Geoff Gillette & Co Chartered Accountants GEOFF GILLETTE ...

Upload

keaton-powersCategory

view

33download

0description

Slide Number #1

Cara Gillette

Finance for the Public Finance for the Public Housing DirectorHousing Director

Slide Number #2

Today’s TopicsToday’s Topics

Overview of the new operating fund formula

Stop-loss provision Project-based accounting Basic financial concepts and reports Excess cash and fungibility

Building BlocksBuilding Blocks

Project-based fundingProject-based funding

Project-based budgetingProject-based budgeting

Project-based accountingProject-based accounting

Project-based managementProject-based management

Project-based Project-based performance assessmentperformance assessment

Slide Number #4

The New FormulaThe New Formula

Requires PHAs with 400 or more PH units to transition to project-based accounting, budgeting, and management Threshold of 400 doesn’t apply to stop-loss PHAS

Is based on HUD’s multifamily industry Will force the PH program to become more

property-based

Slide Number #5

Hot Off the PressHot Off the Press

PIH Notice 2008-16(HA) PHAs with 250-400 units can exempt

themselves But the election for exemption is only

authorized for CY 2008 PHAs that elect the exemption aren’t

“grandfathered” in for future years And there are lots of requirements

Slide Number #6

Key Implementation DatesKey Implementation Dates

Determination of Asset Management Projects (AMPs) – CY 2006

Implementation of new Operating Fund Formula – CY 2007

Operating Subsidy by AMPs – Begins in CY 2008

Project-Based Budgeting/Accounting – Begins with PHA FYs July 1, 2007 and forward

Subsidy is fully fungible in CY 2008

Cost Reasonableness – Begins in Fiscal Year 2009

Slide Number #7

The New Model for PHThe New Model for PH

Fundamental shift for public housing Historically, operating subsidy was calculated

on an aggregate level Op sub was allocated to the central office, which

decided where the subsidy went

Now, subsidy is calculated for and allocated to each project

Slide Number #8

The New Model for PHThe New Model for PH

Funding goes to the projects, and projects pay for everything else

Any service to the project not at the project will come from a cost center Every PHA will have a central office cost center

Direct, indirect, and allocated services

Slide Number #9

The New Model for PHThe New Model for PH

Two main components Project-based management is decentralized

property services tailored to the needs of each property, given the resources available to each property

Asset management is strategic oversight and centralized services tailored to the needs of the portfolio as a whole

Slide Number #10

AMPs – the Economic Engine of PHAMPs – the Economic Engine of PH

Your PHA defined its asset management projects (AMPs) for purposes of project-based accounting, budgeting, and management

Each AMP has its own budget, financial statements, staffing, subsidy, capital plan, and will have its own performance scoring

Not in book

Slide Number #11

AMPS – the Economic EngineAMPS – the Economic Engine

The PHA’s decision on the grouping of AMPS is based on: Geographic location Organizational structure Size of the PHA Housing stock

Not in book

Resident population Delivery systems Maintenance delivery

Slide Number #12

Compliance with Asset Compliance with Asset ManagementManagement

Best definition of compliance so far is notice to stop-loss agencies, since they have to comply early

Slide Number #13

Notice 2006-14(HA)Notice 2006-14(HA)

Even though these are the instructions for stop-loss agencies, this notice, and the Stop Loss Kit, is the clearest roadmap for all PHAs The difference is in the deadline

Slide Number #14

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

1. Project-based accounting Monthly operating statements for each

project – revenues and expenses vs. budget levels, including all fees from the COCC and Capital Fund

Must reasonably reflect the financial performance of each project

Slide Number #15

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

2. Project-based management Property management services are

arranged or provided in the best interest of the property considering needs, cost, and responsiveness, relative to local market standards

Slide Number #16

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

3. Central office cost center (COCC) must charge reasonable fees to the AMPs

COCC must operate on the allowable fees and other permitted reimbursements from its PH and S8 programs

In other words, the COCC must support itself

Slide Number #17

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

4. Centralized services that directly support projects are funded using a fee-for-service approach or through other allowable charge-backs

Each project is charged for actual services received - must be reasonable compared to local market

Slide Number #18

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance PHA systematically reviews financial,

physical, and management performance of each project, and identifies non-performing properties

Slide Number #19

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance – a non-performing property has:

PHAS physical score below 70 Significant crime and drug problems Below 95% occupancy TARS that exceed 7% of monthly rent roll

Slide Number #20

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance – a non-performing property has:

PHAS grade of “D” or below for vacant unit turnaround and work orders

Utility consumption more than 120% of agency average

Other major management problems

Turnaround = D more than 30 daysWOs = D more than 40 days

Slide Number #21

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance Long-term prospects for each property:

Maintain project as is Identify capital improvements needed Dispose of property (demo, sale, etc) Financial condition of each project

Stop-Loss FAQs 9/1/06

Slide Number #22

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

6. Capital planning Physical needs assessment and a five-year

plan for each project Five-year plan needs to consider revenue

sources, market, tenancy, and project needs

Long-range energy consumption reduction

Slide Number #23

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Risk management responsibilities related to regulatory compliance

