CAB FINANCIAL INCLUSION CONFERENCE “PREVENTION IS BETTER THAN CURE” THE CAERPHILLY APPROACH...

25

CAB FINANCIAL INCLUSION CONFERENCE “PREVENTION IS BETTER THAN CURE” THE CAERPHILLY APPROACH Sandra Isaacs (Rents Manager) Caerphilly County Borough Council

-

Upload

norma-byles -

Category

Documents

-

view

217 -

download

0

Transcript of CAB FINANCIAL INCLUSION CONFERENCE “PREVENTION IS BETTER THAN CURE” THE CAERPHILLY APPROACH...

CAB FINANCIAL INCLUSION CONFERENCE

“PREVENTION IS BETTER THAN CURE” THE CAERPHILLY APPROACH

Sandra Isaacs (Rents Manager)Caerphilly County Borough Council

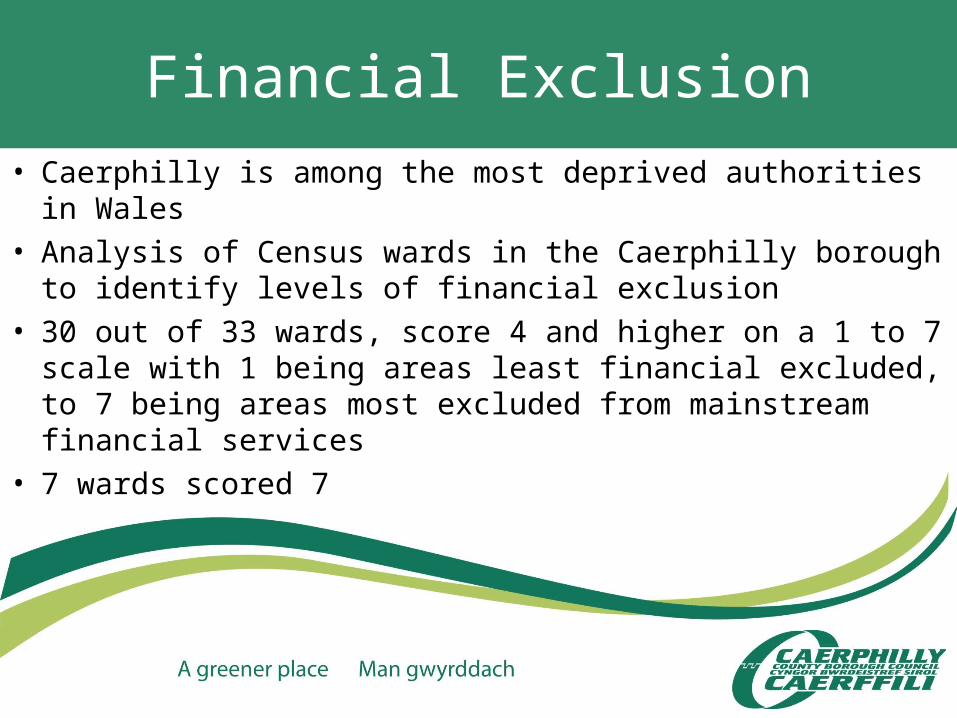

Financial Exclusion

• Caerphilly is among the most deprived authorities in Wales

• Analysis of Census wards in the Caerphilly borough to identify levels of financial exclusion

• 30 out of 33 wards, score 4 and higher on a 1 to 7 scale with 1 being areas least financial excluded, to 7 being areas most excluded from mainstream financial services

