Center of Regulatory Intelligence - FIS of Regulatory Intelligence ... the Consumer Financial...

17

Center of Regulatory Intelligence September 30, 2016 Regulatory Intelligence Briefing – Focus on the Department of Labor’s Fiduciary Rule and the Military Lending Act

Transcript of Center of Regulatory Intelligence - FIS of Regulatory Intelligence ... the Consumer Financial...

Center of Regulatory Intelligence September 30, 2016

Regulatory Intelligence Briefing – Focus on the Department of Labor’s Fiduciary Rule and the Military Lending Act

2

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

Table of Contents

A. Editorial Note from the Managing Director, Center of Regulatory Intelligence ....................... 3

B. Washington, D.C. Regulatory Roundup ................................................................................. 4

C. Congressional Summary – Modernizing the TCPA ................................................................ 5

D. FOCUS – DOL Fiduciary Rule ............................................................................................... 7

E. Key Themes of Military Lending Act Amendments ............................................................... 12

F. Did You Know? ..................................................................................................................... 16

G. About FIS’ Center of Regulatory Intelligence ....................................................................... 17

3

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

A. Editorial Note from the Managing Director, Center of Regulatory Intelligence

During the past several years, the Consumer Financial Protection Bureau (CFPB) has dominated the financial

services industry’s newsfeed as it relates to consumer protection regulations. Since its inception, the agency’s

supervisory and rulemaking authority was built on a basic foundation of consumer protection. However, it is wise

to remain cognizant of additional sources of consumer-driven regulatory activities.

In this edition of the Regulatory Intelligence Briefing (RIB), we review final rules from the U.S. Department of

Labor (DOL) regarding the expansion of the definition of fiduciary and U.S. Department of Defense (DOD)

regarding the Military Lending Act (MLA) rule. These final rules represent ongoing developments in the consumer

protection regulatory space that exists outside the CFPB and have gained their fair share of headlines in recent

years. As 2017 approaches, they will continue to demand attention from financial institutions of all types.

First, we start with this month’s Washington, D.C. Regulatory Roundup of news items that may be of interest to

readers. Next, we provide a summary of a recent hearing by the House Energy and Commerce Committee’s

Subcommittee on Communications and Technology on “Modernizing the Telephone Consumer Protection Act.”

The subcommittee’s discussion of this Act (TCPA) explores a possible disconnect between the language of the

TCPA and the rapidly evolving technological environment in which we live. The impact of technology on consumer

behavior suggests that certain aspects of the TCPA may be difficult for institutions to manage from an operational,

compliance and legal perspective.

In our focus article, we provide an overview of the DOL’s Fiduciary Rule (Conflict of Interest Rule) and highlight

the elements of the rule that act as a gateway to understanding how the rule may impact an institution’s

investment advice activities. With the rule’s initial compliance date almost seven months away, the new fiduciary

responsibilities found in the rule may require a large amount of preparation, training and operational support from

various stakeholders within an institution. Ultimately, this rule is intended to ensure that retirement plan investors

receive advice in their best interest. At the end of the article, we include a list of important considerations and

action items to continue the discussion offline with colleagues.

Finally, we conclude this month’s RIB with a brief review of the DOD’s MLA final rule from July 2015. With the

rule’s initial compliance date about to take place (October 3), lending institutions may already have a plan in place

for compliance. But the wait is over, so we share this article as a reminder of the more provocative requirements

of the new MLA and the expanded protections for servicemembers.

Peter D. Dugas Managing Director, Center of Regulatory Intelligence

Peter has more than 16 years of government and consulting experience in advising clients on supervisory matters before

the U.S. government and in the implementation of enterprise risk management programs. He is a thought leader in

government affairs and regulatory strategies in support of banks and financial institutions compliance with the Dodd-

Frank Act and Basel Accords. Prior to joining FIS™, he served as a director of government relations at Clark Hill and in

senior government positions, including serving as a deputy assistant secretary at the United States Department of the

Treasury.

4

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

B. Washington, D.C. Regulatory Roundup

Regulatory and Compliance Alerts

CFPB Releases August Complaints Report Spotlighting Bank Accounts and Services

On August 30, 2016, the CFPB released a monthly complaint report highlighting consumer complaints about bank

accounts and services. Common issues found in these complaints relate to the use of consumer reports to open

deposit accounts, funds availability and error resolution. Additionally, the geographic focus of the report highlights

trends seen in complaints coming from Ohio.

