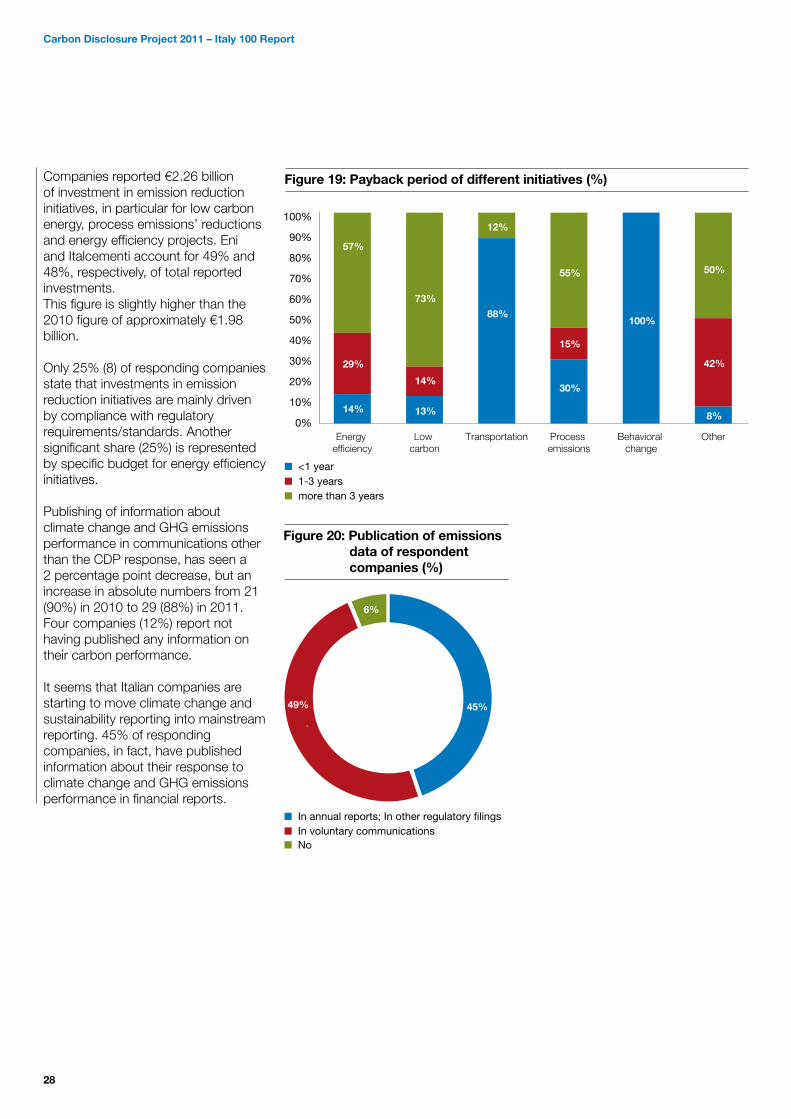

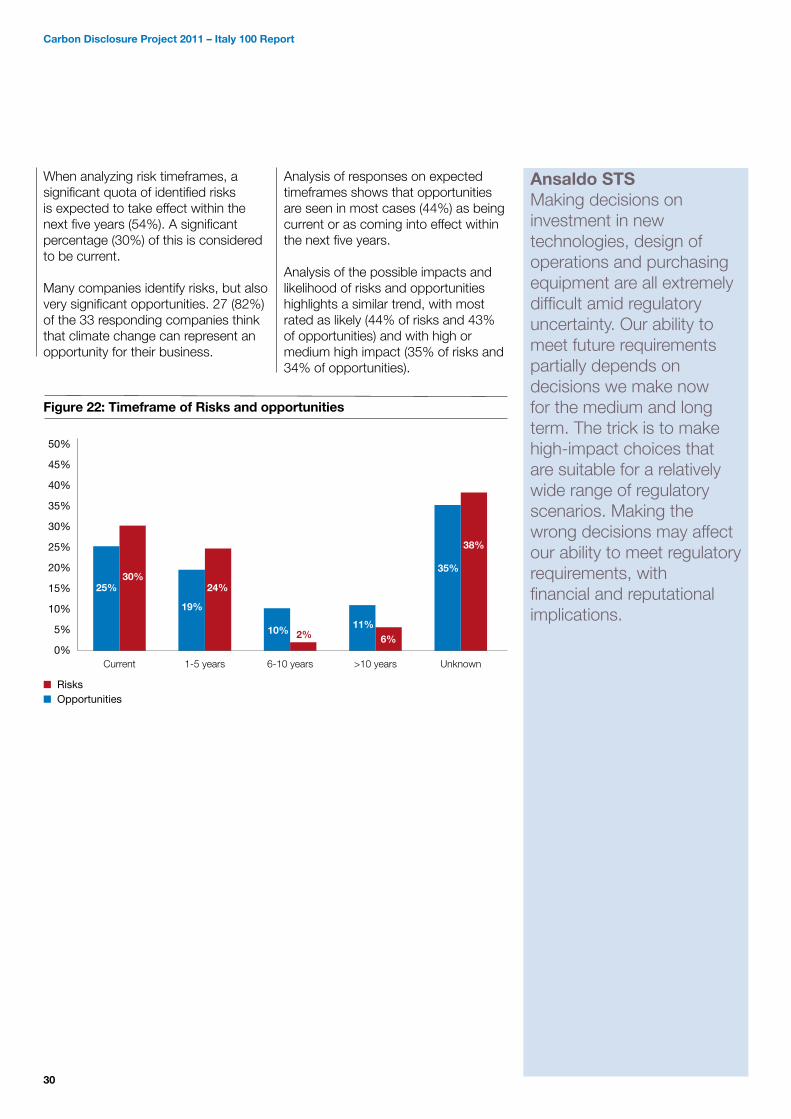

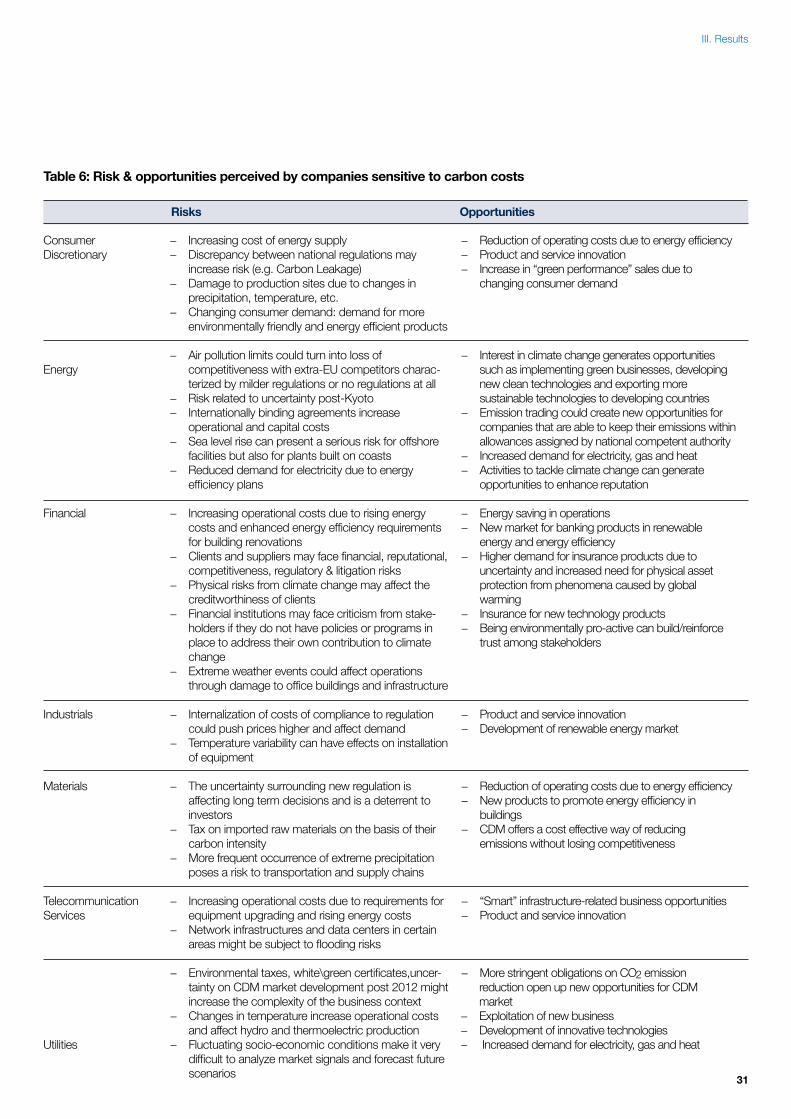

CDP Italy 100 Report 2011 Accelerating carbon … written for Carbon Disclosure Project by Carbon...

52

CDP Italy 100 Report 2011 Accelerating carbon management through business as usual On behalf of 551 investors with assets of US$ 71 trillion Report written for Carbon Disclosure Project by Carbon Disclosure Project [email protected] +1 212 378 2086 www.cdproject.net Carbon Disclosure Partner

Transcript of CDP Italy 100 Report 2011 Accelerating carbon … written for Carbon Disclosure Project by Carbon...

1

CDP Italy 100 Report 2011Accelerating carbon management through business as usual

On behalf of 551 investors with assets of US$ 71 trillion

Report written forCarbon Disclosure Project by

Carbon Disclosure [email protected]+1 212 378 2086www.cdproject.net

Carbon Disclosure Partner

2

2011 Carbon Disclosure Project Investor Members

CDP works with investors globally to advance the investment opportunities and reduce the risks posed by climate change by asking almost 6,000 of the world’s largest companies to report on their climate strategies, GHG emissions and energy use in the standardized Investor CDP format. To learn more about CDP’s member offer and becoming a member, please contact us or visit the CDP Investor Member section at www.cdproject.net/investormembers

ABRAPP - Associação Brasileira das Entidades Fechadas de Previdência ComplementarAEGON N.V.AKBANK T.A.S. Allianz Global Investors Kapitalanlagegesell-schaft mbHATP GroupAviva InvestorsBank of America Merrill LynchBlackRockBP Investment Management LimitedCalifornia Public Employees’ Retirement SystemCalifornia State Teachers’ Retirement SystemCalvert Asset Management Company, Inc.

Catholic SuperCCLA Investment Management LtdEthos FoundationGeneration Investment ManagementHSBC Holdings plcINGKB Kookmin BankKLPLegg Mason, Inc.London Pensions Fund AuthorityMitsubishi UFJ Financial Group (MUFG)Morgan Stanley National Australia BankNEI InvestmentsNeuberger BermanNewton Investment Management LimitedNordea Investment ManagementPFA PensionRaiffeisen Schweiz

Royal Bank of Scotland GroupRobecoRockefeller & Co., Inc.SAM GroupSchroders Scottish Widows Investment PartnershipSEBSompo Japan Insurance Inc.Standard CharteredSun Life Financial Inc.TD Asset Management Inc. and TDAM USA Inc.The Wellcome TrustZurich Cantonal Bank

3

2011 Carbon Disclosure Project Investor Signatories

Carbon Disclosure Project 2011 551 financial institutions with assets of US$71 trillion were signatories to the CDP 2011 information request dated February 1st, 2011

Aberdeen Asset ManagersAberdeen Immobilien KAG mbHABRAPP - Associação Brasileira das Entidades Fechadas de Previdência ComplementarActive Earth Investment ManagementAcuity Investment ManagementAddenda Capital Inc.Advanced Investment PartnersAdvantage Asset Managers (Pty) LtdAEGON Magyarország Befektetési Alapkezelo Zrt.AEGON N.V.AEGON-INDUSTRIAL Fund Management Co., LtdAFP IntegraAIG Asset ManagementAk Asset Management AKBANK T.A.S.Alberta Investment Management Corporation (AIMCo)Alberta Teachers Retirement FundAlcyone FinanceAllianz Elementar Versicherungs-AGAllianz GroupAltira GroupAmalgamated BankAMP Capital InvestorsAmpegaGerling Investment GmbHAmundi AMANBIMA – Associação Brasileira das Entidades dos Mercados Financeiro e de CapitaisAntera Gestão de Recursos S.A.APG GroupAprionisAquila CapitalARIA (Australian Reward Investment Alliance)Arisaig Partners Asia Pte LtdARK Investment Advisors Inc.Arma Portföy Yönetimi A.S.ASB Community TrustASM Administradora de Recursos S.A.ASN BankAssicurazioni Generali SpaATP GroupAustralia and New Zealand Banking Group LimitedAustralian Central Credit Union incorporating Savings & Loans Credit UnionAustralian Ethical Investment LimitedAustralianSuperAvivaAviva InvestorsAXA GroupBaillie Gifford & Co.Bakers Investment Group (Australia) Pty LtdBanco Bradesco S/ABanco de Credito del Peru BCPBanco de Galicia y Buenos Aires S.A.Banco do Brasil S/ABanco Nacional de Desenvolvimento Econômico e Social - BNDESBanco SantanderBanesprev – Fundo Banespa de Seguridade SocialBanesto (Banco Español de Crédito S.A.)Bank of America Merrill LynchBank of MontrealBank Sarasin & Cie AGBank VontobelBankhaus Schelhammer & Schattera Kapitalanlagegesellschaft m.b.H.BANKINTER S.A.BankInvestBanque DegroofBarclays

Baumann and Partners S.A.BAWAG P.S.K. INVEST GmbHBayern LBBayernInvest Kapitalanlagegesellschaft mbHBBC Pension Trust LtdBBVABedfordshire Pension FundBentall KennedyBeutel Goodman and Co. LtdBioFinance Administração de Recursos de Terceiros LtdaBlackRockBlumenthal FoundationBNP Paribas Investment PartnersBNY MellonBNY Mellon Service Kapitalanlage GesellschaftBoston Common Asset Management, LLCBP Investment Management LimitedBrasilprev Seguros e Previdência S/A.British Columbia Investment Management Corporation (bcIMC)BT Investment ManagementBusan BankCAAT Pension PlanCadiz Holdings LimitedCaisse de dépôt et placement du QuébecCaisse des DépôtsCaixa Beneficente dos Empregados da Companhia Siderurgica Nacional - CBSCaixa de Previdência dos Funcionários do Banco do Nordeste do Brasil (CAPEF)Caixa Econômica FederalCaixa Geral de DepositosCaja de Ahorros de Valencia, Castellón y Valencia, BANCAJACaja NavarraCalifornia Public Employees’ Retirement SystemCalifornia State Teachers’ Retirement SystemCalifornia State TreasurerCalvert Asset Management Company, IncCanada Pension Plan Investment BoardCanadian Friends Service Committee (Quakers)Canadian Imperial Bank of Commerce (CIBC)CAPESESPCapital Innovations, LLCCARE Super Pty LtdCarlson Investment ManagementCarmignac GestionCatherine Donnelly FoundationCatholic SuperCbus Superannuation FundCCLA Investment Management LtdCeleste Funds Management LimitedCentral Finance Board of the Methodist ChurchCeresChristian SuperChristopher Reynolds FoundationChurch Commissioners for EnglandChurch of England Pensions BoardCI Mutual Funds’ Signature Global AdvisorsClean Yield Group, Inc.Cleantech Invest AGClearBridge AdvisorsClimate Change Capital Group LtdCM-CIC Asset ManagementColonial First State Global Asset ManagementComerica IncorporatedComite syndical national de retraite BâtirenteCommerzbank AGCommInsureCommonwealth Bank of AustraliaCompton Foundation, Inc.Concordia VersicherungsgruppeConnecticut Retirement Plans and Trust FundsCo-operative Financial Services (CFS)Corston-Smith Asset Management Sdn. Bhd.CRD AnalyticsCrédit AgricoleCredit SuisseGruppo Credito ValtellineseDaegu BankDaiwa Securities Group Inc.de Pury Pictet Turrettini & Cie S.A.DekaBank Deutsche GirozentraleDeutsche Asset Management Investmentgesellschaft mbH

