CCFEI Presentation Prospects for World PTA · IOCL Panipat Capacities ranging from 80,000 to...

20

CCFEI Presentation Prospects for World PTA Presentation by Barbara Kettle PTA Licensing Commercial Manager INVISTA Performance Technologies May 2004 Confidential to INVISTA Copyright INVISTA Key questions for the industry • Question 1 – Is there an optimum company structure for today’s polyester market place?? • Question 2 – What issues face the polyester industry in the short to medium term ?? • Questions 3 – What factors will influence the success or failure of the polyester industry in China ??

Transcript of CCFEI Presentation Prospects for World PTA · IOCL Panipat Capacities ranging from 80,000 to...

1

CCFEI Presentation Prospects for World PTA

Presentation by

Barbara KettlePTA Licensing Commercial Manager INVISTA Performance Technologies

May 2004

Confidential to INVISTA Copyright INVISTA

Key questions for the industry

• Question 1– Is there an optimum company structure for today’s polyester

market place??

• Question 2– What issues face the polyester industry in the short to

medium term ??

• Questions 3– What factors will influence the success or failure of the

polyester industry in China ??

2

Agenda

Introduction to INVISTAPX / PTA supply and demand

Investment choicesSummary

Confidential to INVISTA Copyright INVISTA

Key questions for the industry

• Question 1–Is there an optimum company structure for today's polyester market place??

3

Confidential to INVISTA Copyright INVISTA

Our new name and identity

Confidential to INVISTA Copyright INVISTA

History• February 2002, DuPont announced that it would separate

DTI by year-end 2003

• September 2003, DTI announced a new name for DTI. INVISTA is launched to create a new identity

• November 2003, DuPont and Koch reached agreement for Koch Industries to acquire INVISTA for $4.4B USD

• May 1st 2004 Koch purchase of INVISTA completed. INVISTA will be combined with KoSa to form an integrated $10B USD company upon closing of the sale

4

Koch Industries

• Second largest privately held company in the U.S.

• Currently $42B in sales

• Estimated Sales of $50B in 2005 growing from $200MM in sales in 1967

• Very diverse group of businesses

– Operates 3 refineries as part of Flint Hills Resources– Koch Chemical has a wide range of chemical

operations including Paraxylene – manufacturing and trading

– Koch Technolgies: John Zink and Koch-Glitsch– Largest Commodity Trading company in the U.S.– KoSa - one of the world’s largest polyester producers– Equity and Financial Management Companies

Koch Industries

5

Confidential to INVISTA Copyright INVISTA

Our business

Integrated fibers and intermediates business

Upstream to Downstream

Brandedand generic

WovensNon-wovens

Consumer and industrial

Vertical integrationR+DTechnologiesIntermediatesFibersManufacturingSupportDistributionBrandingMarketingService

Licensing

NylonPolyesterElastane

…with customers

Confidential to INVISTA Copyright INVISTA

Koch and polyester

• Koch Industries with acquisition of INVISTA compliments existing KoSA polyester capability

• INVISTA totally integrated within the polyester value chain and able to supply – PX, raw material sourcing– IPA product – PTA, product and process technology– PET polymerization, product and process technology– Staple and filament fibres product and process technology

and support

6

Confidential to INVISTA Copyright INVISTA

From polyester to performance

•DuPont Polyester Technologies has changed its name to INVISTA Performance Technologies

•Our people, commitment and support to existing and future clients remains undiminished

•The change from Polyester to Performancereflects a widening of our ambition to develop and license innovative technology, not just in polyester but also for the whole of INVISTA

Confidential to INVISTA Copyright INVISTA

INVISTA Performance Technologies

• IPT is now responsible for licensing all INVISTAtechnologies

• PTA • Polyester including

– staple and POY spinning and PET Resins

• Nylon Intermediates including – Cyclohexane oxidation Adiponitrile, HCN

• Spandex Intermediates including – BDO, THF, and PTMEG

7

Confidential to INVISTA Copyright INVISTA

Our strategy for growth

• Aggressively grow our businesses in Asia• Develop unique and creative business models• Investment in R&D and manufacturing assets

in the regions where the market is growing• Increase Asian appreciation of INVISTA’s

globally recognized brands and exploit market knowledge

• Provide an on-going stream of innovation• Have a leading cost position worldwide

