Cashlite C ashlite · regulatory and oversight functions within their organizations. The ethical...

32

Bank Bank Th e Th e Director Director BANK DIRECTORS ASSOCIATION OF NIGERIA A Bi-annual Publication of The Bank Directors Association of Nigeria Cashlite Economy Cashlite Economy Vol 1 No 1 February 2012 Banking Reform Cashlite Economy Women Agents of change Was Steve Jobs a success as CEO and Chairman?

Transcript of Cashlite C ashlite · regulatory and oversight functions within their organizations. The ethical...

Bank Bank Th

eTh

e Director Director BANK DIRECTORS ASSOCIATION OF NIGERIA A Bi-annual Publication of The Bank Directors Association of Nigeria

Cashlite Economy Cashlite Economy

Vol 1 No 1 February 2012

Banking Reform

Cashlite Economy

Women Agents of change

Was Steve Jobs asuccess as CEO and Chairman?

2The Bank Director

C o u n c i l M e m b e r s

The Olor'ogun (Dr.) Sonny F. Kuku - President

Mrs. Foluke K. Abdulrazaq - Vice-President

Mr. Yemi Idowu - Secretary

Mr Ikechi O. Kalu - Financial Secretary

Mr. M.G. Tarfa - Treasurer

Mr. Sam Cookey Jr. - Member

Chief Ope Bademosi - Member

Mr. Chima Akalezi - Member

Mr. Okezie C. Amachukwu - Member

Dr. (Mrs.) Lucy Newman - Member

O.M. Sulaimon - Member

Dr. (Mrs.) Nike Akande - Member

Mr. Nnamdi Oji - Member

C o n t e n t s

New President's Remarks 4

New President's Speech 5

BDAN in brief 6

Banking Focus 10

Photo Splash 12

The Director's Health 13

Quotable Quotes 14

Current Matters 15

Updates for members 16

Pa g e s

3

Current President’s Remarks

Current President’s Remarks

The Bank Director

The Olor'ogun (Dr.) Sonny. F. Kuku OFRPresident, Bank Directors Association of Nigeria (BDAN)

I am pleased to be writing you in this maiden edition of our Newsletter. The Newsletter comes as a result of our continuous concerted effort to position BDAN as an influential body in the financial services industry.

The objectives of the Association are hinged on the premise that we can collectively protect the interests of the banking industry and also the directors of banks. This necessitates our proactive involvement in the processes of formulation of policies and regulations for the industry.

In this light, the Governing Council has approved the report of a survey on the remuneration of directors. BDAN recognizes that a proper remuneration structure of directors is necessary for their independence as they perform their regulatory and oversight functions within their organizations. The ethical burden on directors cannot be over-emphasized and it is important that impediments are removed to allow effective functioning.

As directors and major stakeholders in the industry, it is necessary to have a platform on which regulators can interface with us as a sounding board for regulations that pertain to and affect the sector directly, and also those that

may have indirect impact on us. Our experiences and expertise is such that we can give value to our nation's building process. BDAN gives voice to Bank directors as a body.

BDAN will continuously strive to upgrade and update the knowledge of members. Fora are periodically organized to discuss salient issues relating to the banking industry. The event brings together decision makers in the industry, including the regulators. The Central Bank of Nigeria and the Nigeria Deposit Insurance Company have been notably involved in these fora.

BDAN also affords the directors the unique opportunity to attend bespoke trainings that address the needs of directors of banks in Nigeria. As mentioned earlier, the ethical burden and the past financial system meltdown makes it imperative for us to be well grounded in the rudiments of corporate governance.

BDAN will continue to serve the interests of the directors. We hope that we will continue to have the support of all stakeholders in the industry as we participate in different aspects of building healthy and reliable banks.

Thank you and God bless.

4

B D A N i n b r i e f

The Bank Director

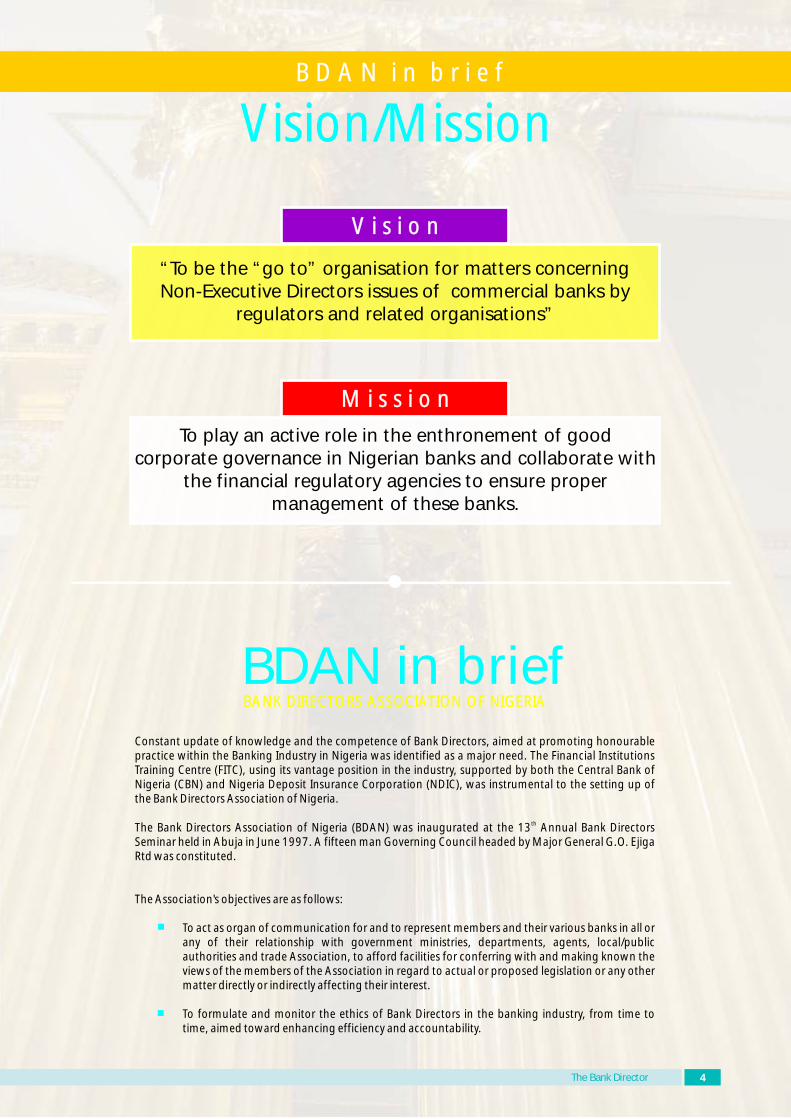

V i s i o n

Vision/Mission

“To be the “go to” organisation for matters concerning Non-Executive Directors issues of commercial banks by

regulators and related organisations”

M i s s i o n

To play an active role in the enthronement of good corporate governance in Nigerian banks and collaborate with

the financial regulatory agencies to ensure proper management of these banks.

Constant update of knowledge and the competence of Bank Directors, aimed at promoting honourable practice within the Banking Industry in Nigeria was identified as a major need. The Financial Institutions Training Centre (FITC), using its vantage position in the industry, supported by both the Central Bank of Nigeria (CBN) and Nigeria Deposit Insurance Corporation (NDIC), was instrumental to the setting up of the Bank Directors Association of Nigeria.

thThe Bank Directors Association of Nigeria (BDAN) was inaugurated at the 13 Annual Bank Directors Seminar held in Abuja in June 1997. A fifteen man Governing Council headed by Major General G.O. Ejiga Rtd was constituted.

The Association's objectives are as follows:

· To act as organ of communication for and to represent members and their various banks in all or any of their relationship with government ministries, departments, agents, local/public authorities and trade Association, to afford facilities for conferring with and making known the views of the members of the Association in regard to actual or proposed legislation or any other matter directly or indirectly affecting their interest.

· To formulate and monitor the ethics of Bank Directors in the banking industry, from time to time, aimed toward enhancing efficiency and accountability.

BANK DIRECTORS ASSOCIATION OF NIGERIA

BDAN in brief

5

B D A N i n b r i e f

The Bank Director

· To enlighten and educate its members in regard to their legal, moral and general rights and responsibilities in respect to their banks, organizations and society as a whole.

· To provide an active forum and effective voice for its members in public affairs.

· To improve the competence and knowledge of its members and promote honourable practice by members within the Banking Industry.

· To take a continuing and effective interest in legislation in order to ensure as far as possible that basic commercial freedoms and rights are preserved, to ensure conductive climate towards strong economic growth in Nigeria.

