CapitaLand Receives ETL from SGX-ST to List its Integrated ...

39

CapitaLand Receives ETL from SGX-ST to List its Integrated Shopping Mall Business Transaction to be Tabled at EGM for Shareholders’ Approval NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES 5 October 2009

Transcript of CapitaLand Receives ETL from SGX-ST to List its Integrated ...

CapitaLand Receives ETL from SGX-ST to List itsIntegrated Shopping Mall Business

Transaction to be Tabled at EGM for Shareholders’ Approval

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

5 October 2009

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

This presentation is for information purposes only and is prepared solely for the purpose of providing shareholders of CapitaLand Limited with information withrespect to the matters for which their approval is being sought at the Extraordinary General Meeting to be convened. This presentation does not constitute orform part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of it form the basis of, or be relied inany connection with, any contract or commitment whatsoever to purchase or subscribe for shares or other securities in CapitaLand Limited, CapitaMalls AsiaLimited or any entity within or which is managed by the CapitaLand Limited group of companies (the "CapitaLand Group"). This presentation should not berelied upon as the basis of an investment decision in such shares or securities.

The information contained in this presentation has not been independently verified. No representation or warranty expressed or implied is made as to, and noreliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this presentation. NeitherCapitaLand Limited, CapitaMalls Asia Limited or any company within the CapitaLand Group, J.P. Morgan (S.E.A.) Limited, nor DBS Bank Ltd, or any of theirrespective affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising, whether directlyor indirectly, from any use, reliance or distribution of this presentation or its contents or otherwise arising in connection with this presentation.

This presentation may contain forward-looking statements that involve risks, uncertainties and other factors. Actual results, performance or achievements of the

Important

11

This presentation may contain forward looking statements that involve risks, uncertainties and other factors. Actual results, performance or achievements of thecompanies described therein may be materially different from any future results, performance or achievements expressed or implied by such forward-lookingstatements. Such forward-looking statements are based on numerous assumptions regarding the present and future business strategies and the environment inwhich the companies described herein will operate in the future, and must be read together with such assumptions. Predictions, projections or forecasts of theeconomy or economic trends of the markets are not necessarily indicative of the future or likely performance of these companies. Past performance is notnecessarily indicative of future performance. The future financial performance of the companies described herein is not guaranteed. You are cautioned not toplace undue reliance on these forward-looking statements.

This presentation is not an offer for sale of the securities in the United States or elsewhere. Shares in CapitaMalls Asia Limited may not be offered or sold in theUnited States absent registration or an exemption from registration under the U.S. Securities Act of 1933, as amended (the Securities Act). Any public offeringof securities of CapitaMalls Asia Limited in the United States would be made by means of a prospectus that would contain detailed information about thecompany and its management, as well as financial statements. CapitaLand Limited does not intend to register any portion of the offering in the United States orto conduct a public offering of securities in the United States.

This presentation may not be forwarded or distributed to any other person and may not be copied or reproduced in any manner whatsoever. Failure to complywith this directive may result in a violation of applicable laws of other jurisdictions.

Transaction Summary

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Transaction Summary

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

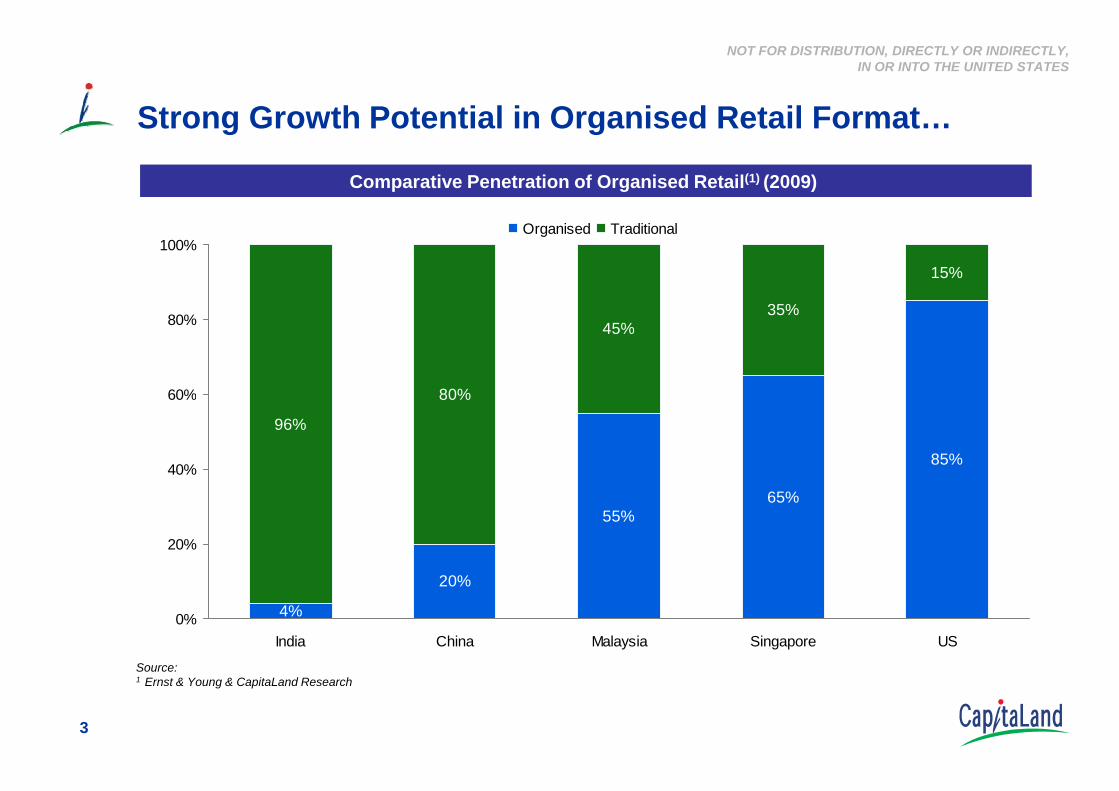

Strong Growth Potential in Organised Retail Format…

80%

45%35%

15%

60%

80%

100%Organised Traditional

Comparative Penetration of Organised Retail(1) (2009)

3

4%

20%

55%65%

85%

96%

80%

0%

20%

40%

60%

India China Malaysia Singapore US

Source:1 Ernst & Young & CapitaLand Research

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

…and High Growth Potential in Asia Retail Real Estate

Asia represents approximately 57% of the world’s population

Economic growth driving affluence & consumer spending power

4

Asia offers good potential for increase in retail space per capita

Capital appreciation potential for markets like China and India

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Proposed Listing of CapitaLand’s Integrated Shopping Mall Business

Real Estate

Australia Residential S’pore China Commercial ILEC

Hospitality Fin. Svcs

Serviced Residences FinancialRetail

29.83% (1)

55

CapitaLand intends to list its integrated shopping mall business(2), including its retail real estate business and its retail real estate fund and REIT management business

CapitaLand will retain majority control in CMA post listing and for the foreseeable future

1

Denotes listed entities

Effective interest 26.98% (1)

Fund & REITManagement

Retail Fund & REIT management

2

1 Stakes in CMT and CRCT as of 30 September 2009 2 Subject to EGM and prevailing market conditions

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Overview

66

Pan-Asian shopping mall portfolio

Unique integrated shopping mall business model

Direct capture of high growth Asian consumer trends

Proven track record

Balanced portfolio with China developments providing growth

Capital structure positioned to seize growth opportunities

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

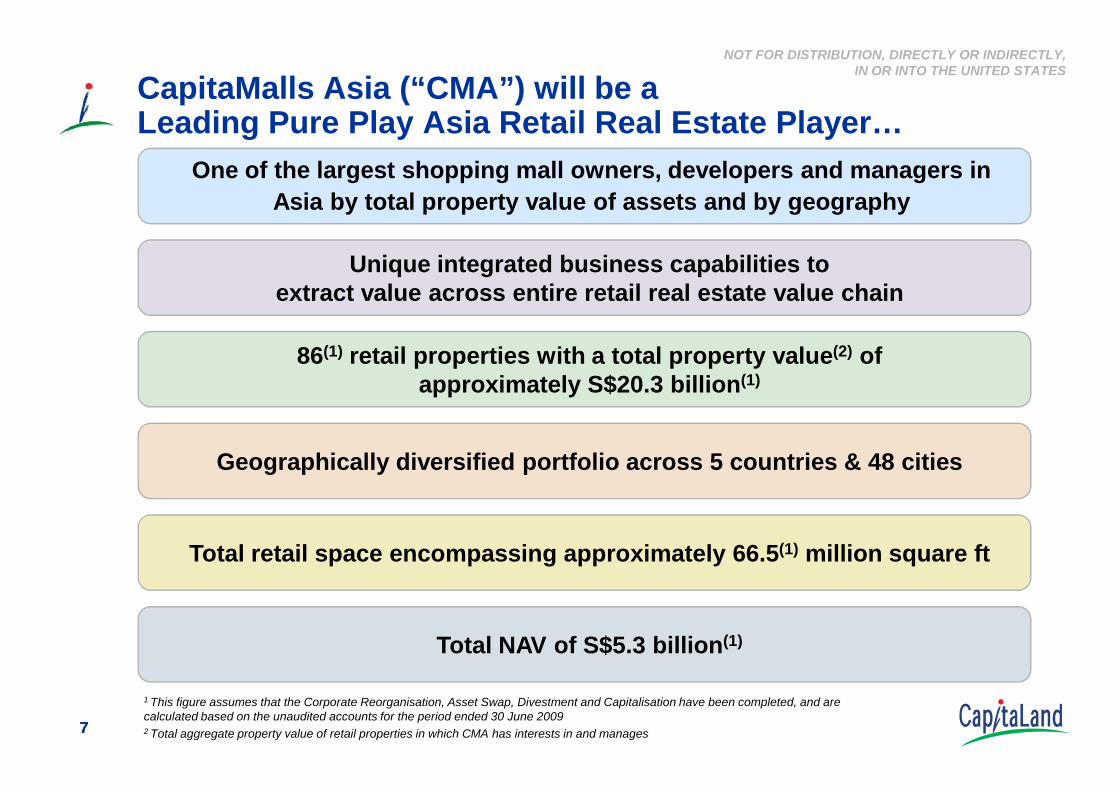

CapitaMalls Asia (“CMA”) will be aLeading Pure Play Asia Retail Real Estate Player…

