Capital Budgeting Decisions. Chapter Objectives Understand the nature and importance of investment...

62

Capital Budgeting Decisions

-

Upload

lindsay-berry -

Category

Documents

-

view

221 -

download

0

Transcript of Capital Budgeting Decisions. Chapter Objectives Understand the nature and importance of investment...

Capital Budgeting Decisions

Chapter Objectives• Understand the nature and importance of investment decisions.• Distinguish between discounted cash flow (DCF) and non-

discounted cash flow (non-DCF) techniques of investment evaluation.

• Explain the methods of calculating net present value (NPV) and internal rate of return (IRR).

• Show the implications of net present value (NPV) and internal rate of return (IRR).

• Describe the non-DCF evaluation criteria: payback and accounting rate of return and discuss the reasons for their popularity in practice and their pitfalls.

• Illustrate the computation of the discounted payback.• Describe the merits and demerits of the DCF and Non-DCF

investment criteria.• Compare and contract NPV and IRR and emphasize the superiority

of NPV rule.

Nature of Investment DecisionsIntroduction• The investment decisions of a firm are generally known

as the capital budgeting, or capital expenditure decisions.

• The firm’s investment decisions would generally include expansion, acquisition, modernisation and replacement of the long-term assets. Sale of a division or business (divestment) is also as an investment decision.

• Decisions like the change in the methods of sales distribution, or an advertisement campaign or a research and development programme have long-term implications for the firm’s expenditures and benefits, and therefore, they should also be evaluated as investment decisions.

Features of Investment Decisions • The exchange of current funds for future

benefits.• The funds are invested in long-term assets.• The future benefits will occur to the firm over

a series of years.

Importance of Investment Decisions• Growth • Risk • Funding • Irreversibility• Complexity

Types of Investment Decisions• One classification is as follows:

– Expansion of existing business– Expansion of new business– Replacement and modernisation

• Yet another useful way to classify investments is as follows:– Mutually exclusive investments– Independent investments– Contingent investments

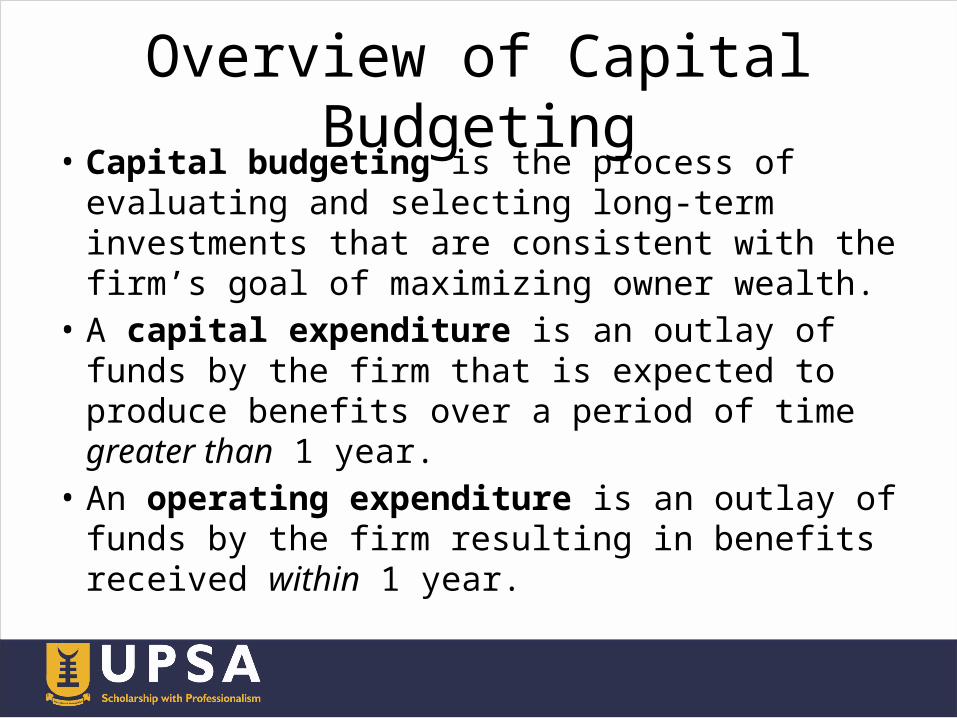

Overview of Capital Budgeting• Capital budgeting is the process of evaluating

and selecting long-term investments that are consistent with the firm’s goal of maximizing owner wealth.

• A capital expenditure is an outlay of funds by the firm that is expected to produce benefits over a period of time greater than 1 year.

• An operating expenditure is an outlay of funds by the firm resulting in benefits received within 1 year.

Overview of Capital Budgeting • The process through which different projects are

evaluated is known as capital budgeting• Capital budgeting is defined “as the firm’s formal

process for the acquisition and investment of capital. It involves firm’s decisions to invest its current funds for addition, disposition, modification and replacement of fixed assets”.

• “Capital budgeting is long term planning for making and financing proposed capital outlays”- Charles T Horngreen.

Overview of Capital Budgeting“Capital budgeting consists in planning development

of available capital for the purpose of maximizing the long term profitability of the concern” – Lynch

• The main features of capital budgeting are a. potentially large anticipated benefits b. a relatively high degree of risk c. relatively long time period between the initial

outlay and the anticipated return.

