Canadian Tax Implications of Owning Foreign Property Tax... · Navigating Tax Implications in...

16

Navigating Tax Implications in Greece for Foreign Residents and the Repercussions For Canadian Taxpayers Canadian Tax Implications of Owning Foreign Property Ryan L. Morris [email protected] 416.947.5001

Transcript of Canadian Tax Implications of Owning Foreign Property Tax... · Navigating Tax Implications in...

Navigating Tax Implications in Greece for Foreign Residentsand the Repercussions For Canadian Taxpayers

Canadian Tax Implications

of

Owning Foreign Property

Ryan L. [email protected]

416.947.5001

General Principles

Canadian residentstaxable on worldwideincome

General Principles

For example:

• Interest income on bank deposits andinvestments held in a foreign country

• Dividends paid by non-resident corporations

• Rental income on rental property located inforeign country

• Gains/income on sale of foreign-situs property

General Principles

Non-residents taxed on Canadian source income

• Income from employment exercised in Canada

• Income from carrying on business in Canada

• Income from Canadian investment property

– E.g., withholding tax on dividends,interest and royalties

• Subject to the application of a treaty

Canadian Residence

• “Ordinarily resident”

• Deemed residency

– Sojourned for ≥ 183 days

• Estate/trust managed in Canada

• Deemed non-residency

– Resident in anothercountry under aCanadian tax treaty

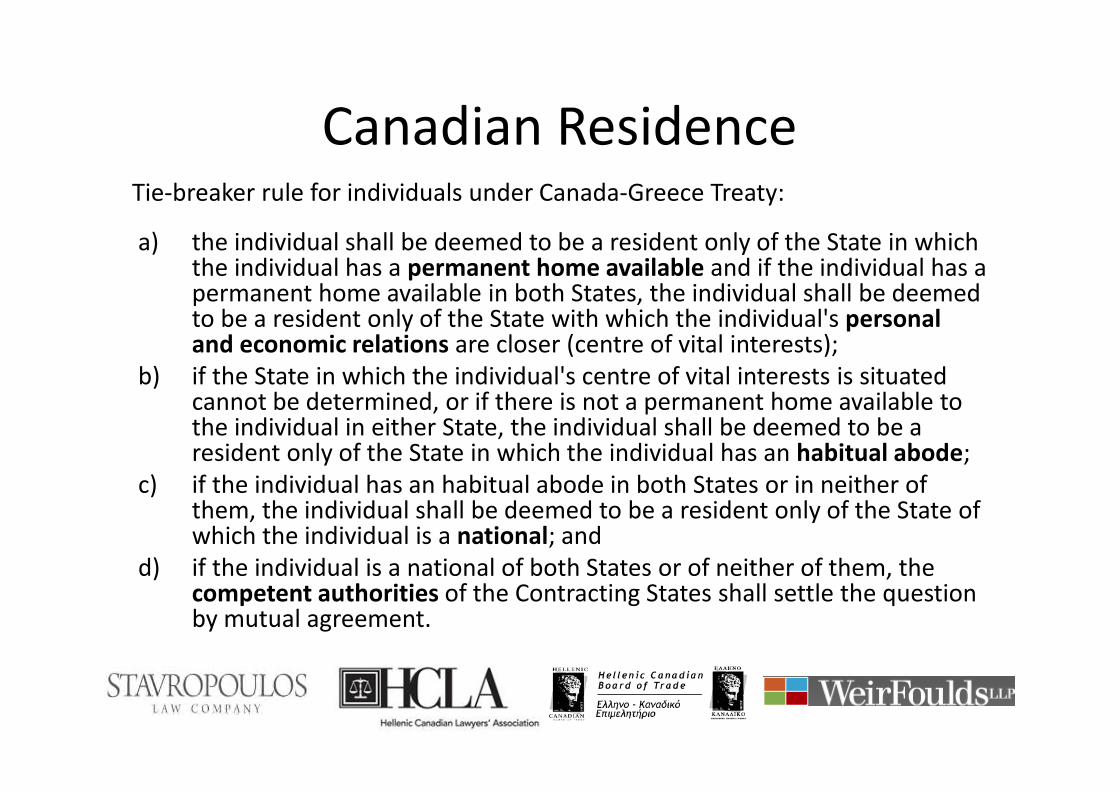

Canadian ResidenceTie-breaker rule for individuals under Canada-Greece Treaty:

a) the individual shall be deemed to be a resident only of the State in whichthe individual has a permanent home available and if the individual has apermanent home available in both States, the individual shall be deemedto be a resident only of the State with which the individual's personaland economic relations are closer (centre of vital interests);

b) if the State in which the individual's centre of vital interests is situatedcannot be determined, or if there is not a permanent home available tothe individual in either State, the individual shall be deemed to be aresident only of the State in which the individual has an habitual abode;

c) if the individual has an habitual abode in both States or in neither ofthem, the individual shall be deemed to be a resident only of the State ofwhich the individual is a national; and

d) if the individual is a national of both States or of neither of them, thecompetent authorities of the Contracting States shall settle the questionby mutual agreement.

Compliance • Self-reporting system

• Foreign propertyreporting requirements

• Subject to verification/reassessment

• Limitation periods(maybe none)

Verification

• Audits

• Whistleblowing programs

• Third partyinformation requests andreporting requirements

• Exchange of informationwith foreign countries andfinancial institutions

Exchange of Information underCanada-Greece Tax Treaty

“The competent authorities of the ContractingStates shall exchange such information as isforeseeably relevant for carrying out theprovisions of this Convention or to theadministration or enforcement of thedomestic laws concerning taxes of every kindand description imposed on behalf of theContracting States…”

Exchange of Information underCanada-Greece Tax Treaty

“If information is requested by a ContractingState in accordance with this Article, the otherContracting State shall use its informationgathering measures to obtain the requestedinformation, even though the other State doesnot need such information for its own taxpurposes.”

Exchange of Information underCanada-Greece Tax Treaty

“In no case shall the provisions of paragraph 3be construed to permit a Contracting State todecline to supply information solely becausethe information is held by a bank, otherfinancial institution, nominee or person actingin an agency or fiduciary capacity or becausethe information relates to ownership interestsin a person.”

Monetary Penalties

Include (but are not limited to):

• 5% - 17% of taxes owing on late-filed returns

• 10% of unreported income for repeat failures

• 50% of the taxes owed on unreported income(if the taxpayer was grossly negligent)

• 50% - 200% of any taxes that were sought to beevaded

• $12,000/$24,000 for failure to file specified foreignproperty information return in certain circumstances

Other Repercussions

• Imprisonment

• Interest

• Stigma

Voluntary Disclosure Program

What to do before…..

Voluntary Disclosure Program• Benefits

• Conditions:

– Voluntary

– Complete

– Penalty

– > 1 Year Overdue

• Qualifying period

• Commence onno-names basis