Canadian L’Institut Institute canadien of des Actuaries...

41

2007 General Meeting Assemblée générale 2007 Montréal, Québec Canadian Institute of Actuaries L’Institut canadien des actuaires

Transcript of Canadian L’Institut Institute canadien of des Actuaries...

2007 General MeetingAssemblée générale 2007

Montréal, Québec

Canadian Institute

of Actuaries

L’Institutcanadiendesactuaires

IFRS Developments and Product Specific Challenges

Dan Doyle, FCIA Partner

PricewaterhouseCoopers LLP

Tim Deacon CA, CPA Vice President – Int’l Accounting & Policy

Manulife Financial

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

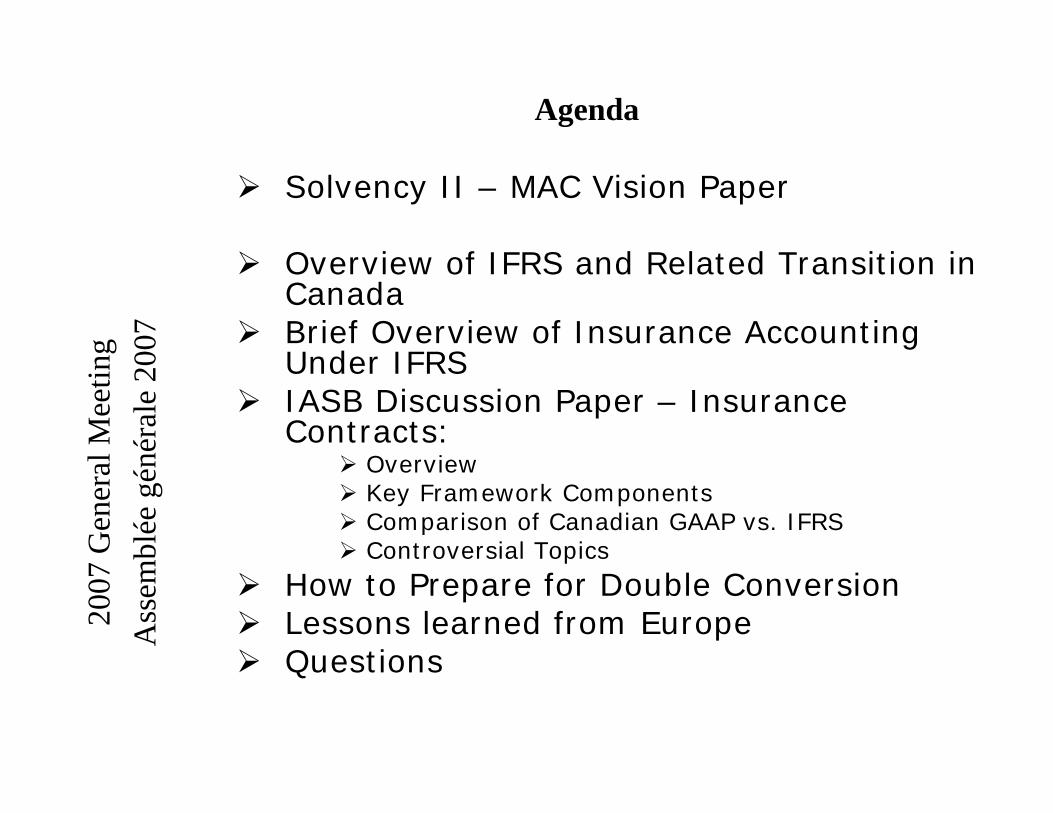

07Agenda

Solvency II – MAC Vision Paper

Overview of IFRS and Related Transition in CanadaBrief Overview of Insurance Accounting Under IFRSIASB Discussion Paper – Insurance Contracts:

OverviewKey Framework ComponentsComparison of Canadian GAAP vs. IFRSControversial Topics

