Candax Energy Corporate Presentation

35

-

Upload

company-spotlight -

Category

Investor Relations

-

view

1.722 -

download

1

Transcript of Candax Energy Corporate Presentation

This presentation contains “forward looking statements” concerning

future operations of Candax Energy Inc. (“Candax” or the “Company”).

All forward looking statements concerning Candax’s future cash flow,

plans, operations, including management’s assessment of the

Company’s projects, expectations or beliefs may be subject to certain

assumptions, risks and uncertainties beyond the Company’s control.

Investors are cautioned that any such statements are not guarantees

of future performance and that actual performance and financial

results may differ materially from any estimates or projections

Sections

Corporate Overview – John Younger (President)

Operational Overview – Pascal Mirville (COO)

Financial Overview – Pierre-Henri Boutant (CFO)

Outlook for the Future – Benoit Debray (Chairman & CEO)

CORPORATE OVERVIEW

Vision and Mission Statements

The Team

Strong Management Team

Benoit Debray – Chairman & CEO

30-years experience in E&P and oil

services business

John Younger – President

20-years experience in finance

including the E&P sector

Pascal Mirville – COO

33-years experience in E&P and oil

services business, 15-yrs as manager

Dominique Didier – Technical

Director

30-years experience in E&P business

Pierre-Henri Boutant– CFO

15-years experience in E&P and oil

services business

Jamil Hamza – Operations Manager

27-years experience in oil business +

19 years with Candax assets

The Team

Experienced Board of Directors

M’hamed Ali Bouleymen – Dir.

Former Mayor of Tunis and former

Chairman and CEO of SITEP.

Steve Drinkwater – Director

35-years experience in E&P and oil

services business

Jean Pouzet – Director

25-years experience in geosciences

and technical aspects of E&P business

Thomas Rebilly– Director (not

shown) 20-years experience in E&P

and oil services business

Benoit Debray – Chairman & CEO

30-years experience in E&P and oil

services business

John Younger – President

20-years experience in finance

including the E&P sector

Key Major Shareholders

Geofinance: 64%

IFC: 17%

Actis: 5%

Ryder Scott Valuation

• According to Ryder Scott, Candax’s 2P Reserves of 3.76

million barrels on a present value basis (10%) are valued at

$119.49 million

• The valuation suggests a price per share of $0.095

• Please see the Appendix for details

IFC/Management Investment

• On February 24th, Candax announced that it had closed an equity

investment of 214.3 million units consisting of warrants and stock, priced

at $0.55

• The company realized gross proceeds of $11.97 million

• The subscribers to the offering were as follows:

– International Finance Corporation - 178 million Units ($9.79 million)

– Management/Directors – 36.36 million Units ($2 million) • Benoit Debray (Chairman & CEO) - $500,000

• John Younger (President) - $490,000

• Pascal Mirville (COO) - $400,000

• Pierre-Henri Boutant (CFO) - $250,000

• Dominique Didier (Technical Director) - $140,000

• Stephen Drinkwater (Director) - $100,000

• M’hamed Ali Bouleymen (Director) - $70,000

• Jamil Hamza (Operations Manager) - $50,000

The personal investment by management and directors is indicative of clear

commitment to the success of Candax

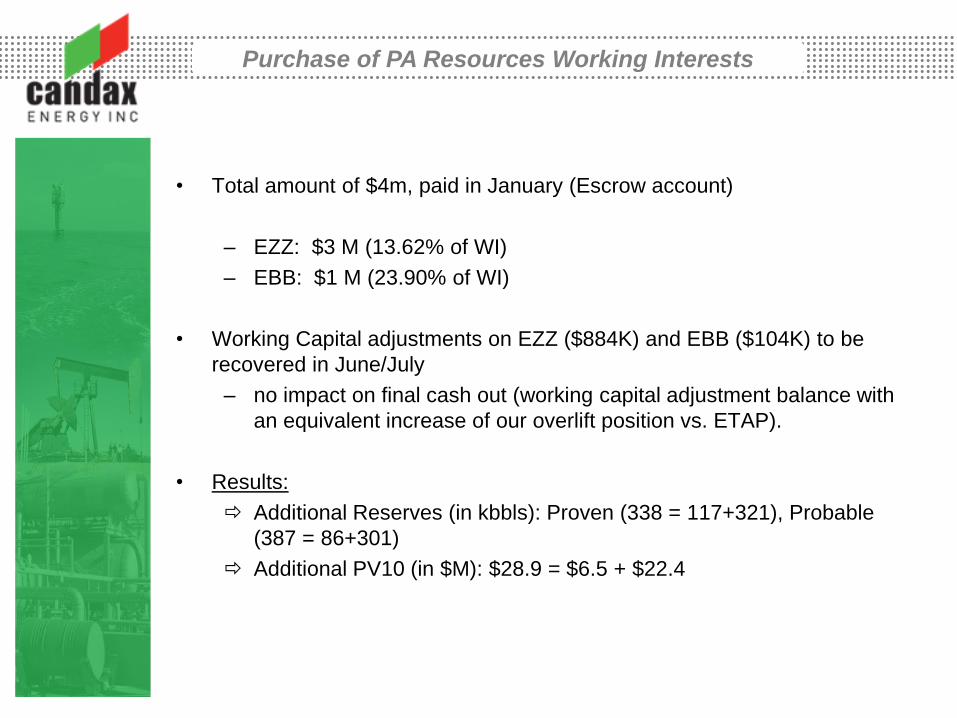

Purchase of PA Resources Working Interests

• Total amount of $4m, paid in January (Escrow account)

– EZZ: $3 M (13.62% of WI)

– EBB: $1 M (23.90% of WI)

• Working Capital adjustments on EZZ ($884K) and EBB ($104K) to be

recovered in June/July

– no impact on final cash out (working capital adjustment balance with

an equivalent increase of our overlift position vs. ETAP).