NCUA Issues Training on the Fundamentals of Strategic Planning

On September 8, 2016, the National Credit Union Association (NCUA) issued a four-part series of training videos

related to the strategic planning process including: effective board management, mergers and credit union

policies and procedures. The intended audience is credit union board members. An online test is also available

for completion after viewing the videos.

FFIEC Releases Revised Information Security Booklet

On September 9, 2016, the Federal Financial Institutions Examination Council (FFIEC) issued a revised

Information Security booklet, which is part of the FFIEC Information Technology Examination Handbook. The

revised booklet addresses the factors necessary to assess risk related to a financial institution’s information

systems. The booklet also helps examiners evaluate the adequacy of the information security program’s

integration into overall risk management.

CSBS Releases White Paper on Community Bank Collaboration

On September 12, 2016, the Conference of State Bank Supervisors (CSBS) released a white paper describing

the benefits of collaboration among community banks. Titled Shared Resource Arrangements: An Alternative to

Consolidation, the paper identifies a number of ways some financial institutions have successfully shared

resources to either improve compliance, increase efficiency or both.

FDIC Announces New Affordable Mortgage Lending Resources

On September 15, 2016, the Federal Deposit Insurance Corporation (FDIC) released The Affordable Lending

Guide, Part I, which organizes information about single-family mortgage products from federal agencies and

government-sponsored enterprises and provides technical assistance for community banks on affordable

mortgage credit options. Institutions can use the guide as a one-stop resource to learn about various program

resources, compare different products and understand Community Reinvestment Act implications.

Additionally, the Affordable Mortgage Lending Center provides a program matrix, program descriptions, data and

fact sheets from the FDIC and other federal resources.

HUD Issues Guidance on Fair Housing Protections for People with Limited English Proficiency

On September 15, 2016, the Department of Housing and Urban Development (HUD) issued new Limited English

Proficiency (LEP) guidance. The guidance addresses how the Fair Housing Act would apply to claims of housing

discrimination brought by people because they do not speak, read or write English proficiently.

5

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

C. Congressional Summary – Modernizing the TCPA

On September 22, 2016, the House Energy and Commerce Committee, Subcommittee on Communications and

Technology held a hearing entitled “Modernizing the Telephone Consumer Protection Act.” The hearing

considered the challenges faced by consumers and companies in a world where technology and consumer

behavior may have outpaced the language of the Telephone Consumer Protection Act of 1991 (TCPA). The law

has triggered class action lawsuits filed against companies from all sectors, including many lawsuits filed against

financial institutions. Despite recent amendments to the act from a declaratory order and ruling by the Federal

Communications Commission (FCC) in July 2015, confusion still exists regarding the law.

At its heart, the TCPA was passed as a consumer protection and privacy measure with restrictions related to

telephone solicitations and the use of automated dialing equipment. According to a congressional statement of

findings, when passing the TCPA, Congress intended to strike a balance between “individuals’ privacy rights,

public safety interests, and commercial freedoms of speech and trade” and do so “in a way that protects the

privacy of individuals and permits legitimate telemarketing practices.”

The hearing consisted of a panel comprised of the following members:

Mr. Shaun W. Mock, chief financial officer, Snapping Shoals Electric Membership Corporation

Mr. Richard D. Shockey, principal, Shockey Consulting

Ms. Michelle Turano, vice president, Government Affairs, WellCare

Mr. Spencer W. Waller, Professor; director, Institute for Consumer Antitrust Studies, Loyola University

Chicago

In his testimony, Shaun W. Mock stated a need for change to the TCPA.

The Subcommittee’s background memo highlights two major issues with the TCPA discussed at length during the

hearing:

1. The broad interpretation of the term “autodialer”

2. The increasing amount of reassigned numbers

Many TCPA lawsuits stem from provisions of the act that prohibit businesses from using autodialers, often

referred to as “robocalling,” to send mass-marketing phone calls or texts without receiving express permission

from the called parties. In a separate order issued in August 2016, the FCC amended the TCPA at the request of

the Obama administration to permit autodialed calls to wireless or residential phones without consent if the call is

made for the purpose of collecting a debt that is owed or guaranteed by the United States.

