Canadian banking

41

1 CHAPTER 1 INTRODUCTION Banking in Canada is widely considered the most efficient and safest banking system in the world, ranking as the world's soundest banking system for the past three years according to reports by the World Economic Forum. Released at October 2010, Global Finance magazine put Royal Bank of Canada at number 10 among the world's safest bank and Toronto- Dominion Bank at number 15. Canada’s banks, also called chartered banks, have over 8,000 branches and almost 18,000 automated banking machines (ABMs) across the country. In addition, "Canada has the highest number of ABMs per capita in the world and benefits from the highest penetration levels of electronic channels such as debit cards, Internet banking and telephone banking" 1.1 THE BEST BANKING SYSTEMS IN THE WORLD According to the survey by the World Economic Forum, Canada has the world’s best banking system. It is followed by Sweden, Luxembourg and Australia. Canada received 6.8 out of total 7 points and topped the list. The United States, which has seen a lot of big name bank failures in the global financial crisis, has fallen down to 40th place. The Criteria According to World Economic Forum, this report is based on findings of top executives. The executives handed the banks a score between 1.0 (insolvent and possibly requiring government bailout) to 7.0 (healthy and with sound balance sheets). This report was released because most of the central banks in Europe, United States, China, Canada, Sweden and

-

Upload

vaibhav-sawant -

Category

Education

-

view

342 -

download

1

Transcript of Canadian banking

1

CHAPTER 1

INTRODUCTION

Banking in Canada is widely considered the most efficient and safest banking system in the

world, ranking as the world's soundest banking system for the past three years according to

reports by the World Economic Forum. Released at October 2010, Global Finance magazine

put Royal Bank of Canada at number 10 among the world's safest bank and Toronto-

Dominion Bank at number 15.

Canada’s banks, also called chartered banks, have over 8,000 branches and almost 18,000

automated banking machines (ABMs) across the country.

In addition, "Canada has the highest number of ABMs per capita in the world and benefits

from the highest penetration levels of electronic channels such as debit cards, Internet

banking and telephone banking"

1.1 THE BEST BANKING SYSTEMS IN THE WORLD

According to the survey by the World Economic Forum, Canada has the world’s best

banking system. It is followed by Sweden, Luxembourg and Australia. Canada received 6.8

out of total 7 points and topped the list. The United States, which has seen a lot of big name

bank failures in the global financial crisis, has fallen down to 40th place.

The Criteria

According to World Economic Forum, this report is based on findings of top executives. The

executives handed the banks a score between 1.0 (insolvent and possibly requiring

government bailout) to 7.0 (healthy and with sound balance sheets). This report was released

because most of the central banks in Europe, United States, China, Canada, Sweden and

2

Switzerland slashed their interest rates in an attempt to end panic selling on the markets and

also to restore much shaken trust in the general banking system to avoid financial meltdown.

The Best Banking System - Canada

The main reason behind the success of Canadian banks is solid funding and conservative

consumer lending. Canadian banks are more stringent in their policies regarding the amount

of loans they can extended to consumers compared to other international banks. Consumers

wanting to lend from Canadian banks are required to set aside a minimum of 7 percent for

Tier 1 capital, compared with 6 percent for U.S commercial banks.According to the Canadian

banking regulator, the institutions can lend up to 20 times their capital base.

The European peers assets were almost more than 30 times their capital. In the U.S and U.K,

the average weighted capital was more than 25 times.

Canadian regulators resisted pressures from the banking executives to loosen the lending

restrictions, while the economy was booming. The banks employed stricter guideline

measures for lending and were better at navigating through the global financial crisis.

Moreover, most of the Canadian banks are also somewhat reluctant to lend to homebuyer

with low credit scores, which provides less exposure to mortgage defaults. Subprime loans

account for only about 5 percent of the total in Canada; while in the U.S it was at 20 percent

where independent lenders and mortgage brokers were competing with commercial banks to

win over the business at the cost of attracting high-risk borrowers.

3

1.2 ORIGINS

Banking in Canada began to migrate in earnest from colonial overseas banking operations to

a local banking system with the founding of the Bank of Montreal in 1817. Other banks soon

followed and began business and after a lengthy approval process began unregulated banking

business. These institutions issued the only local currency notes until amendments in the

British North America Act allowed federal and provincial governments to begin to introduce

their own notes starting in 1866. Official Canadian currency took the form of the Canadian

dollar in 1871, overriding the currency of individual banks. The establishment of the Bank of

Canada in 1935 was also an important milestone in banking and monetary governance.

Despite various loss events (such as the Latin American debt crisis, the collapse of Olympia

and York, Enron-related liabilities, and the U.S. Subprime mortgage crisis), the big five

banks have thus far proven to be safe and stable companies. For example, in securities

prospectuses the Royal Bank of Canada says it has paid a common share dividend in every

year since 1870, the year after it received its banking charter.

According to the Department of Finance, two small regional banks failed in the mid-1980s,

the only such failures since 1923, which is the year Home Bank failed. There were no bank

failures during the Great Depression compared to 9000+ in the US.

In the 1980s and 1990s, the largest banks acquired almost all significant trust and brokerage

companies in Canada. They also started their own mutual fund and insurance businesses. As a

result, Canadian banks broadened out to become supermarkets of financial services.

After large bank mergers were ruled out by the federal government, some Canadian banks

turned to international expansion, particularly in various U.S. markets such as banking and

brokerage.

4

Two other notable developments in Canadian banking were the launch of ING Bank of

Canada (which relies mostly on a branchless banking model), and the slow emergence of

non-bank mortgage origination companies.

A survey conducted by the World Economic Forum called the Global Competitiveness

Report of twelve-thousand corporate executives, in 2008, concluded that Canada has the best

banking system in the world, receiving a score of 6.8 out of possible seven.

1.3 Regulation

Canada's federal government has sole jurisdiction for banks according to the Canadian

Constitution, specifically Section 91(15) of The Constitution Act, 1867 (30 & 31 Victoria, c.3

(UK)), formerly known as the British North America Act, 1867. Meanwhile, credit

unions/caisses populaires, securities dealers and mutual funds are largely regulated by

provincial governments.

The main federal statute for the incorporation and regulation of banks, or chartered banks, is

the Bank Act (S.C. 1991, c.46), where Schedules I, II and III of this Act list all banks

permitted to operate in Canada under these three distinct categories:

Schedule I: Banks allowed accepting deposits and which are NOT subsidiaries of a

foreign bank. Examples include "The Big Five" banks (as mentioned above) and

smaller second tier banks such as National Bank of Canada, Laurentian Bank of

Canada, President's Choice Financial and Canadian Western Bank. Because the

Schedule I banks are not subsidiaries of any foreign bank, they are the true domestic

banks and are the only banks allowed to receive, hold and enforce a special security

5

interest described and provided for under the Bank Act and known to Canadian

lawyers and bankers as the "Bank Act security".

