Cancellation of Indebtedness Income for Pass-Through...

72

Cancellation of Indebtedness Income for Pass-Through Entities Navigating Complex Tax, Exclusion and Deferral Issues Arising in Forms 1099-C and 982 WEDNESDAY, MARCH 13, 2013, 1:00-2:50 pm Eastern WHOM TO CONTACT For Additional Registrations: -Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10) For Assistance During the Program: - On the web, use the chat box at the bottom left of the screen - On the phone, press *0 (“star” zero) If you get disconnected during the program, you can simply call or log in using your original instructions and PIN. IMPORTANT INFORMATION • Participate in the program on your own computer connection or phone line (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa, MasterCard, Discover. • Respond to verification codes presented throughout the seminar. If you have not printed out the “Official Record of Attendance”, please print it now. (see “Handouts” tab in “Conference Materials” box on left-hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form. • Complete and submit the “Official Record of Attendance for Continuing Education Credits” included with the presentation materials. That record must include your PTIN ID #. Instructions on how to return it are included on the form. • To earn full credit, you must remain on the line for the entire program.

Transcript of Cancellation of Indebtedness Income for Pass-Through...

Cancellation of Indebtedness Income for Pass-Through Entities Navigating Complex Tax, Exclusion and Deferral Issues Arising in Forms 1099-C and 982

WEDNESDAY, MARCH 13, 2013, 1:00-2:50 pm Eastern

WHOM TO CONTACT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Program:

- On the web, use the chat box at the bottom left of the screen

- On the phone, press *0 (“star” zero)

If you get disconnected during the program, you can simply call or log in using your original instructions and PIN.

IMPORTANT INFORMATION

• Participate in the program on your own computer connection or phone line (no sharing) – if you need to register additional

people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa,

MasterCard, Discover.

• Respond to verification codes presented throughout the seminar. If you have not printed out the “Official Record of

Attendance”, please print it now. (see “Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found

on the Official Record of Attendance form.

• Complete and submit the “Official Record of Attendance for Continuing Education Credits” included with the presentation

materials. That record must include your PTIN ID #. Instructions on how to return it are included on the form.

• To earn full credit, you must remain on the line for the entire program.

Sound Quality

For best sound quality, we recommend you listen via the telephone by dialing

1-866-873-1442 and entering your PIN when prompted, and viewing the presentation slides

online. However, attendees also can opt to listen online if you choose.

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] so we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

If you have not printed or downloaded the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column

on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the

slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

I. TRANSACTIONS CREATING CODI

By Robert S. Barnett CPA, JD, MS (TAXATION)

CAPELL BARNETT MATALON & SCHOENFELD, LLP.

ATTORNEYS AT LAW

(516) 931-8100

INTRODUCTION – PLANNING APPROACH

• Get the facts!

• Entity considerations

• Some elections are made at entity level

• Loss utilization history

• Review balance sheet & projections

• NOL + PAL credit carryforwards

• Solvency of debtor

5

CANCELLATION OF DEBT

• IRC §61(a)(12)

– Except as otherwise provided in this subtitle, gross income means all income from whatever source derived, including (but not limited to) income from discharge of indebtedness

