CASE STUDY – TRANSFORMATION€¦ · OCT 2006 – JUNE 2009. ... importantly is the change in our...

66

CASE STUDY – TRANSFORMATION Hizamuddin Jamalluddin May 2013 Strictly Private & Confidential

Transcript of CASE STUDY – TRANSFORMATION€¦ · OCT 2006 – JUNE 2009. ... importantly is the change in our...

CASE STUDY –TRANSFORMATION

Hizamuddin JamalluddinMay 2013

Strictly Private & Confidential

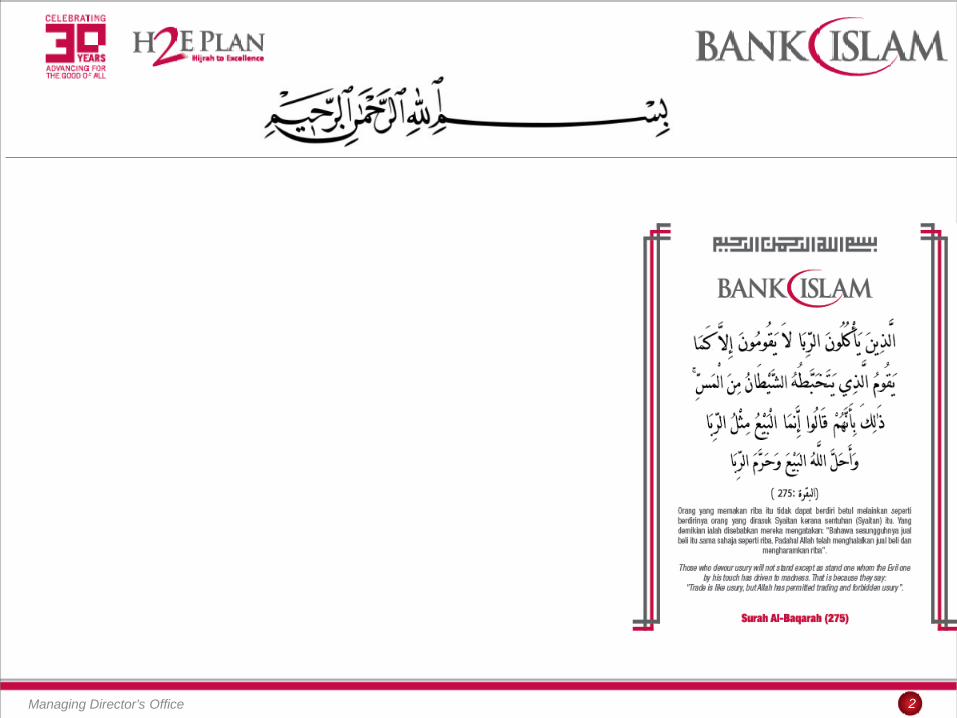

Managing Director’s Office 2

Managing Director’s Office 3

BACKGROUND

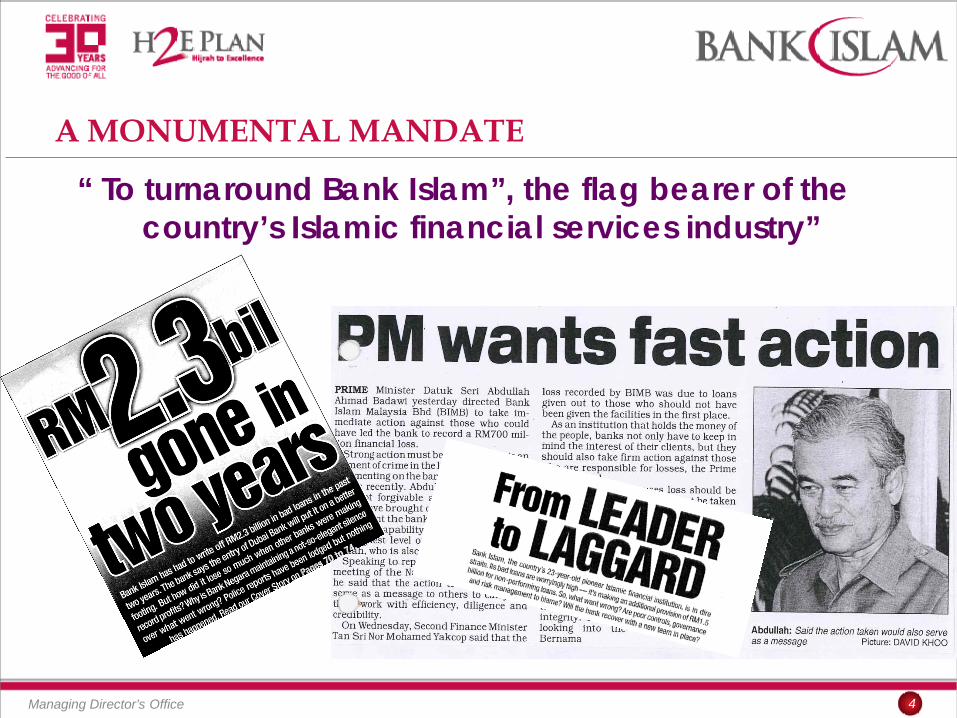

A MONUMENTAL MANDATE

Managing Director’s Office 4

“ To turnaround Bank Islam”, the flag bearer of the country’s Islamic financial services industry”

SIX FEET UNDER THE GROUND

Managing Director’s Office 5

… it was a big mess

LOSS BEFORE ZAKAT & TAX

Managing Director’s Office 6

Note : Deficit shareholders’ funds of RM277.8 million as at 30 June 2006, technically a defunct bank or no longer deemed as a going concern entity

SIX FEET UNDER THE GROUND…CONT

Managing Director’s Office 7

… a mammoth task awaits

ROOT CAUSE OF THE POOR ASSET QUALITY

Managing Director’s Office 8

…poor working culture and attitude… unable to offload NPF to Danaharta during financial crisis 1997/98

Managing Director’s Office 9

TRANSFORMATION JOURNEY

THE JOURNEY BEGINS

Managing Director’s Office 10

NEW BUILDING BLOCKS

Managing Director’s Office 11

OCT 2006 – JUNE 2009 JULY 2009 – DEC 2012

…in our pursuit to be a “Global Leader in Islamic Banking”

JAN 2013 – DEC 2015

TURNAROUND PLAN

Managing Director’s Office 12

RE-INVENTING BANK ISLAM

Managing Director’s Office 13

“Corporate Re-branding is not only limited to change our physical appearance i.e. logo, signage & branch model BUT more importantly is the change in our mindset & working culture i.e. to become more professional, knowledgeable, innovative and customer centric as well as to embrace other qualities as required by Islamic teachings”