[W]e agree that consumer rights are of the utmost importance and every effort should be made to

prevent excessive and bothersome phone calls from unsolicited vendors. However, legitimate business

communication should not be hindered in the process. Some reasonable legislative changes, perhaps

even new legislation, should be considered as we learn how to manage and adapt to ever-changing

consumer communication preferences in the 21st century.

Shaun W. Mock, chief financial officer, Snapping Shoals Electric Membership Corporation.

“

“

6

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

Further, a person can be found liable if a previous caller has received expressed consent from the

intended recipient but the person has changed numbers. While the FCC rules allow a caller to make a first

call to obtain knowledge that a number has been reassigned, a caller can be liable for any calls thereafter

whether they have knowledge of the reassignment or not. The Wall Street Journal cited more than 37

million numbers are reassigned annually, making this problem more evident.

In his written testimony, Spencer Waller suggested the TCPA should be updated with particular attention paid to

improving federal and state government enforcement efforts and increasing the uniformity of interpreting the

statute. He recommended that the Federal Trade Commission (FTC) be given more enforcement responsibilities

due to the agency’s current role as an enforcement body (particularly related to the Do Not Call Rule). In

furtherance, Waller stated in his testimony, “The FTC’s continuing work towards a technical solution to robocalls is

commendable, and should be followed with respect to other types of media currently exposed to unsolicited

commercial messages such as text messages and email.”

Richard Shockey emphasized that the issues raised by the Subcommittee are not just limited to the TCPA.

Shockey stated in his testimony that the Truth in Caller-ID Act should also be revised. He points to The Improving

Rural Call Quality and Reliability Act of 2015 (H.R. 2566) and the Anti-Spoofing Act of 2015 (H.R. 2669), both

introduced in 2015 and still pending in the House, as types of legislation outside of amending the TCPA that could

improve consumer protections.

Conclusion

While Subcommittee Chairman Greg Walden (OR-R) announced this would not be the last hearing on the issue, a

lag in congressional action could lead to large fines or costly litigation for institutions. Given the constant litigation

bred from the TCPA, along with broad interpretation of terms in the Act, compliance with the TCPA is challenging

but paramount, and institutions would be wise to implement enhanced processes and controls specific to TCPA

concerns.

Passed in 2012

Compliance with the TCPA for financial institutions must be a priority. Whether using fax or email for marketing, engaging in

telemarketing, using artificial or pre-recorded voice telephone messages or using an automated dialing system, all of these

activities require specific compliance and record retention. For example, if your financial institution uses an automated

telephone dialing system:

• Is the system programmed to prevent engaging multiple lines of a business simultaneously?

• Are unanswered telemarketing calls disconnected in the appropriate manner?

• Does the autodialing system comply with the rules once it does not detect compatible terminal equipment at the other end?

• Are sequential dialers programmed correctly?

• Is the autodialing system programmed to release the line in a compliant time period once the recipient hangs up?

7

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

D. FOCUS – DOL Fiduciary Rule On April 8, 2016, the Department of Labor (DOL) and Employee Benefits Security Administration (EBSA)

released the final fiduciary rule (DOL Rule), also known as the Conflict of Interest Rule, in the Federal Register,

with an initial compliance or applicability date of April 10, 2017. The rule includes certain delayed exemption

requirements, which will make the rule fully applicable by January 1, 2018.

The final rule results in a stricter version of the Employee Retirement Income Security Act of 1974 (ERISA), which

created a single, comprehensive set of rules to follow regarding employee benefit plans. The key aspects of the

final rule include the expanded definition of the term “fiduciary” and the imposition on investment advisers –

including broker-dealers and insurance agents – to abide by a fiduciary standard that previously was not in effect.

Starting in April 2017, four noteworthy provisions will come into play with the new DOL Rule.

1. Establishment of fiduciary standard – Registered advisers who receive compensation for providing

investment advice involving any non-ERISA retirement plan or Individual Retirement Account (IRA) will be

subject to this fiduciary standard. All financial advisers will be required to recommend what is in the best

interest of their clients when they offer guidance on 401(k) plan assets, IRAs or other qualified monies

saved for retirement. If this requirement is not followed, the adviser will be subject to possible litigation

and financial penalties.