• 7 wards scored 7

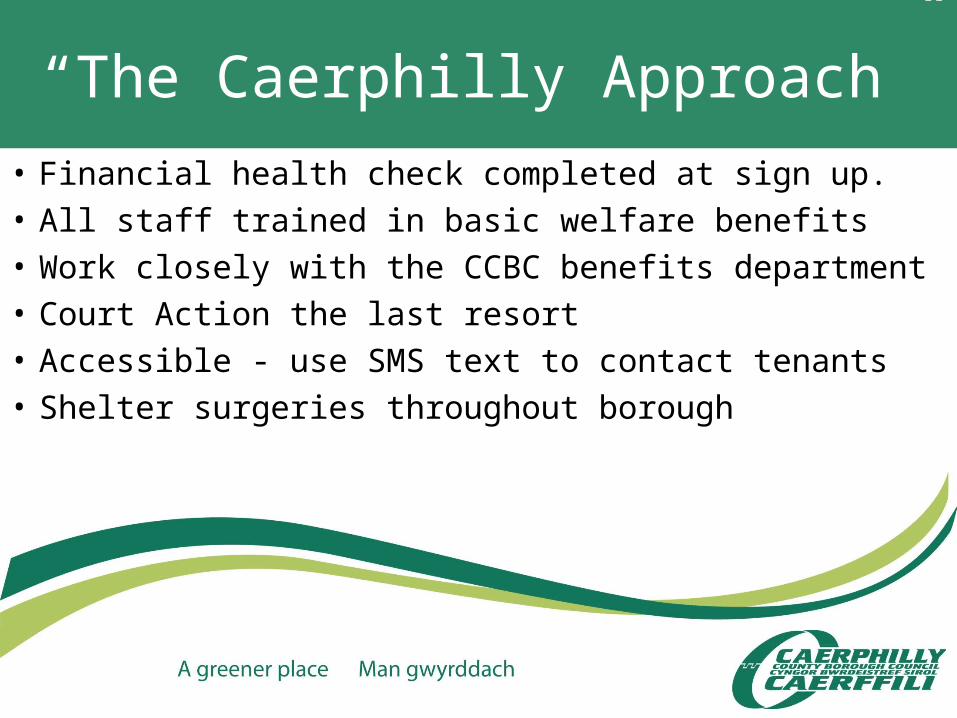

“The Caerphilly Approach”

• Financial health check completed at sign up.