PHA not carrying out responsibilities if: Designated troubled under PHAS Any outstanding FHEO findings or

voluntary compliance agreement not implemented…

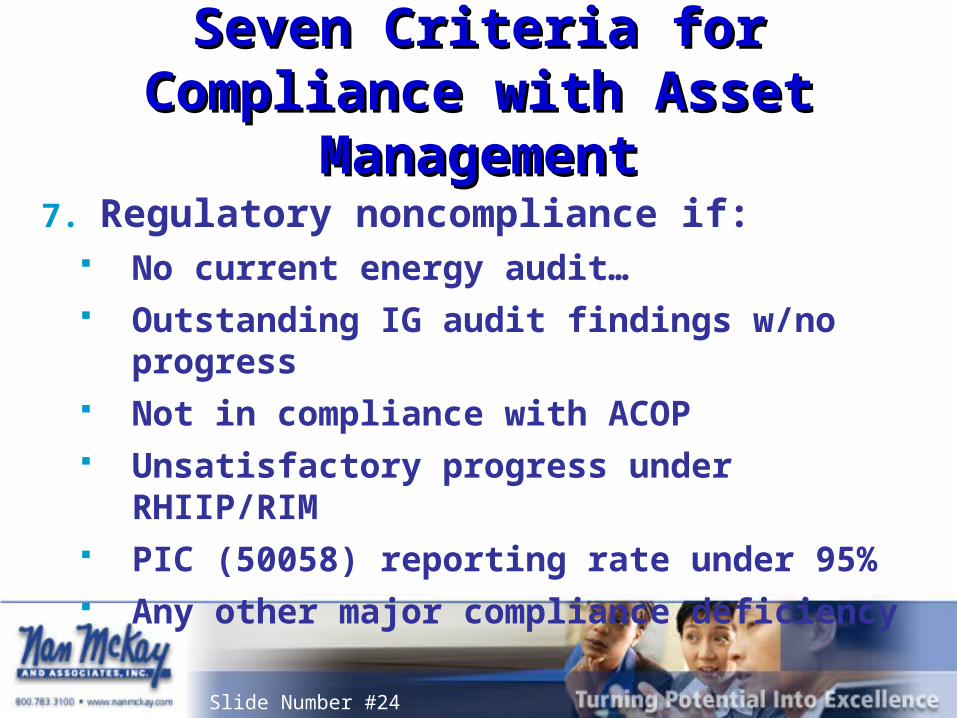

Slide Number #24

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Regulatory noncompliance if: No current energy audit… Outstanding IG audit findings w/no progress Not in compliance with ACOP Unsatisfactory progress under RHIIP/RIM PIC (50058) reporting rate under 95% Any other major compliance deficiency

Slide Number #25

The Deal with Stop-LossThe Deal with Stop-Loss

Under the new op sub formula, about a third of PHAs gained, a third stayed the same, and a third lost op sub

Slide Number #26

The Deal with Stop-LossThe Deal with Stop-Loss

The PHAs who are “losers” under the new formula can stop the loss of subsidy by early conversion to asset management

Slide Number #27

Stop-Loss ProvisionStop-Loss Provision

Deadline for Year 1 was October 15, 2007 If PHA demonstrated conversion by that date,

the reduction of subsidy stopped at 5% of the difference for CY 2007 That means that 95% of the PUM difference

will be added to the lower op sub level under the final rule

Slide Number #28

Stop-Loss ProvisionStop-Loss Provision

For subsequent years, the % of loss goes up

Slide Number #29

Stop-Loss ProvisionStop-Loss Provision

There will be additional requirements for subsequent years Year 2 has more requirements than Year 1

HUD staff will have to monitor

Slide Number #30

Per Unit Month (PUM)Per Unit Month (PUM)

Budgeted income and expense items are shown in a monthly and yearly total dollar amount – and also in a per unit per month (PUM)

Page 6-3

Slide Number #31

Per Unit Month (PUM)Per Unit Month (PUM)

PUM is an important concept PUM applies to any line item ($) that:

Was spent, is being spent, or will be spent Was earned, is being earned, or will be earned

Formula is: Any line item $ ÷ EUM = PUM

Slide Number #32

Per Unit Month (PUM)Per Unit Month (PUM)

PUM also allows the portfolio to be tracked over time as the number of units change Example:

Last year the PHA had 1200 units This year, due to demo/dispo, there are 1100

units

Slide Number #33

Per Unit Month (PUM)Per Unit Month (PUM)

PUM also allows sites to be compared – even if they aren’t of similar size type and age If one AMP’s landscape cost is $26.82 and

another’s of similar common grounds is $10.45, costs may need to be analyzed

Slide Number #34

Operating Subsidy FormulaOperating Subsidy Formula

The Money is Driving the Changes

Page 6-4

Slide Number #35

The New Operating SubsidyThe New Operating Subsidy

The old op sub was aggregate - AEL Under the new formula, subsidy is

calculated and allocated by project - PEL The op sub will go directly to the projects,

and all other activities will be supported by fees paid by the projects

We see these in PUM (per unit month) figures

Slide Number #36

The New Operating SubsidyThe New Operating Subsidy

Operating subsidy formula:Project expense level (PEL)