• Results:

Additional Reserves (in kbbls): Proven (338 = 117+321), Probable

(387 = 86+301)

Additional PV10 (in $M): $28.9 = $6.5 + $22.4

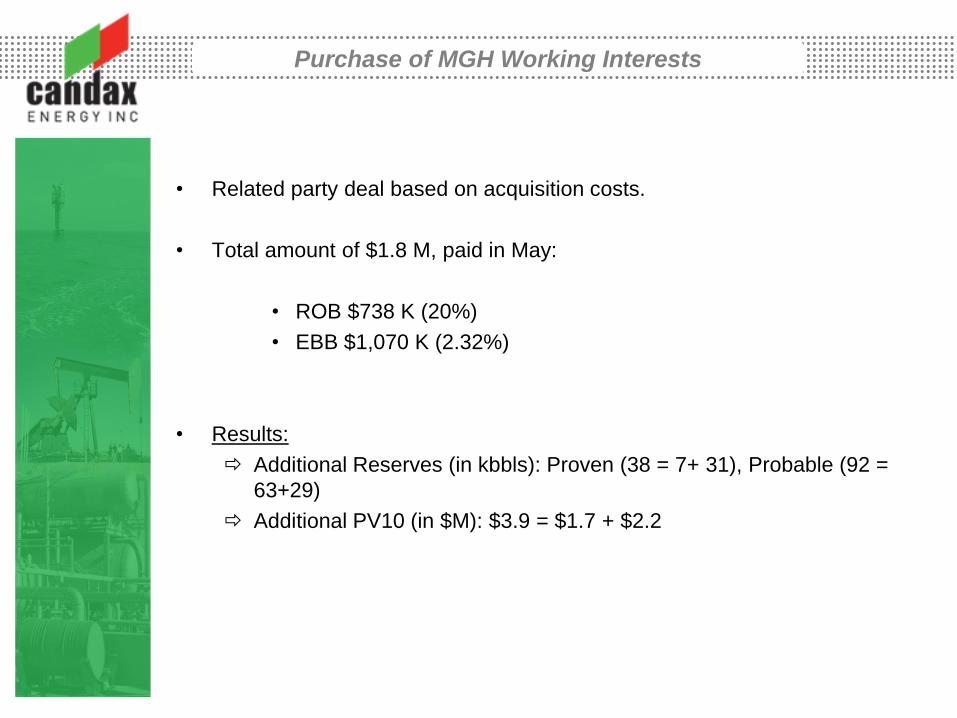

WI interests Consolidation

• Related party deal based on acquisition costs.

• Total amount of $1.8 M, paid in May:

• ROB $738 K (20%)

• EBB $1,070 K (2.32%)

• Results:

Additional Reserves (in kbbls): Proven (38 = 7+ 31), Probable (92 =

63+29)

Additional PV10 (in $M): $3.9 = $1.7 + $2.2

Purchase of MGH Working Interests

WI interests Consolidation

Cash Out = $5.8 M for $32.8 M of additional PV10 (Candax market value

currently at 53% of its PV10).

Improvement of MARETAP governance: 2 remaining partners on

Ezzaouia and Belli (ETAP & ECUMED)

Strong position on EBB and ROB (100%) for development

WI interests Consolidation

Concession Before After

Ezzaouia ETAP 55%

Candax 31.38%

PA Resources 13.62%

ETAP 55%

Candax 45%

Ezzaouia -

Deep Triassic

Dana Gas 50% back-in

right

ETAP 55%

Candax 45%

El Bibane Candax 73.78%

PA Resources 23.90%

Maghreb 2.32%

Candax 100%

El Bibane- Deep

Triassic

Dana Gas 50% back-in

right

Candax 100%

Robbana Candax 80.00%

Maghreb 20.00%

Candax 100%

• The streamlining of our ownership interests will allow us to develop the fields