6

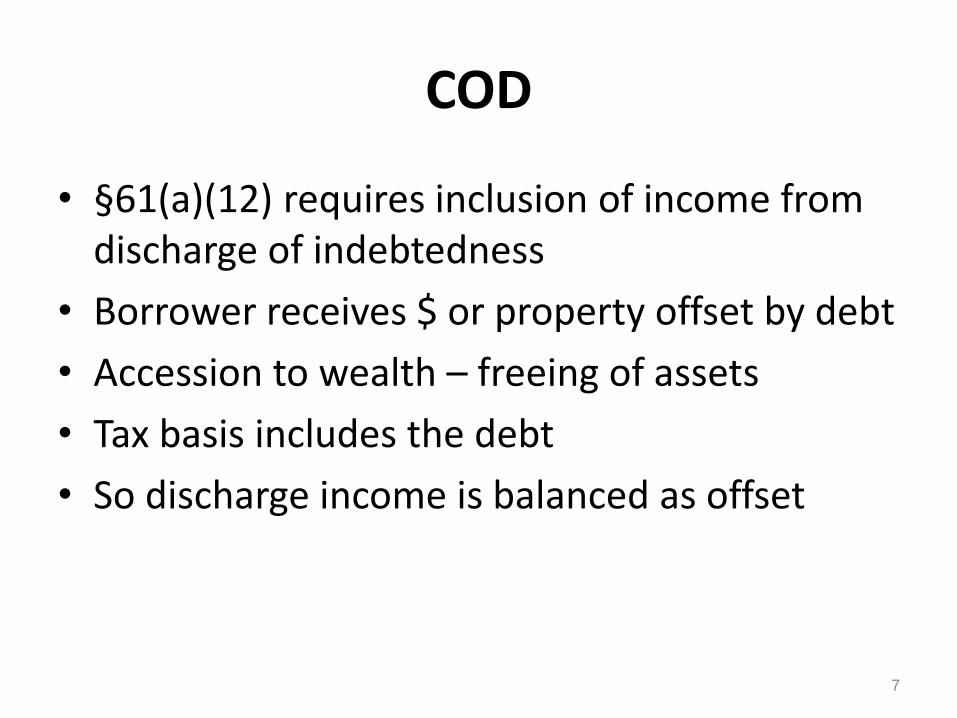

COD

• §61(a)(12) requires inclusion of income from discharge of indebtedness

• Borrower receives $ or property offset by debt

• Accession to wealth – freeing of assets

• Tax basis includes the debt

• So discharge income is balanced as offset

7

EXCEPTIONS – ADJUSTMENTS

• §108 contains numerous exceptions

• §1017 requires certain basis adjustments

• Tax attributes ex. NOL’s are reduced

• CODI does not include debt that would have given rise to a deduction if paid (ex. A/P of Cash Taxpayers §108(e)(2) interest)

8

DEBT

• Income tax effects differ

• RECOURSE vs NONRECOURSE

• Guaranty

9

GUARANTY

• X guarantees $1,000,000 loan to her corp

• Corp renegotiates loan with bank

• Debt reduced to $750,000

• Does X have COD income?

10

ANSWER

• NO

• Mere guarantee is not sufficient

• Merkel v. Comm., 109 T.C. 463 (1997) aff’d, 192 F.3d 844 (9th Cir. 1999)

• Corp should receive 1099C

• Corp is primary obligor

• Debt restructured “freed corporate assets”