· To advance the competence and knowledge of its members by organizing, arranging and sponsoring meetings, conferences, seminars, lectures and courses of study aimed towards the development of the business of banking in Nigeria.

Since inception, BDAN has produced seven Governing Councils peopled by directors of high integrity, innovative minds and disciplined work ethics. Transitions of leadership between successive Governing Councils has been smooth and democratic and has always ensured that capable and committed leaders are elected. This has helped to fuel the growth of the Association. These various leaderships have been able to unite the major banks in Nigeria with nearly all banks being active supporters of the Association.

BDAN has organized several fora to acquaint members with issues of interest to the industry as part of continuing education of members. Such gathering has also been a conduit for expression of members' views on salient nation issues pertaining to the Banking Industry. There is regular interaction between the Association and the regulators and other stakeholders in the industry.

The activities of the Association are being financed by annual subscriptions paid by the banks to the Association.

BANK DIRECTORS ASSOCIATION OF NIGERIA

6The Bank Director

B a n k i n g f o c u s

Banking on Reforms: Perspectives on the Future Landscape of Banking in Nigeria.

- By Dr. Kingsley Chiedu Moghalu

Dr. Moghalu began by remarking on the dramatic developments in the global and domestic financial systems in the last three

years which led to phenomenal changes in the Nigerian banking industry. The lessons learnt from the recent global financial crisis as well as the weaknesses, issues and challenges that preceded the Nigerian banking sector crisis providing the basis for the far-reaching reforms initiated by the CBN in 2009. These reform measures had the objective of strengthening the stability and resilience of the financial system and ensuring that the banking system contributes to the development of the real economy.

Adding that while the reforms may not yet have been fully bedded down, they have nevertheless already changed the shape, structure and character of the banking system as well as redefined both the competitive landscape in which banks operate and the dynamics of risk and return that shape their businesses. He identified some positive outcomes of the reform as:

· A new banking model that replaced the erstwhile Universal Banking regime which now governs the licensing and operation of banks. Under the model, banks are required to operate within defined functional boundaries as commercial, merchant or specialized banks with different levels of capital

requirements commensurate to the depth and scope of their activities.

· A new banking culture taking root in the industry with emphasis on sound corporate governance, effective risk management, t ransparency and disclosure, as well as sound business ethics.

· The improvements being recorded in corporate governance and r i sk management, as well as the impact of Asset Management Corporation of Nigeria (AMCON), manifesting in the significant reduction in the ratio of non-performing loans (NPLs) to total credit in the banking sector.

· Also a considerable improvement in the macroeconomic environment with a broadly stable naira exchange rate sustained for over 18 months, and inflation rate moderating to a single digit of 9.3 per cent.

· The recent take-over of the erstwhile Afribank, BankPHB and Spring Bank Plc. by AMCON following the intervention of the N iger ia Depos i t Insurance Corporation (NDIC) and the conclusion of the mergers and acquisitions involving the five remaining intervened banks which has restored significant value to

This is an extract of the keynote address given by Dr. Kingsley Chiedu Moghalu at the October 2011 Forum of BDAN in Lagos. Dr Moghalu is Deputy Governor of the Central Bank of Nigeria in charge of the Financial Sys tem Stab i l i t y ( FSS ) Directorate. He is responsible for the implementation of far-reaching reforms to enhance the quality and stability of banks and other financial institutions. He is also a member of the President of the Federal Republic of N i g e r i a ' s E c o n o m i c Management Team (EMT).

7The Bank Director

B a n k i n g f o c u s

Banking on Reformthe affected banks and stability to the banking system.

The reform, which has been described as a success by pundits, is as unique in its innovativeness as it is in its efficient execution. This was demonstrated in a number of unique actions and outcomes which revealed that:

· In line with the resolve and commitment

of the CBN, no bank failed or collapsed

and no depositor in any Nigerian bank

lost any funds on account of the banking

crisis.

· No funds from the government treasury

was utilized to bail out banks, making

Nigeria's the only banking system crisis

that was resolved without recourse to tax

payers' funds.

The unique features of AMCON played a

stabilizing role. Unlike “bad banks” in other

jurisdictions, AMCON is a comprehensive banking

sector stabilization vehicle · c o m b i n i n g t h e

mandate to buy non-performing loans,

recapitalize distressed banks and become a

(temporary) shareholder, and restructure debt.

While noting the significant success achieved so

far, Dr. Moghalu emphasized that it is important to

reflect on recent emerging developments

particularly the US debt crisis and the consequent

sovereign rating down-grade by Standard & Poor's

(S & P) as well as the economic crisis in the

Eurozone countries. What do these developments

portend for global financial stability and by

extension the Nigerian financial system? In a

scathing comment on the developments in the US

and Europe, Christine Lagarde, Managing Director

of the International Monetary Fund (IMF) recently

declared that “there are risks emanating from the

US and Europe”. Are we in the throes of another

gathering storm that could crystallize into yet

another global financial crisis? What is the fire next

time? How resilient are Nigerian banks to

withstand another externally induced shock? How

prepared are the various stakeholders?

Indeed, considering the huge consequences of a

banking crisis that has been witnessed, the future of banking cannot be left for the banks alone to decide. It is a task that requires the individual and collective contribution of stakeholders, with each playing its role effectively.

He referred to the umbrella body of non-executive directors of banks in Nigeria, BDAN, as having an important role to play as a key stakeholder through the continuous improvement of the knowledge and competence of Bank Directors, for the purpose of promoting sound corporate governance and ethical practices within the Nigerian banking industry in line with its mandate. Bank directors, being key decision makers in the industry, need to be abreast of how these changes will shape the future of banking in Nigeria, Dr. Moghalu's keynote address dwelt on seven key issues which he believed has implications for the future of the banking sector in Nigeria. They include

The New Supervisory and Regulatory Paradigm

in Nigeria

The New Banking Model and its Implication

Global Trends and the Future of Regulation

Banks’ Contribution to the Real Economy

The Importance of Trust

Financial Inclusion

In conclusion, he stated that the resolution of the banking sector crisis in Nigeria is not a guarantee against another crisis in future. It is true that, with the average capital adequacy of the 20 commercial banks now at 17.12%, Nigerian banks are now the most capitalized in Africa. Yet, whilst it is obvious that the nature of banking has changed as a direct consequence of the reforms, and no doubt useful lessons have been learnt from the experiences and events of the last four years, the responsibility falls on all stakeholders working in collaboration to prevent the next crisis and create a more durable framework for financial stability. In this regard, Dr. Moghalu expressed hope that the CBN will over the next 12 months pursue the following strategic priorities as part of a longer term strategy to respond to future cyclical threats to the financial system:

Develop and establish a framework for the resolution of banking crisis in future, with strong scenario planning.

Develop and implement a strong macro-prudential framework that anticipates a n d a d d r e s s e s t h e s e v e r a l macroeconomic imbalances, shocks and systemic exposures to which the banking and wider financial system in Nigeria is vulnerable, including global economic dynamics.

8The Bank Director

The Olor’ogun (Dr.) Sonny F. Kuku, current President and former Engr. Ashim Oyekan at the 14th AGM of BDAN recently

13The Bank Director

T h e D i r e c t o r ' s H e a l t h

ea, otherwise known as Camellia Sinensis, no doubt, is one of the commonest beverages in Tevery body's menu today. While most people

look at it as a source of refreshment (i.e. something to sip while reading the newspapers in the morning), it is somewhat idolized in the Asian parts of the world where major State receptions are incomplete without it.

Origin The origin of tea as a beverage seems unclear, but history has it that it dates back to the year 2737 BC, when a camellia blossom drifted into a cup of boiled drinking water belonging to Emperor Shen Nung and instead of having it removed from the boiling water, he asked that it be retained. On tasting it, he discovered that it gave off a rich, alluring aroma that he commanded that this leaf be made not only an important part of his daily beverage, but that its bushes be planted in the gardens of his palace. Thus the custom and origin of brewing fresh leaves in hot water (tea) began.

Types All teas are produced from a plant called Camellia Sinensis. Different varieties, however, exist which can be identified by such parameters like the region where it was grown, the time of year when picked, the processing methods, taste, health benefits and level of caffeine. These include:

White Tea

This is the purest and least processed of all teas. It

comes as a loose leaf which, when brewed, shows

a light colour and flavour. It contains healthy

antioxidants and is best for skin and complexion.

With very little caffeine, white tea is prized for its

The Healing Power of Tea

mild and delicate taste, a major reason it was called

the Emperor's Drink in the nineteenth century.