+ Utility expense level- Formula income frozen at 2004 level

+ Applicable add-ons

= Operating subsidy

Slide Number #37

The New Operating SubsidyThe New Operating Subsidy

Ten components used to calculate PEL:1. Geographic variable – one of the two most

significant variables – where you are in the country

2. Central city variable

3. Clientele (occupancy) variable – family properties tend to cost 6% more

Page 6-5

Slide Number #38

The New Operating SubsidyThe New Operating Subsidy

Ten variables used to calculate op sub:4. Property size variable – number of units

5. Building type variable – high-rise, garden walk-up, single family home, etc.

6. Bedroom mix variable – the other most significant variable

Slide Number #39

The New Operating SubsidyThe New Operating Subsidy

Ten variables used to calculate op sub:7. Percent assisted variable – 100%

subsidized tends to cost 6% more

8. Property age variable

9. Neighborhood poverty variable

10. Ownership type variable – for-profits have costs that are 6% less

Slide Number #40

The New Operating SubsidyThe New Operating Subsidy

National floor of $200 PUM for senior properties and $215 PUM for family properties

National ceiling of $420 PUM and 4% reduction for PUMs over $325

Slide Number #41

The New Operating SubsidyThe New Operating Subsidy

Add-ons – the PHA determines which are applicable:

Self-sufficiency Energy loan amortization PILOT Audit cost – actual most recent Resident participation - $25 per unit per yr

Page 6-6

Slide Number #42

The New Operating SubsidyThe New Operating Subsidy

Add-ons – the PHA determines: Asset management fee

$4 PUM for PHAs with 250 or more $2 PUM for smaller PHAS who transition

to PBM who have a COCC

Slide Number #43

The New Operating SubsidyThe New Operating Subsidy

Add-ons – the PHA determines: Information technology fee

$2 PUM Asset repositioning fee (demo or dispo) Costs attributable to changes in federal

law, regulation, or economy

Slide Number #44

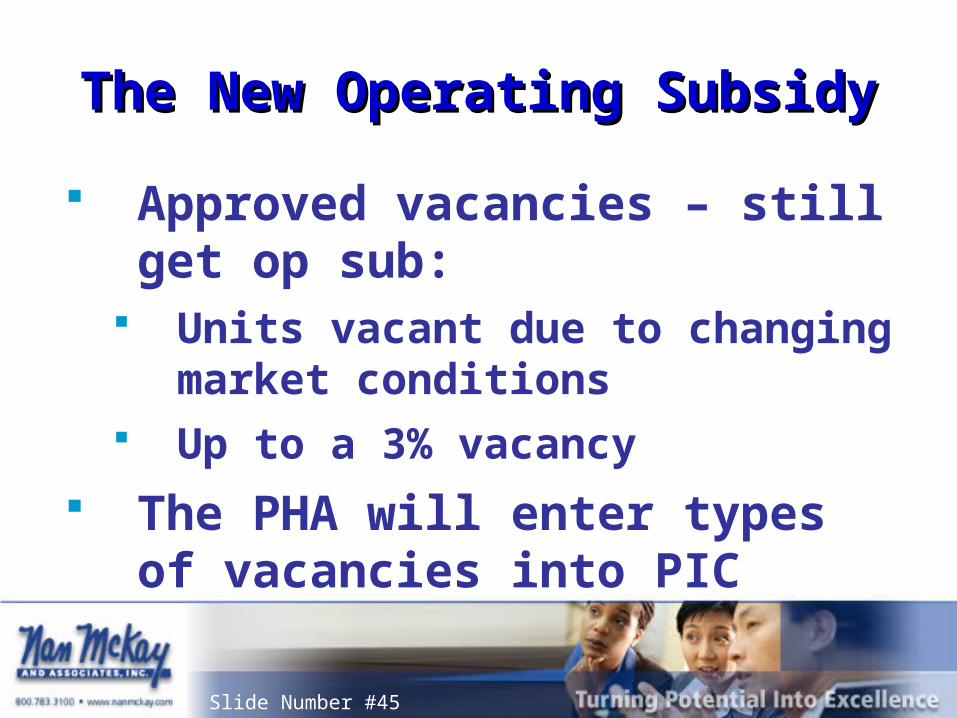

The New Operating SubsidyThe New Operating Subsidy

Approved vacancies – still get op sub: Units undergoing mod (if on schedule) Units approved for resident services Units in court litigation Units undergoing casualty loss settlement Units vacant due to disaster (federal or

state)…

Page 6-7

Slide Number #45

The New Operating SubsidyThe New Operating Subsidy

Approved vacancies – still get op sub: Units vacant due to changing market

conditions Up to a 3% vacancy

The PHA will enter types of vacancies into PIC

Slide Number #46

CostsCosts

Page 6-12

Slide Number #47

CostsCosts

All budget costs and expenses will fall into one of three general categories: Direct cost (at the project) Central office cost center (COCC)

Indirect services Other cost centers (optional)

For direct and allocated services

Slide Number #48

Cost CentersCost Centers

Every PHA will have at least one cost center, the central office cost center (COCC)

Centralized maintenance may also be a cost center

Slide Number #49

Frontline (Direct) CostsFrontline (Direct) Costs

These are expenses of the project: Personnel costs of staff assigned to project Repair and maintenance costs including

supplies, contracted repairs, make-readies, preventive maintenance, etc.