“We need to have a new strategy and approach in the way we do business. We have to find our niche market. We should bank on our own strengths and capitalize them… and be more focused…on a total solution in the overall turnaround plan”

Dato’ Zukri SamatBank Islam Malaysia Berhad

- Feb 2007

TURNAROUND PLAN – FINANCIAL RESTRUCTURING

Managing Director’s Office 14

… moving out from crisis and to return to black

REORGANIZING THE BANK

Managing Director’s Office 15

BUILDING A STRONG & COMMITTED TEAM

Managing Director’s Office 16

…flat hierarchies ensured faster decision-making & reduced organizational complexity

REBUILDING THE BANK

Managing Director’s Office 17

BUSINESS TRANSFORMATION

Managing Director’s Office 18

CHANGE IN MINDSET

Managing Director’s Office 19

… evolution of mind and spirit toward a performance –based and customer service culture

FRANCHISE DEVELOPMENTS

Managing Director’s Office 20

ENHANCEMENT SERVICE DELIVERY TOUCH-POINTS

Managing Director’s Office 21

BRANCH NETWORKSINTERNET BANKING

CONSUMER BANKING CENTERS

AR RAHNU OUTLETS

BUREAU DE CHANGESMS BANKING

CORPORATE DESKTOP BANKING

ELECTRONIC BANKING CENTERS

BRANCH NETWORK

Managing Director’s Office 22

Perlis - 1

Kedah - 10

Kelantan - 11Pulau Pinang - 5

Perak - 9

Pahang - 9

Terengganu - 5

Selangor – 25Kuala Lumpur - 17

NegeriSembilan -5

Melaka - 4

Johor - 14

Sarawak - 6

Sabah - 5

Labuan- 1

Region Total

Central 42

Northern 25

Eastern 25

Southern 23

East Malaysia 12

Total 127… from 90 branches as at June 2006…127 branches as at end of 2012… 6 new branches in 2013 (Sungai Buloh, Bukit Indah (JB), Bandar Baru Tunjung (Kelantan) Sungai Petani (Kedah), Tabung Haji Convention Centre Sepang, & Senawang (N. Sembilan)