• All staff trained in basic welfare benefits

• Work closely with the CCBC benefits department

• Court Action the last resort

• Accessible - use SMS text to contact tenants

• Shelter surgeries throughout borough

Key initiatives

• Money and Debt Advice clinics in partnership with CAB

• Income maximisation

• Welsh Water Assist

• Take up of tenants contents insurance

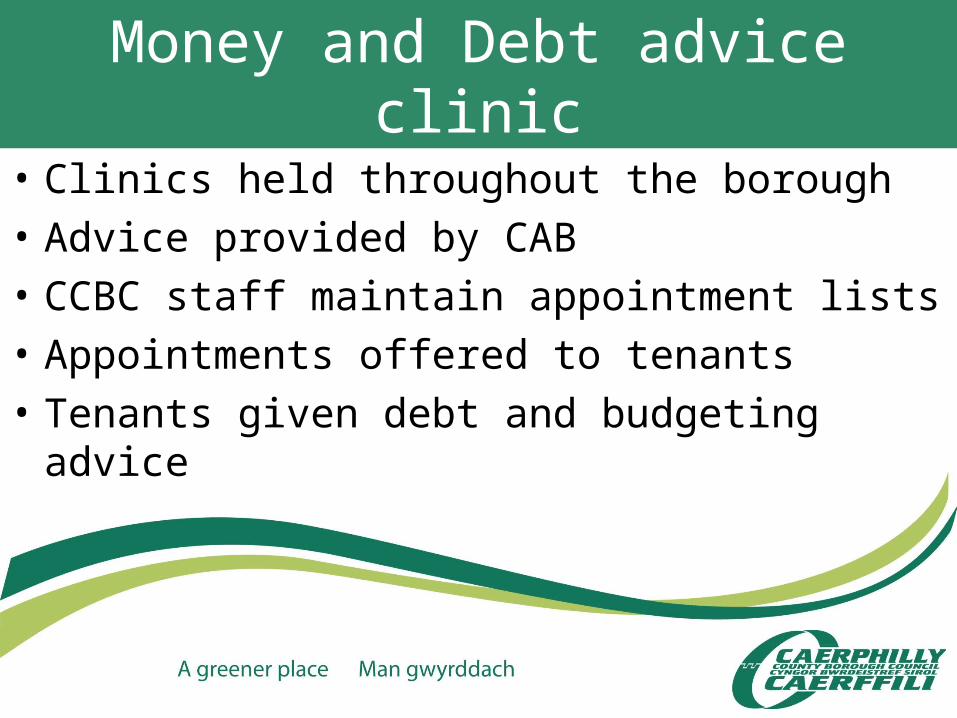

Money and Debt advice clinic

• Clinics held throughout the borough

• Advice provided by CAB

• CCBC staff maintain appointment lists

• Appointments offered to tenants

• Tenants given debt and budgeting advice

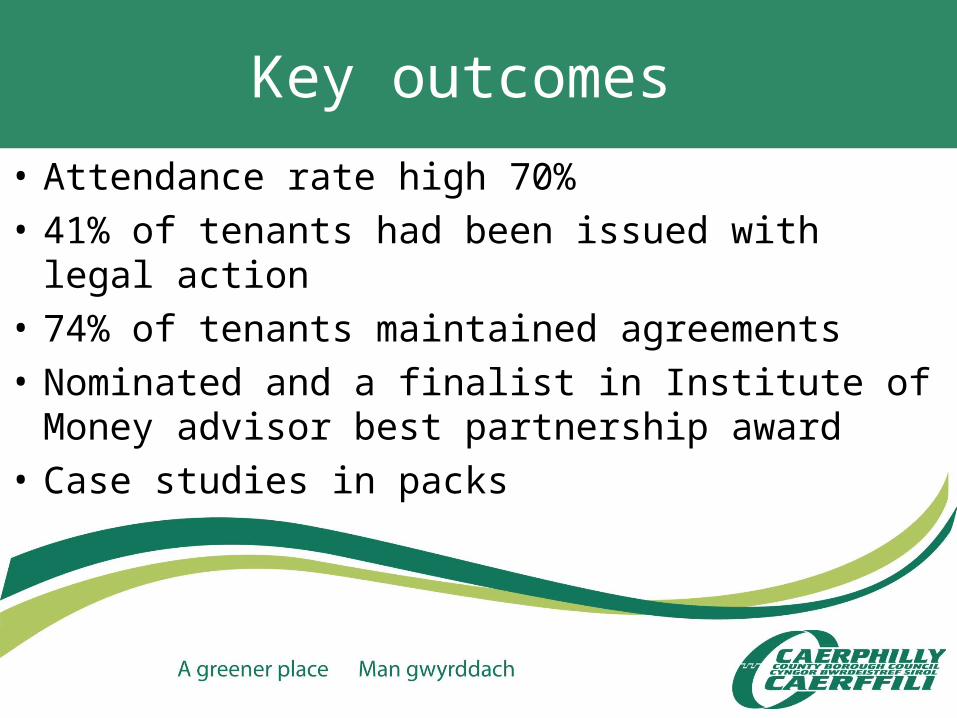

Key outcomes

• Attendance rate high 70%

• 41% of tenants had been issued with legal action

• 74% of tenants maintained agreements