One of the largest shopping mall owners, developers and managers in Asia by total property value of assets and by geography

86(1) retail properties with a total property value(2) of approximately S$20.3 billion(1)

Unique integrated business capabilities toextract value across entire retail real estate value chain

77

pp y

Geographically diversified portfolio across 5 countries & 48 cities

Total retail space encompassing approximately 66.5(1) million square ft

1 This figure assumes that the Corporate Reorganisation, Asset Swap, Divestment and Capitalisation have been completed, and arecalculated based on the unaudited accounts for the period ended 30 June 20092 Total aggregate property value of retail properties in which CMA has interests in and manages

Total NAV of S$5.3 billion(1)

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

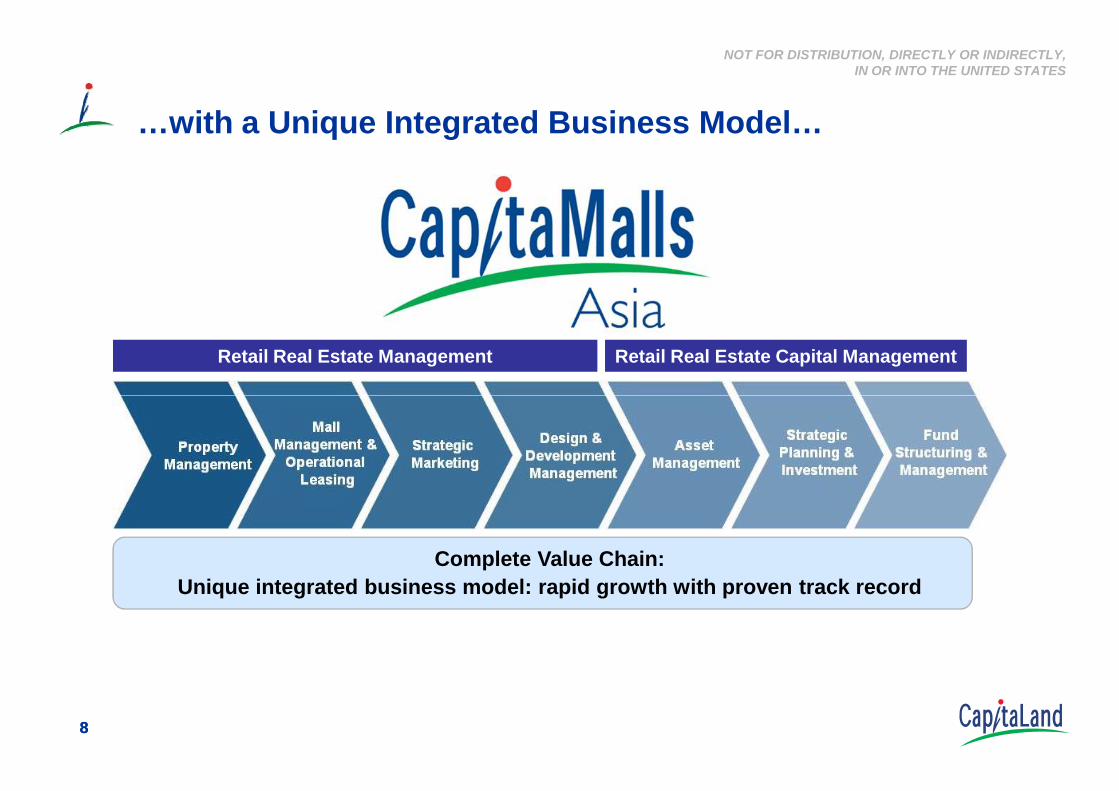

…with a Unique Integrated Business Model…

Retail Real Estate Management Retail Real Estate Capital Management

88

Complete Value Chain:Unique integrated business model: rapid growth with proven track record

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

…and Established Presence in Asia…

Udaip r

Jalandhar

Osaka

Hokkaido

TokyoKobeAnyang

Beijing

Ch h

Chengdu

Dalian

Deyang

Harbin

Hangzhou

Hohhot

Kunshan

Mianyang

Shanghai

Tianjin

Weifang

Wuhan Wuhu

Xinxiang

Yangzhou

Yibin Yiyang

Zibo

Zhengzhou

Rizhao

Xi’an

99

Singapore

Penang

Kuala Lumpur

Udaipur

Nagpur

Hyderabad

Cochin

Mysore

BangaloreMangalore

ChangshaChongqing

Dongguan

Foshan

Maoming

Nanchang

Quanzhou

ZhangzhouZhanjiang Zhaoqing Singapore

ChinaMalaysia

Japan

India

Pan-Asian Presence

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

…with a Proven Track Record…

1.2 1.8 3.5 4.9 6.9 7.01.3 1.1

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Jun-09

1.8 2.7 3.15.2

11.313.3

19.4 20.3

Effective interest in the

property values of CMA’s portfolio

Aggregate property value in which CMA has interest in and manage

As at

10

As of 31 December 2002 As of 30 June 2009 Number of retail property 5 86(4)(5) Staff 182 people 2,764 people Total property value (100% basis)(1) S$1.8 billion S$20.3 billion(6) Total property value (effective interest)(2) S$1.2 billion S$7.0 billion(6) Location of our asset interest Singapore Singapore, China, Malaysia, Japan, India GFA (square feet)(3 2.4 million 66.5 million(6)

Properties

Employees 182

5 10 10 24

659

55 78 96

2,764

86

Notes: (1) 100% basis refers to the aggregate property values of each property in the portfolio in its entirety.(2) Effective interest refers to the property values proportionate to CMA ownership interest in the properties. (3) The aggregate GFA of each property in the portfolio in its entirety.(4) The decrease from 96 retail properties in 2008 to 86 retail properties as of 30 June 2009 is primarily due to the Asset Swap and Divestment and Corporate Reorganisation . (5) Excludes interest in Horizon Realty Fund, which CMA does not manage, our investment in The Link REIT, and management of VivoCity, Singapore in which CMA do not have any ownership interest.(6) This figure assumes that the Corporate Reorganisation, Asset Swap, Divestment and Capitalisation have been completed, and are calculated based on the unaudited accounts for the period ended 30 June 2009.

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

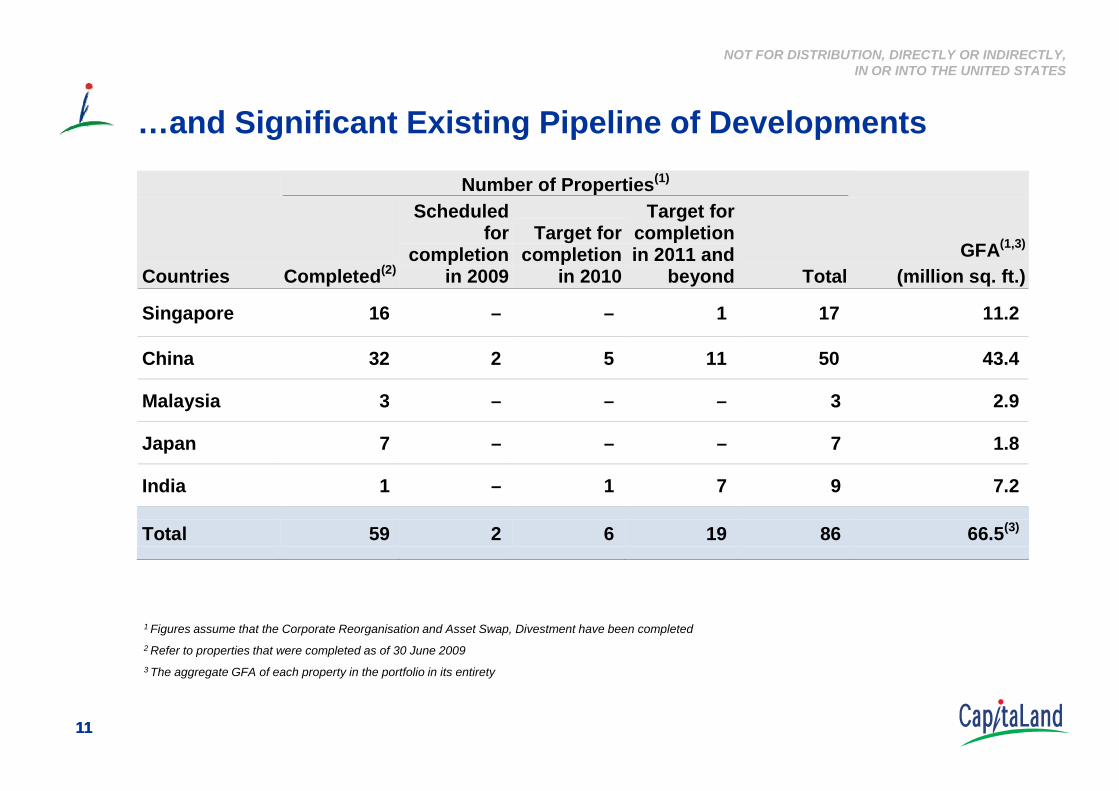

…and Significant Existing Pipeline of Developments

Number of Properties(1)

Countries Completed(2)

Scheduled for

completion in 2009

Target for completion

in 2010

Target for completion in 2011 and

beyond Total GFA(1,3)

(million sq. ft.)