Schedule II: Banks allowed to accept deposits and which are subsidiaries of a foreign

bank. Examples include AMEX Bank of Canada, Citibank Canada, HSBC Bank

Canada, ING Bank of Canada and Wal-Mart Canada Bank. Like the Schedule I banks,

the Schedule II banks are incorporated under the Bank Act.

Schedule III: Foreign banks permitted to carry on business in Canada. Examples

include Bank of America, Capital One, Credit Suisse and Deutsche Bank AG. Unlike

the Schedule I and Schedule II banks, the Schedule III banks are NOT incorporated

under the Bank Act and they operate in Canada, usually within the country's largest

cities (being Toronto, Montreal, Calgary and Vancouver), under certain restrictions

mentioned in the Act.

The bank regulator is the Office of the Superintendent of Financial Institutions (best known

as OSFI), who’s authority stems from the Bank Act. The financial groups are also governed

by regulatory bodies (bank regulators, securities regulators, insurance regulators, etc.) in each

country in which they operate.

1.4 REGULATORY CHALLENGES

Banks in Canada come under the purview of two regulators: The Office of the Superintendent

of Financial Institutions (OSFI) for prudential regulation and the Financial Consumer Agency

of Canada (FCAC) for consumer matters. Every five years, Canada’s Bank Act is reviewed

and updated to stay abreast of industry changes. Regulations and regulatory compliance have

been key to the Canadian banking industry, enabling it to remain strong and stable. However,

the move forward impact of regulatory changes worldwide is a big concern for banks in

6

Canada. As they enter international markets, Canadian banks will be more exposed to global

turmoil and conditions that are in a state of flux due to economic troubles, worries of

sovereign debt and stringent regulations. Adjusting to the regulatory changes will require

transformation of business operations that could slow growth and cause tradeoffs to be made

between risk and profitability.

The key for Canadian banks will be to navigate changes that will have an impact on their

business operations, models, systems and profitability, as regulators continue to introduce and

implement new measures to ensure transparency and stability to the banking system. Banks,

therefore, must effectively manage their resources while complying with regulations, which

calls for retooling and investing in IT systems to ensure compliance and competitive

advantage. Moving forward, this type of investment will put additional pressure on

profitability and operational efficiencies.

1.5 TECHNOLOGY CHALLENGES

The sound business practices of Canadian banks helped them weather the global financial

storm effectively compared with banks from other nations. Going forward, technology will

play a key role for these banks to achieve the balance between compliance and growth.

The Big Six have invested $55.8 billion between 1996 and 2009 in technology to provide

their customers with secure, accessible and convenient banking systems. Investments,

especially on the compliance and reporting front, can be expected to grow as Canadian

banking regulators mandate early adherence with new regulations. Basel III will require

banks to pay more attention to integrating data sources and using newer data modelling

techniques. Liquidity reporting is another area in which banks will need to invest

7

significantly. They will also need to ensure they have a robust IT infrastructure to deal with

data integrity and usability.

Legacy modernization is a major challenge for the Canadian banking industry. Newer banks

are using IT to attract new customers and improve their level of service. More established

institutions face a difficult time deploying new technologies, as a major portion of their

businesses is supported and run on legacy systems. Celent, a prominent research house,

predicts that a significant percentage of IT budgets in the future will be allocated to

maintaining legacy systems .Modern-day innovations such as service-oriented architecture-

based systems and cloud-based technologies can help alleviate upgrade expenditure

challenges. Recently, Scotiabank signed up for a cloud-based software as a service (SaaS)

solution to replace its multiple legacy trade and supply chain applications for its global trade

services.These kinds of systems provide an efficient way of allocating capital, in which the

bank pays only for computing resources that are actually used, while providing a means to

quickly enter new markets and offer new and innovative services. The call for replacing

legacy systems is a longstanding need. Canadian banks need to address this with a slow and

steady, incremental approach, since these heritage systems are pervasive across business

lines; it is too risky to replace them all at once. Competition for customers in the ultra-

competitive Canadian banking market also calls for newer technologies to achieve market

and mind share. Given the state of banking and the economy, taking a middle path is the best

approach for banks that want to conserve capital and maintain operating margins over the

short term.

8

CHAPTER 2

FAST FACTS ABOUT THE CANADIAN BANKING SYSTEM

1. Number of bank branches across Canada: 6,205, of which approximately 2,100 are

rural and small town branches.

2. Number of banks in Canada: 80.

3. Number of transactions logged at bank-owned ABMs in Canada (2012): 842 million.

4. Number of online banking transactions completed with the six largest banks in

Canada in 2012: 583.7 million.

5. Canadians are careful borrowers, and mortgage arrears in Canada remain very low (in

fact, as of June 2013 only 0.31% of bank mortgages are in arrears).

6. Taxes paid in Canada in 2012 (by the six largest banks): $8 billion.

7. Banks contribute approximately 3.1% to Canada’s GDP.

8. Taxes paid worldwide in 2012 (by Canada's six largest banks): $10.2 billion.

9. Amount banks and their subsidiaries paid in salaries and benefits in Canada in 2012:

$20.8 billion.

10. In 2012, banks employed 275,280 Canadians and industry employment has increased

by 14.4% over the past ten years while full-time industry employment has increased

by 25.4% over the same period.

11. Number of people employed by Canadian banks in other countries in 2012: 108,740.

12. Percentage of senior managers with the six largest banks who are women (2011):

33.3%. Women constitute 65.3% of the workforce at Canada’s six largest banks

(excluding subsidiaries).

13. Banks provide financing to some 1.6 million small and medium-sized businesses.

14. Amount six largest Canadian banks spent on technology in 2012: $7.7 billion.

9

15. Amount six largest Canadian banks spent on technology from 2002 to 2012: $60.4

billion.

16. Dividend income paid in 2012 by Canada’s banks to shareholders: $12.6 billion.

17. Canada’s Bank Act is reviewed and updated every five years to ensure the regulatory

structure is keeping pace with changes in the industry.

18. Percentage of Canadians who give banks a good performance rating when it comes to

being stable and secure: 87%.

19. Percentage of Canadians that have a favorable impression of banks in Canada: 86%.

20. Percentage of Canadians who trust banks to protect the privacy of their personal

information and transactions: 83%.

21. #1 – Canada’s ranking by the World Economic Forum for the soundest banking

system in the world, (a ranking achieved six years in a row).

22. The World Economic Forum has ranked Canada’s banking system as the most sound

in the world, five years in a row.

23. Banks employ 275,000 Canadians. Full-time bank employment has increased 25.4%

in the past 10 years.

