Canadian Oil & Gas Sector - Credit Suisse

67

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 13 April 2017 Americas/Canada Equity Research Oil & Gas Canadian Oil & Gas Sector The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Research Analysts David Hewitt 416 352 4583 [email protected] Jason Frew 403 476 6022 [email protected] Brian Ho 403 476 6009 [email protected] David Phung 403 476 6023 [email protected] Robert Loebach 403 476 6021 [email protected] Andrew M. Kuske 416 352 4561 [email protected] Paul Tan 416 352 4593 [email protected] Edward Westlake 212 325 6751 [email protected] Mark Lear, CFA 212 538 0239 [email protected] Thomas Adolff 44 20 7888 9114 [email protected] STRATEGY Canadian Energy in North America Figure 1: N America SMID 18 over 17 Prod’n growth Source: Credit Suisse estimates ■ Canada on the world stage – ‘concentrated’ on the US: Canada has world class oil and gas resources, and an abundant market on its doorstep, but an overconcentration of exports to the US, in our opinion. We would suggest the Government target should be ‘Resource to markets’. ■ Canadian oil patch – growth AND cash: Coming to the end of a major capex cycle Canadian oil players are set to book both production growth and see material increases in free cash-flow. We expect the next phase of growth to be brownfield focused, with break-evens in the US$45 – 60/bbl range. BAT is still a question, i.e., will there be one at all, and in what form. ■ Canadian gas – needed those LNG imports: The Montney & Deep basins hold some of the most economic gas resources in North America; however, the US is materially increasing gas production. Large scale Canadian LNG exports would have helped, but these now seem unlikely near term. We see continued pressure on the AECO differential and prefer the liquids rich gas producers. ■ Seeking out superstars: both in Canada and within North America: We use 4 metrics to score both SMID and large cap North America universes, then use the score to try and identify possible valuation gaps. In the SMID space in Canada we prefer VII and NVA and in the US PE and EGN. For the North America large cap universe we prefer SU and ECA in Canada and PXD, CXO and DVN in the US. Finally looking at global majors SU again stands out as does RDS and BP in Europe.

Transcript of Canadian Oil & Gas Sector - Credit Suisse

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

13 April 2017 Americas/Canada Equity Research

Oil & Gas

Canadian Oil & Gas Sector The Credit Suisse Connections Series leverages our

exceptional breadth of macro and micro research to deliver

incisive cross-sector and cross-border thematic insights for

our clients.

Research Analysts

David Hewitt

416 352 4583

Jason Frew

403 476 6022

Brian Ho

403 476 6009

David Phung

403 476 6023

Robert Loebach

403 476 6021

Andrew M. Kuske

416 352 4561

Paul Tan

416 352 4593

Edward Westlake

212 325 6751

Mark Lear, CFA

212 538 0239

Thomas Adolff

44 20 7888 9114

STRATEGY

Canadian Energy in North America

Figure 1: N America SMID 18 over 17 Prod’n growth

Source: Credit Suisse estimates

■ Canada on the world stage – ‘concentrated’ on the US: Canada has

world class oil and gas resources, and an abundant market on its doorstep,

but an overconcentration of exports to the US, in our opinion. We would

suggest the Government target should be ‘Resource to markets’.

■ Canadian oil patch – growth AND cash: Coming to the end of a major

capex cycle Canadian oil players are set to book both production growth

and see material increases in free cash-flow. We expect the next phase of

growth to be brownfield focused, with break-evens in the US$45 – 60/bbl

range. BAT is still a question, i.e., will there be one at all, and in what form.

■ Canadian gas – needed those LNG imports: The Montney & Deep

basins hold some of the most economic gas resources in North America;

however, the US is materially increasing gas production. Large scale

Canadian LNG exports would have helped, but these now seem unlikely

near term. We see continued pressure on the AECO differential and prefer

the liquids rich gas producers.

■ Seeking out superstars: both in Canada and within North America: We

use 4 metrics to score both SMID and large cap North America universes,

then use the score to try and identify possible valuation gaps. In the SMID

space in Canada we prefer VII and NVA and in the US PE and EGN. For

the North America large cap universe we prefer SU and ECA in Canada

and PXD, CXO and DVN in the US. Finally looking at global majors SU

again stands out as does RDS and BP in Europe.

13 April 2017

Canadian Oil & Gas Sector 2

Table of contents

Focus charts 3

Investment summary 4

Canada: global resources–US concentrated 5

Canadian Oil: growth AND cash… 19

Gas: need those LNG exports… 25

Stocks: 38

Relative Valuation 48

13 April 2017

Canadian Oil & Gas Sector 3

Focus charts

Figure 2: Canada: oil production, consumption &

exports

Figure 3: Risked BAT, carbon charge & Keystone XL

for Canadian bitumen producers

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 4: Western Canada Heavy in Asia / EU

Figure 5: Canadian oil sands – possible growth

projects

Source: BBG, Credit Suisse estimates Source: Company data, Credit Suisse estimates; Spot WTI as of April 11, 2017

Figure 6: Oil sands capex / production outlook Figure 7: N America large cap – PPS growth

Source: CAPP, Credit Suisse estimates Source: Credit Suisse estimates

30

35

40

45

50

55

60

65

70

0 50 100 150 200 250 300 350 400 450 500 550 600

WTI

Bre

akeven (

US

$/b

)

Production Capacity (mbd)

P2B

EM

SA

GP

LloydThermal

CL-G

Bro

wnfield

Kirby

Nort

h

Aspen

Horizo

n

Debott

leneck

FC

-H

NL-A

Prim

rose

E

xpansi

on

Cold

Lake

Exp

ansi

on

MEG

HSE

CVE

CNQ

IMO

Spot WTI

CS 2018F WTI

Avg. Breakeven

13 April 2017

Canadian Oil & Gas Sector 4

Investment summary World class resources – largest global market on your doorstep: In a way Canada is

twice blessed – world scale resources in both oil and gas and the world’s largest economy

right next door. In reality Canada has under-performed the US in terms of resource to

reserve conversion and production growth. The degree of supply concentration is

staggering, with Canada exporting 73% of its oil production – 99% of which goes to the

US, with a similar story with gas. All of which might have seemed satisfactory until the US

selected a new type of President, the antithesis of Canada’s liberal Prime Minister, who

immediately introduced the idea of a new tax regime with a Border Adjustment Tax at its

core – suddenly concentration looks a little less good. We see the calculation as nuanced

– BAT alone could penalize, but the same President approved the Keystone XL pipeline,

which will help alleviate rail export economics. The Canadian government's catchphrase

is ‘Resource to Market’ – we would politely suggest an ‘s’ is added to the final world.

Canadian oil: at the end of a growth spurt it’s time to collect the cash: Canada is at

the end of a greenfield oil sands build-out that started before crude 2014 capitulation, with

production and material cash flow to follow. With a carbon cap in Alberta and abundant

shale oil growth in the US we expect the sector to shift away from major greenfield

developments to more accretive and selective brownfield growth. A common mis-

conception seems to be that oil sands projects need US$70/bbl+ to ‘work’; CS estimates a

range of US$45 to US$60 (WTI) for the likely next set of projects to breakeven. As with the

US costs have fallen in Canada, but with less capex intensity in the next cycle we expect

less cost reflation pressure than in the US shale ‘hotspots’. On the technology front the

application of solvent technology will significantly lower water requirements, with Imperial

Oils Aspen project leading the way. With increased production and lower capex comes

greater free cash-flow, and we expect dividend growth and buybacks going forward.

Canadian Gas – some great rocks, unfortunate timing: CS views the Montney and

Deep basins to hold some of the most economic gas resources in North America, which

along with attractive fiscal terms positions them well. The challenge is the wall of

competitive gas being developed in Canada’s core market – the US. The big hope was for

LNG exports, but the major projects have not eventuated, and the next market window is

two years away, in our opinion. With abundant low cost gas we assume the AECO

differential remains at a similar level (-US$1/mcf vs NYMEX) going forward, but watch for

wildcard outcomes like major LNG project sanctions, more oil sands growth (than

forecast), or other demand growth for example petrochemical additions and the eventual

phase out of coal fired generation in Alberta. Given these dynamics we prefer liquids rich

gas producers. With challenged gas economics we would expect further consolidation in

the space.

Stocks: new metric to look for potential outliers, both in Canada and across North

America: We segregate into two universes – SMID and large cap, focus on Canada

initially and then NA as a whole. We use 4 metrics (production growth, operating

margin/boe, D/CF and yield) to ‘score’ each stock and then use that score to compare an

implied 2018 EBITDA multiple for that universe to our current forecast – seeking outliers.

In the SMID space in Canada we prefer VII and NVA and in the US PE and EGN. For the

North America large cap universe we prefer SU and ECA in Canada and PXD, CXO and

DVN in the US. Finally looking at global majors SU again stands out as does RDS and BP

in Europe.

13 April 2017

Canadian Oil & Gas Sector 5

Canada: global resources–US concentrated

World class resources – largest global market on your doorstep: In a way Canada is

twice blessed – world scale resources in both oil and gas and the world’s largest economy

right next door. In reality Canada has under-performed the US in terms of resource to

reserve conversion and production growth. The degree of supply concentration is

staggering, with Canada exporting 73% of its oil production – 99% of which goes to the

US, with a similar story with gas. All of which might have seemed satisfactory until the US

selected a new type of President, the antithesis of Canada’s liberal Prime Minister, who

immediately introduced the idea of a new tax regime with a Border Adjustment Tax at its

core – suddenly concentration looks a little less good. We see the calculation as nuanced

– BAT alone could penalize, but the same President approved the Keystone XL pipeline,

which will help alleviate rail export economics. The Canadian government's catchphrase

is ‘Resource to Market’ – we would politely suggest an ‘s’ is added to the final world.

Canada: world scale oil and gas resource geography: Using BP’s 2016 Statistical

Review (2015 data) Canada ranks as the 3rd

largest Proved Reserve after Saudi Arabia

and Venezuela. In gas it’s not in the same league as players such as Iran and Russia, but

still holds 12 billion boe, a little more than half of Australia. If you integrate the oil and gas

holdings Canada’s Proved Reserves are 185 billion boe, ahead of the US at 123bn boe

but behind Russia, Iran and Saudi Arabia. Canada is clearly an important source of

hydrocarbons on a global basis. Given recent gains in US shale namely the Permian we

would expect the reserves figure to rise with the next update.

Figure 8: Oil: largest Proved Reserve

by geography - end 2015

Figure 9: Gas: largest Proved Reserve

by geography - end 2015

Source: BP Statistical Review Source: BP Statistical Review

0

50

100

150

200

250

300

350Billion bbl

0

50

100

150

200

250

Billion boe

13 April 2017

Canadian Oil & Gas Sector 6

The US has grown oil and gas reserves faster than Canada: The oil reserves spike in

Canada (1999) was driven by a re-determination of Oil Sands as a Proved Reserve.

Although a lower quantum the US has been growing its oil reserve pool in recent years

where Canadian Proved Reserves have been in decline. The story is similar in gas, where

the US Proved Reserves grew by an average 7% over the last 10 years vs 2% for

Canada.