Singapore 16 – – 1 17 11.2

China 32 2 5 11 50 43.4

M l i 3 3 2 9

1111

Malaysia 3 – – – 3 2.9

Japan 7 – – – 7 1.8

India 1 – 1 7 9 7.2

Total 59 2 6 19 86 66.5(3)

1 Figures assume that the Corporate Reorganisation and Asset Swap, Divestment have been completed2 Refer to properties that were completed as of 30 June 2009 3 The aggregate GFA of each property in the portfolio in its entirety

Transaction Rationale

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

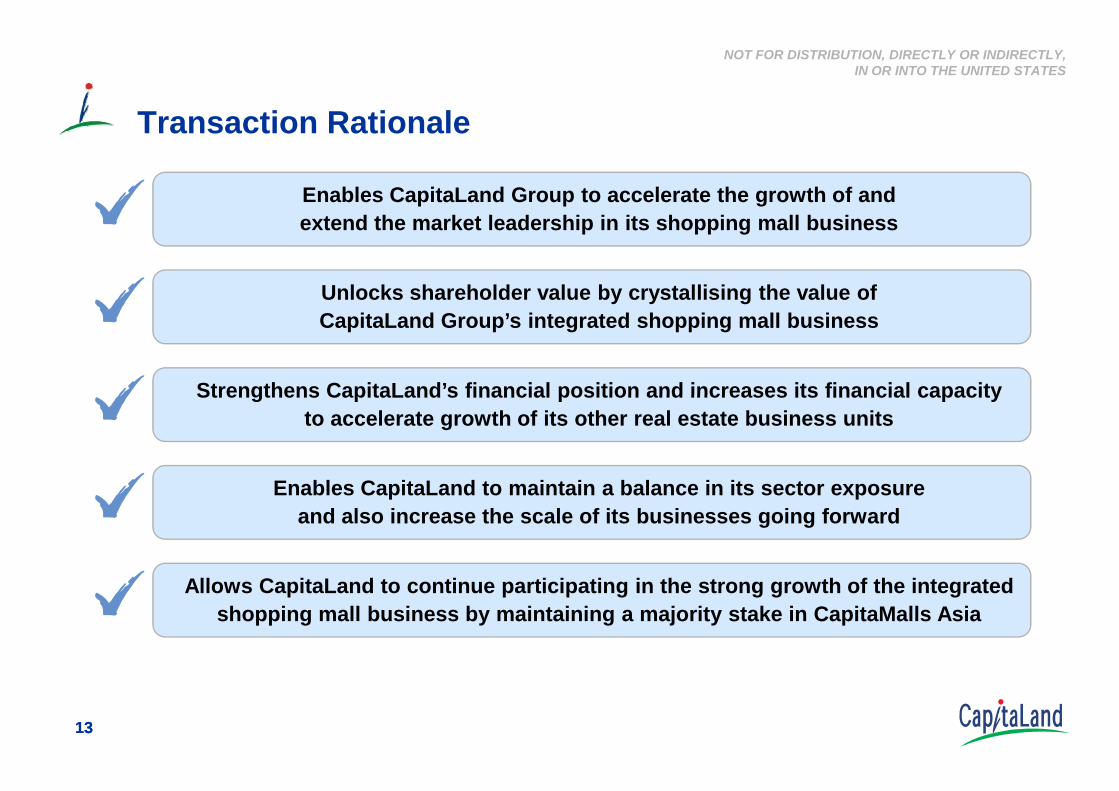

Transaction Rationale

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Transaction Rationale

Unlocks shareholder value by crystallising the value ofCapitaLand Group’s integrated shopping mall business

Strengthens CapitaLand’s financial position and increases its financial capacity

Enables CapitaLand Group to accelerate the growth of andextend the market leadership in its shopping mall business

1313

Strengthens CapitaLand s financial position and increases its financial capacity to accelerate growth of its other real estate business units

Allows CapitaLand to continue participating in the strong growth of the integrated shopping mall business by maintaining a majority stake in CapitaMalls Asia

Enables CapitaLand to maintain a balance in its sector exposureand also increase the scale of its businesses going forward

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Accelerates Growth of Shopping Mall Business 1

Significant financial capacity to seize opportunities in

Significant debt capacity(1)A

Direct access to the capital markets B

1414

Asia’s retail real estate sector, with primary focus in China

1 Assuming a net debt to equity ratio of 0.3 to 0.5, this will represent a potential debt capacity of approximately S$1.6 billion to S$2.6 billion

Acquisition of land for greenfield projects

Acquisition of completed malls

Asset enhancement initiatives

Asia wide M&A “roll-up” strategy

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

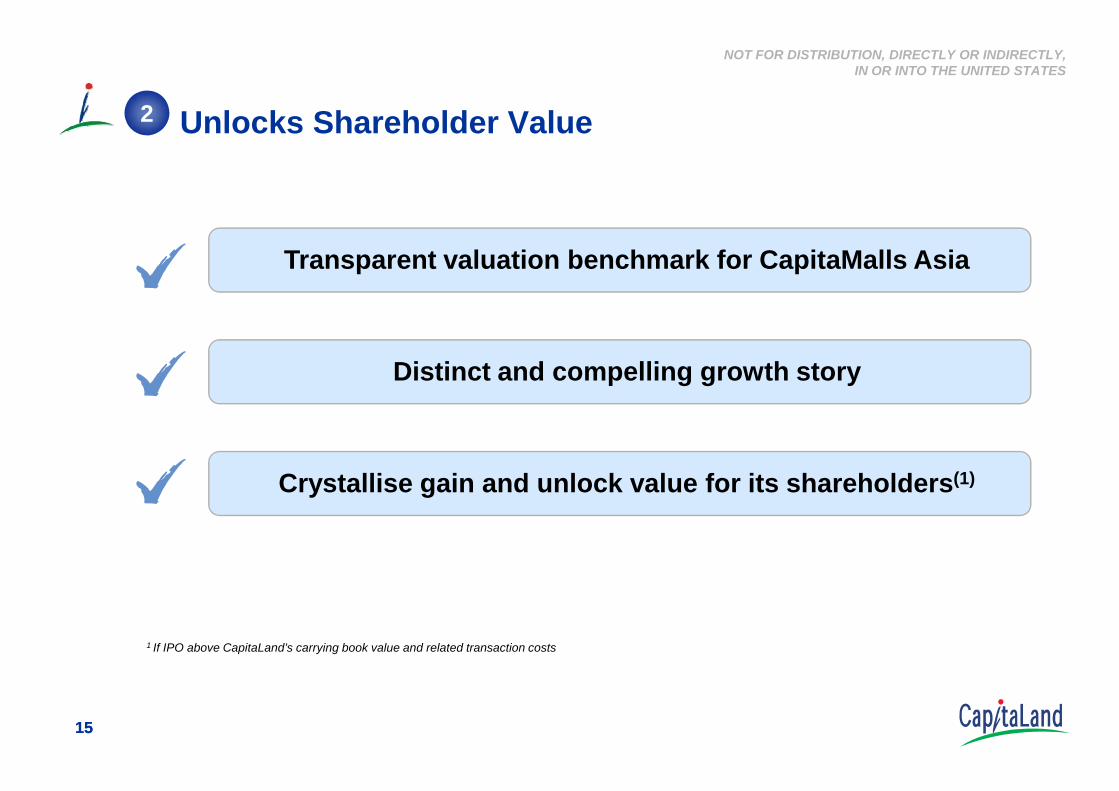

Unlocks Shareholder Value

Transparent valuation benchmark for CapitaMalls Asia

Distinct and compelling growth story

2

1515

Crystallise gain and unlock value for its shareholders(1)