SELF SERVICE TERMINALS

Managing Director’s Office 23

ATM – 8 CDM – 4

CQM – 1 SP - 1

Location Type ATM

CDM CQM SP Total

Branch 271 197 109 43 620

Shopping Centers 94 14 4 1 113

Academic Buildings

119 19 4 4 146

Corporate Offices 69 28 11 4 112

Others 132 48 1 0 183

Total 685 306 129 52 1172

ATM – 31 CDM – 12

CQM – 6 SP -1

ATM – 30 CDM – 15

CQM – 6 SP -3

ATM – 2 CDM – 1

CQM – 1 SP - 1

ATM – 57 CDM – 26

CQM – 13 SP -4

ATM – 49 CDM –27

CQM – 10 SP - 4

ATM – 62 CDM – 34

CQM – 11 SP - 4

ATM – 39 CDM – 16

CQM – 6 SP - 1

ATM – 30 CDM – 12

CQM – 3 SP - 1

ATM – 38 CDM – 21

CQM – 7 SP - 2

ATM – 50 CDM – 17

CQM – 10 SP - 7

ATM -148 CDM – 53

CQM – 26 SP - 10

ATM – 31 CDM – 14

CQM – 6 SP -2

ATM – 78 CDM- 37

CQM – 16 SP – 7

ATM – 32 CDM – 17

CQM – 7 SP - 4

ATM – Automated Teller MachineCDM – Cash Deposit MachineCQM – Cheque Deposit MachineSP – Statement Printer

… continue to invest for customer’s convenience

BRAND EQUITY & POSITIONING

Managing Director’s Office 24

BANKING FOR ALL

BANKING FOR MUSLIMS

BRAND IMAGE– PRIOR TO 2007

Managing Director’s Office 25

NEW IDENTITY & BANKING EXPERIENCE

Managing Director’s Office 26

“…with the new feel and look, we hope to make Bank Islam more appealing and accessible to all”

…Dato’ Zukri Samat

BUILDING A VALUE –BASED ORGANIZATION

Managing Director’s Office 27

“Employer brand is a mirror image of customer/client brand because as an organization, employees deliver the touch-points that define customer’s experience of value proposition and brand. “

KEY DRIVER TO CUSTOMERS’ SATISFACTION

Managing Director’s Office 28

People Basic Shariah knowledge, Ethics, Islamic values, Courtesy and etc

Place/Presentation Ambiance, Accessibility, Branding, Signage, Marketing etc

Product Value Proposition, Transparency, Innovative, Differentiation and etc

Process

Paper-work, waiting time, hassle free, etc

Price Value, Price Option

TRANSFORMATION STAKEHOLDERS

Managing Director’s Office 29

• Negative• Often says ‘It’ll never work’• Has a ‘we’ versus ‘them’

mindset• Does not believe in brand

building• Does not see customer

experience as critical factor• Can exert negative influence• Resistant to change• Prefer the status quo

• Influencers within theorganisation

• Believes in branding• Has a positive and ‘can do’attitude

• Able to motivate and convertmindset of Skeptics andFence-sitters

• Agents of change• Views the customer experienceand other key touch points aspart of Branding process

• Indifferent towards the changeand brand building

• ‘Tidak apa’ attitude –Whatever goes-lah!

• Does not want to takeresponsibility

• Rather be passenger thandriver

• Can be influenced

Skeptics Fence-sitters Champions

TRANSFORMATION CHALLENGES

Managing Director’s Office 30

We can win if we help each other

I don’t agree with where we are going, I am changing course

What are they going to do to help me through this? Why am I here

with these people?

I will help for a while until I see a problem

I am afraid of change and what it may mean to my department

WORKING AS A TEAM

Managing Director’s Office 31

Follow the transformation Strategy!

Wow, Look at us go now!

I feel like I am a contributor!

This is fun!

What a team! What else can we do?