Deutsche Bank AGDeutsche Postbank Vermögensmanagement S.A.Development Bank of Japan Inc.Development Bank of the Philippines (DBP)Dexia Asset ManagementDexus Property GroupDnB NOR ASADomini Social Investments LLCDongbu InsuranceDWS Investment GmbHEarth Capital Partners LLPEast Sussex Pension FundEcclesiastical Investment ManagementEcofi Investissements - Groupe Credit CooperatifEdward W. Hazen FoundationEEA Group LtdElan Capital PartnersElement Investment ManagersELETRA - Fundação Celg de Seguros e PrevidênciaEnvironment Agency Active Pension fundEpworth Investment ManagementEquilibrium Capital GroupErste Asset ManagementErste Group BankEssex Investment Management Company, LLCESSSuperEthos FoundationEureko B.V.Eurizon Capital SGREvangelical Lutheran Church in Canada Pension Plan for Clergy and Lay WorkersEvli Bank PlcF&C Management Ltd FAELCE – Fundacao Coelce de Seguridade SocialFAPERS- Fundação Assistencial e Previdenciária da Extensão Rural do Rio Grande do SulFASERN - Fundação COSERN de Previdência ComplementarFédéris Gestion d’ActifsFIDURA Capital Consult GmbHFIM Asset Management LtdFIPECq - Fundação de Previdência Complementar dos Empregados e Servidores da FINEP, do IPEA, do CNPqFIRA. - Banco de MexicoFirst Affirmative Financial Network, LLCFirst Swedish National Pension Fund (AP1)Firstrand LimitedFive Oceans Asset Management Pty LimitedFlorida State Board of Administration (SBA)FolketrygdfondetFolksamFondaction CSNFondation de LuxembourgFondiaria-SAIFonds de Réserve pour les Retraites – FRRFourth Swedish National Pension Fund (AP4)FRANKFURT-TRUST Investment-Gesellschaft mbHFukoku Capital Management IncFUNCEF - Fundação dos Economiários FederaisFundação AMPLA de Seguridade Social - BrasiletrosFundação Atlântico de Seguridade SocialFundação Attilio Francisco Xavier FontanaFundação Banrisul de Seguridade SocialFundação de Assistência e Previdência Social do BNDES - FAPESFUNDAÇÃO ELETROBRÁS DE SEGURIDADE SOCIAL - ELETROSFundação Forluminas de Seguridade Social - FORLUZFUNDAÇÃO ITAUBANCOFundação Itaúsa IndustrialFundação Promon de Previdência SocialFundação Vale do Rio Doce de Seguridade Social - VALIAFundação Rede Ferroviaria de Seguridade Social – ReferFundação Sistel de Seguridade Social (Sistel)FUNDIÁGUA - FUNDAÇÃO DE PREVIDENCIA COMPLEMENTAR DA CAESBFuturegrowth Asset ManagementGartmore Investment Management LtdGEAP Fundação de Seguridade SocialGenerali Deutschland Holding AGGeneration Investment ManagementGenus Capital ManagementGjensidige Forsikring ASAGLS Gemeinschaftsbank eG

4

Goldman Sachs Group Inc.GOOD GROWTH INSTITUT für globale Vermögensentwicklung mbHGovernance for OwnersGovernment Employees Pension Fund (“GEPF”), Republic of South AfricaGreen Cay Asset ManagementGreen Century Capital ManagementGroupe Crédit CoopératifGroupe Investissement Responsable Inc.GROUPE OFI AMGrupo Banco PopularGrupo Santander BrasilGruppo Credito ValtellineseGruppo MontepaschiGuardian Ethical Management IncGuardians of New Zealand SuperannuationGuosen Securities Co., LTD.Hang Seng BankHarbourmaster CapitalHarrington Investments, IncHauck & Aufhäuser Asset Management GmbHHazel Capital LLPHDFC Bank LtdHealth Super FundHealthcare of Ontario Pension Plan (HOOPP)Henderson Global InvestorsHermes Fund ManagersHESTA SuperHSBC Global Asset Management (Deutschland) GmbHHSBC Holdings plcHSBC INKA Internationale Kapitalanlagegesellschaft mbHHyundai Marine & Fire Insurance. Co., Ltd.Hyundai Securities Co., Ltd.Ibgeana Society of Assistance and Security SIAS / Sociedade Ibgeana de Assistência e Seguridade (SIAS)IDBI Bank LtdIlmarinen Mutual Pension Insurance CompanyImpax Group plcIndusInd Bank LimitedIndustrial Bank (A)Industrial Bank of KoreaIndustry Funds ManagementInfrastructure Development Finance CompanyINGInsight Investment Management (Global) LtdInstituto de Seguridade Social dos Correios e Telégrafos- PostalisInstituto Infraero de Seguridade Social - INFRAPREVInstituto Sebrae De Seguridade Social - SEBRAEPREVInsurance Australia GroupInvestec Asset ManagementIrish Life Investment ManagersItau Asset ManagementItaú Unibanco Holding S AJanus Capital Group Inc.Jarislowsky Fraser LimitedJPMorgan Chase & Co.Jubitz Family FoundationJupiter Asset ManagementKaiser Ritter Partner (Schweiz) AGKB asset ManagementKB Kookmin BankKBC Asset Management NVKDB Asset Management Co., Ltd.KEPLER-FONDS Kapitalanlagegesellschaft m. b. H.KfW BankengruppeKlimaINVESTKLPKorea Investment Management Co., Ltd.The Korea Teachers Pension (KTP)Korea Technology Finance Corporation (KOTEC)KPA PensionLa Banque Postale Asset ManagementLa Financiere ResponsableLampe Asset Management GmbHLandsorganisationen i SverigeLBBW - Landesbank Baden-WürttembergLBBW Asset Management Investmentgesellschaft mbHLD Lønmodtagernes DyrtidsfondLegal & General Investment Management

Legg Mason, Inc.LGT Capital Management Ltd.LIG Insurance Co., LtdLight Green Advisors, LLCLiving Planet Fund Management Company S.A.Local Authority Pension Fund ForumLocal Government SuperLocal SuperLombard Odier Darier Hentsch & CieLondon Pensions Fund AuthorityLothian Pension FundLupus alpha Asset Management GmbHMacif GestionMacquarie Group LimitedMAMA Sustainable Incubation AGManMaple-Brown Abbott LimitedMarc J. Lane Investment Management, Inc.Maryland State TreasurerMatrix Asset ManagementMcLean BuddenMEAG MUNICH ERGO Asset Management GmbHMeeschaert Gestion PrivéeMeiji Yasuda Life Insurance CompanyMendesprev Sociedade PrevidenciáriaMerck Family FundMeritas Mutual FundsMetallRente GmbHMetrus – Instituto de Seguridade SocialMetzler Investment GmbhMFS Investment ManagementMidas International Asset ManagementMiller/Howard InvestmentsMirae Asset Global Investments Co. Ltd.Mirae Asset Securities Co., Ltd.Missionary Oblates of Mary ImmaculateMistra, Foundation for Strategic Environmental ResearchMitsubishi UFJ Financial Group (MUFG)Mizuho Financial Group, Inc.Mn ServicesMonega Kapitalanlagegesellschaft mbHMorgan StanleyMotor Trades Association of Australia Superannuation Fund Pty LtdMutual Insurance Company Pension-FenniaNatcan Investment ManagementNathan Cummings Foundation, TheNational Australia BankNational Bank of CanadaNational Grid Electricity Group of the Electricity Supply Pension SchemeNational Grid UK Pension SchemeNational Pensions Reserve Fund of IrelandNational Union of Public and General Employees (NUPGE)NATIXISNedbank LimitedNeedmor FundNEI InvestmentsNelson Capital Management, LLCNest SammelstiftungNeuberger BermanNew Amsterdam Partners LLCNew Mexico State TreasurerNew York City Employees Retirement SystemNew York City Teachers Retirement SystemNew York State Common Retirement Fund (NYSCRF)New Zealand Earthquake CommissionNewton Investment Management LimitedNGS SuperNH-CA Asset ManagementNikko Asset Management Co., Ltd.Nikko Cordial SecuritiesNissay Asset Management CorporationNORD/LB Kapitalanlagegesellschaft AGNordea Investment ManagementNorfolk Pension FundNorges Bank Investment Management (NBIM)North Carolina Retirement SystemNorthern Ireland Local Government Officers’ Superannuation Committee (NILGOSC)

Northern TrustNykreditOddo & CieOECO Capital Lebensversicherung AGOld Mutual plcOMERS Administration CorporationOntario Teachers’ Pension PlanOP Fund Management Company LtdOppenheim Fonds Trust GmbHOpplysningsvesenets fond (The Norwegian Church Endowment)OPSEU Pension TrustOregon State TreasurerOrion Asset Management LLCParnassus InvestmentsPax World FundsPensioenfonds VervoerPension DenmarkPension Fund for Danish Lawyers and EconomistsPension Protection FundPensionsmyndighetenPETROS - The Fundação Petrobras de Seguridade SocialPFA PensionPGGMPhillips, Hager & North Investment Management Ltd.PhiTrust Active InvestorsPhoenix Asset Management Inc.Pictet Asset Management SAPKAPluris Sustainable Investments SAPNC Financial Services Group, Inc.Pohjola Asset Management LtdPortfolio 21 InvestmentsPorto Seguro S.A.PREVHAB PREVIDÊNCIA COMPLEMENTARPREVI Caixa de Previdência dos Funcionários do Banco do BrasilPREVIG Sociedade de Previdência ComplementarProvinzial Rheinland HoldingPrudential Investment ManagementPsagot Investment House LtdPSP InvestmentsPSS - Seguridade SocialQ Capital Partners Co. LtdQBE Insurance GroupRabobankRaiffeisen SchweizRailpen InvestmentsRathbones / Rathbone Greenbank InvestmentsReal Grandeza Fundação de Previdência e Assistência SocialRei SuperReliance Capital LtdResolutionResona Bank, LimitedReynders McVeigh Capital ManagementRLAMRobecoRockefeller Financial Rose Foundation for Communities and the EnvironmentRoyal Bank of CanadaRoyal Bank of Scotland GroupRREEF Investment GmbHSAM GroupSAMPENSION KP LIVSFORSIKRING A/SSAMSUNG FIRE & MARINE INSURANCESamsung SecuritiesSanlamSanta Fé Portfolios LtdaSAS Trustee CorporationSauren Finanzdienstleistungen GmbH & Co. KGSchrodersScotiabankScottish Widows Investment PartnershipSEBSEB Asset Management AGSecond Swedish National Pension Fund (AP2)SEIU Master TrustSeligson & Co Fund Management PlcSentinel InvestmentsSERPROS - Fundo MultipatrocinadoSeventh Swedish National Pension Fund (AP7)Shinhan Bank

Carbon Disclosure Project 2011 – Italy 100 Report

5

Shinhan BNP Paribas Investment Trust Management Co., LtdShinkin Asset Management Co., LtdSiemens Kapitalanlagegesellschaft mbHSignet Capital Management LtdSMBC Friend Securities Co., LTDSmith Pierce, LLCSNS Asset ManagementSocial(k)Sociedade de Previdencia Complementar da Dataprev - PrevdataSolaris Investment Management LimitedSompo Japan Insurance Inc.Sopher Investment ManagementSPF Beheer bvSprucegrove Investment Management LtdStandard CharteredStandard Chartered Korea LimitedStandard Life InvestmentsState Bank of IndiaState Street CorporationStatewideSuperStoreBrand ASAStrathclyde Pension FundStratus GroupSumitomo Mitsui Banking CorporationSumitomo Mitsui Card Company, LimitedSumitomo Mitsui Finance & Leasing Co., LtdSumitomo Mitsui Financial GroupThe Sumitomo Trust & Banking Co., Ltd.Sun Life Financial Inc.Superfund Asset Management GmbHSUSI Partners AGSustainable CapitalSvenska Kyrkan, Church of SwedenSwedbank ABSwiss ReSwisscanto Holding AGSyntrus Achmea Asset ManagementT. Rowe PriceT. SINAI KALKINMA BANKASI A.S.T.GARANTI BANKASI A.S.Tata Capital Limited TD Asset Management Inc. and TDAM USA Inc.Teachers Insurance and Annuity Association – College Retirement Equities Fund (TIAA-CREF)Telluride AssociationTempis Asset Management Co. LtdTerra Forvaltning ASTerraVerde Capital Management LLCThe Brainerd FoundationThe Bullitt FoundationThe Central Church Fund of FinlandThe Collins FoundationThe Co-operative Asset ManagementThe Co-operators Group LtdThe Daly FoundationThe GPT GroupThe Hartford Financial Services Group, Inc.The Japan Research Institute, LimitedThe Joseph Rowntree Charitable TrustThe Local Government Pensions InstitutionThe Pension Plan For Employees of the Public Service Alliance of CanadaThe Pinch GroupThe Presbyterian Church in CanadaThe Russell Family FoundationThe Shiga Bank, Ltd.The Standard Bank GroupThe United Church of Canada - General CouncilThe University of Edinburgh Endowment FundThe Wellcome TrustThird Swedish National Pension Fund (AP3)Threadneedle Asset ManagementTokio Marine & Nichido Fire Insurance Co., Ltd.Toronto Atmospheric FundTrillium Asset Management CorporationTriodos Investment ManagementTrygUBSUniCredit GroupUnion Asset Management Holding AG

UnipensionUNISON staff pension schemeUniSuperUnitarian Universalist AssociationUnited Methodist Church General Board of Pension and Health BenefitsUnited Nations FoundationUniversities Superannuation Scheme (USS)Vancity Group of CompaniesVCH Vermögensverwaltung AGVeris Wealth PartnersVeritas Investment Trust GmbHVermont State TreasurerVexiom Capital, L.P.VicSuper Pty LtdVictorian Funds Management CorporationVietNam Holding Ltd.Vision SuperVOLKSBANK INVESTMENTSWaikato Community Trust IncWalden Asset Management, a division of Boston Trust & Investment Management CompanyWARBURG - HENDERSON Kapitalanlagegesellschaft für Immobilien mbHWARBURG INVEST KAPITALANLAGEGESELLSCHAFT MBHWells Fargo & CompanyWest Yorkshire Pension FundWestLB Mellon Asset Management (WMAM)Westpac Banking CorporationWhite Owl Capital AGWinslow Management, A Brown Advisory Investment GroupWoori BankWoori Investment & Securities Co., Ltd.YES BANK LimitedYork University Pension FundYouville Provident Fund Inc.Zegora Investment ManagementZevin Asset ManagementZurich Cantonal Bank

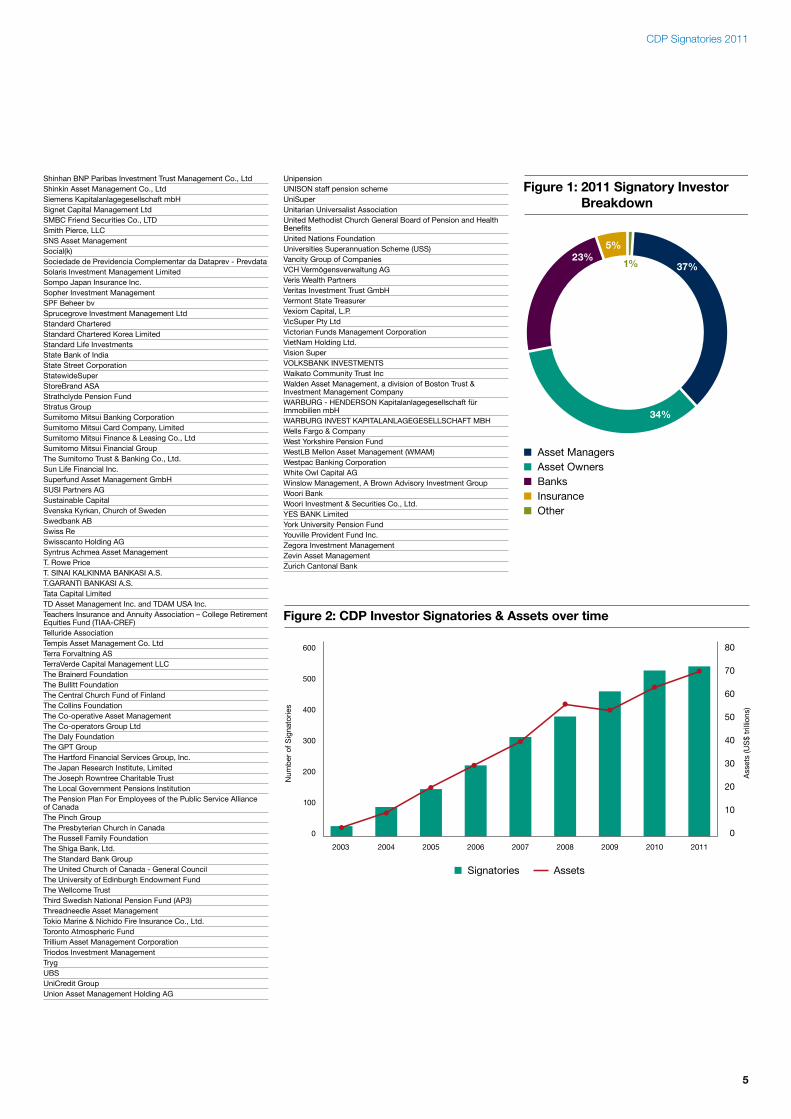

CDP Signatories 2011

Figure 1: 2011 Signatory Investor Breakdown

Asset ManagersAsset OwnersBanksInsuranceOther

1% 37%

5%23%

34%

Figure 2: CDP Investor Signatories & Assets over time

600

500

400

300

200

100

0

80

70

60

50

40

30

20

10

0

Num

ber

of S

igna

torie

s

Ass

ets

(US

$ tr

illio

ns)