11

TRANSACTIONS CREATING CODI

1. Debt Discharge – paying less than full debt CODI = Debt Amount > Cash Payment

2. Significant Modification of Debt: CODI = Principal Amount Old Debt > Principal Amount New Debt

3. Exchange of debt instruments CODI = Issue Price of OLD Debt > Issue Price of NEW Debt (using OID rules)

12

TRANSACTIONS continued

4. Repurchase

5. Forclosure / Short Sale

6. Debt / Equity Exchanges – may be a deemed exchange if modification.

7. Not disputed amount

13

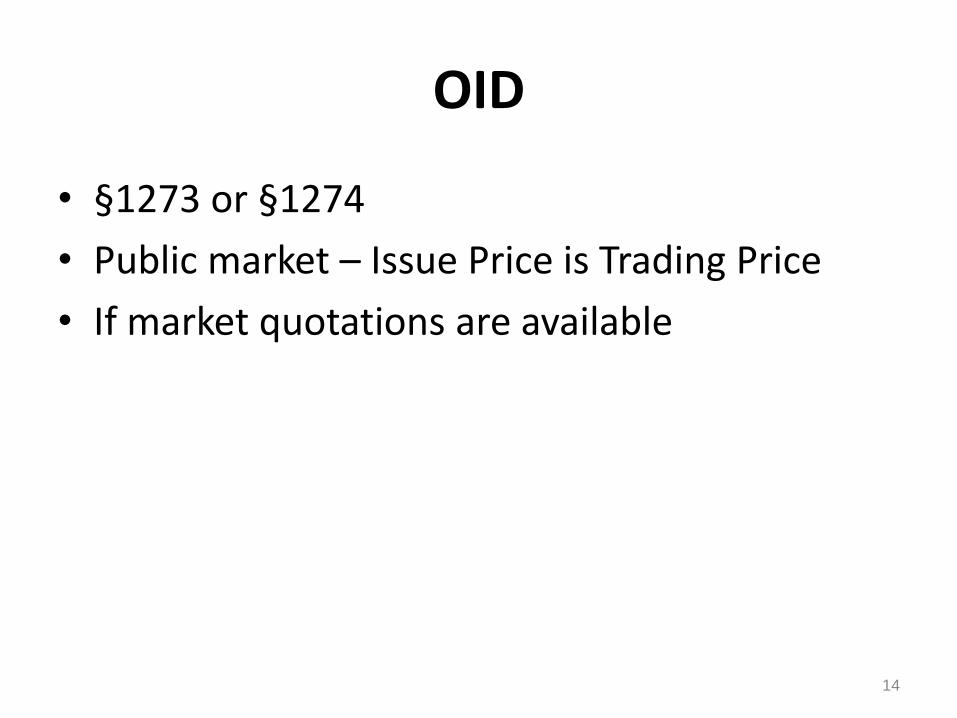

OID

• §1273 or §1274

• Public market – Issue Price is Trading Price

• If market quotations are available

14

CODI

• Generally the difference between the balance of the indebtedness and the amount of consideration accepted by the lender.

• Income is realized at the time the debt is satisfied.

• Solvent taxpayers generally report ordinary income on canceled or reduced debt.

15

Slide Intentionally Left Blank

McCORMICK, TC Memo 2009-39

• What is correct amount of CODI?

• The McCormick family received a 1099 C from Citi Financial – Contest of Amount

• IRC §6201(d) - In any court proceeding:

– Taxpayer asserts reasonable dispute

– To income reported on an information return

– Taxpayer fully cooperated

THEN… 17

BURDEN OF PROOF SHIFTS

• To IRS

• Correct CODI was $49.66

• IRS could not rely on 1099C

• CCA 201112008 – borrowers received payments in settlement of unfair lending dispute. Viewed as equitable reformation

• Timing Gaffney, TC Summary 2010-128.

18

EXAMPLE 1

• Debtor transfers property in a voluntary foreclosure

• Of RECOURSE DEBT

• RECOURSE DEBT - Debt for which a borrower is personally liable. Whether a debt is recourse or nonrecourse may vary from state to state, depending on state law.

19

EXAMPLE 1 CONTINUED

• 1099C reports – Debt cancelled in BOX 2 $465,000 Box 7 – FMV $195,000

• Box 3 should report accrued but unpaid interest.

• Request computations from lender 20

EXAMPLE 1 CONTINUED

• Recourse debt is bifurcated:

• Amount of Debt Cancelled= $465,000

• Fair Market Value= - $195,000

• CODI: $270,000

OR IS IT?

21

CODI

• §108(e)(2)

–Should NOT include amounts which would give rise to a tax deduction if paid

• How was FMV determined?

22

GAIN/LOSS

• Taxpayer’s gain or loss is measured by the difference between the amount realized and the adjusted basis of the property.

23

EXAMPLE - RENTAL

• RENTAL PROPERTY

• Purchase Price = $500,000

• Adjusted Basis = $400,000

• IRC § 1231 Loss = $205,000

(400,000 – 195,000)

24

NON RECOURSE DEBT

• Transfer of property: Tufts v. Commissioner

• Amount realized= $465,000

• Basis= - $400,000

• Capital Gain= $65,000

• Non Recourse debt is defined as – Debt for which a borrower is not personally liable.

25

WHEN IS DEBT DISCHARGED?

• Debt Modification – Any change in terms, collateral, etc.

• Significant Modification – Will trigger an exchange of the old debt for a new debt. §1001.

• Old Debt satisfied for issue price of New Debt.

26

REPURCHASE

• Debtor buys back its debt

• Related parties – example: Acquire $1,000 of debt for $500.

• COD + OID Result

• OID income recognized by related party over term of new debt. Debtor has corresponding deduction.

• Presumption (6 months prior). 27

EXCHANGES

• DEBT FOR DEBT – Satisfied old debt with amount of $ equal to the ISSUE PRICE of new debt.

• Significant modification triggers an exchange

28

EXCHANGES CONTINUED

• CODI = Adjusted issue price of Old Debt minus issue price of New Debt

• OID = Stated Redemption Price at Maturity Minus Issue Price of New Debt.

• USE AFR INTEREST RATE on New Debt, so debt is equivalent

29

FORM 982

• FORM 982 is used to reduce tax attributes due to discharge of indebtedness.

• The form must be attached to a timely filed return – extensions of time to file may be allowed if the taxpayer acted reasonably and in good faith under Treas. Reg. 301.9100-3.

• IRC §1017 provides rules for basis reduction.

30

Slide Intentionally Left Blank

32

33

II. TAX TREATMENT FOR PASS-THROUGH ENTITIES

By Robert S. Barnett CPA, JD, MS (TAXATION)

CAPELL BARNETT MATALON & SCHOENFELD, LLP.