24. Banks contributed approximately 3.1% or $53 billion to Canada’s GDP.

25. Banks paid $12.6 billion in dividends (2012) to shareholders.

26. Banks provide financing to 1.6 million small and medium-sized businesses.

10

CHAPTER 3

CANADIANS DOMINATE WORLD’S 10 STRONGEST BANKS

Banks from Citigroup Inc. (C) in the U.S. to BNP Paribas SA (BNP) in France are racing to

shed assets and raise money ahead of new global capital rules that start taking effect in 2015.

For Canadian lenders, these moves have created the opportunity to go on a shopping spree.

Canada’s six largest banks have spent $37.8 billion since 2008 on about 100 acquisitions at

home and abroad, Bloomberg Markets magazine reports in its June issue.

“We and our Canadian competitors are only able to do that because we have some flexibility

as a result of our strength,” says Gerald McCaughey, chief executive officer of Canadian

Imperial Bank of Commerce, which bought JPMorgan Chase & Co.’s minority stake in asset

management firm American Century Investments last year. “Over the longer term, this should

actually help to maintain the strength of the Canadian banking system and its

competitiveness.”

CIBC (CM) was No. 3 in Bloomberg Markets’ second annual ranking of the world’s

strongest banks, followed by three of its Canadian rivals: Toronto-Dominion Bank (TD) (No.

4), National Bank of Canada (NA) (No. 5) and Royal Bank of Canada (No. 6), the country’s

largest lender. Bank of Nova Scotia ranked 18th, and Bank of Montreal was 22nd.

No other country dominated the list as did Canada: The nation of 34.7 million people has

only eight publicly traded banks, two of which are regional lenders. Only three U.S. banks --

JPMorgan Chase (JPM) (No. 13), PNC Financial Services Group Inc. (PNC) (No. 17)

and BB&T Corp. (BBT) (No. 20) -- made the top 20. Four European banks were included:

two from Sweden and one each from the U.K. and Switzerland.

11

3.1 $100 BILLION OR MORE

For the ranking, they considered only banks with at least $100 billion in assets. They weighed

and combined five criteria, comparing Tier 1 capital with risk-weighted assets, for example,

and nonperforming assets with total assets. Tier 1 capital includes a bank’s cash reserves,

outstanding common stock and some classes of preferred stock, all of which combine to act

as a buffer against losses.

Banks that posted an annual loss for last year or that failed government stress tests weren’t

eligible for consideration.

Canadian banks invoke their strong capital levels, the country’s conservative lending culture

and strict regulatory oversight under a single supervisor as reasons for their showing. The

supervisor requires Canadian banks to hold a higher level of capital than do international

standards.

Major banks around the world follow the rules of the Basel Committee on Banking

Supervision -- an arm of the Bank for International Settlements, based in Basel, Switzerland,

that draws banking regulators from 27 nations to set standards for lenders. The committee

issued its first internationally accepted capital guidelines in 1988.

3.2 BEYOND BASEL

Those rules, known as Basel I, focused on credit risk: the possibility that borrowers might not

pay back their bank loans. The committee required banks to hold total capital, at least half of

it in Tier 1 capital, equal to at least 8 percent of their risk-weighted assets.

Canada’s regulator, the Office of the Superintendent of Financial Institutions Canada, has

gone beyond those levels in its requirements, a stance that has shielded lenders from some of

the financial follies that undermined other global banks, especially in 2008. As far back as

January 1999, OSFI sent a letter to Canadian banks telling them to set aside at least 10

12

percent of total capital as a cushion for losses. “I do not think it was popular at the time,” says

Julie Dickson, OSFI’s superintendent. “That’s where having a supervisor with a pretty clear

mandate allows you to take those unpopular decisions.”

3.3 EXCEEDING REQUIREMENTS

The Canadian regulator also set criteria on the quality of banks’ assets, requiring them to hold

75 percent of their capital in equity. “When the crisis erupted, we realized we had stuck to a

fairly basic rule, which was that the bulk of Tier 1 capital had to be in equity,” Dickson says.

“That turned out to be very, very important.”

Some of Canada’s lenders elected to exceed OSFI’s requirements. Investors criticized Bank

of Nova Scotia (BNS), CEO Richard Waugh says, for holding too much cash. “So many

people in 1999 and 2001 said: ‘Scotia, you’ve got excess capital because you’re way above

Basel, way above OSFI. You should do stock buybacks and extra dividends,’” Waugh recalls

in an interview at an annual investor meeting in Saskatoon, Saskatchewan. “We said, ‘It’s not

excess, because it was getting 18 percent return on capital, which was a very good place, and

our shareholders would have had a difficult time reinvesting elsewhere.’”

Waugh credits the high returns to profits spread equally among four main businesses: global

wealth management and domestic, international and wholesale banking.

3.4 INTERNAL MODELS

Since 1988, the BIS has further tweaked global rules. The 2004 Basel II accord set more

guidelines on how to address and quantify the risks of a bank’s assets -- allowing them to use

internal models, for instance.

And in 2010, regulators rewrote the rules again to address shortcomings that arose out of the

financial crisis. The group will require banks to hold 7 percent of their assets as core reserves,

13

or equity core Tier 1 capital, by 2019 when the latest rules -- known as Basel III -- are fully

implemented. Banks will be required to have minimum Tier 1 capital of 6 percent starting in

2015.

While having strong capital is crucial, Canadian banks will prosper only if they can expand

their reach, Waugh says. “Because if you don’t grow, you’re going to eventually have some

issues on capital and strength,” he says. Scotiabank has units in about 50 countries and is

looking in particular at Latin America and Asia, says Waugh, who’s also vice chairman of the

Washington-based Institute of International Finance.

Expanding in the U.S.

Canadian banks spent $14.4 billion last year on acquisitions, many of them aimed at growth

in the U.S. “Having conservative capital standards in Canada going into the downturn clearly

was a competitive advantage,” TD Bank CEO Edmund Clark says. He says Canada’s second-

biggest bank was ferocious at managing liquidity.

TD Bank has accelerated a U.S. expansion strategy that Clark began in 2004. In 2008, the

bank took over Commerce Bancorp of Cherry Hill, New Jersey, in a $7.1 billion transaction

that helped give the Canadian lender 1,284 branches in the U.S. today -- more than the 1,150

it currently has in Canada. TD’s green logo is now a common sight on the streets of New

York, where it aims to become the city’s third-largest lender by number of branches within

four years, and in Boston, where its name adorns the TD Garden, home to the Boston Celtics

basketball team and Boston Bruins hockey team.

3.5 ‘ONCE-IN-A-LIFETIME OPPORTUNITY’

“We were in there and said: ‘We have a once-in-a-lifetime opportunity. Let’s take advantage

of it,’” Clark says. Toronto- Dominion -- one of four banks globally to boast the top Aaa

long-term debt rating from Moody’s Investors Service -- added further to its U.S. clout last

14

year when it acquired auto lender Chrysler Financial Corp. from Cerberus Capital

Management LP.