Significance of capital budgeting

• The success and failure of business mainly depends on how the available resources are being utilised.

• Main tool of financial management• All types of capital budgeting decisions are exposed to

risk and uncertainty.• They are irreversible in nature.• Capital rationing gives sufficient scope for the

financial manager to evaluate different proposals and only viable project must be taken up for investments.

• Capital budgeting offers effective control on cost of capital expenditure projects.

• It helps the management to avoid over investment and under investments.

Capital Budgeting Process1. Project generation: Generating the proposals for

investment is the first step. The investment proposal may fall into one of the following

categories: • Proposals to add new product to the product line,• proposals to expand production capacity in existing lines• proposals to reduce the costs of the output of the

existing products without altering the scale of operation. • Sales campaigning, trade fairs people in the industry, R

and D institutes, conferences and seminars will offer wide variety of innovations on capital assets for investment.

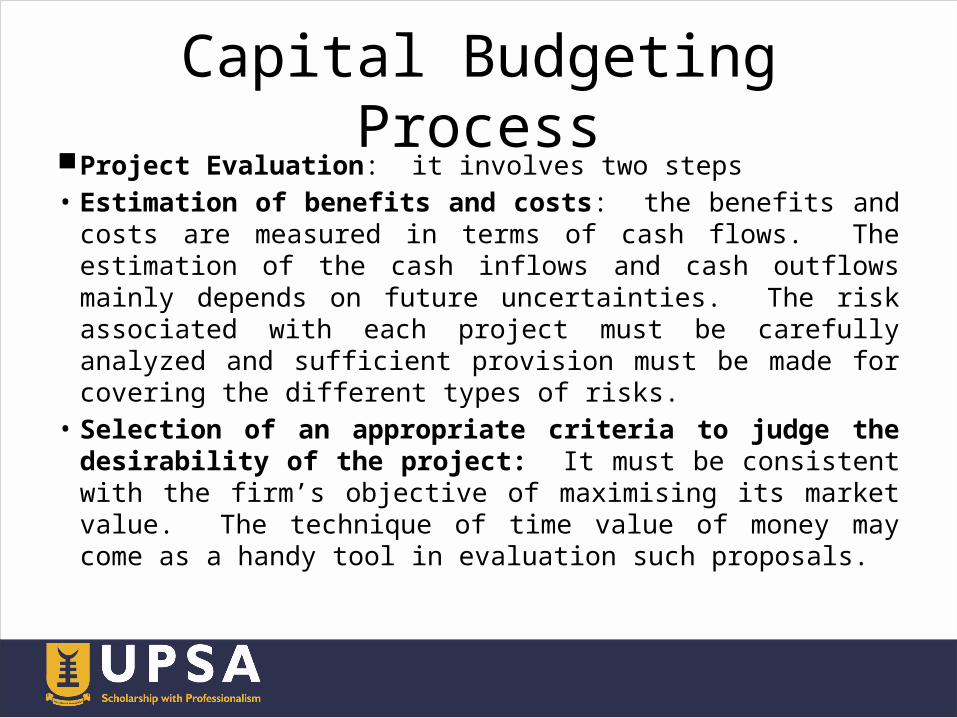

Capital Budgeting Process Project Evaluation: it involves two steps• Estimation of benefits and costs: the benefits and costs

are measured in terms of cash flows. The estimation of the cash inflows and cash outflows mainly depends on future uncertainties. The risk associated with each project must be carefully analyzed and sufficient provision must be made for covering the different types of risks.

• Selection of an appropriate criteria to judge the desirability of the project: It must be consistent with the firm’s objective of maximising its market value. The technique of time value of money may come as a handy tool in evaluation such proposals.

Capital Budgeting Process Project Selection: No standard administrative procedure can be

laid down for approving the investment proposal. The screening and selection procedures are different from firm to firm.

Project Evaluation: Once the proposal for capital expenditure is finalized, it is the duty of the finance manager to explore the different alternatives available for acquiring the funds. He has to prepare capital budget. Sufficient care must be taken to reduce the average cost of funds. He has to prepare periodical reports and must seek prior permission from the top management. Systematic procedure should be developed to review the performance of projects during their lifetime and after completion. The follow up, comparison of actual performance with original estimates not only ensures better forecasting but also helps in sharpening the techniques for improving future forecasts.

Factors Influencing Capital Budgeting

• Availability of funds• Structure of capital• Taxation policy• Government policy• Lending policies of financial institutions• Immediate need of the project• Earnings• Capital return• Economical value of the project• Working capital • Accounting practice• Trend of earnings

Investment Evaluation Criteria• Three steps are involved in the evaluation of

an investment:– Estimation of cash flows– Estimation of the required rate of return (the opportunity

cost of capital)– Application of a decision rule for making the choice

Investment Decision Rule• It should maximise the shareholders’ wealth.• It should consider all cash flows to determine the true profitability

of the project.• It should provide for an objective and unambiguous way of

separating good projects from bad projects.• It should help ranking of projects according to their true

profitability.• It should recognise the fact that bigger cash flows are preferable to

smaller ones and early cash flows are preferable to later ones.• It should help to choose among mutually exclusive projects that

project which maximises the shareholders’ wealth.• It should be a criterion which is applicable to any conceivable

investment project independent of others.