according to our vision of the potential of the fields and allow us to bring in

partners who share that vision

OPERATIONAL OVERVIEW

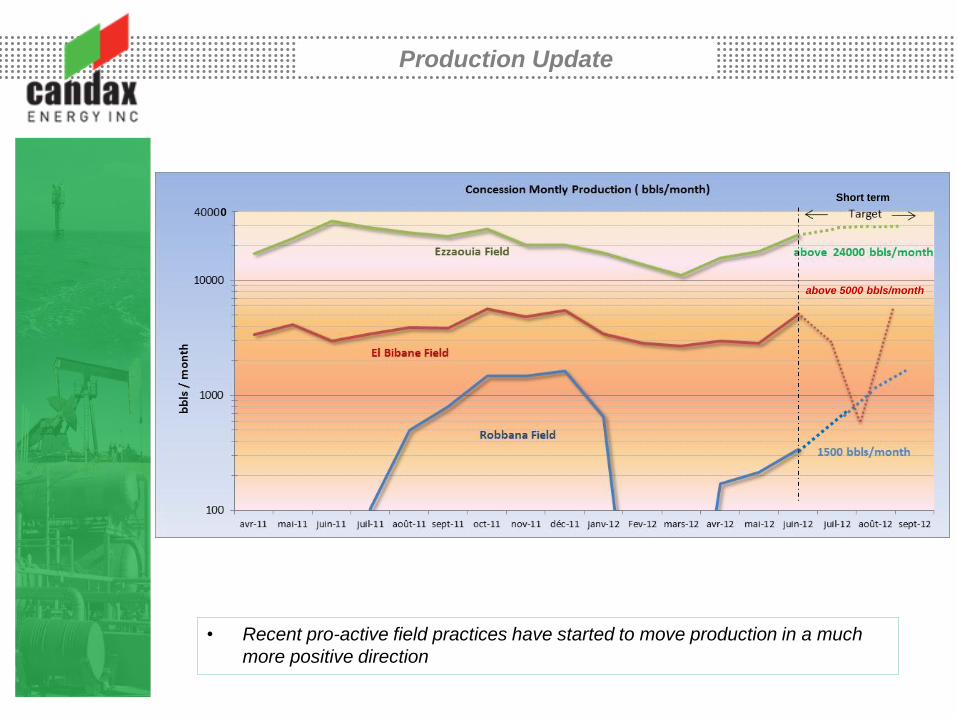

Production Update

• Recent pro-active field practices have started to move production in a much

more positive direction

above 5000 bbls/month

Short term

0

Update on Ezzaouia

• On going intervention on most of wells for tubing and jet

pump cleaning induced a very low current production (below

200 bopd) for most of Q1.

• EZZ-18 WO started in April. BHA retrieved beginning of May

showing cement obstruction. WO duration: 6 weeks. Back in

production on May 24th with jet pump re-installed. WO cost =

1.5 MM$

• EZZ 17 and EZZ 9 scale inhibitor injection pump connection

completed mid may.

• EZZ 2 ST WO currently ongoing . Expected back in

Production by beginning of July.

• Slickline operations ongoing on EZZ11 (perforation) and

EZZ1 (fishing)

Objective: to bring back a « decent »

production (ie above 700 bopd)

• Today and without the EBB2 W/O completed, the average daily prod is

around 670 bopd.

• Knowing that the previous production of EZZ-2 was above 200 bopd, we are

confident to reach a production level above 800 bopd.

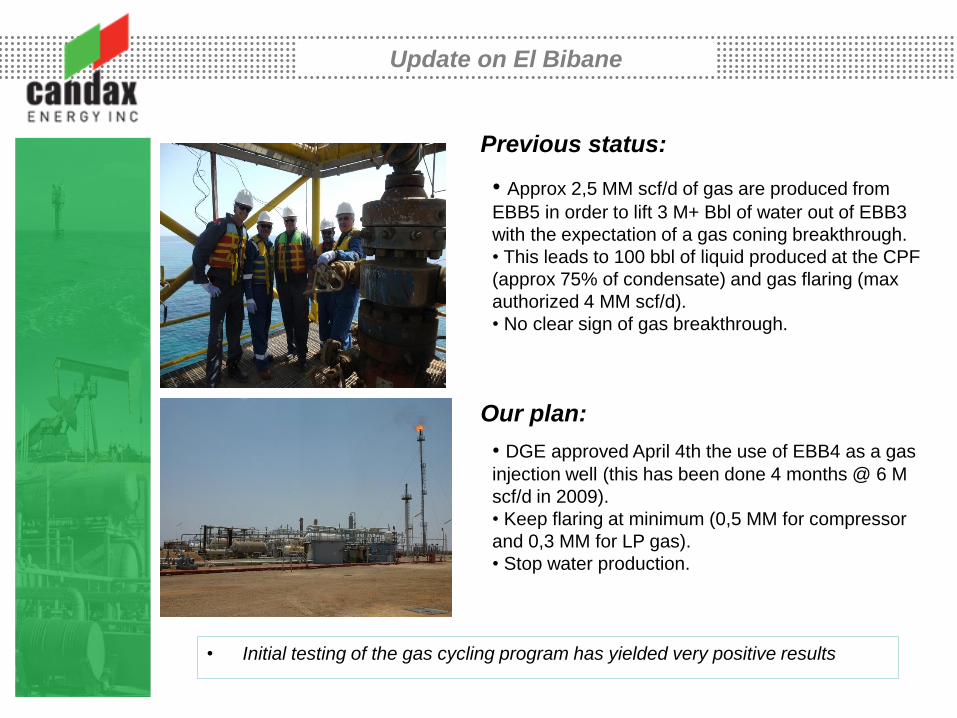

• Approx 2,5 MM scf/d of gas are produced from

EBB5 in order to lift 3 M+ Bbl of water out of EBB3

with the expectation of a gas coning breakthrough.

• This leads to 100 bbl of liquid produced at the CPF

(approx 75% of condensate) and gas flaring (max

authorized 4 MM scf/d).

• No clear sign of gas breakthrough.

Previous status:

Our plan:

• DGE approved April 4th the use of EBB4 as a gas

injection well (this has been done 4 months @ 6 M

scf/d in 2009).

• Keep flaring at minimum (0,5 MM for compressor

and 0,3 MM for LP gas).

• Stop water production.