ATTORNEYS AT LAW

(516) 931-8100

ENTITY OR INDIVIDUAL

• Certain items are treated at the entity level

• Differences arise depending on entity type

• §108 exclusions are discussed in more detail below, but bankruptcy and insolvency exceptions are tested at the S Corp level but for partnerships at each partner’s level

• Single member LLC’s are disregarded entities

SEE REV. RULE. 1999-5 for conversion to partnership

35

CONVERSION OF DEBT INTO EQUITY

• CORPORATE DEBTOR

• The Corp. is treated as having satisfied debt with $$ equal to the FMV of stock issued

• CODI = Debt > Value of Stock Issued

• §108(e)(8)

• Bankruptcy and insolvency exclusions may apply

36

EXAMPLE

• ABC owes creditor $1,000

• Cancels debt for equity FMV $700

• COD = $300

37

SHAREHOLDER EXCEPTION

• Shareholder cancellation §108(e)(6)

• As if corporation satisfied the debt with an amount of $ equal to the shareholder’s basis in the debt

• No CODI if shareholder’s basis in the debt is equal to the issue price; example: of loan of $

38

PARTNERSHIP DEBTOR

• Similar rules apply BUT NO PARTNER EXCEPTION

• §721 nonrecognition – not if for unpaid rent, royalties, or interest

• TRAP – But CODI if amount of debt > FMV of partnership interest

• Recognized by each partner immediately before transaction

• Creditors basis in partnership interest §722 would include her basis in the debt exchanged

39

PARTNERSHIP continued

• Can debt be converted as a capital contribution?

• Example: debt cancelled to partner/lender as capital contribution

• Economic substance over form CODI resulted

• What if $ repaid to partner who then made a capital infusion?

40

§108(i)

• Watch for §108(i) entity deferrals

• §108(i), part of the American Recovery and Reinvestment Tax Act, allowed for deferral of business CODI realized in 2009 and 2010

• Deferrals must be included in income ratably over 5 years beginning in 2014 2018

• Rules provided flexible elections and allocations

• Election at entity level 41

§108(i) continued

• Partnership permitted to allocate among partners

• CODI not deferred was able to be excluded under §108

• §108 exclusions DO NOT apply to recognition years

• Inclusion must occur ratably in 2014 2018

• Accelerations required – Death, Sale, Redemption of shareholder or partner, Sale of substantially all assets, Cessation of business, Liquidation

42

OTHER PARTNERSHIP CONSIDERATIONS

• Attribute reduction includes election to reduce basis in depreciable property

• This election may preserve NOL’s

• Partnership interest may qualify

– To extent partnership is holding depreciable property

– IF partnership also reduces its basis in such property (to extent of partner’s proportionate interest)

43

IRC §1017

• IRC §1017 provides that the partners interest in the partnership is treated as depreciable real property to the extent of the partner’s proportionate interest in the partnership’s depreciable real property.

• Partner’s election to treat the partnership interest as depreciable real property will result in both the partner’s partnership basis and the partnership’s basis in the depreciable real property allocable to such partner as reduced.

• Generally, the partnership may grant or withhold consent unless the taxpayer owns more than 50% partnership interest.

• §1250 Recapture and §751 if partnership interest reduced

44

RECAPTURE

• Capital asset basis reductions retain a recapture requirement

• Any gain on disposition is subject to recapture

45

Slide Intentionally Left Blank

III. APPLICATION OF §108

By Renato Matos, Esq.

CAPELL BARNETT MATALON & SCHOENFELD, LLP.

ATTORNEYS AT LAW

(516) 931-8100

§108 PROVIDES EXCEPTIONS TO RECOGNITION OF CODI

1. The §108(a)(1)(A) exception for discharges in bankruptcy cases

2. The §108(a)(1)(B) exception for insolvency situations

3. The §108(a)(1)(C) exception for “qualified farm indebtedness”

4. The §108(a)(1)(D) exception for “qualified real property indebtedness” [SEE SECTION VI]

48

§108 continued

5. The §108(e)(2) exception for debts that would have been deductible when paid

6. The §108(e)(5) exception for reduction of certain purchase price debt obligations

7. The §108(e)(6) exception for contribution to capital from a shareholder creditor

8. The §108(f) exception for certain student loans

9. §108(i) previously discussed 49

ATTRIBUTE REDUCTION

• Price to be paid for the EXEMPTIONS

• IRS prescribes precise order and timing

• Attribute reduction §108(b)(3) of tax items such as NOL’s, business credits, capital loss carryovers, basis of property, passive loss carryovers, and foreign tax credit carryovers