How to Prepare for Double ConversionLessons learned from EuropeQuestions

12/7/2007 4

Solvency II and Economic Capital

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Regulatory/Economic Capital

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07MCCSR- Current

• Factor Based • No Correlation

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

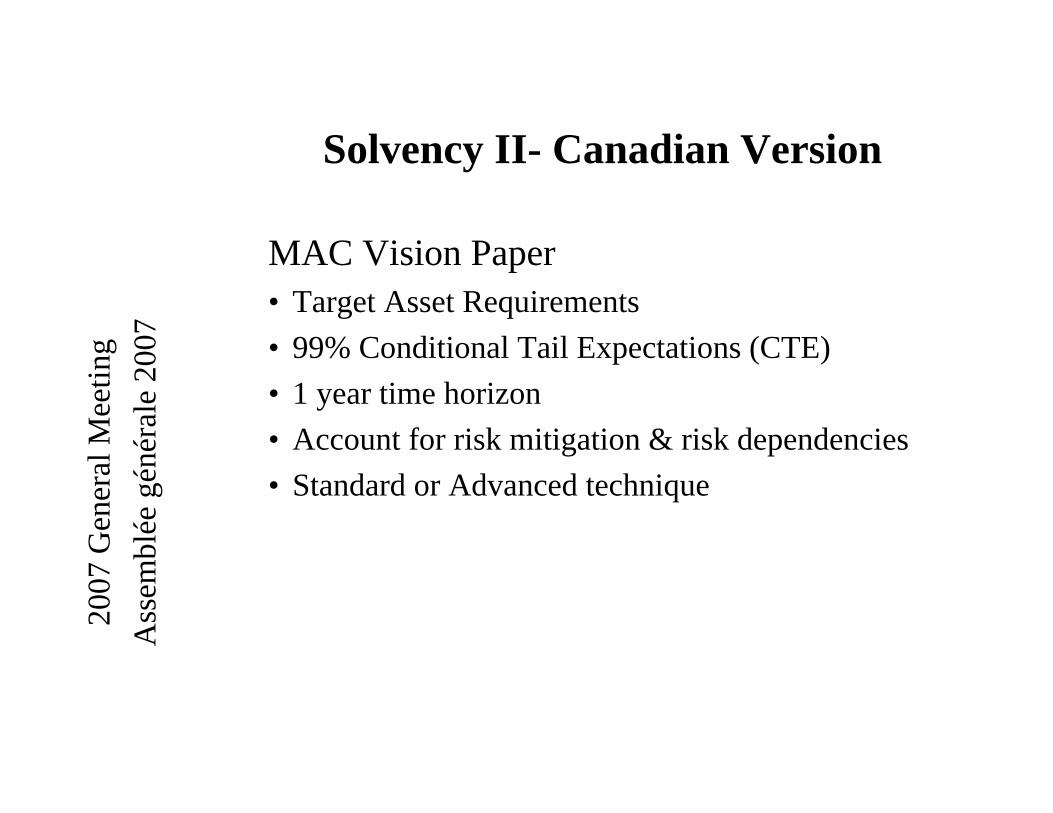

07Solvency II- Canadian Version

• MCCSR Advisory Committee (MAC) Vision Paper

• Principle based• Integrated asset Total Balance Sheet (TBS)• Two levels of capital

– Minimum– Target

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Required capital to be determined indirectly:

Required = Total Asset - Reported GAAP Capital Requirement Liabilities

Assets Liabilities & Capital

solvencybuffer

expected asset requirement

margins

required capital

CGAAP policy liabilities

best estimate policy liability

total asset requirement

Solvency IIFocus on Total Asset Requirement

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Solvency II- Canadian Version

MAC Vision Paper• Target Asset Requirements• 99% Conditional Tail Expectations (CTE)• 1 year time horizon • Account for risk mitigation & risk dependencies• Standard or Advanced technique

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Risk Classification

Insurance Risks

Credit Risks

Total Risk

Market Risks

Interest Rates

Equity

FX

Real Estate

Alt Invest.

Concentration

Model

Migration

Reinsurers

Concentration

Model

Operational Risks

qualitatively

Financial Risks

quantitatively

Liquidity Risks

Group Risks

Regulatory Risks

Group Behavior Risk

Capital Mobility

Group Internal Risk

Spreads

Shares

Defaults P&C

Premium Risk

Reserve Risk

Small Claims

Large Claims

Catastrophes

Life

Biometric

Policyholder

Mortality

Longevity

Morbidity

Reactivation

Lapse

Other options

Cost

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Economic Capital

• “Sufficient surplus to cover potential losses at a given tolerance level over a specified time horizon”

• Looks like Solvency II – Canada– 99% CTE – 1 Year– Terminal provisions

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Banks - Basel lI

• Banks have already developed EC/RC models• Expertise in a model building and stochastic

processes exist

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Bank Lessons• Lack of data to develop some correlations• Correlations behave differently under stress• OSFI will defer full benefits• Timelines are significant• Evolving process

12/7/2007 14

IFRS

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Overview of IFRS

International Financial Reporting Standards (IFRS) are a set of global accounting principles set by the International Accounting Standards Board (IASB).