Cash Flow Estimation• General outline for estimating new venture cash flows

– Pre-start-up, the initial outlay—everything that has to be spent before the project is started

– Sales forecast—units and revenues– Cost of sales and expenses– Assets—new assets to be acquired, including changes in

working capital– Amortization—non-cash expense but affects income taxes– Taxes and earnings– Summarize and combine—adjust earnings for amortization

and combine result with balance sheet items to arrive at a cash flow estimate

A Few Specific Issues• The Typical Pattern

• At beginning of the project, some amount must be spent to invest in the project (Initial outlay)

– Subsequent cash flows tend to be positive

• Project Cash Flows Are Incremental• What cash flows will occur if we undertake this project

that wouldn’t occur if we left it undone and continued business as before?

A Few Specific Issues• Sunk Costs

– Costs that have already occurred and cannot be recovered—should not be included in project’s cash flows

• Only future costs are relevant

• Opportunity Costs– What is given up to undertake the new project– The opportunity cost of a resource is its value in its best

alternative use – For instance, if firm needs a new warehouse, it could either:

– Lease warehouse space– Buy warehouse– Build warehouse on land they currently own (but could

sell for $1,000,000)—the $1,000,000 represents an opportunity cost

A Few Specific Issues• Impacts on Other Parts of Company

– Sales erosion (cannibalization)—when firm sells a product that competes with other products within the same firm (Diet Coke vs. Coke Classic)

– Margin lost in other line—negative cash flow for project

• Taxes– Cash outflow– Use after-tax cash flows

• Cash Versus Accounting Results– Capital budgeting deals only with cash flows; however

business managers want to know project’s net income

A Few Specific Issues• Working Capital

– New project often requires investment in working capital—inventory, for instance

– Increasing net working capital means cash outflow • Ignore Financing Costs

– Do not include interest expense on debt (or dividends on shares) as cash outflow

– Addressed via discount rate when determining NPV or evaluating IRR

• Old Equipment– If this is replacement project, old equipment can be sold

(thereby generating a cash inflow)

Cash Flow Estimation

Calculation of cash outflow

Cost of project/asset xxxxTransportation/installation charges xxxxWorking capital xxxxCash outflow xxxx

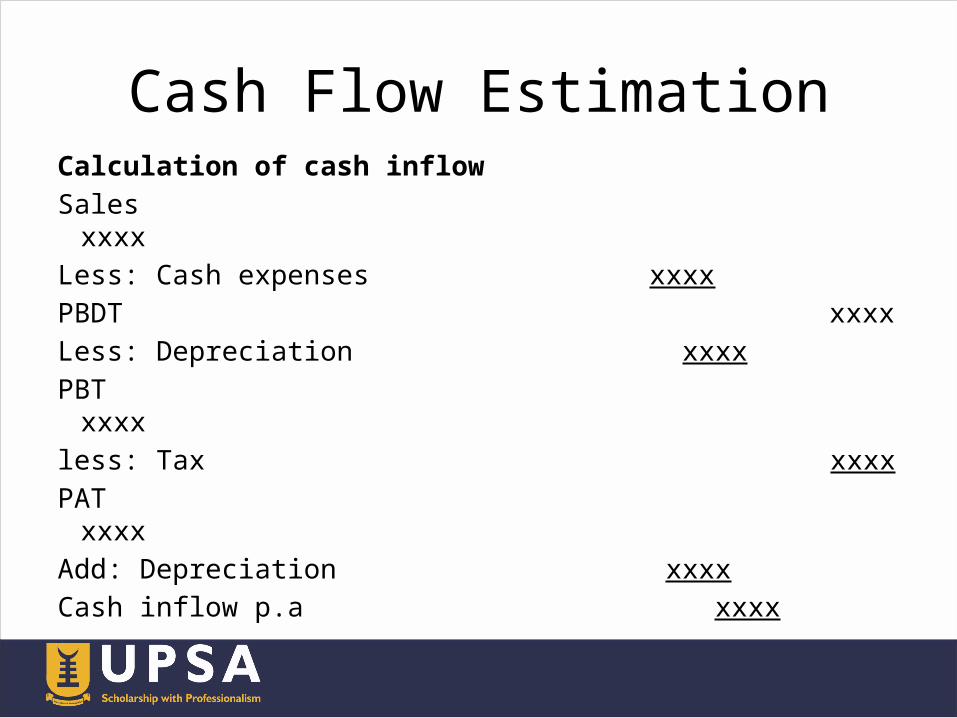

Cash Flow EstimationCalculation of cash inflowSales xxxxLess: Cash expenses xxxxPBDT xxxxLess: Depreciation xxxxPBT xxxxless: Tax xxxxPAT xxxxAdd: Depreciation xxxxCash inflow p.a xxxx

Evaluation Techniques1. Non-discounted Cash Flow Criteria

– Payback Period (PB)– Accounting Rate of Return (ARR)

2. Discounted Cash Flow (DCF) Criteria– Net Present Value (NPV)– Internal Rate of Return (IRR)– Profitability Index (PI)– Discounted Payback Period (DPB)

Accounting Rate of Return It considers the earnings of the project of the economic life. This

method is based on conventional accounting concepts. The rate of return is expressed as percentage of the earnings of the investment in a particular project. The profits under this method is calculated as profit after depreciation and tax of the entire life of the project.

