CECL Jim McGough, CPA, CGMA - Wolf & Company, P.C. · PDF file · 2017-07-01CECL...

24

MEMBER OFALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2017 Wolf & Company, P.C. 2017 CEO & Board University What Boards Need to Know About CECL Jim McGough, CPA, CGMA

Transcript of CECL Jim McGough, CPA, CGMA - Wolf & Company, P.C. · PDF file · 2017-07-01CECL...

MEMBER OFALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2017 Wolf & Company, P.C.

2017 CEO & Board UniversityWhat Boards Need to Know About

CECL

Jim McGough, CPA, CGMA

Introduction

2

Jim McGough, CPA, CGMA

Senior Audit Manager

Agenda

Overview

CECL Transition – Where to start

Implementation Considerations

– Loan pools

– Appropriate methodology

– Historical loss data

– Reasonable and supportable forecasts

Scope of CECL on Investments

– CECL for HTM securities

3

Overview Topic 326, Financial Instruments-

Credit Losses

Problem

• Too many accounting models for impairment

• Too little – too late

What changed?

• Life-of-loan loss period

• “Impaired” trigger is gone

• Group similar assets

• Forward looking requirement

General observations

• ALL estimate is more complicated under CECL

• More judgment required for principle based model

• Scalable & Flexible

• Quicker recognition of losses

4

CECL Transition – Where to Start

1. Learn the standard, and understand the basis for

conclusions included therein.

• Principles-based standard

• Requirements of the standard and best practices

will evolve

• Effective for calendar year entities: o 2020 for public business entities (PBE) that are SEC filers,

including interim periods

o 2021 for other public business entities, including interim periods

o Dec 31, 2021 for all others

5

CECL Transition – Where to Start

2. Establish your working group, including

professionals outside the accounting function

such as lending, IT, risk management.

• CECL is a critical estimate for the senior

management team

• Delineation of roles and responsibilities for

personnel involved in the estimation process

• When to involve internal audit?

6

CECL Transition – Where to Start

3. Develop your project plan, including

governance/oversight and milestone dates.

• Define responsibilities

• Assess data needs (build and test)

• Establish time frames and milestones

• Dry/parallel runs

• Determine implementation has appropriate

resources and priority

Key question for Board to ask: “What mechanisms will

give us timely knowledge of the ongoing status of

implementation?”

7

CECL Transition – Where to Start

4. Incorporate internal control considerations along

the way to achieve design effectiveness.

• Written policies and procedures

• Completeness and accuracy of data

• Management review and approval

• Process must hold up under a quarterly frequency

• Outsourced model might be in scope of

supervisory guidance for model risk management

Can the estimate be validated/audited?

8

CECL Transition – Where to Start

5. Communicate with your auditor and primary

regulator.

• Scalability of the model exposes the bank to

regulatory interpretation

• Regulatory agencies will develop supervisory

guidance to clarify expectations but will not

provide an approved model or example calculation

• Best practices will evolve

• Conclude on PBE status with external auditor so

there are no surprises with effective date

9

Implementation Considerations

Determine loan pools (those with similar risk

characteristics)

Identify an appropriate methodology for each loan pool

Obtain sufficient historical loss data

Develop reasonable and supportable forecasts

10

Loan Pools

• Loan pooling is a critical decision point; impacting all

subsequent actions

• Does not prescribe a unit of account, but does require

pooling of assets with similar risk characteristics.

• Loan segments utilized for current GAAP or call report

have to be reevaluated

• Excessive aggregation/disaggregation may be

problematic

11

Loan Pools – Risk Characteristics

12

In evaluating financial assets on a collective (pool) basis,

aggregate financial assets on the basis of similar risk

characteristics, which may include any one or a combination

of the following (the following list is not intended to be all

inclusive):