Green Tea Because it is the beverage of choice in Asia, green tea is the most popular type of tea. Sometimes, they are scented with flowers or mixed with fruits to change their scents and flavours. It also contains healthy antioxidants and helps to regulate cholesterol levels by keeping them within normal range and to maintain good skin and healthy teeth, and can be used as part of your diet to maintain a healthy blood sugar levels.

Oolong Tea This is full-bodied specie with a rich flavour and sweet aroma. It is semi-fermented. Oolong teas can be a healthy part of your weight loss plan, little wonder why it is most commonly served in Chinese restaurants.

Black Tea Black tea is fully fermented and helps to maintain cholesterol at levels that are already within the normal range. It also helps in maintaining cardiovascular function and a healthy circulatory system. Black tea is the most popular type of tea. Herbal Tea Also referred to as tisane because it doesn't contain any leaves from the Camellia plant family, herbal tea contains herbal infusions (made from pure herbs, flowers, and fruits) which make them caffeine-free and rich in vitamin C.

Rooibos or Red Tea Rooibos tea, or Red tea, is made from a South

This is an article submitted by Mrs. Foluke K. Abdul-Razaq, a Director of United Bank for Africa where she serves as the Chairperson of Board Credit Committee, Member of Board Audit Committee and Member of Nomination & Governance Committee. She is also the vice – president of Bank Directors Association of Nigeria.

African red bush. It is a healthy source of vitamins and minerals and contains active antioxidants. Naturally caffeine-free, the red tea helps to promote digestion, support immunity and promote healthy skin, teeth and bones.

Mate Tea This is the coffee lover's favorite tea. Made from the leaves and twigs of the yerba mate plant, it gives the same energy as coffee without the jitters. They increase appetite and contain 21 vitamins and minerals.

Blooming Tea Also called artisan or flowering teas, these teas actually 'bloom' as they steep. They are hand-tied by tea artists and often include some type of flavor or scent along with the beautiful design.

Importance Tea is a good beverage. Generally it carries anti-cancer properties of polyphenols which helps the body to fight cancer. It also prevents blood from clotting and helps to decrease cholesterol levels and risk of heart disease. Research has also shown that having 2 cups of tea every day can reduce the risk of developing ovarian cancer by 50%. Other benefits include:

? Lowering cholesterol ? Weight loss by burning calories ? Reduction of high blood pressure ? Prevention of arthritis ? Boosting of the immune system ? Lowering of blood sugar ? Prevention of cavities and tooth decay ? Slowing down the aging process ? Reduction in the risk of heart disease ? Reduction in the risk of stroke

Conclusion Make a point of taking time out to enjoy, taste and appreciate tea every now and then. To do this, sit down in a pleasant environment away from your desk or computer avoiding excess noise and stimulation. This invites warmth, calm and nourishment to your senses and body. Also, when business and work seems so stressful, do yourself the favour of inviting a friend for a cup of tea in a quiet and serene environment and enjoy a boost from the healing qualities of tea and friendship preferably in a new café and new location where you meet different people. This will shake off any overwhelm and put things back into perspective again.

Source:

1.www.foodeditorials.com 2. www.ealingphilosophy.com

14The Bank Director

T h e D i r e c t o r ' s H e a l t h

The Healing Power of Tea

Each year the World Health Organization (WHO) celebrates World Health Day on 7 April to mark the anniversary of the

founding of WHO in 1948. A topic is chosen that highlights an area of priority for the health of the world. The theme of World Health Day in 2012 is "Good health adds life to years" . Quality along with quantity of life seems to be the message for this year. The focus will be on how good health throughout life can help us lead full and productive lives and be a resource for our families and communities. It provides an opportunity for individuals and corporate bodies to initiate collective action to protect people's health and well being.

What is the imperative for addressing 'quality issues' of health in the workplace? Today's workplace demands more from employees and key decision makers than it has ever done before, particularly in the financial services sector. The world economy is on the brink of another downturn. Global economic growth started to decelerate in 2011 and this economic slowdown is expected to continue into 2012 and 2013. The United Nations baseline forecast for the growth of world gross product is 2.6 per cent for 2012 and 3.2 per cent for 2013, which is below the pre-crisis pace of global growth , . Some of the financial

turmoil in Europe has spread to developing and other high-income countries, which until earlier had been unaffected. This has pushed up borrowing costs in many parts of the world, pushed down stock markets and world trade has slowed sharply. The key to riding this storm may be in the quality of leadership available to individual companies, institutions and national governments.

Executive health is also about the quality of thought that informs decisions and the accuracy of judgment in a dynamic and ever changing business environment. Psychologists have coined the interesting phrase 'presenteeism' to capture the apparently healthy but sub-productive segment of the workforce. Absenteeism is being sick and staying away from work. What is Presenteeism? Presenteeism is being sick but still coming to work. It is defined as loss of productivity resulting from workers who are present but affected by health problems and/or personal issues . Even though physically present at work, they are unable to fully perform their duties and are more likely to make mistakes in their judgment. Researchers believe that it accounts for more aggregate productivity loss than absenteeism . Health and wellbeing is a critical factor for success in today's business world.

For leadership at management level, health goes well beyond turning up at work.

The Business Case for Health and Wellbeing in 2012

Dr Bolaji Obadeyi MBChB, MPH, is a Public Health practitioner with more than 25 years post-qualification experience in various aspects of preventive medicine including reform of health policy relating to the organization and financing of healthcare services. Her last assignment provided technical program support to the Nigerian Academy of Science under the African Science Academies Development Initiative (ASADI). Dr Obadeyi has been a regular facilitator at training programs for Nigerian financial institutions since 1996.

14The Bank Director

T h e D i r e c t o r ' s H e a l t h

Another factor to contemplate at board level is the impact of age on health. One of the considerations for a position on the board of a financial institution or a multinational would probably be qualitative experience garnered over many years of public service or engagement in the private sector. The board is not the place for 'kindergarten managers'. Years of experience constitute value-added in the boardroom. Unfortunately there appears to be an inverse relationship between health on the one hand and age as a variable. Age is not a disadvantage but calls for greater attention to health and wellness.

The functional capacity of an individual's biological system increases during the first years of life, reaches its peak in early adulthood and naturally declines thereafter. The rate of decline is determined, at least in part, by our behavior and exposure across the whole life course. These include what we eat, how physically active we are and our exposure to health risks such as those caused by smoking, harmful consumption of alcohol, or exposure to toxic substances. Taking dietary factors alone, it is said that food is not just about what we eat; it is about how much we eat, in what combination it is eaten, with whom we dine and what we choose to do after we have eaten it.

What then is the need to be established in respect of executive health? The primary need is to promote physical and intellectual health of bank directors. We need to develop and share information, skills and other resources that will give our health the same chance of success as we give our careers. This is particularly relevant as the Nigerian financial sector repositions itself for a better future. Innovation, enterprise, creative out-of-the-box thinking only comes from healthy bodies and exceptionally healthy minds. And so this column may not be directly concerned with diseases. Rather, it will take a pro-active, anticipatory approach to consider the determinants of disease for this elite sector of our population bearing in mind the demands and peculiarities of high-level positions in Africa. Health promotion, disease prevention, wellness, improved productivity are all

a developing country and will set the parameters for this column.

Why take this route? There are two options for achieving the goal of positioning oneself for enhanced work performance and improved qual i ty of thought. A contemporary approach that is gaining global acceptance is to be interested in health maintenance rather than the illness management. Wellness programs are built on this premise that promoting good health is more cost effective than managing an illness. The maintenance program is driven by each ind iv idua l tak ing more responsibility for his/her health rather than relying on the magic pill from the clinic.

The more traditional approach is hospital based, reactive, crisis oriented and we now know that it does not deliver the best results. As a newly qualified medical doctor, this is the approach with which I identified for years as a practitioner in industrial clinics. Over the years, I had to ask and answer a simple question several times over: "What if I had seen this manager 6 months ago, given this counseling on lifestyle changes and followed him up? Wouldn't the result be different from the crisis we have on our hands today?" A particular case was life changing for me. I was working in the insurance industry and had to conduct comprehensive medical examinations for clients proposing to purchase life insurance. One of such high-end clients had his office on the 14th floor of a building on Broad Street in Lagos. I was excited to do this particular medical; after all how many times do you get to see top management clients in the penthouse suite? In fact, this

particular office suite had a dedicated elevator reserved for that floor! My client turned out to be a very pleasant person with a curious sense of humor who apparently enjoyed the 20 minute diversion from his normally stressful day. After examining him, taking his blood and filling forms for imaging tests we exchanged pleasantries on my way out probably thinking our paths will never cross again. But it did. Twice.