2. Best Interest Contract Exemption (BICE) – This exemption allows firms to continue with commission

and revenue sharing-based compensation practices as long as:

Firms adopt policies and procedures designed to mitigate conflicts of interest.

Firms clearly and prominently disclose any conflicts of interest, like hidden fees, that might prevent

the adviser from providing advice in the client’s best interest.

8

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

The intention of the BICE written agreement requirement is for an IRA and other non-ERISA-governed

clients to have a contractual cause of action against the adviser if the client suffers financial harm as a

result of the adviser’s conflict of interest. The DOL rule does not ban commission or revenue sharing, but

it requires advisers to have clients sign a BICE agreement. This contract ensures that the adviser will act

in the client's best interest and maintain a sensible level of compensation.

3. Principal Transaction Exemption (PTE) – This exemption allows advisers to recommend inventory

securities, fixed rate annuity contracts and insurance contracts. The nuance is that the adviser must

adhere to the exemption's proactive consumer-protection conditions and standards.

4. Pre-existing Transaction Exemption – This exemption allows advisers to receive ongoing

compensation payments in connection with a prohibited transaction that was completed before the

enactment of the proposed rule. This exemption is applicable as long as the adviser does not provide

additional advice to the plan or IRA regarding the same asset after the enactment of the proposed rule.

Definition:

Covered investment advice is a recommendation to a plan, plan fiduciary or IRA owner for a fee or other direct or indirect compensation. Covered investment advice includes recommendations on:

The management of securities or other investment property

Investment policies or strategies

Portfolio composition

Selection of other persons to provide investment advice or investment management services

Selection of investment account arrangements (e.g., brokerage versus advisory)

Recommendations with respect to rollovers, transfers or distributions from a plan or IRA, including whether, in what amount, in what form and to what destination such a rollover, transfer or distribution should be made

Exemptions:

These do not constitute fiduciary investment advice communications because they do not meet the definition of “recommendation.”

Education: Hypothetical asset allocation models or interactive investment materials intended to educate participants and beneficiaries as to what investment options are available.

General Communication: Circulation newsletters; commentary in publicly broadcast talk shows; remarks and presentations in widely attended speeches and conferences; research or news reports prepared for general distribution.

Platform Providers: Marketing or making available a platform of investment alternatives without regard to the individualized needs of the plan, its participants or beneficiaries if the plan fiduciary is independent of the service provider.

Transactions with Independent Plan Fiduciaries with Financial Expertise: True arm's length transactions between advisers and investment professionals or large asset managers who do not have a legitimate expectation that they are in a relationship where they can rely on the other adviser for impartial advice.

Swap and Security-Based Swap Transactions: Communications and activities by counterparties to swap and security-based swap transactions do not result in the counterparty being covered by this rule (conditions apply).

Employee of Plan Sponsors, Affiliates, Employee Benefit Plans, Employee Organizations or Plan Fiduciaries: Reports and recommendations routinely developed by employees in a company's payroll, accounting, human resources or finance departments for the company and other named fiduciaries of the sponsors' plans.

What is a covered investment under the

Fiduciary Rule?

What is NOT covered

investment advice:

The rule imposes certain compliance requirements on small service providers, such as broker-dealers, registered investment advisers, insurance companies and agents, pension consultants and others providing investment advice to plans or IRA investors. Additionally, understanding the exemptions is critical to preparing for and maintaining

compliance with the rule.

9

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

Investor Challenges

Investors will receive more paperwork to review and store.

Fees may rise to offset the cost of compliance and implementation.

Investors may not have as much access to traditional non-fee-based advisers.

ACCURATE DATA COLLECTION Investors may have different experiences from firm to firm.

Investors may not have as many options as products are cut due to risk or limited revenue opportunity.

Potential Challenges

The DOL Rule may present challenges for

institutions and investors alike, forcing them to

re-evaluate their business models to ensure

they are in compliance. Some institutions may

move to fee-based services, while others will

choose not to offer certain products for

retirement accounts. For example, some firms

have hinted they will stop offering clients

mutual funds and exchange-traded funds

(ETFs) for commission-based retirement

accounts. Other possible reactions to the rule

include cutting prices and account minimums

or launching a fund-only brokerage IRA

option.