• This method of ARR is not commonly accepted in assessing the profitability of capital expenditure. Because the method does not consider the heavy cash inflow during the project period as the earnings with be averaged. The cash flow advantage derived by adopting different kinds of depreciation is also not considered in this method.

Accounting Rate of Return• Accept or Reject Criterion: Under the method,

all project, having Accounting Rate of return higher than the minimum rate establishment by management will be considered and those having ARR less than the pre-determined rate. This method ranks a Project as number one, if it has highest ARR, and lowest rank is assigned to the project with the lowest ARR.

Accounting Rate of Return• Under this method average annual profit(after

tax) is expressed as percentage of investment. ARR is found out by dividing average income by the average investment. ARR is calculated with the help of the following formula ;

• ARR = Average income or return × 100 average investment

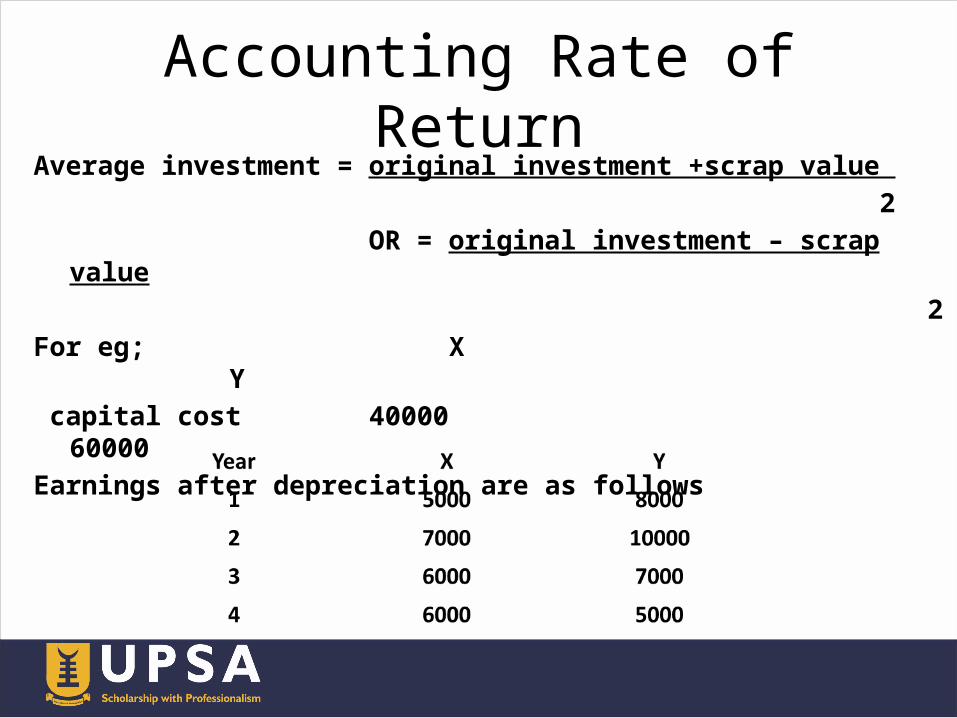

Accounting Rate of ReturnAverage investment = original investment +scrap value 2 OR = original investment – scrap value 2For eg; X Y capital cost 40000 60000Earnings after depreciation are as follows

Accounting Rate of ReturnThe average earnings of project X = 24000 = GH¢ 6000. 4 The average investment = cost at the beginning + cost at the end of the life. 2 40000+0 = GH¢ 20000. 2 ARR =6000 × 100 = 30 % 20000Average earnings of project y = 30000 4 = GH¢ 7500.Average investment = 60000+0 = GH¢ 30000. 2 ARR = 7500 × 100 = 25 % 30000

Accounting Rate of ReturnMerits• It is very simple to understand and use.• This method takes into account saving over the entire

economic life of the project. Therefore, it provides a better means of comparison of project than the pay back period.

• This method through the concept of "net earnings" ensures a compensation of expected profitability of the projects and

• It can readily be calculated by using the accounting data.

Accounting Rate of ReturnDemerits• 1. It ignores time value of money.• 2. It does not consider the length of life of the

projects.• 3. It is not consistent with the firm's objective

of maximizing the market value of shares.• 4. It ignores the fact that the profits earned

can be reinvested.

Payback PeriodIt refers to the period in which the project will generate

the necessary cash to recover the initial investment. It does not take the effect of time value of money. It emphasizes more on annual cash inflows, economic life

of the project and original investment. The selection of the project is based on the earning

capacity of a project. It involves simple calculation, selection or rejection of

the project can be made easily, results obtained is more reliable, best method for evaluating high risk projects.

Payback PeriodDecision criteria:

– The length of the maximum acceptable payback period is determined by management.

– If the payback period is less than the maximum acceptable payback period, accept the project.

– If the payback period is greater than the maximum acceptable payback period, reject the project.