• Act as a tax deferral

• Required even if bankruptcy and insolvency exceptions apply

• Occur in the following year 50

S CORPORATION ATTRIBUTE REDUCTION

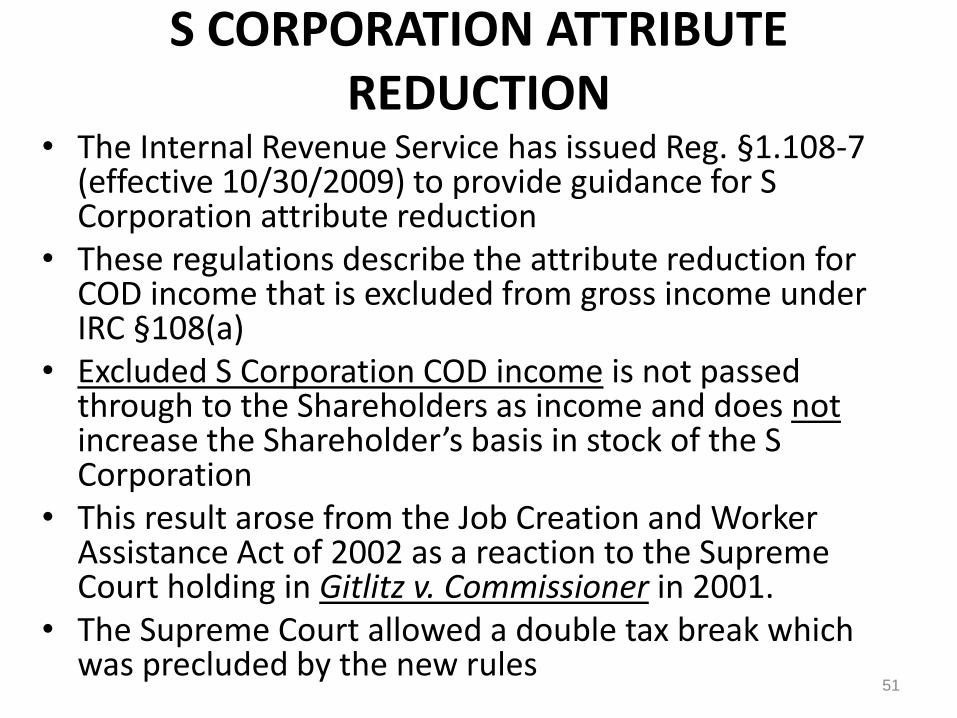

• The Internal Revenue Service has issued Reg. §1.108-7 (effective 10/30/2009) to provide guidance for S Corporation attribute reduction

• These regulations describe the attribute reduction for COD income that is excluded from gross income under IRC §108(a)

• Excluded S Corporation COD income is not passed through to the Shareholders as income and does not increase the Shareholder’s basis in stock of the S Corporation

• This result arose from the Job Creation and Worker Assistance Act of 2002 as a reaction to the Supreme Court holding in Gitlitz v. Commissioner in 2001.

• The Supreme Court allowed a double tax break which was precluded by the new rules

51

S CORP CONTINUED

• S Shareholders cannot take losses or deductions in excess of their basis in stock and debt owed to the Shareholder by the S Corporation

• Any loss or deduction that is disallowed as a result of the taxpayer having insufficient basis will be treated as an NOL of the S Corporation

• This “deemed NOL” includes all losses and deductions disallowed under the S Corporation basis rules

52

BANKRUPTCY EXCEPTION §108(A)(1)(A)

• Excludes CODI if discharge occurs in bankruptcy

• Includes Title II

• Discharge must be under court approval

53

INSOLVENCY §108(a)(1)(B)

• See Part IV Below

54

PURCHASE PRICE REDUCTION

• §108(e)(5) – no CODI if adjust purchase money debt

• Obligation to ORIGINAL SELLER (not bank loan)

• Treated as reduction of purchase price

55

BANKRUPT OR INSOLVENT PARTNERSHIP

• May use the §108(e)(5) purchase price reduction

• If all partners treat consistently

56

IV. APPLICATION OF INSOLVENCY EXCEPTION

By Robert S. Barnett CPA, JD, MS (TAXATION)

CAPELL BARNETT MATALON & SCHOENFELD, LLP.