Bank of Montreal (BMO), Canada’s fourth-largest lender, also ramped up its presence in the

U.S. by buying Marshall & Ilsley Corp., a Milwaukee-based bank, last year for $4.19 billion.

Prior to that, its main U.S. asset had been the small Chicago- based Harris Bank franchise it

bought in 1984.

Royal Bank has also been active. In April, it agreed to buy the 50 percent of RBC Dexia

Investor Services Ltd. it didn’t already own from Banque Internationale a Luxembourg SA

for about C$1.1 billion ($1.1 billion) in cash.

As they flex their muscles with acquisitions, Canadian banks may face tougher times ahead.

Consumer lending is slowing this year. RBC Capital Markets predicts that Canadian bank

profits will rise 7 percent in 2012, slightly more than half the 13 percent rate in 2011.

3.6 STOCKS OUTPERFORM

Canadian bank stocks have outperformed those from south of the border. In the four years

ended on Dec. 31, the Standard & Poor’s/TSX Composite Commercial Banks Industry Index

(STCBNK) that tracks Canada’s eight traded banks rose 4.8 percent compared with a 56

percent decline for the 24-member KBW Bank Index (BKX), which includes the biggest U.S.

banks.

Canadian banks haven’t been completely immune to the woes faced by their counterparts in

the U.S. and Europe in recent years. CIBC had more than C$10 billion in writedowns

following the U.S. mortgage-related financial crisis of 2007, more than any other Canadian

bank. CIBC also was one of the first to rebuild its balance sheet, selling C$2.94 billion of

stock nine months before Lehman Brothers Holdings Inc. collapsed and markets seized up.

15

Still, writedowns at Canadian banks were a fraction of the $2.08 trillion taken by financial

companies worldwide.

There’s no reason for Canadian banks to become smug, the country’s banking regulator says.

“Complacency is a real danger for Canada,” OSFI’s Dickson says. “The bar is always rising

in risk management, and if you become complacent, you may say you’re doing a good

enough job and you don’t really have to change anything.”

16

CHAPTER 4

"BIG FIVE" BANKS

In everyday commerce, the banks in Canada are generally referred to in two categories: 1) the

five large national banks and 2) smaller second tier banks (notwithstanding that a large

national bank and a smaller second tier bank may share the same legal status and regulatory

classification.

The five largest banks in Canada are:

Royal Bank of Canada

Toronto Dominion Bank

Bank of Nova Scotia

Bank of Montreal

Canadian Imperial Bank of Commerce

Notable second tier banks include the ATB Financial, National Bank of Canada, the

Laurentian Bank, the Desjardins Group (technically not a bank but an alliance of credit

unions), HSBC Bank Canada, and ING Bank of Canada. These second tier organizations are

largely Canadian domestic banking organizations. Insurance companies in Canada have also

created deposit-taking bank subsidiaries.

Unlike the smaller Canadian banks, the Big Five are not just Canadian banks, but are instead

better described as international financial conglomerates, each with a large Canadian banking

division. In fiscal 2007, RBC's Canadian segment called "Personal Financial Services" (the

segment most related to what was traditionally thought of as retail banking) had revenue of

only CAD$5,082 million (or 22.6%) of a total revenue of CAD$22,462 million. Canadian

17

retail operations of the Big Five comprise other activities that do not need to be operated from

a regulated bank. These other activities include mutual funds, insurance, credit cards, and

brokerage activities. In addition, they have large international subsidiaries. The Canadian

banking operations of the Big Five are largely conducted out of each parent company, unlike

U.S. banks that use a holding company structure to hold their primary retail banking

subsidiaries.

Canada's 5 largest banks have been designated as too big to be allowed to fail for the country

by the federal regulator, meaning they will be subject to more stringent capital requirements

and supervision.

The Office of the Superintendent of Financial Institutions said the designation stems from a

framework issued by the Basel committee on banking oversight in October that set out

guidelines for assessing domestic financial institutions.

Under the OSFI requirements, the Bank of Montreal, Bank of Nova Scotia, Canadian

Imperial Bank of Commerce, National Bank of Canada, Royal Bank of Canada and Toronto-

Dominion Bank will be subject to an additional one per cent capital buffer for risk, meaning

they will have to hold more assets in reserve to protect against a sudden run on deposits.

The banks will need to have a common equity tier 1 ratio of eight per cent as compared with

seven per cent for smaller, less important financial institutions as of Jan. 1, 2016.

"The measures are designed to limit the likelihood that a major bank would encounter distress

or failure that could negatively impact the Canadian economy or taxpayers," OSFI head Julie

Dickson said in a news release.

18

In November, the Financial Stability Board updated its list of 28 international financial

institutions that were assessed too big to fail, but none of the Canadian banks made the grade.

However, OSFI said the banks are systemically important to the Canadian economy by virtue

of their size, interconnectedness, substitutability and flexibility.

In its explanation, OSFI said a bank's distress or failure is more likely to damage the

Canadian financial system or economy if its activities comprise a large share of domestic

banking activity."

It noted the six biggest banks account for over 90 per cent of total banking assets in Canada

and that "the differences among the largest banks are smaller if only domestic assets are

considered, and relative importance declines rapidly after the top five banks and after the

sixth bank (National)."