Update on El Bibane

• Initial testing of the gas cycling program has yielded very positive results

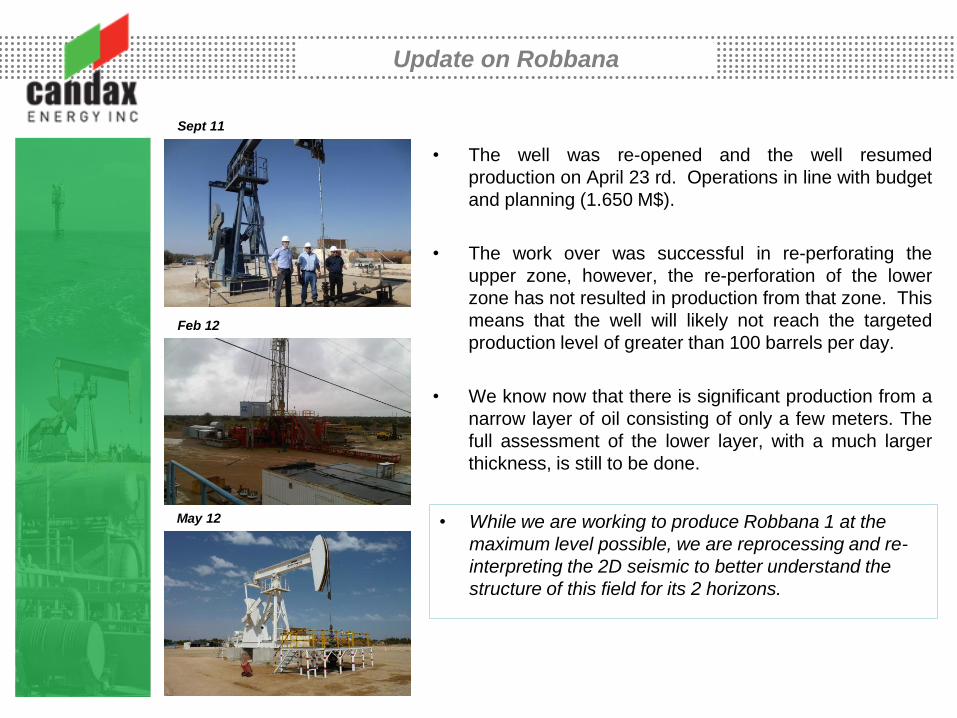

• The well was re-opened and the well resumed

production on April 23 rd. Operations in line with budget

and planning (1.650 M$).

• The work over was successful in re-perforating the

upper zone, however, the re-perforation of the lower

zone has not resulted in production from that zone. This

means that the well will likely not reach the targeted

production level of greater than 100 barrels per day.

• We know now that there is significant production from a

narrow layer of oil consisting of only a few meters. The

full assessment of the lower layer, with a much larger

thickness, is still to be done.

Update on Robbana

Sept 11

Feb 12

May 12 • While we are working to produce Robbana 1 at the

maximum level possible, we are reprocessing and re-

interpreting the 2D seismic to better understand the

structure of this field for its 2 horizons.

