CECL Workshop Discounted Cash Flow Method Caine & Alan... · 8 Key Concepts and Inputs...

19

MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2017 Wolf & Company, P.C. CECL Workshop Discounted Cash Flow Method Martin M. Caine, CPA Alan D. Lloyd, CPA

Transcript of CECL Workshop Discounted Cash Flow Method Caine & Alan... · 8 Key Concepts and Inputs...

MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2017 Wolf & Company, P.C.

CECL Workshop

Discounted Cash Flow Method

Martin M. Caine, CPA

Alan D. Lloyd, CPA

2

Introduction

www.wolfandco.com

Alan Lloyd, CPA

Senior Audit Manager, Wolf & Company, P.C.

Voice: (215) 983-5996

Email: [email protected]

LinkedIn: alan-lloyd

Martin Caine, CPA

Member of the Firm, Wolf & Company, P.C

Voice: (413) 726-6852

Email: [email protected]

LinkedIn: martin-caine

3

Agenda

• Discounted Cash Flow Model

– Key concepts and inputs

– Pros and cons

– Sample DCF model review

– Q&A

4

Key Concepts and Inputs

From ASC 326-20-30-4:

If an entity estimates expected credit losses using methods

that project future principal and interest cash flows (that is, a

discounted cash flow method), the entity shall discount

expected cash flows at the financial asset’s effective

interest rate. When a discounted cash flow method is

applied, the allowance for credit losses shall reflect the

difference between the amortized cost basis and the

present value of the expected cash flows.

5

Key Concepts and Inputs

For variable rate loans benchmarked to an index:

Projections of changes in the factor (e.g LIBOR, prime rate,

etc.) shall not be made for purposes of determining the

effective interest rate or estimating expected future cash

flows.

6

Key Concepts and Inputs

From ASC 326-20-30-6:

An entity shall consider estimated prepayments in the

future principal and interest cash flows when utilizing a

method in accordance with paragraph 326-20-30-4 (DCF).

An entity shall not extend the contractual term for

expected extensions, renewals, and modifications unless

it has a reasonable expectation at the reporting date that it

will execute a troubled debt restructuring with the borrower.

7

Key Concepts and Inputs

Information that can be used:

• Internal, external or combination of both related to past

events, current conditions, and reasonable, supportable

forecasts

• Consider quantitative and qualitative factors in the

environment

• Not required to search for all possible information that is

not readily available without undue cost and effort

8

Key Concepts and Inputs

Collateral-dependent loans:

Regardless of the initial measurement method, an entity shall

measure expected credit losses based on the fair value of

the collateral when the entity determines that foreclosure is

probable.

An entity also shall consider any credit enhancements that

are applicable to the financial asset when recording the

allowance for credit losses.

9

Key Concepts and Inputs

Changes in present value over reporting periods:

May result not only from the passage of time but also from

changes in estimates of the timing or amount of expected

future cash flows. DCF users are permitted to report the

entire change in present value as credit loss expense (or

reversal of credit loss expense). Alternatively, an entity may

report the change in present value attributable to the

passage of time as interest income.

10

Key Concepts and Inputs

Key Inputs:

• Loan Data:

– Loan number

– Unpaid principal balance (UPB), Book Balance

– Payment amount

– Maturity Date

– Segment Information (e.g. call code, product code, geography, risk

rating, FICO scores, etc.)

– Payment structure

– Revolving status

– Available credit balances

– Government guarantee info

– Participation information, etc.

11

Key Concepts and Inputs

Key Inputs:

• Assumptions:

– Prepayment rate (Conditional Prepayment Rate (CPR), Single

Monthly Mortality (SMM))

– Expected default rates

– Expected loss rates

– Timing to recovery

12

Key Concepts and Inputs

Example SMM calculation that can be translated to CPR:

TOTALS 25,376,213 11,933,614 76,169,702 1.24% 13.85%

Month

Beginning

Balance

Contractual

Payment

Contractual

Principal

Contractual

Interest Ending Balance

Actual Payments

Collected SMM CPR

1 300,000,000 3,109,152 1,984,152 1,125,000 293,846,416 6,153,584 1.02% 11.6%

2 293,846,416 3,109,152 2,007,228 1,101,924 287,436,704 6,409,711 1.13% 12.7%

3 287,436,704 3,109,152 2,031,265 1,077,888 280,918,095 6,518,609 1.19% 13.4%

4 280,918,095 3,109,152 2,055,709 1,053,443 274,738,317 6,179,778 1.10% 12.4%

5 274,738,317 3,109,152 2,078,884 1,030,269 268,315,888 6,422,429 1.21% 13.6%

6 268,315,888 3,109,152 2,102,968 1,006,185 262,007,906 6,307,981 1.20% 13.5%

7 262,007,906 3,109,152 2,126,623 982,530 255,773,425 6,234,481 1.20% 13.5%

8 255,773,425 3,109,152 2,150,002 959,150 249,455,112 6,318,313 1.26% 14.1%

9 249,455,112 3,109,152 2,173,696 935,457 242,977,159 6,477,953 1.36% 15.1%

10 242,977,159 3,109,152 2,197,988 911,164 236,575,062 6,402,096 1.36% 15.2%

11 236,575,062 3,109,152 2,221,996 887,156 230,252,965 6,322,097 1.36% 15.2%

12 230,252,965 3,109,152 2,245,704 863,449 223,830,298 6,422,667 1.44% 16.0%

Pros & Cons

13

Pros Cons

Less historical data required Significant amount of computational

power required

Works well for amortizing loans,

balloons, fixed P&I, etc.

Does not work well for revolving loans

Can be easily leveraged for other areas

(e.g. Stress-testing, pricing, fair value

calculations, etc.)

Not as practical as some other models

such as historical loss and vintage

Useful if lack of loss history

Back-testing to support and fine-tune

assumptions

Go-forward analysis instead of historical

14

Sample DCF Model Review - Mortgage

Excerpt from model for single mortgage loan:TOTALS 99,858 55,707 156,549 18,592 2,789 15,804 327,918