Figure 10: Canada / US Proved

Reserve history - Oil: 1980 - 2015

Figure 11: Canada / US Proved

Reserve history - Gas: 1980 - 2015

Source: BP Statistical Review Source: BP Statistical Review

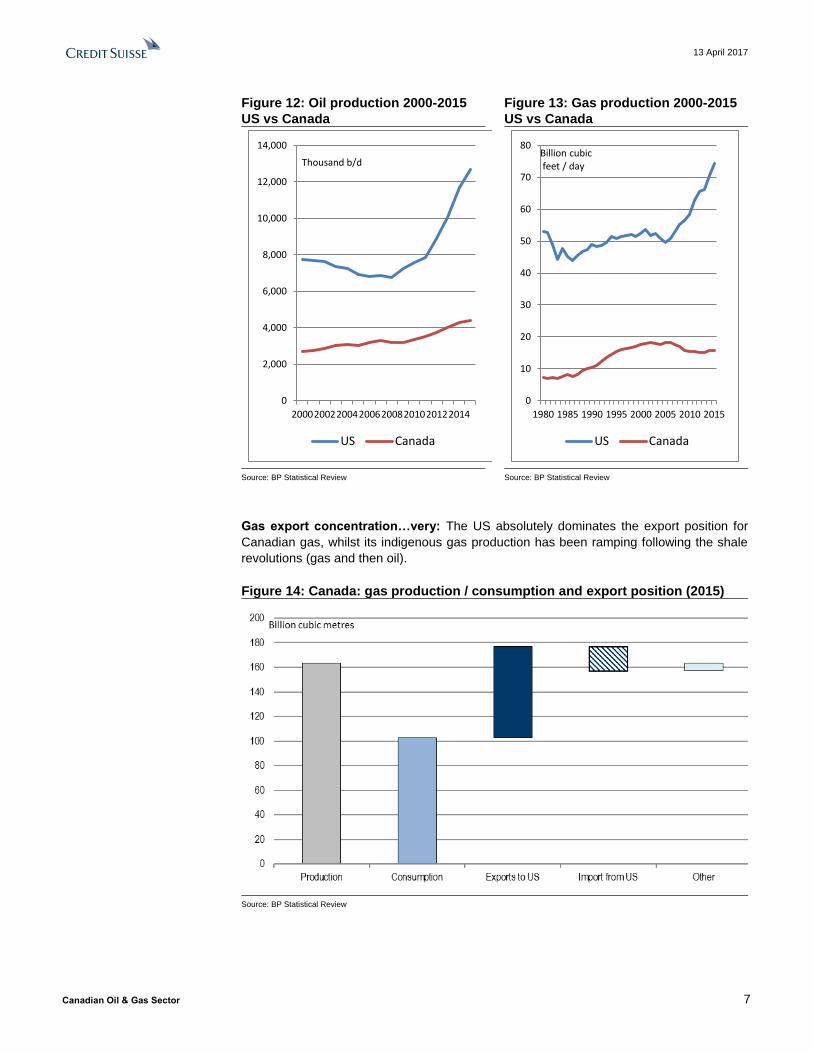

The US has also outgrown Canada in oil and gas production: In oil the US grew on

average by 5.4% between 2005 and 2015 vs 3.3% in Canada; in gas the US grew on

average by 3.5% in the same period where Canada was flat.

13 April 2017

Canadian Oil & Gas Sector 7

Figure 12: Oil production 2000-2015

US vs Canada

Figure 13: Gas production 2000-2015

US vs Canada

Source: BP Statistical Review Source: BP Statistical Review

Gas export concentration…very: The US absolutely dominates the export position for

Canadian gas, whilst its indigenous gas production has been ramping following the shale

revolutions (gas and then oil).

Figure 14: Canada: gas production / consumption and export position (2015)

Source: BP Statistical Review

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

20002002200420062008201020122014

US Canada

Thousand b/d

0

10

20

30

40

50

60

70

80

1980 1985 1990 1995 2000 2005 2010 2015

US Canada

Billion cubic feet / day

13 April 2017

Canadian Oil & Gas Sector 8

The story is similarly concentrated for oil: With Canada exporting 73% of its total

production to the US, an incredible 99% of its total exports. With access to both the Pacific

and Atlantic oceans this statistic comes as somewhat of a surprise to a recent arriver to

the country.

Figure 15: Canada: Oil production, consumption and exports

Source: BP Statistical Review

So why has the US outpaced Canada in converting opportunity into production?

One could probably write a book on the topic but here we venture a few broad thoughts:

The US shale revolution, firstly in gas then oil which has been cost competitive

even before the distance disadvantage Canadian production has when selling into

the US

The oil cost curve: Great strides have been made in oil sands unit costs through

the current crude price cycle, but oil sands projects still don’t sit on the left-hand

side of the global oil cost curve.

The lack of infrastructure (both pipe and liquefaction) to the Pacific and

Atlantic: Without reach to non-US export points, Canada is limited to the

takeaway capacity for both oil and natural gas to the US.

Fiscal prudence: Canadian upstream producers are, for the most part, well run

and tend to expand broadly within cash-flow constraints. This was clearly not the

case for a number of the US players participating in the US shale revolution.

A larger economic home base: It’s hard to argue with demographics...Canada

has a population of circa 35 million; the US weighs in at 320 million. Hence

resources growth depends on exports.

Politics: Trudeau vs. Trump: Their names start with the same letter: and that may be

where the similarity ends. Trudeau is a classical liberal, running a country that broadly

follows the European model (healthcare and education) and of course recently joined the

EU, at least in a trade agreement. Trump is a Republican president, appearing to askew

globalization in favor of a domestically focused, economically strong and competitive US.

Trudeau appears committed to respect for the environment, and for developing

13 April 2017

Canadian Oil & Gas Sector 9

hydrocarbons in a way that takes both that and human issues into consideration. President

Trump seems less concerned about climate change and is set to focus on reducing

regulatory controls for oil and gas development / production, and developing indigenous oil

and gas, creating jobs in America.

Trudeau: ‘resource to market’ – or should it be marketS: Mr. Trudeau has repeatedly

used the expression ‘resource to market’. Figure 14 and Figure 15 above suggest his

predecessors and the Canadian industry have been following the advice literally, i.e.,

supplying the single market of the US. We would respectfully suggest that, given the over

concentration of supply into the US and the discussion around the border tax (more later),

a better slogan would be ‘resource to marketS’, i.e., a deliberate and co-ordinated effort to

increase take-away capacity for oil and gas production to ports in the East and West coast

to facilitate the sale of Canadian oil and gas to markets other than (or in addition to) the

US.

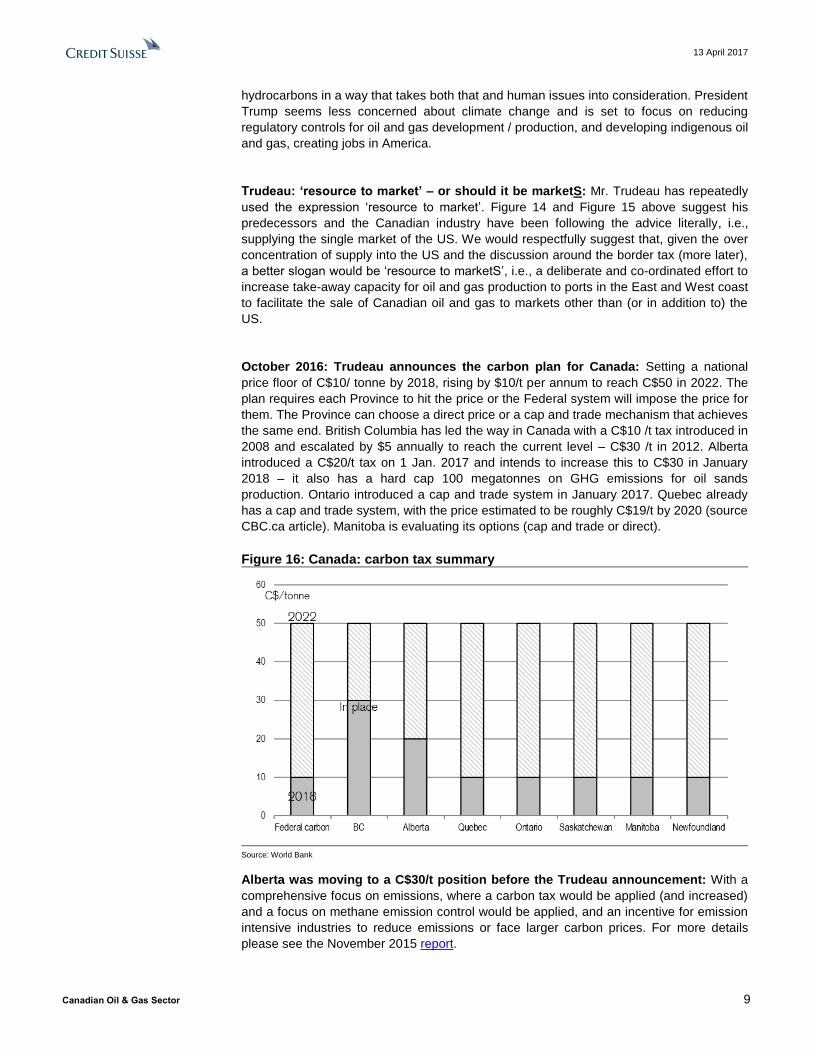

October 2016: Trudeau announces the carbon plan for Canada: Setting a national

price floor of C$10/ tonne by 2018, rising by $10/t per annum to reach C$50 in 2022. The

plan requires each Province to hit the price or the Federal system will impose the price for

them. The Province can choose a direct price or a cap and trade mechanism that achieves

the same end. British Columbia has led the way in Canada with a C$10 /t tax introduced in

2008 and escalated by $5 annually to reach the current level – C$30 /t in 2012. Alberta

introduced a C$20/t tax on 1 Jan. 2017 and intends to increase this to C$30 in January

2018 – it also has a hard cap 100 megatonnes on GHG emissions for oil sands

production. Ontario introduced a cap and trade system in January 2017. Quebec already

has a cap and trade system, with the price estimated to be roughly C$19/t by 2020 (source

CBC.ca article). Manitoba is evaluating its options (cap and trade or direct).

Figure 16: Canada: carbon tax summary

Source: World Bank

Alberta was moving to a C$30/t position before the Trudeau announcement: With a

comprehensive focus on emissions, where a carbon tax would be applied (and increased)

and a focus on methane emission control would be applied, and an incentive for emission

intensive industries to reduce emissions or face larger carbon prices. For more details

please see the November 2015 report.

13 April 2017

Canadian Oil & Gas Sector 10

North America is not at the leading edge re carbon pricing: Figure 17 shows global

carbon tax rates, with Sweden leading the way, and all of the major current carbon tax

geographies being in Europe.

Figure 17: Global carbon tax rates

Source: World Bank pricing watch

So Canada making a start – the new US administration (ex-California) not so

inclined: The Canadian government is working on implementing a graduated carbon tax –

to reach a country wide C$50/t (US$38/t) by 2022. The new US administration appears to

be taking a different approach to the issue of carbon charging, with no immediate plans for

the application of a national carbon tax. California is the largest exception, where a cap

and trade mechanism is in place, but is being challenged with businesses trying to

invalidate the State’s fee for carbon pollution via a case filed at the State appeals court.

There is also an initiative titled the Regional Greenhouse Gas Initiative ‘RGGI’, known as

Reggie – involving the states of Connecticut, Delaware, Maine, Maryland, Massachusetts,

New Hampshire, New York, Rhode island and Vermont, which is targeted at power sector

emissions only, and for those plants that are 25MW and larger.

Indicatory cost for Canadian producers vs US re carbon charging: Using the Alberta

analysis in the above report we concluded that a typically emission intensive SAGD

producer would pay C$0.17 /bbl when the carbon tax was C$10/t – hence the initial cost

next year in Canada (if the State was not exceeding the $10/t minimum) would be

US$0.12 / bbl, but that would rise to US$0.60/bbl once the carbon tax rose to C$50/t, i.e.

in 2022.

13 April 2017

Canadian Oil & Gas Sector 11

Figure 18: US vs Canada - cost of carbon charging

Source: Credit Suisse estimates

For context, a typical SAGD netback is in the range of ~C$30/b at our long term oil price of

US$62.50WTI (see Figure 23 below).

US Border Adjustment Tax (BAT)

Border Adjustment Tax = wake-up call for export diversification: While it’s clear that

nobody could have forecast the sea change in the US’s trade strategy, and in reality

nobody can accurately forecast the eventual outcome of the Border Tax Adjustment

proposal, it does serve to remind Canada’s energy planners that export concentration

carries fiscal risk. Whatever the BAT outcome one would expect a shift in long term

planning for hydrocarbon export pathways in Canada.