More than 100 countries and most of the major stock exchanges (outside US) have mandated the use of IFRS for public companies.

Many global peers already report under IFRS.

Foreign subsidiaries (i.e. HK and Singapore) may already report under IFRS for local statutory purposes.

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Transition to IFRS in Canada

• Migration to IFRS over next 4 years – 2011 expected implementation date

• Final CICA transition plan to be released by March 2008

• Numerous moving parts - need to watch the horizon:– Insurance contracts standard (double conversion)– Number of current IASB projects (derecognition,

consolidation of VIE’s) will change existing standards

– Joint FASB projects (Memorandum of Understanding)

– CICA “Migration” plan

• SEC rule to eliminate US GAAP reconciliation for foreign private issuers that file financial statements under IFRS.

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Transition to IFRS in CanadaKey Milestones

Disclose IFRS convergence plan including quantification of anticipated effectsandOpening Balance Sheet under IFRS (Jan 1, 2010)

Dec 31-08 Dec 31-09 Dec 31-10 Mar 31-11 Dec 31-11

Disclose IFRSconvergence plan and anticipated effects

First quarterly IFRS-based financial statementsandFirst OSFI Filing under IFRS

First annual IFRS-based financial statements

January 1, 2011 changeover to

IFRS

First comparative figures under IFRS

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Very limited guidance for insurance contracts available under current IFRS.

IFRS 4 – “Insurance Contracts” permits entities to retain previous basis of accounting (i.e. CALM) for contracts that are within scope.

If a contract is not in scope, an entity must follow other IFRS guidance (i.e. IAS 39).

IFRS 4 currently under revision – IASB issued Discussion Paper on recognition and measurement of insurance contracts – proposing use of “current exit value”

Brief Overview of Insurance Accounting Under IFRS (Pre Discussion Paper)

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Brief Overview of Insurance Accounting Under IFRS

IFRS 4 has limited scope but does contain the following:

Definition of an insurance contract

Prohibits recognition of catastrophe and equalization provisions

Prescribes a liability adequacy test

Permits (not requires) unbundling and shadow accounting

Reinsurance balances (I/S and B/S) must be shown on gross basis

Addresses discretionary participation features

Embedded derivatives

Increased disclosure requirements

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Insurance contract - ‘contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.’

Brief Overview of Insurance Accounting Under IFRS – Some Definitions

“Insurance risk is significant if, and only if, an insured event could cause an insurer to pay significant additional benefits in any scenario, excluding scenarios that lack commercial substance

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Does the contract need to be unbundled?

Are any discretionary participation features

present?

Insurance Component Deposit Component

Yes YesNo

Does contract contain significant

insurance risk?

Investment Contract(IAS 39)

Investment Contract with discretionary participation

features

Insurance Contract

No

NoYes

Brief Overview of Insurance Accounting Under IFRS – Product Classification Flowchart

Use CALM Amortized Cost or FVLiability or equity

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

• Under IAS 39, Deferred Acquisition Costs must be expensed unless:

• Amortized cost method used for valuing liability:– “Transaction Costs” must be incremental and directly

attributable and does not include internal allocation of administrative expenses or allocation of overheads.

– Effectively non-commission expenses are likely to be expensed unless they wouldn’t have been incurred if the contract was not issued.

• Relate to securing right to receive Investment Mgmt fees:– Capitalised as an intangible asset representing the right to

receive this revenue if can separately be measured.– Asset is amortized as entity provides the services and

recognizes related revenue.

• Difference to existing CGAAP and US GAAP.