1 If IPO above CapitaLand’s carrying book value and related transaction costs

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

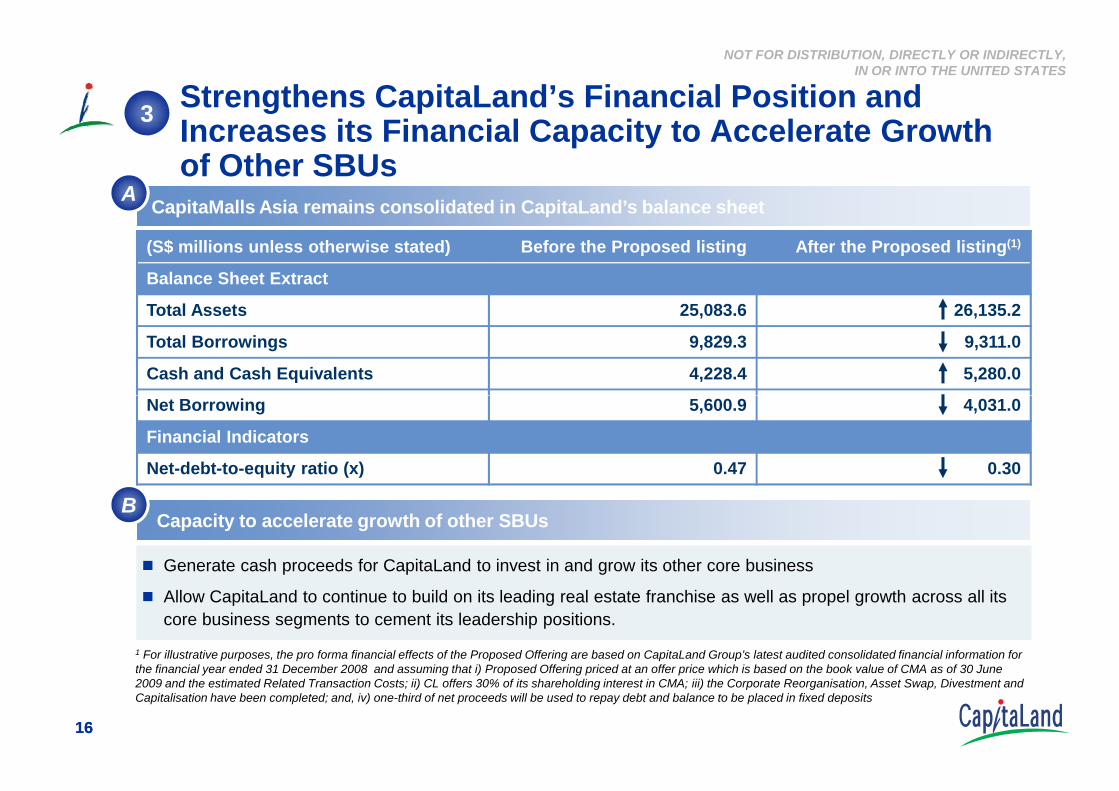

Strengthens CapitaLand’s Financial Position and Increases its Financial Capacity to Accelerate Growth of Other SBUs Cash

CapitaMalls Asia remains consolidated in CapitaLand’s balance sheet

3

A

(S$ millions unless otherwise stated) Before the Proposed listing After the Proposed listing(1)

Balance Sheet Extract

Total Assets 25,083.6 26,135.2

Total Borrowings 9,829.3 9,311.0

Cash and Cash Equivalents 4,228.4 5,280.0

1616

Capacity to accelerate growth of other SBUs

Generate cash proceeds for CapitaLand to invest in and grow its other core business

Allow CapitaLand to continue to build on its leading real estate franchise as well as propel growth across all its core business segments to cement its leadership positions.

B

Net Borrowing 5,600.9 4,031.0

Financial Indicators

Net-debt-to-equity ratio (x) 0.47 0.30

1 For illustrative purposes, the pro forma financial effects of the Proposed Offering are based on CapitaLand Group’s latest audited consolidated financial information for the financial year ended 31 December 2008 and assuming that i) Proposed Offering priced at an offer price which is based on the book value of CMA as of 30 June 2009 and the estimated Related Transaction Costs; ii) CL offers 30% of its shareholding interest in CMA; iii) the Corporate Reorganisation, Asset Swap, Divestment and Capitalisation have been completed; and, iv) one-third of net proceeds will be used to repay debt and balance to be placed in fixed deposits

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

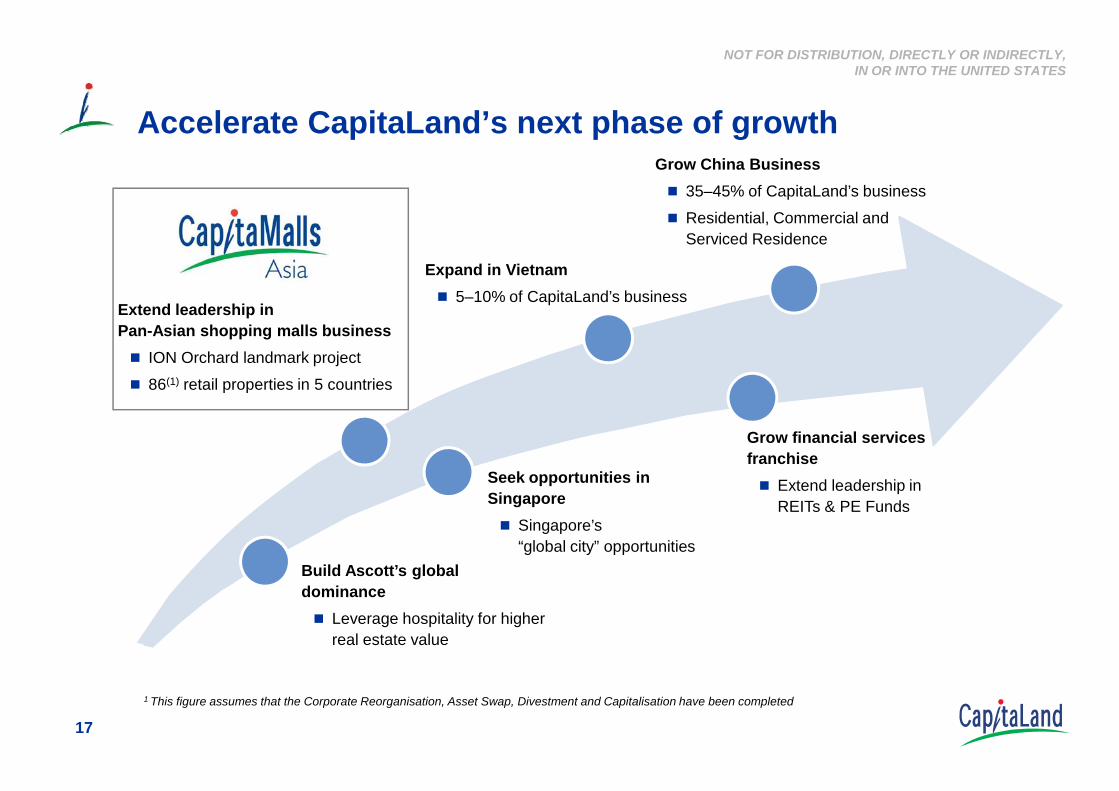

Accelerate CapitaLand’s next phase of growth

Extend leadership in Pan-Asian shopping malls business

ION Orchard landmark project

86(1) retail properties in 5 countries

Expand in Vietnam5–10% of CapitaLand’s business

Grow China Business35–45% of CapitaLand’s business

Residential, Commercial and Serviced Residence

17

Build Ascott’s global dominance

Leverage hospitality for higher real estate value

Seek opportunities in Singapore

Singapore’s “global city” opportunities

Grow financial services franchise

Extend leadership in REITs & PE Funds

1 This figure assumes that the Corporate Reorganisation, Asset Swap, Divestment and Capitalisation have been completed

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Maintains a Balance in its Sector Exposure and Increases the Scale of its Businesses Going Forward

Corporate Strategy

4

1818

Focus ScaleBalance

Enable CapitaMalls Asia to continue to expand rapidly to achieve scale with a direct access to capital markets

Allow CapitaLand to maintain a good balance of exposure in its portfolio of businesses

Incremental financial capacity will enable CapitaLand to increase scale of its other real estate business units

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Continues to Participate in the Strong Growth of theIntegrated Shopping Mall Business Through Majority Stake

5

1919

1 This figure assumes that the Corporate Reorganisation, Asset Swap, Divestment and Capitalisation have been completed, and are calculated based on the unaudited accounts for the period ended 30 June 2009

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

CapitaMalls Asia will be CapitaLand’s Vehiclefor Growth in Shopping Mall Business

CapitaMalls Asia will spearhead CapitaLand Group’s growth in the shopping mall business

To facilitate future collaboration, CL and CMA have entered into a Collaboration Agreement as set out below

Key collaboration framework

Other businesses apart from CMA business CMA business

2020

Retail Focus Properties /

Funds(2)

Other businesses – Residential, commercial,

serviced residence etc

Non-Retail Focus Properties /

Funds(1)

CL to offer CMA a right(3) to participate in CL’s stake pro-rata by retail contribution

1 Mix / integrated developments will fall under this category 2 Retail Focus Properties (including entities holding the properties) / Funds have retail component that contributes 65% or more of GFA, asset value, rental income of an asset, property or development Note: Such Retail Focus Properties currently form more than 90% of the total number of properties in CapitaMalls Asia's portfolio. 3 Right of first refusal does not apply to any non-retail property where the retail GFA component is less than 200,000 sq ft and to any non-retail entity where GFA of the retail component is less than 20%

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Potential Special Dividend

Upon the successful listing of CMA, the board of Directors may consider recommending a special dividend to CL shareholders, after taking into account:

The gain arising from the planned listing;

The overall cash position;

The net debt-to-equity ratio; and

2121

The growth strategies of other CapitaLand business units and their capital requirements

CapitaLand’s priority is to continue the growth of its business units

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Transaction Summary for CapitaLand

Unlock shareholder value

Increase overall financial capacity and flexibility of CapitaLand Groupto accelerate the growth of its other strategic business units

Accelerate growth of shopping mall business

2222

Achieve a balanced exposure in its business units

Increase scale of its business going forwardwhile still maintaining a conservative capital structure

Consistent with CapitaLand’s approach of optimising business growth with prudent capital management

Key highlights of CMA

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Key highlights of CMA

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

2424

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Key Competitive Strengths of CapitaMalls Asia

2525

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

CapitaMalls Asia’s Strategy

Strategic Initiatives

Focus

Balance Scale &Scalability

Singapore: Portfolio anchored by stable home base

China: Accelerate growth to build on early mover status

Malaysia: Extract organic growth & operational synergies

Japan: Tap on quality & established tenant base

India: Build presence through development pipeline

Other Asian markets: When suitable opportunities arise

FOCUS: Asian Retail Market

2626

Recurring income from operational malls & management fees

Support expansion plans in Asia

China expected to contribute significantly in medium term

India expected to contribute in the longer term

Benefit from economies of scale & tenant network effect

Achieve scale by through capital efficiency & productivity

Continue to invest in human capital to maximise capability to extract value across entire retail real estate value chain