Payback Period• For e.g- if a project requires GH¢20000 as initial

investment and it will generate an annual cash flow of GH¢5000 for ten years, the pay-back period will be 4 years, calculated as follows

• Pay –back period =

• The Annual cash flow is calculated on the basis of Net income before depreciation but after considering the tax. (PAT + Depreciation)

Initial investment Annual cash Flow

Payback Period

GH¢19000 is recovered in 3years and GH¢1000 is left out of initial investment. The cash inflow in 4th year is GH¢4000 which indicates that pay-back period is in between 3rd and 4th year.i.e.3+(1000/4000) = 3.25 years

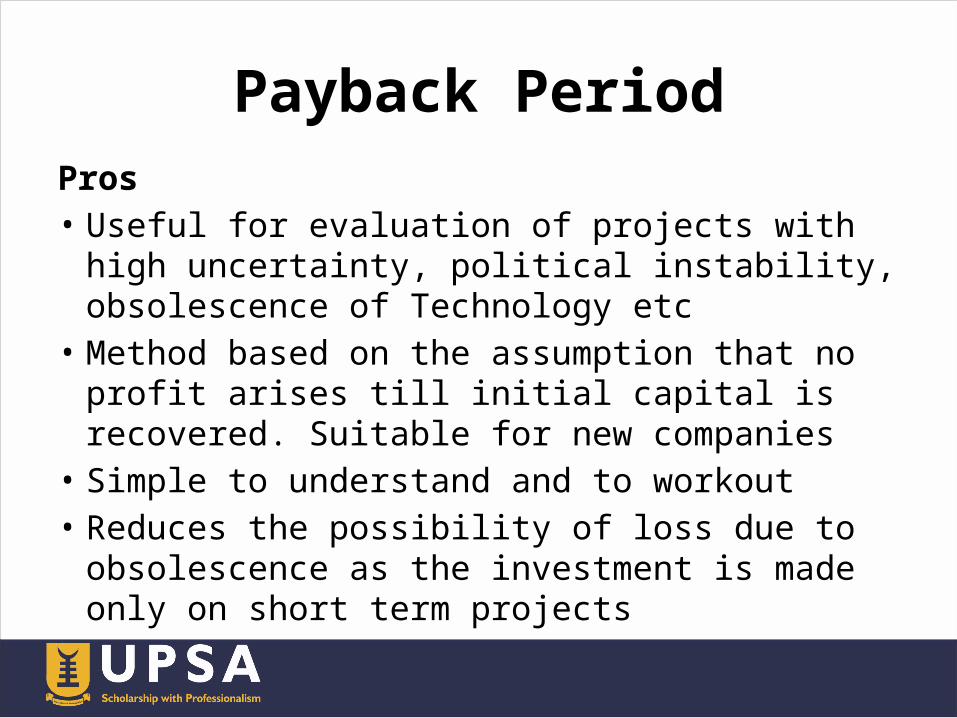

Payback PeriodPros• Useful for evaluation of projects with high uncertainty,

political instability, obsolescence of Technology etc• Method based on the assumption that no profit arises

till initial capital is recovered. Suitable for new companies

• Simple to understand and to workout• Reduces the possibility of loss due to obsolescence as

the investment is made only on short term projects

Discounted Payback Period• The discounted payback period is the number

of periods taken in recovering the investment outlay on the present value basis.

• The discounted payback period still fails to consider the cash flows occurring after the payback period.

3 DISCOUNTED PAYBACK ILLUSTRATED

Cash Flows

(Rs)