Brief Overview of Insurance Accounting Under IFRS –Deferred Acquisition Costs

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

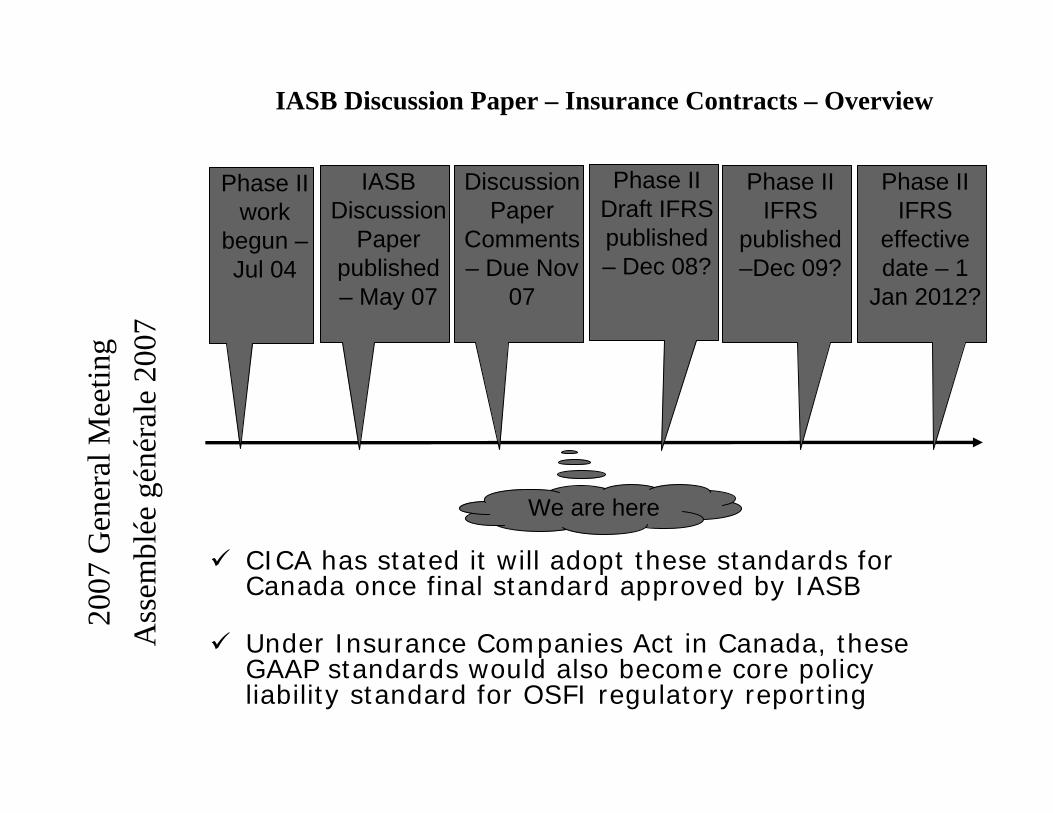

07IASB Discussion Paper – Insurance Contracts – Overview

CICA has stated it will adopt these standards for Canada once final standard approved by IASB

Under Insurance Companies Act in Canada, these GAAP standards would also become core policy liability standard for OSFI regulatory reporting

Phase II work

begun –Jul 04

IASB Discussion

Paper published – May 07

Phase II Draft IFRS published – Dec 08?

Phase II IFRS

published –Dec 09?

Phase II IFRS

effective date – 1

Jan 2012?