As firms prepare for compliance with the rule,

additional issues are likely to appear. An

example of this includes the delay of front-end

development work until firms determine the impact BICE may have on their business. Other considerations that

are necessary when managing these new requirements include:

Will the BICE need to be reviewed and tracked if there is an exemption prior to order submission? If so,

will the institution need to make it accessible for review (including in the audit trail)?

Will the BICE require that updates be shared between the adviser and investor?

Are electronic signatures and/or forms management required?

In addition to the issues above, firms may also find value in monitoring the lawsuits filed against the DOL

pertaining to the DOL Rule. Court judgments may impact how certain aspects of the rule will be interpreted and

implemented in the future.

While customers may enjoy the

benefit of lower costs as a result of

actions taken by some firms, there

may also be fewer investment

options. The DOL rule could create a

risk-based shift in the products firms

recommend to clients. According to

statistics gathered by Bloomberg,

advisers revealed that variable

annuities may be recommended less

often, with managed accounts being

recommended more often.

10

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

Source: DOL, https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/dol-final-rule-to-

address-conflicts-of-interest

Conclusion

The new rule comes with advantages and disadvantages for impacted institutions. The main consideration these

institutions may have to evaluate is how to balance the operational and legal implications with the heightened

responsibilities at the core of the investor relationship that could have a great effect on institutions. Significant

disruptions could occur for firms with a large non-fee based business and insurance companies selling variable

annuities and other high-risk products.

From a punitive perspective, prohibiting the adviser from recommending products that put their personal

compensation concerns in front of the best investment product for a particular customer opens the door for a

greater chance of legal difficulties. On the other side of the equation the operational impact could be great.

Brokers will have to track every non-fee based account transaction and whether or not the contents of the trade

have met the BICE requirements. The required audit trail could immensely impact the data storage requirements

for institutions.

As the compliance date approaches, institutions will need to take steps to ensure full understanding and

compliance within the institution. On the next page are some additional considerations to spark conversation for

stakeholders responsible for the implementation and ongoing oversight of these requirements.