Month

Beginning

Balance

Contractual

Payment Principal Interest Prepayment

Defaulted

Principal

Estimated

Loss

Estimated

Recovery Ending Balance Cash Flows

1 275,000 1,393 20 1,030 2,914 344 52 - 271,723 3,963

2 271,723 1,393 36 1,018 2,879 340 51 - 268,468 3,933

3 268,468 1,393 52 1,005 2,844 336 50 - 265,236 3,902

4 265,236 1,393 68 993 2,810 332 50 - 262,026 3,872

5 262,026 1,393 84 981 2,776 328 49 - 258,839 3,841

6 258,839 1,393 100 969 2,742 324 49 - 255,673 3,811

7 255,673 1,393 116 958 2,708 320 48 - 252,529 3,782

8 252,529 1,393 132 946 2,674 316 47 - 249,407 3,752

9 249,407 1,393 148 934 2,641 312 47 - 246,307 3,723

10 246,307 1,393 163 922 2,608 308 46 - 243,228 3,694

11 243,228 1,393 178 911 2,575 304 46 292 240,170 3,957

12 240,170 1,393 194 900 2,543 300 45 289 237,133 3,925

13 237,133 1,393 209 888 2,511 296 44 285 234,117 3,893

124 2,771 1,393 1,380 10 15 3 1 18 1,373 1,423

125 1,373 1,393 1,371 5 0 2 0 17 0 1,393

126 15 - 15

15

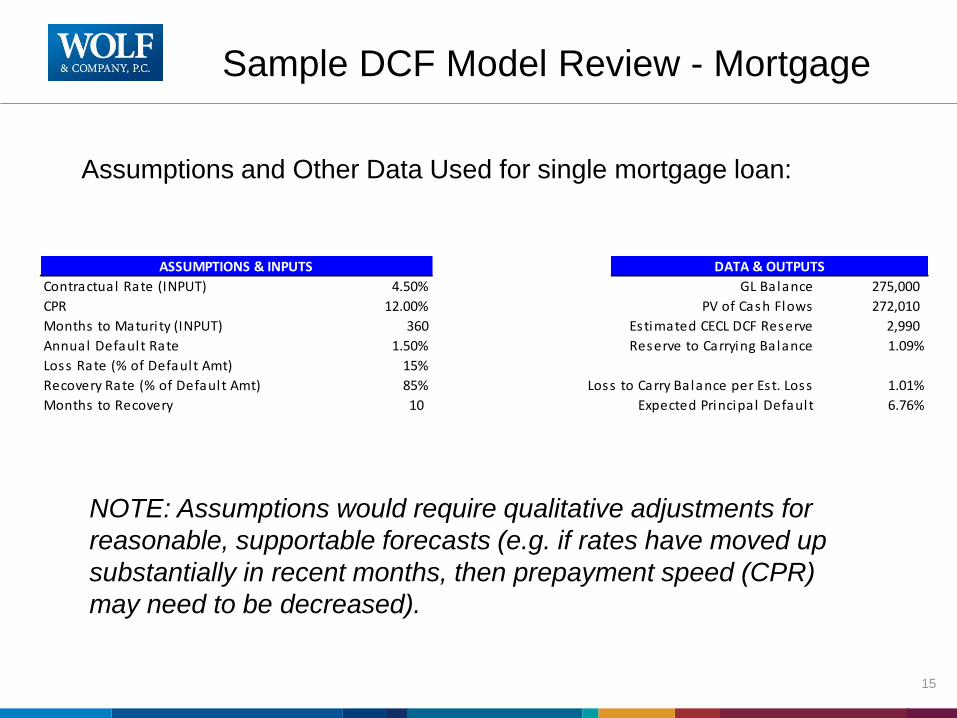

Sample DCF Model Review - Mortgage

Assumptions and Other Data Used for single mortgage loan:

NOTE: Assumptions would require qualitative adjustments for

reasonable, supportable forecasts (e.g. if rates have moved up

substantially in recent months, then prepayment speed (CPR)

may need to be decreased).

Contractual Rate (INPUT) 4.50% GL Balance 275,000

CPR 12.00% PV of Cash Flows 272,010

Months to Maturi ty (INPUT) 360 Estimated CECL DCF Reserve 2,990

Annual Default Rate 1.50% Reserve to Carrying Balance 1.09%

Loss Rate (% of Default Amt) 15%

Recovery Rate (% of Default Amt) 85% Loss to Carry Balance per Est. Loss 1.01%

Months to Recovery 10 Expected Principal Default 6.76%

DATA & OUTPUTSASSUMPTIONS & INPUTS

16

Sample DCF Model Review - Pool

Excerpt from model for pool:

TOTALS 169,479,009 35,934,473 117,727,983 12,793,007 1,535,161 11,257,846 334,399,312

Month

Beginning

Balance

Contractual

Payment Principal Interest Prepayment

Defaulted

Principal

Estimated

Loss

Estimated

Recovery Ending Balance Cash Flows

1 300,000,000 3,109,152 1,585,652 1,123,500 3,727,171 400,000 48,000 - 294,287,177 6,436,323

2 294,287,177 3,109,152 1,614,664 1,102,105 3,655,456 392,383 47,086 - 288,624,674 6,372,225

3 288,624,674 3,109,152 1,643,420 1,080,899 3,584,373 384,833 46,180 - 283,012,048 6,308,692

4 283,012,048 3,109,152 1,671,923 1,059,880 3,513,916 377,349 45,282 - 277,448,860 6,245,718

5 277,448,860 3,109,152 1,700,174 1,039,046 3,444,079 369,932 44,392 - 271,934,675 6,183,299

6 271,934,675 3,109,152 1,728,177 1,018,395 3,374,857 362,580 43,510 - 266,469,061 6,121,430

7 266,469,061 3,109,152 1,755,934 997,927 3,306,246 355,292 42,635 - 261,051,590 6,060,106

8 261,051,590 3,109,152 1,783,445 977,638 3,238,238 348,069 41,768 - 255,681,837 5,999,322

9 255,681,837 3,109,152 1,810,715 957,528 3,170,830 340,909 40,909 - 250,359,384 5,939,073

10 250,359,384 3,109,152 1,837,744 937,596 3,104,015 333,813 40,058 - 245,083,812 5,879,355

11 245,083,812 3,109,152 1,864,535 917,839 3,037,789 326,778 39,213 352,000 239,854,709 6,172,163

12 239,854,709 3,109,152 1,891,090 898,256 2,972,146 319,806 38,377 345,297 234,671,667 6,106,789