C0 C1 C2 C3 C4 Simple

PB Discounted

PB NPV at

10%

P -4,000 3,000 1,000 1,000 1,000 2 yrs – –

PV of cash flows -4,000 2,727 826 751 683 2.6 yrs 987

Q -4,000 0 4,000 1,000 2,000 2 yrs – –

PV of cash flows -4,000 0 3,304 751 1,366 2.9 yrs 1,421

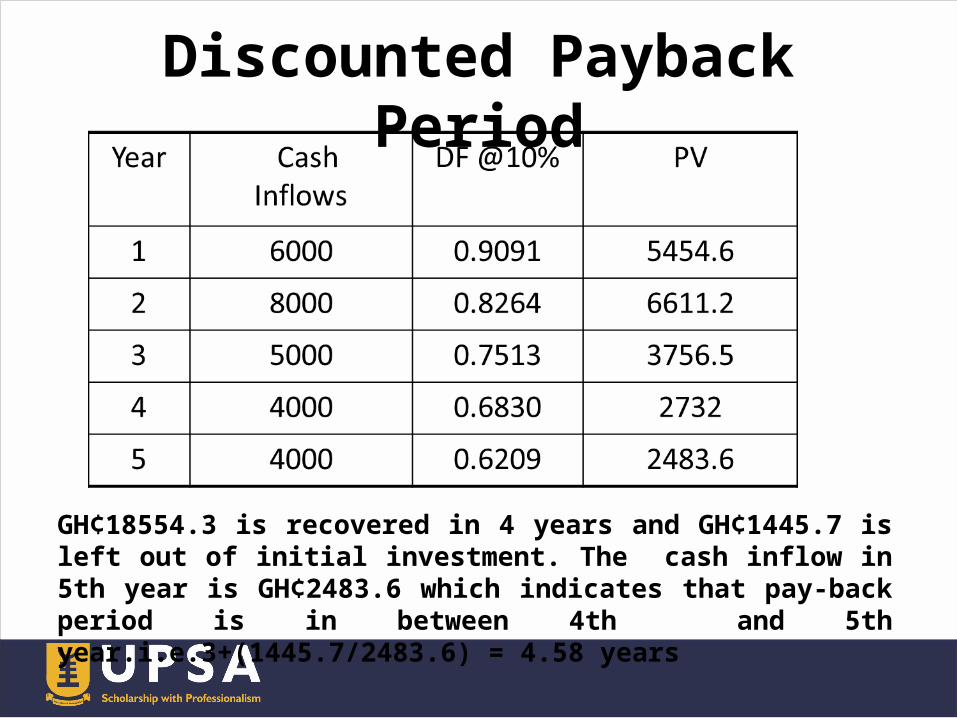

Discounted Payback PeriodExample 2:

Assuming the cost of capital for the firm is 10%. Calculate the discounted cash flows and the discounted payback period.

Discounted Payback Period

GH¢18554.3 is recovered in 4 years and GH¢1445.7 is left out of initial investment. The cash inflow in 5th year is GH¢2483.6 which indicates that pay-back period is in between 4th and 5th year.i.e.3+(1445.7/2483.6) = 4.58 years

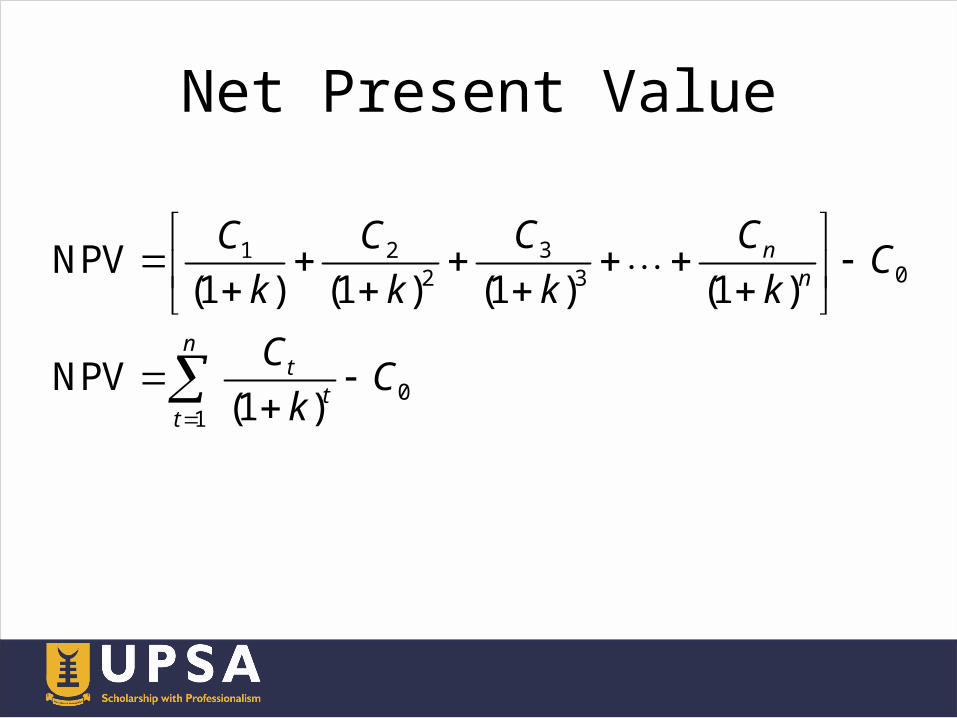

Net Present ValueNet present value (NPV) is a sophisticated

capital budgeting technique; found by subtracting a project’s initial investment from the present value of its cash inflows discounted at a rate equal to the firm’s cost of capital.

NPV = Present value of cash inflows – Initial investment

Net Present Value

31 202 3

01

NPV(1 ) (1 ) (1 ) (1 )

NPV(1 )

nn

nt

tt

C CC CC

k k k k

CC

k

Net Present ValueDecision criteria:

– If the NPV is greater than $0, accept the project.– If the NPV is less than $0, reject the project.

If the NPV is greater than $0, the firm will earn a return greater than its cost of capital. Such action should increase the market value of the firm, and therefore the wealth of its owners by an amount equal to the NPV.

Net Present Value• Cash flows of the investment project should

be forecasted based on realistic assumptions.• Appropriate discount rate should be identified

to discount the forecasted cash flows. The appropriate discount rate is the project’s opportunity cost of capital.

• Present value of cash flows should be calculated using the opportunity cost of capital as the discount rate.