The first time was at my instance. I received results of his blood work-up, which I was obliged to forward to the reinsurer. Looking through the result, some of his parameters were on the upper side of normal while many of them were frankly elevated. Yet, he was symptomless. He did not present in a hospital neither did he have any complaints on the day of examination. The ethics of medical examinations for insurance forbid the doctor from disclosing the results of these tests to the insuree. But how could I watch this pleasant gentleman stand on the precipice of health and look the other way? Against ethics, I called his office and made an appointment to see him as soon as possible. The following Wednesday, I shared the results with him and reiterated the urgency of changing his lifestyle even though he appeared to be in a relatively stable state of health. I promised to check up on him again but I never did.

Our second meeting was more fortuitous. I had gone to see a relation in hospital and walked past a patient with a heavily bandaged head in the hospital corridor. The patient was first to call me but I couldn't place his face or person even after rebooting my brain several times. He then reminded me of his 14th floor office and it flooded back to my memory. "Did you have an accident sir?" No, he replied. He was just recovering from brain surgery after a stroke. His neurosurgeon told him that the stroke could have been fatal if he had not made concerted efforts over the past year to manage his stress levels, lower his blood pressure, change his diet to drastically reduce his cholesterol levels and take up regular exercise. I remembered a particular challenge he had with alcohol and I wanted to know how he dealt with that issue. "Alcohol is history" he said. This was a chilling

14The Bank Director

T h e D i r e c t o r ' s H e a l t h

encounter. It was surreal. And it changed my point of reference for practicing my profession. I have since then always asked myself what we can do now with this 'patient-to-be' to ensure that he/she does not become a patient. And I never miss the opportunity to tell busy, stressed managers how to protect their health by making small but regular investments in health. After all, on a rainy day, one can only draw down on cumulative investments.

The strategy and thought process underpinning a bank director's health cannot be less robust. We cannot afford to take the traditional approach of waiting for patients to present in the hospital. We must collectively be on the look out for 'patients-to-be' and make sure they do not become patients. Considering that the nation is entrusting you with our collective resources, your health and wellbeing is paramount. What can you do today and now, that costs little but will have great impact for your health, wellbeing and productivity? How will you do it? When can you make these subtle lifestyle changes with the best results? How will know when you are successful in repositioning your health even as you strive to reposition your bank or financial institution?

The health promotion interventions and lifestyle adaptation being promoted today can hardly be considered groundbreaking. In fact many of them have been advocated since the time of Hippocrates more than 2000 years ago. He believed that positively moderating health revolved around key decisions and personal choices we make everyday rather than decisions we take in the face of a health crisis . The benefits of this proactive approach are obvious and numerous. Nonetheless I am aware that managers are often more concerned about cost. In the context of this business case what is the cost of health and the cost of illness?

Health economists have done extensive work on calculating the value of health/life and the cost of illness. The consensus is that it is difficult to place monetary value on a human life although there are various tested techniques for estimating the value of life. Determining the cost of illness appears to be easier. The full cost of absence due to illness is calculated to be more than four times total medical payments when the productivity loss from absence is added. I believe however, that the real cost of illness is personal. It is not only the cost of the

medical payments but also the opportunity cost of caregivers' time. It is the cost of lost man-hours, missed opportunities and sometimes lost opportunities. It is about the cost of recovery with loss of full capacity for speech, vision or movement. Its extremely difficult to put a figure on that - the real cost of ill health is personal.

That is why we must take a holistic view of health especially in light of the current demands of the economic challenges and

Q u o t e s o f Hippocrates - a m e d i c a l practitioner who is regarded as the father of medicine and author of the Hippocratic oath (circa 460-377 BC)

1. A wise man should consider that health is the greatest of human blessings, and learn how by his own thought to derive benefit from his illnesses.

2. If we could give every individual the right amount of nourishment and exercise, not too little and not too much, we would have found the safest way to health.

3. Walking is man's best medicine.

4. Everything in excess is opposed to nature.

5. There are, in effect, two things, to know and to believe one knows; to know is science, to believe one knows is ignorance.

6. It is far more important to know what

Sources:i.

ii.

iii.

v.

vi.

World Health Organisation 2012. Available at http://www.afro.who.int/en/media-centre/events/details/252-world-health-day.html Accessed on 29th February 2012

World Bank 2012. Global Economic Prospects Jan 2012: Uncertainties and vulnerabilities. Available at http://web.worldbank.org/WBSITE/EXTERNAL/EXTDEC/EXTDECPROSPECTS/EXTGBLPROSPECTS/0,, menuPK:615470~pagePK:64218926~piPK:64218953~theSitePK:612501,00.html on 1st march 2012.

United Nations 2012. World Economic Situation and Prospects 2012. Available at http://www.un.org/en/development/desa/policy/wesp/index.shtml. Accessed on 1st March 2012iv. Investopedia. Available at http://www.investopedia.com/terms/p/presenteeism.asp accessed 1st March 2012 Integrated Benefits Institute 2011. The Business Case for Managing Health and Productivity. Available at http://www.acoem.org/uploadedFiles/Career_Development/Tools_for_Occ_ Health_ Professional/Health_and_Productivity/IBIFull-CostResearch.pdf Accessed on 29th February 2012

Brainy Quotes. Available at http://www.brainyquote.com/quotes/authors/h/hippocrates.html Accessed on 29th February 2012

person the disease has than what disease the person has.

7. Everyone has a doctor in him or her; we just have to help it in its work. The natural healing force within each one of us is the greatest force in getting well. Our food should be our medicine. Our medicine should be our food.

8. Any man who is intelligent must, on considering that health is of the utmost value to human beings, have the personal understanding necessary to help himself in diseases, and be able to understand and to judge what physicians say and what they administer to his body, being versed in each of these matters to a degree reasonable for a layman.

9. Even when all is known, the care of a man is not yet complete, because eating alone will not keep a man well; he must also take exercise. For food and exercise, while possessing opposite qualities, yet work together to produce health.

10. Prayer indeed is good, but while calling on the gods a man should himself lend a hand.

the growing cal l for innovat ion, resourcefulness and ingenuity in the Nigerian financial sector. The Director's Health will position itself to be the resource of first choice for top rate, cutting edge information on executive health and wellness. The objective is to identify the patient-to-be and steer him/her towards health, away from illness.

Our paths may cross; it does not have to be on a hospital corridor.

9The Bank Director

Mrs. Foluke K. Abdul-Razaq, Vice President, BDAN at the 14th AGM of BDAN recently in Lagos

15The Bank Director

Cashlite, Secureand Virtual

C u r r e n t M a t t e r s

Introduction / background

This presentation describes how Chams see the development of this industry going forward based on its experience over the last twenty-six years in the provision of identity management and electronic payment solutions to the financial services industry.

Indeed we have witnessed more technological advancement in banking technologies and processes in this year than the past five decades combined. The next few months and years promise to be very revolutionary for your industry.

Moreover, I think we will have a CASHLITE and not Cashless Nigeria. No economy in the world has reached that utopian state of Cashlessness yet, as far as we know. Becoming Cashlite, will substantially reduce the terrible wastes in currency management, corruption, terrorism, robberies and business risk. It will promote efficiency, accountability, non-repudiation and rule of law in our society.

When the Cashless/Cashlite program of CBN is combined with the Identity Management program, three of the major fundamental issues confronting you as banker KYC, PKI, and Non-repudiation of transactions would have been resolved. Chams Consortium is implementing the Identity Management Program with the Federal Government through NIMC.

The future we seeThe Banking industry and its stakeholders have grown significantly over the years. Despite all these, a large percentage of the country remains unbanked. To reach out this population, we will need even more innovative products and a spirit of exploration to go beyond the orthodoxy of serving urban markets to creating products that truly serve the needs of our rural, agrarian and remote populations.

It is crucial that we continue to expand access to financial services to the unbanked, across the country and to create effective and secure

The Future of Banking in Nigeria:

instruments to serve the unbanked, This will deepen the revenue base for the nation as more activity is brought into the formal sector and increase the deposit base of our banks as a larger portion of the economy comes into the formal economy.

ReformsIt is difficult to ascertain what role the Bank Directors will play in driving the reforms. The roles you ought to play in strategies and policies are crucial and will even become more crucial with the new waves of reforms coming your way. Reforms have almost been the exclusive preserve of the government and the question is, should it be so?