19

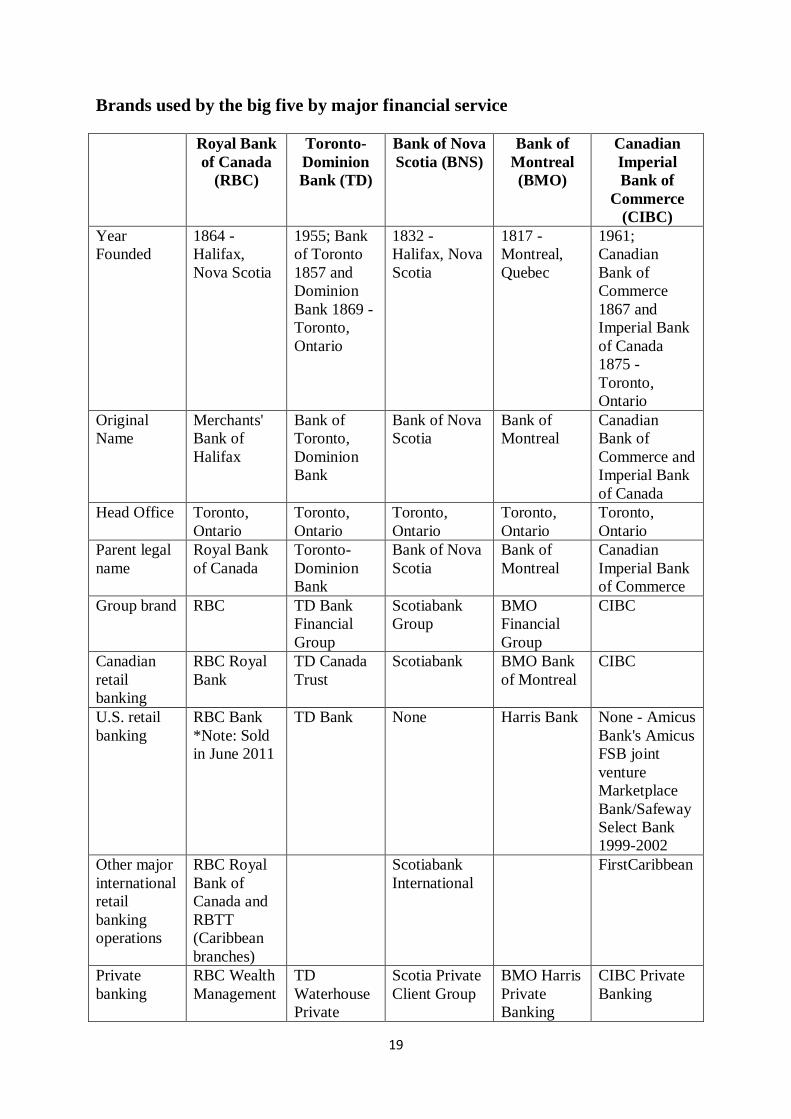

Brands used by the big five by major financial service

Royal Bank

of Canada

(RBC)

Toronto-

Dominion

Bank (TD)

Bank of Nova

Scotia (BNS)

Bank of

Montreal

(BMO)

Canadian

Imperial

Bank of

Commerce

(CIBC)

Year

Founded

1864 -

Halifax,

Nova Scotia

1955; Bank

of Toronto

1857 and

Dominion

Bank 1869 -

Toronto,

Ontario

1832 -

Halifax, Nova

Scotia

1817 -

Montreal,

Quebec

1961;

Canadian

Bank of

Commerce

1867 and

Imperial Bank

of Canada

1875 -

Toronto,

Ontario

Original

Name

Merchants'

Bank of

Halifax

Bank of

Toronto,

Dominion

Bank

Bank of Nova

Scotia

Bank of

Montreal

Canadian

Bank of

Commerce and

Imperial Bank

of Canada

Head Office Toronto,

Ontario

Toronto,

Ontario

Toronto,

Ontario

Toronto,

Ontario

Toronto,

Ontario

Parent legal

name

Royal Bank

of Canada

Toronto-

Dominion

Bank

Bank of Nova

Scotia

Bank of

Montreal

Canadian

Imperial Bank

of Commerce

Group brand RBC TD Bank

Financial

Group

Scotiabank

Group

BMO

Financial

Group

CIBC

Canadian

retail

banking

RBC Royal

Bank

TD Canada

Trust

Scotiabank BMO Bank

of Montreal

CIBC

U.S. retail

banking

RBC Bank

*Note: Sold

in June 2011

TD Bank None Harris Bank None - Amicus

Bank's Amicus

FSB joint

venture

Marketplace

Bank/Safeway

Select Bank

1999-2002

Other major

international

retail

banking

operations

RBC Royal

Bank of

Canada and

RBTT

(Caribbean

branches)

Scotiabank

International

FirstCaribbean

Private

banking

RBC Wealth

Management

TD

Waterhouse

Private

Scotia Private

Client Group

BMO Harris

Private

Banking

CIBC Private

Banking

20

Banking

Canadian

mutual

funds

RBC Funds

and PH&N

Funds

TD Mutual

Funds

Scotia Mutual

Funds

BMO

Mutual

Funds and

Guardian

Group of

Funds

CIBC Mutual

Funds

U.S. mutual

funds

Tamarack

Funds

Canadian

brokerage

RBC Direct

Investing and

RBC

Dominion

Securities

TD

Waterhouse

ScotiaMcLeod BMO

InvestorLine

and BMO

Nesbitt

Burns

CIBC

Investor's

Edge and

CIBC Wood

Gundy

U.S.

brokerage

RBC Wealth

Management

formerly

RBC Dain

Rauscher

TD

Ameritrade

(45%)

BMO Harris

Investor

Services

International

Brokerage

West Indies

Stockbrokers

Limited

TD

Waterhouse

(UK), TD

Direct

Investing

International

(LU)

Canadian

insurance

RBC

Insurance

TD

Insurance

Scotia

Insurance

BMO Life CIBC Creditor

Insurance,

CIBC Travel

Insurance

U.S.

insurance

RBC

Insurance

TD

Insurance

Capital

markets

RBC Capital

Markets

TD

Securities

Scotia Capital BMO

Capital

Markets

CIBC World

Markets

Major

custodial

operations

RBC Dexia

(June 27,

2012, RBC

purchased

the

remaining

50% from

Dexia)

CIBC Mellon

(50%)

Precious

metals

ScotiaMocatta

21

4.1 ROYAL BANK OF CANADA (RBC)

Canada’s largest bank by assets and market capitalization with broad leadership in

financial services.

A leading diversified financial services company in North America.

11th largest bank globally based on market capitalization(1), with operations in 46

countries.

80,000 full- and part-time employees.

More than 15 million clients worldwide

1. Personal & Commercial Banking

The Canadian market leader continuing to gain profitable market share.

RBC is the largest and most profitable retail bank in Canada; named “Best Bank in

North American and Canada.”

A major Caribbean Banking Group with branches in 20 countries and territories.

U.S. cross-border banking for Canadian clients and U.S. Wealth Management

clients.

Broad suite of products and financial services to individual and business clients

2. Wealth Management

A leading global wealth and asset manager.

Top 6 Global Wealth Manager by assets.

Ranked #1 in Canada in both retail asset management(3) and high net worth

market share.

Investment, trust, banking, credit and other wealth management and asset

management solutions.

22

3. Insurance

A market leader with a broad suite of products and strong distribution.

Canadian market leader in living benefits and one of Canada’s largest bank-

owned insurance companies.

Achieved highest ever marks for “Likelihood to Recommend” and “Ease of

Doing Business”.

Life, health, home, auto, travel, wealth accumulation solutions as well as

reinsurance solutions

4. Investor & Treasury Services

A specialist provider of global custody, fund administration and asset

servicing to institutional investors.

Leader in cash management, correspondent banking and trade finance for

financial institutions worldwide.

Funding and liquidity management for RBC

5. Capital Markets

A leading North American investment bank with select global reach

10th largest global investment bank by net revenue.

Best Investment Bank in Canada across Equity, Debt and M&A for 6th

consecutive year.

Corporate and investment banking, equity and debt origination and

distribution, and structuring and trading.

23

4.2 TORONTO DOMINION BANK

The Toronto-Dominion Bank is a Canadian multinational banking and financial

services corporation headquartered in Toronto. It is the second-largest bank in Canada

by market capitalization and based on assets, and is the sixth largest bank branch network in

North America. Commonly known as TD and operating as TD Bank Group, The bank was

created in 1955 through the merger of the Bank of Toronto and the Dominion Bank, which

were founded in 1855 and 1869, respectively.