Signatories Assets

2003 2004 2005 2006 2007 2008 2009 2010 2011

6

7

2011 Carbon Disclosure Project 2Investor Members

2011 Carbon Disclosure Project 3Investor Signatories

CEO Foreword 8

Accenture Foreword 9

Executive Summary 10

Key Themes 12

Analysis of Responses 15

2011 Carbon Leaders 17

Results 23

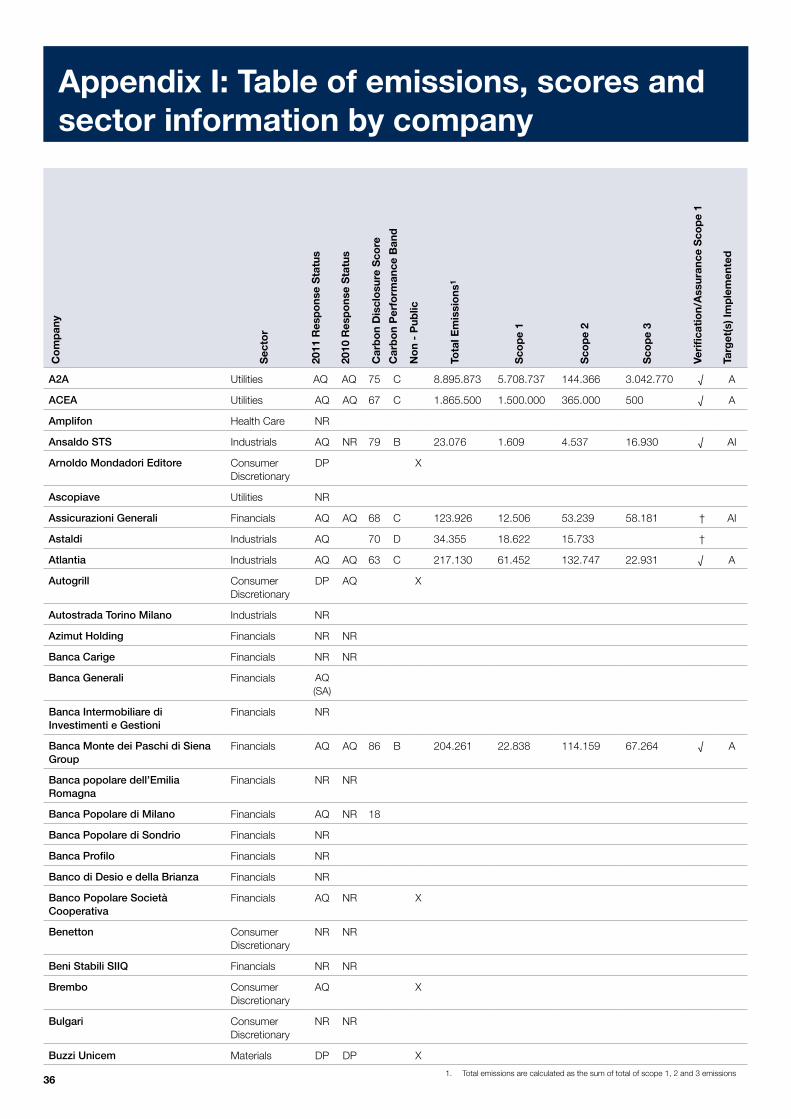

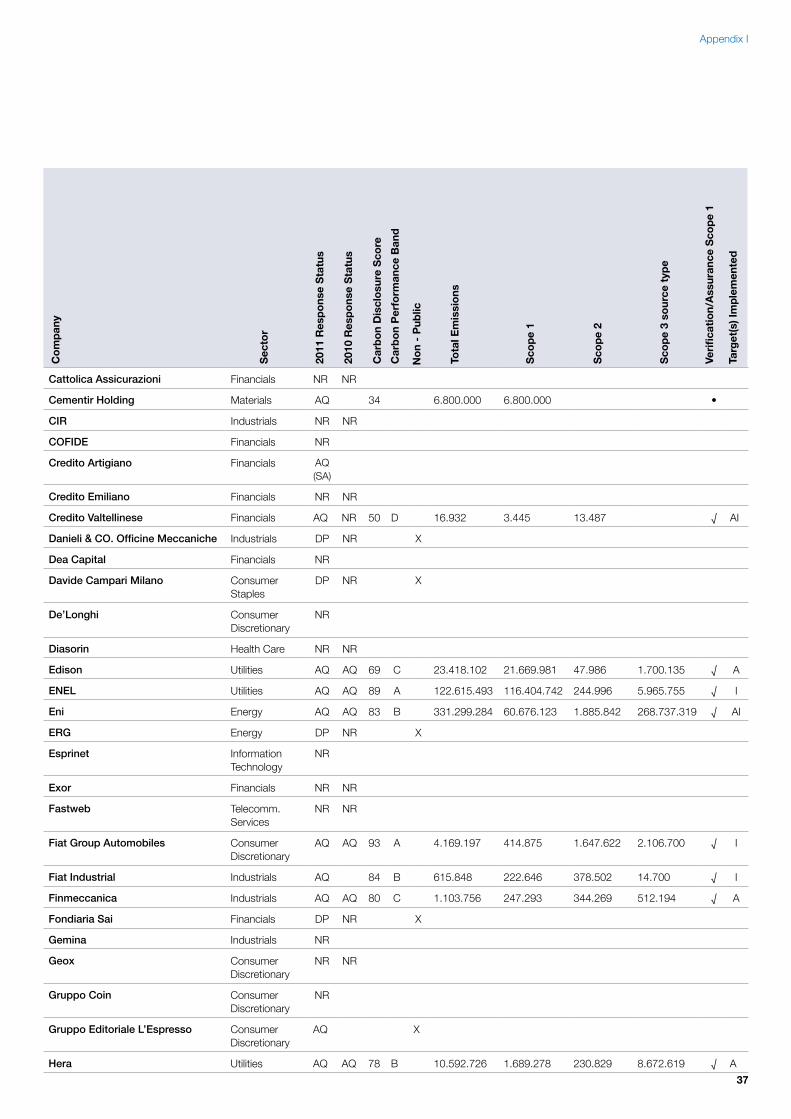

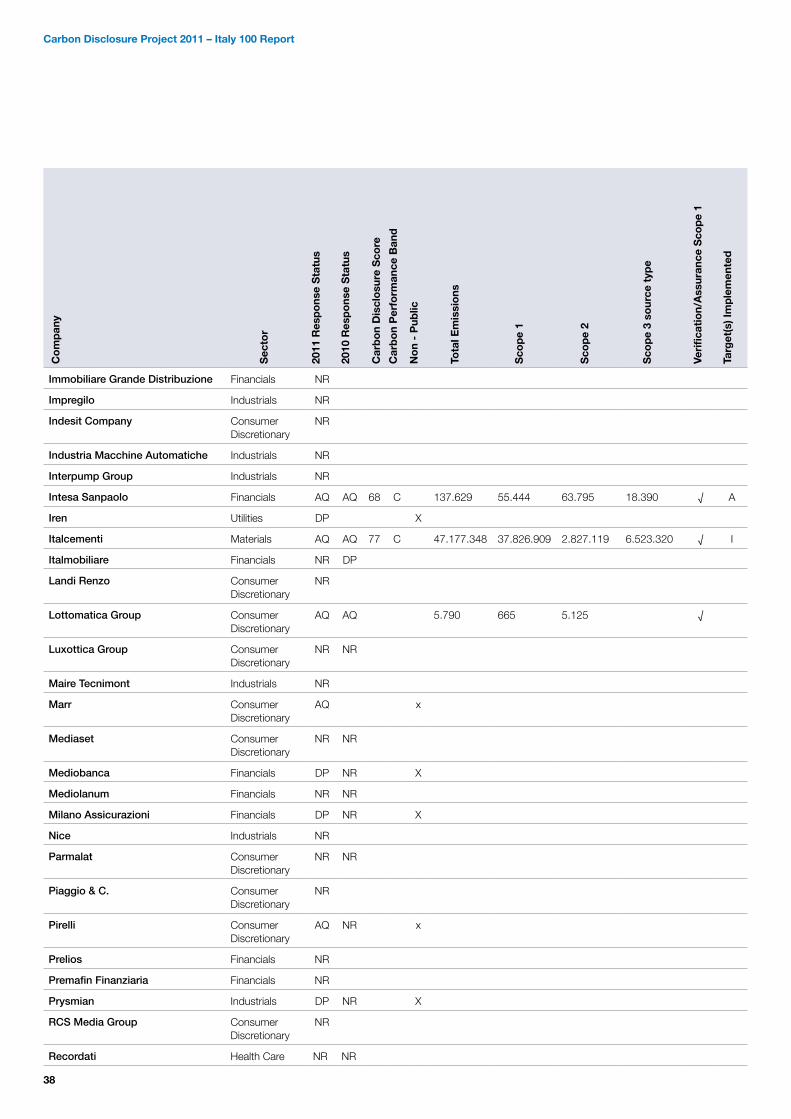

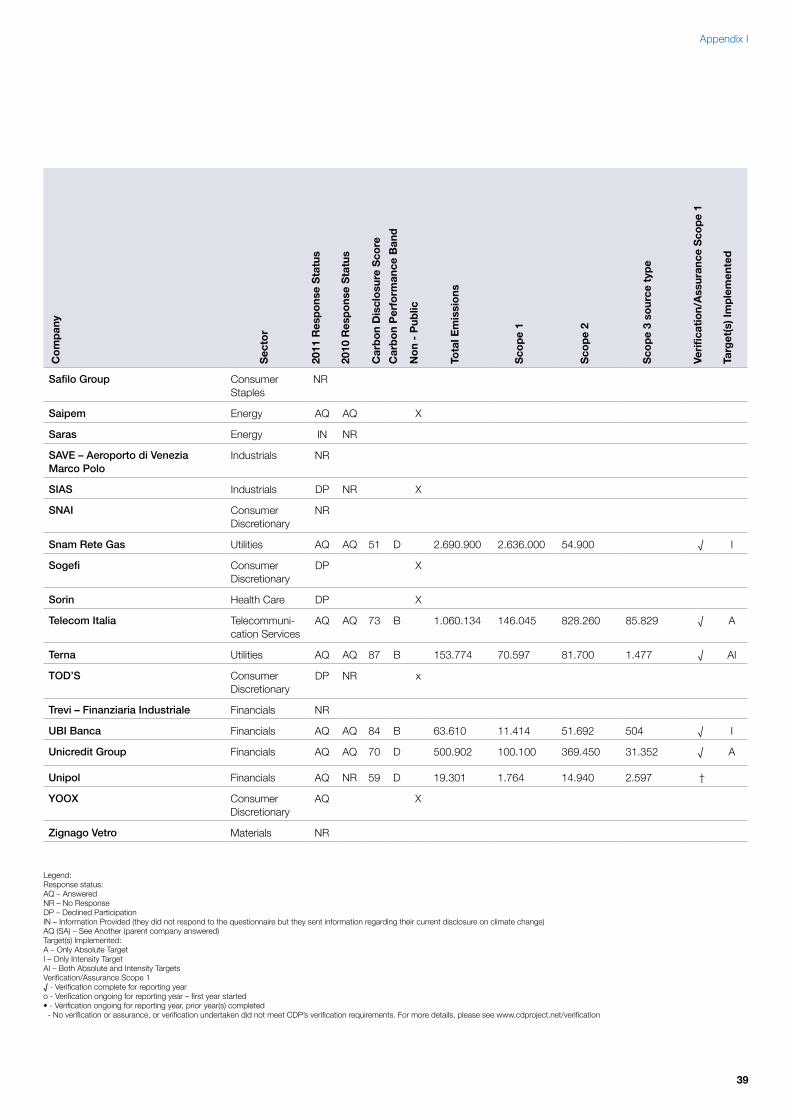

Appendix I: 36Table of emissions

Appendix II: 41Key trends

Appendix III: 43Investor CDP request 2011

Contents

8

Corporations, investors and governments today are faced with a choice: to compete aggressively for finite resources, or to advance towards a low carbon economy that enables sustainable, profitable growth, whilst reducing reliance on increasingly scarce materials.

Last year, global energy-related carbon dioxide emissions reached a record high. The International Energy Agency’s estimates made for bleak reading but compounded the necessity to take bold and decisive action if we are to have any chance of limiting temperature increase to the 2°C level agreed by world leaders to protect against catastrophic climate change.

What’s more, rising energy demands are competing for a limited supply of fossil fuels. The competition for increasingly scarce natural resources is putting pressure on commodity prices and having a growing impact both socially and economically. It is clear that today, more than ever, we must build momentum to decouple economic growth from emissions.

Managing carbon emissions and protecting business from climate change impacts are fundamental to achieving sustainable and strong shareholder returns. Earlier this year, the investment consultancy Mercer released a report concluding that the best way for institutional investors to manage portfolio risk associated with climate change may be to shift 40% of their portfolios into climate-sensitive assets with an emphasis on those that can adapt to a low carbon environment.

An important part of investors’ strategy should be to engage with the companies in which they invest to encourage performance improvement. Carbon Action is a new initiative launched by CDP this year. It is driven by a leading group of investors to encourage their portfolio companies to reduce emissions by investing in emissions’ reduction activities with a satisfactory payback period. Carbon Action reflects a growing recognition that there is a huge range of carbon reduction activities that companies can undertake and which have a very clear business case. It is therefore in the interests of all investors, and not just the more active owners of investments, to ensure these actions are taken.

As the management of carbon continues to move into companies’ core business strategies and mainstream investment thinking, demand for primary corporate climate change information grows around the world. As well as working on behalf of 551 institutional investors to gather relevant information from large corporations around the world, CDP is also working with global businesses and governments to strengthen the resilience and sustainability of their supply chains through the CDP Supply Chain program. CDP Cities has been launched to help the world’s major cities reduce climate change risk and bolster economic growth, whilst CDP Water Disclosure is now in its second year of working with major global companies to improve water management. A key part of CDP’s strategy is to ensure the effective use of data collected. To assist with this companies are able to obtain tools that help them to measure, report and manage carbon more effectively through CDP Reporter Services.

It is through partnerships that CDP can achieve the greatest impact. In Italy we are delighted to be working with our local partners: Accenture SpA, Banca Monte dei Paschi di Siena and Kyoto Club. In addition, we highly value the continued support of our Global Advisor, PwC, as well as that of Accenture, Microsoft, SAP and Bloomberg. These and our other partners around the world are integral to the acceleration of CDP’s mission.

Whilst we wait patiently for much needed global regulation, business must continue to forge ahead, innovate and seek out opportunities by doing more with less. The decisions that perpetuate a legitimate, low carbon and high growth economy will bring considerable value to those who have the foresight to make them. The information contained in this report and the companies’ responses assist in illuminating that path.

Paul SimpsonCEOCarbon Disclosure Project

CEO Foreword

CEO Foreword

9

In the last 3 years we at Accenture have witnessed, in our day to day work with our clients, an increasing commitment from Italian companies towards sustainability and carbon management.

This increased commitment is strongly represented in the results of this year’s Italy CDP Investor program: the number of responding companies rose from 18 in 2009 to 35 in 2011. Numbers talk: 82% of responding companies declared that they have integrated climate change in their business strategy. 91% reported having emissions’ reduction initiatives in place. 67% set a carbon reduction target. 88% declared they have assigned responsibility for carbon management at least to senior management level. And, most importantly, 42% declared that they have reduced their emissions.

These figures tell a story of very significant commitment and improvement. Nevertheless, when compared to European 300 and Global 500 companies’ results, the evidence is that Italian companies are somewhat lagging behind and show some room for improvement.

We are also committed to disclosure and improvement of our carbon performance. To that extent we have been disclosing our climate change commitment in the most recent five years through the CDP Investor program and in the last three years also through the CDP Supply Chain program. We share with our clients a commitment to sustainability and we are glad to be in partnership with leading global organizations tackling the integration of sustainability in business practices, among them: United Nations Global Compact, the World Business Council for Sustainable Development, the World Economic Forum and, of course, CDP.

Accenture’s global partnership with CDP dates back to 2009 when, in cooperation with SAP and Microsoft, we supported the implementation of a new Global Climate Change Data and Reporting Platform to collect, manage and disseminate climate change data. In 2010 Accenture partnered with the CDP on the preparation of a White Paper highlighting the benefits of disclosing cities’ climate change related information.

In addition to this global partnership, we are also proud to be a strategic partner in Italy for the first time this year. Accenture is pleased to have supported the CDP in preparing the CDP Investor Report 2011 for Italy and, in particular, to have contributed to increasing the number of respondent companies from 21 in 2010 to 35. This report is the first product of a collaboration that we hope will intensify in the coming years.

Mauro Marchiaro Managing Director ResourcesItaly, Greece, Central & Eastern Europe, Russia, Middle East

Accenture Foreword

Accenture Foreword

10

Executive Summary

CDP overview

CDP is an independent not-for-profit organization that has been working, since 2000, to collect companies’ data on climate change strategy, GHG emissions’ disclosure and water use. The CDP was founded to put information on companies’ climate change strategies and GHG emissions management at the heart of financial and policy decision-making. The authority behind CDP’s information request lies in its list of investor signatories which has grown from 35 investors with assets of US$4.5 trillion under management in 2003 to 551 in 2011 with assets of US$71 trillion under management.