Some of the benefits of being proactive include: - Corporate governance - Lowering the cost of transaction - Reaching the unbanked profitably - Resolving Security issues – physical / electronic - Proffer locally based and sustainable technology solutions. - It allows a structured approach to examine successful models and solutions in similar environments with regards to: Mobile banking; and The future innovation of Electronic Wallets

The future is in your hands or should I say in our hands. All the points earlier mentioned can be expanded to further buttress what needs to be done for the future of banking to be relevant and secure in our environment.

We commend our CBN for the mobile licenses recently granted and with more to come in the next few weeks. In many parts of this country, a mobile phone is the most sophisticated technology available. Now imagine that with a little cooperation between the banks, the telecoms and mobile banking operators, we can create another industry as large and transformative to the Nigerian public.

We need to break out of the current models of banking with branches, to engaging and empowering the populace to act as middle-men in

This is an extract of a paper presented by Mr. Demola Aladekomo at the October 2011 Forum of BDAN in Lagos. Mr Aladekomo is the Group Managing Director of Chams Plc. An Alumni of university of Ife, University of Lagos and The Lagos Business School, he is also the President of the Nigerian Computer Society and the Vice president of The Lagos Business School Alumni Society. Mr. Aladekomo is one of the pioneers of the N i g e r i a n I n f o r m a t i o n Technology Industry especially in the Payment and Identity fields and he established Chams in 1985.

transaction processing. We need to share or transfer some of the risks to a lower level business transaction. We need to start thinking and finding solutions. The current western models are expensive to run and maintain and they have shown huge cracks.

ConclusionIn conclusion, we must diversify our banking products and deepen service, not only in the urban areas but also in the rural areas. If it is not profitable to bring bank branches to these areas, then let the banks work aggressively to support mobile and terminal distributors who can bring alternative modes of service to them.

The Bank Director's Association, The Banker's Committee and all of you in this room have it in your power to play a fundamental role in increasing the nation's prosperity by boldly pushing banking to the unbanked,

In a report from 2010, the McKinsey Global Institute estimates that Nigeria's manufacturing and services account for less than 45% of Nigeria's GDP. As access to financial services expands, we have the opportunity to raise that number, helping reduce the nation's dependence on oil, create prosperity and financial independence for a larger portion of the public.

These technologies have in them the power to be truly transformative; to reduce waste by making business more efficient and encouraging entrepreneurship and giving banking access to people who might not otherwise have it.

As we all work towards a future of banking in Nigeria that is cashlite, secure and virtual, we wish you our Bank Directors very fruitful deliberations.

Thank you for your time and God Bless You.

C u r r e n t M a t t e r s

The Future of Banking in Nigeria:

THE ECONOMY AND BANKING TERRAIN

16The Bank Director

Integration of virtual bank Account for mobile platform with POS terminals for phone POS paymentPervasive usage of Bank debit cards for POS transactions

Integration of virtual bank Account for mobile platform with POS terminals for phone POS paymentPervasive usage of Bank debit cards for

POS transactions

11The Bank Director

Mr. Sam Cookey Jr. at the 14th AGM of BDAN in November, 2011

17The Bank Director

Significant opportunities available to various stakeholders

Stakeholder/Expected Benefits Areas to support (not exhaustive)

Government

? Optimize tax revenue collection ? Increased economic growth

(positive correlation with increased payment efficiency)

? Increased financial inclusion

? Tax incentives to drive adoption of electronic payments

? Laws to support electronic processing and payments

? Continued support of E-payments drive through own internal processes

Consumers

? Faster, easier payments ? Increased convenience/access

(more payment options)

? Reduced risk of robbery

? Consumer sensitization and awareness ? Consumer education-knowledge of their

rights

? Feedback forums to regularly engage various customer segments and monitor

quality of dispute resolution

Corporations

? Better access to capital due to shorter payment processing times

? Increased efficiency of payment processes and accounting

? Reduced revenue leakages ? More efficient treasury

management

? Embrace alternative channels – for internal use and dealing with 3rd parties

? Sign-up for Direct Debit (where applicable)

? Transfer some efficiency benefits to customers via incentives to encourage e-channels

Banks

? Efficiency through electronic payment processing

? Reduced cost of operations (cash handling)

? Increased banking penetration

? Increase availability, functionality and dispute resolution process for e-channel solutions

? Begin customer engagement on alternative platforms now and participate in engagement sessions

? Order POS terminals and source merchants

? Leverage NIBSS service offerings

This list has been culled from a paper presented in October 2011at the last BDAN forum in Lagos by Ms. Eyitope St. Mathew-Daniel, “Cash-Lite Lagos: An Assessment of our State of Readiness.” Ms. Eyitope St. Mathew-Daniel is the Head, Shared Services, Central Bank of Nigeria

Question: What is your experience so far with “Cashless Lagos”

went grocery shopping sometime in January and I could not pay with

my card because the POS was not functioning. I was given the goods on Ithe condition that the teller follows me to a nearby ATM to retrieve their

money. On getting to the ATM of a very prominent bank, the machine was

not dispensing cash. You can imagine my frustration at the system. How

can we say we are ready for a cashless society when all the infrastructure

are not put in place?”

- An HR Management professional, wife and mother

had a funny experience at a bank weeks ago. I sent my accountant to

draw N750k (on a company account to which I am sole signatory) and Iforgot it was Cashless Lagos (sic). He was sent back. I called the Head of

Operations of the bank (branch) and threatened to close the account if

they closed before I got the money. They got creative! I was told to write 5

cheques for the same guy of 150k each. He came back with my 750k and

everybody was happy!

- Printing Press Business Owner

e are doing a turnover of over a million (naira) on the average

per day {monday - friday}. In preparation for the cashless WLagos, we applied for the POS terminals from our bankers

(please excuse my not mentioning them) since last year. I personally signed

the documents for the application since last year. We, as at this moment

have not received any terminals. Our conclusion as a company is to open

several accounts for our receipts within the same bank or several banks and

consolidate later or spend directly as the need arises.

- Owner of a medium sized poultry farm

n as much as I appreciate the idea...i think a lot still has to be done in the

area of awareness. More and more people still dont know what they Istand to benefit or why they should embrace the policy.

Personally, I am bothered with effective implementation...for instance I

had to travelled more than 1km few weeks back before I got an ATM to

dispense cash..."NO CASH" in most available ATMs...also, if i risked paying

for an Item online and at the point of making payment the receiving portal

and website of the issuing bank lost connection and my card already

debited..it will take more than 10days to get refund..a lot of issues like

these are still yet unattended to.

- Business Development officer for an indigenous social marketing site

18The Bank Director

Personal Feedback on Cashless Lagos

Personal Feedback on Cashless Lagos

“

support the cashless Lagos because it is easy, convenient, fast and reduces manpower

wasted on the road and in banks (my staff used to do a lot of this); but my major fear is for Ithe hackers as we're all aware of the increasing internet crime rate in this country of ours.

- Business Manager of an SME

rom experience in my company, as so many customers that make cash lodgment into our

accounts are already finding it very difficult as we mandated them to do fund transfer or Flodge in cheque. Though the penalty is yet to begin, it appears that it will slow down

predominantly cash based business transactions when fully enforced. From my view as a

church pastor - churches and related religious organizations where tithes and offerings are paid

mainly in cash, so many members may not be able to pay even when they are able and willing to

do so.

- Official at a company involved in manufacturing and sales of livestock feeds, Vet drugs, Poultry

Equipments and Day Old Chicks

y unit is involved in the payment of troops for various operations within Lagos and

the country at large. The Lagos state Operation Mesa comes to mind. The soldier to Mbe sent on a mission must be paid his allowances (in cash) before he is even given a

weapon to go and prevent crime or terrorist. Telling him that funds will be paid electronically to

his account that he probably won't have access to throughout the operation will not fly. The

slogan here is that - his salary can go to his accounts for his family, but his operations allowances

must be paid to him CASH! We would get there but some of these policies require time…

- Finance officer in one of the arms of the military

o be honest, I have found it a bit inconvenient not being able to issue a cash cheque of

over N150,000.00 to a third party. It meant having to leave my desk to do this. But as Tusual, when there is a will, ...It simply means, I have to explore the other available

electronic transfer options

- Pharmacy business owner

adam, they one we have been doing, they have not given (remitted) us our money”

- the response of the cashier at a busy supermarket in Ebute Metta. I had to drive to Ma bank ATM to withdraw N40,000 to pay for my monthly shopping for groceries.

At another mega store, they only accept Visa Card from us, not Master Card nor Verve!

- Management Consultant, wife and mother

takes a pulse of a random selection of people living in Nigeria. They provide

feedback on a number of issues that change with each edition of the Bank Director.