Utility costs Costs related to the site office – phones, office

supplies, computers, postage, etc.

Slide Number #50

Frontline (Direct) CostsFrontline (Direct) Costs

These are expenses of the project: Advertising including procurement and

employment notices Costs of employee recruiting and screening PILOT Insurance (allocated) Legal fees

Slide Number #51

Frontline (Direct) CostsFrontline (Direct) Costs

These are expenses of the project: Property management fees, bookkeeping

fees, and asset management fees Audit costs (allocated) Vehicle expense for site-based vehicles

Slide Number #52

Charging for MaintenanceCharging for Maintenance

Maintenance is an example of services that may need to be provided directly to projects that are centrally located and charged based on time spent or actual work performed

Slide Number #53

Charging for MaintenanceCharging for Maintenance

How to organize maintenance is an important PBM decision A PHA can decide to organize maintenance:

Decentralized – front line Supervised by the property manager

Centrally A mix

Slide Number #54

Charging for MaintenanceCharging for Maintenance

If the PHA uses centralized maintenance, will be required to use fee-for-service method when charging the project Project can only be charged for actual

services provided Could be a single blended hourly rate,

separate hourly rates for various activities, or flat fee – must be reasonable

Slide Number #55

Centralized Maintenance Centralized Maintenance

For all centralized maintenance staff providing direct services, the PHA can charge up to the market rate Even if it’s above what the

technician is actually paid

Slide Number #56

Centralized MaintenanceCentralized MaintenanceHow Much Can the PHA Charge?How Much Can the PHA Charge?

Sally is a maintenance worker $52.26 Wages

$23.52 Benefits (45%)

$75.78 Hourly rate

If the market rate is $100, the hourly charge could be $100, regardless of what Sally is paid

Slide Number #57

Charging for MaintenanceCharging for Maintenance

Costs of overall labor cost include: Gross salary, employer FICA contributions,

federal unemployment tax, state unemployment tax, worker’s comp insurance, health insurance premiums, cost of fidelity or comparable insurance, performance incentives and or annual bonuses, and retirement benefits (pre and post retirement)

Not in book

Slide Number #58

Charging for MaintenanceCharging for Maintenance

PHAs may charge for actual materials used as well as labor

Not in book

Slide Number #59

Costs of Other FunctionsCosts of Other Functions

Charging the project Where it’s cost-effective,

PHA can prorate across projects, the cost of centralized staff who perform frontline functions

Page 6-17

Slide Number #60

Charging Back to the ProjectCharging Back to the Project

These are called front line allocated costs For example, collecting rent centrally,

employee handing rent collection, as well as direct costs, could be charged back to applicable projects on any reasonable basis

Not necessary for the rent collection clerk to track his or her activity per AMP

Slide Number #61

Charging Back to the ProjectCharging Back to the Project

Two exceptions to charging projects for centralized staff performing frontline functions: Can’t charge projects for cost of a centralized

supervisor Can’t charge projects cost of centralized staff

handling procurement

Slide Number #62

Update – Centralized WarehouseUpdate – Centralized Warehouse

FAQ December 1, 2006 If a warehouse at the COCC is for

“storerooms” of scattered sites, with HUD approval, this can be an eligible frontline cost

Not in book

Slide Number #63

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project: Central waiting lists, screening, leasing and

occupancy – PHAs can prorate costs direct costs of these functions to the AMPs, including supervisory personnel The proration can be based on the number of units

leased at a project, average turnover at a project, or other reasonable allocation method

Page 6-18

Slide Number #64

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project: Resident programs – PHA can prorate

centralized resident programs across projects on a reasonable basis, including supervisory staff

Slide Number #65

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project: Protective services – PHAs can charge

centralized protective services, either in-house or through local law enforcement, including supervisory staff

HUD eventually wants these tracked by project

Slide Number #66

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project: Work order processing

Although it is the norm in multifamily housing to handle work order processing on site, a PHA may charge the cost of centralized work order processing only if the PHA can document/justify that the cost pro rated is reasonable and necessary

Slide Number #67

Shared Resource CostsShared Resource Costs

HUD knows it may not make economic sense to have FT maintenance staff dedicated to one AMP In this case the PHA may establish a

reasonable method to spread these personnel costs to the AMPs receiving the service

Page 6-19

Slide Number #68

Shared Resource CostsShared Resource Costs

Shared resource costs are distinguished from front line prorated costs in that the services being shared are limited to a few projects as opposed to being prorated across all projects An example of a shared resource cost might

be a maintenance person assigned to and paid for by two projects

Slide Number #69

Shared Resource CostsShared Resource Costs

- What if there is PHA personnel who provide services both to the projects and the central office cost center?