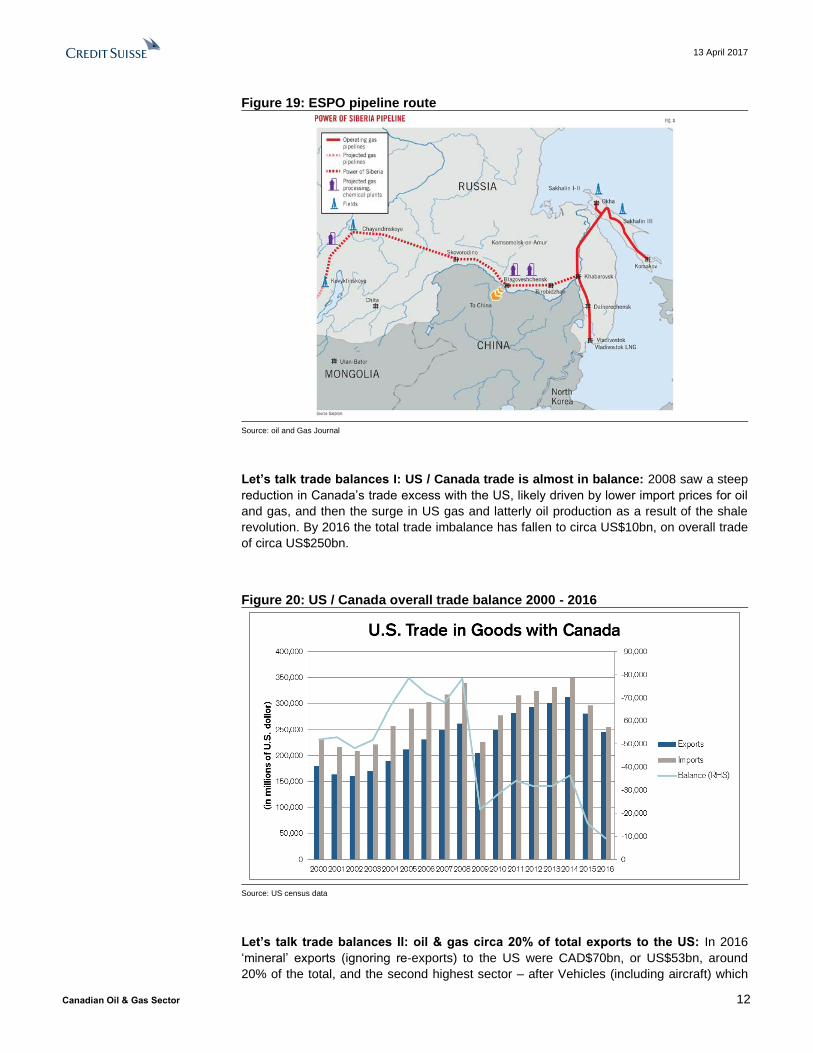

Take Russia’s lead…the ESPO pipeline was all about energy security: Russia set a

target to increase exports to Asia from 6% to 20% with the development of the East

Siberia Pacific Ocean (ESPO) pipeline. It also provides supply flexibility for Russia,

reducing its dependence on Europe as the dominant sump for its oil exports (sound

familiar…). At the time of project sanction then Prime Minister Putin was quoted as saying

“this is not just a pipe” but rather “a geopolitical project”. Transneft, the pipeline operator,

set a tariff of US$55/ton, despite estimated costs of US$130/tonne (source euractiv.com).

13 April 2017

Canadian Oil & Gas Sector 12

Figure 19: ESPO pipeline route

Source: oil and Gas Journal

Let’s talk trade balances I: US / Canada trade is almost in balance: 2008 saw a steep

reduction in Canada’s trade excess with the US, likely driven by lower import prices for oil

and gas, and then the surge in US gas and latterly oil production as a result of the shale

revolution. By 2016 the total trade imbalance has fallen to circa US$10bn, on overall trade

of circa US$250bn.

Figure 20: US / Canada overall trade balance 2000 - 2016

Source: US census data

Let’s talk trade balances II: oil & gas circa 20% of total exports to the US: In 2016

‘mineral’ exports (ignoring re-exports) to the US were CAD$70bn, or US$53bn, around

20% of the total, and the second highest sector – after Vehicles (including aircraft) which

13 April 2017

Canadian Oil & Gas Sector 13

account for just shy of 25%. Of Canada’s imports from the US Vehicles also represents

the largest sector (again just shy of 25%), followed by machinery (20%).

Figure 21: Canadian exports to the US - by sector Figure 22: Canadian imports from the US - by sector

Source: Statistics Canada Source: Statistics Canada

BAT – the story so far: Our colleagues in Washington published an excellent summary of

the basic design and aim of the BAT (Link here). In summary:

A 20% tax on imported goods and services – no tax on goods and services

exports.

Estimated to raise an estimated US$1 trillion over 10 years.

Also known as “cash-flow tax” – If implemented the US would be the only OECD

member to use this; all of the others using Value Added Tax (VAT) in relation to

border adjustment.

World Trade organization classification unclear: the question being whether BAT

would be classified as a direct or indirect tax (which VAT is).

The Republican Party developed blueprint does NOT currently envisage

exceptions.

CS expects action to commence in the house in the spring, with an aim to place

the bill on the President’s desk by August.

CS believes that tax reform is a top priority for the Republican Congress and

Administration.

While it’s far too early to forecast the outcome of the proposal through the US political

process it seems clear that the desire for an adjustment tax is a broad Republican

leadership project, rather than a twinkle in a tweet…

If implemented, and without FX adjustment, BAT would penalize a bitumen producer

by circa US$8.5/bbl: In our report on the possible BAT effect in Canada (Link here) we

considered a series of factors that could affect a theoretical Canadian bitumen producer.

The application of the 20% tax would reduce the realized price from C$45 to C$34 /bbl,

and reduce the producers' netback by 40%.

13 April 2017

Canadian Oil & Gas Sector 14

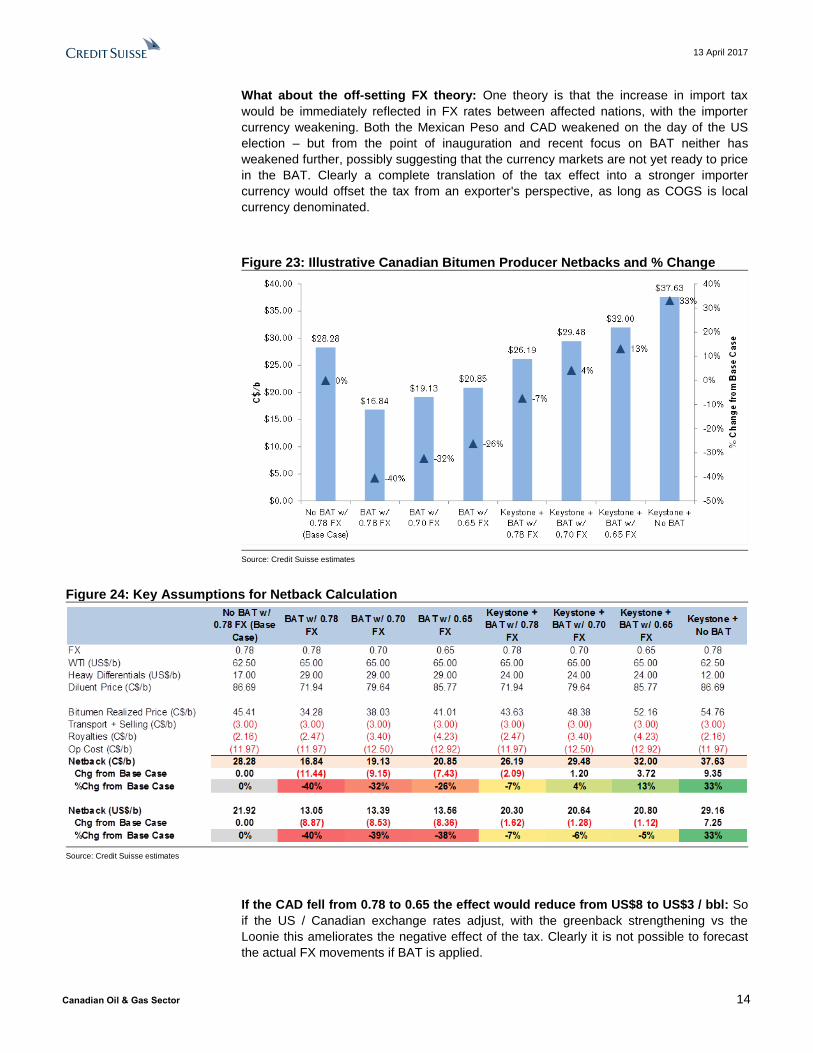

What about the off-setting FX theory: One theory is that the increase in import tax

would be immediately reflected in FX rates between affected nations, with the importer

currency weakening. Both the Mexican Peso and CAD weakened on the day of the US

election – but from the point of inauguration and recent focus on BAT neither has

weakened further, possibly suggesting that the currency markets are not yet ready to price

in the BAT. Clearly a complete translation of the tax effect into a stronger importer

currency would offset the tax from an exporter's perspective, as long as COGS is local

currency denominated.

Figure 23: Illustrative Canadian Bitumen Producer Netbacks and % Change

Source: Credit Suisse estimates

Figure 24: Key Assumptions for Netback Calculation

Source: Credit Suisse estimates

If the CAD fell from 0.78 to 0.65 the effect would reduce from US$8 to US$3 / bbl: So

if the US / Canadian exchange rates adjust, with the greenback strengthening vs the

Loonie this ameliorates the negative effect of the tax. Clearly it is not possible to forecast

the actual FX movements if BAT is applied.

13 April 2017

Canadian Oil & Gas Sector 15

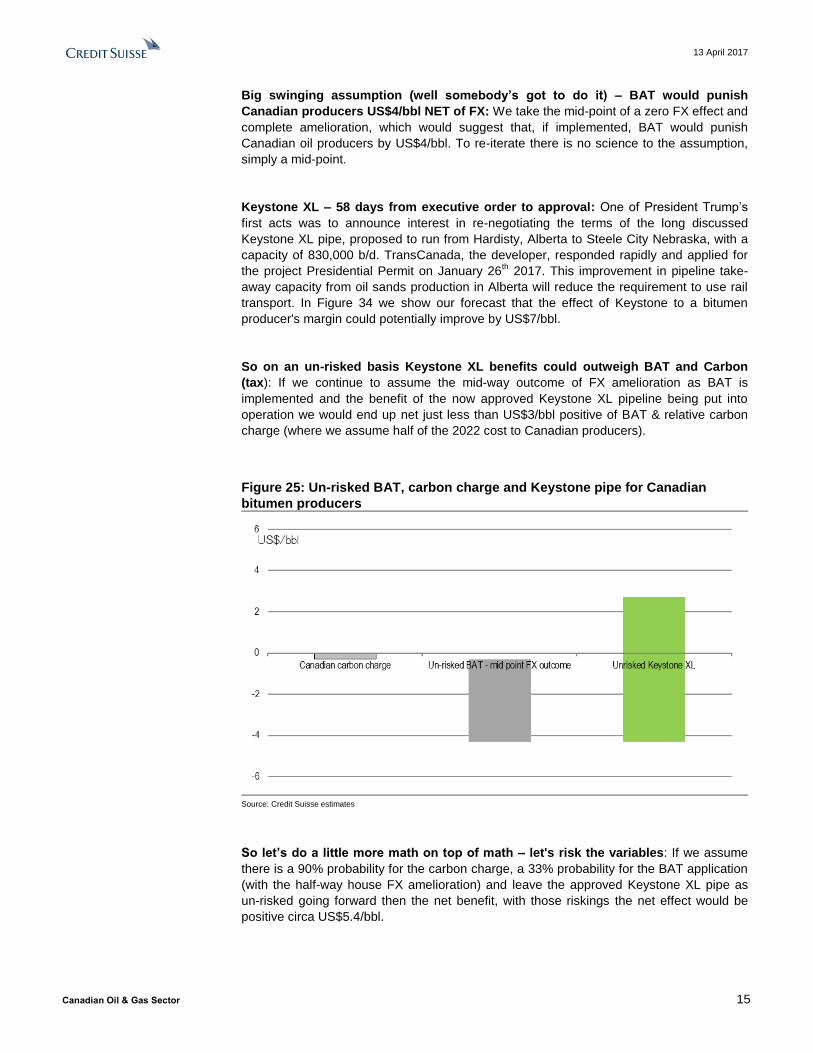

Big swinging assumption (well somebody’s got to do it) – BAT would punish

Canadian producers US$4/bbl NET of FX: We take the mid-point of a zero FX effect and

complete amelioration, which would suggest that, if implemented, BAT would punish

Canadian oil producers by US$4/bbl. To re-iterate there is no science to the assumption,

simply a mid-point.