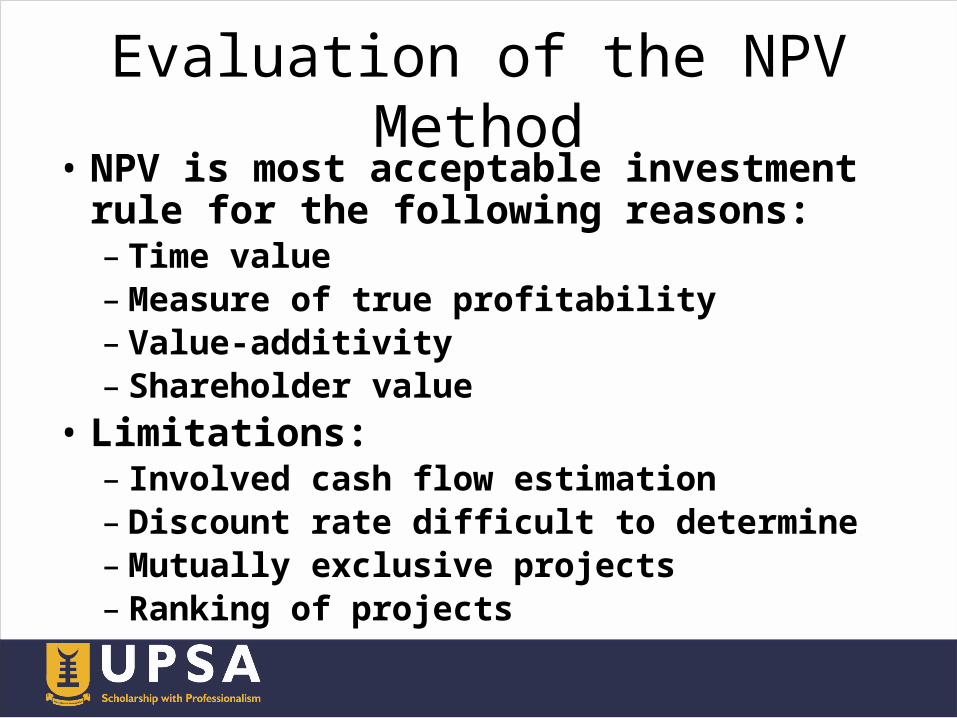

Evaluation of the NPV Method• NPV is most acceptable investment rule for the

following reasons:– Time value – Measure of true profitability – Value-additivity – Shareholder value

• Limitations:– Involved cash flow estimation – Discount rate difficult to determine– Mutually exclusive projects – Ranking of projects

Internal Rate of Return• The internal rate of return (IRR) is the rate that

equates the investment outlay with the present value of cash inflow received after one period. This also implies that the rate of return is the discount rate which makes NPV = 0.

31 20 2 3

01

01

(1 ) (1 ) (1 ) (1 )

(1 )

0(1 )

nn

nt

tt

nt

tt

C CC CC

r r r r

CC

r

CC

r

Calculation of IRR • Uneven Cash Flows: Calculating IRR by Trial

and Error– The approach is to select any discount rate to compute the

present value of cash inflows. If the calculated present value of the expected cash inflow is lower than the present value of cash outflows, a lower rate should be tried. On the other hand, a higher value should be tried if the present value of inflows is higher than the present value of outflows. This process will be repeated unless the net present value becomes zero.

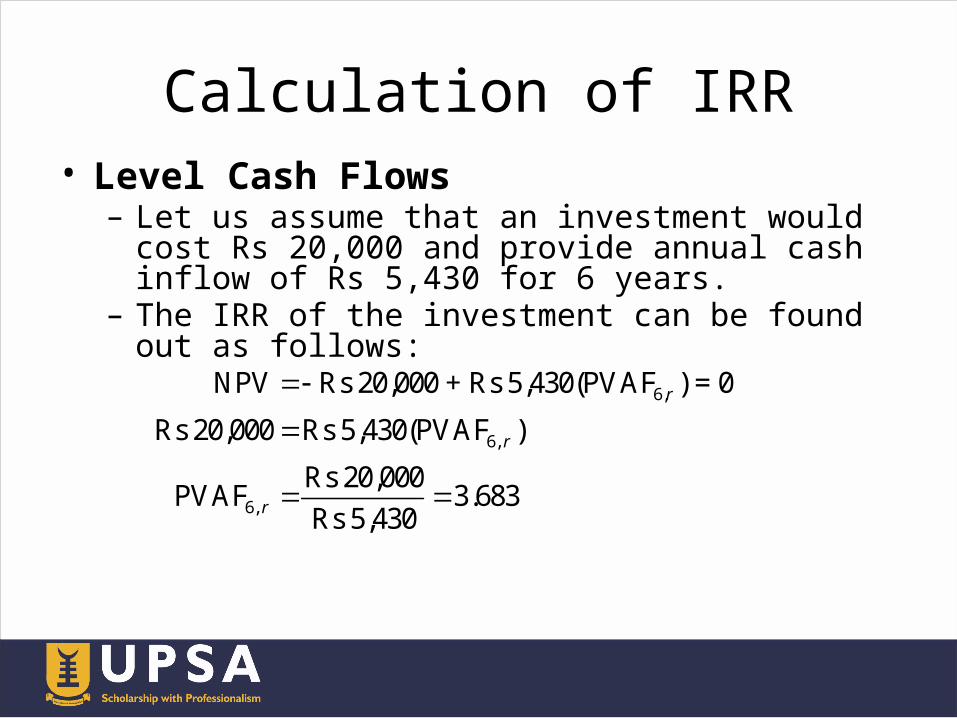

Calculation of IRR• Level Cash Flows

– Let us assume that an investment would cost Rs 20,000 and provide annual cash inflow of Rs 5,430 for 6 years.