BALANCE: Stable income supports expansion SCALE: Focus on markets that offer scale

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

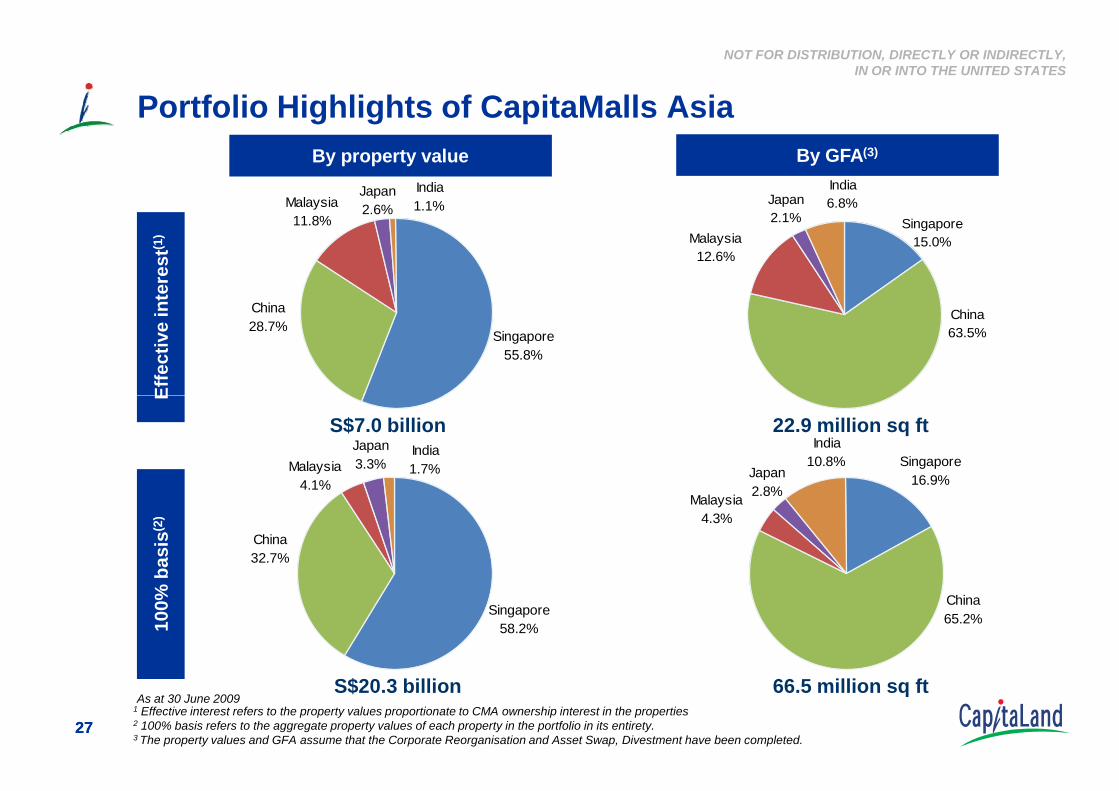

Singapore15.0%Malaysia

12.6%

India6.8%Japan

2.1%

China63.5%

Portfolio Highlights of CapitaMalls AsiaEf

fect

ive

inte

rest

(1)

By property value By GFA(3)

Singapore55.8%

Malaysia11.8%

India1.1%

Japan2.6%

China28.7%

2727

As at 30 June 20091 Effective interest refers to the property values proportionate to CMA ownership interest in the properties2 100% basis refers to the aggregate property values of each property in the portfolio in its entirety.3 The property values and GFA assume that the Corporate Reorganisation and Asset Swap, Divestment have been completed.

E10

0% b

asis

(2)

Singapore58.2%

Malaysia4.1%

India1.7%

Japan3.3%

China32.7%

S$20.3 billion

Singapore16.9%

Malaysia4.3%

India10.8%

Japan2.8%

China65.2%

22.9 million sq ft

66.5 million sq ft

S$7.0 billion

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

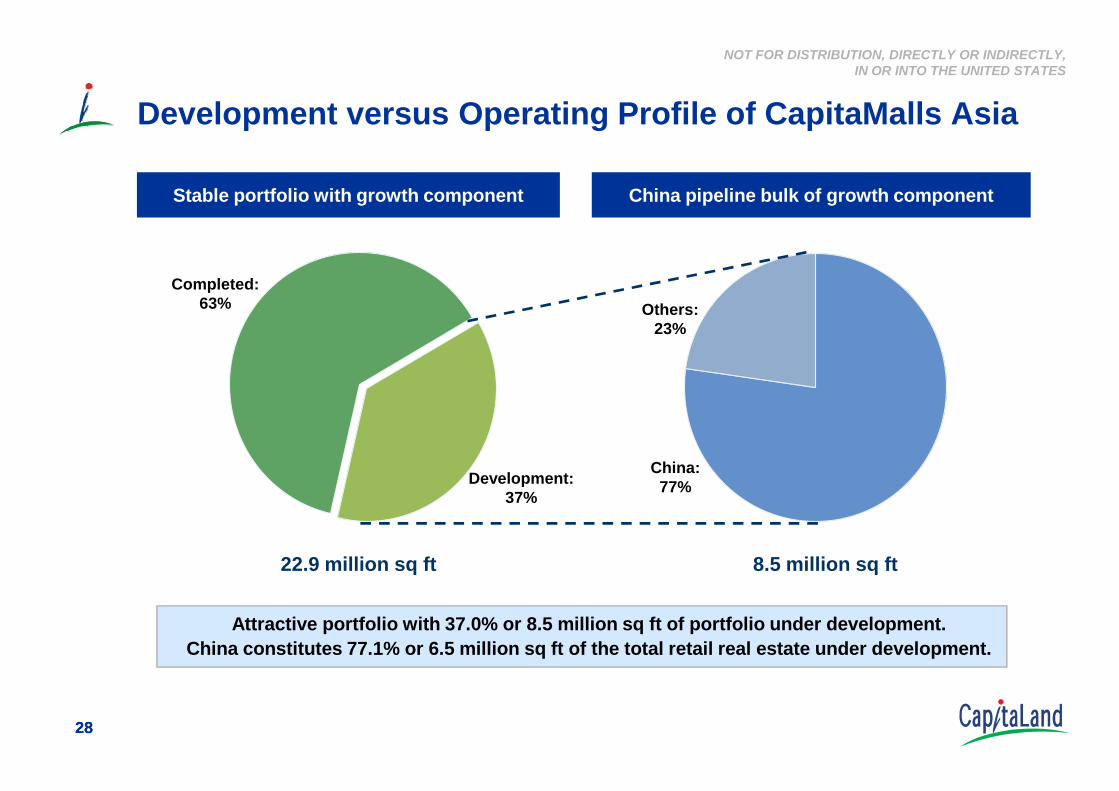

Development versus Operating Profile of CapitaMalls Asia

Stable portfolio with growth component China pipeline bulk of growth component

Completed: 63% Others:

23%

2828

Attractive portfolio with 37.0% or 8.5 million sq ft of portfolio under development.China constitutes 77.1% or 6.5 million sq ft of the total retail real estate under development.

22.9 million sq ft 8.5 million sq ft

Development: 37%

China: 77%

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

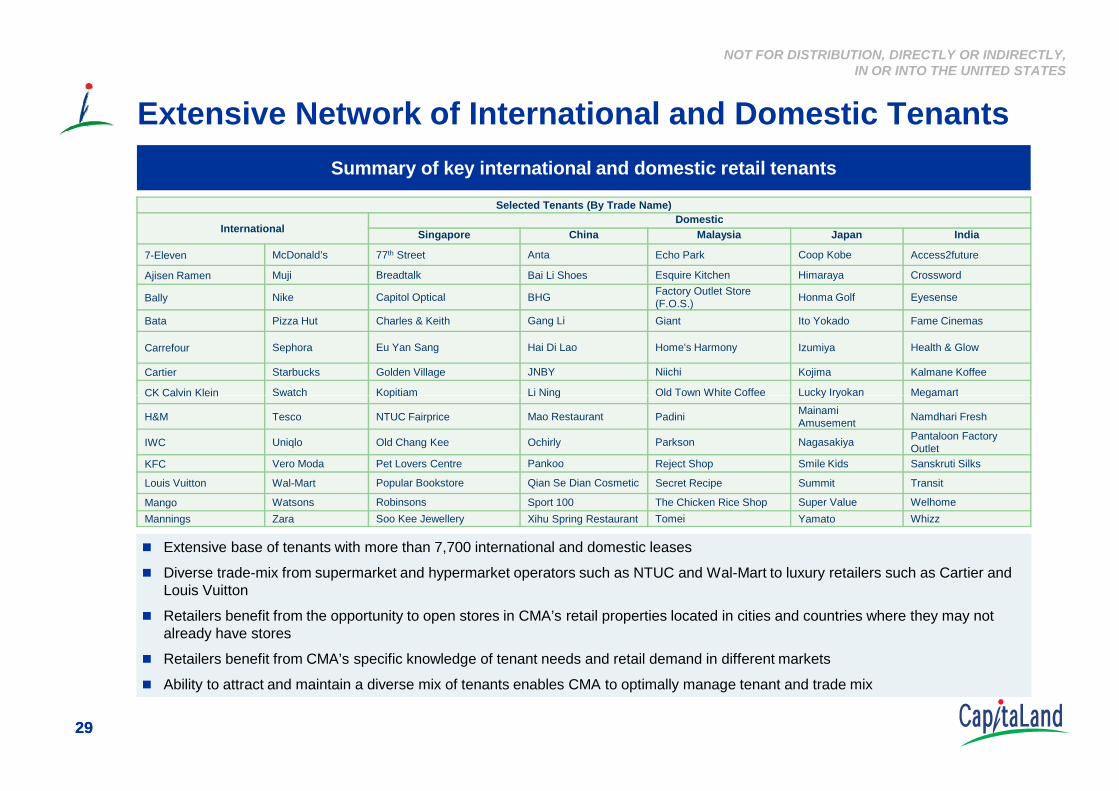

Extensive Network of International and Domestic Tenants Summary of key international and domestic retail tenants