Keystone XL – 58 days from executive order to approval: One of President Trump’s

first acts was to announce interest in re-negotiating the terms of the long discussed

Keystone XL pipe, proposed to run from Hardisty, Alberta to Steele City Nebraska, with a

capacity of 830,000 b/d. TransCanada, the developer, responded rapidly and applied for

the project Presidential Permit on January 26th 2017. This improvement in pipeline take-

away capacity from oil sands production in Alberta will reduce the requirement to use rail

transport. In Figure 34 we show our forecast that the effect of Keystone to a bitumen

producer's margin could potentially improve by US$7/bbl.

So on an un-risked basis Keystone XL benefits could outweigh BAT and Carbon

(tax): If we continue to assume the mid-way outcome of FX amelioration as BAT is

implemented and the benefit of the now approved Keystone XL pipeline being put into

operation we would end up net just less than US$3/bbl positive of BAT & relative carbon

charge (where we assume half of the 2022 cost to Canadian producers).

Figure 25: Un-risked BAT, carbon charge and Keystone pipe for Canadian

bitumen producers

Source: Credit Suisse estimates

So let’s do a little more math on top of math – let's risk the variables: If we assume

there is a 90% probability for the carbon charge, a 33% probability for the BAT application

(with the half-way house FX amelioration) and leave the approved Keystone XL pipe as

un-risked going forward then the net benefit, with those riskings the net effect would be

positive circa US$5.4/bbl.

13 April 2017

Canadian Oil & Gas Sector 16

Figure 26: Risked BAT, carbon charge and Keystone pipe for Canadian bitumen

producers

Source: Credit Suisse estimates

Canada has ‘spoken’ about border tariffs – saying ‘je n’aime pas le tariff’: Foreign

Minister Freeland met with officials in Washington, including US Secretary of State

Tillerson, and informed the media that “we would be strongly opposed to any imposition of

new tariffs between Canada and the United States…and that if such an idea were ever to

come into being, Canada would respond accordingly”. It would appear the velvet glove

was partially removed to reveal a steelier fist…

Is Tax reform next after Obamacare? Looks like it… President Trump was quoted thus

“I would say that we probably start going very, very strongly for the big tax cuts and tax

reform. That will be next.” The target for the bill is to attain congressional approval by

August, failing that by the Fall. A New York Times media article (here) suggests that the

Border Tax component is not universally agreed to by some of the President's senior

advisors, with Stephen Bannon a proponent, however with Wilbur Ross, Gary Cohn and

Steven Mnuchin less so. With the savings from the Obamacare reform now missing from

the equation, the question becomes is there a yet greater focus on BAT as a funds raising

exercise, or is it seen as ‘difficult’ and at risk from a lack of support from certain

Republican factions.

Canadian Resources Minister in Washington: “very little support” for BAT: Minister

Jim Carr visited Washington on the 30th March, visiting Senators, members of Congress,

lobby groups and business leaders. He told media that “There was very little support for it”

and that “It’s not just that people here are expressing an agreement in principal with free

trade, it’s that they are specifically saying that a border adjustment tax would not move

along the interests of Canada and the United States.”

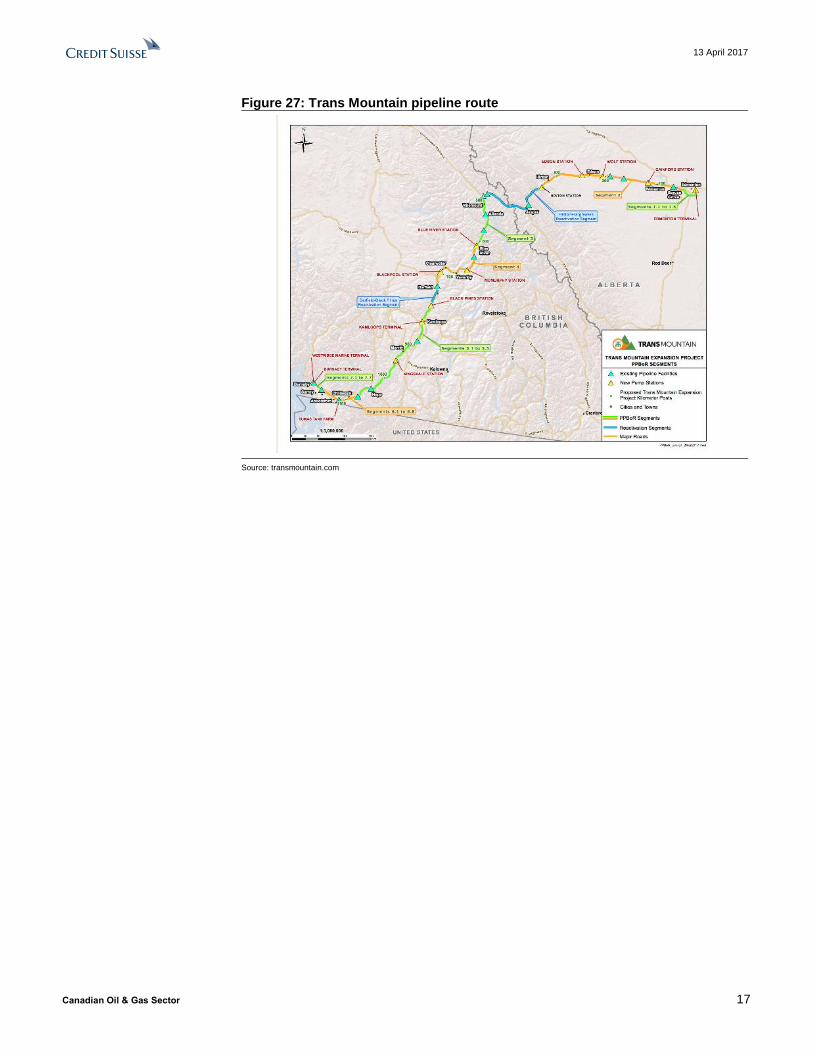

The Trans Mountain pipeline is set to increase capacity to 890kb/d: the pipe has a

current capacity of 300kb/d most of which is used to carry crude to configured refineries in

Washington state. The expansion was approved by the Trudeau government and the pipe

owners (Kinder Morgan) expect about 450kb/d to target exports to North East Asia,

presumably to complex refiners in South Korea and China. The pipe ends at the Westridge

marine terminal in BC.

13 April 2017

Canadian Oil & Gas Sector 17

Figure 27: Trans Mountain pipeline route

Source: transmountain.com

13 April 2017

Canadian Oil & Gas Sector 18

Better global reach for Canadian crude could pay: We looked at Iraqi Basrah Heavy

priced in both Asia and Europe, both (as at 29 March 2017) circa US$45/bbl. We used

Basrah as a reasonably similar assayed crude (WCS 20 API, Basrah 23.5). For the Asia

route we assume it costs US$2.5/bbl to reach the BC coast (via the Transmountain pipe)

and a further US$4/bbl for Aframax shipping to an Asian port. Aframax because the Port of

Vancouver cannot accept VLCC’s – there being 3 bridges in the access route to the port).

Certain countries in Asia have complex refinery systems (including the ability to deal with

high TAN crudes), including South Korea, certain Chinese refineries and Reliance in India.

These assumptions suggest an arb value for WCS in Asia of circa US$0.85/bbl. To reach

North West Europe we assume a Canadian pipeline cost of US$5/bbl to the Nova Scotia

coast and a further US$1/bbl for VLCC transportation to the refining centre in NWE -

suggesting an arb value of US$1.35/bbl. From both a current economics (although price

differentials can of course be volatile) and from an energy security perspective, a greater

capacity to export crude would seem logical.

Figure 28: Western Canadian Heavy in Asia / EU vs Basrah Heavy

Source: BBG, Credit Suisse estimates – as at 29 March 2017.

13 April 2017

Canadian Oil & Gas Sector 19

Canadian Oil: growth AND cash…

Canadian oil: at the end of a growth spurt it’s time to collect the cash: Canada is at

the end of a greenfield oil sands build-out that started before crude 2014 capitulation, with

production and material cash flow to follow. With a carbon cap in Alberta and abundant

shale oil growth in the US, we expect the sector to shift away from major greenfield

developments to more accretive and selective brownfield growth. A common mis-

conception seems to be that oil sands projects need US$70/bbl+ to ‘work’; CS estimates a

range of US$45 to US$60 (WTI) for the likely next set of projects to break even. As with

the US, costs have fallen in Canada, but with less capex intensity in the next cycle we

expect less cost reflation pressure than in the US shale ‘hotspots’. On the technology front

the application of solvent technology will significantly lower water requirements, with

Imperial Oils Aspen project leading the way. With increased production and lower capex

comes greater free cash-flow, and we expect dividend growth and buybacks going

forward.

Canadian Oil Sector:

Oil I: Carbon emission limit of 100MT/pa in Alberta: As part of its emissions planning

Alberta has imposed a 100MTpa CO2 emissions limit for oil sands production in the State.

As Figure 29 shows production (and hence emissions) has grown rapidly since the start of

the decade, as a result of a major capex cycle. That cycle is largely complete, and as we

will argue below, we believe the Canadian oil sands sector is moving from higher growth to

more of a harvest mode. In order to prolong post-2020 growth (i.e., beyond committed

projects), oil sands producers will likely need to accelerate the evaluation and

implementation of new technologies that offer both incremental and step-change

improvements in project economics and emission profiles.

Figure 29: Alberta - carbon cap

Source: Wood Mackenzie

13 April 2017

Canadian Oil & Gas Sector 20

Oil II: Misconception I ‘oil sands sanctions needs $75/bbl’: As we move away from

capital intensive (in oil and gas terms) greenfield oils sands projects, future growth can be

leveraged with brownfield expansions. Figure 30 shows the CS view of the more likely (but

not certain) additions to oil sands capacity. All but Imperials Aspen greenfield project are

brownfield expansions, some using new technology like solvent assisted SAGD, and CO2

management technology.

Figure 30: Canadian oil sands: possible future growth projects

Source: Credit Suisse estimates; Spot WTI as of April 11, 2017

Oil II (II): 500kb/d of possible production additions–balanced not breakneck growth:

Across the unsanctioned cost curve the total production associated with these projects is

just north of 500kb/d. While new sanction likelihood will increase with higher crude prices

the next phase of oil sands growth in Canada is likely to be balanced, without inciting a

significant unit cost cycle.

Oil III: Break-evens have reduced in this price cycle – less reflationary risk vs US

shale? Figure 31 shows that thus far through the current oil price cycle typical full (i.e.

inclusive of sustaining capex) breakeven for Canadian oil sands have fallen from circa

US$60 to US$40/bbl (WTI). Going forward the highly labor intensive projects like Fort Hills

& Horizon (2B + 3) are coming off construction peak, and without another major capex

cycle (please see Figure 38) we expect sedentary wage growth for oil sands labour. In

terms of energy costs our view is that Western Canada gas prices will continue to be

challenged going forward (see the gas section of the report) and hence do not model an

energy input cost escalating with crude oil price improvements. This clearly contrasts with,

for example, the Permian which is rapidly ramping up for another capital intensive growth

spurt.

30

35

40

45

50

55

60

65

70

0 50 100 150 200 250 300 350 400 450 500 550 600

WTI

Bre

ake

ve

n (

US

$/b

)

Production Capacity (mbd)

P2B

EM

SA

GP

LloydThermal

CL-G

Bro

wnfie

ld

Kirb

y N

ort

h

Aspen

Horiz

on

Debott

leneck

FC

-H

NL-A

Prim

rose

E

xpan

sion

Cold

Lak

e

Exp

ansi

on

MEG

HSE

CVE

CNQ

IMO

Spot WTI

CS 2018F WTI

Avg. Breakeven

13 April 2017

Canadian Oil & Gas Sector 21

Figure 31: Oil sands operating & sustaining WTI breakeven

Source: CAPP, Credit Suisse estimates

We expect oil sands costs to stay low: For illustration, we show CVE's Christina Lake

operating costs per barrel forward estimates below. With an abundance of gas production

in Western Canada, oil sands producers will continue to benefit from lower gas prices as

an input. For non-energy cash costs, we understand a large portion of cost savings could

be retained given a number of factors including work practices, better reliability, and that

facilities design have structurally improved. For Christina Lake, production ramp up is

expected to continue through 2017-18, bringing the per barrel non-energy op cost down

further with higher productivity and utilization of facilities. Unlike the Permian we don’t

expect another major capex cycle in the Canadian oil sands sector, hence less cost

reflation.