OBSERVED LEADERSHIP STYLE

Managing Director’s Office 32

COMMUNICATION STRATEGY

Managing Director’s Office 33

SUSTAINABLE GROWTH PLAN … ENDED DEC 2012

Managing Director’s Office 34

DRIVING INNOVATION

Managing Director’s Office 35

Prior 2009 2009 2010 2011 2012

Managing Director’s Office 36

KEY RESULTS

MEASURE OF SUCCESS

Managing Director’s Office 37

KEY FINANCIAL RATIOS

Managing Director’s Office 38

AuditedFY

June 07

AuditedFY

June 08

Audited FY

June 09

ActualFYE Dec 2010**

Audited FYDec 11 **

Actual Dec 12

IslamicBanking System

Banking System

PROFITABILITY

Return on equity (%) – based on PBT 23.3% 26.5% 16.5% 14.4% 18.5% 20.4% ^ 19.6% * 17.5% *

Return on assets (%) – based on PBT 1.4% 1.5% 0.9% 1.2% 1.6% 1.7% ^ 1.4% * 1.6% *

Cost Income Ratio (%) 68.2% 60.8% 56.7% 55.4% 53.8% 51.4% 46.1% * 46.6% *

Non-Fund Based Income Ratio (%) 9.0% 7.8% 10.3% 10.8% 13.8% 13.5% 11.0% * 19.6% *

ASSET QUALITY

Gross Non-Performing/Impaired Financing Ratio (%) 24.7% 21.2% 16.4% 4.5% 2.6% 1.6% 1.6% # 2.0 % #

Net Non-Performing/Impaired Financing Ratio - Less IA & CA (%) 11.4% 7.8% 6.7% 1.1% -0.2% -0.7% -0.3% # -0.02% #

Financing Loss Coverage Ratio (%) 67.7% 75.8% 80.8% 77.2% 106.2% 142.6% 119.3% # 100.9% #

EFFICIENCY

Financing to Deposits (%) 57.6% 52.0% 43.5% 45.7% 51.5% 61.2% 77.2% # 78.7% #

CAPITALISATION

RWCR (%) – before proposed dividend 12.0% 12.9% 13.6% 16.8% 16.9% 14.1% 14.3% *

# 15.2% *#

…healthy capitalisation

…financing-to deposit ratio inching closer to optimum level

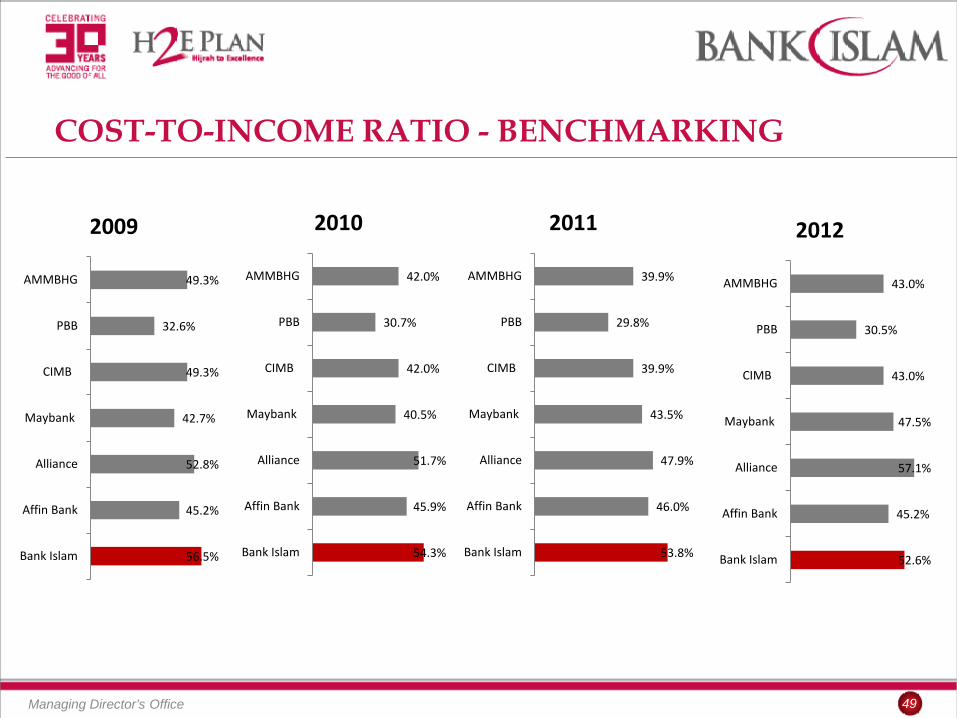

…cost income ratio continue to trend downwards

…commendable post 2006 asset quality

PBZT - CONTINUES TO BREAK NEW RECORDS

Managing Director’s Office 39

Jun 07 Jun 08 Jun 09 Dec 10 Dec 11 Dec 12

236.7 308.3

233.1 342.5

493.0 600.3

Turnaround Plan Sustainable Growth Plan “Stop the bleeding” Focus on recovery and return to

operational profit Transformation (Mindset, Business

Model, Brand Identity, Corporate culture etc)