Selected Tenants (By Trade Name)

InternationalDomestic

Singapore China Malaysia Japan India

7-Eleven McDonald’s 77th Street Anta Echo Park Coop Kobe Access2future

Ajisen Ramen Muji Breadtalk Bai Li Shoes Esquire Kitchen Himaraya Crossword

Bally Nike Capitol Optical BHG Factory Outlet Store (F.O.S.) Honma Golf Eyesense

Bata Pizza Hut Charles & Keith Gang Li Giant Ito Yokado Fame Cinemas

Carrefour Sephora Eu Yan Sang Hai Di Lao Home's Harmony Izumiya Health & Glow

Cartier Starbucks Golden Village JNBY Niichi Kojima Kalmane Koffee

CK Calvin Klein Swatch Kopitiam Li Ning Old Town White Coffee Lucky Iryokan Megamart

2929

Extensive base of tenants with more than 7,700 international and domestic leases

Diverse trade-mix from supermarket and hypermarket operators such as NTUC and Wal-Mart to luxury retailers such as Cartier and Louis Vuitton

Retailers benefit from the opportunity to open stores in CMA’s retail properties located in cities and countries where they may not already have stores

Retailers benefit from CMA’s specific knowledge of tenant needs and retail demand in different markets

Ability to attract and maintain a diverse mix of tenants enables CMA to optimally manage tenant and trade mix

CK Calvin Klein Swatch Kopitiam Li Ning Old Town White Coffee Lucky Iryokan Megamart

H&M Tesco NTUC Fairprice Mao Restaurant Padini Mainami Amusement Namdhari Fresh

IWC Uniqlo Old Chang Kee Ochirly Parkson Nagasakiya Pantaloon Factory Outlet

KFC Vero Moda Pet Lovers Centre Pankoo Reject Shop Smile Kids Sanskruti Silks

Louis Vuitton Wal-Mart Popular Bookstore Qian Se Dian Cosmetic Secret Recipe Summit Transit

Mango Watsons Robinsons Sport 100 The Chicken Rice Shop Super Value WelhomeMannings Zara Soo Kee Jewellery Xihu Spring Restaurant Tomei Yamato Whizz

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

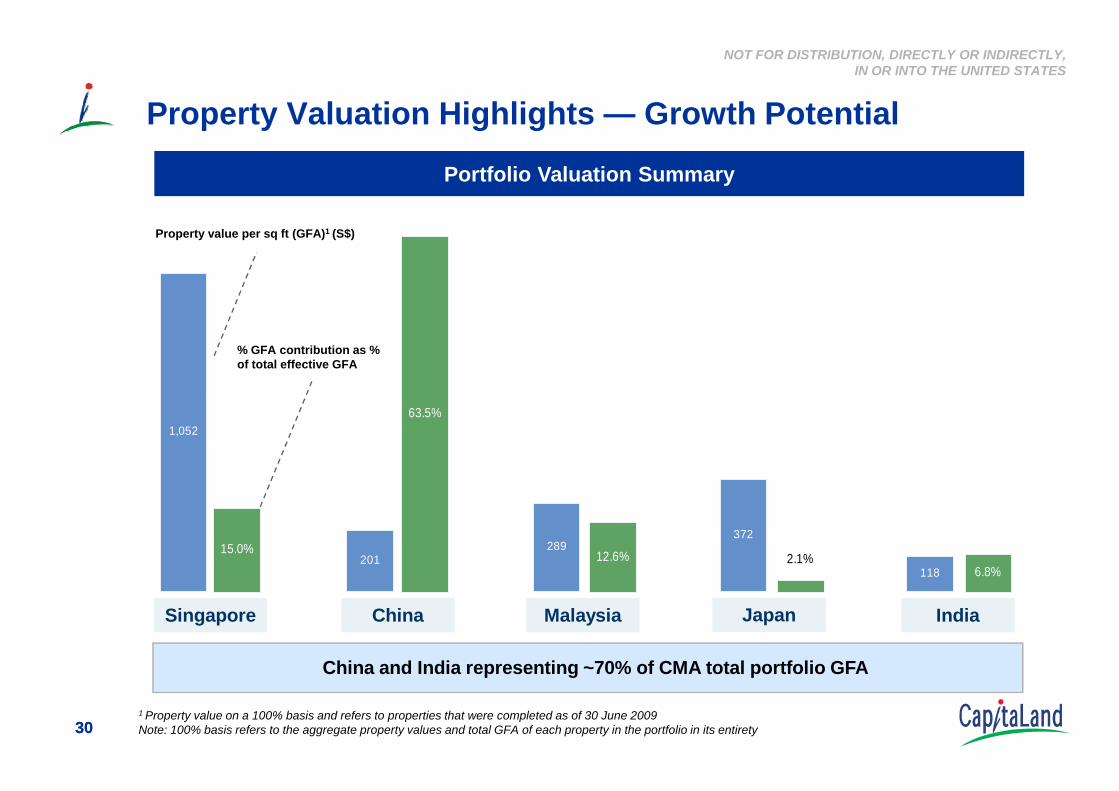

Property Valuation Highlights — Growth Potential

Property value per sq ft (GFA)1 (S$)

% GFA contribution as % of total effective GFA

Portfolio Valuation Summary

3030

China and India representing ~70% of CMA total portfolio GFA

1 Property value on a 100% basis and refers to properties that were completed as of 30 June 2009Note: 100% basis refers to the aggregate property values and total GFA of each property in the portfolio in its entirety