11

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

12

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

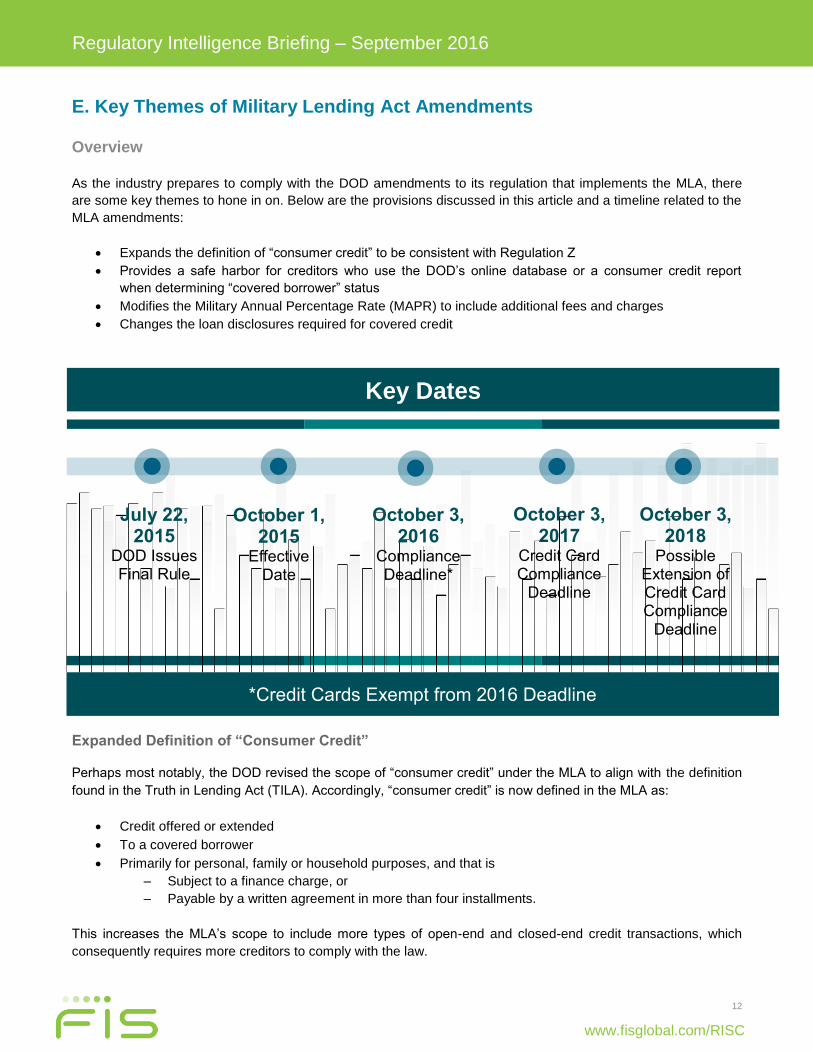

E. Key Themes of Military Lending Act Amendments

Overview

As the industry prepares to comply with the DOD amendments to its regulation that implements the MLA, there

are some key themes to hone in on. Below are the provisions discussed in this article and a timeline related to the

MLA amendments:

Expands the definition of “consumer credit” to be consistent with Regulation Z

Provides a safe harbor for creditors who use the DOD’s online database or a consumer credit report

when determining “covered borrower” status

Modifies the Military Annual Percentage Rate (MAPR) to include additional fees and charges

Changes the loan disclosures required for covered credit

Expanded Definition of “Consumer Credit”

Perhaps most notably, the DOD revised the scope of “consumer credit” under the MLA to align with the definition

found in the Truth in Lending Act (TILA). Accordingly, “consumer credit” is now defined in the MLA as:

Credit offered or extended

To a covered borrower

Primarily for personal, family or household purposes, and that is

– Subject to a finance charge, or

– Payable by a written agreement in more than four installments.

This increases the MLA’s scope to include more types of open-end and closed-end credit transactions, which

consequently requires more creditors to comply with the law.

October 3, 2017

Credit Card Compliance

Deadline

REDUCE

*Credit Cards Exempt from 2016 Deadline

October 1, 2015

Effective Date

October 3, 2016

Compliance Deadline*

July 22, 2015

DOD Issues Final Rule

October 3, 2018

Possible Extension of Credit Card Compliance

Deadline

Key Dates

13

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

Overview of Coverage

Existing Coverage New Coverage**

Certain types of closed-end: Credit cards

Payday loans Lines of credit

Vehicle title loans Student loans

Tax refund anticipation loans Installment loans

Single pay loans

**Not a comprehensive list

It will be important for a financial institution offering covered

types of credit to ensure that it incorporates

MLA compliance into its compliance management system

and operations.

“Covered Borrower” and Safe Harbor

While the amendments do not change who is a covered

borrower under the MLA, they do change how a creditor can

obtain a safe harbor for compliance when establishing

whether a borrower is covered.

A “covered borrower” is defined in the Final Rule as:

A member of the armed forces who is:

– Serving on active duty under a call order of

longer than 30 days or

– Serving on active Guard and Reserve duty

Dependents of qualifying servicemembers

The MLA continues to offer creditors a safe harbor for

compliance when a covered-borrower check is performed in

conformity with the rule’s requirements; however, the

amendments change what constitutes a safe harbor.

