Carbon Sequestration Carbon Capture and Storage · CCS COAL COAL + CCS From Gibbins, J. et al....

52

Cambridge Energy Forum Sustainable Energy Conference 1st December 2006 Cavendish Laboratory Cambridge Carbon Sequestration Carbon Capture and Storage Jon Gibbins & Hannah Chalmers Energy Technology for Sustainable Development Group Mechanical Engineering Department Imperial College London UK Carbon Capture and Storage Consortium www.ukccsc.co.uk

Transcript of Carbon Sequestration Carbon Capture and Storage · CCS COAL COAL + CCS From Gibbins, J. et al....

Cambridge Energy ForumSustainable Energy Conference

1st December 2006Cavendish Laboratory

Cambridge

Carbon SequestrationCarbon Capture and Storage

Jon Gibbins & Hannah ChalmersEnergy Technology for Sustainable Development Group

Mechanical Engineering DepartmentImperial College London

UK Carbon Capture and Storage Consortiumwww.ukccsc.co.uk

WHY?

CRITICAL ROLE FOR CARBON CAPTURE & STORAGE? http://www.ipcc.ch/

CARBON IN

FOSSIL FUELS

CARBON THAT CAN BE EMITTED TO ATMOSPHERE

‘Unconventional oil’ includes oil sands and oil shales but not CTL. ‘Unconventional gas’includes coal bed methane, deep geopressured gas etc. but not gas from coal and a possible 12,000 GtC from gas hydrates. (www.ipcc.ch/pub/un/syreng/q1to9.pdf)

Caldeira et al, Nature 425, Sep. 2003

Ocean Acidification

Coal Oil Gas Uranium*

Australia/New Australia/New ZealandZealand

Sources: BP Statistical Review 2005; WEC Survey of Energy Resources 2001; Reasonably Assured Sources plus inferred resources to US$80/kg U 1/1/03 from OECD NEA & IAEA Uranium 2003; Resources, Production & Demand updated 2005; *energy equivalence of uranium assumed to be ~20,000 times that of coal

N o rth A m e ric a

C e n tra l/S o u th A m e ric a

O th e r A sia /P a c ific in c In d ia n S u b c o n tin e n t

M id d le E a st

A fric a

C h in a

E u ro p e (e xc l. R u ssia n F e d )

R u ssia n F e d e ra tio n

A u stra lia /N e w Z e a la n d

AfricaAfrica

World Energy Reserves 2004 (Mtoe)

EuropeEurope

Russian Russian FederationFederation

Middle EastMiddle EastChinaChina

Other Other Asia/PacificAsia/Pacific

North AmericaNorth America

South AmericaSouth America

Brendan Beck, World Coal Institute, Coal, 3M Sustainable Energy Engineering, Imperial College, 12 October 2006

HOW?

Carbon Storage Options

IPCC (2005)

270 GtC2700 GtC

185 GtC 245 GtC55 GtC<4 GtC

www.ipcc.ch

Sleipner, aquifer storage for 1Mt/yr CO2

www.statoil.com, 2002

www.statoil.com, 2002

www.statoil.com, 2002

Time lapse (4D) seismic trackingof injected CO2

After Jordal, K. et. al. (2004) Oxyfuel combustion for coal-fired power generation with CO2 capture – opportunities and challenges Proceedings of 7th International Conference on Greenhouse Gas Control Technologies, www.ghgt7.ca

O2

CO2 dehydration, compression transport and

storage

CO2 separationPower & Heat

Air separation

Gasification + shift + CO2 separation

Air separation

Coal

Air

Power & Heat

Power & Heat

Flue gas

N2, O2, H2O

CO2

Air

Coal

Air

H2

N2, O2, H2O

CO2

Coal

O2Air N2

CO2 (with H2O)

Recycle

POST-COMBUSTION CAPTURE

PRE-COMBUSTION CAPTURE

OXYFUEL (O2/CO2 RECYCLE COMBUSTION) CAPTURE

Statoil/Shell 860 MW gas fired power plant, Tjeldbergodden, Norway

Up to 2.5 million tonnes CO2injected annually

DTI TSR008

GE, SLURRY FEED, REFRACTORY-LINED GASIFIER WITH QUENCH COOLING

Shell gasifier literature

SHELL, DRY FEED, MEMBRANE WALL GASIFIER WITH DRY SYNGAS COOLING

Pre-combustion capture (IEA GHG www.ieagreen.co.uk)