– The IRR of the investment can be found out as follows:

6,

6,

6,

NPV Rs 20,000 + Rs 5,430(PVAF ) = 0

Rs 20,000 Rs 5,430(PVAF )

Rs 20,000PVAF 3.683

Rs 5,430

r

r

r

NPV Profile and IRR A B C D E F G H

1 NPV Profile

2 Cash Flow Discount

rate NPV 3 -20000 0% 12,580 4 5430 5% 7,561 5 5430 10% 3,649 6 5430 15% 550 7 5430 16% 0 8 5430 20% (1,942) 9 5430 25% (3,974)

Figure 8.1 NPV Profile

IRR

Calculation of IRR• You intended to invest in a project with the

following cash flows;

Calculation of IRR

Using a rate of return of 15%,• Calculate the NPV of the project• Calculate the IRR

Calculation of IRR

Calculation of IRR

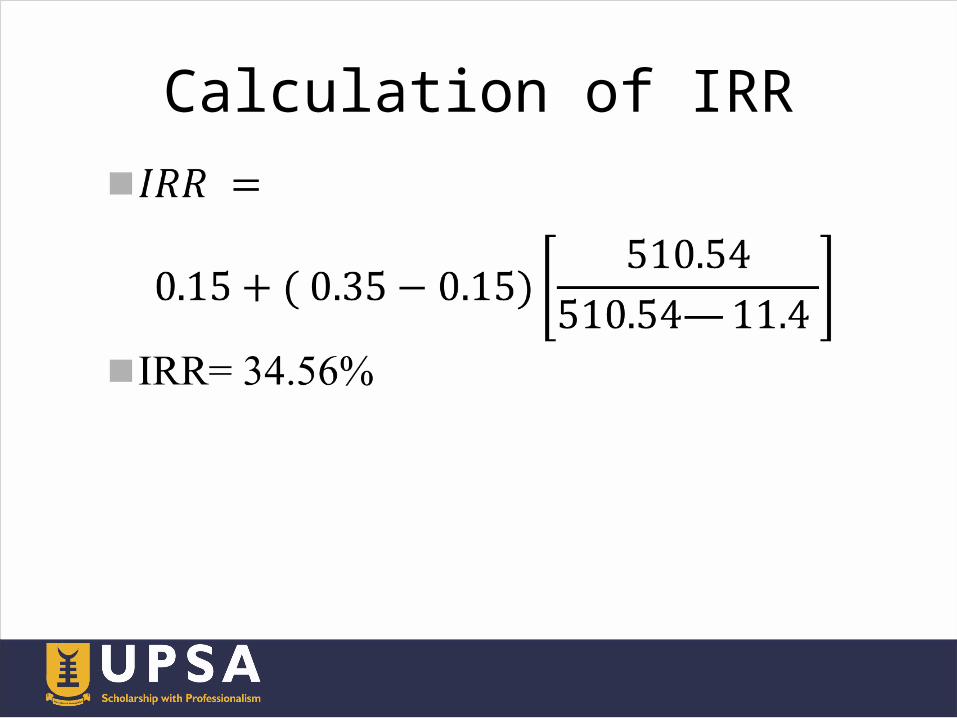

𝐼𝑅𝑅 = 𝑎 +( 𝑏−𝑎)ቂ 𝑁𝑃𝑉𝑎𝑁𝑃𝑉𝑎 −𝑁𝑃𝑉𝑏 ቃ

Calculation of IRR

Calculation of IRR

Calculation of IRR

Acceptance Rule• Accept the project when r < k.• Reject the project when r < k.• May accept the project when r = k.• In case of independent projects, IRR and NPV

rules will give the same results if the firm has no shortage of funds.

Evaluation of IRR• IRR method has following merits:

– Time value – Profitability measure – Acceptance rule – Shareholder value

• IRR method may suffer from:– Multiple rates – Mutually exclusive projects – Value additivity

Profitability Index• Profitability index is the ratio of the present

value of cash inflows, at the required rate of return, to the initial cash outflow of the investment.

Profitability Index• The initial cash outlay of a project is Rs

100,000 and it can generate cash inflow of Rs 40,000, Rs 30,000, Rs 50,000 and Rs 20,000 in year 1 through 4. Assume a 10 per cent rate of discount. The PV of cash inflows at 10 per cent discount rate is:

Acceptance Rule• The following are the PI acceptance rules:

– Accept the project when PI is greater than one. PI < 1– Reject the project when PI is less than one. PI < 1– May accept the project when PI is equal to one. PI = 1

• The project with positive NPV will have PI greater than one. PI less than means that the project’s NPV is negative.

Evaluation of PI Method• It recognises the time value of money. • It is consistent with the shareholder value

maximisation principle. A project with PI greater than one will have positive NPV and if accepted, it will increase shareholders’ wealth.

• In the PI method, since the present value of cash inflows is divided by the initial cash outflow, it is a relative measure of a project’s profitability.

• Like NPV method, PI criterion also requires calculation of cash flows and estimate of the discount rate. In practice, estimation of cash flows and discount rate pose problems.