CDP conveys the information to its 551 investor signatories, as well as distributing it throughout the global market place, both to increase transparency around climate-related investment risk and commercial opportunity and to drive investment towards a low carbon economy. In order to better assess and compare companies’ responses, CDP developed a methodology that scores companies on the quality of their disclosure and performance on actions they take to mitigate climate change. The highest scoring companies per sample are recognized in two indexes: the Carbon Disclosure Leadership Index (CDLI) and the Carbon Performance Leadership Index (CPLI). In 2011 more than 3,000 companies have been scored according to the CDP methodology, making CDP the largest existing database for corporate climate data.

CDP 2011 in Italy

This report will especially focus on carbon measurement and reporting - the crucial first steps towards carbon management and the backbone to any robust and credible carbon strategy - and emission reduction initiatives.

The Italian companies invited to respond to CDP 2011 are the 100 largest companies, by market capitalization, on the Italian stock exchange. The first country specific report was published in 2008 with responses from 18 companies, managing more than 220 MtCO2e. The current report represents the management of almost 258 MtCO2e (Scope 1 emissions) from 35 companies.

Companies were scored according to the CDP methodology explained in the CDP 2011 Reporting Guidance and available to all through the CDP website. Kyoto Club is the scorer for the Italy 100 sample.

Overview of results

The number of Italian companies responding to CDP has increased significantly, from 21 in 2010 to 35 in 2011. The increased number of respondents of course adds value to the overall results, making the sample more representative. Nevertheless the response rate (35%) has not increased. The highest response rate in the Italy 100 sample comes from the Utility sector followed by the Energy, Materials and Telecommunications sectors.

Management

Most companies declare that climate change has been integrated into the fundamental pillars of management: overall strategy, risk management and employees’ reward. Responsibility for climate change management is assigned, in almost all responding companies (29), at least to senior management level, proving that basic sustainability practices such as carbon reporting are becoming integrated into the way business is done, both strategically and operationally. One of the questions in the CDP 2011 asks whether climate change is integrated in business strategy: 82% (27) of companies responding answered in the affirmative.

Calculation and reporting of carbon emissions have become common practice, but only few companies provide data on non CO2 GHG emissions. Third party verification/assurance has also become common: 24 companies have some verification on Scope 1 emissions.

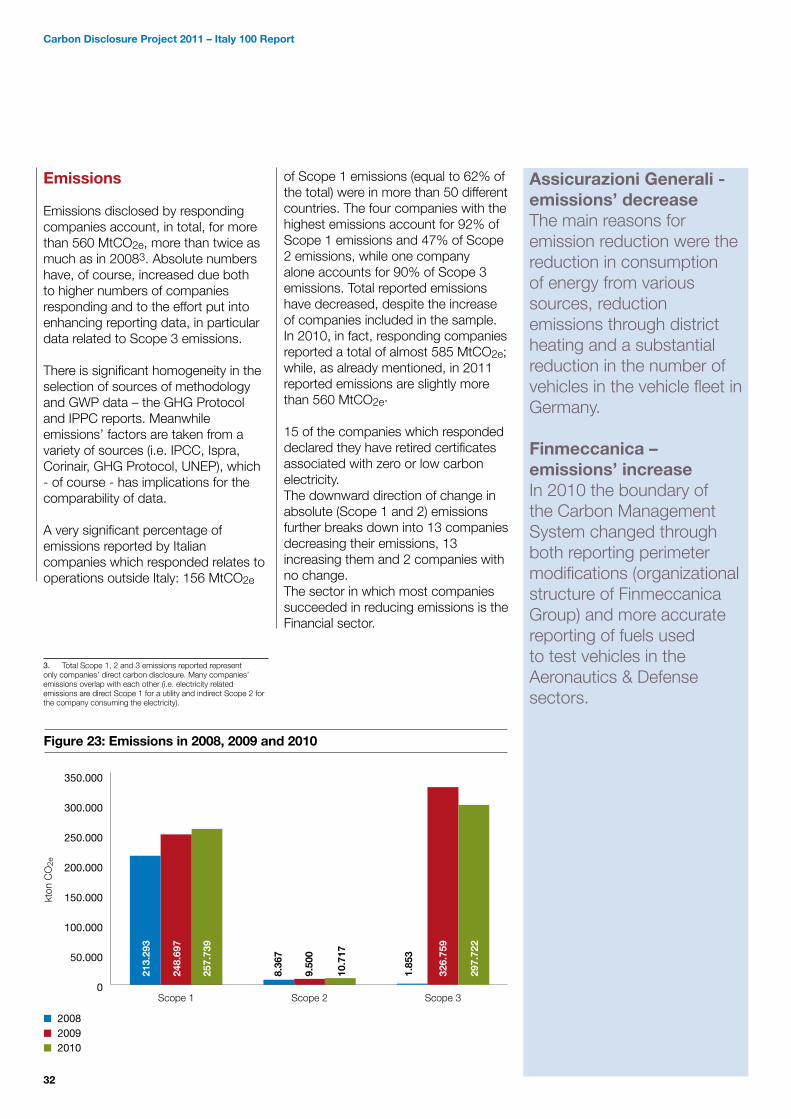

Companies in the Italy 100 sample report almost 258 MtCO2e of Scope 1 emissions and almost 11 MtCO2e of Scope 2 emissions. Both values are in line with last year (249 MtCO2e for Scope 1 and 9.5 MtCO2e for Scope 2). Scope 3 emissions count for about 300 MtCO2e, 10% less than last year.

As far as performance is concerned, responding companies are almost equally divided between those which succeeded in decreasing their emissions and those whose emissions increased in 2011. When significant decreases have been reported these are in most cases the result of specific reduction initiatives, while increases are due to changes in both company reporting and system boundaries. 91% (30) of responding companies reported having emissions’ reduction initiatives in place. This is higher than the proportion of companies with an emissions reduction target (67%): it seems that the importance of reducing emissions is somehow translated into actions before becoming a formal commitment. 186 emissions’ reduction initiatives (mainly related to energy efficiency, transportation and low carbon energy) have been reported.

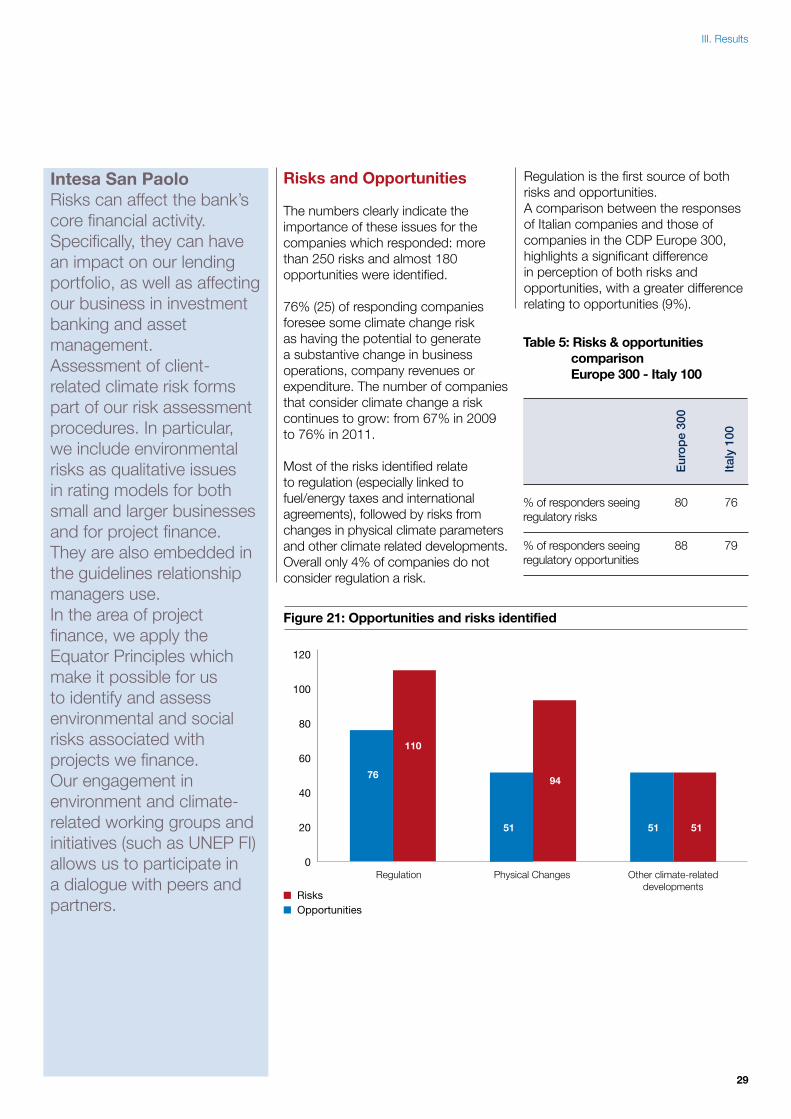

Risks and Opportunities

79% (26) of companies consider climate change is a source of opportunities related to regulation, changes in physical parameters and other possible climate-related developments. Regulation is the most important driver for both risks and opportunities. Companies identify more than 250 different risk events related to climate change, with 10 companies – from 5 different sectors – foreseeing

11

the inability to do business at all, as one of them. Of the 178 opportunities identified, the increase in demand for existing products, as well as the creation of new products/ business services, are the two most significant.

Emissions

Only four companies have not published any information on their GHG emissions performance. The norm for the vast majority of responding companies is to disclose their GHG emissions performance in several company documents (such as annual report, regulatory filings and voluntary communications).

A final appraisal of companies’ responses highlights the trend that Italian companies are shifting from the traditional paradigm of considering climate change only as a compliance and risk driven issue, to a new paradigm that regards climate change also as an accelerator of business performance and value creation. Commitment to defining and implementing emissions’ reduction initiatives is very high, as demonstrated by the data. Nevertheless only half of the companies adopt traditional financial analysis and metrics to back up these initiatives and assess their overall financial impact: another sign that a course towards carbon management integration has been set, but there is still work to be done.

CDLI and CPLI overview of results

Ten companies (Ansaldo STS, Banca Monte dei Paschi di Siena, Enel, Eni, Fiat, Fiat Industrials, Finmeccanica, Hera, Terna and UBI Banca) are included in the CDLI for the Italy 100 and two companies (Enel and Fiat) have made CPLI for the Italy 100.

Compared to last year, the average disclosure score for companies in the CDLI has increased (84 in 2011 vs. 80 in 2010), while the average disclosure score among all responding companies is stable (63 both in 2010 and in 2011).

Executive Summary

12

Key ThemesEmanuele Cacciatore – Senior Manager, Accenture

Integrating Sustainability into Business As Usual

82% (27) of Italian companies responding to the CDP 2011 information request reported that they have integrated climate change into core business strategy

Right in the middle of an economic recession, with the European economy struggling to solve the sovereign debt crisis, pressure on organizations to drive corporate action on sustainability issues has not weakened at all. Policy makers, institutional investors and customers are scrutinizing firms’ corporate behavior more carefully than ever, demanding greater accountability and performance from business in providing positive contributions to the economy, society and the environment. Corporations that wish to future proof their business must establish capacity to report coherently to stakeholders on the implications of sustainability for their economic and financial performance. The integration of sustainability into corporate strategy is now a key issue on many CEOs’ agenda.

Results from Accenture 2010 UN Global Compact CEOs Study had already highlighted how the economic downturn has raised the importance of sustainability as a leadership issue for top Italian managers (91% of Italian CEOs interviewed agree on that). 72% stated that the crisis had already led Italian companies to increase alignment of core business strategies with sustainability issues. One of the most eye-catching pieces of evidence from the study was that 100% of CEOs state that sustainability issues should be fully embedded into a company’s strategy and operations. More interestingly still, the gap between statements of intent and actual practice was remarkably low: 82% of respondents, in fact, confirmed that these issues were in reality fully

embedded into the strategy and operations of their companies. It is worth noting that 82% (27) Italian companies responding to the CDP information request in 2011 report that they have integrated climate change into their core business strategy and that they have increased the level of involvement and accountability of senior management in managing climate change related issues. A survey on sustainability performance management, conducted this year by Accenture among leading Italian companies to assess the level of integration of sustainability into business as usual, confirms that management of sustainability has advanced to a significant degree of integration with corporate strategy and strategic direction. That survey also highlighted that well-functioning measurement and surrounding processes have been established, although not yet integrated, into traditional enterprise performance management processes and systems. Emission Reduction Targets and Initiatives

Despite an increase in the absolute number of companies with emissions’ reduction targets, from 16 to 22 in 2011, the percentage of responding companies with emissions’ reduction targets has decreased: 67% (22) of respondents disclose absolute or intensity emission reduction targets, a decrease from 76% of respondents in 2010

67% (22) of responding companies have set an emission reduction target for the current fiscal year, compared to 76% (16) in 2010: this translates to a decrease of 9% from last year. Among those which report reduction targets, 90% of companies have set a target within the next five years. Only A2A, Edison and Unicredit have disclosed reduction targets addressing the next ten years to 2020.

“In Pukrang, Thailand, a waste heat recovery (WHR) system will be built into the current plant structure. Heat recovered from the kiln will be used to generate electricity fed to the grid. An installed capacity of 18MW is foreseen corresponding to a 70 ktonCO2 annual reduction in emissions.”Italcementi

“Even in a context such as the current one, we cannot forget that we must develop our business by acting responsibly, as we know that sustainability is the key to our future and the future of our children. Environmental protection is for us not only a commitment but also a significant business opportunity.”Unicredit Group

13

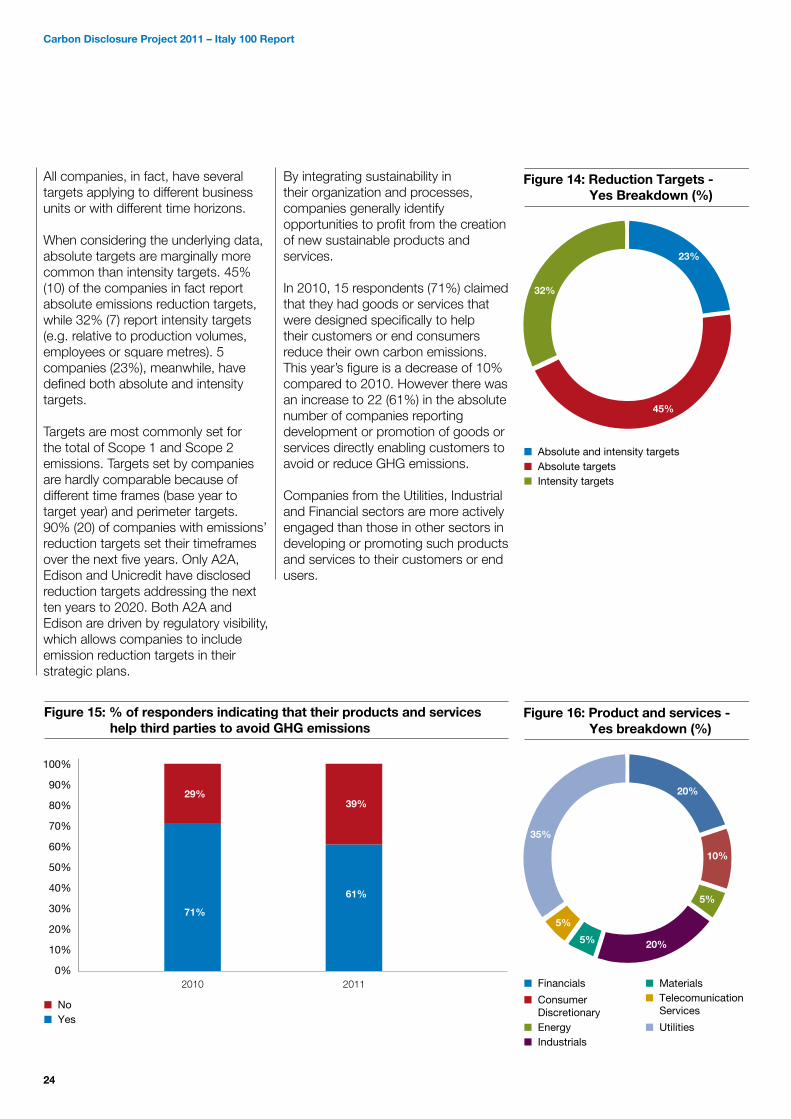

Absolute targets are marginally more common than intensity targets.

100% (22) of companies reporting reduction targets for the current fiscal year have defined more than one numeric emission reduction target. All companies, in fact, have several targets applying to different business units or with different time horizons.

When considering the underlying data, absolute targets are marginally more common than intensity targets. 45% of targets (set by 10 companies) include absolute emissions’ reductions, while 32% (set by 7 companies) are intensity targets (e.g. relating to production volumes, employees or square metres). The remaining 23% relate to 5 companies that set both absolute and intensity targets.