Slide Number #70

Shared Resource CostsShared Resource Costs

- For PHA staff who provide services both to the projects and the central office cost center, the PHA must separate the amount of time spent on providing services to the projects and the central office cost center, based on a reasonable methodology

Slide Number #71

Shared Resource CostsShared Resource Costs

- The time spent by the staff on projects must be at an hourly rate that does not exceed the reasonable hourly fee for the service

Slide Number #72

Fees Allowed under PBMFees Allowed under PBM

Slide Number #73

Fees Allowed under PBMFees Allowed under PBM

Fees the projects will pay to the COCC: Property management fees Bookkeeping fees Asset management fees Capital fund management fees

Page 6-20

Slide Number #74

Fees Allowed under PBMFees Allowed under PBM

Property management fee Is “reasonable fee” paid by project to COCC

for project oversight HUD has established some “reasonability”

guidelines Notice: Guidance on Implementation of

Asset Management, issued Sept 6, 2006

Slide Number #75

Fees Allowed under PBMFees Allowed under PBM

Management fee – “reasonable” Based on multifamily fee (annual letter from

field office); or 80th percentile as established by HUD; or Other compelling data of local market

Might include fees paid pay the PHA for private management of other properties

Updated April 10, 2007Updated April 10, 2007

Slide Number #77

Fees Allowed under PBMFees Allowed under PBM

Management fee Based on units leased (occupied units and

approved vacancies, but not the 3% limited vacancies) (EUM) using monthly lease-up rate Stop-loss FAQs (question 12) says that the

PHA can use either the first day or last day of the month (but must be consistent)

Slide Number #78

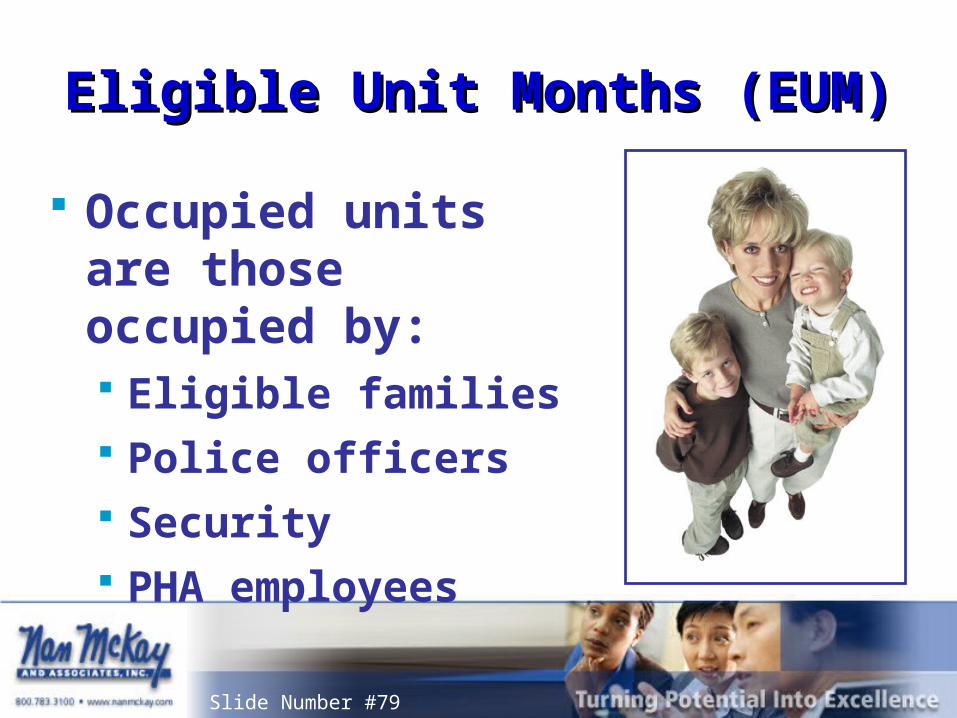

Eligible Unit Months (EUM)Eligible Unit Months (EUM)

The AMP’s eligible unit months (EUM) is used to monitor on a per unit basis, and to calculate property management fees the AMP will pay to the COCC

Slide Number #79

Eligible Unit Months (EUM)Eligible Unit Months (EUM)

Occupied units are those occupied by: Eligible families Police officers Security PHA employees

Slide Number #80

Property Management Fee Property Management Fee Calculation ExampleCalculation Example

X { + + }

The Elms has 120 units = 1440 total unit months 1200 occupied unit months last year 100 HUD-Approved Vacant Unit Months

Management fee = $45 Calculation: 1200 + 100 x $45 = $58,500

PUM Prop Mgmt Fee

OccupiedHUD-

Approved Vacancy

Demo/DispUnit Mos

Slide Number #81

Fees Allowed under PBMFees Allowed under PBM

Property Management Fee – Demolition Year 1 75% of PUM management fee Year 2 50% of PUM management fee Year 3 25% of PUM management fee

Slide Number #82

Fees Allowed under PBMFees Allowed under PBM

Property Management Fee – Disposition Year 1 75% of PUM management fee Year 2 50% of PUM management fee

Slide Number #83

Fees Allowed under PBMFees Allowed under PBM

Bookkeeping fee An extension of the management fee For accounting for project funds, charged to

the project from the COCC Based on occupied units and allowable

vacancies HUD will consider $7.50 PUM reasonable

Page 6-22

Slide Number #84

Fees Allowed under PBMFees Allowed under PBM

Asset management fee Fee paid by project to COCC for oversight of

portfolio Based on total ACC Must be reasonable, not to exceed $10 PUM Only paid if the project has excess cash flow