Extra steam(or water quench)

Jon Gibbins, Imperial College London, New Europe, New Energy. Oxford, 27 Sep 2006

Oxyfuel Capture Concept

Source: IEA GHG

0

20

40

60

80

100

No CCS Electricity +Fischer-

Tropsch withCCS

DME only(recycle) with

CCS

Electricity +DME withone-stage

CCS

Electricity +DME withtwo-stage

CCS

Coal toelectricity

with NGCCperformance

standard

Coal toelectricity+

full CCS

% o

f coa

l C e

mitt

ed to

atm

osph

ere

Estimated percentage of coal C going into the atmosphere for various coal utilization options

ALSO POSSIBLE FROM COAL-TO-LIQUIDSAND OTHER UNCONVENTIONAL FUELS

BUT NOT ALL CCS HAS EQUAL ENVIRONMENTAL BENEFIT

Power plant efficiencies

0

10

20

30

40

50

60

Coal nocapture(Fluor)

Coalcapture(Fluor)

CoalCapture

(MHI)

Gas nocapture(fluor)

Gascapture(Fluor)

Gascapture(MHI)

Efficiency, % (LHV)

IGCC from IEA GHG PH4/19International Network for CO2 Capture

J M Topper, Introduction to 7th Workshop, Vancouver, Sep 2004

9FA gas turbines (i.e. not H class)600/620 SC

Pulverised coal plant

Costs of Capture

IEA GHG (2006), CO2 capture as a factor in power station investment decisions, Report No. 2006/8, May 2006

Costs include compression to 110 bar but not storage and transport costs. These are very site-specific, but indicative aquifer storage costs of

$10/tonne CO2 would increase electricity costs for natural gas plants by about 0.4 c/kWh and for coal plants by about 0.8 c/kWh.

Natural gas plants Coal/solid fuel plants

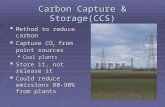

CCS Uncertainty - Fuel and Carbon Prices Matter

• Discount rate of 10%• Investment lifetime of

25 years• 8000 hours operation

per year• Coal price, £1.4/GJ

(net)• CO2 delivery pressure

of 110 bar (and pipeline quality)

• Indicative cost of transport to offshore aquifer storage, £5.50 per tonne CO2 stored

2 3 4 5Gas price £/GJ

10

20

30

40

50

0

Car

bon

Pric

e (£

/tonn

e C

O2)

4 p/kWh

3 p/kWh

GAS

GAS +

CCS

COAL

COAL +

CCS

From Gibbins, J. et al. (2006) Interim Results from the UK Carbon Capture and Storage Consortium ProjectProc. 8th International Conference on Greenhouse Gas Control Technologies, Trondheim, Norway, 19th-23rd June 2006. www.ghgt8.no. Also quoted in Stern Review

WHEN?

POSSIBLE CCS TIMING IN KYOTO PHASES

2008-2012 Kyoto Phase 1• Some early deployment projects

2013-2017? Kyoto Phase 2• Greater emphasis on technology• More widespread CCS development & deployment• CCS standard on some plants (e.g. coal to liquids)?

2018? - 2022? Kyoto Phase 3• CCS becomes standard in Annex 1 countries?

2023? -? Kyoto Phase 4• CCS becomes standard in all countries?

New build? Retrofit?

IEA World Energy Outlook 2006

Reference case: ~ BAU

Alternative Policy Scenario:Reduced climate impact,

more efficiency, nuclear and renewables.

Beyond Alternative Policy Scenario:Achieve 2004 emissions in 2030,

some new policies and technologies.

WEO 2006

WEO 2006

WEO 2006 Beyond Alternative Policy Scenario (BAPS)

The goal adopted in this Case … is to ensure that global energy-related CO2 emissions in 2030 are no higher than the 2004 level of 26.1 Gt CO2.

The BAPS Case is not constrained by the criterion that only policies already under consideration by governments are adopted. Accordingly, this case assumes even faster and more widespread deployment of the most efficient and cleanest technologies, thanks to more aggressive policies and measures and the adoption of new technologies, beyond those which have already been applied commercially today.