• Nominated and a finalist in Institute of Money advisor best partnership award

• Case studies in packs

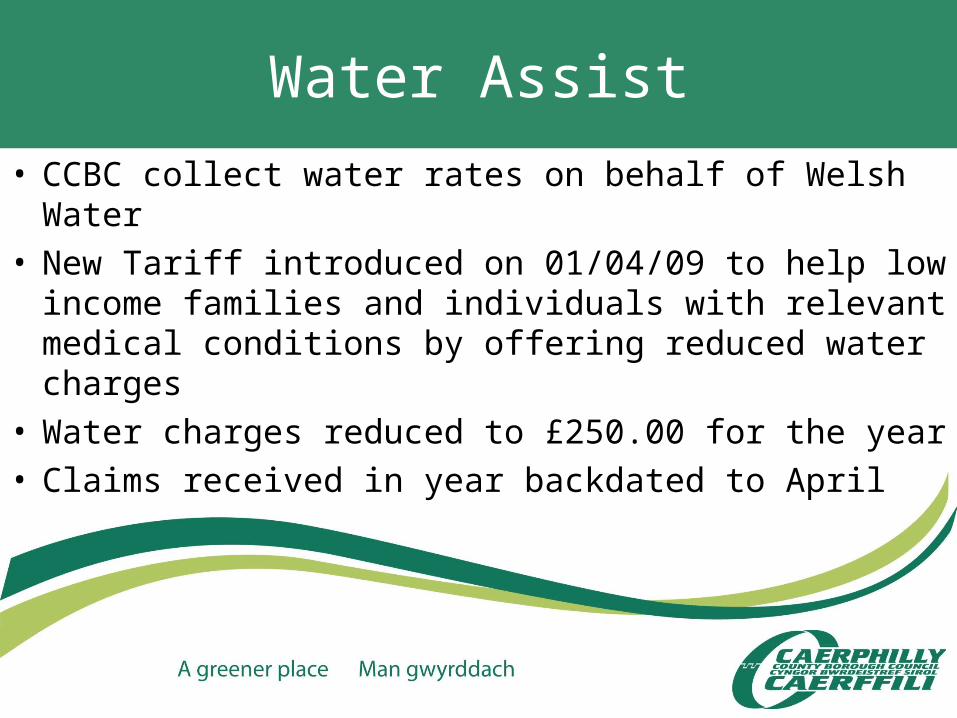

Water Assist

• CCBC collect water rates on behalf of Welsh Water• New Tariff introduced on 01/04/09 to help low income

families and individuals with relevant medical conditions by offering reduced water charges

• Water charges reduced to £250.00 for the year • Claims received in year backdated to April

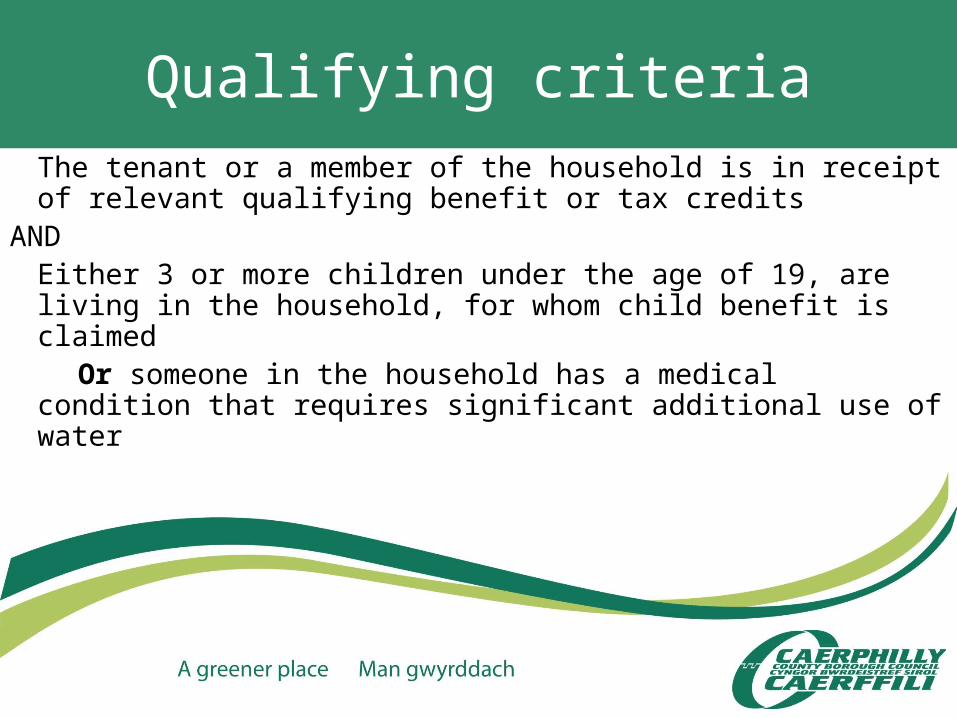

Qualifying criteria

The tenant or a member of the household is in receipt of relevant qualifying benefit or tax credits

ANDEither 3 or more children under the age of 19, are living in the household, for whom child benefit is claimed

Or someone in the household has a medical condition that requires significant additional use of water