Figure 32: Cenovus - Christina Lake Operating Costs (C$/b)

Source: Company data, Credit Suisse estimates

$0

$20

$40

$60

$80

$100

$120

Q314 Q414 Q115 Q215 Q315 Q415 Q116 Q216 Q316 Q416

US

$/b

SU CVE IMO CNQ WTI

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2014 2015 2016 2017e 2018e

Non-energy ($/boe) Energy ($/boe)

13 April 2017

Canadian Oil & Gas Sector 22

Oil IV: Take-away capacity would move to excess if Keystone happens: The

requirement to use rail to export oil clearly diminishes returns vs pipeline take-away

capacity. Figure 33 shows our supply forecast and the various components of take-away

capacity. The potential sanction of Keystone XL in 2017 and its capacity coming online in

2019 would move the total take-away capacity to excess until the middle of next decade.

Beyond Keystone XL, Enbridges L3R and the TMX pipeline could further extend the

pipeline capacity, keeping take-away in excess through the 2020’s (basis our forecast for

Alberta oil supply growth).

Figure 33: Illustrative Western Canada supply outlook and take-away capacity

Source: Credit Suisse estimates / CAPP

Hence netbacks are set to materially improve post the Keystone XL decision: Figure

34 shows the degree of uplift to the heavy differential should the takeaway capacity move

to excess as a result of the Keystone XL pipeline, adding US$7/bbl in our illustrative

scenario. Compared to our current model of US$14/15 heavy oil differential for 2017/18+,

some widening could occur if more Canadian heavy oil is transported through rail between

now until new pipes come on stream which should then improve the heavy differential.

Figure 34: Illustrative heavy oil differentials scenario

Source: Credit Suisse estimates and CAPP

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

-1,600

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

200

400

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

He

avy

Dif

fere

nti

als

(US$

/b)

Ne

t Su

pp

ly/D

em

and

(m

bd

)

Net Supply/Demand

Heavy Differentials

Heavy Differentials(ex. New Pipe)

Full Pipe Economics to USGC

Full Rail Economics to USGC

13 April 2017

Canadian Oil & Gas Sector 23

Oil V: The exception to the (brownfield) rule: solvent technology: Imperial Oil has

been investing in R&D to develop solvent technology for SAGD production (SA-SAGD).

The use of the solvent reduces the amount of water required in the extraction process, a

major component of the cost. Imperial may sanction its greenfield Aspen project in 2017-

2018 timeframe, subject to regulatory approvals, to develop a 1.3 billion bbl bitumen

resource in two production phases (both with a capacity of 75kb/d).

Figure 35: SA - SAGD image

Figure 36: SA-SAGD and SAGD

comparison

Source: Credit Suisse estimates Source: Credit Suisse estimates

Oil VI: oil sands = long life cash generators: While capital intensive vs conventional oil

production oil sands projects have much longer production profiles vs conventional and

certainly unconventional oil production, as Figure 37 (source Suncor) illustrates.

Figure 37: Oil sands entering the long life free cash flow generating phase

Source: Suncor

13 April 2017

Canadian Oil & Gas Sector 24

Oil 3 key themes:

Keystone XL + other pipes moving to take-away excess: We note that, a year

ago, when we had no clarity on new pipelines, marginal barrels would have to

clear on rail to the U.S. Gulf Coast, pushing heavy differentials wider to

accommodate for more rail economics. Some widening could still occur in 2017-

19 as committed supply continues to ramp up. However, an alternate future is

beginning to shape out wherein heavy oil differentials could narrow meaningfully

toward full pipe economics, with progress now evident on pipelines, especially

with the Keystone Xl approval in the US.

BAT: As a stand-alone proposition BAT would challenge Canadian oil growth, but

we think the potential amelioration of FX shifts and margin benefits from Keystone

XL should also be considered.

ATM: With previously committed large-scale mining projects still ramping up or

set to come on-stream over the next couple of years, oil sands supply continues

to rise rapidly. However, total oil sands capex is set to continue its downward

trajectory, leading to substantial incremental free cash generation for the

Canadian majors such as CNQ, IMO, and SU where return of cash could

accelerate via dividend growth and share buybacks. Going forward, a different

picture emerges – significantly reduced capital intensity with greater focus on in

situ vs. mining, emphasis on debottlenecking of existing facilities and brownfield

development, and deployment of capital-efficient solvent-based technologies.

Figure 38: Oil Sands Capex and Production Outlook with LT ~US$55WTI

Source: CAPP, Credit Suisse estimates

13 April 2017

Canadian Oil & Gas Sector 25

Gas: need those LNG exports…

Canadian Gas – some great rocks, unfortunate timing: CS views the Montney and

Deep basins to hold some of the most economic gas resources in North America, which

along with attractive fiscal terms positions them well. The challenge is the wall of

competitive gas being developed in Canada’s core market – the US. The big hope was for

LNG exports, but the major projects have not eventuated, and the next market window is

two years away, in our opinion. With abundant low cost gas we assume the AECO

differential remains at a similar level (-US$1/mcf vs NYMEX) going forward, but watch for

wildcard outcomes like major LNG project sanctions, more oil sands growth (than

forecast), or other demand growth for example petrochemical additions and the eventual

phase out of coal fired generation in Alberta. Given these dynamics, we prefer liquids rich

gas producers. With challenged gas economics we would expect further consolidation in

the space.

Gas I: some great rocks in the Montney: the Montney play crosses the Alberta / British

Columbia state line. The reservoir thickens toward the Southwest, and becomes more

liquids prone moving to the Northeast. The play has dry gas, liquids rich gas and oil

windows and has been extensively drilled, with ~330 horizontal wells drilled through 2016

(and ~560 put on production in 2016). The reservoir thickness moves up to a maximum of

990 feet.

Figure 39: Montney / Doig cross section

Source: National Energy Board of Canada

13 April 2017

Canadian Oil & Gas Sector 26

Gas II: Western Canada has attractive fiscal terms: In both Alberta and BC the

provincial governments have royalty programs aimed at supporting early drilling /

development, specifically for deep, shale and new wells. Figure 40 shows the application

of BC, Alberta and US fiscal terms to production curves from the Marcellus and Utica area.

The relative advantage is particularly clear in the liquids rich / wet gas plays.

Figure 40: Fiscal terms comparison – economics of Marcellus and Utica wells if

drilled in Western Canada - IRR% update

Source: Credit Suisse estimates – assumes US$50/bbl WTI, US$3/mmBtu NYMEX

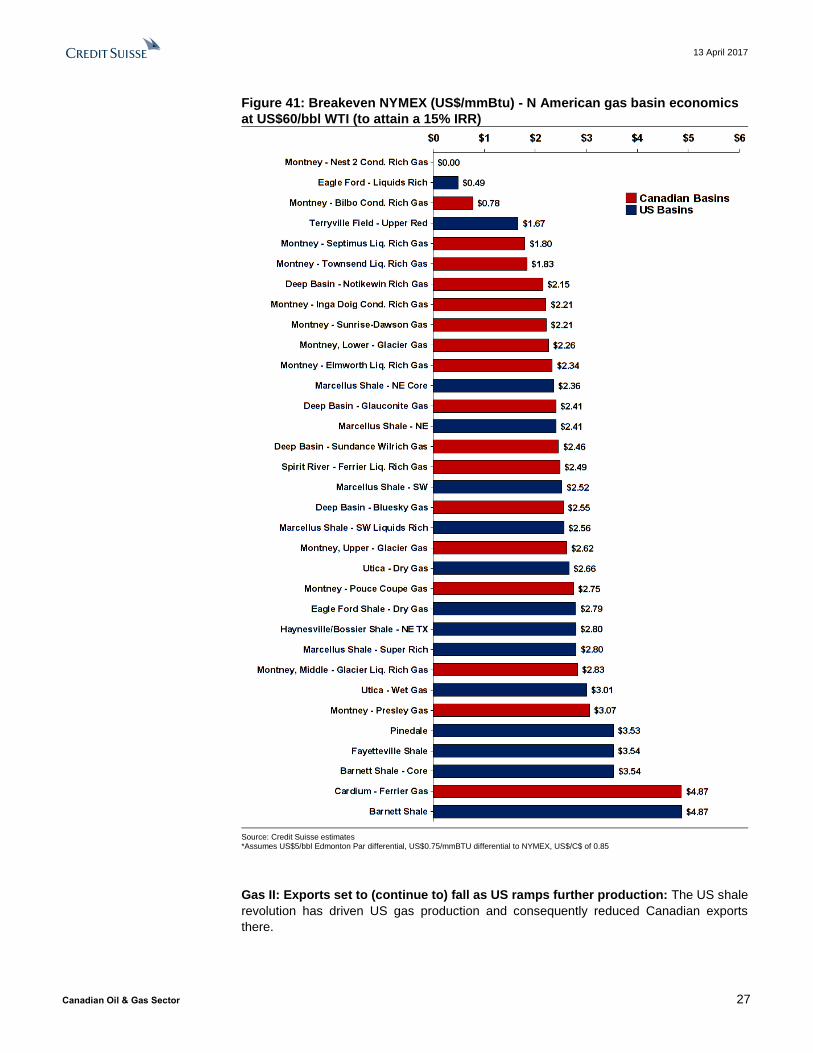

Gas IV: Canadian molecules are competitive in the North American arena: As figure

Figure 41 shows multiple plays in the Montney and Deep Basin are top quartile in terms of

economics in the North American context.

13 April 2017

Canadian Oil & Gas Sector 27

Figure 41: Breakeven NYMEX (US$/mmBtu) - N American gas basin economics

at US$60/bbl WTI (to attain a 15% IRR)

Source: Credit Suisse estimates *Assumes US$5/bbl Edmonton Par differential, US$0.75/mmBTU differential to NYMEX, US$/C$ of 0.85

Gas II: Exports set to (continue to) fall as US ramps further production: The US shale

revolution has driven US gas production and consequently reduced Canadian exports

there.

13 April 2017

Canadian Oil & Gas Sector 28

Figure 42: Supply and Demand Balance, Natural Gas, Reference Case

Source: Canadian National Energy Board

Gas IV: Canadian LNG will likely not save this day: Next demand window 2024: CS

models the next demand window opening in 2024, a consequence of nearly 120MTpa of

new capacity being added in Australia and the US in the latter part of this decade. If our

timing forecast is broadly correct then the next project sanctions are only required in the

2019 window (assuming it takes 5 years to construct new liquefaction capacity – and later

if we assume less time to construct). One of the current discussion points in the LNG

space is the idea that multiple new LNG geographies will augment demand and accelerate

the sanction window. An issue with new LNG geographies is that they will likely require

more of holistic LNG offering, including regas and possibly power being provided as part of

a turnkey solution. Clearly not all LNG developers would have the balance sheet strength,

risk appetite or skill set to develop those new markets.

Figure 43: CS: Global LNG supply / demand balance forecast

Source: Credit Suisse estimates

-30

-20

-10

0

10

20

30

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Excess (shortfall)

MTpa

Construction lag (FID to 1st LNG)

You are here

13 April 2017

Canadian Oil & Gas Sector 29

Canadian LNG – Are all of the major project promoters in the West strongly

engaged?: The Government (Provincial and Federal) appear supportive of LNG exports

becoming a reality for Canada, if the recent approval (albeit with multiple conditions) of the

Pacific NorthWest project is an indication. The reality is that for the 3 large proposals the

project developers may not be fully engaged in sanctioning the projects in the next 12 – 18

month period. Chevron, the Kitimat operator, is likely fully engaged bringing Gorgon,

Angola and Wheatstone to operational stability rather than sanctioning another project

(with no announced sales this far). Shell has said it will sanction 0 – 2 LNG projects at

some point in the future – we would expect a focus on cost reduction rather than a drive

toward sanction will be the focus this year, however the CEO did say at CERA week that a

project sanction may come ‘in a few quarters’. The Pacific Northwest project developers,

led by Petronas as the Operator, are reviewing the cost effect of the additional conditions

applied as a condition for approval. We still wonder if Petronas, holder of 62% of the

project is ready to commit to another major capex requirement when it works to complete

its US$27bn RAPID refining and petrochemical project in Johor Bahru, Malaysia. Our

current working assumption is that the Woodfibre LNG project in Squamish has the

greatest likelihood of sanctioning in the near / mid-term in Canada. This is a 2.1MTpa

facility (circa 0.27bcf/d).

