Cash Basis Accounting and Internal Controls fo r...

7

2/10/2017 1 Cash Basis Accounting and Internal Controls for Small Governments 10th Annual BIAS Rally February 23, 2017 Deborah Pennick, Program Manager Philip Mendoza, Local Government Support Washington State Auditor’s Office 1 Objectives Why SAO audits internal controls Management’s responsibility for internal controls Common internal control weaknesses Tools to design/implement effective internal control over financial statement preparation 2 Washington State Auditor’s Office Understanding internal controls over financial reporting Understanding the Entity and Its Environment Assessing the Risks of Material Misstatement Washington State Auditor’s Office 3 Understanding internal controls over financial reporting Necessary to properly plan the audit: • identify types of potential misstatements • consider factors that affect the risk of material misstatement • design appropriate audit procedures Washington State Auditor’s Office 4

Transcript of Cash Basis Accounting and Internal Controls fo r...

2/10/2017

1

Cash Basis Accounting and Internal Controls for Small Governments

10th Annual BIAS Rally February 23, 2017

Deborah Pennick, Program ManagerPhilip Mendoza, Local Government Support

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 1

Objectives

Why SAO audits internal controls

Management’s responsibility for internal controls

Common internal control weaknesses Tools to design/implement

effective internal controlover financial statement preparation

2W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Understanding internal controls over financial reporting

Understanding the Entity and Its Environment

Assessing the Risks of Material Misstatement

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 3

Understanding internal controls over financial reporting

Necessary to properly plan the audit:

• identify types of potential misstatements

• consider factors that affect the risk of material misstatement

• design appropriate audit procedures

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 4

2/10/2017

2

Understanding internal controls over financial reporting

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 5

Understanding internal controls over financial reporting

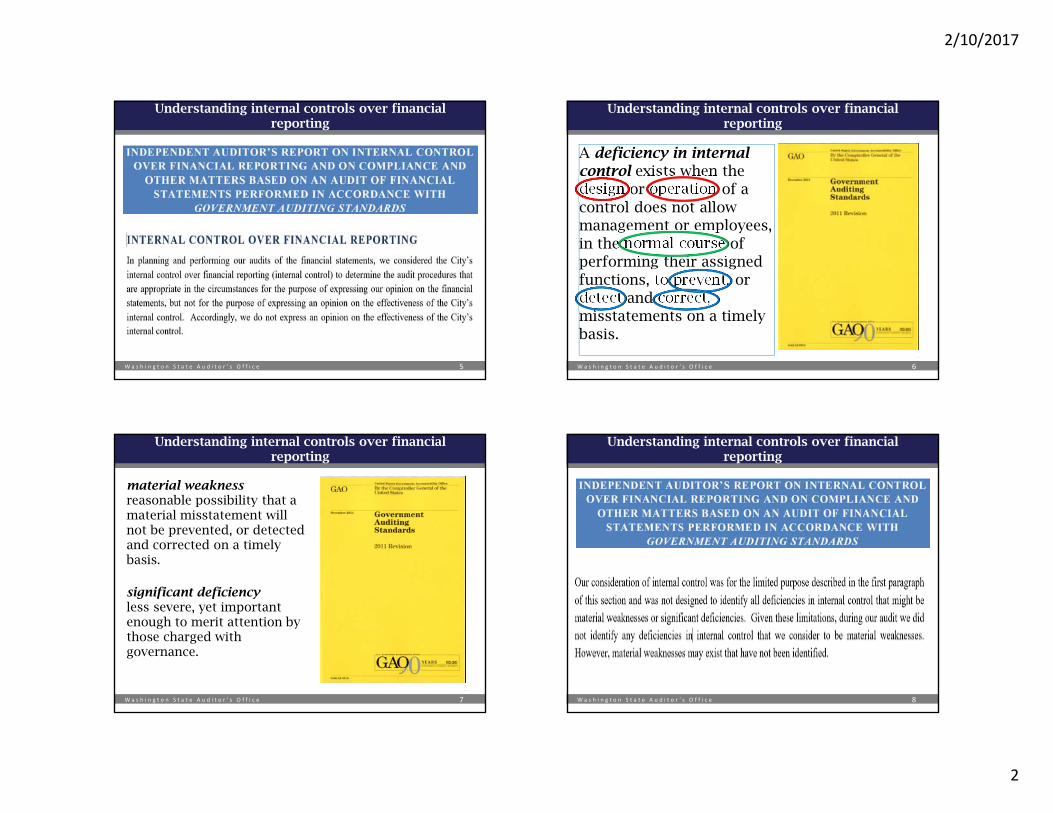

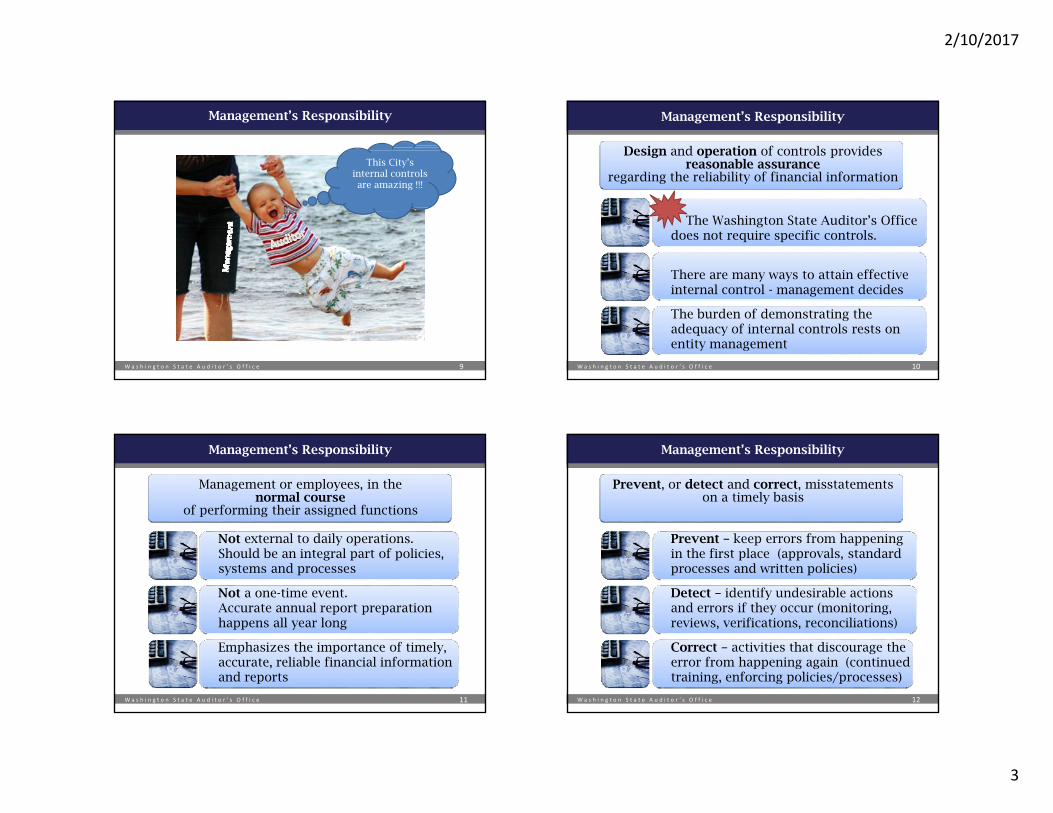

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis.

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 6

Understanding internal controls over financial reporting

material weakness reasonable possibility that a material misstatement will not be prevented, or detected and corrected on a timely basis.

significant deficiencyless severe, yet important enough to merit attention by those charged with governance.

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 7

Understanding internal controls over financial reporting

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 8

2/10/2017

3

Wa s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 9

This City’s internal controls are amazing !!!

Management’s Responsibility

The Washington State Auditor’s Office does not require specific controls.

There are many ways to attain effective internal control - management decides

The burden of demonstrating the adequacy of internal controls rests on entity management

Design and operation of controls providesreasonable assurance

regarding the reliability of financial information

10W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Management’s Responsibility

Not external to daily operations. Should be an integral part of policies, systems and processes

Not a one-time event. Accurate annual report preparation happens all year long

Emphasizes the importance of timely, accurate, reliable financial information and reports

Management or employees, in the normal course

of performing their assigned functions

11W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Management’s Responsibility

Prevent – keep errors from happening in the first place (approvals, standard processes and written policies)

Detect – identify undesirable actions and errors if they occur (monitoring, reviews, verifications, reconciliations)

Correct – activities that discourage the error from happening again (continued training, enforcing policies/processes)

Prevent, or detect and correct, misstatements on a timely basis

12W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Management’s Responsibility