ATTORNEYS AT LAW

(516) 931-8100

INSOLVENCY

• §108(a)(1)(B) excludes DOI if the discharge occurs when the taxpayer is insolvent

• Income excluded shall not exceed the amount by which the taxpayer is insolvent

• Insolvency is computed immediately before the discharge

58

ASSETS/LIABILITIES • Insolvency is the excess of liabilities over the FMV

of assets

• Assets include exempt assets including pensions which could be withdrawn

• Consider obligations that offset assets

• With sufficient degree of certainty

• Taxpayers must prove application of insolvency

• Look at obligation, not ability to pay

• 9th Cir. applied “more likely than not” test

• Contingent liabilities – only if can prove payment is required

59

BURDEN OF PROOF

• Local tax assessment is not accepted

• Obtain qualified appraisal at time of discharge

• IRS’s determinations in a notice of deficiency are presumed correct

• Taxpayer bears burden of proof that such determinations are not correct

60

Slide Intentionally Left Blank

NONRECOURSE DEBT

• Asset 1 FMV $1,000; $900 Recourse Debt

• Asset 2 FMV $2000; $2300 Nonrecourse Debt

• TP’s Liability = $900 + $2000 + amount of nonrecourse debt cancelled

• Therefore, cancellation of up to $200 of nonrecourse debt may be excluded from CODI

• If recourse debt is cancelled, TP is not insolvent (assets $3,000; liabilities $2,900)

• Rev. Rul. 92-53 62

PARTNERSHIPS

• Insolvency (and bankruptcy) is tested at each individual partner’s level

• CODI may be excluded only by those partners who are themselves bankrupt or insolvent

• Attribute reduction is applied at the individual partner level

63

S CORPORATIONS

• Insolvency and bankruptcy exceptions are applied at the corporate level

• No basis step up allowed

64

V. QUALIFIED REAL PROPERTY BUSINESS INDEBTEDNESS

By Renato Matos, Esq.

CAPELL BARNETT MATALON & SCHOENFELD, LLP. ATTORNEYS AT LAW

(516) 931-8100 [email protected]

65

QRPBI – QUALIFIED REAL PROPERTY BUSINESS INDEBTEDNESS

• Taxpayers other than C Corporations can exclude from gross income discharge of qualified real property business indebtedness

• Amount excluded must reduce the taxpayers’ basis in real property

• Amount cannot exceed the basis of real property held by the taxpayer

• Anti-Stuffing provision disallows purchase in contemplation of such discharge

66

ELECTION

• Elective exclusion – USE FORM 982

• Qualified real property business indebtedness - debt incurred to acquire, construct, or substantially renovate real property – special rules for pre-1993 debt

• Used in a trade or business, and

• Secured by such real property

• Note that the insolvency and bankruptcy exceptions come first

67

LIMITATIONS & RECAPTURE

• The exclusion cannot exceed

– The amount by which the principal amount of the debt exceeds the fair market value of the property securing the debt, or

– The aggregate adjusted bases of the taxpayer’s depreciable real property

• The basis reduction is treated as ordinary income RECAPTURE upon sale of the property based upon the IRC §1250 depreciation rules using the straight line method of depreciation

68

PARTNERSHIP

• PARTNERSHIP discharge and whether the debt was incurred in connection with a real property trade or business is made by reference to the business of the partnership

• The ELECTION to exclude or discharge real property business indebtedness is made at the partner level on a partner by partner basis

69

IRC §1017

• IRC §1017 provides that the partners interest in the partnership is treated as depreciable real property to the extent of the partner’s proportionate interest in the partnership’s depreciable real property.

• Partner’s election to treat the partnership interest as depreciable real property will result in both the partner’s partnership basis and the partnership’s basis in the depreciable real property allocable to such partner as reduced.

• Generally, the partnership may grant or withhold consent unless the taxpayer owns more than 50% partnership interest.

• §1250 Recapture and §751 apply if partnership interest reduced

70

S CORPORATION

• Election made at corporate level + attribute reduction

• No adjustment to shareholder stock

• Acts as a deferral

71

PRINCIPAL RESIDENCE

• Temporary Exclusion before January 1, 2013 - EXTENDED

• QUALIFIED principal residence indebtedness

• Not a second home

• Later §121 Exclusion may protect basis reduction

• Insolvency Exclusion may be preferable

72