Figure 44: Canada - major LNG export proposals vs current gas exports

Source: Credit Suisse estimates

Canadian LNG – Asia likely still attracted to Canadian supply; it’s all about timing:

We continue to expect that there is a place for Western Canadian molecules in Asia,

bringing a low risk relatively proximal source from a resource focused country – the

question is whether the project pool will be ready to compete in the next market and

sanction window.

The end of the pipe I: Let’s think about US gas supply / demand dynamics: On the

demand side growth continues to come from gas to power switching along with

petrochemical and increasingly going forward LNG international exports along with

increased pipe exports to Mexico. Figure 45 shows our US supply / demand balance to

2018, with LNG ramping to 3.4bcf/d next year and Mexico exports increasing to 5.1bcf/d

that year. On the supply side we forecast the Northeast growing by circa 3bcf/d in both

0

1

2

3

4

5

6

kitimat LNG Shell CanadaLNG

PacificNorthWest

LNG

Jordan CoveLNG

WoodfibreLNG

WesternCanada gas

export

WoodfibreLNG

Bcf/d

13 April 2017

Canadian Oil & Gas Sector 30

2017 and 2018. We also see growth in the gas Permian (1bcf/d both in 17 and 18) as well

as in associated gas production. On the demand side we expect actual demand (i.e. not

exports) to rise circa 2bcf/d in 2018 over 2017. Please see our recent North American gas

price report (report).

Figure 45: US natural gas supply and demand

Source: Company data, Credit Suisse estimates

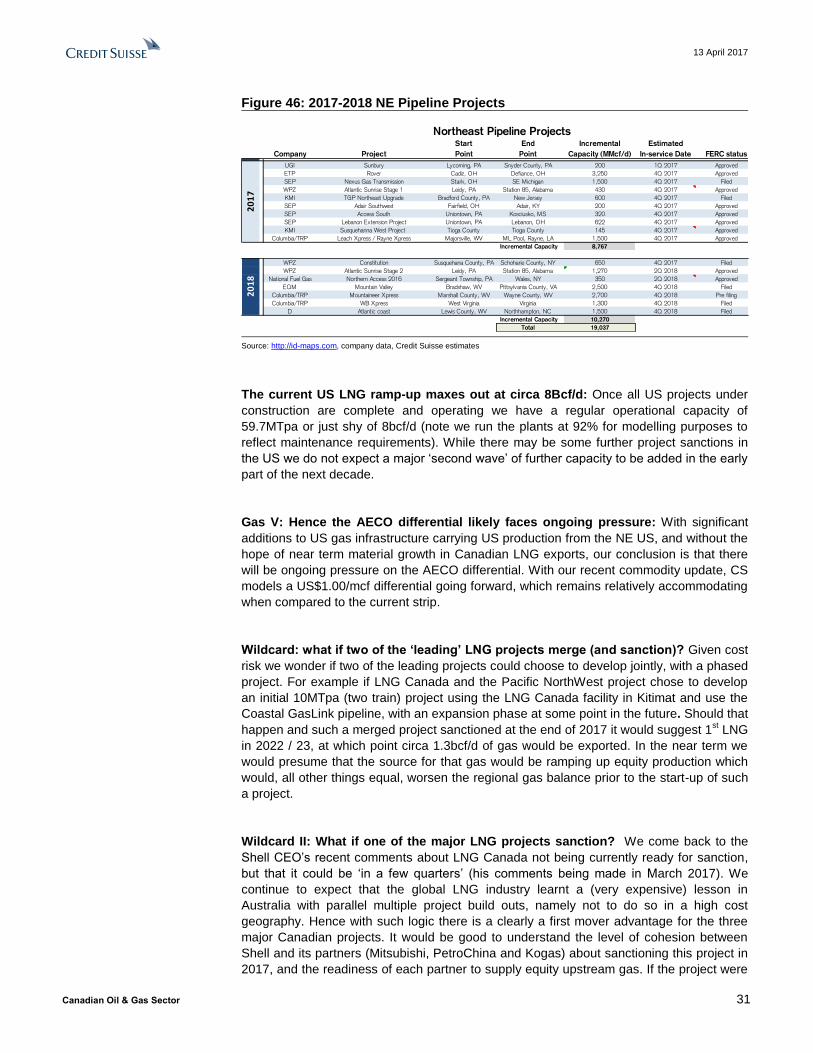

We also see significantly more take-away capacity in the US: Figure 46 shows our

forecast of a ~19bcf/d take-away increase in the 2017 – 2018 timeframe in the NorthEast

US, where we forecast the Northeast take-away capacity to move into excess from Q3

2017, including an increase in access to the Eastern Ontario market from the US

NorthEast.

13 April 2017

Canadian Oil & Gas Sector 31

Figure 46: 2017-2018 NE Pipeline Projects

Source: http://id-maps.com, company data, Credit Suisse estimates

The current US LNG ramp-up maxes out at circa 8Bcf/d: Once all US projects under

construction are complete and operating we have a regular operational capacity of

59.7MTpa or just shy of 8bcf/d (note we run the plants at 92% for modelling purposes to

reflect maintenance requirements). While there may be some further project sanctions in

the US we do not expect a major ‘second wave’ of further capacity to be added in the early

part of the next decade.

Gas V: Hence the AECO differential likely faces ongoing pressure: With significant

additions to US gas infrastructure carrying US production from the NE US, and without the

hope of near term material growth in Canadian LNG exports, our conclusion is that there

will be ongoing pressure on the AECO differential. With our recent commodity update, CS

models a US$1.00/mcf differential going forward, which remains relatively accommodating

when compared to the current strip.

Wildcard: what if two of the ‘leading’ LNG projects merge (and sanction)? Given cost

risk we wonder if two of the leading projects could choose to develop jointly, with a phased

project. For example if LNG Canada and the Pacific NorthWest project chose to develop

an initial 10MTpa (two train) project using the LNG Canada facility in Kitimat and use the

Coastal GasLink pipeline, with an expansion phase at some point in the future. Should that

happen and such a merged project sanctioned at the end of 2017 it would suggest 1st LNG

in 2022 / 23, at which point circa 1.3bcf/d of gas would be exported. In the near term we

would presume that the source for that gas would be ramping up equity production which

would, all other things equal, worsen the regional gas balance prior to the start-up of such

a project.

Wildcard II: What if one of the major LNG projects sanction? We come back to the

Shell CEO’s recent comments about LNG Canada not being currently ready for sanction,

but that it could be ‘in a few quarters’ (his comments being made in March 2017). We

continue to expect that the global LNG industry learnt a (very expensive) lesson in

Australia with parallel multiple project build outs, namely not to do so in a high cost

geography. Hence with such logic there is a clearly a first mover advantage for the three

major Canadian projects. It would be good to understand the level of cohesion between

Shell and its partners (Mitsubishi, PetroChina and Kogas) about sanctioning this project in

2017, and the readiness of each partner to supply equity upstream gas. If the project were

Northeast Pipeline ProjectsStart End Incremental Estimated

Company Project Point Point Capacity (MMcf/d) In-service Date FERC status

UGI Sunbury Lycoming, PA Snyder County, PA 200 1Q 2017 Approved

ETP Rover Cadiz, OH Defiance, OH 3,250 4Q 2017 Approved

SEP Nexus Gas Transmission Stark, OH SE Michigan 1,500 4Q 2017 Filed

WPZ Atlantic Sunrise Stage 1 Leidy, PA Station 85, Alabama 430 4Q 2017 Approved

KMI TGP Northeast Upgrade Bradford County, PA New Jersey 600 4Q 2017 Filed

SEP Adair Southwest Fairfield, OH Adair, KY 200 4Q 2017 Approved

SEP Access South Uniontown, PA Kosciusko, MS 320 4Q 2017 Approved

SEP Lebanon Extension Project Uniontown, PA Lebanon, OH 622 4Q 2017 Approved

KMI Susquehanna West Project Tioga County Tioga County 145 4Q 2017 Approved

Columbia/TRP Leach Xpress / Rayne Xpress Majorsville, WV ML Pool, Rayne, LA 1,500 4Q 2017 Approved

Incremental Capacity 8,767

WPZ Constitution Susquehana County, PA Schoharie County, NY 650 4Q 2017 Filed

WPZ Atlantic Sunrise Stage 2 Leidy, PA Station 85, Alabama 1,270 2Q 2018 Approved

National Fuel Gas Northern Access 2016 Sergeant Township, PA Wales, NY 350 2Q 2018 Approved

EQM Mountain Valley Bradshaw, WV Pittsylvania County, VA 2,500 4Q 2018 Filed

Columbia/TRP Mountaineer Xpress Marshall County, WV Wayne County, WV 2,700 4Q 2018 Pre filing

Columbia/TRP WB Xpress West Virginia Virginia 1,300 4Q 2018 Filed

D Atlantic coast Lewis County, WV Northhampton, NC 1,500 4Q 2018 Filed

Incremental Capacity 10,270

Total 19,037

20

17

20

18

13 April 2017

Canadian Oil & Gas Sector 32

to sanction it would, once completed, require 12MTpa or 1.6bcf/d of gas which we would

expect to have a positive effect on the AECO differential.

Wildcard III – further pipeline take-away capacity added: We assume that the recent

1.5bcf/d mainline open bid is largely a roll-over of existing use on the line, but with a lot of

spare capacity (mainline has run at circa 8bcf/d, but is now running at circa 4bcf/d) there is

further take-away capacity opportunity on mainline – the question is at what price. A

significant proportion of the spare capacity is earmarked for the Energy East oil pipeline

project, as yet unsanctioned, but with a plan to convert the second pipe to an oil pipeline.

The North Montney mainline has now been re-proposed as a 1.5bcf/d pipe linking to

AECO, and thence beyond, with off-takers already lined up. One scenario is that the line

capacity is increased (it was originally designed as a 3.5bcf/d pipe). The Alliance pipeline,

carrying to the Chicago hub has proposed an additional 0.5bcf/d, currently seeking

expressions of interest with a potential start date (for the additional capacity) of Q4 2020.

Given our view that certain plays in the WCSB can compete with US gas additional reach

could have a positive effect on the AECO differential.

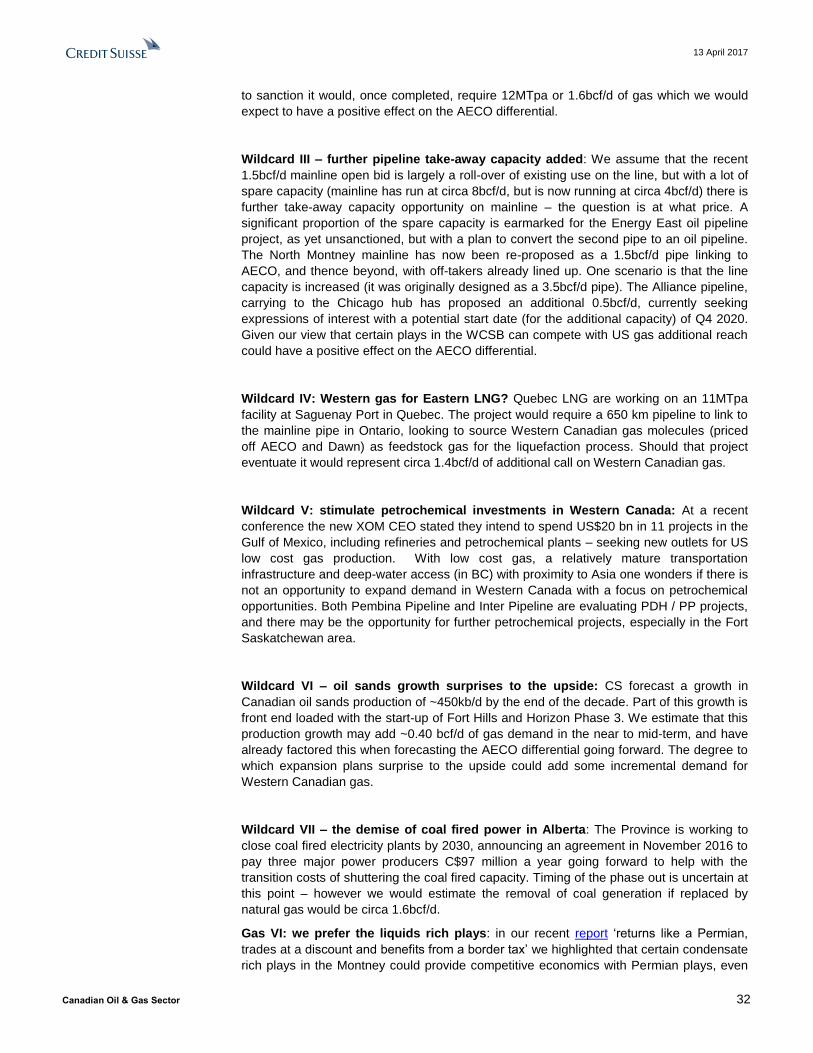

Wildcard IV: Western gas for Eastern LNG? Quebec LNG are working on an 11MTpa

facility at Saguenay Port in Quebec. The project would require a 650 km pipeline to link to

the mainline pipe in Ontario, looking to source Western Canadian gas molecules (priced

off AECO and Dawn) as feedstock gas for the liquefaction process. Should that project

eventuate it would represent circa 1.4bcf/d of additional call on Western Canadian gas.