Confidential to INVISTA Copyright INVISTA

INVISTA’s commitment to R&D

• Over $150 Million / year on research and development– ~400 R&D Professionals– >23% of revenue from products less than 5 years old

• A large patent estate– 3,750 patents worldwide owned by INVISTA – 3,635 patents under prosecution worldwide– Over 1,000 patents licensed from DuPont– Over 250 Notices of Invention since January 1, 2002

Does not include KoSa

8

Confidential to INVISTA Copyright INVISTA

Question 1

• Is there an optimum company structure fortodays polyester market place??

• Yes, but only those who are ready and willing to adapt, optimising and change their structure to be responsive to the needs of the industry….there is more change to come!

Confidential to INVISTA Copyright INVISTA

Key questions for the industry

• Question 2–What issues face the polyester industry in the short to medium term ??

9

Agenda

Introduction to INVISTAPX / PTA supply and demand

Investment choicesSummary

Confidential to INVISTA Copyright INVISTA

Global demandStaple, Filament, Resin

02468

10121416182022

1990 1995 2000 2005 2010 2015

StapleFilamentPET Resin

YEAR

Mill

ion

tons

per

Yea

r

Source : PCI Q2 2004

10

Confidential to INVISTA Copyright INVISTA

PX Global supply and demand

-

500

1,000

1,500

2,000

2,500

Jan-

03Apr

-03

Jul-0

3O

ct-0

3Ja

n-04

Apr

-04

Jul-0

4O

ct-0

4Ja

n-05

Apr

-05

Jul-0

5O

ct-0

5Ja

n-06

Apr

-06

Jul-0

6O

ct-0

6

'000 Tonnes

Inventory Production DemandUpper Limit Lower Limit

Source : PCI Q2 2004

Confidential to INVISTA Copyright INVISTA

PX Net World Trade

-1,500

-1,000

-500

-

5 0 0

1,000

1,500

2003

2004

2005

2006

'000 Tonnes

North America South America West Europe

East Europe Middle East/Africa Asia

Source : PCI Q2 2004

11

Confidential to INVISTA Copyright INVISTA

China PX Supply and demand

-100200300400500600700800

Jan-

03Apr

-03

Jul-03

Oct

-03

Jan-

04Apr

-04

Jul-04

Oct

-04

Jan-

05Apr

-05

Jul-05

Oct

-05

Jan-

06Apr

-06

Jul-06

Oct

-06

'000 Tonnes

Inventory Production Demand

Upper Limit Lower Limit

Source : PCI Q2 2004

Confidential to INVISTA Copyright INVISTA

PTA Global supply and demand

-500

1,0001,500

2,0002,5003,0003,500

Jan-

03Ap

r-03

Jul-03

Oct

-03

Jan-

04Ap

r-04

Jul-04

Oct

-04

Jan-

05Ap

r-05

Jul-05

Oct

-05

Jan-

06Ap

r-06

Jul-06

Oct

-06

'000 Tonnes

Inventory Production DemandUpper Limit Lower Limit

Source : PCI Q2 2004

12

Confidential to INVISTA Copyright INVISTA

PTA Net world trade

-1,500

-1,000

-500

-

500

1,000

1,500

2003

2004

2005

2006

'000 Tonnes

North America South America West Europe

East Europe Middle East/Africa Asia

Source : PCI Q2 2004

Confidential to INVISTA Copyright INVISTA

China PTA supply and demand

-200

400600

800

1,000

1,200

Jan-

03Ap

r-03

Jul-03

Oct

-03

Jan-

04Ap

r-04

Jul-04

Oct

-04

Jan-

05Ap

r-05

Jul-05

Oct

-05

Jan-

06Ap

r-06

Jul-06

Oct

-06

'000 Tonnes

Inventory Production DemandUpper Limit Lower Limit

Source : PCI Q2 2004

13

Confidential to INVISTA Copyright INVISTA

Question 2

– What issues face the polyester industry in the short to medium term ??