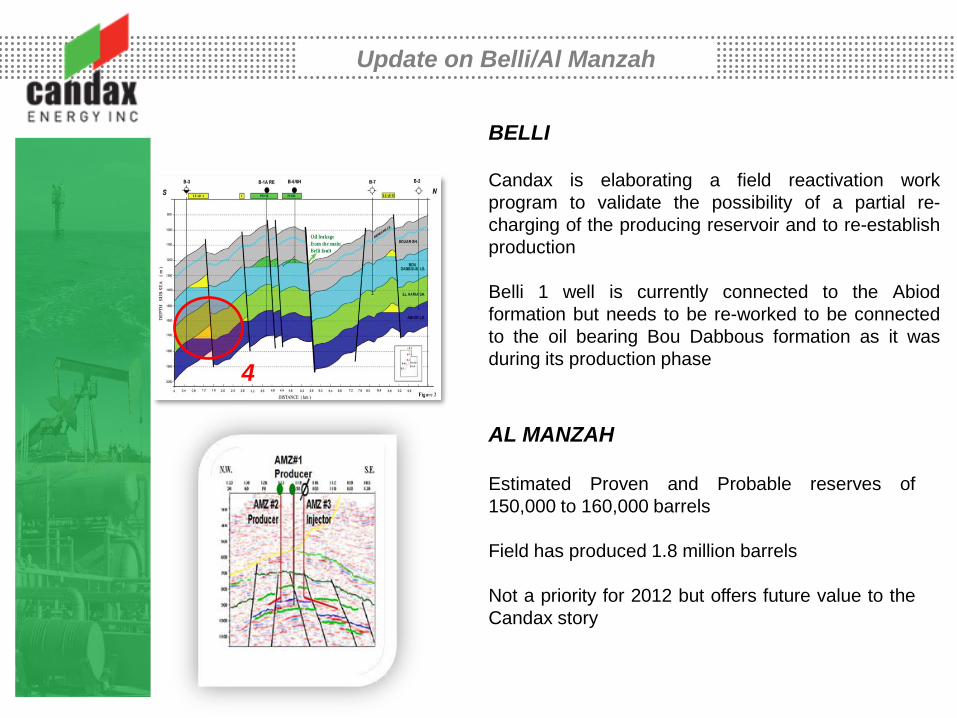

Update on Belli/Al Manzah

4

BELLI

Candax is elaborating a field reactivation work

program to validate the possibility of a partial re-

charging of the producing reservoir and to re-establish

production

Belli 1 well is currently connected to the Abiod

formation but needs to be re-worked to be connected

to the oil bearing Bou Dabbous formation as it was

during its production phase

AL MANZAH

Estimated Proven and Probable reserves of

150,000 to 160,000 barrels

Field has produced 1.8 million barrels

Not a priority for 2012 but offers future value to the

Candax story

Update on Deep Triassic

Multi TCF gas prospect in both the El Bibane

and the Ezzaouia concessions

Original targets of 1980 prospection

Geosciences focus for 2012

Update on Madagascar

Billion barrel potential analogous to fields in region

Operator is Afren with 90% working interest

First Drilling expected to take place in early 2013

FINANCIAL OVERVIEW

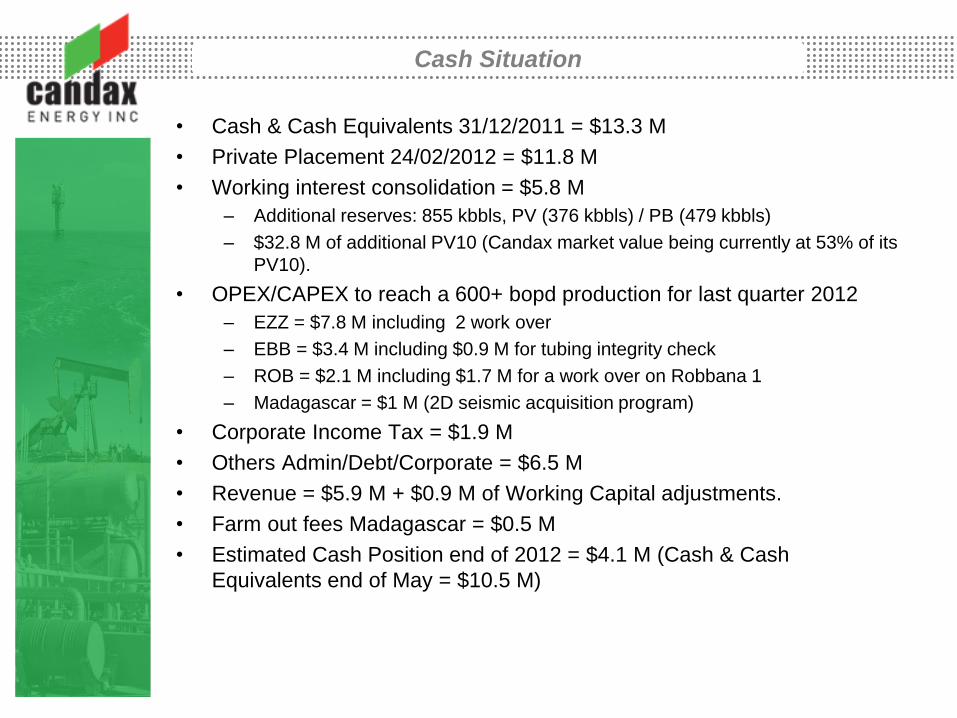

Cash Situation

• Cash & Cash Equivalents 31/12/2011 = $13.3 M

• Private Placement 24/02/2012 = $11.8 M

• Working interest consolidation = $5.8 M

– Additional reserves: 855 kbbls, PV (376 kbbls) / PB (479 kbbls)

– $32.8 M of additional PV10 (Candax market value being currently at 53% of its

PV10).

• OPEX/CAPEX to reach a 600+ bopd production for last quarter 2012

– EZZ = $7.8 M including 2 work over

– EBB = $3.4 M including $0.9 M for tubing integrity check

– ROB = $2.1 M including $1.7 M for a work over on Robbana 1

– Madagascar = $1 M (2D seismic acquisition program)

• Corporate Income Tax = $1.9 M

• Others Admin/Debt/Corporate = $6.5 M

• Revenue = $5.9 M + $0.9 M of Working Capital adjustments.

• Farm out fees Madagascar = $0.5 M

• Estimated Cash Position end of 2012 = $4.1 M (Cash & Cash

Equivalents end of May = $10.5 M)

Forecast Production

• EBB production trending up at over 120 bopd net in June 2012 (Pilot

phase of gas cycling).

• EZZ production trending up at over 294 bopd net in June 2012 with 2

wells to be restarted.

• Conservative approach on 2013 FCST:

• Only include additional production of one Side Track on Ezzaouia.

• Decline rate on the Jurassic considered at 1.8%/month.

• No production on Belli

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2012 2012 2012 2013 2013 2013 2013