Wildcard V: stimulate petrochemical investments in Western Canada: At a recent

conference the new XOM CEO stated they intend to spend US$20 bn in 11 projects in the

Gulf of Mexico, including refineries and petrochemical plants – seeking new outlets for US

low cost gas production. With low cost gas, a relatively mature transportation

infrastructure and deep-water access (in BC) with proximity to Asia one wonders if there is

not an opportunity to expand demand in Western Canada with a focus on petrochemical

opportunities. Both Pembina Pipeline and Inter Pipeline are evaluating PDH / PP projects,

and there may be the opportunity for further petrochemical projects, especially in the Fort

Saskatchewan area.

Wildcard VI – oil sands growth surprises to the upside: CS forecast a growth in

Canadian oil sands production of ~450kb/d by the end of the decade. Part of this growth is

front end loaded with the start-up of Fort Hills and Horizon Phase 3. We estimate that this

production growth may add ~0.40 bcf/d of gas demand in the near to mid-term, and have

already factored this when forecasting the AECO differential going forward. The degree to

which expansion plans surprise to the upside could add some incremental demand for

Western Canadian gas.

Wildcard VII – the demise of coal fired power in Alberta: The Province is working to

close coal fired electricity plants by 2030, announcing an agreement in November 2016 to

pay three major power producers C$97 million a year going forward to help with the

transition costs of shuttering the coal fired capacity. Timing of the phase out is uncertain at

this point – however we would estimate the removal of coal generation if replaced by

natural gas would be circa 1.6bcf/d.

Gas VI: we prefer the liquids rich plays: in our recent report ‘returns like a Permian,

trades at a discount and benefits from a border tax’ we highlighted that certain condensate

rich plays in the Montney could provide competitive economics with Permian plays, even

13 April 2017

Canadian Oil & Gas Sector 33

taking into consideration a wide AECO differential (US$1/ mmBtu), with for example Seven

Generations Nest 2 play making a 15% IRR at circa US$30/bbl, and NuVista’s Bilbo play

in the Montney at less than US$40/bbl. Condensate will likely continue to be a premium

product in Canada, given its use as a diluent in the oil sands. Additionally, both companies

continue to reduce their cost structure while improving their well performance, which

should continue to drive improving economic returns moving forward.

Gas VII: Hard times drive consolidation: We have argued before that a combination of

factors may drive consolidation in Western Canada that favors larger companies,

including:

- The Montney is a large resource, and therefore it should generally gravitate to

companies with a large balance sheet over time

- Widening basis differentials, coupled with limited infrastructure, may place greater

pressure on lesser capitalized companies

- Pipeline companies are increasingly asking for longer term contracts, and less

capitalized companies may not have the necessary credit profile to commit to longer term

contracts

- Larger scale companies with existing infrastructure may have a competitive

advantage over time

Gas 3 key themes:

Great rocks

But excess gas supply which LNG won’t fix in the short term

Favour liquids rich players, watch for consolidation

Infrastructure / Pipeline:

Canadian Mainline: As one may expect, the Canadian Mainline's ongoing rate base

erosion reflects several factors, including pipeline age along with original capital cost,

changing natural gas flows, competitive pipelines, and capital allocation decisions

reflecting available returns. In light of these factors, there should be no surprise about the

System's declining throughput appearing in Figure 47. It is important to note that the

mainline has run at 8bcf/d transmission – there is certainly capacity that could be used

going forward, although the second pipe could be converted to an oil pipeline as part of

the Energy East pipeline proposal.

13 April 2017

Canadian Oil & Gas Sector 34

Figure 47: Selected Historical Natural Gas Volume Throughputs

Note Before 2007, Canadian Mainline’s throughput volumes in the above table reflect physical deliveries to domestic and export markets. Throughput volumes reported in previous years reflected contract deliveries. However, customer contracting patterns have changed in recent years making physical deliveries a better measure of system utilization. Source: Company data.

In relation to pipeline access options, TransCanada recently announced and concluded an

open season for the Canadian Mainline. This revised open season followed an originally

failed attempt to secure longer-term shippers in late 2016. The new binding open season

for the Dawn Long Term Fixed Price Service (LTFP) was centered around a changed

tolling structure. Very simply, the tolling structure was changed with the toll being set at

C$0.77/GJ/d on a ten-year term with a sliding schedule of tolls for more reduced service

terms as appears in Figure 48.

Figure 48: TRP's Mainline Fixed Price Service Open Season

Source: Company data.

TransCanada sought and secured interest for 1.5 PJ/d of commitments from the open

season. Versus other offerings, TRP's newly proposed tolls are extremely competitive.

Yet, that toll competitiveness is only one factor to consider for producers, purchasers, and

shippers. On a fundamental basis, TRP's Mainline should best be considered as a multi-

region system with a Western leg, the Northern Ontario system, and the Eastern Triangle

portion as appears in Figure 49.

0

2

4

6

8

10

12

14

Do

me

sti

c &

Ex

po

rt V

olu

me

(b

cf/

d)

NGTL System Canadian Mainline ANR

13 April 2017

Canadian Oil & Gas Sector 35

Figure 49: Canadian Mainline

Source: Company data.

The dynamics associated with natural gas shipments are rather complex, with a significant

captive load along the Western and Northern Ontario systems (power generation, natural

gas distribution utilities, and industrials). For additional perspective, please refer to our

note from September 12th, titled, "Western Canadian Natural Gas: Diving into Western

Canada Gas Production Trends and Other Topics".

The relative basin competitiveness is a critical consideration for accessing the longer-term

potential of the western Canadian resource. The prime threat for that resource tends to

come from the Marcellus and Utica basins that are geographically much closer to Western

Canada's traditional end markets of Ontario and Quebec. Yet, relative returns and pipeline

costs and existing connectivity versus prospective connectivity provide some advantages

to the incumbent positioning.

Quebec LNG (1.4bcf/d) plans to source Western Canadian gas: The project, in

Saguenay, uses 11MTpa as its design capacity (circa 1.4bcf/d). It plans to use an as yet

unconstructed 650km pipe to link to the mainline, bring Western Canadian gas to the East

and thence for export as LNG. Clearly should such a project materialize it would be a

material shift in the gas balance.

13 April 2017

Canadian Oil & Gas Sector 36

Figure 50: Quebec LNG plans on using Western Canadian gas

Source: Quebec LNG project presentation May 2015

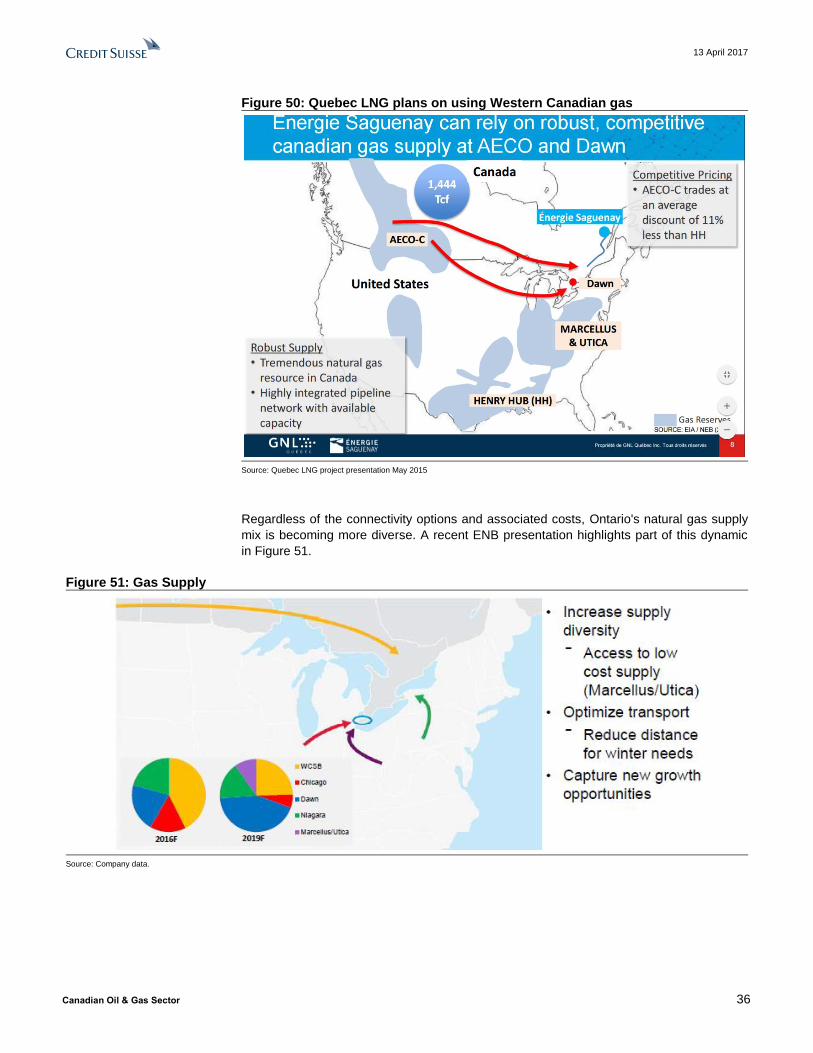

Regardless of the connectivity options and associated costs, Ontario's natural gas supply

mix is becoming more diverse. A recent ENB presentation highlights part of this dynamic

in Figure 51.

Figure 51: Gas Supply

Source: Company data.

13 April 2017

Canadian Oil & Gas Sector 37

North Montney Mainline Project: Originally designed as a 3.5bcf/d pipeline that would

partially serve the proposed Petronas operated PacificNorthWest LNG project in Prince

Rupert. As part of the original application a clause required that LNG project to take FID as

a condition precedent to developing the North Montney mainline pipeline. In March

TransCanada announced it has secured approximately 1.5bcf/d of long term (20 year)

contracts – half of which with Progress Energy (owned by Petronas). As part of the project

redesign TransCanada filed a variance application with the National Energy Board to

remove the LNG FID requirement. The line will increase the reach of the producers to the

AECO hub and beyond. We would not be surprised that the capacity could be uprated

should the PNW LNG project sanction at some point in the future.

13 April 2017

Canadian Oil & Gas Sector 38

Stocks: Stocks: new metric to look for potential outliers, both in Canada and across North

America: We segregate into two universes – SMID and large cap, focus on Canada

initially and then NA as a whole. We use 4 metrics (production growth, operating

margin/boe, D/CF and yield) to ‘score’ each stock and then use that score to compare an

implied 2018 EBITDA multiple for that universe to our current forecast – seeking outliers.

In the SMID space in Canada we prefer VII and NVA and in the US PE and EGN. For the

North America large cap universe we prefer SU and ECA in Canada and PXD, CXO and

DVN in the US. Finally looking at global majors SU again stands out as does RDS and BP

in Europe.

Let’s start in Canada with the SMID universe: We have four screens on our dashboard

for the Canadian universe, namely 2018 over 2017 production growth, 2018 operating

margin / BoE (CSE), 2018 D/CF (CSE) and 2018 dividend yield (CSE). With a

conservative view on AECO differentials we prefer the condensate rich plays, or those that

have flat out superior production costs to defend netback per boe.