We are here

Discussion Paper

Comments – Due Nov

07

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

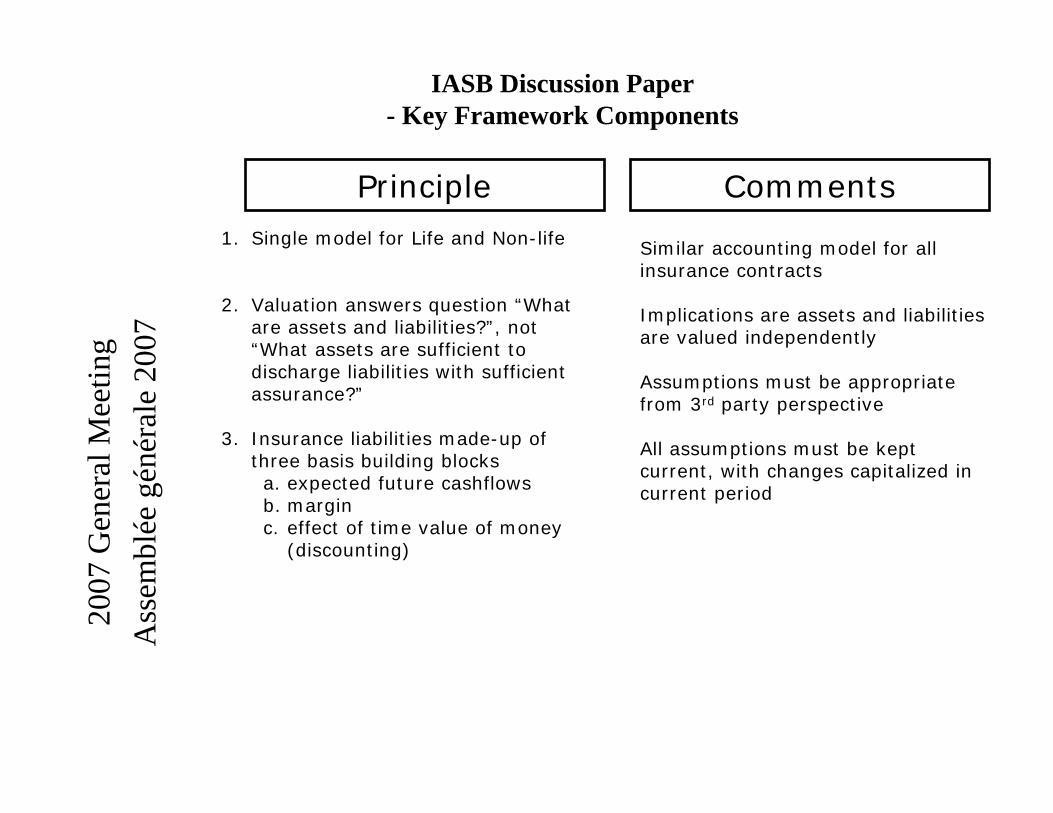

IASB Discussion Paper- Key Framework Components

Principle Comments1. Single model for Life and Non-life

2. Valuation answers question “What are assets and liabilities?”, not “What assets are sufficient to discharge liabilities with sufficient assurance?”

3. Insurance liabilities made-up of three basis building blocksa. expected future cashflowsb. marginc. effect of time value of money

(discounting)