The bank and its subsidiaries have over 79,000 employees and over 19 million clients

worldwide. In Canada, the bank operates as TD Canada Trust and serves more than 11

million customers at over 1,150 branches. In the United States, the company operates as TD

Bank (the initials are used officially for all U.S. operations). The U.S. subsidiary was created

through the merger of TD Bank north and Commerce Bank, and serves more than 6.5 million

customers with a network of more than 1,300 branches in the eastern United States.

The company is ranked at number 86 on the Forbes Global 2000 2010 listing. In October

2008, the company was named in the listings of Canada's Top 100

Employers in Maclean's and Greater Toronto's Top Employers by the Toronto

Star. Furthermore, in February 2011, it was named one of Canada's top 10 employers by

the Financial Post.

24

4.3 BANK OF NOVA SCOTIA

The Bank of Nova Scotia , commonly known as Scotia bank, is the third largest bank in

Canada by deposits and market capitalization. It serves some 19 million customers in more

than 55 countries around the world and offers a broad range of products and services

including personal, commercial, corporate and investment banking. With assets of

$754 billion, Scotia bank shares trade on the Toronto and New York stock exchanges.

Scotiabank is one of North America's premier financial institutions and the most

international of Canadian banks. We provide personal, commercial, corporate and investment

banking services to individuals, small and medium-sized businesses, corporations and

governments in more than 50 countries around the world, and coast to coast across Canada.

In today's complex financial services market, success belongs to companies that can balance

innovative technologies with a personal touch. The Scotiabank Group provide these balances

by "putting people first." While technological advances are making routine banking

transactions increasingly convenient and efficient, Scotiabank employees are focused on

constantly building stronger, deeper relationships with their customers in a human,

straightforward and knowledgeable way.

The bank was incorporated by the Legislative Assembly of Nova Scotia on March 30, 1832,

in Halifax, Nova Scotia, with William Lawson (1772–1848) serving as the first

president. The bank moved its executive offices to Toronto, Ontario, in March 1900. Scotia

bank has billed itself as "Canada's International Bank" due to its acquisitions primarily in

Latin America and the Caribbean, but also in Europe and India as well. BNS Institution

Number (or bank number) is 002. The company ranked at number 92 on the Forbes Global

2000 listing in 2012 and is currently under the leadership of Richard E. Waugh who serves as

CEO and Brian Porter, who serves as President.

25

4.4 BANK OF MONTREAL

The Bank of Montreal, (commonly BMO in either official language), or BMO Financial

Group, is one of the Big Five banks in Canada. On June 23, 1817, John Richardson and eight

merchants signed the Articles of Association to establish the Bank of Montreal in a rented

house in Montreal, Quebec. The bank officially opened its doors for business on November 3,

1817, making it Canada's oldest bank. In Canada, the bank operates as BMO Bank of

Montreal and has more than 900 branches, serving over seven million customers. The

company also has substantial operations in the Chicago area and elsewhere in the United

States, where it operates as BMO Harris Bank. BMO Capital Markets is BMO's investment

and corporate banking division, while the wealth management division is branded as BMO

Nesbitt Burns.

The company is ranked at number 150 on the Forbes Global 2000 list.

4.5 CANADIAN IMPERIAL BANK OF COMMERCE

The Canadian Imperial Bank of Commerce (French: Banque Canadienne Impériale de

Commerce), commonly CIBC, is one of Canada's chartered banks, fifth largest by deposits.

The bank is headquartered at Commerce Court in Toronto, Ontario.

The bank's two strategic business units, CIBC World Markets and CIBC Retail Markets, also

have international operations in the United States, the Caribbean, Asia and the United

Kingdom. Globally, CIBC serves more than eleven million clients, and has over 40,000

employees. The company ranks at number 172 on the Forbes Global 2000 listing. CIBC was

named the strongest bank in Canada and North America, and the 3rd strongest bank in the

world, by Bloomberg Markets magazine, in May 2012.

26

CHAPTER 5

4 CANADIAN BANKS ON TOP 10 LIST OF WORLD'S STRONGEST

Four of Canada's biggest banks have landed among the top 10 in a global ranking of the

strongest banks, although two of them have seen their rankings slip from last year.

According to data compiled by Bloomberg Markets magazine, CIBC, Royal Bank,

Scotiabank and TD were ranked 3rd, 4th, 7th and 8th, respectively, on the publication’s

annual ranking of the world’s strongest and safest lenders.

Bloomberg Markets maintains a list of global banks with at least $100 billion US in assets.

This year, 78 firms made that cut-off.

The magazine then ranks the lenders based on five broad categories, including the size of

their capital reserves, the amount they keep on hand to cover bad loans, the percentage of

their assets that are inefficient or considered ‘non-performing’ and the amount they take in

deposits.

Among the Canadian banks. Royal Bank and Scotia saw their ranking improve, while CIBC

and TD slipped. In TD’s case, the bank slipped from 4th in the world to 8th.

A particular source of strength for Canadian lenders is how big their Tier 1 capital ratios are.

That’s the financial term for a lender’s cash reserves and how many of its own shares it owns

— both of which are valuable assets to have act as shock absorbers if and when the economy

hits a rough patch.

27

“Every year, our stress tests tell us we’re stronger than the previous year,” Toronto-Dominion

bank president Ed Clark told the magazine. “You don’t have to go out on the risk curve to

look after the shareholder, and it’s a foolish bet to do that,” he said.

Although they continue to compare favourably internationally, Canadian banks aren’t

immune to the signs of slowdown in the global and domestic economies. Ratings agencies

Moody’s and S&P each downgraded their outlooks for most of Canada’s major lenders late in

the year. And official data shows Canadians’ debt loads continue to tick alarmingly high, a

trend that could make the banks who loaned out all that debt vulnerable.

Another eye-opening placement on the list is U.S lender Citibank. Bloomberg Markets

ranked America’s biggest lender in fifth overall.

Citi’s presence so high on the list is significant because it wasn’t that long ago — 2008 to be

precise — that the bank was saved from bankruptcy thanks to a $45 billion US bailout from

the U.S. government.

Citi was disqualified from Bloomberg’s rankings as recently as last year because it failed the

U.S. Federal Reserve’s so-called “stress test” of banks that may be vulnerable to financial

shocks.

28

CHAPTER 6

THE BENEFITS

Canada’s banks have been rated the soundest in the world, five years in a row. Why does this

matter to Canadians? When we have banks we can depend on, we can plan ahead, take

advantage of opportunities and know that our banks will be there when we need them.

6.1 STRONG AND STABLE BANKS BENEFIT ALL CANADIANS:

Since Canada’s first bank opened its doors almost 200 years ago, banks have played – and

continue to play – a central role in financing much of Canada’s growth. Canada’s financial

services sector is an essential contributor to the country’s economic growth and well-being.