– PX supply• The supply demand position looks tight, securing

adequate PX for PTA is a priority

– PTA supply• PTA supply looks tight up until 2006 / 2007 when many

new PTA investments come on line in China. Will they run at full capacity with PX constraints?

Confidential to INVISTA Copyright INVISTA

Key questions for the industry

• Questions 3–What factors will influence the success or failure of the polyester industry in China ??

14

Agenda

Introduction to INVISTAPX / PTA supply and demand

Investment choicesSummary

Confidential to INVISTA Copyright INVISTA

Advanced technology

Yizheng PTA 2 Deploying INVISTA technology

15

Confidential to INVISTA Copyright INVISTA

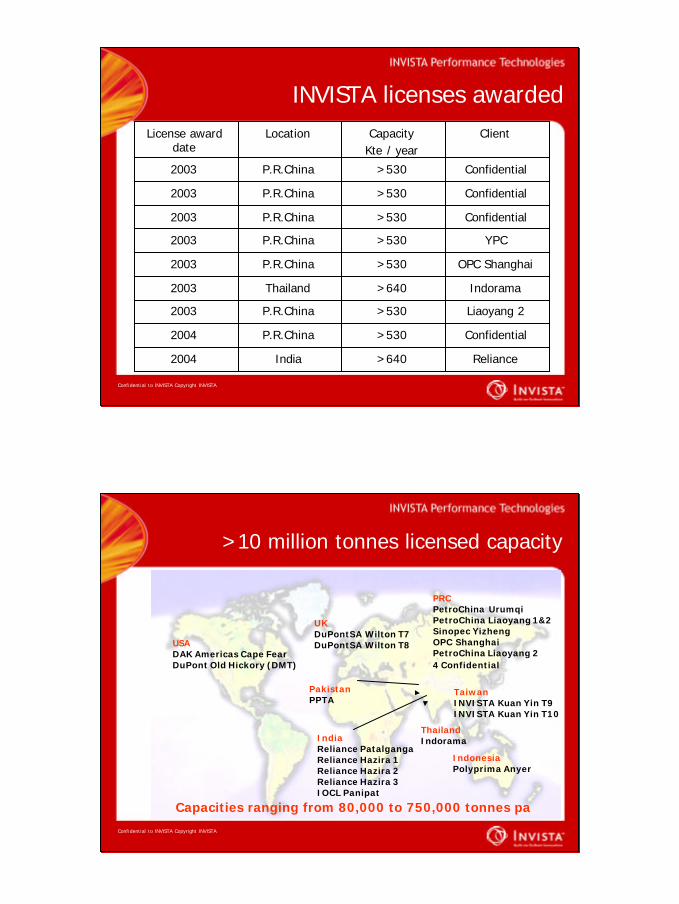

INVISTA licenses awarded

YPC>530P.R.China2003

Reliance>640India2004

Confidential>530P.R.China2004

Liaoyang 2>530P.R.China2003

Indorama>640Thailand2003

OPC Shanghai>530P.R.China2003

Confidential>530P.R.China2003

Confidential>530P.R.China2003

Confidential>530P.R.China2003

ClientCapacity Kte / year

LocationLicense award date

Confidential to INVISTA Copyright INVISTA

>10 million tonnes licensed capacity

PRCPetroChina UrumqiPetroChina Liaoyang 1&2Sinopec YizhengOPC ShanghaiPetroChina Liaoyang 24 Confidential

TaiwanINVISTA Kuan Yin T9INVISTA Kuan Yin T10

IndonesiaPolyprima Anyer

UKDuPontSA Wilton T7DuPontSA Wilton T8USA

DAK Americas Cape FearDuPont Old Hickory (DMT)

PakistanPPTA

IndiaReliance PatalgangaReliance Hazira 1Reliance Hazira 2Reliance Hazira 3IOCL Panipat