Actual Forecast Forecast Forecast Forecast Forecast Forecast Forecast

El Bibane 91 106 81 139 153 170 175 175

Ezzaouia 165 234 432 417 403 474 453 432

Robbana 7 7 29 58 65 75 75 75

Belli

263 347 542 615 622 719 703 682

Average daily net Oil Production

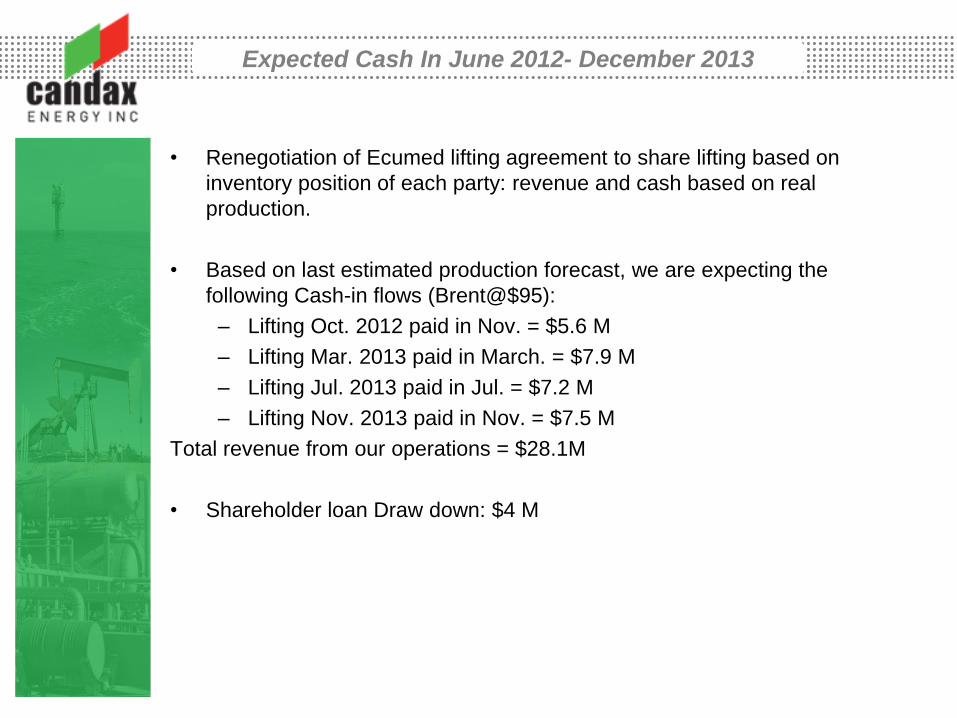

Expected Cash In June 2012- December 2013

• Renegotiation of Ecumed lifting agreement to share lifting based on

inventory position of each party: revenue and cash based on real

production.

• Based on last estimated production forecast, we are expecting the

following Cash-in flows (Brent@$95):