a. Internal or external (third-

party) credit score or credit

ratings

b. Risk ratings or classification

c. Financial asset type

d. Collateral type

e. Size

f. Effective interest rate

g. Term

h. Geographical location

i. Industry of the borrower

j. Vintage

k. Historical or expected credit loss

patterns

l. Reasonable and supportable

forecast periods

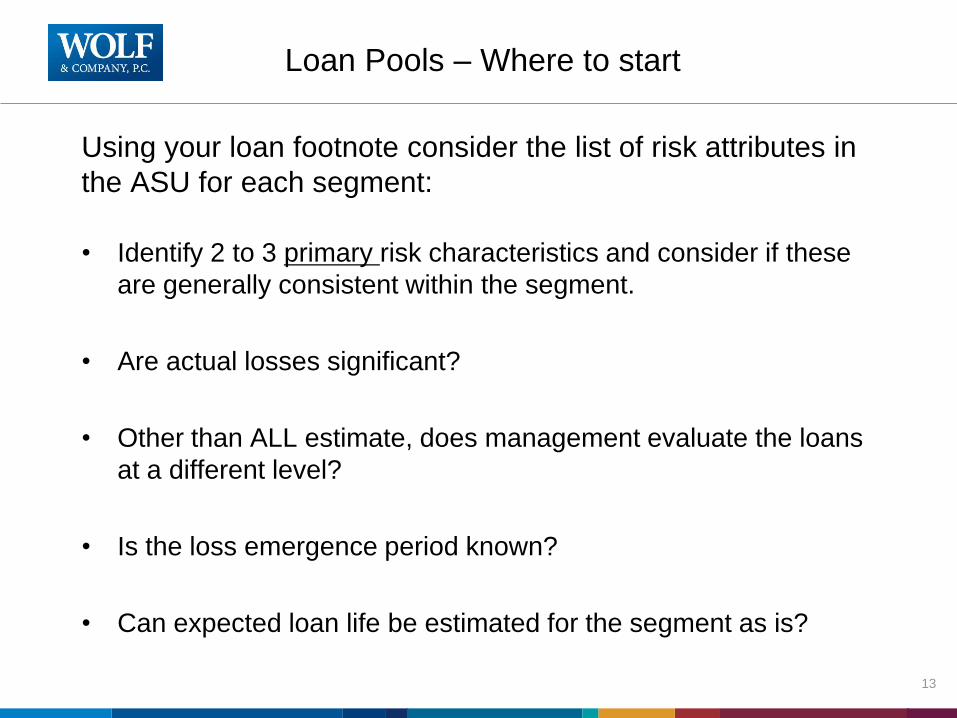

Loan Pools – Where to start

Using your loan footnote consider the list of risk attributes in

the ASU for each segment:

• Identify 2 to 3 primary risk characteristics and consider if these

are generally consistent within the segment.

• Are actual losses significant?

• Other than ALL estimate, does management evaluate the loans

at a different level?

• Is the loss emergence period known?

• Can expected loan life be estimated for the segment as is?

13

Loan Pools – Exclude Certain Loans

• Estimated credit loss for an asset should be measured

individually if there are no similar risk characteristics with

other loans.

• Practical expedients (FV of collateral) exist for:

– Collateral-dependent loans (borrower experiencing financial

difficulties and repayment expected through sale or operation of the

property)

– Loans secured by collateral maintenance provisions

14

Appropriate Methodology

GAAP requirement is explicitly scalable and allows

preparers to develop estimation methods that are

appropriate and practical for their circumstances.

• One impairment model but many methods.

• Methodology by loan segment should be determined

early because relevant data and software needs may

vary.

15

Appropriate Methodology

FASB concluded that different outcomes for expected credit

losses are acceptable, given different levels of complexity

and sophistication.

Principles based

Scalable

FASB provided examples that illustrate implementation in a

noncomplex environment. (Example 1 in the ASU)

16

Appropriate Methodology

Considerations for scalability:

What is the entity’s strategic plan and who will be relying on the financial

statements now and in the immediate future?

Does the primary banking regulator classify the entity as a smaller, less

complex institution?

Would the cost of a more complex methodology exceed the benefits? The

result may not be better, and model/error risk may be elevated.

Is a sophisticated model required or desired for any segment based on the

nature of the loans and relevant loss history?

17

Historical Loss Data

An entity’s loss history loss remains as the starting point and

generally provides a basis for expected credit losses.

GAAP does not specify a particular methodology for

determining historical credit loss experience. “That

methodology may vary depending on the size of the entity,

the range of the entity’s activities, the nature of the entity’s

financial assets, and other factors.” [ASU 326-20-55-2]

The loan segment and the chosen method will determine the

data needs.

Historical data is still adjusted using qualitative factors.

18

Reasonable and Supportable Forecasts

Identify risk drivers for each loan segment

For example, real estate values and unemployment rates for mortgage loans

Q-Factor analysis will document whether historical loss data requires adjustment

based on the forecast for these drivers.

Entities are required to adjust for reasonable and supportable forecasts of the

future, by adjusting historical loss information for future expected events that

are not reflected in historical losses.

For periods where an entity is unable to support its forecast, it is required to

revert to historical loss information.

Consider consistency with other forecasts within the entity (ALM, risk

management, MSR valuation, budget, capital planning, other loan segments).

Some entities may begin with external forecasts (e.g. Federal Reserve) and

adjust to what management foresees in its area of operations.19

Reasonable and Supportable Forecasts

The adjustments for current conditions and reasonable and

supportable forecasts may continue to be qualitative, similar to the

approach applied by many institutions today.

• More robust quantitative models and/or greater segmentation may

result in a smaller qualitative component, depending on the

circumstances.

• Q-Factor adjustments may be more significant because of the life-

of-loan measurement period.

• Qualitative analysis may not always be directionally consistent

with current trends/events.

For example, an increase in delinquency rates may have been

previously considered/anticipated when estimating expected

credit losses.

20

Scope of CECL on Investments

Type Current New

Equity Securities Topic 320 Carried at FV with changes

through earnings – no

impairment analysis required

(ASU 2016-01)

AFS Debt Securities Topic 320 Topic 326-30

HTM Debt Securities Topic 320 Topic 326

CECL for HTM Securities

• Evaluate securities on a pool basis (similar risk

characteristics)

• Individual basis (if not similar risk characteristics)

• Consider qualitative and quantitative factors that relate to

operating environment and specific to entity, both internal

and external

• When determining contractual cash flows and life of

related asset, should consider expected prepayments

• Should revert to unadjusted historical credit loss for future

periods beyond which an entity can make reasonable

forecast

• Estimate should always reflect risk of loss, even if remote

CECL Implementation Considerations

Questions ?

Thank you!

24

Jim McGough, CPA, CGMA

Senior Audit Manager