Point of View

19The Bank Director

Personal Feedback on Cashless Lagos

“

20The Bank Director

P r u d e n t i a l G u i d e l i n e s

Introduction

The appraisal of facilities is one of the key functions of banks' Board of Directors and its management. The Code of Corporate Governance for banks in Nigeria, section 5.3.12, therefore, makes it compulsory for banks' Board to have a committee specifically dedicated to the appraisal of credits. Experience has however, shown that it is one of the most 'tricky' assignments of banks – both at the Board and Management levels. This difficulty has manifested in the high level of 'toxic' facilities within the Nigerian banking system, which contributed in no small way to the distress witnessed in the sector between 2008 and 2010. As a consequence, the CBN intervened, through the Asset Management Corporation of Nigeria (AMCON) to take about N 4 trillion of non-performing loans (NPLs) off the books of the banks.

One of the key constraints is 'time' – the need for the bank to quickly appraise a customer's performance so as to decide whether or not to avail him more funds. There is also the need to monitor the performance of facilities proactively so that corrective actions can be taken early enough before the facility becomes irredeemably bad.

Haircut adjustments, which was introduced into the Nigerian banking system in May, 2010, through the Prudential Guidelines (PG) for Banks, have globally proved useful in improving credit appraisal in the banking system.

Definition and Use of “Haircut” Adjustments in Nigeria

A haircut is defined as the percentage that is subtracted from the valuation of an asset that is being used as collateral for a facility to reflect the perceived risk of holding the asset. The process for haircut adjustment was introduced to encourage banks to utilize more credit enhancement and mitigation strategies. Haircut adjustments are also used for other purposes, including: for the calculation of capital requirement and in setting margins.

Collateral instruments that are eligible for haircuts in the Nigerian banking sector include: · Cash (as well as certificates of deposit or comparable instruments issued by the lending bank) or

deposits with the bank which is incurring the counterparty exposure)· Treasury bills and other government securities.· Quoted equities and other traded securities.

“Haircut” Ajustments – A Handy Tool for Quick Basic Credit Appraisal

This is an article written by Mr. Amachukwu C. Okezie, a deputy director of the Central bank of Niger ia. He represents CBN on the council of BDAN

21The Bank Director

N e w s

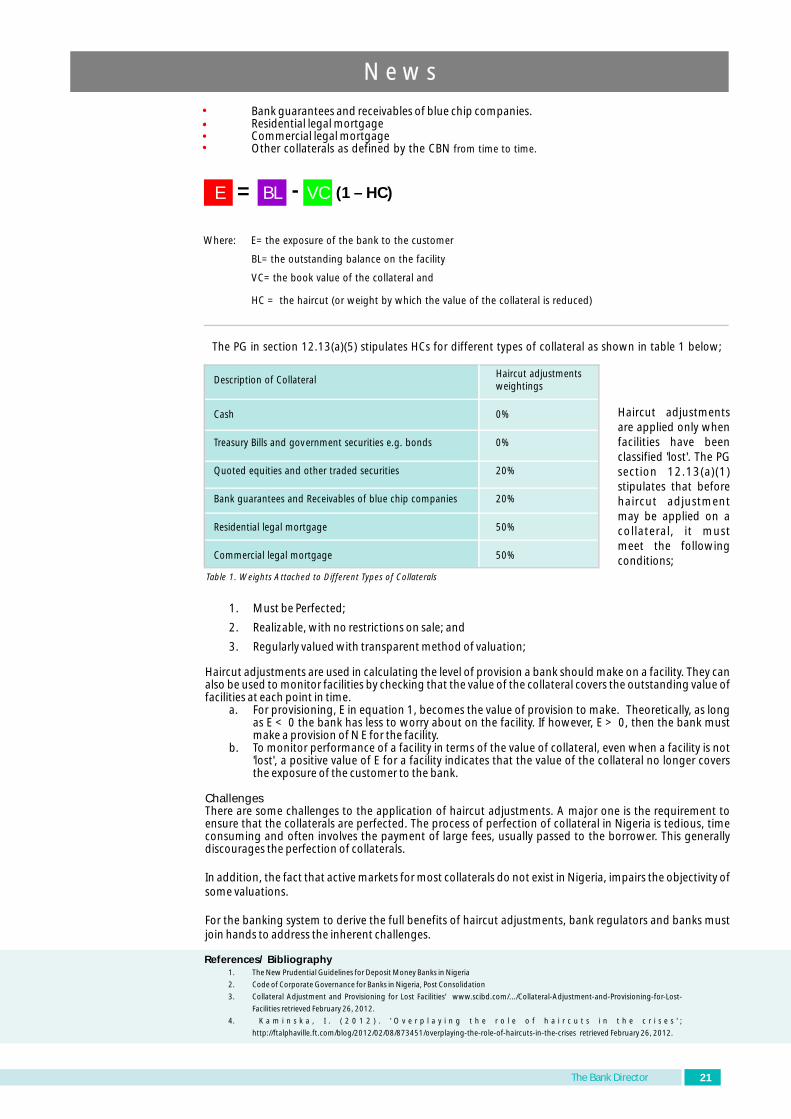

· Bank guarantees and receivables of blue chip companies.· Residential legal mortgage· Commercial legal mortgage· Other collaterals as defined by the CBN from time to time.

Where: E=the exposure of the bank to the customer

BL=the outstanding balance on the facility

VC=the book value of the collateral and

HC = the haircut (or weight by which the value of the collateral is reduced)

Description of CollateralHaircut adjustments weightings

Cash 0%

Treasury Bills and government securities e.g. bonds

0%

Quoted equities and other traded securities

20%

Bank guarantees and Receivables of blue chip companies

20%

Residential legal mortgage

50%

Commercial legal mortgage 50%

The PG in section 12.13(a)(5) stipulates HCs for different types of collateral as shown in table 1 below;

Table 1. Weights Attached to Different Types of Collaterals

Haircut adjustments are applied only when facilities have been classified 'lost'. The PG section 12.13(a)(1) stipulates that before haircut adjustment may be applied on a collateral, it must meet the following conditions;

1. Must be Perfected;

2. Realizable, with no restrictions on sale; and

3. Regularly valued with transparent method of valuation;

Haircut adjustments are used in calculating the level of provision a bank should make on a facility. They can also be used to monitor facilities by checking that the value of the collateral covers the outstanding value of facilities at each point in time.

a. For provisioning, E in equation 1, becomes the value of provision to make. Theoretically, as long as E < 0 the bank has less to worry about on the facility. If however, E > 0, then the bank must make a provision of N E for the facility.

b. To monitor performance of a facility in terms of the value of collateral, even when a facility is not 'lost', a positive value of E for a facility indicates that the value of the collateral no longer covers the exposure of the customer to the bank.

ChallengesThere are some challenges to the application of haircut adjustments. A major one is the requirement to ensure that the collaterals are perfected. The process of perfection of collateral in Nigeria is tedious, time consuming and often involves the payment of large fees, usually passed to the borrower. This generally discourages the perfection of collaterals.

In addition, the fact that active markets for most collaterals do not exist in Nigeria, impairs the objectivity of some valuations.

For the banking system to derive the full benefits of haircut adjustments, bank regulators and banks must join hands to address the inherent challenges.

E = - (1 – HC) BL VC

References/ Bibliography1. The New Prudential Guidelines for Deposit Money Banks in Nigeria

2. Code of Corporate Governance for Banks in Nigeria, Post Consolidation

3. Collateral Adjustment and Provisioning for Lost Facilities' www.scibd.com/.../Collateral-Adjustment-and-Provisioning-for-Lost-

Facilities retrieved February 26, 2012.

4. K a m i n s k a , I . ( 2 0 1 2 ) . ' O v e r p l a y i n g t h e r o l e o f h a i r c u t s i n t h e c r i s e s ' ;

http://ftalphaville.ft.com/blog/2012/02/08/873451/overplaying-the-role-of-haircuts-in-the-crises retrieved February 26, 2012.

22The Bank Director

This quote rings true of the findings from a recent

survey by the FITC on behalf of BDAN on

Remuneration of Non-Executive Directors in the

financial services sector. The report supported the

notion that payment of remuneration to non-

executive directors

(NEDs) of banks has

b e c o m e a v e r y

sensitive issue, as it

could affect the

motivation of the

staff, executives and

nonexecutives of

these banks. The aim of the survey was to develop a r e m u n e r a t i o n framework that will takecognisance of both the similarities and d i f f e r e n c e s i n c o n t e x t u a l characteristics of themember banks in Nigeria, reflect the r e n e w e d responsibilities of the board of thesebanks and evaluate best practices of their contemporaries in other nations.