(no limit first year)

Slide Number #85

Fees Allowed under PBMFees Allowed under PBM

In the 1st year of PBM, there is no excess cash requirement for the payment of the asset management fee

In the 2nd year, each AMP must have excess case to pay the asset management fee

In the 3rd year, excess cash must equal specific assets minus current liabilities minus one month’s operating expenses

Slide Number #86

Asset Management Fee Asset Management Fee Calculation ExampleCalculation Example

X

AMP has 120 units: $10 x 120 units x 12 months = $14,400

$10 PUMAsset Mgmt Fee

Total ACC Units

Slide Number #87

Capital Fund Management FeeCapital Fund Management Fee

CFG management fee will be an optional fee paid to the central office to cover all costs of the central office’s oversight and management (program administration) of the CFG

Page 6-22

Slide Number #88

Capital Fund Management FeeCapital Fund Management Fee

Fee may be up to 10% of the CFG including replacement housing funds The fee is paid by each AMP from CFG

proceeds

HUD is still defining the way the fee will be earned

Slide Number #89

Capital Fund Management FeeCapital Fund Management Fee

Examples of costs covered by the CFG management fee include the physical needs assessment, planning, preparation of the Annual Plan, processing of LOCCs draw downs, preparation of reports, budgeting, accounting, and procurement paid for with CFG

Slide Number #90

Capital Fund Management FeeCapital Fund Management Fee

This fee is not intended to cover costs associated with construction supervision and inspection These costs are considered frontline costs to

the project

Slide Number #91

Management Fees for Other PIH & Management Fees for Other PIH & HUD GrantsHUD Grants

If a fee rate has not been established for a grant: The COCC can charge up to 15% of the grant

amount as a management fee Where administrative costs are set through other

notices, regulations and existing grant agreements these policies and agreements are controlling

Slide Number #92

Fee Income Non-Program Fee Income Non-Program IncomeIncome

Reasonable fees charged to AMPs and programs are not considered federal program income for the purposes of 24 CFR part 85 Fee income is considered local revenue Control over its use is subject only to state or

local requirements imposed on individual PHAs

Slide Number #93

COCC – Working CapitalCOCC – Working Capital

Working capital for the COCC: HUD will allow the COCC to be initially

funded (year 1) with working capital of up to six months of property management, bookkeeping, and asset management fees based on 100% occupancy of all ACC units

Slide Number #94

Costs of a ProjectCosts of a Project

Project

Front line costs:Direct admin costsDirect maintenanceDirect office costsUtilitiesFees paid by project Management fee Asset management fee Bookkeeping fee Other fees for services

Central OfficeCost Center

Slide Number #95

How Cost Centers are How Cost Centers are FundedFunded

Central OfficeCost Center

Central MaintenanceCost Center

Waiting ListEligibility

Cost recovery based on fees paid by projects and from other programs

Cost recovery will occur based billing projects for services performed

Some centrally provided service costs will be allowed to be allocated to projects

RevenuesRevenuesProject

Revenues

- Dwelling rent

- Other tenant revenue

- Interest income

- Misc. income

- Operating subsidy

- Capital grant funds

-Management fees earned-Bookkeeping fees-Asset mgmt fees earned-Capital fund mgmt fees-S8 management fees-Other eligible reimbursements-No direct subsidy!!

COCCRevenues

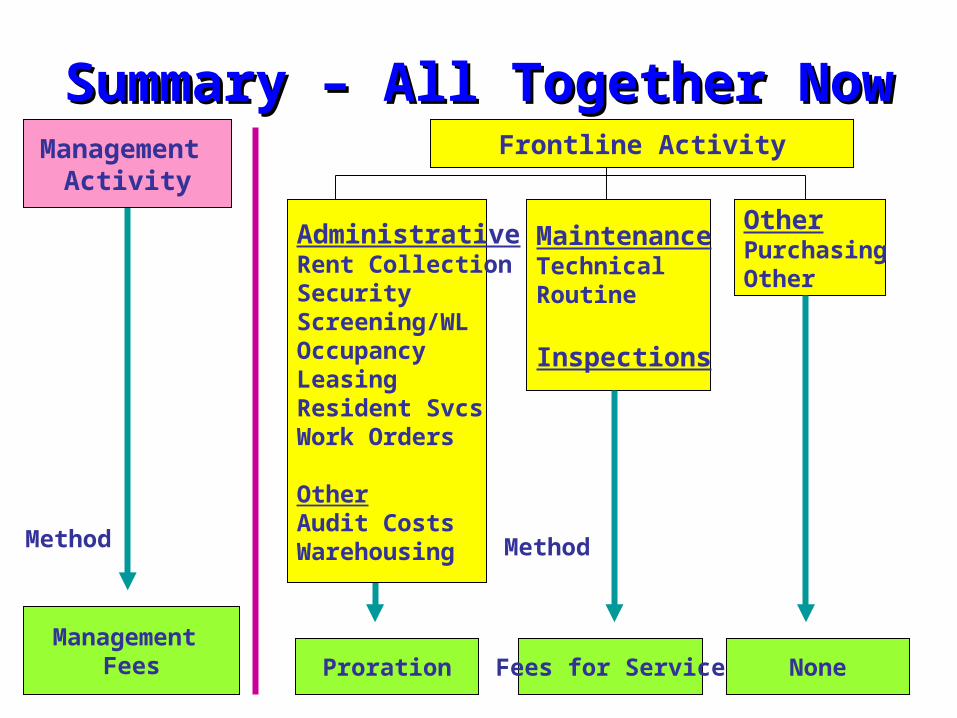

Summary – All Together NowSummary – All Together NowManagement

ActivityFrontline Activity

Method

Management Fees

AdministrativeRent CollectionSecurityScreening/WLOccupancyLeasingResident SvcsWork Orders