In 2012, the banking sector contributed $53 billion to the Canadian economy, and they paid

$12.6 billion in dividends to shareholders and that includes individual Canadians who hold

shares through their pensions and their retirement funds.

Why does this matter to Canadians?

1. Helping Canadians save for retirement

Millions of Canadians count on retirement savings products offered by Canada’s banks to

plan for their future.

2. Making small businesses a reality

Dependable banks also allow dreams to flourish when opportunity knocks. More than 1.6

million small businesses look to banks for the money they need to grow and business loans

help to create jobs.

29

3. Supporting young Canadians to succeed

Banks understand the role that they have in contributing to a positive future for Canada.

From helping Canadians better manage their money to improving the financial literacy of

youth, to student loans; banks can be depended upon to provide what people need.

4. Being part of the community

Banks employ over 275,000 Canadians across the country and we’re good customers too.

And banks and their employees are among the country’s most active corporate donors

supporting the arts, sports, culture, music, health and the environment.

6.2 THEY PROVIDE WHAT PEOPLE NEED:

More than 90 per cent of Canadians feel positively about their bank. This exceeds what you

find for other service-oriented industries and it’s been on the rise over the last twenty years.

Canadians value the stability and soundness of our banks with 81 per cent of

Canadians believing that Canada’s banks are more stable than other banks around the

world. And for a good reason. Canada’s banks came through the recent global

financial crisis without any taxpayer funded bailouts, there were no bank failures and

they continued to lend. And it’s why the World Economic Forum, for the fifth year in

a row, said Canada’s banks are the soundest in the world.

Canadians value the safety that banks provide in terms of financial transactions and

personal information with 83 per cent of Canadians seeing banks as doing a good job

of protecting their personal information and transactions.

30

Canadians value the added convenience and choice in how they bank with 76 per cent

rating the performance of banks as good when it comes to introducing technologies

that improve the convenience of banking.

Canadians see the value in having banks that are profitable with 81 per cent

understanding that, like any company that has shareholders, banks have to focus first

on providing good returns to those who own their shares.

6.3 THEY PLAY BY THE RULES, MANAGE RISKS SENSIBLY AND

HAVE A STRONG REGULATORY SYSTEM:

Canada’s banks are well managed, well regulated and well capitalized. We play by the rules

and our national banking system is a key strength. By diversifying regional risk, a downturn

in an individual economic sector is balanced since funds can be moved from areas of excess

deposits to regions where growth is creating demand for new credit.

Banks in Canada are also among the best capitalized in the world, exceeding Bank for

International Settlements’ norms by significant margins. This allows banks to continue

lending and provides a cushion against loan losses, which tend to increase during economic

downturns.

And Canada has been recognized by the International Monetary Fund and others as having a

sound regulatory system. Our streamlined bank regulatory system has two primary regulators:

the Office of the Superintendent of Financial Institutions (OSFI) for prudential regulation and

the Financial Consumer Agency of Canada (FCAC) for financial consumer matters. In

contrast, the United States, for example, has a complex network of different regulators. And

31

Canada’s Bank Act is reviewed and updated every five years to ensure the regulatory

structure is keeping pace with changes in the industry.

And Canadians have a strong track record when it comes to paying their mortgages. Less than

half of one per cent of all mortgage holders with the country's largest banks have gone more

than three months without making a payment. This number has been stable for more than two

decades, in times of high and low unemployment, high and low interest rates, and a strong or

weak Canadian dollar.

32

CHAPTER 7

WHAT HELPED CANADA'S BIG BANKS WEATHER THE

FINANCIAL CRISIS

The little-discussed safety net that helped the big banks through the financial crisis was their

complete, masters-of-the-world dominance over the day-to-day financial affairs of almost all

Canadians.

When the banks need revenue and profits, they simply have their clients supply it. And so

they did in 2007, as the crisis began to take shape, and for years afterward.

Let us recount the ways, starting with the re-pricing of variable-rate mortgages. Before the

crisis, these mortgages were available at your lender’s prime rate minus a discount as large as

0.9 of a percentage point. At the height of the crisis, variable-rate mortgages were being sold

with a mark-up over prime of one to 1.5 of a percentage point. Since then, the discount has

gradually returned and is now at roughly 0.4 off prime.

A case can be made that fixed-rate mortgages would also be lower if pre-crisis pricing was

used. Data from Canada Mortgage and Housing Corp. shows that in the 7.5 years prior to the

crisis, posted five-year fixed-rate mortgages were priced at 2.44 percentage points on average

above the yield on the five-year Government of Canada bond. Today, the gap is around 3.2

points, down a bit from peak levels but still higher than it was.

Discounted mortgages are also more expensive than they might have been, precrisis. They

used to be sold at roughly one percentage point above the five-year Canada bond; today, the

gap is more like 1.6 points for a well-discounted mortgage.

33

The home-equity line of credit is one more example of higher costs as a result of the crisis.

HELOCs, as they’re called in the banking world, used to be available at prime. Today, the

rate for these widely used borrowing tools is prime plus 0.5 to prime plus one. Rates on

unsecured credit lines – where you don’t pledge your house as security – have also risen.

Banks made the argument that the crisis forced them to pay higher rates to raise funds for

lending to clients, and that this cost had to be reflected in higher borrowing costs. Haven’t

things calmed down by now?

To some extent, yes. But mortgage planner David Larock said banks have come under tighter

regulations in the past few years that continue to play a role in higher lending costs.

Customers have still come out ahead, he argues. “The [interest rate] discount we’ve enjoyed

because of the crisis has far outweighed the marginally increased costs that lenders have for

the most part passed on to consumers.”

The crisis was a stressful time for the banks, and they took it out on their customers in a

variety of ways. One bank had the bright idea, just as a recession was asserting itself, to

charge people a $35 inactivity fee if they left their unsecured credit line unused over a 12-

month period. The fee was later cancelled after some embarrassing publicity.

Another gift of the crisis was one bank’s decision to bump up its credit card interest rate by

five percentage points if a customer missed two consecutive minimum payments.

Even today, the banks continue to get tough with customers about borrowing. Some have

started to adjust the interest rates on credit cards and other lending products according to a

customer’s credit record. People who pay on time see no change, or a token rate cut. Those

struggling with debt get loaded down with higher interest rates.

34

Not all changes in the banking business have been negative. In an effort to create pools of

money they can profitably lend out, the banks have embraced the high-interest savings

account. Thanks to competition between banks, interest rates in these accounts are in the low

1-per-cent range. That’s tiny by historical standards, but decent when compared to one-year

term deposits and bond yields.

The consulting firm McVay and Associates says that savings deposit rates are 75 per cent

higher than they were five years ago, with much of the cash coming out of money market

mutual funds. Even after recent fee cuts, money market funds are only producing returns

around 0.5 per cent.