Similar accounting model for all insurance contracts

Implications are assets and liabilities are valued independently

Assumptions must be appropriate from 3rd party perspective

All assumptions must be kept current, with changes capitalized in current period

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

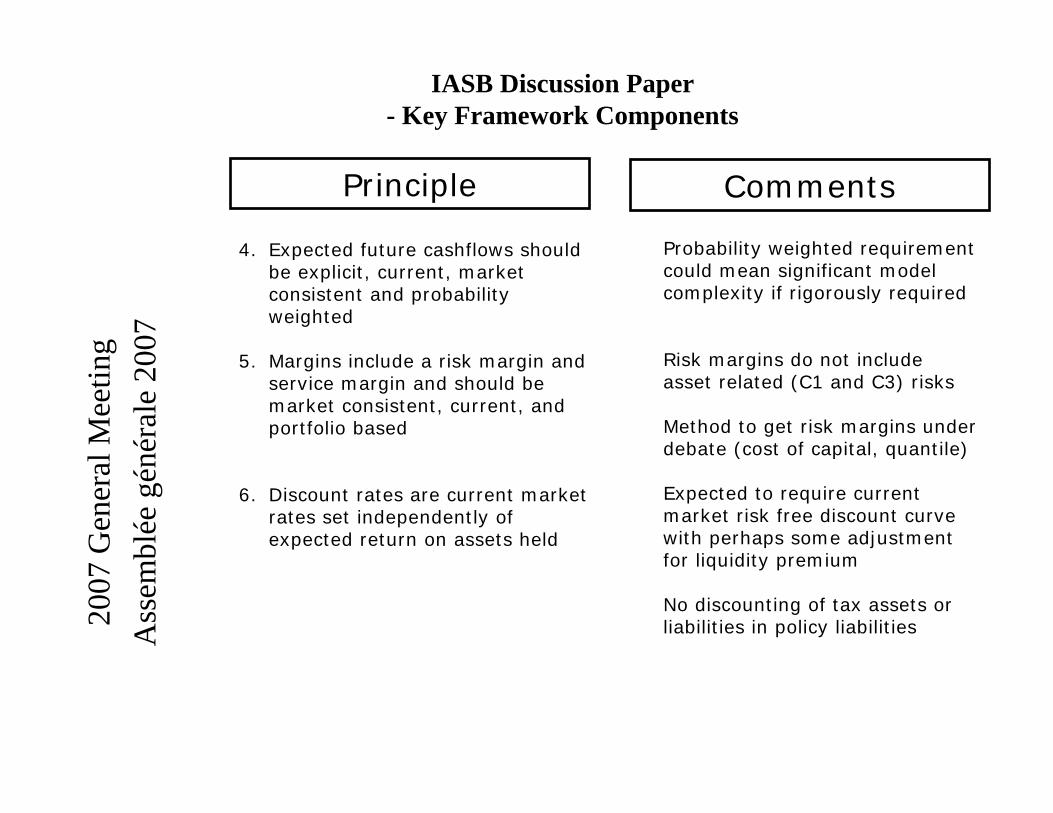

IASB Discussion Paper - Key Framework Components

Principle Comments

4. Expected future cashflows should be explicit, current, market consistent and probability weighted

5. Margins include a risk margin and service margin and should be market consistent, current, and portfolio based

6. Discount rates are current market rates set independently of expected return on assets held

Probability weighted requirement could mean significant model complexity if rigorously required

Risk margins do not include asset related (C1 and C3) risks

Method to get risk margins under debate (cost of capital, quantile)

Expected to require current market risk free discount curve with perhaps some adjustment for liquidity premium

No discounting of tax assets or liabilities in policy liabilities

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Key Framework Components

Principle Comments

7. All assumptions, margins and discount rates must be kept current with impact of changes capitalized in current period

8. Gain/Loss permitted at contract inception

9. Acquisition expenses expensed immediately but offset by implicit liability reduction

10. Contracts valued over term to which insured has guaranteed insurability

11. Contractual cashflows include future premiums required to keep contract in-force

Approach described as “current exit value”under which valuation is intended to be consistent with cashflows/assumptions that a transferee would use in acquiring the block

Practically, would expect a high hurdle to recognize profit at issue

No explicit DAC assetLiability reduction from margins in premium/revenue capitalized in reserve

Term for valuation ends at point at which insurer can cancel contract or adjust it in unconstrained way, unless extending term increases the liability

May not be all expected premiums, but just the minimums to keep policy in-force if there is a significant discretionary element (e.g. UL)

Liability reduction from margins in premium/revenue capitalized in reserve

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Key Framework Components

Principle Comments

12. Participation features (e.g. dividends) reflected only to extent there is a legal or constructive obligation to pay the dividends

13. Insurer own credit standing to be reflected in liability valuation

Definition of constructive obligation not yet clear – may be very restrictiveSame issue applies to adjustable contract elements such as credited interest rates

Theoretically, value of liabilities reducedas company credit standing reduced – not expected to have material impact

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Comparison of CGAAP (CALM) vs IFRS

CGAAP and international models contain a number of similarities in basic framework with the exception of the approach to discounting and treatment of asset/liability mismatch

Canadian model is considered to be most similar to international model

There are a number of differences in details that could make application quite different

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Comparison of CGAAP (CALM) vs. IFRS – Framework

√√No cash value floors

√√Acquisition costs expensed with reserve offset to extent recoverable over valuation term

√√Gain/Loss permitted at contract inception

√√Best estimate cashflows and margins unlock and are kept current with changes capitalized in current income

√√Based on best estimate cashflows plus margins

√√Prospective cashflow valuation√√Principle not rules based

IFRSCGAAP

(third party perspective and different margin

methods)

(but no provision toextend term to offset acquisition expenses)

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Comparison of CGAAP (CALM) vs. IFRS – Framework (cont’d)

√xOwn credit standing adjustment to liabilities

x√Standard applies to all policy liabilities of insurance company

x√Liabilities include asset/liability mismatch risk

x√Discount rates based on actual assets held

√√Incorporate par dividends and contract adjustment features

√√Policyholder behaviour reflected

√√Cost of options/guarantees reflected

IFRSCGAAP

(more rigorous)

(limits on discretionary premiums)

(but potentially significant restrictions.