Building strong foundation (i.e. good credit portfolio and operation)

Rebuilt infrastructure (risk management, IT, delivery network etc)

Enhanced Capability (Skill-set & competency)

RM

mill

ion

+21.7%

TOTAL ASSETS : CAGR OF 12.1% OVER THE LAST 5 YEARS

Managing Director’s Office 40

Turnaround Plan Sustainable Growth Plan Recapitalisation Balance Sheet Restructuring Rejuvenate Bank Islam brand

Robust Risk Management Optimising Balance Sheet Mix

RM

mill

ion

+16.2%

June 07 June 08 June 09 Dec 10 Dec 11 Dec 12

19,091.2 23,559.4

27,497.5 30,397.9 32,226.5

37,450.8

ASSETS GROWTH – BENCHMARK

Managing Director’s Office 41

23.5 26.7 30.4 32.2

37.5 31.3

37.9

47.5

75.5

91.4

18.7

27.3

36.0 43.1

51.2

16.5 22.7 23.7 29.4 29.3 13.4 16.7 18.0

22.4 29.6

9.4 11.2 13.1 22.7 27.1

41.7

50.6

61.9

72.5

-

Dec-08 Dec-09 Dec-10 Dec-11 Dec'12

Bank Islam

Maybank Islamic

CIMB Islamic

Public Islamic

AmIslamic

RHB Islamic

Bank Rakyat

Banking industry market share (%) Dec-08 Dec-09 Dec-10 Dec-11 Dec'12Bank Islam 1.8% 1.9% 2.0% 1.8% 2.0%Maybank Islamic 2.3% 2.7% 3.1% 4.2% 4.8%CIMB Islamic 1.4% 1.9% 2.3% 2.4% 2.7%Public Islamic 1.2% 1.6% 1.5% 1.7% 1.5%AmIslamic 1.0% 1.2% 1.2% 1.3% 1.5%RHB Islamic 0.7% 0.8% 0.8% 1.3% 1.4%

Total Assets (RM’bil)

Islamic banking market share (%) Dec-08 Dec-09 Dec-10 Dec-11 Dec'12

5-year CAGR

Bank Islam 12.2% 11.4% 11.4% 9.6% 9.8% 12.1%Maybank Islamic 16.2% 16.2% 17.8% 22.5% 24.0% 29.6%CIMB Islamic 9.7% 11.7% 13.5% 12.9% 13.4% 41.6%Public Islamic 8.5% 9.7% 8.8% 8.8% 7.7% 16.3%AmIslamic 6.9% 7.1% 6.7% 6.7% 7.8% 25.5%RHB Islamic 4.9% 4.8% 4.9% 6.8% 7.1% 26.4%

ROBUST FINANCING GROWTH

Managing Director’s Office 42

June 07 June 08 June 09 Dec 10 Dec 11 Dec 12

8,472.1 9,061.3 9,661.9 11,857.1 14,160.3

19,508.7

…still primarily a retail bank

“Putting the House in Order” Revamp Business Model

Risk based Target Market Focus on Secured Financing

11,000.2

1,812.8 1,500.5 250.3

14,696.8

2,454.1 2,610.5 187.6

Consumer Commercial Corporate BILOB

Dec 11 Dec 12

Gross Financing by Business Unit

3,696.6 (62.7)641.3 1,110.0

+37.8%

GROSS FINANCING – BENCHMARK

Managing Director’s Office 43

32.1

39.7

46.6 50.7

-

23.2

31.2

38.7

52.4

62.0

6.1

16.4 22.7

28.4 33.3

12.2 14.6 16.6 19.5 20.4 9.8 12.3 13.1

15.8 20.4

11.0 11.5 12.3 14.6 16.3 5.5 6.1 9.0

13.1 13.1

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Bank Rakyat

Maybank Islamic

CIMB Islamic

Public Islamic

AmIslamic

Bank Islam

RHB Islamic

Industry market share (%) Dec-08 Dec-09 Dec-10 Dec-11 Dec-12Maybank Islamic 3.2% 4.0% 4.4% 5.2% 5.6%CIMB Islamic 0.8% 2.1% 2.6% 2.8% 3.0%Public Islamic 1.7% 1.9% 1.9% 1.9% 1.8%AmIslamic 1.3% 1.6% 1.5% 1.6% 1.8%Bank Islam 0.8% 0.8% 1.0% 1.3% 1.5%RHB Islamic 0.6% 0.5% 0.6% 1.2% 1.2%