– Lifting Oct. 2012 paid in Nov. = $5.6 M

– Lifting Mar. 2013 paid in March. = $7.9 M

– Lifting Jul. 2013 paid in Jul. = $7.2 M

– Lifting Nov. 2013 paid in Nov. = $7.5 M

Total revenue from our operations = $28.1M

• Shareholder loan Draw down: $4 M

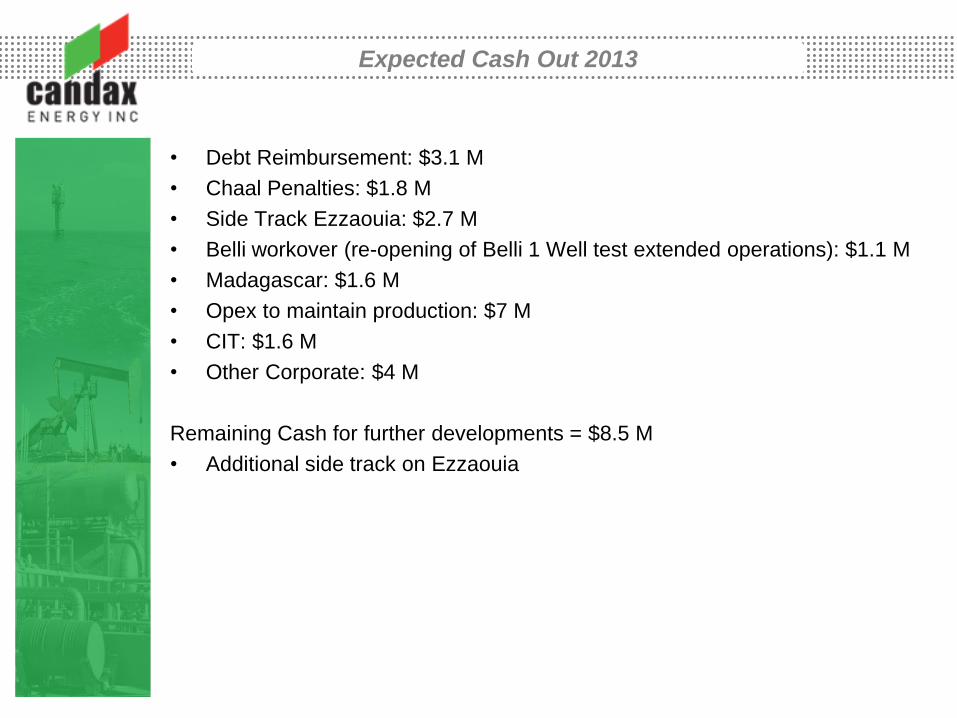

Expected Cash Out 2013

• Debt Reimbursement: $3.1 M

• Chaal Penalties: $1.8 M

• Side Track Ezzaouia: $2.7 M

• Belli workover (re-opening of Belli 1 Well test extended operations): $1.1 M

• Madagascar: $1.6 M

• Opex to maintain production: $7 M

• CIT: $1.6 M

• Other Corporate: $4 M

Remaining Cash for further developments = $8.5 M

• Additional side track on Ezzaouia

Cost Control Initiatives

• Accounting personnel consolidation in Tunis

• Change in Corporate Secretary

• Pending change in Toronto office location

• Closure of Madagascar office

• Closure of Geneva office

• Pre-approval process for legal fees

• Focus on investing on operations and saving on overhead

OUTLOOK FOR THE

FUTURE

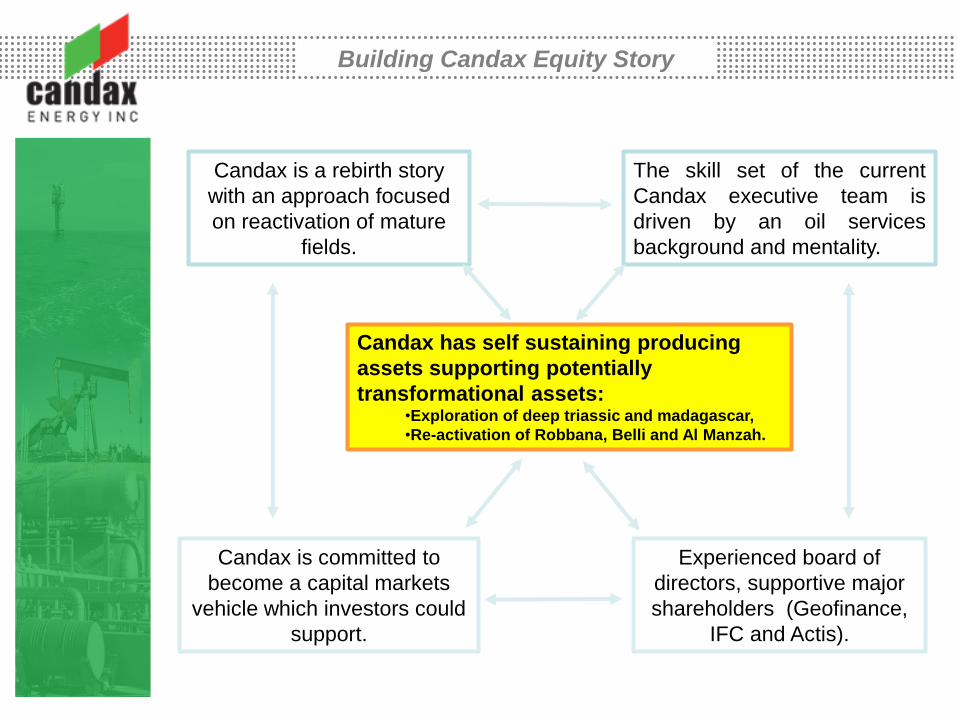

Building Candax Equity Story

Candax is a rebirth story

with an approach focused

on reactivation of mature

fields.

The skill set of the current

Candax executive team is

driven by an oil services

background and mentality.

Candax has self sustaining producing

assets supporting potentially

transformational assets: •Exploration of deep triassic and madagascar,

•Re-activation of Robbana, Belli and Al Manzah.

Candax is committed to

become a capital markets

vehicle which investors could

support.

Experienced board of

directors, supportive major

shareholders (Geofinance,

IFC and Actis).

Where we are

0

100

200

300

400

500

600

700

Bo

ep

d

Total Net CAX Prod. (boepd)

BUD

REV1

ACT

FCST

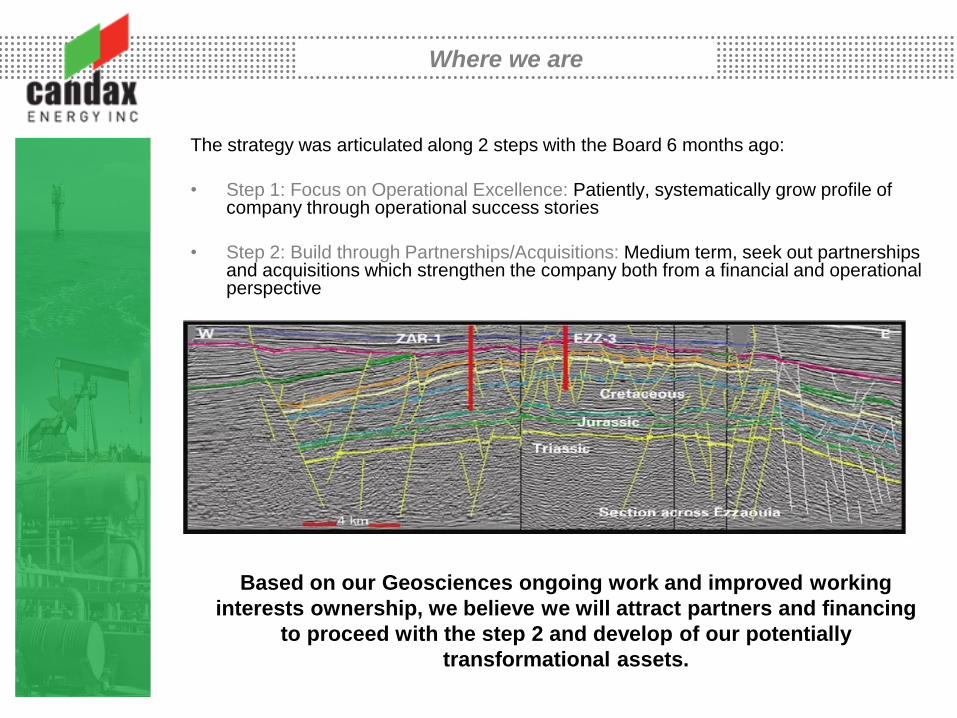

The strategy was articulated along 2 steps with the Board 6 months ago:

• Step 1: Focus on Operational Excellence: Patiently, systematically grow profile of company through operational success stories

• Step 2: Build through Partnerships/Acquisitions: Medium term, seek out partnerships and acquisitions which strengthen the company both from a financial and operational perspective

Based on Current Working Program, Candax is achieving the first step of

its strategy: self sustaining producing assets support Company long

term activity.