CCS in the Beyond Alternative Policy Scenario (BAPS)Introduction of CO2 capture and storage in power generation: The introduction of CCS in the power sector would reduce emissions by 2 Gt CO2 in 2030. Approximately 3100 TWh of electricity would then be generated from coal and natural gas plants equipped with CCS. Some 70% of new coal-fired capacity and 35% of new gas-fired plants would be equipped with CCSover the projection period. CCS in coal plants would account formore than 80% of the captured emissions. Such a solution would be particularly productive in China and India. Potential policies to implement this strategy are diverse: funding for research and development, incentives for large-scale demonstration plants, loan guarantees for new plants, performance standards for emissions from new plants, international cooperation to facilitate the building of new plants in the developing world and the widerintroduction of financial penalties on carbon emissions (taxes or cap-and- trade arrangements).

WEO 2006

WEO 2006

WEO 2006

WEO 2006

WEO 2006

WEO 2006

WEO 2006

WEO 2006

WEO 2006

LONGER TERM POTENTIAL FOR BIOMASS WITH CCS?

Tyndall Centre'Decarbonising the UK’http://www.tyndall.ac.uk

Tyndall UK aviation emissions projections for 2050 ~ 30 MtCRCEP estimates for max UK biomass production by 2050 ~ 60 Mt Carbon content of biomass available for conversion ~ 24 MtCCarbon captured using biomass with CCS ~ 90%Energy recovered compared to use without CCS ~ 75%Oil price equivalent of $50/tonne CO2 $22/barrelTransport Atmosphere carries CO2 from plane to plant for free!

But need to supply biomass to CCS plants

ACTUAL IMPLEMENTATION

PLANS

CCS Implementation Proposals – UK

2016 PC (supercritical retrofit) + post-combustion (may be capture ready)

~500 MW(£800m)

CoalRWE, Tilbury, UK

2011IGCC + shift + precombustion?(may be capture ready)

450 MW(£1bn)

Coal(+petcoke?)

E.ON, Killingholme, Lincolnshire coast, UK

2010(for CHP)

IGCC+CCS addition to planned NGCC CHP plant

450 MW (or more, with retrofit)

Coal(+petcoke?)

Conoco-Phillips, Immingham, UK

2010IGCC + shift + precombustion~900 MWCoalPowerfuel/KuzbassrazrezugolHatfield Colliery, UK

2010Autothermal reformer + precombustion

475 MW, (>$600M)

Natural gasBP/SSE DF1, Peterhead/Miller, Scotland

2009IGCC + shift + precombustion800 MW (+ H2 to grid) ($1.5bn)

Coal (petcoke)

Progressive Energy/Centrica, Teeside, UK

Start Capture technologyPlant output/cost

FuelCompany/ Project Name

• Proposed full-scale (~300 MWe and above) CCS projects• Based on media reports, press releases and personal communication

so indicative only!

• Plus capture-ready plants at Ferrybridge (SSE) and Kingsnorth (E.On)

CCS Implementation Proposals – World (not UK)

2014IGCC + shift + precombustion450 MW(Є1bn)

CoalRWE, GermanyGermany

2013IGCC, may be partial capture only300-350MWCoal (sub.bit)Xcel Colorado, USA.

2012IGCC + shift + precombustion275 MWCoalFuturegen, USA

2012IGCC + shift + precombustion275 MWCoalStanwell, Queensland, Australia

2011PC oxyfuel300 MWLignite coalSaskPower, Saskatchewan,Canada

2011NGCC+ Post-combustion amine, CO2 for EOR (Draugen)

860 MWNatural gasStatoil/Shell, Tjeldbergodden, Norway

2011IGCC + shift + precombustion, CO2 for EOR

500 MW, ($1bn)

PetcokeBP DF2, Carson, USA

2010NGCC+ Post-combustion amine 100,000 tCO2/yr from 2010, 1.3Mt CO2 from 2014, CO2 for EOR (Gullfaks and others)

280 MWNatural gasStatoil/Dong, Mongstad, Norway

Start Capture technologyPlant output/cost

FuelCompany/ Project Name

• Proposed full-scale (~300 MWe and above) CCS projects• Based on media reports, press releases and personal communication

so indicative only!

http://biz.yahoo.com/prnews/061106/nym208.html?