2/10/2017

4

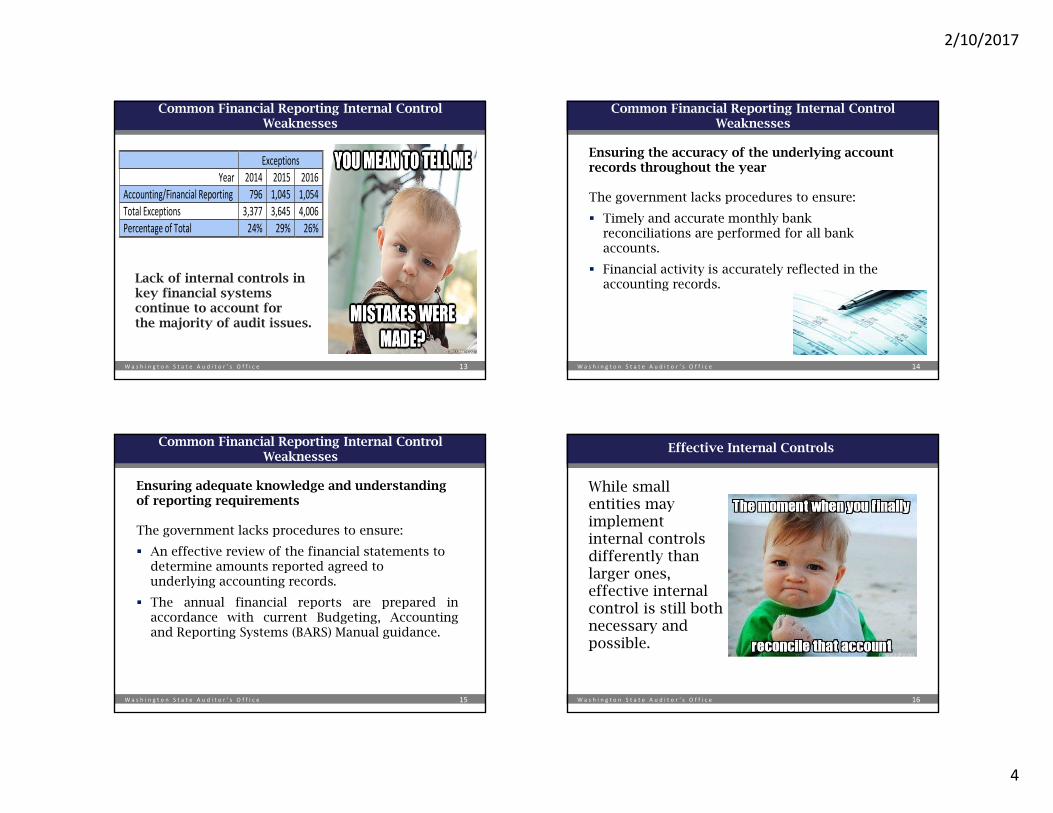

Common Financial Reporting Internal ControlWeaknesses

Exceptions Year 2014 2015 2016

Accounting/Financial Reporting 796 1,045 1,054 Total Exceptions 3,377 3,645 4,006 Percentage of Total 24% 29% 26%

Lack of internal controls in key financial systems continue to account for the majority of audit issues.

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 13

Ensuring the accuracy of the underlying account records throughout the year

The government lacks procedures to ensure:

Timely and accurate monthly bank reconciliations are performed for all bank accounts.

Financial activity is accurately reflected in theaccounting records.

14W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Common Financial Reporting Internal ControlWeaknesses

Ensuring adequate knowledge and understanding of reporting requirements

The government lacks procedures to ensure:

An effective review of the financial statements todetermine amounts reported agreed tounderlying accounting records.

The annual financial reports are prepared inaccordance with current Budgeting, Accountingand Reporting Systems (BARS) Manual guidance.

15W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Common Financial Reporting Internal ControlWeaknesses

Effective Internal Controls

While small entities may implement internal controls differently than larger ones, effective internal control is still both necessary and possible.

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 16

2/10/2017

5

Question

Are there resources that help facilitate our review of the financial statements and other internal control processes and procedures?