Capacities ranging from 80,000 to 750,000 tonnes pa

ThailandIndorama

16

Confidential to INVISTA Copyright INVISTA

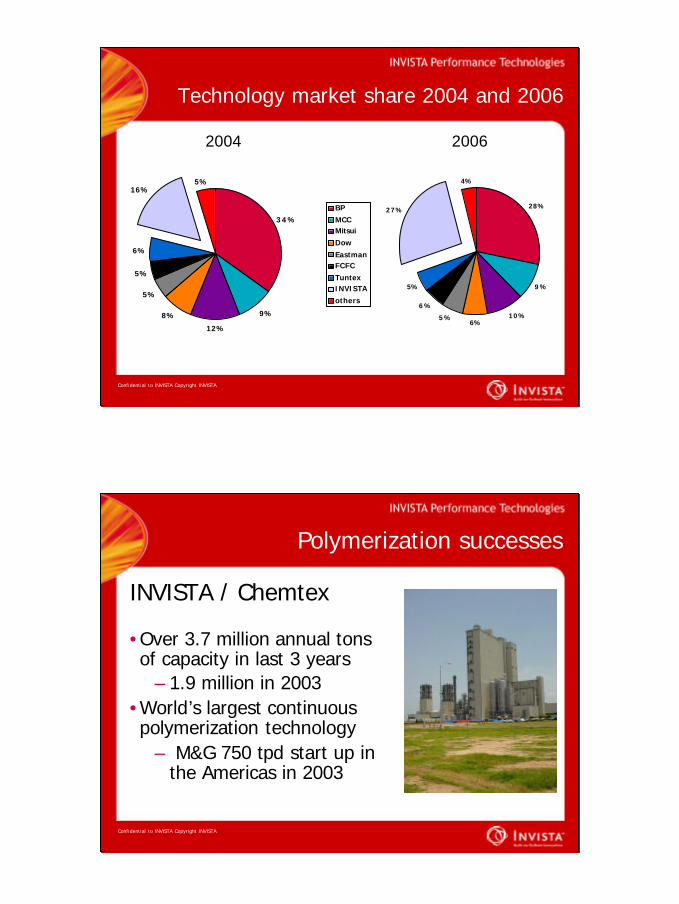

Technology market share 2004 and 2006

34%

9%

12%

8%

5%

5%

6%

16%5%

BP

MCCMitsui

Dow

EastmanFCFC

TuntexINVISTA

others

28%

9%

10%6%

5%

6%

5%

27%

4%

2004 2006

Confidential to INVISTA Copyright INVISTA

Polymerization successes

INVISTA / Chemtex

•Over 3.7 million annual tons of capacity in last 3 years

– 1.9 million in 2003 •World’s largest continuous polymerization technology

– M&G 750 tpd start up in the Americas in 2003

17

Confidential to INVISTA Copyright INVISTA

– What factors will influence the success or failure of the polyester industry in China ??

– Investment choices• Technology integration

• Proven operational reliability• Largest scale • Lowest variable and fixed costs

Question 3

Agenda

Introduction to INVISTAPX / PTA supply and demand

Investment choicesSummary

18

Confidential to INVISTA Copyright INVISTA

Key questions for the industry

• Question 1– Is there an optimum company structure for today’s polyester

market place??

• Question 2– What issues face the polyester industry in the short to

medium term ??

• Questions 3– What factors will influence the success or failure of the

polyester industry in China ??

Confidential to INVISTA Copyright INVISTA

Summary

• Only those who are ready and willing to adapt and keep optimising and changing their structures to meet the changing industry….there is more change to come!

• The supply demand position looks tight, securing adequate PX for PTA manufacturing is a priority

• PTA supply looks tight up until 2006 / 2007 when many new PTA investments come on line in China. Will they run at full capacity with PX constraints?

19

Confidential to INVISTA Copyright INVISTA

Summary

• Investment choices• Technology integration• Proven operational reliability• Largest scale • Lowest variable and fixed costs

Confidential to INVISTA Copyright INVISTA

Summary

• INVISTA has the– technology, – people, – commitment, – scale, – proven track record, and

– global reach

• We are the largest, integrated intermediates and fiber company in the world

• Step Forward™ together with INVISTA

20

CCFEI presentationProspects for World PTA

Presentation by

Barbara KettlePTA Licensing Commercial Manager INVISTA Performance Technologies