OtherAudit CostsWarehousing

MaintenanceTechnical Routine

Inspections

OtherPurchasingOther

Method

Proration Fees for Service None

Slide Number #98

Some Basic Financial ConceptsSome Basic Financial Concepts

Page 6-26

Slide Number #99

Key Financial TermsKey Financial Terms

Financial Data Schedule (FDS) is the HUD-required financial statement that’s submitted electronically to HUD FDS is submitted for each program of PHA PHAs will now be preparing the FDS to report

financial activity at the AMP level Balance sheet and income statement

Slide Number #100

Financial Data ScheduleFinancial Data Schedule

Slide Number #101

Financial Data ScheduleFinancial Data Schedule

Slide Number #102

Financial ReportsFinancial Reports

Income statement reports on an accrual basis how much the project has earned (revenue) and subtracts expenses, resulting in how much your project has made or lost in the period Gives you a sense of how well the project is

operating for the period of time assessed

Page 6-32

Slide Number #103

Financial ReportsFinancial Reports

Balance sheet shows the overall status of your project’s finances at a fixed point in time – a snapshot Totals all assets and subtracts liabilities to

compute overall net worth (or net loss) What the project owns, what it owes, what

it’s worth

Assignment of Assets and Assignment of Assets and LiabilitiesLiabilities

At the end of the first year of project-based accounting PHAs will assign all items on the balance sheet between the COCC, AMPs, and other programs

PHA Fiscal Year End Allocation Date

June June 30, 2008

September September 30, 2008

December December 31, 2008

March March 31, 2009

Slide Number #105

The BudgetThe Budget

The budget is a management tool Each AMP will have

its own budget Property managers

need to manage to their budgets

Page 6-65

Slide Number #106

Financial ReportsFinancial Reports

Budget is a financial forecast Estimates what each AMP expects to spend

(expenses) and earn (revenue) for period of time

It’s important for the PHA to train property managers to understand their AMP budgets and manage to them

Slide Number #107

Key Budgetary ConceptsKey Budgetary Concepts

Itemized projection of income and expenses over a specific period

Guideline for operating the project Tool to prevent fraud and theft Measure of project’s financial health Measure of staff performance

Slide Number #108

The BudgetThe Budget

Operating budget should be a realistic estimate and should contain: Operating receipts Operating admin Tenant service Utility expenses Maintenance

Protective services General expenses Nonroutine expenses

Slide Number #109

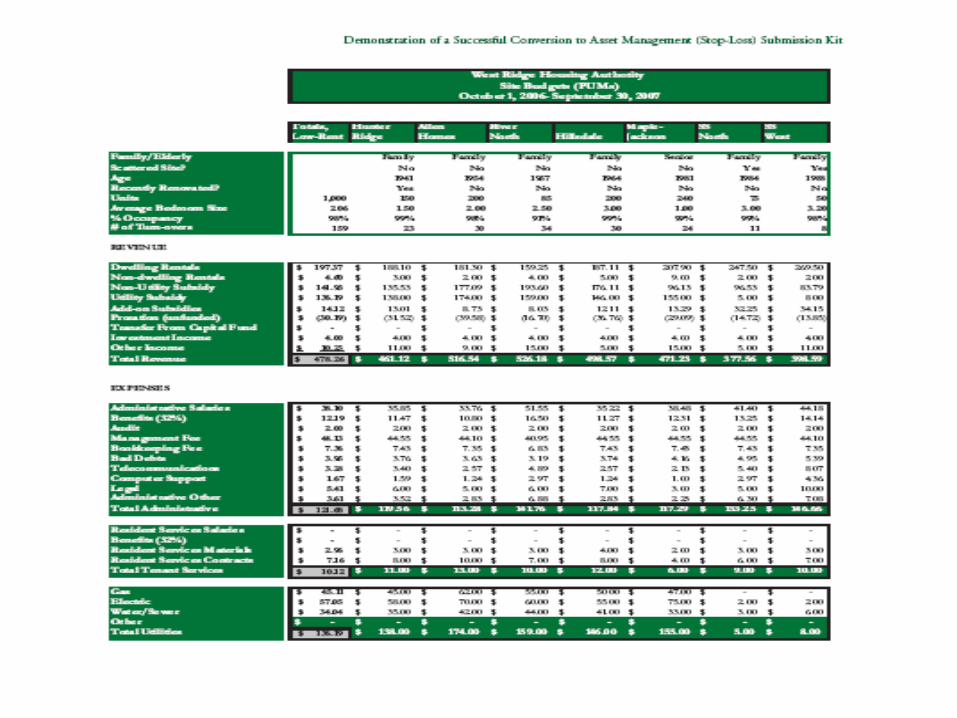

An AMP BudgetAn AMP Budget

Stop Loss Kit provides template Budgets for each projects must total budget of PH Budgets should include all charges and fees from

the COCC, and Capital expenses One budget spreadsheet will reflect PUM, and one

budget spreadsheet will reflect annual figures

Slide Number #110

An AMP BudgetAn AMP Budget

Sample AMP budget

The BudgetThe Budget

Sample Conventional BudgetSample Conventional Budget

Gross Potential Income (GPI)

