on account from Cumberland Center, $1,176.00, covering Sales Invoice No. 74 for $1,200.00, less 2% discount, $24.00. Receipt No. 91.

4. Write the original invoice amount.1. Write the date.

2. Write the customer’s name.

3. Write the receipt number.

5. Write the amount of sales discount.

6. Write the debit to cash.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

16

LESSON 10-2

TOTALING, PROVING, AND RULING A TOTALING, PROVING, AND RULING A CASH RECEIPTS JOURNALCASH RECEIPTS JOURNAL page 283

Proving Cash:

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

17

LESSON 10-2

LET’S REVIEWLET’S REVIEW

What transactions are recording in the cash receipts journal?

What is a POS system and why is it preferable to a regular cash register?

What information can be gained from the terminal summary?

What is meant by “batching out”? Explain a sales discount? Explain the accounting concept

page 284

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 10-3LESSON 10-3

Recording Transactions Using a General JournalSales Related Transactions

Sales ReturnsSales Allowances

Credit Memorandums – Source Document for a return or an allowance

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

19

LESSON 10-3

CREDIT MEMORANDUM FOR SALES CREDIT MEMORANDUM FOR SALES RETURNS AND ALLOWANCESRETURNS AND ALLOWANCES page 285

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

20

LESSON 10-3

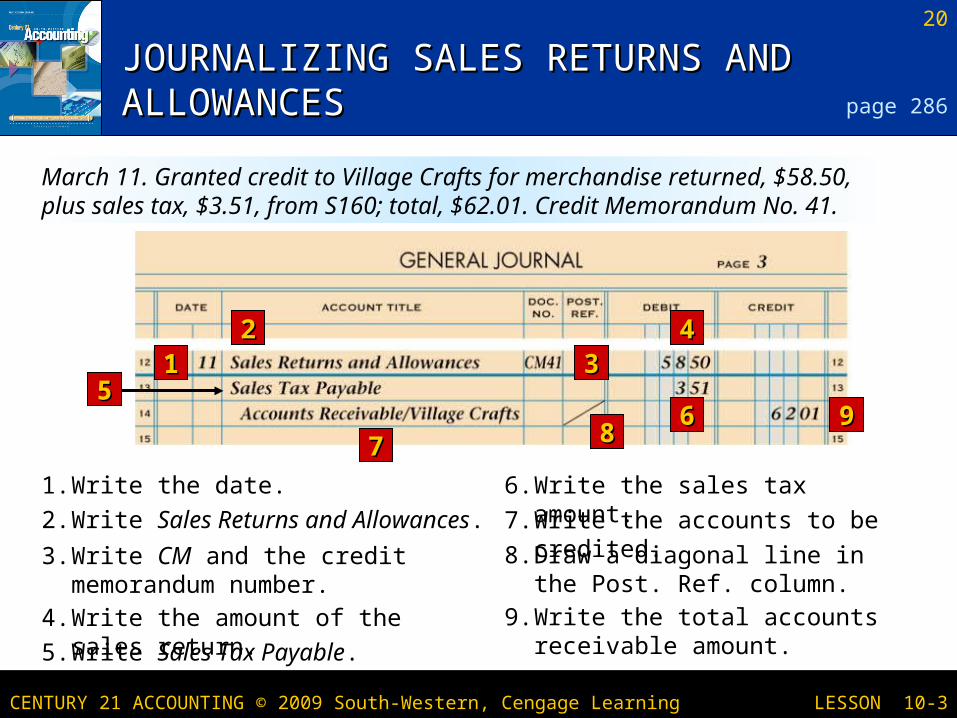

JOURNALIZING SALES RETURNS AND JOURNALIZING SALES RETURNS AND ALLOWANCESALLOWANCES

1122

3344

66

page 286

March 11. Granted credit to Village Crafts for merchandise returned, $58.50, plus sales tax, $3.51, from S160; total, $62.01. Credit Memorandum No. 41.

77 8899

55

1. Write the date. 6. Write the sales tax amount.

2. Write Sales Returns and Allowances. 7. Write the accounts to be credited.

3. Write CM and the credit memorandum number.

8. Draw a diagonal line in the Post. Ref. column.

4. Write the amount of the sales return. 9. Write the total accounts receivable amount.5. Write Sales Tax Payable.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

21

LESSON 10-3

ITEMS FOR REVIEW:ITEMS FOR REVIEW:

What is the difference between a sales return and sales allowance?

What is the source document for a sales return and allowance?

What general ledger accounts are affected, and how, by a sales returns and allowances transaction?

Why are sales returns and allowances not debited to the sales account?

page 287