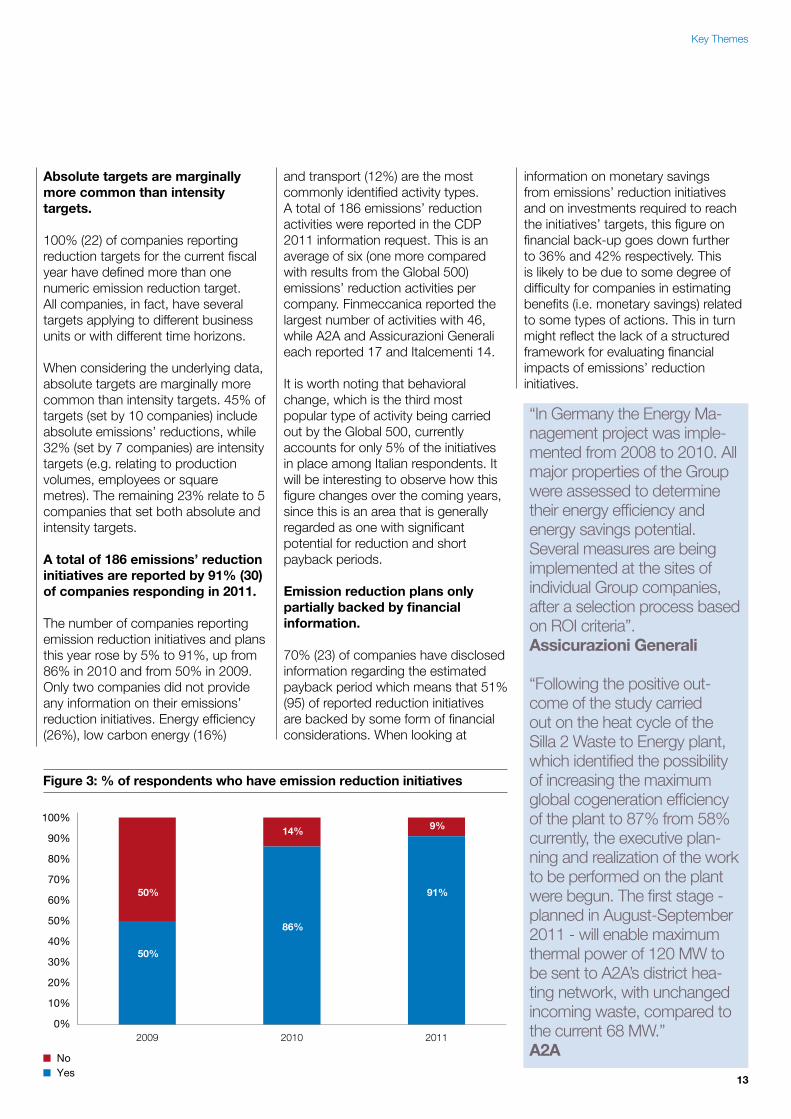

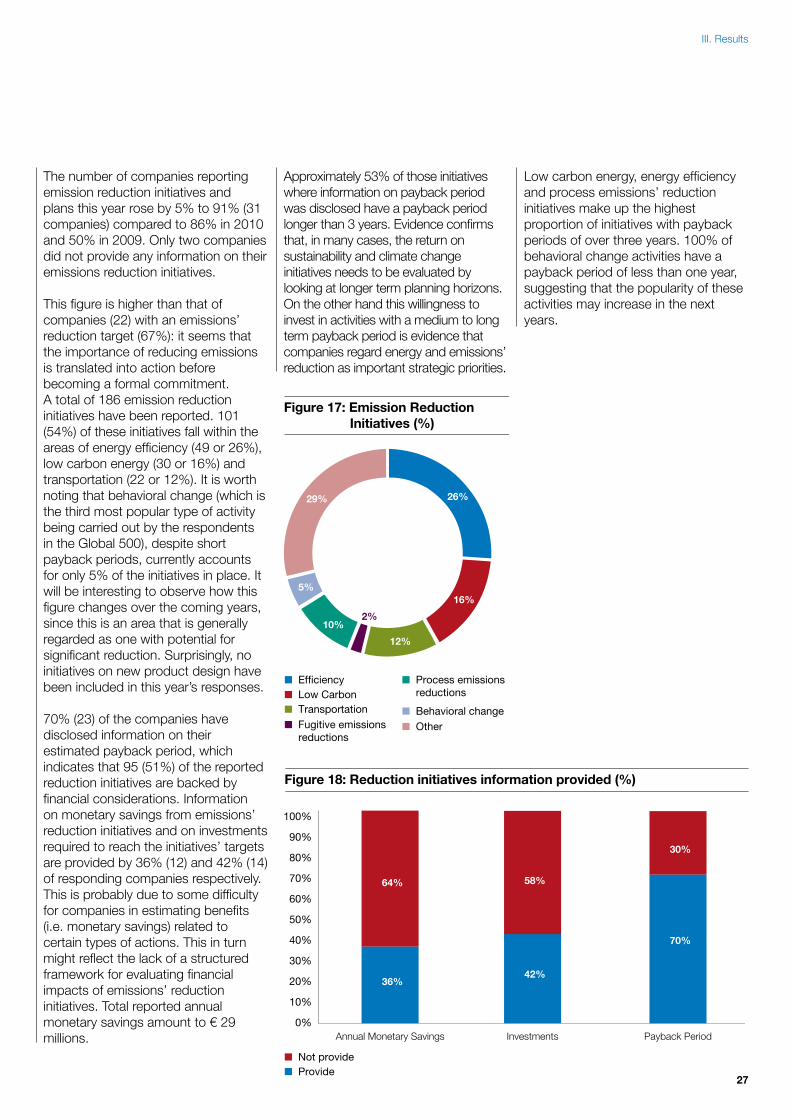

A total of 186 emissions’ reduction initiatives are reported by 91% (30) of companies responding in 2011.

The number of companies reporting emission reduction initiatives and plans this year rose by 5% to 91%, up from 86% in 2010 and from 50% in 2009. Only two companies did not provide any information on their emissions’ reduction initiatives. Energy efficiency (26%), low carbon energy (16%)

and transport (12%) are the most commonly identified activity types. A total of 186 emissions’ reduction activities were reported in the CDP 2011 information request. This is an average of six (one more compared with results from the Global 500) emissions’ reduction activities per company. Finmeccanica reported the largest number of activities with 46, while A2A and Assicurazioni Generali each reported 17 and Italcementi 14.

It is worth noting that behavioral change, which is the third most popular type of activity being carried out by the Global 500, currently accounts for only 5% of the initiatives in place among Italian respondents. It will be interesting to observe how this figure changes over the coming years, since this is an area that is generally regarded as one with significant potential for reduction and short payback periods.

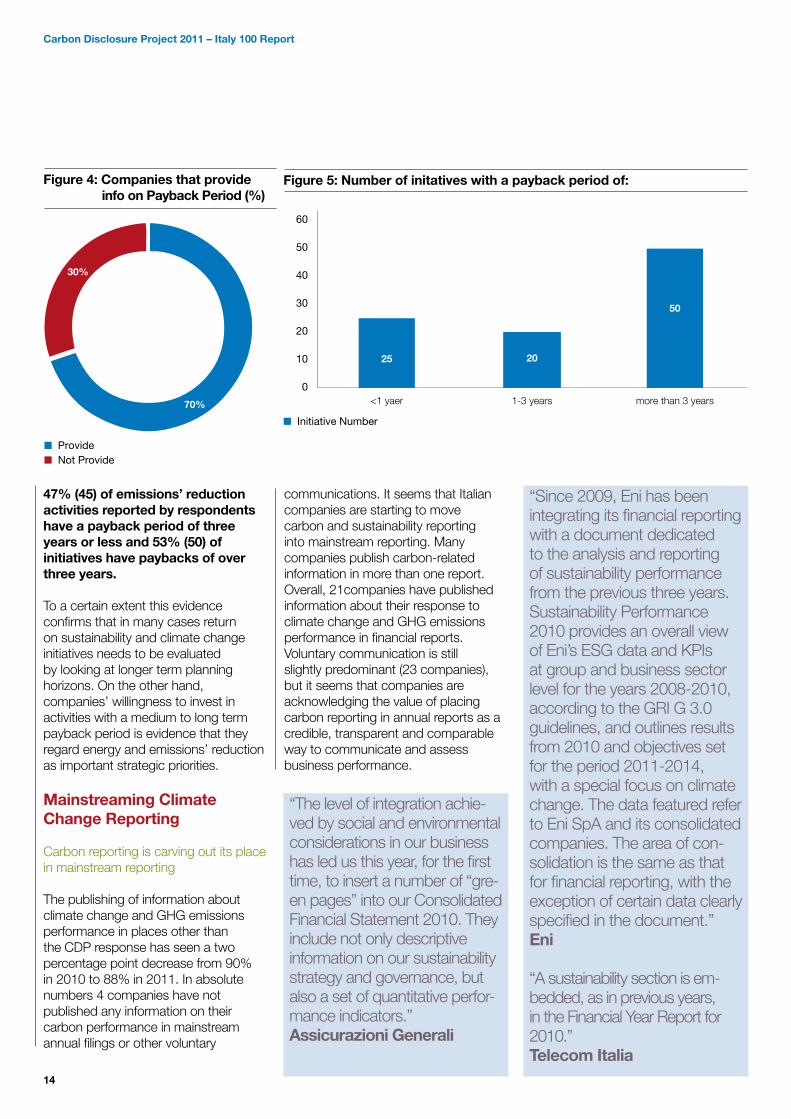

Emission reduction plans only partially backed by financial information.

70% (23) of companies have disclosed information regarding the estimated payback period which means that 51% (95) of reported reduction initiatives are backed by some form of financial considerations. When looking at

information on monetary savings from emissions’ reduction initiatives and on investments required to reach the initiatives’ targets, this figure on financial back-up goes down further to 36% and 42% respectively. This is likely to be due to some degree of difficulty for companies in estimating benefits (i.e. monetary savings) related to some types of actions. This in turn might reflect the lack of a structured framework for evaluating financial impacts of emissions’ reduction initiatives.

“In Germany the Energy Ma-nagement project was imple-mented from 2008 to 2010. All major properties of the Group were assessed to determine their energy efficiency and energy savings potential. Several measures are being implemented at the sites of individual Group companies, after a selection process based on ROI criteria”.Assicurazioni Generali

“Following the positive out-come of the study carried out on the heat cycle of the Silla 2 Waste to Energy plant, which identified the possibility of increasing the maximum global cogeneration efficiency of the plant to 87% from 58% currently, the executive plan-ning and realization of the work to be performed on the plant were begun. The first stage - planned in August-September 2011 - will enable maximum thermal power of 120 MW to be sent to A2A’s district hea-ting network, with unchanged incoming waste, compared to the current 68 MW.”A2A

Figure 3: % of respondents who have emission reduction initiatives

NoYes

50%

50%

2009 2010

14%

86%

2011

9%

91%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Key Themes

14

“Since 2009, Eni has been integrating its financial reporting with a document dedicated to the analysis and reporting of sustainability performance from the previous three years. Sustainability Performance 2010 provides an overall view of Eni’s ESG data and KPIs at group and business sector level for the years 2008-2010, according to the GRI G 3.0 guidelines, and outlines results from 2010 and objectives set for the period 2011-2014, with a special focus on climate change. The data featured refer to Eni SpA and its consolidated companies. The area of con-solidation is the same as that for financial reporting, with the exception of certain data clearly specified in the document.”Eni

“A sustainability section is em-bedded, as in previous years, in the Financial Year Report for 2010.” Telecom Italia

47% (45) of emissions’ reduction activities reported by respondents have a payback period of three years or less and 53% (50) of initiatives have paybacks of over three years.

To a certain extent this evidence confirms that in many cases return on sustainability and climate change initiatives needs to be evaluated by looking at longer term planning horizons. On the other hand, companies’ willingness to invest in activities with a medium to long term payback period is evidence that they regard energy and emissions’ reduction as important strategic priorities.

Mainstreaming Climate Change Reporting

Carbon reporting is carving out its place in mainstream reporting

The publishing of information about climate change and GHG emissions performance in places other than the CDP response has seen a two percentage point decrease from 90% in 2010 to 88% in 2011. In absolute numbers 4 companies have not published any information on their carbon performance in mainstream annual filings or other voluntary

communications. It seems that Italian companies are starting to move carbon and sustainability reporting into mainstream reporting. Many companies publish carbon-related information in more than one report. Overall, 21companies have published information about their response to climate change and GHG emissions performance in financial reports. Voluntary communication is still slightly predominant (23 companies), but it seems that companies are acknowledging the value of placing carbon reporting in annual reports as a credible, transparent and comparable way to communicate and assess business performance.

Figure 4: Companies that provide info on Payback Period (%)

ProvideNot Provide

30%

70%

Figure 5: Number of initatives with a payback period of:

Initiative Number

25

<1 yaer 1-3 years

20

more than 3 years

50

60

50

40

30

20

10

0

Carbon Disclosure Project 2011 – Italy 100 Report

“The level of integration achie-ved by social and environmental considerations in our business has led us this year, for the first time, to insert a number of “gre-en pages” into our Consolidated Financial Statement 2010. They include not only descriptive information on our sustainability strategy and governance, but also a set of quantitative perfor-mance indicators.”Assicurazioni Generali

15

I. Analysis of responses

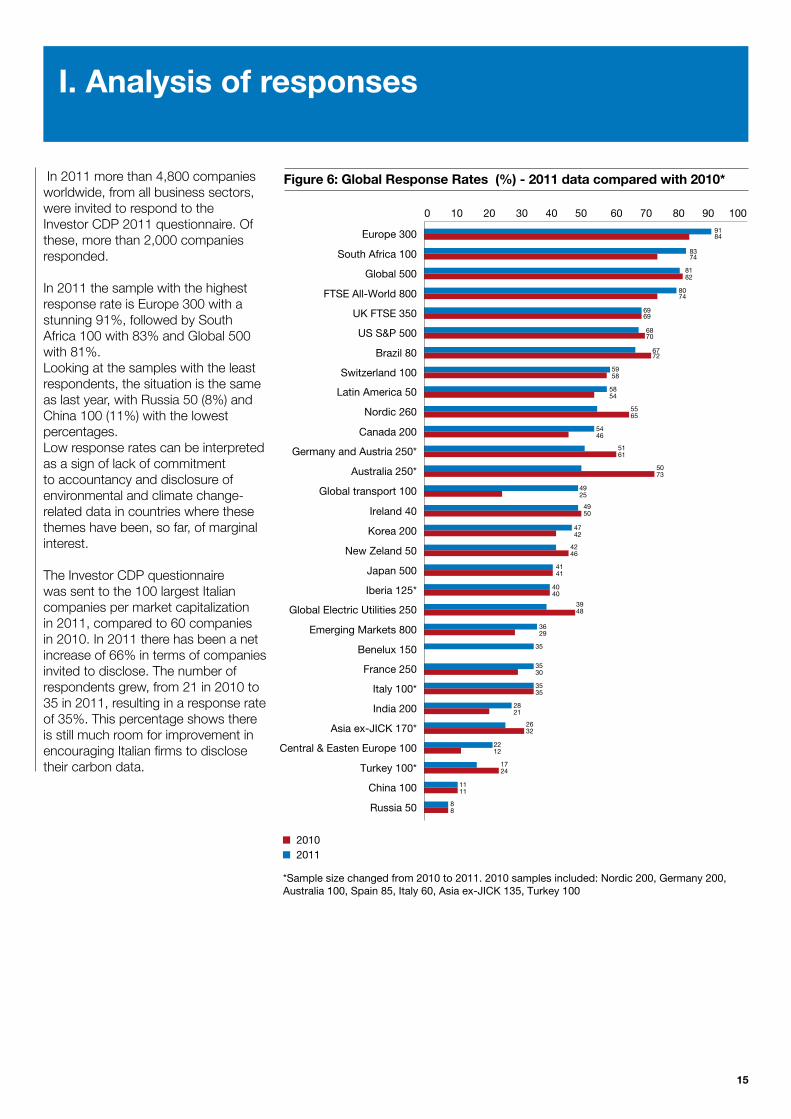

In 2011 more than 4,800 companies worldwide, from all business sectors, were invited to respond to the Investor CDP 2011 questionnaire. Of these, more than 2,000 companies responded.

In 2011 the sample with the highest response rate is Europe 300 with a stunning 91%, followed by South Africa 100 with 83% and Global 500 with 81%. Looking at the samples with the least respondents, the situation is the same as last year, with Russia 50 (8%) and China 100 (11%) with the lowest percentages.Low response rates can be interpreted as a sign of lack of commitment to accountancy and disclosure of environmental and climate change-related data in countries where these themes have been, so far, of marginal interest.

The Investor CDP questionnaire was sent to the 100 largest Italian companies per market capitalization in 2011, compared to 60 companies in 2010. In 2011 there has been a net increase of 66% in terms of companies invited to disclose. The number of respondents grew, from 21 in 2010 to 35 in 2011, resulting in a response rate of 35%. This percentage shows there is still much room for improvement in encouraging Italian firms to disclose their carbon data.