Singapore MalaysiaChina IndiaJapan

1,052

201289

372

118

15.0%

63.5%

12.6%6.8%

2.1%

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

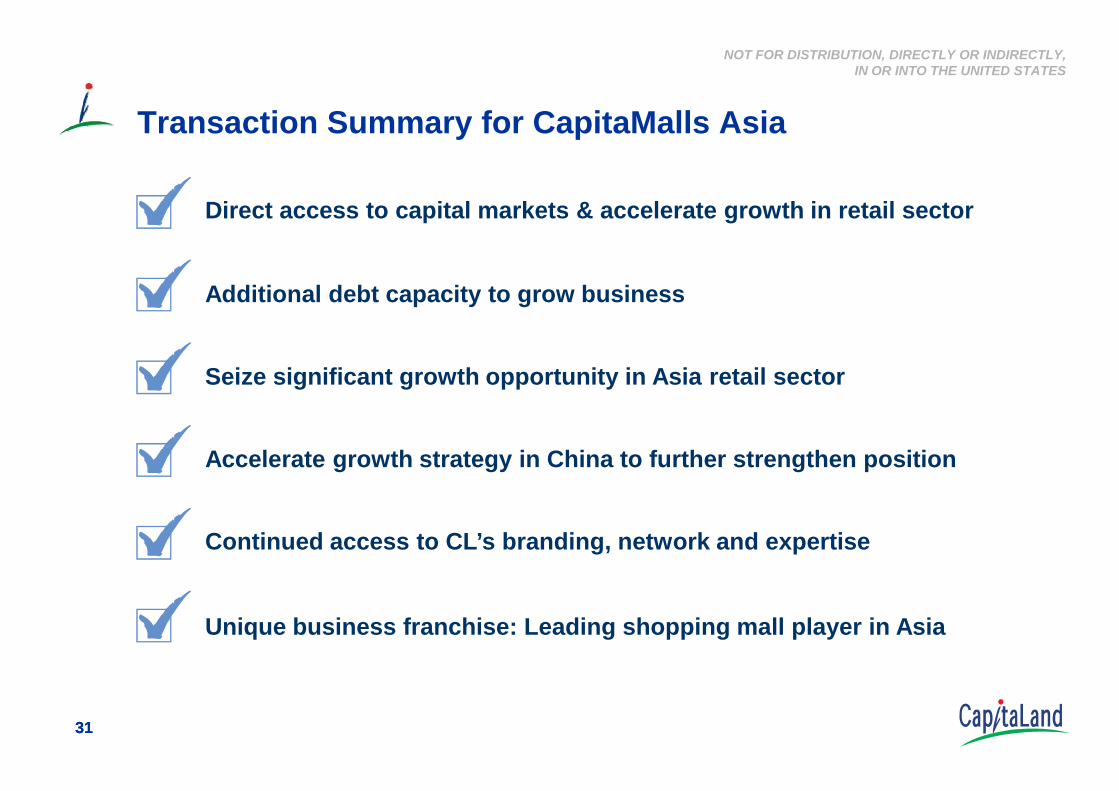

Transaction Summary for CapitaMalls Asia

Direct access to capital markets & accelerate growth in retail sector

Additional debt capacity to grow business

Seize significant growth opportunity in Asia retail sector

3131

Continued access to CL’s branding, network and expertise

Unique business franchise: Leading shopping mall player in Asia

Accelerate growth strategy in China to further strengthen position

Appendix

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

pp

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

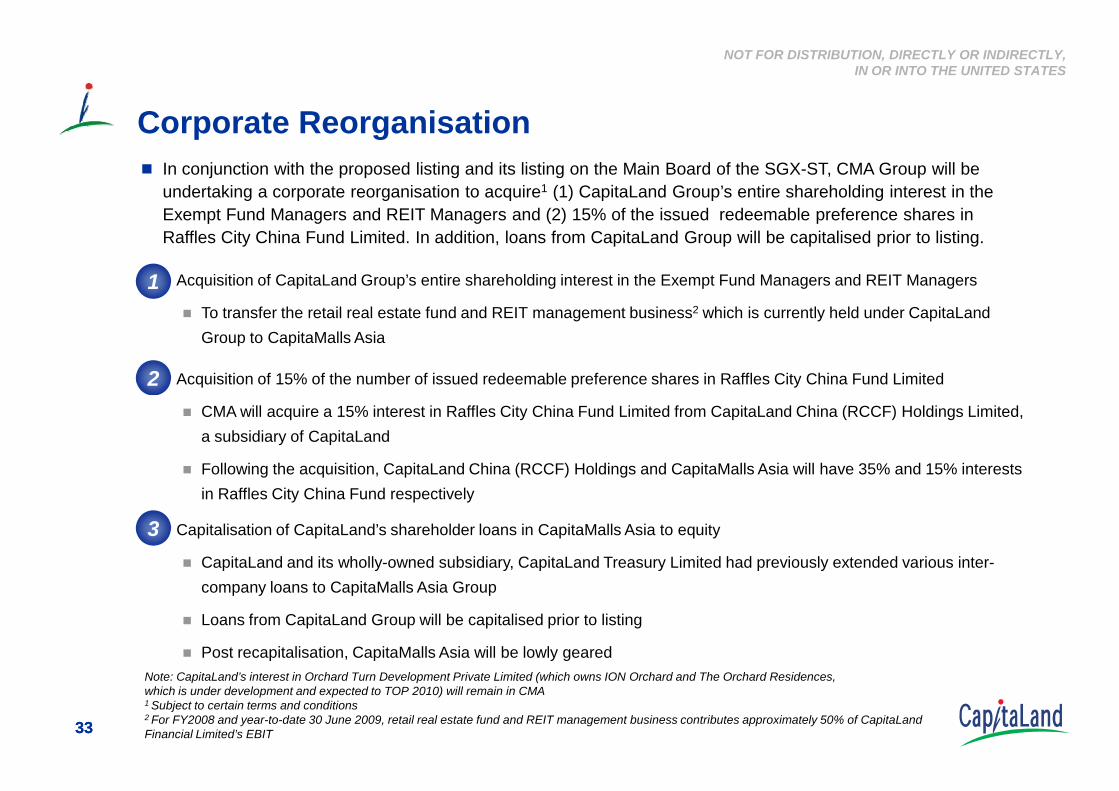

– Acquisition of 15% of the number of issued redeemable preference shares in Raffles City China Fund Limited

– Acquisition of CapitaLand Group’s entire shareholding interest in the Exempt Fund Managers and REIT Managers

To transfer the retail real estate fund and REIT management business2 which is currently held under CapitaLand Group to CapitaMalls Asia

Corporate Reorganisation In conjunction with the proposed listing and its listing on the Main Board of the SGX-ST, CMA Group will be undertaking a corporate reorganisation to acquire1 (1) CapitaLand Group’s entire shareholding interest in the Exempt Fund Managers and REIT Managers and (2) 15% of the issued redeemable preference shares in Raffles City China Fund Limited. In addition, loans from CapitaLand Group will be capitalised prior to listing.

1

2

3333

CMA will acquire a 15% interest in Raffles City China Fund Limited from CapitaLand China (RCCF) Holdings Limited, a subsidiary of CapitaLand

Following the acquisition, CapitaLand China (RCCF) Holdings and CapitaMalls Asia will have 35% and 15% interests in Raffles City China Fund respectively

– Capitalisation of CapitaLand’s shareholder loans in CapitaMalls Asia to equity

CapitaLand and its wholly-owned subsidiary, CapitaLand Treasury Limited had previously extended various inter-company loans to CapitaMalls Asia Group

Loans from CapitaLand Group will be capitalised prior to listing

Post recapitalisation, CapitaMalls Asia will be lowly geared Note: CapitaLand’s interest in Orchard Turn Development Private Limited (which owns ION Orchard and The Orchard Residences, which is under development and expected to TOP 2010) will remain in CMA 1 Subject to certain terms and conditions2 For FY2008 and year-to-date 30 June 2009, retail real estate fund and REIT management business contributes approximately 50% of CapitaLand Financial Limited’s EBIT

3

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

Overview of Business Structure

5 directly held retail properties

China Funds

CapitaRetail China Development Fund (45.0%)

CapitaRetail China De elopment F nd II (45 0%)

Directly held retail properties

Clarke Quay (100%)

One North (100%)

JV

Orchard Turn Development (50%)

China JapanMalaysia India(2)Singapore

Directly held retail properties

Gurney Plaza (100%)

Sungei Wang Plaza(1)

Mines Shopping Fair(1)

Japan fund

CapitaRetail Japan Fund (26.3%)

India fund

CapitaRetail India Development Fund (45.5%)

3434

Interest in and manage 17 properties(3)

(1 under development)

11.2 mil sq ft of GFA(3)

Interest in and manage 50 properties(3)

(18 under development)

43.4 mil sq ft of GFA(3)

Interest in and manage 3 properties(3)

2.9 mil sq ft of GFA(3)

Interest in and manage 9 properties(3)

(8 under development)

7.2 mil sq ft of GFA(3)

Interest in and manage 7 properties(3)

1.8 mil sq ft of GFA(3)

Development Fund II (45.0%)

CapitaRetail China Incubator Fund (30.0%)

Raffles City China Fund (15.0%)

21.10%29.83%

19.70%

Note: As of 30 September 2009 1 CMA holds 100% of the junior bonds issued in respect of Sungei Wang Plaza and Mines Shopping Fair 2

CMA has a 21.40% interest in Horizon Realty Fund in India 3 Number of properties and GFA assumes that the Corporate Reorganisation and Asset Swap, Divestment have been completed

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

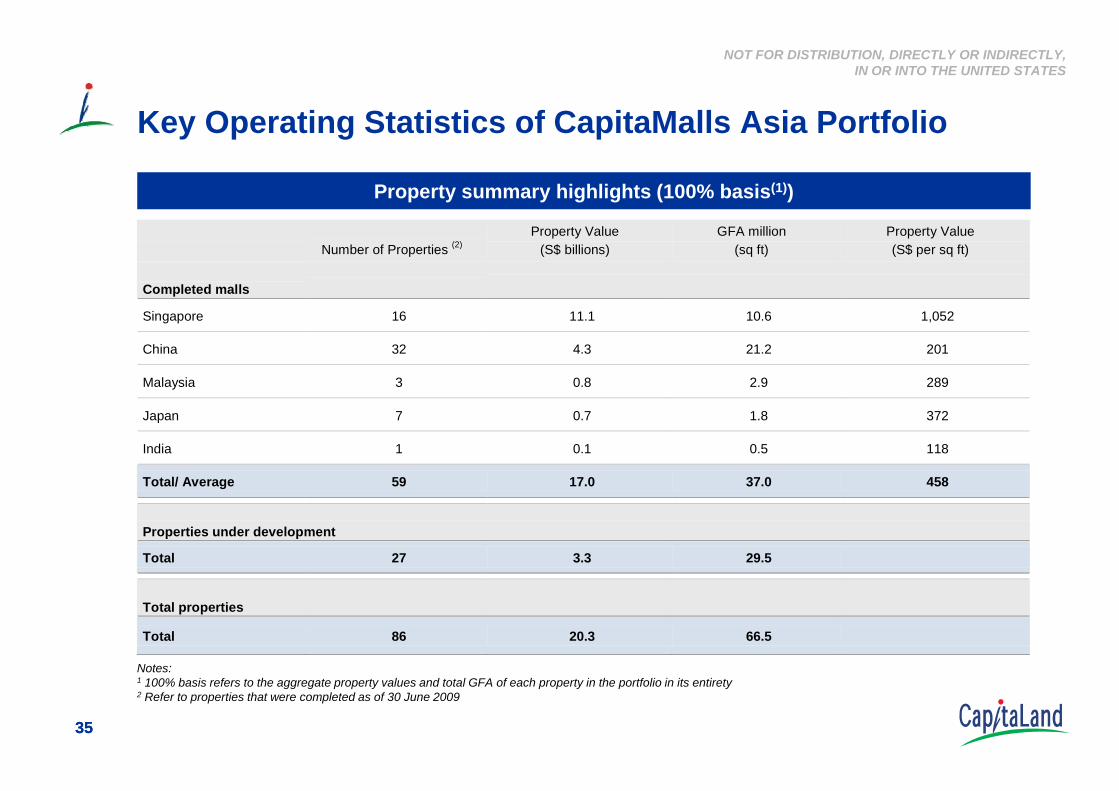

Key Operating Statistics of CapitaMalls Asia Portfolio

Number of Properties (2) Property Value

(S$ billions) GFA million

(sq ft) Property Value (S$ per sq ft)

Completed malls

Singapore 16 11.1 10.6 1,052

China 32 4.3 21.2 201

Malaysia 3 0.8 2.9 289

Property summary highlights (100% basis(1))

3535

Japan 7 0.7 1.8 372

India 1 0.1 0.5 118

Total/ Average 59 17.0 37.0 458

Properties under development

Total 27 3.3 29.5

Total properties

Total 86 20.3 66.5

Notes: 1 100% basis refers to the aggregate property values and total GFA of each property in the portfolio in its entirety2 Refer to properties that were completed as of 30 June 2009