13 234,671,667 3,109,152 1,917,411 878,845 2,907,082 312,896 37,547 338,653 229,534,278 6,041,992

70 3,666,330 3,109,152 3,090,533 13,730 7,192 4,888 587 42,533 563,717 3,153,989

71 563,717 3,109,152 563,717 2,114 - - - 38,556 - 604,387

72 34,614 - 34,614

17

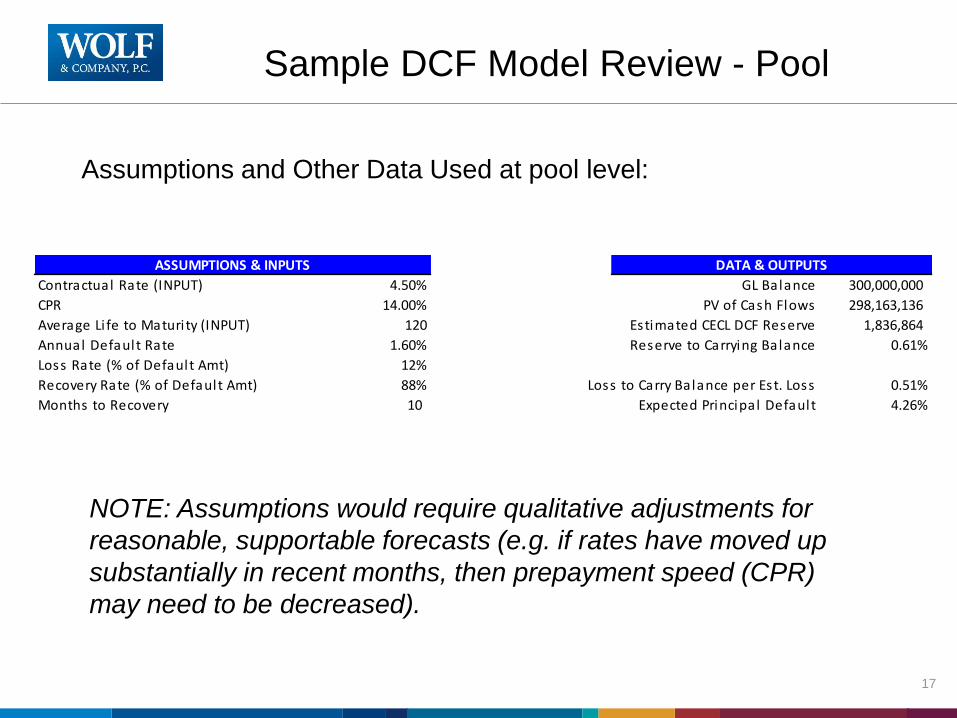

Sample DCF Model Review - Pool

Assumptions and Other Data Used at pool level:

NOTE: Assumptions would require qualitative adjustments for

reasonable, supportable forecasts (e.g. if rates have moved up

substantially in recent months, then prepayment speed (CPR)

may need to be decreased).

Contractual Rate (INPUT) 4.50% GL Balance 300,000,000

CPR 14.00% PV of Cash Flows 298,163,136

Average Li fe to Maturi ty (INPUT) 120 Estimated CECL DCF Reserve 1,836,864

Annual Default Rate 1.60% Reserve to Carrying Balance 0.61%

Loss Rate (% of Default Amt) 12%

Recovery Rate (% of Default Amt) 88% Loss to Carry Balance per Est. Loss 0.51%

Months to Recovery 10 Expected Principal Default 4.26%

DATA & OUTPUTSASSUMPTIONS & INPUTS

Discussion points

1. Any concerns with the complexity?

2. Any concerns with the required assumptions?

3. How can this analysis be improved?

3. Does anyone plan to use a DCF model for CECL?

18

Sample DCF Model Review

19

Thank You

www.wolfandco.com

Alan Lloyd, CPA

Senior Manager, Wolf & Company, P.C.

Voice: (215) 983-5996

Email: [email protected]

LinkedIn: alan-lloyd

Martin Caine, CPA

Member of the Firm, Wolf & Company, P.C.

Voice: (413) 726-6852

Email: [email protected]

LinkedIn: martin-caine