T h e recommendations were based on research (using relevant and verifiable primary and secondary data), in the interest of all stakeholders, with a focus on business continuity and effective governance of respective banks.

From FITC's findings, remuneration payable to the NEDs of banks are mostly fixed by each bank. This is probably a reason for the distinct concern among the respondents, that their remuneration be increased. The findings also covered local and international issues of bonuses, share schemes,

“Different persons bring different levels of expertise to the Board. It is time to pay directors based on experience and performances and not flat across the board”– Chairman, Lloyds Business Group, 2010

Remuneration Survey

pension contributions for directors, cash retainer, influence of regulation, shareholder optics, board meeting fees and differentials, committee pay, decline of perquisite offerings relationship of size of bank to directors' remuneration, etc.

O n e o f t h e foundational principles g leaned from the report is that: “Director compensation should be approached on an overall basis, rather than as an array of separate elements”. Fur thermore , F ITC recommended three types of remuneration frameworks which any bank in Nigeria can choose and consider in d e v e l o p i n g a remuneration policy for i t s Non -E xecu t i v e Directors. The report also highlighted global practices on ways of ensuring principles of e q u i t y , f a i r n e s s , transparency, risk and accountability apply in any consideration of changes in stakeholder expectations and NED remuneration

At the end, FITC recommended number of general principles to guide remuneration of NEDs. BDAN has considered the possibility of making this survey a regular event and thereby advocate that, for enhanced corporate governance practices in the sector, publicly quoted banks fully disclose the philosophy and processes used in determining director compensation and the value of all elements of compensation, in their annual accounts.

B o a r d C o m p e n s a t i o n

For a copy of the report, representatives of organisations can contact the BDAN President, The Olor’ogun (Dr.) Sonny. F. Kuku OFR through the BDAN Secretariat 164/166 Murtala Muhammed Way Ebute Metta, Lagos Nigeria.

23The Bank Director

Lloyds Banking Group has canceled bonus

payments for its former chief executive and a

dozen other directors over their involvement in the

costly misselling of payment protection insurance.

Lloyds, struggling to emerge from part-nationalization, has set aside 3.2 billion pounds ($5.1 billion) to reimburse people persuaded to buy policies which they did not need. That's by far the biggest provision by any British bank.

Former CEO Eric Daniels will lose 40 percent of his bonus for 2010, Lloyds announced Monday, worth about 580,000 pounds ($920,000). The bank will withhold shares of that value which were part of his deferred bonus.

Four other directors would lose 25 percent of their bonuses, and eight senior executives would lose 10 percent, the bank said.

Lloyds Banking Group confirms bonus clawback

Source -

Olympus names boardmember as new president

Executive Directors ofWorld Bank visit Accra

News around the world

Scandal-hit Olympus on Monday 27 February, 2012, named current board member and executive officer Hiroyuki Sasa as its new president after one of the biggest financial scandals in Japanese corporate history. Olympus plans to hold an extraordinary general meeting on April 20, at which shareholders will be asked to approve the new 11-member management board, which includes eight people from outside the company. Olympus, embroiled in a cover-up of massive losses from the 1990s, said Monday its entire board will tender resignations at the April 20 shareholders' meeting.

Source – AFP & www.canadianbusiness.com

Executive Directors of the World Bank Group (WBG) were in Accra for a five-day familiarisation visit, between 2 – 6 February 2012 according to a statement from the Public Relations

Unit of the Ministry of Finance and Economic Planning of Ghana.

The visit afforded the Directors, who were accompanied by two Alternative Executive Directors and four advisors, the opportunity to acquaint themselves with the programmes and priorities of the Government and to ascertain the impact of the WBG's interventions in Ghana.

Source - www.ghanaweb.com

terling Bank recently announced the appointment of two non-executive directors Sto its board. They are Mr. Aderemi Kolarinwa

and Mr. Akanji Fashanu. Their appointment which has since been approved by the Central Bank, takes immediate effect.

Mr. Rasheed Aderemi Kolarinwa holds a Masters degree in Business Administration from the Schulich School of Business, York University Toronto, Canada in 1979 while Mr. Musibau Akanji Fashanu holds a Bachelor of Science degree in Economics from the University of Ibadan and is currently a Fellow of the Economic Development Institute (EDI) of the World Bank.

Source – www.sterlingbankng.com

Sterling Bank AppointsDirectors...

Australia: Proposed amendments to directors' liability laws have recently been released for public comment. The proposed amendments, including proposed amendments to the Corporations Act 2001, aim to ensure that where legislation imposes personal criminal liability for corporate fault, it is imposed in accordance with principles of good corporate governance and criminal justice and in a manner that will promote responsible entrepreneurialism and economic growth.

The proposed amendments form the first part of the Commonwealth government's implementation of the Council of Australian Governments' (COAG) Directors' Liability reform project. The exposure draft of the Personal L i a b i l i t y f o r C o r p o r a t e F a u l t R e f o r m B i l l 2 0 1 2 c a n b e f o u n d a t http://www.treasury.gov.au/documents/2300/PDF/Exposure_draft.pdf

Source: http://www.boardmatters.com.au

Changes to directors' personal criminal liability

First City Monument Bank (FCMB) Plc has appointed a new Management Team for the acquired FinBank led by Mr. Peter Obaseki as

Managing Director/Chief Executive Officer. This appointment comes following the recent approval by the Securities and Exchange Commission (SEC) of the acquisition of FinBank. His appointment takes immediate effect.

Source: Thisday Newspaper 15 Febraury 2012 pg 9

FCMB appoints management team for Finbank

24The Bank Director

The World Bank's Board of Executive Directors approved a US$15 million loan for the Municipal

Water Project for Armenia, Tuesday. The Project will support improvement of the quality and

availability of water supply in selected service areas of the Armenian Water and Sewerage Company

(AWSC), the WB Office in Armenia reports.

The activities proposed under the Project will directly benefit over 133,000 residents in the cities of Ashtarak (Aragatsotn region), Masis (Ararat region) and Echmiadzin (Armavir region) and 15 neighboring rural settlements. The investments will increase average daily supply of drinking water service from 12 hours to 17 hours, improve water quality, decrease water pollution risks and improve customer service. About 21,000 residents will also benefit from installation of new meters. The Project will generate multiple benefits for the public and private sectors by creating a more conducive environment for service delivery to users and stimulating economic activities.

Source - ARMINFO News Agency

News around the world

World Bank Board of Executive Directors approves US$15 million loan for Municipal Water Project for Armenia

$1.1 trillion - Islamic banking assets forecast by end of 2012 (Source: Ernst & Young (2011) World Islamic Banking Competitiveness Report 2011 – 2012; E&Y, Dubai).

$1.1

Billion – number of naira notes Nigeria prints annually (Punch newspaper)

Estimated number of days NEDs spend attending to board matters (FITC, BDAN Bank directors’ Remuneration Survey)

89 number of banks in Nigeria before July 2004 recapitalization

Estimated ratio of NEDs to EDs (Source: estimated from information on NDIC website)

3 10589 to3 2

The International Society for Performance Improvement (ISPI) has elected Dr (Mrs) Lucy Surhyel

Newman, Managing Director/CEO of FITC as its International Director. With this, she becomes the

first Non American/European to hold the International Director role, on the 9 – Member Board of the

professional association based in Maryland, USA since it was founded 50 years ago. She will serve in this

capacity for the period 2012-2014 over which she will work with the ISPI Board in championing policies

that will impact the growth of ISPI globally.

Dr (Mrs) Newman has over 24 years of experience derived from a development finance institution, four

banks in Nigeria, the Performance Improvement Practice of PricewaterhouseCoopers (PwC) Nigeria, and

FITC where she has been CEO since May 2009. She is also chairman, FSS2020 Human Capital Development

Implementation Committee; member, Sub-Committee on Ethics & Professionalism of the Nigerian

Bankers' Committee; and member, Executive Committee, West African Bankers' Association and member,

Bank Directors Association of Nigeria (BDAN). Under her leadership, FITC has witnessed a phase of its own

transformation, while assisting the implementation of various performance improvement programs for

organisations across sectors in Nigeria. In furtherance to this, she also got FITC admitted aa an

organisational member of ISPI as its principles compliment the FITC mandate of human capital acquisition

deployment development asn optimisation.

Lucy Surhyel NewmanElected International Director of the Global ISPI Board

F L A S H P O I N T SF L A S H P O I N T S

25The Bank Director

W o m e n i n L e a d e r s h i p

Background

Introduction

What is Affirmative Action and Enabling Legislation?