Safe Harbor

Old Safe Harbor New Safe Harbor

Use of covered borrower statement DOD online database

Consumer report from a nationwide consumer reporting agency

14

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

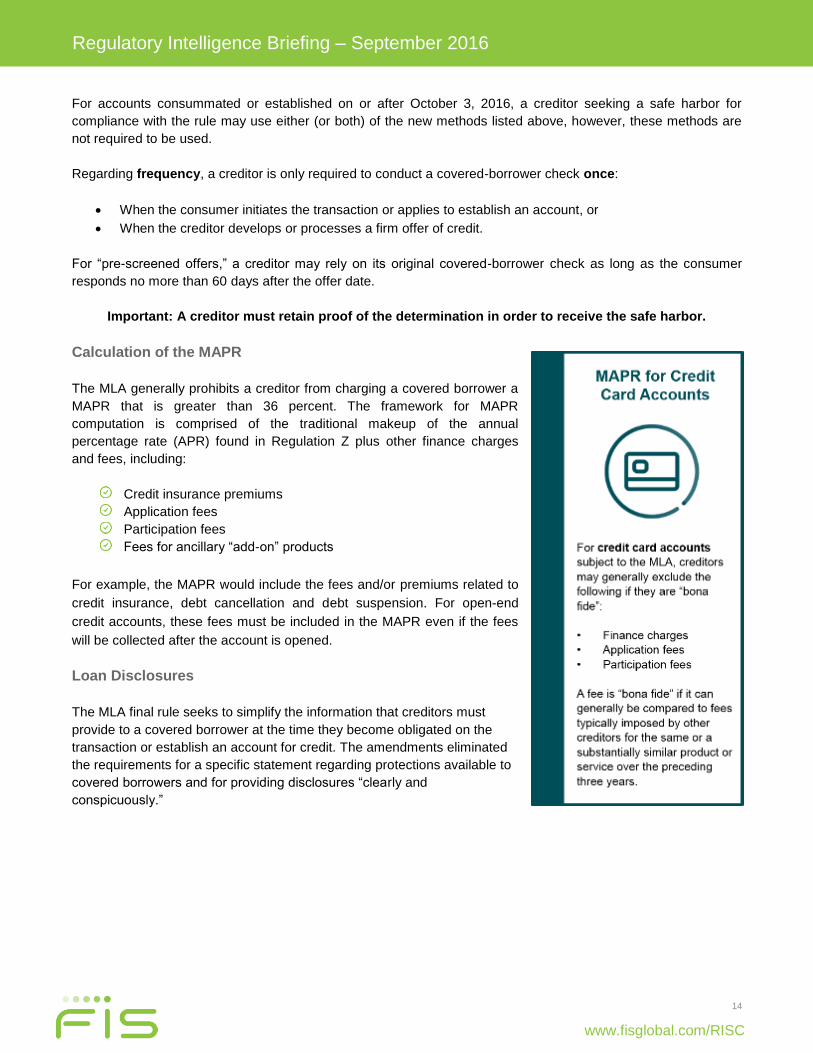

For accounts consummated or established on or after October 3, 2016, a creditor seeking a safe harbor for

compliance with the rule may use either (or both) of the new methods listed above, however, these methods are

not required to be used.

Regarding frequency, a creditor is only required to conduct a covered-borrower check once:

When the consumer initiates the transaction or applies to establish an account, or

When the creditor develops or processes a firm offer of credit.

For “pre-screened offers,” a creditor may rely on its original covered-borrower check as long as the consumer

responds no more than 60 days after the offer date.

Important: A creditor must retain proof of the determination in order to receive the safe harbor.

Calculation of the MAPR

The MLA generally prohibits a creditor from charging a covered borrower a

MAPR that is greater than 36 percent. The framework for MAPR

computation is comprised of the traditional makeup of the annual

percentage rate (APR) found in Regulation Z plus other finance charges

and fees, including:

Credit insurance premiums

Application fees

Participation fees

Fees for ancillary “add-on” products

For example, the MAPR would include the fees and/or premiums related to

credit insurance, debt cancellation and debt suspension. For open-end

credit accounts, these fees must be included in the MAPR even if the fees

will be collected after the account is opened.

Loan Disclosures

The MLA final rule seeks to simplify the information that creditors must

provide to a covered borrower at the time they become obligated on the

transaction or establish an account for credit. The amendments eliminated

the requirements for a specific statement regarding protections available to

covered borrowers and for providing disclosures “clearly and

conspicuously.”

15

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

New disclosure requirements include:

A statement of the applicable MAPR that describes the charges the creditor may impose, instead of the

periodic rate of the MAPR itself and the total dollar amount of all charges included in the MAPR

Any disclosure required by Regulation Z, delivered in accordance with the requirements of Regulation Z

A clear description of the payment obligation of the covered borrower, which may be satisfied by a

payment schedule (closed-end credit) or an account opening disclosure (open-end credit)

Provision of the required MLA disclosures to the borrower both in writing and orally. A creditor may elect

to provide the oral disclosures either in person or by providing the covered borrower with a toll-free

telephone number.