Figure 52: Canadian SMID – 18 over 17 Prod’n

growth Figure 53: Canadian SMID – Operating margin- BoE

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 54:Canadian SMID 2018 D/CF Figure 55: Canadian SMID – 2018 Dividend yield

Source: Credit Suisse estimates Source: Credit Suisse estimates

13 April 2017

Canadian Oil & Gas Sector 39

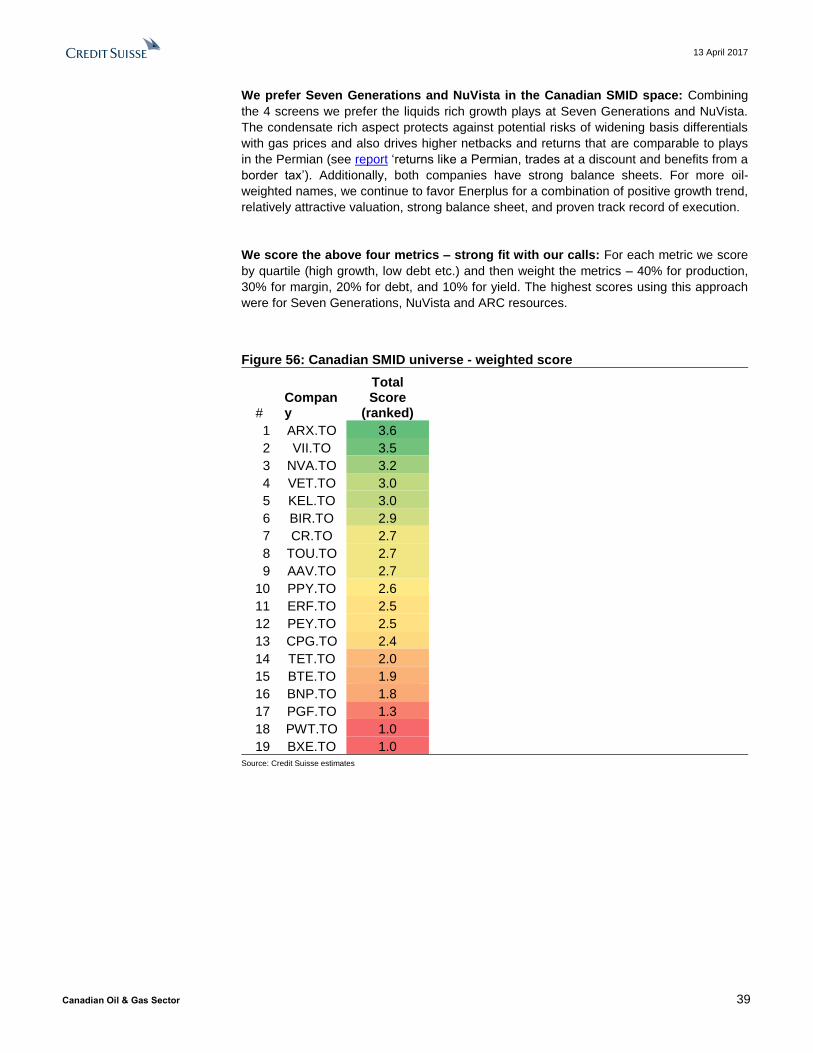

We prefer Seven Generations and NuVista in the Canadian SMID space: Combining

the 4 screens we prefer the liquids rich growth plays at Seven Generations and NuVista.

The condensate rich aspect protects against potential risks of widening basis differentials

with gas prices and also drives higher netbacks and returns that are comparable to plays

in the Permian (see report ‘returns like a Permian, trades at a discount and benefits from a

border tax’). Additionally, both companies have strong balance sheets. For more oil-

weighted names, we continue to favor Enerplus for a combination of positive growth trend,

relatively attractive valuation, strong balance sheet, and proven track record of execution.

We score the above four metrics – strong fit with our calls: For each metric we score

by quartile (high growth, low debt etc.) and then weight the metrics – 40% for production,

30% for margin, 20% for debt, and 10% for yield. The highest scores using this approach

were for Seven Generations, NuVista and ARC resources.

Figure 56: Canadian SMID universe - weighted score

# Company

Total Score

(ranked)

1 ARX.TO 3.6

2 VII.TO 3.5

3 NVA.TO 3.2

4 VET.TO 3.0

5 KEL.TO 3.0

6 BIR.TO 2.9

7 CR.TO 2.7

8 TOU.TO 2.7

9 AAV.TO 2.7

10 PPY.TO 2.6

11 ERF.TO 2.5

12 PEY.TO 2.5

13 CPG.TO 2.4

14 TET.TO 2.0

15 BTE.TO 1.9

16 BNP.TO 1.8

17 PGF.TO 1.3

18 PWT.TO 1.0

19 BXE.TO 1.0

Source: Credit Suisse estimates

13 April 2017

Canadian Oil & Gas Sector 40

Figure 57: Canadian SMID E&P upside / downside at CS deck and strip

Source: Credit Suisse estimates

Moving to Canadian oil sands / majors: We use the same screens as the SMID

universe, however we change the weightings, namely 20% for production growth, 30% for

margin, 30% for debt, and 20% for yield.

AAV.TO

BXE.TO

BIR.TO

BNP.TO

CR.TO

KEL.TO

NVA.TO

PPY.TO

POU.TO

PEY.TO

VII.TO

TOU.TO

TET.TO

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

-20% -10% 0% 10% 20% 30% 40%

% U

psid

e / D

ow

nsid

e a

t S

trip

% Upside / Downside at CS Deck

OUTPERFORMNEUTRAL UNDERPERFORM

13 April 2017

Canadian Oil & Gas Sector 41

Figure 58: Canadian majors – 18 over 17 Prod’n

growth

Figure 59: Canadian majors – Operating margin-

BoE

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 60: Canadian majors: 2018 D/CF Figure 61: Canadian majors: 2018 Dividend yield

Source: Credit Suisse estimates Source: Credit Suisse estimates

In the Canadian majors space we prefer Suncor: basis a combination of improving FCF

post major capex cycles, resilient cash costs (and less risk of cost in or reflation vs US

shale plays). With previously committed large-scale mining projects still ramping up or set

to come on-stream over the next couple of years, oil sands supply continues to rise

rapidly. However, total oil sands capex is set to continue its downward trajectory, leading

to substantial free cash generation for the Canadian majors such as CNQ, IMO, and SU

where return of cash could accelerate via dividend growth and share buybacks. Moreover,

SU/IMO and CNQ will benefit over time from a number of regional synergies and cost

opportunities from the consolidation of Syncrude and AOSP, respectively.

Figure 62: Canadian large cap weighted score

# Company

Total Score

(ranked)

1 SU.TO 3.6

2 HSE.TO 2.6

3 IMO.TO 2.2

4 ECA 1.9

5 CNQ.TO 1.6

13 April 2017

Canadian Oil & Gas Sector 42

Source: Credit Suisse estimates

So on a Canada wide basis we prefer Suncor, 7 Gen’s and Encana: Seven

Generations and Encana are our preferred names in the E&P space. Additionally, we

believe Canadian majors continue to screen well relative to the multinationals, including

Imperial Oil and CNRL. We remain concerned on Pengrowth and Penn West due to

relatively weaker fundamentals.

We like spreadsheets – so we created a tool to try and ‘score’ potentially mispriced

stocks: We use the same 4 screening metrics namely production growth (’18 over ‘17

CSe), 2018 operating margin / boe (CSe), D/CF (2018) and dividend yield. We then grade

each stock into a quartile for each metric. We then weight each metric – for the Canadian

O&G universe we applied 30% for Operating margin/boe, D/CF, production growth and

10% for yield and applied those weightings to produce an overall score. We then apply a Z

score vs the median 2018 EV/EBITDA and use that to generate an implied EV/EBITDA

multiple to compare against our forecast. It should be stressed that this is not being used

as a valuation tool, but rather to look for potential outliers basis the 4 variables used within

that defined universe.

Figure 63: CS Canadian universe - forecast vs

scored implied 2018 EV / EBITDA

Figure 64: CS Canadian universe - forecast vs

scored implied 2018 EV / EBITDA difference

Source: Credit Suisse estimates Source: Credit Suisse estimates

Gran Tierra and Parex have the highest implied difference: Parex and Gran Tierra

both screen favorably given their high growth, oil focused operations in Colombia. While

both companies are rated Outperform with balance sheets that are essentially debt free,

the portfolios and execution to date are relatively different. Parex's assets are generally

located in established basins in the center of Colombia where there has historically been

less surface risks, security and otherwise, and long term execution has been exceptional

and has resulted in a premium valuation. Gran Tierra has undergone a transition in the

management team and portfolio in recent years, and is currently centered in the Putumayo

basin and Middle Magdalena basin. Execution to date has been somewhat more

challenging as the Putumayo has been an area of greater surface risks, although we

expect it to improve moving forward after a successful peace process.

13 April 2017

Canadian Oil & Gas Sector 43

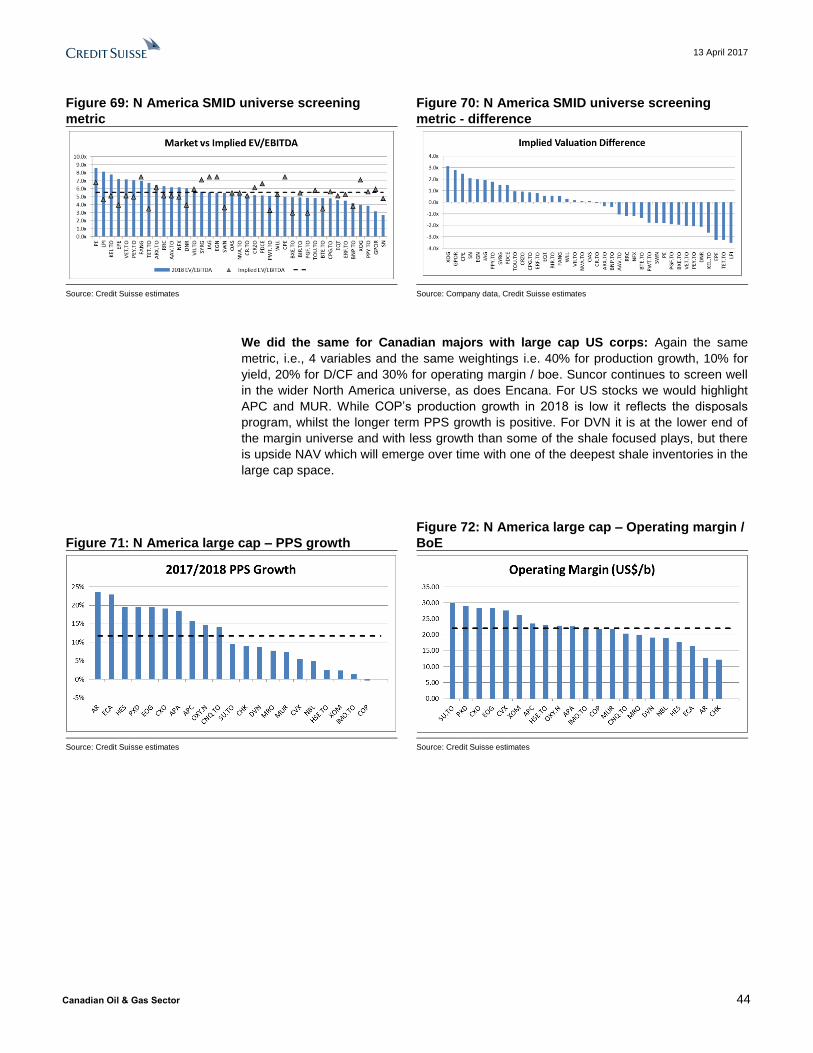

Zooming out to a North American view

For North American SMID plays we use the same metric to look for possible

dislocations. We use the same 4 screening metrics as described above namely

production growth (’18 over ‘17 CSe), 2018 operating margin / boe (CSe), D/CF (2018)

and dividend yield – but we apply different weightings, increasing production growth to

40%, reducing return to 10% and D/CF to 20%. In Canada Tourmaline, Painted Pony and

to a lesser degree Seven Generations score well in the broader universe, while in the US

XOG and Gulfport screen well.

Figure 65: N America SMID 18 over 17 Prod’n

growth Figure 66: N America SMID – operating margin BoE

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 67: N American SMID: 2018 D/CF Figure 68: N American SMID: 2018 Dividend yield

Source: Credit Suisse estimates Source: Credit Suisse estimates

13 April 2017

Canadian Oil & Gas Sector 44

Figure 69: N America SMID universe screening

metric

Figure 70: N America SMID universe screening

metric - difference

Source: Credit Suisse estimates Source: Company data, Credit Suisse estimates