Islamic banking growth rate (%) Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 5 yr CAGRMaybank Islamic 10.2% 8.5% 7.6% 7.3% 8.4% 26.0%CIMB Islamic 21.6% 23.1% 23.9% 26.1% 26.2% 90.2%Public Islamic 5.7% 12.1% 14.0% 14.2% 14.1% 14.0%AmIslamic 11.4% 10.8% 10.2% 9.7% 8.6% 21.0%Bank Islam 9.1% 9.1% 8.1% 7.9% 8.6% 14.6%RHB Islamic 5.1% 4.5% 5.6% 6.5% 6.9% 29.2%

FROM WORST TO BEST ASSET QUALITY

Managing Director’s Office 44

11.78%

4.50%

2.61%

1.55%

Dec-09 Dec-10 Dec-11 Dec-12

Total Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

Bank Rakyat

Gross Impaired Financing Ratio

Net Impaired Financing Ratio

Dec’12:Industry 2.00%IB Industry 1.64%

Dec’12:Industry -0.02%IB Industry -0.32%

3.35%

1.08%

-0.17%

-0.67%

Dec-09 Dec-10 Dec-11 Dec-12

Total Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

Bank Rakyat

74.1% 76.8%

106.2%

142.6%

Dec-09 Dec-10 Dec-11 Dec-12

Total Banking Industry

Islamic Banking Industry

Bank Islam

MIB

CIMB-i

PIBB

Financing Loss Coverage Ratio

Dec’12:Industry 100.9%IB Industry 119.3%

STRONG DEPOSIT FRANCHISE

Managing Director’s Office 45

17,617 20,763 25,212 26,888 28,305 32,583

June 07 June 08 June 09 Dec 10 Dec 11 Dec 12

DepositsGrowth+ 15.1%

of which Al-Awfar

7032.5%

of which Al-Awfar

1120.4%

of which Al-Awfar1,1213.6%

of which Al-Awfar

1090.4%

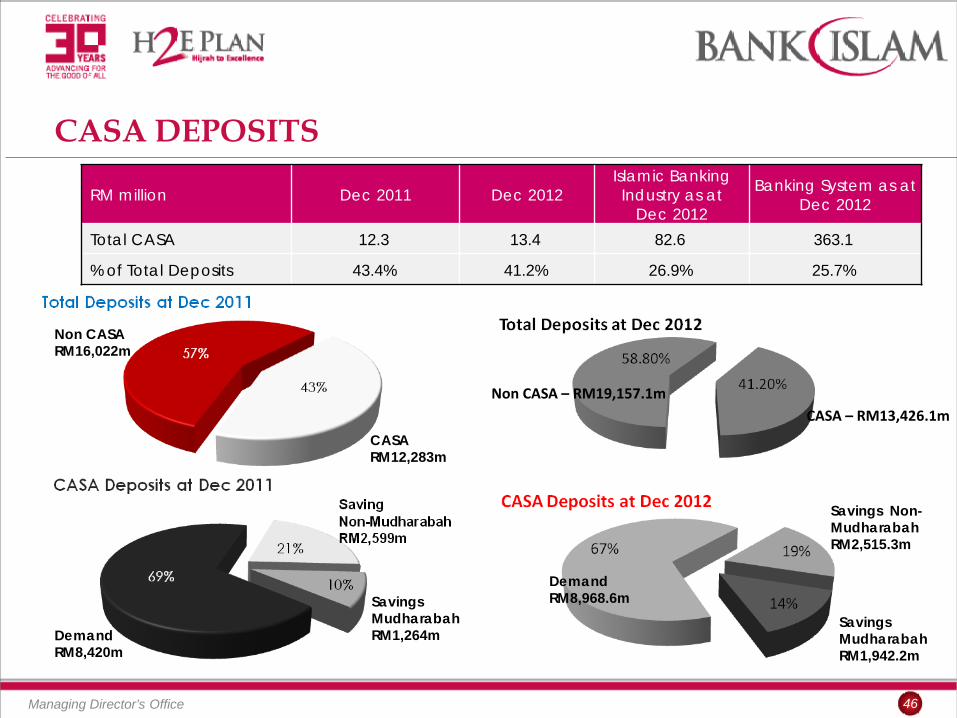

CASA DEPOSITS

Managing Director’s Office 46

RM million Dec 2011 Dec 2012Islamic Banking Industry as at

Dec 2012

Banking System as at Dec 2012

Total CASA 12.3 13.4 82.6 363.1

% of Total Deposits 43.4% 41.2% 26.9% 25.7%

Non CASA RM16,022m

CASA RM12,283m

Demand RM8,420m

Savings MudharabahRM1,264m

CASA – RM13,426.1mNon CASA – RM19,157.1m

Demand RM8,968.6m

Savings MudharabahRM1,942.2m

Savings Non-MudharabahRM2,515.3m

CASA DEPOSIT – BENCHMARK

Managing Director’s Office 47

40.1%

42.2%

22.0%

43.4%

16.3%

31.3%

23.2%

30.2%

28.9%

6.1%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-09

39.7%

35.6%

23.9%

39.3%

19.6%

23.4%

21.4%

31.8%

25.0%

6.0%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-10

38.9%

28.2%

23.6%

33.5%

21.9%

15.8%

25.4%

30.0%

23.8%

5.0%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-11

41.2%

33.1%

26.8%

30.2%

24.6%

16.5%

26.3%

32.8%

24.1%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Dec-12

FINANCING TO DEPOSIT RATIO

Managing Director’s Office 48

49.1%

111.1%

93.6%

111.6%

96.5%

74.9%

55.9%

63.8%

50.8%

103.6%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-09

45.7%

105.0%

100.3%

108.4%

101.4%

90.8%

56.1%

65.9%

52.4%

96.5%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-10

51.5%

86.6%

97.0%

97.3%

92.9%

76.6%

71.5%

59.8%

57.9%

86.7%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Bank Rakyat

Dec-11

61.2%

87.3%

94.3%

86.2%

94.2%

87.2%

78.8%

57.7%

62.6%

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Affin-i

Muamalat

Dec-12

COST-TO-INCOME RATIO - BENCHMARKING