Financially, Canada’s banks are in strong shape right now. Profits are rich, shares have been

rising in price and dividends are being cranked higher on a regular basis. Take a moment to

admire the turnaround. You helped pay for it.

35

CHAPTER 8

WHY CANADA CAN AVOID BANKING CRISES AND U.S. CAN’T

Since 1790, the United States has suffered 16 banking crises. Canada has experienced zero —

not even during the Great Depression.

It turns out Canada can thank the French for their stable system, according to a paper by

Columbia University’s Charles Calomiris, presented at the Atlanta Fed’s 2013 Financial

Markets Conference.

When it became a British colony, the majority of Canada’s population was of French origin

— and the French inhabitants hated the British government.

So to keep the colony firmly within the Empire, British policymakers steered toward a

government structure that would limit the power of the French-majority while also giving

Canada more and more self-government. The eventual result was a highly-centralized federal

36

government which controlled economic policy making and had built-in buffers for banker

interests against populist forces, the paper argues.

That anti-populist political system — known in political science as liberal constitutionalism

or liberal democracy — is a key ingredient in Canada’s stable banking track record, Mr.

Calomiris contends in his paper, which is a summary of a much longer book he’s written with

Stephen Haber due out in September. That’s because this kind of political system makes it

difficult for political majorities to gain control of the banking system for their own purposes,

the authors contend.

Populist democracies like the U.S., on the other hand, tend to create dysfunctional banking

systems because a majority of citizens gain control over banking regulation that steers credit

to themselves and to their friends at the expense of the citizens that are excluded from the

banking system, he said.

The contrast between the U.S. and Canada was part of Mr. Calomiris broader argument that

dysfunctional banking systems — which are by far the norm rather than the exception around

the world — are the result of political factors.

“Whether societies have dysfunctional banking systems is really not a technical issue at all.

It’s a political issue,” Mr. Calomiris said at the conference, introducing his premise as “we do

know how to avoid dysfunctional banking but that we make political choices – you might

even say consciously” not to have functional banking systems for most of the modern era in

most countries of the world.

The history of the U.S. banking system is one in which the government forms partnerships

with different interest groups at different points in history, and those coalitions jointly

influenced the way the banking system was regulated, Mr. Calomiris argues.

37

“In populist democracies, such as the United States, the regulation of banking is used as a

political tool to favor some parties over others. It is not that the dominant political coalition in

charge of banking policy desires instability, per se, but rather, that it is willing to tolerate

instability as the price for obtaining the benefits that it extracts from controlling banking

regulation,” he writes in his paper.

Backing up their argument: Only six countries – including Canada — have been crisis-free

and at the same time have banking systems that provide abundant credit. Three of these –

Singapore, Malta and Hong Kong – are small, island-bound city-states where the

homogeneity of the population makes it politically difficult to create losers. The other three –

Canada, Australia and New Zealand – all share histories of liberal democracy.

Mr. Calomiris argues that in the U.S., a coalition that emerged in the 1990s of government,

big banks and activist consumer groups came helped fuel the housing crisis. Regulatory

changes opened the door to a wave of mergers and acquisitions that created today’s

megabanks. But banks still had to get approval – usually from the Federal Reserve – to

complete those mergers and outside groups were able to weigh in on the wisdom of the deal

as part of the Fed’s decision-making process.

Community groups, with the Clinton administration’s encouragement, used the Fed’s

approval process to extract binding concessions from banks to loosen underwriting standards

for poor, urban communities – concessions to which the Fed agreed, Mr. Calomiris argues.

The banks had to apply the looser standards to everyone. That helped fuel an explosion in

poorly underwritten mortgages that contributed to the depth and severity of the housing crisis,

he contends.

All in all, Mr. Calomiris’ theory is a bleak one for the ability of financial reform efforts to

make much of a difference.

38

“Smart economists with their regulatory ideas are sort of dead on arrival,” he said. “Political

coalitions will decide — not whether you’ve got the right VAR model — [but] whether a

banking system is going to be set up with rules that will lead it to be stable and have abundant

credit or not.”

39

CHAPTER 9

CONCLUSION

For all the recognition that the Canadian banking industry receives, it operates in a limited

and insular market. The industry’s move outside Canada for growth will expose banks to

global economic challenges, as well as a slew of regulatory compliance challenges. The

industry can overcome these obstacles by leveraging its strong banking system, built on

plain-vanilla products, limited exposure to riskier businesses and products, as well as a strong

focus on long-term returns and customer service.

Another strength is that the government offers no incentives for consumers to take on higher

debt, resulting in prudent borrowing. The Dodd-Frank Act began mandating stress-testing to

measure the health of banks following the global economic crisis, but OSFI, the Canadian

banking regulator, has been administering stress tests even before the crisis took place. This

places Canadian banks in a strong position to contend with new challenges and opportunities.

Emerging technologies such as analytics, social media, mobile devices and cloud computing

will play a greater role in the coming years. As the millennial generation grows in size and

influence, demand for services that make use of these tools and techniques will play a

significant role in determining growth and pecking order. Social media is already proving to

be a critical platform to appeal to various segments of customers. According to the JD Power

2011 Canadian Retail Banking Customer Satisfaction Study,9 more than 60% of retail

banking customers use social media, and among those who use social media for banking

purposes, 24% say they do so to discuss their banking experience or inform their bank of a r

service issue. As more and more consumers use online and mobile banking services, it will be

40

imperative for banks to consider how they can integrate these technologies and tap into their

power to support and grow their businesses.

Regulations and economic conditions worldwide remain a cause for concern. Banks today are

required to deal with more stringent capital, liquidity and risk management requirements. In

such a scenario, improving operational efficiencies and gaining additional ground by utilizing

their existing competitive advantages will determine which banks will succeed in the future.

Canadian banks will do well by:

Maintaining the fine balance of meeting growth targets while complying with more

stringent regulatory requirements.

Diversifying into markets and related businesses with strong growth potential, while

applying the experience gained in their home markets.

Effectively dealing with the economic, political, cultural and regulatory hurdles in

markets where they operate.

Developing and providing innovative products and solutions.

A recent Global CEO survey by PricewaterhouseCoopers says that 87% of banking and

capital market CEOs believe that innovation will lead to operational efficiencies; 64% believe

that IT investments will help them tap into new marketing and transactional opportunities.

Achieving operational efficiencies with smart use of technology and third-party services to

keep focused on acquiring, retaining and delighting customers.

The Canadian banking industry weathered the global financial storm. In fact, no Canadian

financial institution required a government bailout.

41

Given their strong fundamentals, track record and operational strategies, Canadian banks are

well positioned to tap into new growth opportunities. But this can only happen if they can

quickly and cost-effectively upgrade their legacy systems and apply historically solid risk

mitigation strategies to expand into new geographies and offer ancillary products that will

enable them to incrementally improve their top and bottom lines.