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

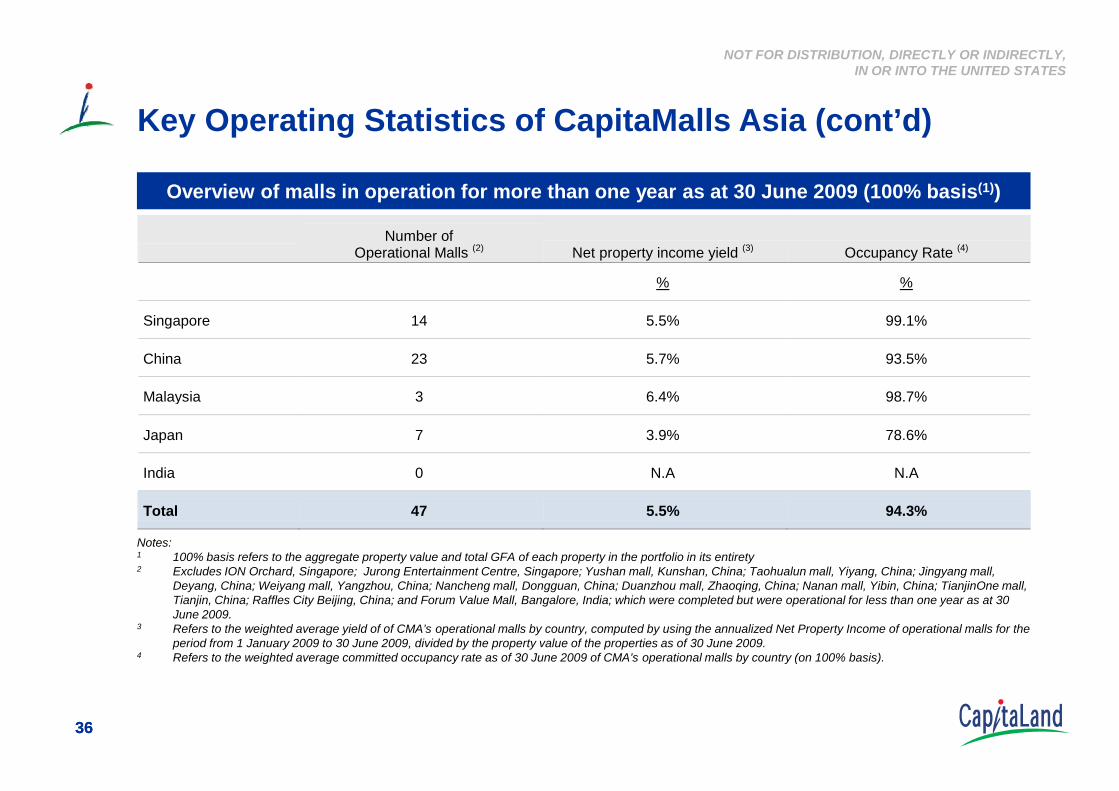

Number of

Operational Malls (2) Net property income yield (3) Occupancy Rate (4) % %

Singapore 14 5.5% 99.1%

China 23 5.7% 93.5%

Malaysia 3 6 4% 98 7%

Overview of malls in operation for more than one year as at 30 June 2009 (100% basis(1))

Key Operating Statistics of CapitaMalls Asia (cont’d)

3636

Malaysia 3 6.4% 98.7%

Japan 7 3.9% 78.6%

India 0 N.A N.A

Total 47 5.5% 94.3%

Notes: 1 100% basis refers to the aggregate property value and total GFA of each property in the portfolio in its entirety2 Excludes ION Orchard, Singapore; Jurong Entertainment Centre, Singapore; Yushan mall, Kunshan, China; Taohualun mall, Yiyang, China; Jingyang mall,

Deyang, China; Weiyang mall, Yangzhou, China; Nancheng mall, Dongguan, China; Duanzhou mall, Zhaoqing, China; Nanan mall, Yibin, China; TianjinOne mall, Tianjin, China; Raffles City Beijing, China; and Forum Value Mall, Bangalore, India; which were completed but were operational for less than one year as at 30 June 2009.

3 Refers to the weighted average yield of of CMA’s operational malls by country, computed by using the annualized Net Property Income of operational malls for the period from 1 January 2009 to 30 June 2009, divided by the property value of the properties as of 30 June 2009.

4 Refers to the weighted average committed occupancy rate as of 30 June 2009 of CMA’s operational malls by country (on 100% basis).

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

CMA’s EBIT ContributionFY2008 EBIT contribution by segments (unaudited)

EBIT (S$’Mil) Singapore China Malaysia Japan India Total

Property Business

Income from Property 66 71 27 4 (5) 163

Revaluation 96 19 43 (23) - 135

Management Business 37 14 (1) 1 - 51

Total 199 104 69 (18) (5) 349

1H09 EBIT contribution by segments (unaudited)

3737

1H09 EBIT contribution by segments (unaudited)

EBIT (S$’Mil) Singapore China Malaysia Japan India Total

Property Business

Income from property 44 15 26 6 (2) 89

Revaluation 161 (10) 0 (18) - 133

Management Business 15 8 (1) 1 - 23

Total 220 13 25 (11) (2) 245 Note: The Earnings Before Interests and Tax (EBIT) information presented above is derived from the combined financial information of the Group for the year ended 31 December 2008 and 6-month period ended 30 June 2009. The combined financial information presents CMA’s financial position and results of operations as if the Corporate Reorganisation (including the transfer of Exempt Funds and REIT managers and interests in Raffles City China Fund), had occurred as of the beginning of the earliest period presented. The combined financial information are prepared on a historical basis and does not take into account the intended capitalisation of shareholders' or related corporations loans.

EBIT presented may not be comparable to similarly titled measures presented by other companies and should not be compared against EBIT presented by other companies because not all companies use the same definition.

NOT FOR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

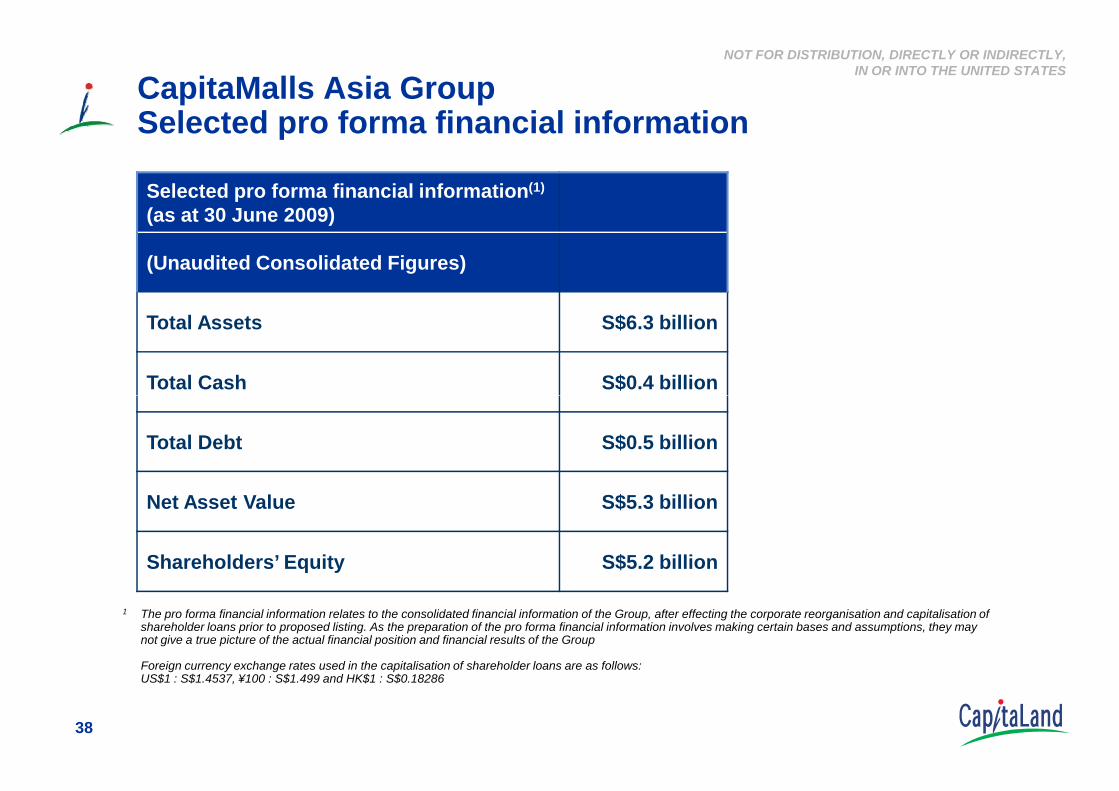

Selected pro forma financial information(1)

(as at 30 June 2009)

(Unaudited Consolidated Figures)

Total Assets S$6.3 billion

Total Cash S$0.4 billion

CapitaMalls Asia Group Selected pro forma financial information

38

Total Debt S$0.5 billion

Net Asset Value S$5.3 billion

Shareholders’ Equity S$5.2 billion

1 The pro forma financial information relates to the consolidated financial information of the Group, after effecting the corporate reorganisation and capitalisation of shareholder loans prior to proposed listing. As the preparation of the pro forma financial information involves making certain bases and assumptions, they may not give a true picture of the actual financial position and financial results of the Group

Foreign currency exchange rates used in the capitalisation of shareholder loans are as follows: US$1 : S$1.4537, ¥100 : S$1.499 and HK$1 : S$0.18286