Managing Director’s Office 49

56.5%

45.2%

52.8%

42.7%

49.3%

32.6%

49.3%

Bank Islam

Affin Bank

Alliance

Maybank

CIMB

PBB

AMMBHG

2009

54.3%

45.9%

51.7%

40.5%

42.0%

30.7%

42.0%

Bank Islam

Affin Bank

Alliance

Maybank

CIMB

PBB

AMMBHG

2010

53.8%

46.0%

47.9%

43.5%

39.9%

29.8%

39.9%

Bank Islam

Affin Bank

Alliance

Maybank

CIMB

PBB

AMMBHG

2011

52.6%

45.2%

57.1%

47.5%

43.0%

30.5%

43.0%

Bank Islam

Affin Bank

Alliance

Maybank

CIMB

PBB

AMMBHG

2012

RETURN ON EQUITY - BENCHMARK

Managing Director’s Office 50

26.5%

5.9%

29.4%

17.4%

22.0%

20.5%

15.4%

33.4%

19.1%

17.9%

Bank Islam

Muamalat

Bank Rakyat

Affin Bank

Alliance Bank

Maybank

CIMB

PBB

RHB Bank

AMMBHG

2009

16.5%

11.8%

31.9%

15.0%

11.8%

7.3%

18.6%

30.3%

18.6%

16.1%

Bank Islam

Muamalat

Bank Rakyat

Affin Bank

Alliance Bank

Maybank

CIMB

PBB

RHB Bank

AMMBHG

2010

16.6%

11.1%

30.5%

16.6%

14.9%

19.7%

19.7%

31.4%

20.3%

15.5%

Bank Islam

Muamalat

Bank Rakyat

Affin Bank

Alliance Bank

Maybank

CIMB

PBB

RHB Bank

AMMBHG

2011

20.3%

11.9%

18.2%

18.0%

19.7%

21.8%

29.1%

17.7%

18.4%

Bank Islam

Muamalat

Affin Bank

Alliance Bank

Maybank

CIMB

PBB

RHB Bank

AMMBHG

2012

CAPITAL ADEQUACY - BENCHMARKING

Managing Director’s Office 51

15.36%

15.21%

17.22%

10.52%

11.34%

13.36%

14.99%

13.78%

21.74%

14.29%

Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Bank Rakyat

Dec-09

14.77%

14.93%

16.78%

11.19%

17.21%

14.15%

14.00%

13.56%

19.33%

13.32%

Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Bank Rakyat

Dec-10

15.65%

14.92%

16.86%

12.61%

14.42%

13.27%

13.52%

13.95%

11.34%

16.45%

Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Bank Rakyat

Dec-11

15.24%

14.30%

14.09%

12.59%

9.00%

13.01%

15.90%

14.74%

13.39%

Banking Industry

IB Industry

Bank Islam

MIB

CIMB-i

PIBB

AmIslamic

RHB-i

HL-i

Dec-12

BUILT A STRONG CUSTOMERS PORTFOLIO

Managing Director’s Office 52

INDUSTRY RECOGNITIONS

Managing Director’s Office 53

2009 2010 2011 2012

EMPLOYER OF CHOICE

Managing Director’s Office 54

38. Bank Islam (2011 – 62 place)

Managing Director’s Office 55

“Bank Islam has transformed into a reputable and adequately capitalized banking institution, characterized by a trusted

brand name through excellent service delivery and increased accessibility to its products & services (wide network of

branches and other delivery chanels); continuous product innovation; consistent and sustainable profitability track; dynamic and proactive risk management systems and

mechanisms; strong corporate governance; prudent balance sheet expansion and asset-liability management; favorable credit profile; high quality asset mix and manageable non-

performing financings.

After achieving all the performance targets and having implemented all the pillars set under the three-year

Turnaround Plan and Sustainable Growth Plan, the challenge is to sustain our momentum and continue our journey to place