- Vacancy and Collection Loss

+ Miscellaneous Income

= Effective Gross Income (EGI)

- Operating Expenses

= Net Operating Income (NOI)

- Reserves for Replacement

- Annual Debt Service (ADS)

= Cash Flow

Slide Number #113

The Budget ProcessThe Budget Process

To approach developing a budget, look at actual data from the past – see where the project underspent and overspent Decide what needs to change and what needs

to stay the same For example, a major marketing campaign may

be needed to improve lease-up Costs may need to be cut in some areas

Page 6-72

Slide Number #114

Excess Cash and FungibilityExcess Cash and Fungibility

Overview There are limitations and

freedoms on the use of project income depending whether your project has excess cash

Slide Number #115

Excess Cash and FungibilityExcess Cash and Fungibility

Excess cash is the project’s net liquid assets, or “surplus cash”

After the first year, calculation is based on prior year-end financial statements

Audited statements will determine final excess cash amount

Slide Number #116

Uses of Excess CashUses of Excess Cash

Retain funds for future project use Transfer funds to other AMP Pay as asset management fee to COCC Use for other HUD-approved eligible

purposes Financing new units, handling lawsuits,

covering accrued pension and retirement

Slide Number #117

Excess Cash and FungibilityExcess Cash and Fungibility

Uses of excess cash not permitted: Loaning or giving COCC cash other than as

the asset management fee Proceeds from the sale of assets to the

COCC – these belong to the AMP Except with HUD approval

Slide Number #118

Excess Cash DefinedExcess Cash Defined

Excess cash will be calculated from the FDS – it’s the sum of certain current assets minus the sum of all current liabilities, minus one month’s operating expenses for the AMP

Slide Number #119

Calculation of Excess CashCalculation of Excess Cash

Calculation of excess cash:Sum of asset accounts on the FDS

- Sum of ALL current liabilities- One month operating expenses for AMP

= Excess cash

Slide Number #120

FungibilityFungibility

Fungibility effective date Prior to first project-based submissions, on

or after July 1, 2008, all funds are considered fully fungible, including to the COCC Once the PHA has reported PBM data,

excess cash restrictions and limitations apply

Slide Number #121

FungibilityFungibility

In the 1st year of project-based accounting, full fungibility of op funds between projects

In the 2nd year, fungibility is allowed provided project has excess cash

In the 3rd year, fungibility will require that excess cash must equal at least one month of operating expenses

Slide Number #122

Allowable FungibilityAllowable Fungibility

Is this transfer fungible? Yes No

Transfer cash from AMP 1 to AMP2 Transfer cash from AMP 1 to COCC Transfer cash from HCV to AMP1 Transfer cash from Cap Fund to AMP1 Transfer cash from COCC to AMP1

Slide Number #123

Summary of Building BlocksSummary of Building Blocks

Slide Number #124

Project-Based FundingProject-Based Funding

Separate subsidy form for each project

Project Expense Level (PEL) is a major component

Ensures appropriate resources are allocated to each AMP based on unique characteristics

Project-based fundingProject-based funding

Slide Number #125

Project-Based BudgetingProject-Based Budgeting

Used for planning purposes Budgeted amounts must reconcile

to FDS Must be approved by PHA Board Not subject to HUD approval

Project-based funding

Project-based budgetingProject-based budgeting

Slide Number #126

Project-Based AccountingProject-Based Accounting

Income & expense are reported at the project level

Project financial statements are submitted to HUD at year end

Can only charge projects for services actually received

Fees must be reasonable Project-based funding

Project-based budgeting

Project-based accountingProject-based accounting

Slide Number #127

Project-Based ManagementProject-Based Management

Arrange property management services in the best interest of the project

Assign skilled management personnel to each project Project-based funding

Project-based budgeting

Project-based accounting

Project-based Project-based

managementmanagement

Slide Number #128

Project-Based Project-Based Performance AssessmentPerformance Assessment

PHAS will be revised to emphasize project-based monitoring

Each project will be evaluated on financial, managerial, physical condition, and Capital Fund Project-based funding

Project-based budgeting

Project-based accounting

Project-based management

Project-based Project-based performance assessmentperformance assessment

Slide Number #129

SummarySummary

Thank you for attending!

Join us again

Slide Number #130

Summary of Building BlocksSummary of Building Blocks

Thank you for attending! Join us again

Slide Number #131

Upcoming Lunch ‘n’ LearnsUpcoming Lunch ‘n’ Learns

April 4 – Adjusted Income April 25 – Housing 101: Overview for New

Managers and Directors May 2 – Verification Issues May 9 – Managing PHAS May 16 – Managing SEMAP