Figure 6: Global Response Rates (%) - 2011 data compared with 2010*

*Sample size changed from 2010 to 2011. 2010 samples included: Nordic 200, Germany 200, Australia 100, Spain 85, Italy 60, Asia ex-JICK 135, Turkey 100

Europe 300

South Africa 100

Global 500

FTSE All-World 800

UK FTSE 350

US S&P 500

Brazil 80

Switzerland 100

Latin America 50

Nordic 260

Canada 200

Germany and Austria 250*

Australia 250*

Global transport 100

Ireland 40

Korea 200

New Zeland 50

Japan 500

Iberia 125*

Global Electric Utilities 250

Emerging Markets 800

Benelux 150

France 250

Italy 100*

India 200

Asia ex-JICK 170*

Central & Easten Europe 100

Turkey 100*

China 100

Russia 50

0 10 20 30 40 50 60 70 80 90 100

9184

8374

8182

8074

6969

6870

6772

5958

5854

5565

5446

5161

5073

4925

4950

4742

4246

4141

4040

3948

3629

35

3530

3535

2821

2632

2212

1724

1111

88

20102011

16

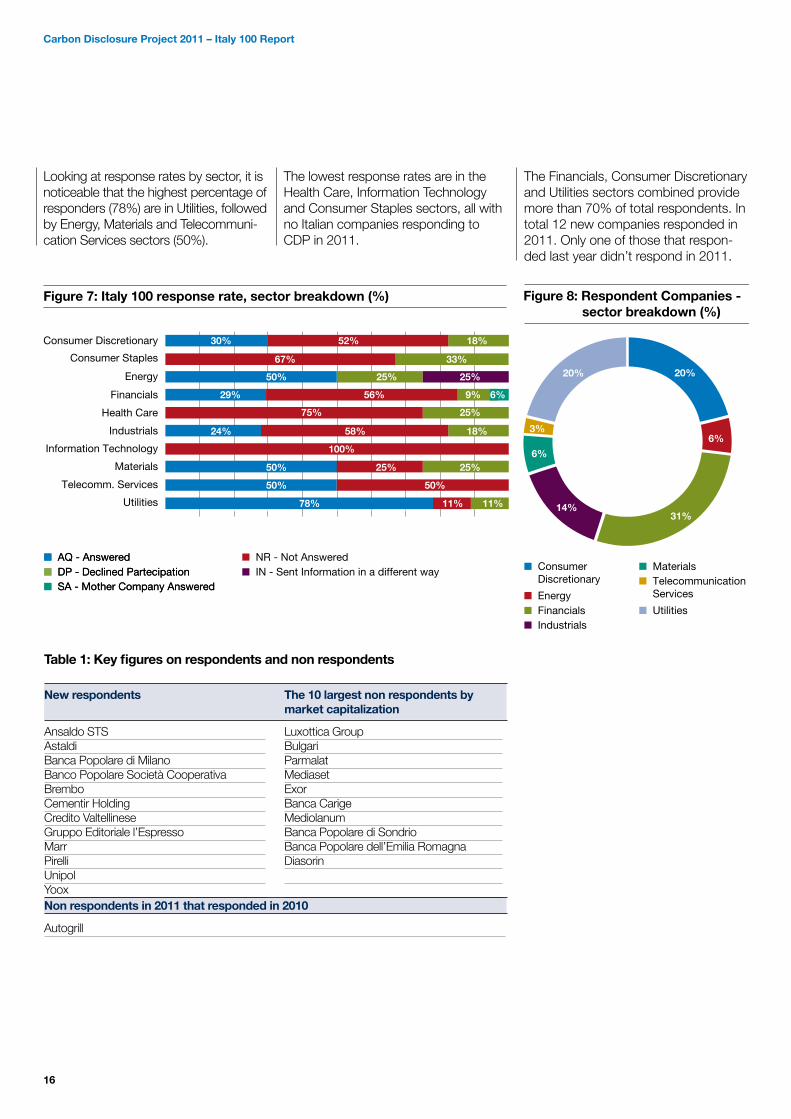

Looking at response rates by sector, it is noticeable that the highest percentage of responders (78%) are in Utilities, followed by Energy, Materials and Telecommuni-cation Services sectors (50%).

The lowest response rates are in the Health Care, Information Technology and Consumer Staples sectors, all with no Italian companies responding to CDP in 2011.

The Financials, Consumer Discretionary and Utilities sectors combined provide more than 70% of total respondents. In total 12 new companies responded in 2011. Only one of those that respon-ded last year didn’t respond in 2011.

Table 1: Key figures on respondents and non respondents

New respondents

Ansaldo STSAstaldiBanca Popolare di MilanoBanco Popolare Società CooperativaBremboCementir HoldingCredito ValtellineseGruppo Editoriale l’EspressoMarrPirelliUnipolYoox

The 10 largest non respondents by market capitalization

Luxottica GroupBulgariParmalatMediasetExorBanca CarigeMediolanumBanca Popolare di SondrioBanca Popolare dell’Emilia RomagnaDiasorin

Non respondents in 2011 that responded in 2010

Autogrill

AQ - AnsweredDP - Declined PartecipationSA - Mother Company Answered

Figure 7: Italy 100 response rate, sector breakdown (%)

AQ - AnsweredDP - Declined PartecipationSA - Mother Company Answered

NR - Not AnsweredIN - Sent Information in a different way

Consumer Staples 67% 33%

Information Technology 100%

Health Care 75% 25%

Utilities 78% 11% 11%

Telecomm. Services 50% 50%

Materials 50% 25% 25%

Industrials 24% 58% 18%

Energy 50% 25% 25%

Consumer Discretionary 30% 52% 18%

Financials 29% 56% 9% 6%

Figure 8: Respondent Companies - sector breakdown (%)

Consumer Discretionary

Energy

20% 20%

6%

31%14%

6%

3%

FinancialsIndustrials

MaterialsTelecommunication Services

Utilities

Carbon Disclosure Project 2011 – Italy 100 Report

17

II. 2011 Carbon leaders

Introduction to the Carbon Disclosure Leadership Index (CDLI) and the Carbon Performance Leadership Index (CPLI)

Each year, company responses are reviewed, analyzed and scored for the quality of disclosure and performance on actions taken to mitigate climate change. This results in a disclosure score and, where sufficient disclosure exists, a performance score.

Disclosure scores • Disclosure scores are anassessment of the quality and completeness of a company’s response; they are not a measure of a company’s performance in relation to climate change management

• Scores are plotted over a 100-point normalized scale

• Companies are assessed based on their level of disclosure of carbon emissions measurement techniques and subsequent public disclosure

• Companies with the highest disclosure scores are listed in the CDLI

Performance bands • Where a company’s disclosure score is 50 or more, its performance in contributing to climate change mitigation, adaptation and transparency is assessed and ranked in a performance band

• In 2011 there are six performance bands (there were four bands in 2010)

• Companies with the highest performance bands that meet additional CPLI criteria are listed in the CPLI

Analysis of the CDLI and CPLI provides insights into the characteristics and common trends among the leading companies on carbon disclosure, and highlights good practices in reporting, governance, risk management, emissions reductions and other areas. Interrelations between the CDLI and CPLI companies are analyzed to determine if those companies with better data use it within the business to drive value adding activities.

“ Fiat is one of the automotive groups most strongly committed to reducing the environmental impacts of transportation: between 2000 and 2010, average CO2 emissions for vehicles sold by Fiat Group Automobiles (FGA) in Europe fell 20%.” Fiat

18

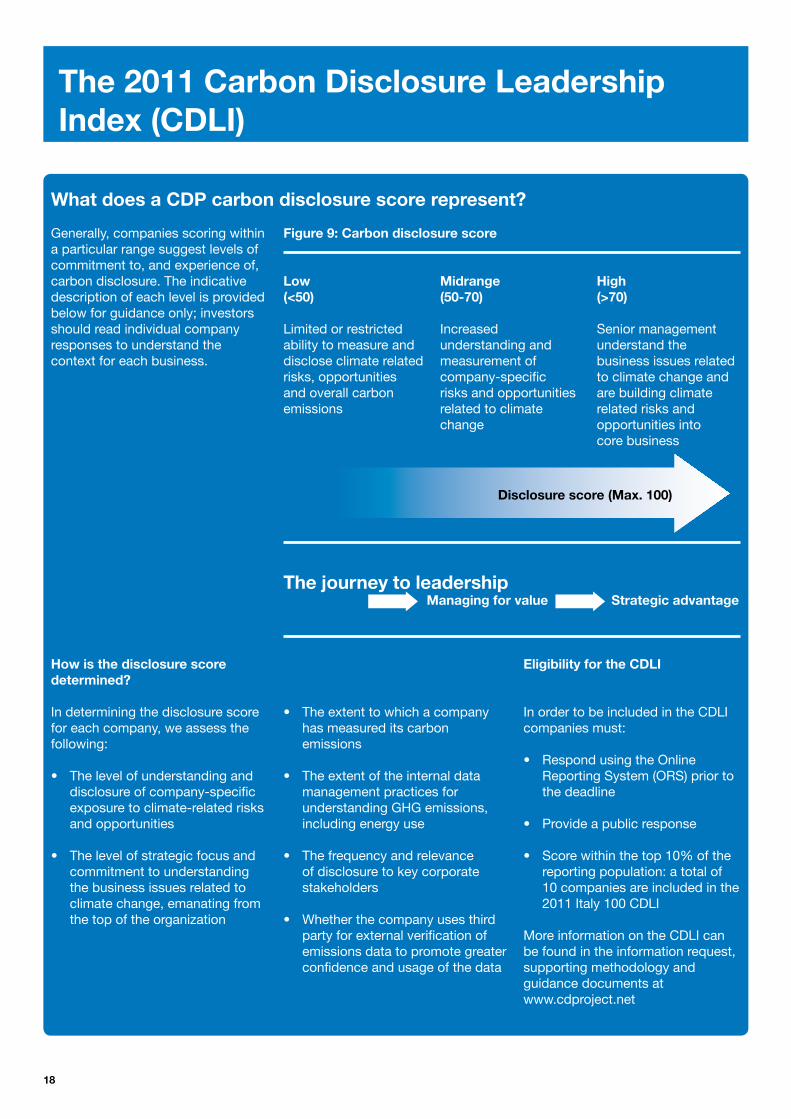

The 2011 Carbon Disclosure Leadership Index (CDLI)

Generally, companies scoring within a particular range suggest levels of commitment to, and experience of, carbon disclosure. The indicative description of each level is provided below for guidance only; investors should read individual company responses to understand the context for each business.

Low (<50)

Limited or restricted ability to measure and disclose climate related risks, opportunities and overall carbon emissions

Midrange (50-70) Increased understanding and measurement of company-specific risks and opportunities related to climate change

High (>70) Senior management understand the business issues related to climate change and are building climate related risks and opportunities into core business

The journey to leadership

Figure 9: Carbon disclosure score

Managing for value Strategic advantage

How is the disclosure score determined?

In determining the disclosure score for each company, we assess the following:

• The level of understanding and disclosure of company-specific exposure to climate-related risks and opportunities

• The level of strategic focus and commitment to understanding the business issues related to climate change, emanating from the top of the organization

• The extent to which a company has measured its carbon emissions

• The extent of the internal data management practices for understanding GHG emissions, including energy use

• The frequency and relevance of disclosure to key corporate stakeholders

• Whether the company uses third party for external verification of emissions data to promote greater confidence and usage of the data

Eligibility for the CDLI

In order to be included in the CDLI companies must:

• Respond using the Online Reporting System (ORS) prior to the deadline

• Provide a public response

• Score within the top 10% of the reporting population: a total of 10 companies are included in the 2011 Italy 100 CDLI

More information on the CDLI can be found in the information request, supporting methodology and guidance documents at www.cdproject.net

What does a CDP carbon disclosure score represent?

Disclosure score (Max. 100)

19

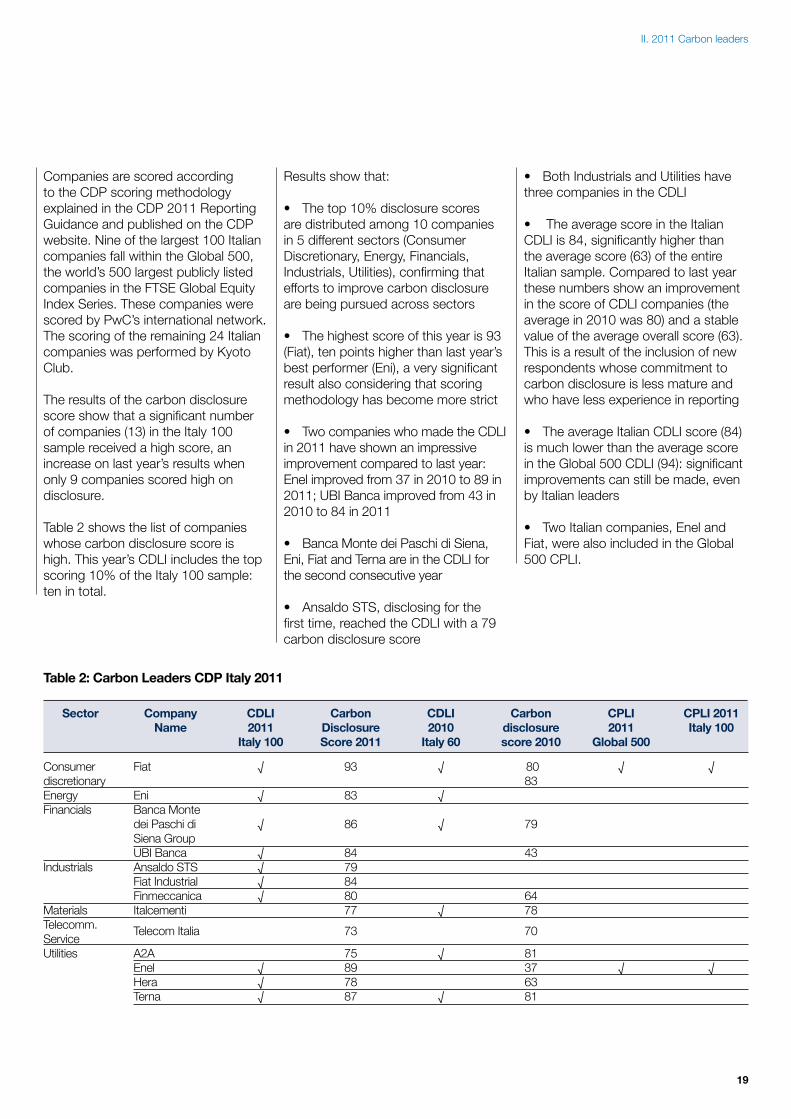

Companies are scored according to the CDP scoring methodology explained in the CDP 2011 Reporting Guidance and published on the CDP website. Nine of the largest 100 Italian companies fall within the Global 500, the world’s 500 largest publicly listed companies in the FTSE Global Equity Index Series. These companies were scored by PwC’s international network. The scoring of the remaining 24 Italian companies was performed by Kyoto Club.

The results of the carbon disclosure score show that a significant number of companies (13) in the Italy 100 sample received a high score, an increase on last year’s results when only 9 companies scored high on disclosure.

Table 2 shows the list of companies whose carbon disclosure score is high. This year’s CDLI includes the top scoring 10% of the Italy 100 sample: ten in total.

Results show that:

• The top 10% disclosure scores are distributed among 10 companies in 5 different sectors (Consumer Discretionary, Energy, Financials, Industrials, Utilities), confirming that efforts to improve carbon disclosure are being pursued across sectors

• The highest score of this year is 93 (Fiat), ten points higher than last year’s best performer (Eni), a very significant result also considering that scoring methodology has become more strict

• Two companies who made the CDLI in 2011 have shown an impressive improvement compared to last year: Enel improved from 37 in 2010 to 89 in 2011; UBI Banca improved from 43 in 2010 to 84 in 2011

• Banca Monte dei Paschi di Siena, Eni, Fiat and Terna are in the CDLI for the second consecutive year

• Ansaldo STS, disclosing for the first time, reached the CDLI with a 79 carbon disclosure score

• Both Industrials and Utilities have three companies in the CDLI

• The average score in the Italian CDLI is 84, significantly higher than the average score (63) of the entire Italian sample. Compared to last year these numbers show an improvement in the score of CDLI companies (the average in 2010 was 80) and a stable value of the average overall score (63). This is a result of the inclusion of new respondents whose commitment to carbon disclosure is less mature and who have less experience in reporting

• The average Italian CDLI score (84) is much lower than the average score in the Global 500 CDLI (94): significant improvements can still be made, even by Italian leaders

• Two Italian companies, Enel and Fiat, were also included in the Global 500 CPLI.