Key Takeaways

While impacted institutions may have taken steps to prepare for compliance with the MLA final rule, there may be

additional work to be done. Below are some key steps for ensuring compliance with the MLA amendments.

Please note this list is not exhaustive. It is intended to spark an institution’s internal discussion.

Update regulatory applicability matrix so all newly covered products are appropriately mapped to the

MLA.

Review written and oral disclosures and their accompanying procedures for compliance with

requirements.

For open-end credit accounts, establish procedures to monitor the MAPR each billing cycle and prevent

the MAPR from exceeding 36 percent.

Establish procedures on open-end credit accounts to address when the borrower is no longer covered.

Assess the institution’s usage (if any) of the safe harbor provision.

Evaluate methods for identifying covered borrowers and adjust those procedures if needed.

Update all impacted policies, procedures, job aids and training materials.

Train staff in affected business units on the changes.

Include MLA in upcoming monitoring and audit schedules for covered products and services.

Flag calendars for future credit card compliance deadlines and implement an action plan for implementing

the changes, including clear lines of responsibility, key milestones and deadlines.

Report to the board of directors on changes implemented to ensure compliance.

16

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

SECURITIES COMPLIANCE SERVICES

FIS RISC Solutions is your trusted partner for all things risk and compliance. Contact us today to help with your RISC needs. Call us toll-free: 1.800.822.6758 Email us: [email protected]

Visit us online: fisglobal.com/RISC

F. Did You Know?

FIS Risk, Information Security and Compliance (RISC) Solutions provides a

practical, risk-based approach to securities compliance.

Our methodology is to first understand a firm’s business and then tailor a sound

compliance program that satisfies regulatory requirements.

We specialize in identifying, measuring and mitigating compliance risks. Through

a combination of consulting, technology and managed services, we will work with

you to mitigate risks and lower the cost of compliance.

FIS RISC Solutions Offers:

Compliance program assessments and remediation

Compliance program development and implementation

Compliance co-sourcing

Code of conduct and ethics

Regulatory impact assessments

Compliance reviews, audits, and mock examinations

Supervisory control testing

Advertising reviews

Branch examinations

Transaction monitoring and trade surveillance

Forensic investigations

Comprehensive training

Registration and reporting

On-site support during regulatory examinations

BSA/AML and sanctions consulting

Information security and cybersecurity consulting

Additionally, we can provide dedicated, experienced, virtual back-office staff

resources to perform a variety of risk, information security, and compliance tasks.

We specialize in identifying, measuring and mitigating securities compliance risks.

17

Regulatory Intelligence Briefing – September 2016

www.fisglobal.com/RISC

G. About FIS’ Center of Regulatory Intelligence

FIS™ (NYSE: FIS), a global leader in banking and payments technology as well as consulting and outsourcing

solutions, opened its Center of Regulatory Intelligence (“Center”) in Washington, D.C. on June 16, 2015. The

primary goal of the Center is to translate policy, legislative and regulatory developments into actionable

intelligence for FIS clients to enable knowledge advantage. The unique perspective gained by monitoring

regulatory change at such close proximity to the policymakers and regulators enables the Center to empower FIS

clients to stay one step ahead, identify impact precisely, make smart business decisions and succeed. FIS clients

receive insights from the Center through regularly published regulatory intelligence briefings and thought

leadership insights intended to give client institutions deep intelligence into regulatory initiatives coming out of the

legislature, administration and regulatory agencies. Input from the Center also helps drive FIS research and

development efforts as well as consulting services aimed at helping institutions address regulatory changes prior

to implementation.

The Center provides the latest intelligence, thought leadership and cutting-edge regulatory insights into risk,

information security and compliance issues facing the financial services industry. This FIS thought leadership

center provides early insight on regulatory changes, helping financial services clients stay compliant with new

regulations. Through the Center, FIS interfaces with key policymakers to provide industry perspectives on the

potential impacts of regulatory mandates to financial institutions.

Contact Us

FIS Center of Regulatory Intelligence

1101 Pennsylvania Ave., NW Suite 300

Washington, DC 20004

P: 202.756.2263

©2016 FIS and/or its subsidiaries. All Rights Reserved.