TXU Corp. Outlines Vision to Displace Older Power Generation with Advanced TechnologiesMonday November 6, 8:30 am ETProgress on Texas Projects; Expansion of Plans Outside of Texas; Update of Financial Outlook; Board Declaration of Increased Dividend, Authorization of Share Repurchases- TXU's power generation strategy has progressed substantially, and now includes line of sight on the development of 16 to 23 gigawatts (GW) of new capacity, including new opportunities outside of Texas. -TXU has engineered its reference plant design to be the most advanced supercritical coal technology of any plant under construction in the U.S. today and to meet carbon capture and storage ready criteria.

See Imperial BCURA Project B70& new IEA GHG report coming soon

Barriers for Commercial Deployment

• Need to establish whole CCS value chain and appropriate criteria for comparing options

• No long term framework to establish an appropriate value for CO2 reductions

• Some technical issues, but mostly scale-up and integration of known technology for first plants

• Uncertainty over costs and risks – should be reduced if series of large scale demos occurs BUT these need to be funded

• Investors want to avoid making the wrong choice, also need to be robust to policy change

Legal and Regulatory Issues

• HMG has a regulatory task force which is reviewing current regulations, gaps and required changes– Offshore Licensing– Decommissioning and

long term liability– Licensing onshore installations– Licensing onshore storage

• Making progress with international conventions on the marine environment (London/OSPAR)

• CCS within EUETS and CDM?

Figure from IPCC (2005)

POLICYBACKGROUND

14. We will work to accelerate the development and commercialization of Carbon Capture and Storage technology by: (a) endorsing the objectives and activities of the Carbon Sequestration Leadership Forum (CSLF), and encouraging the Forum to work with broader civil society and to address the barriers to the public acceptability of CCS technology; (b) inviting the IEA to work with the CSLF to hold a workshop on short-term opportunities for CCS in the fossil fuel sector, including from Enhanced Oil Recovery and CO2 removal from natural gas production; (c) inviting the lEA to work with the CSLF to study definitions, costs, and scope for ‘capture ready’ plant and consider economic incentives; (d) collaborating with key developing countries to research options for geological CO2 storage; and (e) working with industry and with national and international research programmes and partnerships to explore the potential of CCS technologies, including with developing countries.

THE GLENEAGLES COMMUNIQUÉ

(E.ON, Mitsui Babcock, Imperial IEA GHG project)

CCS in Stern Review – Role of CCS

• “There is still time to avoid the worst impacts of climate change, if we take strong action now.”

• “Carbon capture and storage is essential to maintain the role of coal in providing secure and reliable energy for many economies.”

• “[CCS] is a technology expected to deliver a significant portion of the emission reductions. The forecast growth in emissions from coal, especially in China and India, means CCS technology has particular importance.”

• “There is a strong case for greater international co-ordination of programmes to demonstrate carbon capture and storage technologies, and for international agreement on deployment.”

• “Building on these announcements, the enhanced co-ordination of national efforts could allow governments to allocate support to the demonstration of a range of different projects…”

• “One element that enhanced co-ordination could focus on is understanding the best way to make new plants “capture-ready”…”

CCS in Stern Review – What Next?

CONCLUSIONS • CCS offers unique solution for fossil carbon• Geological storage capacity probably comparable

to fossil C (but need to assess this resource)• Political support growing• Industry ready to go• But need to get funding and regulation established – lagging behind

• Make any new plants capture-ready (urgent - UK & US will help with India and China)

• Build some full-scale plants with capture for learning by doing

• Train some young people – key university role

Acknowledgements• The authors gratefully acknowledge financial support from

the Research Councils’ TSEC programme for the UK Carbon Capture and Storage Consortium, to which they both belong, and to the DTI, BCURA, and IEA GHG for support for projects that have contributed to the background to this work. Discussions and advice from many colleagues on these projects is also much appreciated.

• The opinions and interpretations expressed in this paper are, however, entirely the responsibility of the authors.

Further Information• www.ukccsc.co.uk• [email protected]