II. 2011 Carbon leaders

Table 2: Carbon Leaders CDP Italy 2011

Sector Company Name

CDLI2011

Italy 100

Carbon Disclosure Score 2011

CDLI2010

Italy 60

Carbon disclosure score 2010

CPLI2011

Global 500

CPLI 2011 Italy 100

Consumer discretionaryEnergyFinancials

Industrials

MaterialsTelecomm. ServiceUtilities

Fiat

EniBanca Monte dei Paschi di Siena GroupUBI BancaAnsaldo STSFiat IndustrialFinmeccanicaItalcementi

Telecom Italia

A2AEnelHeraTerna

√

√ √

√√ √√

√√√

93

83

86

8479 848077

73

75 897887

√

√ √

√

√

√

80 83

79

43

6478

70

8137 6381

√

√

√

√

20

The 2011 Carbon Performance Leadership Index (CPLI)

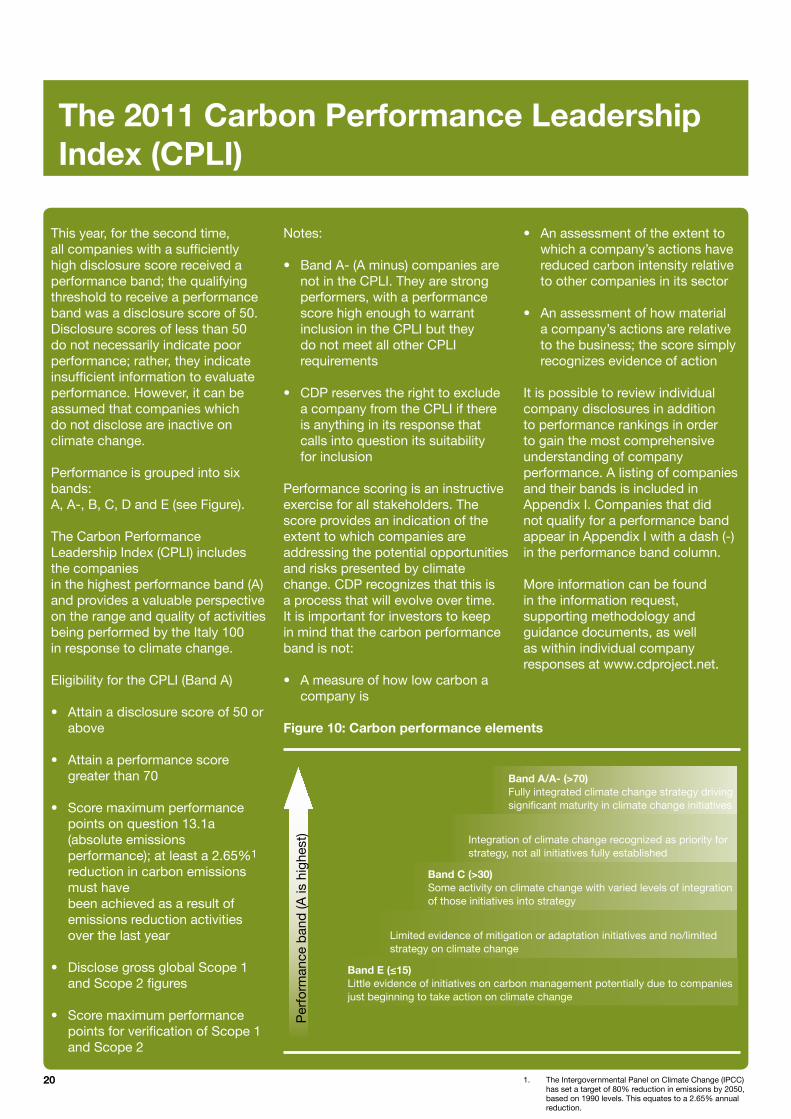

This year, for the second time, all companies with a sufficiently high disclosure score received a performance band; the qualifying threshold to receive a performance band was a disclosure score of 50. Disclosure scores of less than 50 do not necessarily indicate poor performance; rather, they indicate insufficient information to evaluate performance. However, it can be assumed that companies which do not disclose are inactive on climate change.

Performance is grouped into six bands: A, A-, B, C, D and E (see Figure).

The Carbon Performance Leadership Index (CPLI) includes the companies in the highest performance band (A) and provides a valuable perspective on the range and quality of activities being performed by the Italy 100 in response to climate change.

Eligibility for the CPLI (Band A) • Attain a disclosure score of 50 or

above

• Attain a performance score greater than 70

• Score maximum performance points on question 13.1a (absolute emissions performance); at least a 2.65%1

reduction in carbon emissions must have been achieved as a result of emissions reduction activities over the last year

• Disclose gross global Scope 1 and Scope 2 figures

• Score maximum performance

points for verification of Scope 1 and Scope 2

Notes:

• Band A- (A minus) companies are not in the CPLI. They are strong performers, with a performance score high enough to warrant inclusion in the CPLI but they do not meet all other CPLI requirements

• CDP reserves the right to exclude a company from the CPLI if there is anything in its response that calls into question its suitability for inclusion

Performance scoring is an instructive exercise for all stakeholders. The score provides an indication of the extent to which companies are addressing the potential opportunities and risks presented by climate change. CDP recognizes that this is a process that will evolve over time. It is important for investors to keep in mind that the carbon performance band is not:

• A measure of how low carbon a company is

• An assessment of the extent to which a company’s actions have reduced carbon intensity relative to other companies in its sector

• An assessment of how material a company’s actions are relative to the business; the score simply recognizes evidence of action

It is possible to review individual company disclosures in addition to performance rankings in order to gain the most comprehensive understanding of company performance. A listing of companies and their bands is included in Appendix I. Companies that did not qualify for a performance band appear in Appendix I with a dash (-) in the performance band column.

More information can be found in the information request, supporting methodology and guidance documents, as well as within individual company responses at www.cdproject.net.

Figure 10: Carbon performance elements

Per

form

ance

ban

d (A

is h

ighe

st)

Band A/A- (>70)Fully integrated climate change strategy driving significant maturity in climate change initiatives

Integration of climate change recognized as priority for strategy, not all initiatives fully established

Band C (>30)Some activity on climate change with varied levels of integration of those initiatives into strategy

Limited evidence of mitigation or adaptation initiatives and no/limited strategy on climate change

Band E (≤15)Little evidence of initiatives on carbon management potentially due to companies just beginning to take action on climate change

1. The Intergovernmental Panel on Climate Change (IPCC) has set a target of 80% reduction in emissions by 2050, based on 1990 levels. This equates to a 2.65% annual reduction.

21

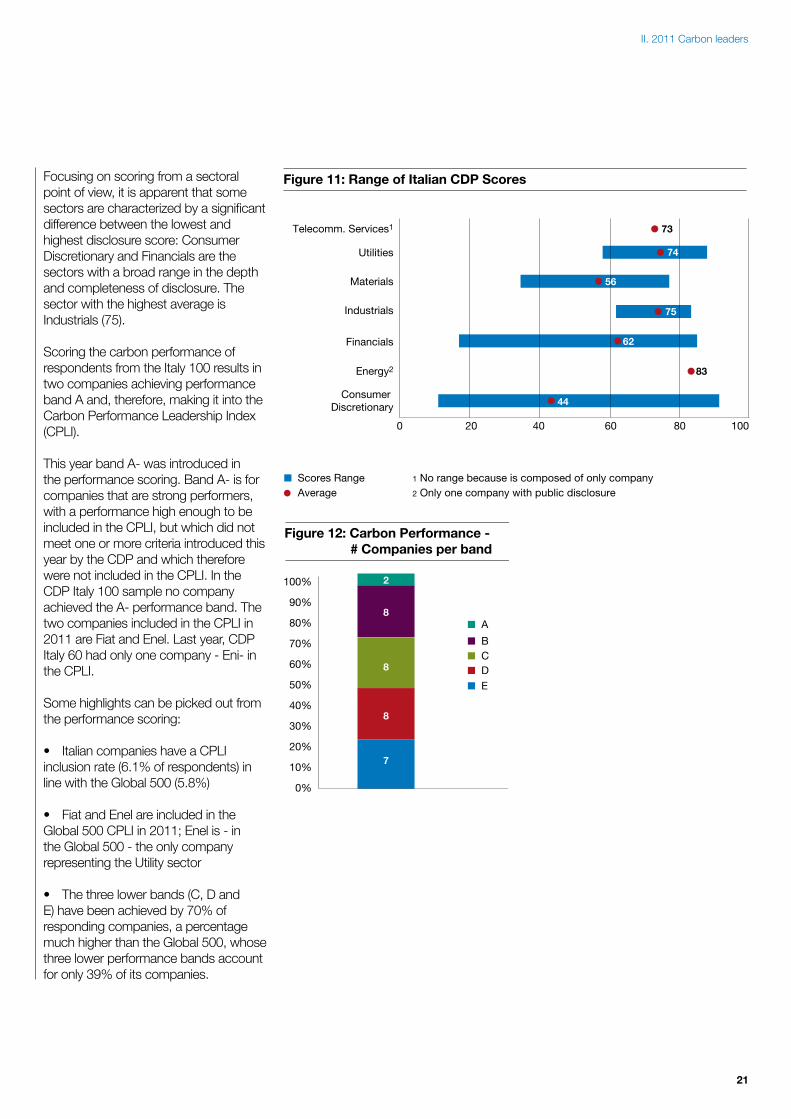

Focusing on scoring from a sectoral point of view, it is apparent that some sectors are characterized by a significant difference between the lowest and highest disclosure score: Consumer Discretionary and Financials are the sectors with a broad range in the depth and completeness of disclosure. The sector with the highest average is Industrials (75).

Scoring the carbon performance of respondents from the Italy 100 results in two companies achieving performance band A and, therefore, making it into the Carbon Performance Leadership Index (CPLI).

This year band A- was introduced in the performance scoring. Band A- is for companies that are strong performers, with a performance high enough to be included in the CPLI, but which did not meet one or more criteria introduced this year by the CDP and which therefore were not included in the CPLI. In the CDP Italy 100 sample no company achieved the A- performance band. The two companies included in the CPLI in 2011 are Fiat and Enel. Last year, CDP Italy 60 had only one company - Eni- in the CPLI.

Some highlights can be picked out from the performance scoring:

• Italian companies have a CPLI inclusion rate (6.1% of respondents) in line with the Global 500 (5.8%)

• Fiat and Enel are included in the Global 500 CPLI in 2011; Enel is - in the Global 500 - the only company representing the Utility sector

• The three lower bands (C, D and E) have been achieved by 70% of responding companies, a percentage much higher than the Global 500, whose three lower performance bands account for only 39% of its companies.

Figure 11: Range of Italian CDP Scores

Scores RangeAverage

Telecomm. Services1

Utilities

Materials

Industrials

Financials

Energy2

Consumer Discretionary

1 No range because is composed of only company

0 20 40 60 80 100

73

74

56

75

62

83

44

2 Only one company with public disclosure

7

8

8

8

2

Figure 12: Carbon Performance - # Companies per band

A

BCDE

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

II. 2011 Carbon leaders

22

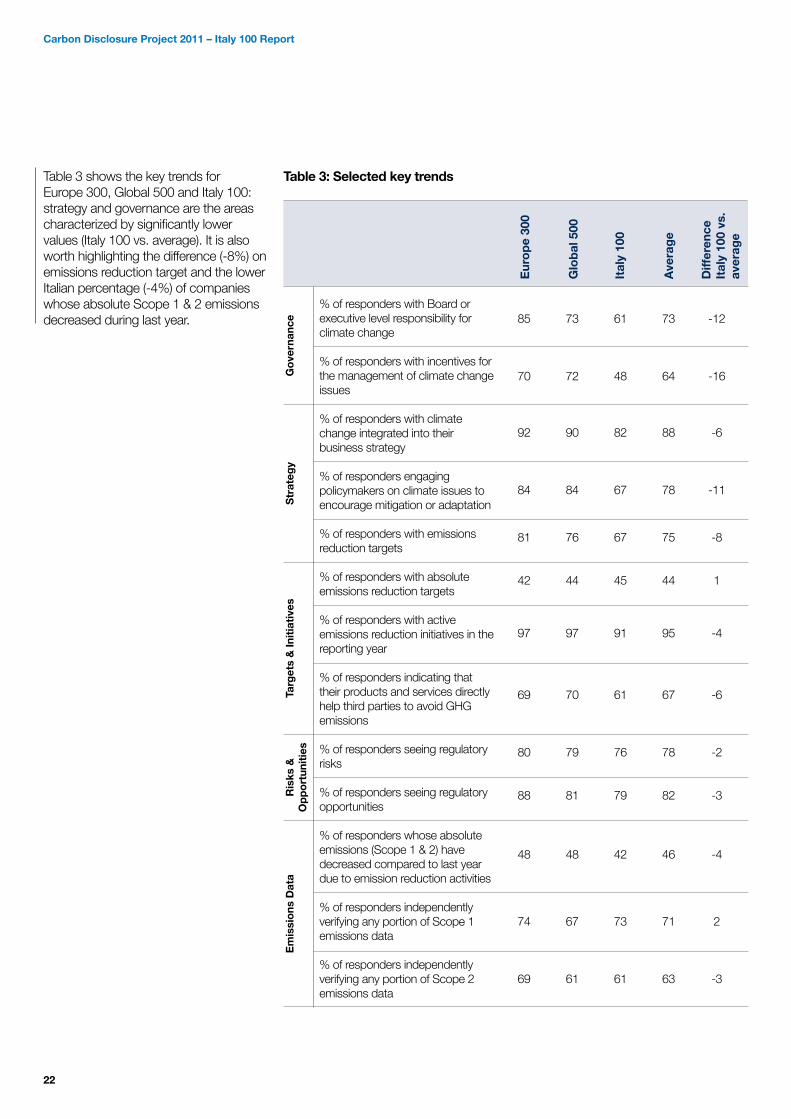

Table 3 shows the key trends for Europe 300, Global 500 and Italy 100: strategy and governance are the areas characterized by significantly lower values (Italy 100 vs. average). It is also worth highlighting the difference (-8%) on emissions reduction target and the lower Italian percentage (-4%) of companies whose absolute Scope 1 & 2 emissions decreased during last year.

Table 3: Selected key trends

% of responders with Board or executive level responsibility for climate change

% of responders with incentives for the management of climate change issues

% of responders with climate change integrated into their business strategy

% of responders engaging policymakers on climate issues to encourage mitigation or adaptation

% of responders with emissions reduction targets

% of responders with absolute emissions reduction targets

% of responders with active emissions reduction initiatives in the reporting year

% of responders indicating that their products and services directly help third parties to avoid GHG emissions

% of responders seeing regulatory risks

% of responders seeing regulatory opportunities

% of responders whose absolute emissions (Scope 1 & 2) have decreased compared to last year due to emission reduction activities

% of responders independently verifying any portion of Scope 1 emissions data

% of responders independently verifying any portion of Scope 2 emissions data

85

70

92

84

81

42

97

69

80

88

48

74

69

73

72

90

84

76

44

97

70

79

81

48

67

61

61

48

82

67

67

45

91

61

76

79

42

73

61

73

64

88

78

75

44

95

67

78

82

46

71

63

-12

-16

-6

-11

-8

1

-4

-6

-2

-3

-4

2

-3

Eur

op

e 30

0

Glo

bal

500

Ital

y 10

0

Ave

rag

e

Diff

eren

ce

Ital

y 10

0 vs

. av

erag

e

Go

vern

ance

Str

ateg

yTa

rget

s &

Init

iati

ves

Ris

ks &

Op

po

rtun

itie

sE

mis

sio

ns D

ata

Carbon Disclosure Project 2011 – Italy 100 Report

23

III. Results

This section of the report focuses on the company responses to the questionnaire. The 2011 questionnaire is made up of three main sections:

• Management (including governance, strategy, targets, initiatives and communications);

• Risks and opportunities (including physical, regulatory and other risks and opportunities related to climate change);

• Emissions (including reporting methodology, emissions data and performance and emissions’ trading)

The CDP 2011 questionnaire has changed compared to last year. It now includes questions, among others, on the payback period of emissions’ reduction initiatives, as well as the expected magnitude of impact on company business of risks and opportunities related to climate change.

As hereafter presented, many aspects of carbon management are included in the request for information. The data provided by companies in their responses helps painting a very interesting picture of how climate change is being addressed in all its aspects by companies.