Bank Islam at greater heights”

Managing Director’s Office 56

MOVING FORWARD

NOT THE TIME TO REST ON OUR LAURELS

Managing Director’s Office 57

… to meet increasingly sophisticated needs of customer and competitive market place

MOVING FORWARD

Managing Director’s Office 58

… transformation as a continuous journey

TRANSFORMING ISLAMIC BANKING

Managing Director’s Office 59

LESSON LEARNT

With the right people, you can move mountains

Change the mindset is the most difficult

Innovation is the key to stay relevant

Be the best in class. “Whatever you are, be a good one” - Abraham Lincoln

The world is full of uncertainty. Change is the only constant

Managing Director’s Office 60

Q & A SESSION

Managing Director’s Office 61

“Bank Islam wishes to register its appreciation to all its stakeholders especially regulators, shareholders and

customers for their unwavering commitment and continuous support especially in transforming Bank Islam into a viable,

sound, adequately capitalized and competitive banking institution, in line with its vision to become a “global leader in

Islamic banking”.

Bank Islam seeks the recognition as an integrated financial solutions provider with a panoply of innovative Shariah-

based financial products & services that respond to customer needs and requirements.”

www.bankislam.com.my

Managing Director’s Office 62

& Thank You

Disclaimer: This presentation material has been prepared by Bank Islam Malaysia Berhad (the Bank”) for information purposes onlyand does not purport to contain all the information that may be required to evaluate the Bank or its financial position. No

representation or warranty, express r implied, is given by or on behalf of the Bank as to the accuracy of the information or opinions contained in this presentation. The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities , nor should it or any part of it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever. The Bank does not accept any liability whatsoever for any loss howsoever arising

from any use of this presentation or their contents or otherwise arising in connection therewith.

TRANSFORMATION MANDATES

Managing Director’s Office 63

TRANSFORMATION MANDATES…CONT

Managing Director’s Office 64

TRANSFORMATION MANDATES…CONT

Managing Director’s Office 65

TRANSFORMATION MANDATES…CONT

Managing Director’s Office 66

Jaafar Abu, Head – Business Support

• Joined Bank Islam on 1 July 2009• “Driving Trade Finance & Services”

Mizan Masram, Head – Recovery & Rehabilitation

• Joined Bank Islam on 1 July 2009 • “Maximizing Recovery & Sustainability of Strong Asset Quality”

Mohd Nazri Chik, Head - Shariah

• Joined Bank Islam on 1 June 2004• “Shariah Centre of Excellence”

Jeroen Petrus Mergaretha Maria Thijs, Chief Risk Officer

Joined Bank Islam on 12 January 2009

“Inculcating Risk Culture & Proactive Risk Management”

Leong David @ Leong Sze Khiong, Chief Internal Audit

• Joined Bank Islam on 7 May 2012• “Risk-based Auditing”