What is happening in Africa?

Much has been written and said about the absence of women in senior decision making roles in Africa. But we know that from the beginning, it was not so! In the past, we had women in Nigeria like Moremi, Ladi Kwali, Margret Ekpo, Sawaba Gambo, Mrs Ransome Kuti, Efunsetan Aniwura and so on. It was then practically impossible to ignore women in decision making process. Women and their views were considered to be important, critical and highly valued in the development of the society. Today, we are continuously faced with socio-cultural, political, institutional, and economic barriers which has resulted in less women occupying board of corporations, top government hierarchy and leadership positions.

Sixteen years ago, in September, 1995 to be precise, women around the world gathered in Beijing, China for the Fourth World Conference on Women. The product of that Conference was the Beijing Declaration and Platform for Action. The Beijing Platform had two goals: 1. To take measures to ensure Women's access to and full participation in power structures and decision making 2. To increase women's capacity to participate in decision-making and leadership Among the various action plans proposed to achieve the above goals include measures to protect and promote women's equal rights with men, creating a critical mass of women leaders in strategic positions, governments to establish the goal of gender balance; women to hold 50% of managerial and decision-making posts by year 2000, etc. The Dakar Platform which is the African regional version of the Beijing platform reinforces the objectives of the Beijing Platform as it seeks to promote affirmative action to develop a critical mass of women in leadership positions; ensure women take 35% of decision-making positions, reviewing and challenging electoral processes and discriminatory practices that hurt women's aspiration to political office, etc Sixteen years after, one can say that some level of progress has been made. We have seen women breaking the traditional boundaries and taking up ministerial positions hitherto dominated by men such as, Finance, Industry, Works and Petroleum Resources and acquitting themselves creditably. In terms of elective positions, we have witnessed female deputy governors, state assembly speakers, and a house of representative speaker. We have also witnessed more female representation in the national and state assemblies, as well as, more female Chairmen of Local Government Councils. The Federal Government has also put in place a National Gender Policy which stipulates 35% affirmative action for women in politics and public positions. In this paper, I want to focus on three key areas: " What is happening in Africa, " What is happening in Nigeria, and " What we need to do differently.

Affirmative action refers to policies that take factors including "race, colour, religion, gender, or national origin" into consideration in order to benefit an underrepresented group, usually as a means to counter the effects of a history of discrimination. It is a collective agreement to give preference to certain groups in a society in order to correct certain imbalances. The focus of such policies ranges from leadership, employment and education to public contracting and health programs. In this case, the affirmative action is to ensure that women who constitute 50% of our population have equal access to leadership positions as their male counterparts.An enabling act on the other hand is a legislation by which a legislative body grants an entity which depends on it for authorization and/or legitimacy the power to take certain actions. For example, enabling acts often establish government agencies to carry out specific government policies in a modern nation state. The effects of enabling acts from different times and places vary widely. In a nutshell, within the context of this paper, the enabling legislation is to provide legal framework for women to occupy leadership positions in institutions, corporations and government positions.

Progress report from other Countries in Africa shows that in South Africa, the ruling African National Congress (ANC) Committed itself to affirmative action by reserving 30% of parliamentary seats and 50% of local government seats for women. Uganda has created a policy that ensures that women constitute at least one third of any government committee and that each district selects one woman representative to parliament.

Appointing Women into Boards of Corporations, Companies and Government Owned Agencies; Will Affirmative Action or Enabling Legislation Work?

By Dr (Mrs.) Nike Akande OONDirector, Union Bank of Nigeria Plc

Women: Agents of change

This is an article submitted by Dr. (Mrs.) Nike Akande OON, a Non-Executive Director of Union Bank of Nigeria Plc and a current member of the BDAN council. Dr. (Mrs.) Akande is a former Minister of Industry, an Investment expert and a consultant.

Namibia has a quota system for its local councils which ensure that women fill a certain percent of the positions at the regional and local levels. Zimbabwe, Angola and Tanzania also have quota legislations that guarantees certain number of women in the legislative assemblies. In terms of actual representation of women in the national assemblies, South Africa leads other African Countries with over 29% women representation and this owes mainly to the affirmative action.

Notwithstanding the marginal progress made so far, we are still a long way from attaining the objectives of the Beijing and Dakar Platforms.

The present score card of women with elective positions in Nigeria is to say the least, worrisome. A comparative analysis of the performance of women in the 2007 elections and the recently concluded 2011 elections reveal that the fortunes of women appear to have declined. In 2007, we had six (6) Deputy Governors as against two (2) in 2011; nine (9) Senators in 2007 against seven (7) in 2011 and twenty-seven (27) House of Reps members in 2007 against 19 in 2011. As I speak to you, there is no woman among the principal officers of the two legislative chambers. In other words, there is a 0% representation of women in the leadership of the Senate and House of Representatives. Of the 36 State Assembly Speakers, only one is a woman. Of course, there is no female President, Vice President or Governor. This poor showing is in spite of the vigorous campaign by our dear first Lady, Her Excellency Dame (Dr.) Patience Jonathan, across the nation through her Women for Change Initiative (W4CI) advocating for 35% female representation in public offices. A major campaign promise of the President is to ensure that women enjoy at least 35% representation in decision making process.

Mr. President has started on a promising note with the appointment of 13 women (which is about 31%) as ministers. This underscores his willingness to abide by the affirmative action plan which the government has committed itself to. We hope that this will be sustained in board appointment for federal agencies.

However, we must note that no matter his good intentions and willingness to keep his campaign promise to women, there are a lot of factors and forces that come into play when it comes to sharing political offices. Goodwill and willingness alone cannot get us to the Promised Land. The fate of Hon. Mulikat Akande-Adeola is a case in point. In spite of Mr. President's support and the backing of her party, as well as being favoured by the zoning principle, she still lost in a manner that suggests that she probably lost on account of her gender. We all know that she would have been Speaker today if there is a constitutional provision for a woman to occupy one of the top four offices in the country. Some may argue that President Yar'Adua with Chief Obasanjo's support ensured that Hon. Patricia Etteh emerged Speaker of the lower Chamber in 2007. But we all witnessed what happened to her. It can arguably be said that she was removed on spurious allegation. Let us face the truth; except we work concertedly to get the Gender Affirmative action enshrined in the nation's constitution, the goal of the Beijing Conference will remain a mirage. If African countries like, South Africa, Angola, Zimbabwe, Tanzania, Namibia and Uganda have constitutional provisions for Gender affirmative action, I honestly see no reason why Nigeria does not yet have a constitutional framework guaranteeing 35% women representation in strategic decision making positions. It is against this backdrop that I think the topic: Appointing Women into Boards of Corporations, Companies and Government Owned Agencies; will Affirmative Action or Enabling Legislation work? is appropriate and timely. This is more important since the Beijing Conference targets 35% women representation in all areas of decision making and not just with respect to ministerial appointments. Whilst enabling legislation will create room and remove all obstacles - political, economic, social, cultural etc - impeding women's appointment into such strategic leadership positions, it is imperative to note that eternal vigilance on the part of women interest groups is needed to ensure absolute and sustained compliance. Enabling legislation is needed to empower women groups with the legal powers to enforce compliance just as vigilance, sustained advocacy and orientation are also required to prevent any form of manipulation. Interestingly, framers of the Nigerian constitution had the Federal Character principle enshrined in Section 153 of the 1999 Constitution (As Amended). This guarantees all geo-political zones/states fair/equal consideration in the appointments/recruitments into ministries and government agencies. A Federal Character Commission is established to monitor and ensure compliance by the Ministries, Departments and Agencies (MDAs). There is also an unwritten code which stipulates that the President and the Vice President, the Senate President and the Deputy, the Speaker and the Deputy Speaker, Governors and their Deputies do not come from the same geo-political zone. This code is strictly adhered to by all the major political parties. My question is: if we can have geographical balancing, ethnic balancing and to some extent religious balancing, why can't we have gender balancing? Do we not have enough qualified and competent women to man the positions? We have had women who have served with distinction and their performances were generally

What is Happening in Nigeria?

26The Bank Director

W o m e n i n L e a d e r s h i pWomen: Agents of change

Notwithstanding the marginal progress made so far, we are still a long way from attaining the objectives of the B e i j i n g a n d Dakar Platforms.

if we can have g e o g r a p h i c a l balancing, ethnic balancing and to s o m e e x t e n t r e l i g i o u s balancing, why can't we have g e n d e r balancing?