Management

Regulatory uncertainty, over future developments in international agreements on emissions’ reduction, is still a restraint on companies’ long term decision making. It has to be said, however, that with or without agreement on an international framework over the next year or so, the likelihood is high that policymakers in most developed economies — and even in some developing countries — will adopt national GHG emissions targets and implement them through policies and regulations. This helps to explain why, despite the uncertainty, companies’ initiatives, investments and reporting standards have gone far

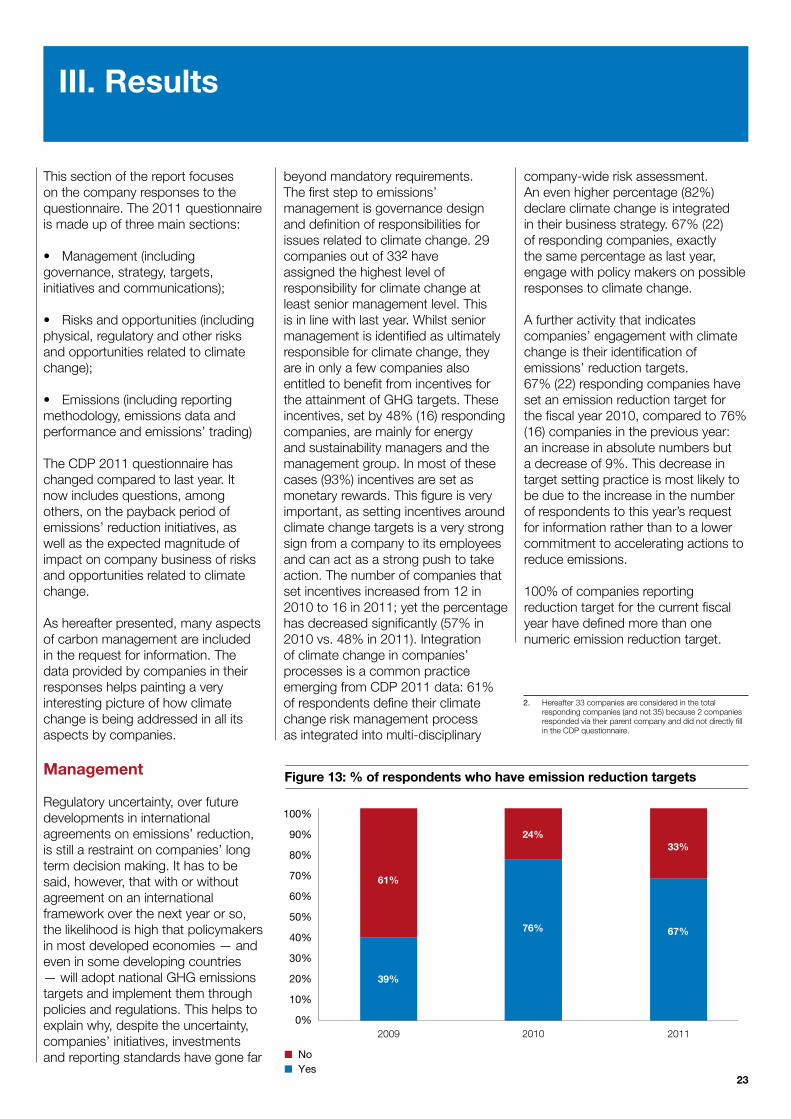

beyond mandatory requirements.The first step to emissions’ management is governance design and definition of responsibilities for issues related to climate change. 29 companies out of 332 have assigned the highest level of responsibility for climate change at least senior management level. This is in line with last year. Whilst senior management is identified as ultimately responsible for climate change, they are in only a few companies also entitled to benefit from incentives for the attainment of GHG targets. These incentives, set by 48% (16) responding companies, are mainly for energy and sustainability managers and the management group. In most of these cases (93%) incentives are set as monetary rewards. This figure is very important, as setting incentives around climate change targets is a very strong sign from a company to its employees and can act as a strong push to take action. The number of companies that set incentives increased from 12 in 2010 to 16 in 2011; yet the percentage has decreased significantly (57% in 2010 vs. 48% in 2011). Integration of climate change in companies’ processes is a common practice emerging from CDP 2011 data: 61% of respondents define their climatechange risk management process as integrated into multi-disciplinary

company-wide risk assessment. An even higher percentage (82%) declare climate change is integrated in their business strategy. 67% (22) of responding companies, exactly the same percentage as last year, engage with policy makers on possible responses to climate change.

A further activity that indicates companies’ engagement with climate change is their identification of emissions’ reduction targets. 67% (22) responding companies have set an emission reduction target for the fiscal year 2010, compared to 76% (16) companies in the previous year: an increase in absolute numbers but a decrease of 9%. This decrease in target setting practice is most likely to be due to the increase in the number of respondents to this year’s request for information rather than to a lower commitment to accelerating actions to reduce emissions.

100% of companies reporting reduction target for the current fiscal year have defined more than one numeric emission reduction target.

Figure 13: % of respondents who have emission reduction targets

NoYes

61%

39%

2009 2010

24%

76%

2011

33%

67%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2. Hereafter 33 companies are considered in the total responding companies (and not 35) because 2 companies responded via their parent company and did not directly fill in the CDP questionnaire.

24

All companies, in fact, have several targets applying to different business units or with different time horizons.

When considering the underlying data, absolute targets are marginally more common than intensity targets. 45% (10) of the companies in fact report absolute emissions reduction targets, while 32% (7) report intensity targets (e.g. relative to production volumes, employees or square metres). 5 companies (23%), meanwhile, have defined both absolute and intensity targets.

Targets are most commonly set for the total of Scope 1 and Scope 2 emissions. Targets set by companies are hardly comparable because of different time frames (base year to target year) and perimeter targets. 90% (20) of companies with emissions’ reduction targets set their timeframes over the next five years. Only A2A, Edison and Unicredit have disclosed reduction targets addressing the next ten years to 2020. Both A2A and Edison are driven by regulatory visibility, which allows companies to include emission reduction targets in their strategic plans.

By integrating sustainability in their organization and processes, companies generally identify opportunities to profit from the creation of new sustainable products and services.

In 2010, 15 respondents (71%) claimed that they had goods or services that were designed specifically to help their customers or end consumers reduce their own carbon emissions. This year’s figure is a decrease of 10% compared to 2010. However there was an increase to 22 (61%) in the absolute number of companies reporting development or promotion of goods or services directly enabling customers to avoid or reduce GHG emissions.

Companies from the Utilities, Industrial and Financial sectors are more actively engaged than those in other sectors in developing or promoting such products and services to their customers or end users.

Figure 14: Reduction Targets - Yes Breakdown (%)

32%

23%

45%

Absolute and intensity targetsAbsolute targetsIntensity targets

Figure 15: % of responders indicating that their products and services help third parties to avoid GHG emissions

NoYes

29%

71%

2010 2011

39%

61%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Figure 16: Product and services - Yes breakdown (%)

Consumer Discretionary

Financials

35%

20%

10%

5%

20%5%

5%

Energy Industrials

MaterialsTelecomunication Services

Utilities

Carbon Disclosure Project 2011 – Italy 100 Report

25

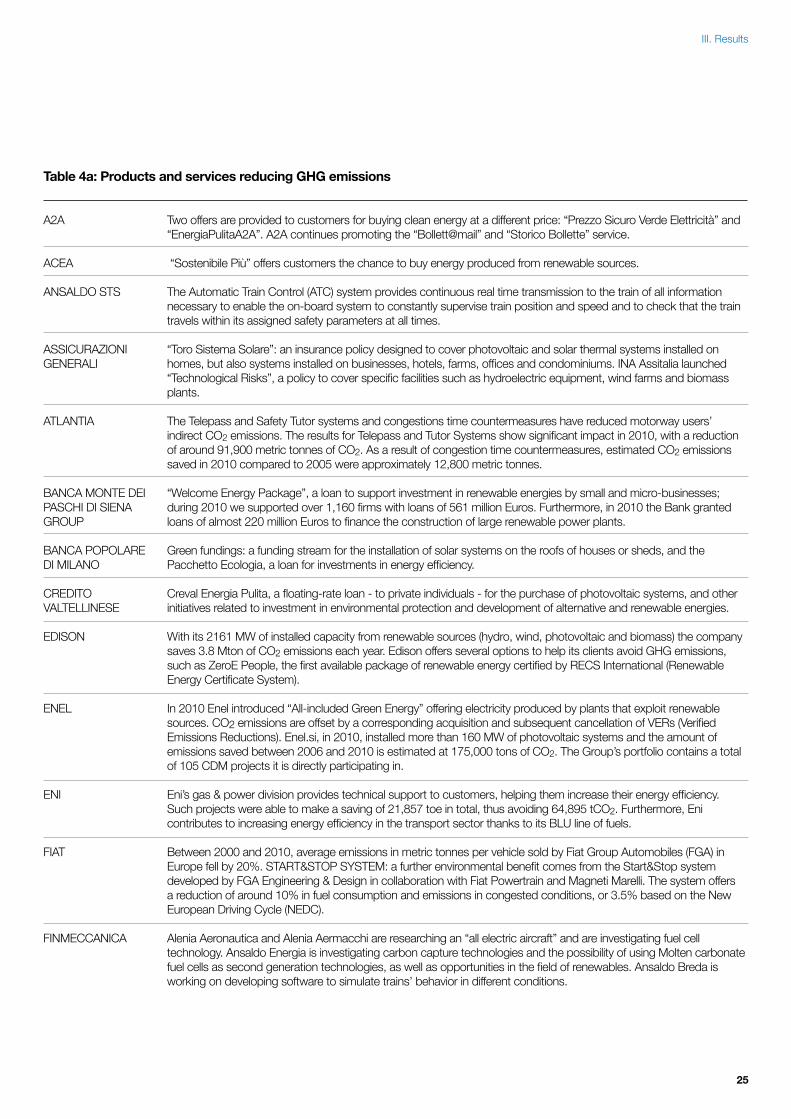

Table 4a: Products and services reducing GHG emissions

A2A Two offers are provided to customers for buying clean energy at a different price: “Prezzo Sicuro Verde Elettricità” and “EnergiaPulitaA2A”. A2A continues promoting the “Bollett@mail” and “Storico Bollette” service.

ACEA “Sostenibile Più” offers customers the chance to buy energy produced from renewable sources.

ANSALDO STS The Automatic Train Control (ATC) system provides continuous real time transmission to the train of all information necessary to enable the on-board system to constantly supervise train position and speed and to check that the train travels within its assigned safety parameters at all times.

ASSICURAZIONI “Toro Sistema Solare”: an insurance policy designed to cover photovoltaic and solar thermal systems installed on GENERALI homes, but also systems installed on businesses, hotels, farms, offices and condominiums. INA Assitalia launched “Technological Risks”, a policy to cover specific facilities such as hydroelectric equipment, wind farms and biomass plants.

ATLANTIA The Telepass and Safety Tutor systems and congestions time countermeasures have reduced motorway users’ indirect CO2 emissions. The results for Telepass and Tutor Systems show significant impact in 2010, with a reduction of around 91,900 metric tonnes of CO2. As a result of congestion time countermeasures, estimated CO2 emissions saved in 2010 compared to 2005 were approximately 12,800 metric tonnes.

BANCA MONTE DEI “Welcome Energy Package”, a loan to support investment in renewable energies by small and micro-businesses; PASCHI DI SIENA during 2010 we supported over 1,160 firms with loans of 561 million Euros. Furthermore, in 2010 the Bank granted GROUP loans of almost 220 million Euros to finance the construction of large renewable power plants.

BANCA POPOLARE Green fundings: a funding stream for the installation of solar systems on the roofs of houses or sheds, and theDI MILANO Pacchetto Ecologia, a loan for investments in energy efficiency.

CREDITO Creval Energia Pulita, a floating-rate loan - to private individuals - for the purchase of photovoltaic systems, and other VALTELLINESE initiatives related to investment in environmental protection and development of alternative and renewable energies.

EDISON With its 2161 MW of installed capacity from renewable sources (hydro, wind, photovoltaic and biomass) the company saves 3.8 Mton of CO2 emissions each year. Edison offers several options to help its clients avoid GHG emissions, such as ZeroE People, the first available package of renewable energy certified by RECS International (Renewable Energy Certificate System).

ENEL In 2010 Enel introduced “All-included Green Energy” offering electricity produced by plants that exploit renewable sources. CO2 emissions are offset by a corresponding acquisition and subsequent cancellation of VERs (Verified Emissions Reductions). Enel.si, in 2010, installed more than 160 MW of photovoltaic systems and the amount of emissions saved between 2006 and 2010 is estimated at 175,000 tons of CO2. The Group’s portfolio contains a total of 105 CDM projects it is directly participating in.

ENI Eni’s gas & power division provides technical support to customers, helping them increase their energy efficiency. Such projects were able to make a saving of 21,857 toe in total, thus avoiding 64,895 tCO2. Furthermore, Eni contributes to increasing energy efficiency in the transport sector thanks to its BLU line of fuels.

FIAT Between 2000 and 2010, average emissions in metric tonnes per vehicle sold by Fiat Group Automobiles (FGA) in Europe fell by 20%. START&STOP SYSTEM: a further environmental benefit comes from the Start&Stop system developed by FGA Engineering & Design in collaboration with Fiat Powertrain and Magneti Marelli. The system offers a reduction of around 10% in fuel consumption and emissions in congested conditions, or 3.5% based on the New European Driving Cycle (NEDC).

FINMECCANICA Alenia Aeronautica and Alenia Aermacchi are researching an “all electric aircraft” and are investigating fuel cell technology. Ansaldo Energia is investigating carbon capture technologies and the possibility of using Molten carbonate fuel cells as second generation technologies, as well as opportunities in the field of renewables. Ansaldo Breda is working on developing software to simulate trains’ behavior in different conditions.

III. Results

26

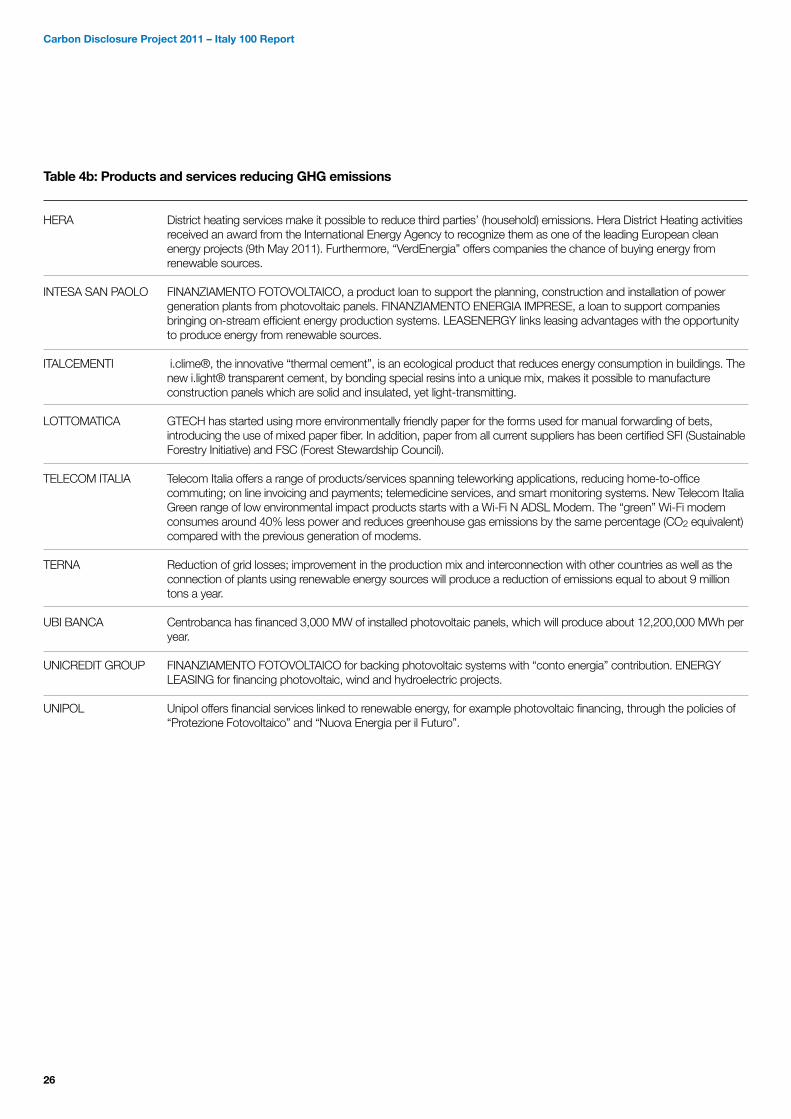

Table 4b: Products and services reducing GHG emissions

HERA District heating services make it possible to reduce third parties’ (household) emissions. Hera District Heating activities received an award from the International Energy Agency to recognize them as one of the leading European clean energy projects (9th May 2011). Furthermore, “VerdEnergia” offers companies the chance of buying energy from renewable sources.

INTESA SAN PAOLO FINANZIAMENTO FOTOVOLTAICO, a product loan to support the planning, construction and installation of power generation plants from photovoltaic panels. FINANZIAMENTO ENERGIA IMPRESE, a loan to support companies bringing on-stream efficient energy production systems. LEASENERGY links leasing advantages with the opportunity to produce energy from renewable sources.

ITALCEMENTI i.clime®, the innovative “thermal cement”, is an ecological product that reduces energy consumption in buildings. The new i.light® transparent cement, by bonding special resins into a unique mix, makes it possible to manufacture construction panels which are solid and insulated, yet light-transmitting.

LOTTOMATICA GTECH has started using more environmentally friendly paper for the forms used for manual forwarding of bets, introducing the use of mixed paper fiber. In addition, paper from all current suppliers has been certified SFI (Sustainable Forestry Initiative) and FSC (Forest Stewardship Council).

TELECOM ITALIA Telecom Italia offers a range of products/services spanning teleworking applications, reducing home-to-office commuting; on line invoicing and payments; telemedicine services, and smart monitoring systems. New Telecom Italia Green range of low environmental impact products starts with a Wi-Fi N ADSL Modem. The “green” Wi-Fi modem consumes around 40% less power and reduces greenhouse gas emissions by the same percentage (CO2 equivalent) compared with the previous generation of modems.