Where we are

The strategy was articulated along 2 steps with the Board 6 months ago:

• Step 1: Focus on Operational Excellence: Patiently, systematically grow profile of company through operational success stories

• Step 2: Build through Partnerships/Acquisitions: Medium term, seek out partnerships and acquisitions which strengthen the company both from a financial and operational perspective

Based on our Geosciences ongoing work and improved working

interests ownership, we believe we will attract partners and financing

to proceed with the step 2 and develop of our potentially

transformational assets.

APPENDIX

Reserves 2011 (as per RS 2011 report)

(A)

Status Gross WI Net Gross WI Net Gross WI Net

El Bibane Concession, Tunisia 73,77% 97,68% +23,9%

PV 1 265 933 898 1 400 1 367 1 314 135 434 416

PB 1 539 1 135 1 056 1 364 1 332 1 228 (175) 197 173

T2P 2 804 2 069 1 953 2 764 2 700 2 542 (40) 631 589

Ezzaouia Concession, Tunisia 31,38% 88,00% 45,00% 1 +13,62% 88,00%

PV 1 022 321 282 977 440 387 (45) 119 105

PB 2 620 822 724 721 324 285 (1 899) (498) (438)

T2P 3 642 1 143 1 006 1 698 764 672 (1 944) (379) (334)

Robbana Concession, Tunisia 80,00% 80,00% =

PV 44 35 34 35 28 27 (9) (7) (7)

PB 326 261 245 338 270 254 12 9 9

T2P 370 296 279 373 298 281 3 2 2

CANDAX ENERGY INC. - GRAND SUMMARY

PV 2 331 1 289 1 214 2 412 1 835 1 728 81 546 514

PB 4 485 2 218 2 024 2 422 1 927 1 768 (2 062) (291) (257)

T2P 6 816 3 508 3 238 4 835 3 762 3 495 (1 982) 254 257

Oil (MBbl) Oil (MBbl) Oil (MBbl)

2010 2011 VAR 2011-2010

NPV of future Net Reserves

NP

V A

fter

Inco

me T

ax

N

PV

Befo

re In

co

me T

ax

EPZ CML

(US$ in mllion) El Bibane Robbana Ezzaouia Al Manzah Belli Madagascar Total 2011 Ref. 2010 Ref. 2009

P1 (proved)

PV Undiscounted 24.9 0.7 13.3 - - - 38.9 32.5 62.3

PV @ 5% discount rate 21.2 0.7 12.7 - - - 34.7 25.2 55.7

PV @ 10% discount rate 17.4 0.8 12.1 - - - 30.3 19.1 50.0

PV @ 15% discount rate 13.6 0.8 11.5 - - - 26.0 14.4 45.1

PV @ 20% discount rate 10.1 0.8 10.9 - - - 21.9 10.3 40.8

P2 (probable)

PV Undiscounted 104.8 11.1 12.4 - - - 128.3 144.4 154.9

PV @ 5% discount rate 88.0 8.1 10.7 - - - 106.8 109.0 124.3

PV @ 10% discount rate 74.1 5.9 9.2 - - - 89.2 83.6 102.6

PV @ 15% discount rate 62.7 4.3 7.8 - - - 74.8 65.2 86.5

PV @ 20% discount rate 53.5 3.0 6.6 - - - 63.1 51.7 74.2

P1 + P2

PV Undiscounted 129.8 11.8 25.7 - - - 167.2 176.9 217.2

PV @ 5% discount rate 109.2 8.9 23.5 - - - 141.5 134.2 180.0

PV @ 10% discount rate 91.5 6.7 21.3 - - - 119.5 102.8 152.6

PV @ 15% discount rate 76.3 5.1 19.3 - - - 100.8 79.7 131.6

PV @ 20% discount rate 63.6 3.8 17.6 - - - 85.0 61.9 115.0

EPT EPG

EPZ CML

(US$ in mllion) El Bibane Robbana Ezzaouia Al Manzah Belli Madagascar Total 2011 Ref. 2010 Ref. 2009

P1 (proved)

PV Undiscounted 23.4 0.6 10.1 - - - 34.1 29.6 55.9

PV @ 5% discount rate 19.9 0.7 9.7 - - - 30.3 22.5 50.1

PV @ 10% discount rate 16.2 0.8 9.2 - - - 26.2 16.8 45.0

PV @ 15% discount rate 12.6 0.8 8.7 - - - 22.1 14.8 40.6

PV @ 20% discount rate 9.2 0.8 8.2 - - - 18.3 8.3 36.8

P2 (probable)

PV Undiscounted 94.9 10.8 10.6 - - - 116.3 126.9 130.3

PV @ 5% discount rate 80.9 7.9 9.1 - - - 97.8 96.5 105.9

PV @ 10% discount rate 68.9 5.7 7.6 - - - 82.3 74.6 87.3

PV @ 15% discount rate 59.0 4.1 6.4 - - - 69.5 67.6 73.5

PV @ 20% discount rate 50.7 2.9 5.3 - - - 58.9 46.4 63.5

P1 + P2

PV Undiscounted 118.3 11.4 20.6 - - - 150.4 156.5 186.2

PV @ 5% discount rate 100.8 8.6 18.8 - - - 128.2 119.0 156.0

PV @ 10% discount rate 85.2 6.5 16.9 - - - 108.5 91.4 132.3

PV @ 15% discount rate 71.6 4.9 15.1 - - - 91.6 82.4 114.1

PV @ 20% discount rate 59.9 3.7 13.6 - - - 77.2 54.8 100.3

EPT EPG