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 17

Checklist for Preparing Cash Basis Financial Statements

• Helps cash basis governments to review and check the financial statements for reasonableness and the most common errors

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 18

Checklist for Preparing Cash Basis Financial Statements

Control procedures identified within the checklist:

• Performed at Year-end

• Performed throughout the year

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 19

Checklist for Preparing Cash Basis Financial Statements

Most common areas of cash financial statements errors:

1. Journal entries

• Adequate and appropriate support• Review and proper posting

2. Funds

• Managerial roll-ups• Use of different types of funds

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 20

2/10/2017

6

Checklist for Preparing Cash Basis Financial Statements

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 21

Checklist for Preparing Cash Basis Financial Statements

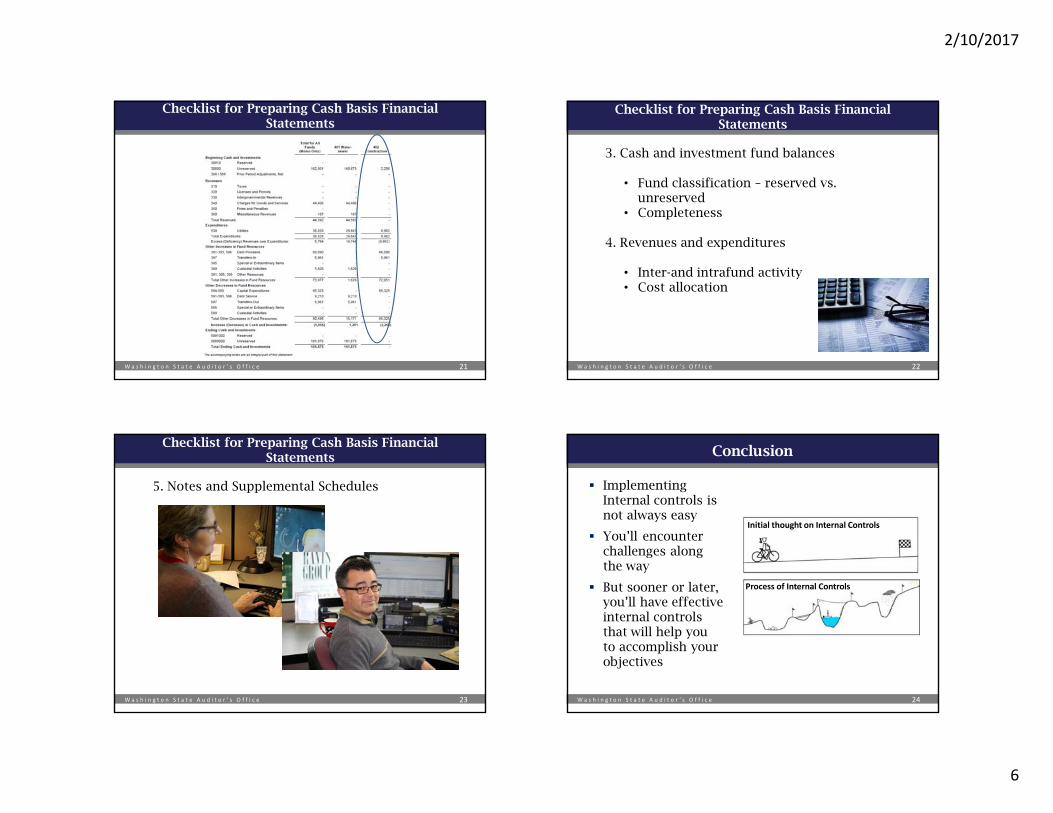

3. Cash and investment fund balances

• Fund classification – reserved vs. unreserved

• Completeness

4. Revenues and expenditures

• Inter-and intrafund activity• Cost allocation

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 22

Checklist for Preparing Cash Basis Financial Statements

5. Notes and Supplemental Schedules

W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e 23

Conclusion

Implementing Internal controls is not always easy

You’ll encounterchallenges alongthe way

But sooner or later, you’ll have effective internal controls that will help you to accomplish your objectives

24W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Initial thought on Internal Controls

Process of Internal Controls

2/10/2017

7

Budgeting, Accounting and Reporting Systems(BARS) Manual

Governmental Accounting Standards Board (GASB)

Local Government Performance Center (LGPC)

Municipal Research and Services Center (MRSC)

Available Resources

25W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Deborah Pennick, CPA Program Manager

[email protected](509) 334-5825 x108

Philip Mendoza, CPALocal Government Support

[email protected](360) 725-5557

26W a s h i n g t o n S t a t e A u d i t o r ’ s O f f i c e

Contact information