Also classification liability vs. equity)

(risk free)

(insurance contracts only)

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Comparison of CGAAP vs. IFRS – Profit Emergence Components

√

X

√

√

√

√

X

X

MarginsInsurance margins

Mismatch, market and credit margins

Service margins

Expected Investment Returns – risk free

√

√(IAS 39)

√

√

Actual – Expected Insurance Assumptions

Actual – Expected Investment Returns

Experience Gains

IFRSCGAAP

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Controversial Topics– Draft Framework

Discount rate approachuse of risk free discount rates will not allow companies to anticipate in the valuation earning positive spread on fixed income assets or yield premium on non-fixed income assets – disconnect from pricing and economic managementpotential to cause significant earnings strain at issueunclear how rates will be set where there is an observable curve (e.g. beyond 30 years)a model where assets are held at fair value and liabilities discounted at current market curves will show significant volatility from spread changes, risk free rate movement for mismatch position and, movements in fair value of non-fixed income assets supporting liabilities

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Controversial Topics– Draft Framework

Alternatives focus on minimizing capitalization volatility One alternative would increase/decrease margins to “re-spread” capitalization impacts over contract lifetimesAnother alternative would ignore unlocking unless “loss recognition” (i.e. reserve inadequate on current best estimate assumption basis without MfADs

Full contract unlocking ofassumptions, margins and discount rates each periodwith change impactcapitalized to earnings incurrent period

Should liability valuation be calibrated to the premium?No gain could be achieved by increasing margins to offset potential inception gains

Gains/losses permitted atcontract inception

DiscussionCurrent Exit ValueModel Proposal

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Controversial Topics– Draft Framework

Elements that drive liability cashflows away from true best estimates1. Potential exclusion of discretionary future premiums above

those needed to keep contract in-force, even where those premiums expected

could be material impact for UL and distort earnings emergence

2. Requirement that policyholder dividends or other contract adjustment consistent with future expected assumptions can only be reflected if legally required or the result of a constructive obligation

unclear what is sufficient to be deemed a constructive obligationLiability vs. equity classificationcould materially distort earnings emergence

3. Valuation term limitations may limit revenue capitalization to offset acquisition expenses

deposit annuities could be most impacted

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Universal Life Example

Mid & Max funded policies

-150%9%Lower premiums

15%Adjust MCCSR

-42%10%Risk Free

4%16%Base

FY Income/ Premiums

ROE

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

IASB Discussion Paper - Controversial Topics– Draft Framework

Inclusion of own credit standing adjustment to discount ratesthis concept has counter intuitive result of reducing liabilities as credit rating is lowered

Requirement that best estimate assumptions be probability weighted

if applied rigorously, could require advanced multi path modeling for all risks in all productswould be very significant development/implementation issue

Lack of clarity around methods to establish marginssignificant uncertainty around profit emergence patterns, and what will be acceptable methods to set margins“Cost of Capital” method is favoured

Lack of clarity around impact of “third party perspective” and how this will be measured

details of paper tend to suggest that assumptions would start with internal perspective and only be adjusted for evidence that they are not appropriate from market perspective

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07How to prepare for “Double Conversion”

Unlikely final insurance contract standard in place before transition to IFRS in 2011.

Will result in “double conversion” – once to implement IFRS 4 (phase I) in 2011 and second conversion once final standard in place.

Insurers will need to keep abreast of latest developments at IASB and assess proposals against existing reserves to ensure impacts on financial results, systems and processes are understood well in advance of adoption in order to implement in timely manner.

Take opportunity to provide comments on proposals to IASB.

Never been a better time to be an actuary (or an accountant!)

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

PwC Survey of 26 global insurers first annual report under IFRS (2005) resulted in the following key findings:

•Enormous implementation challenges

•Extensive new disclosure requirements

•First internationally-agreed definition of an insurance contract

•Little diversity in accounting policy beyond insurance contracts and investments

•Use of alternative measures of profit – European Embedded Value (EEV)

Experience of IFRS Conversions for insurers in Europe PwC Survey

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

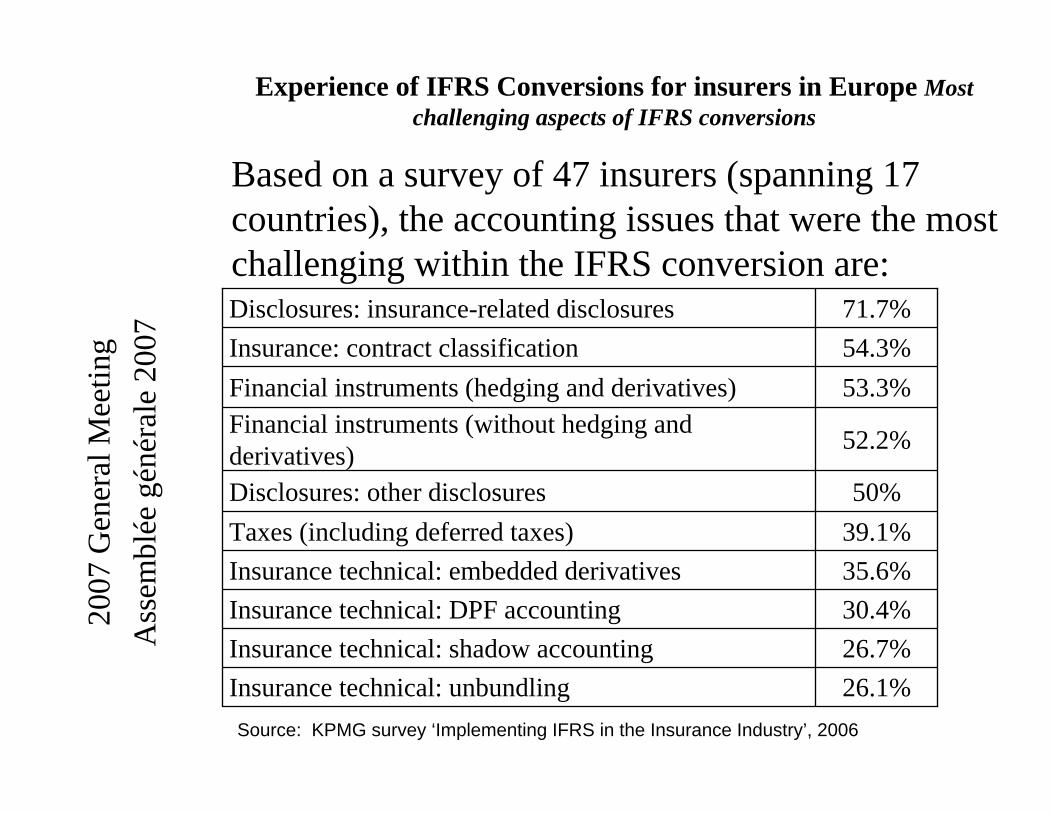

Experience of IFRS Conversions for insurers in Europe Most challenging aspects of IFRS conversions

Based on a survey of 47 insurers (spanning 17 countries), the accounting issues that were the most challenging within the IFRS conversion are:

26.1%Insurance technical: unbundling 26.7%Insurance technical: shadow accounting 30.4%Insurance technical: DPF accounting 35.6%Insurance technical: embedded derivatives 39.1%Taxes (including deferred taxes) 50%Disclosures: other disclosures

52.2%Financial instruments (without hedging and derivatives)

53.3%Financial instruments (hedging and derivatives) 54.3%Insurance: contract classification 71.7%Disclosures: insurance-related disclosures

Source: KPMG survey ‘Implementing IFRS in the Insurance Industry’, 2006

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07

Experience of IFRS Conversions for insurers in Europe Increase inSize of Financial Statements

Increase in length 2005 in IFRS 2004 in local GAAP

138% 112 47

82% 100 55

75% 100 57

67% 87 52

14% 90 79

112% 70 33

59% 129 81

210% 124 40

82% 60 33

2007

Gen

eral

Mee

ting

Ass

embl

éegé

néra

le20

07Questions?

![Welcome [cicc.or.jp]cicc.or.jp/japanese/hyoujyunka/pdf_ppt/04SEbangladesh.slide.pdf · ¾Bangladesh has already adopted ISO 9000, ISO 14000, HACCP and many other international standards,](https://static.fdocuments.net/doc/165x107/5e7e97ec6f2d5e4fef3b2170/welcome-ciccorjpciccorjpjapanesehyoujyunkapdfppt-bangladesh-has.jpg)