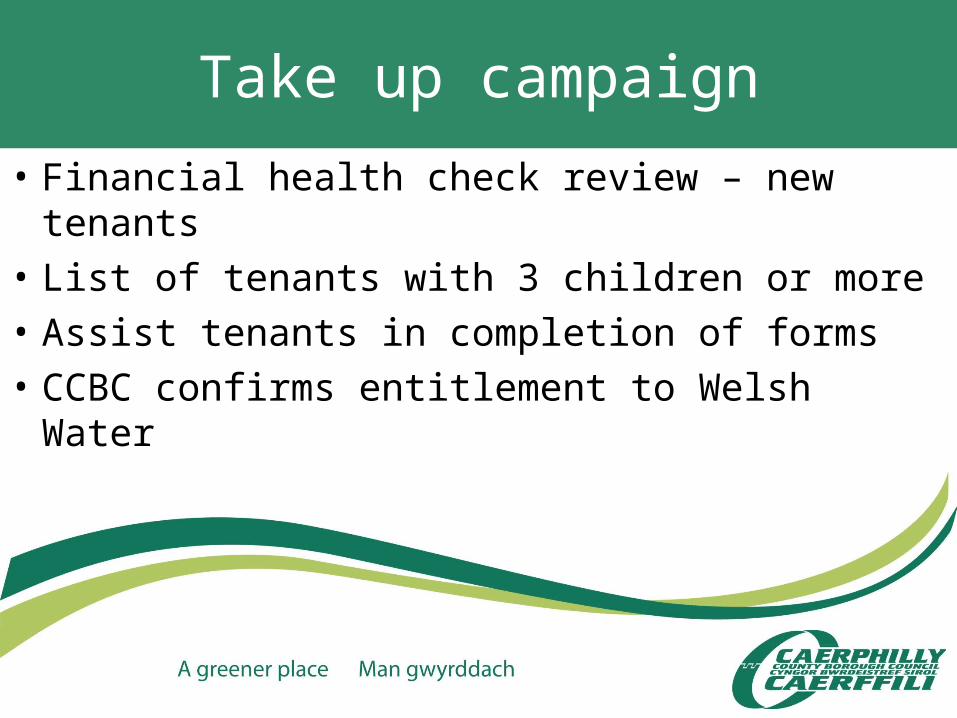

Take up campaign

• Financial health check review – new tenants

• List of tenants with 3 children or more

• Assist tenants in completion of forms

• CCBC confirms entitlement to Welsh Water

Key outcomes

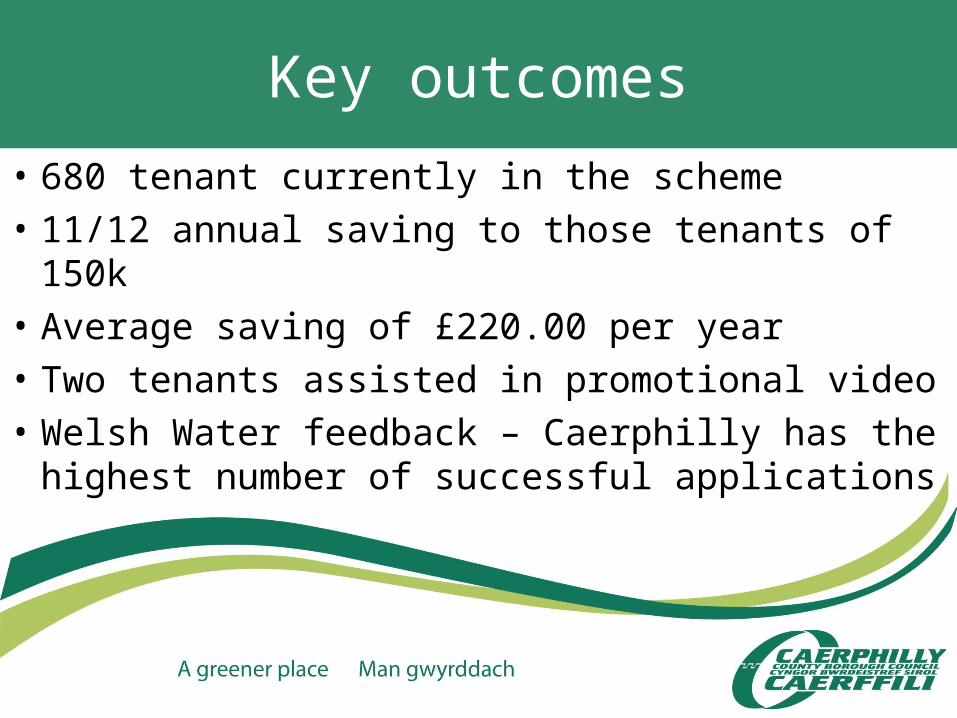

• 680 tenant currently in the scheme

• 11/12 annual saving to those tenants of 150k

• Average saving of £220.00 per year

• Two tenants assisted in promotional video

• Welsh Water feedback – Caerphilly has the highest number of successful applications

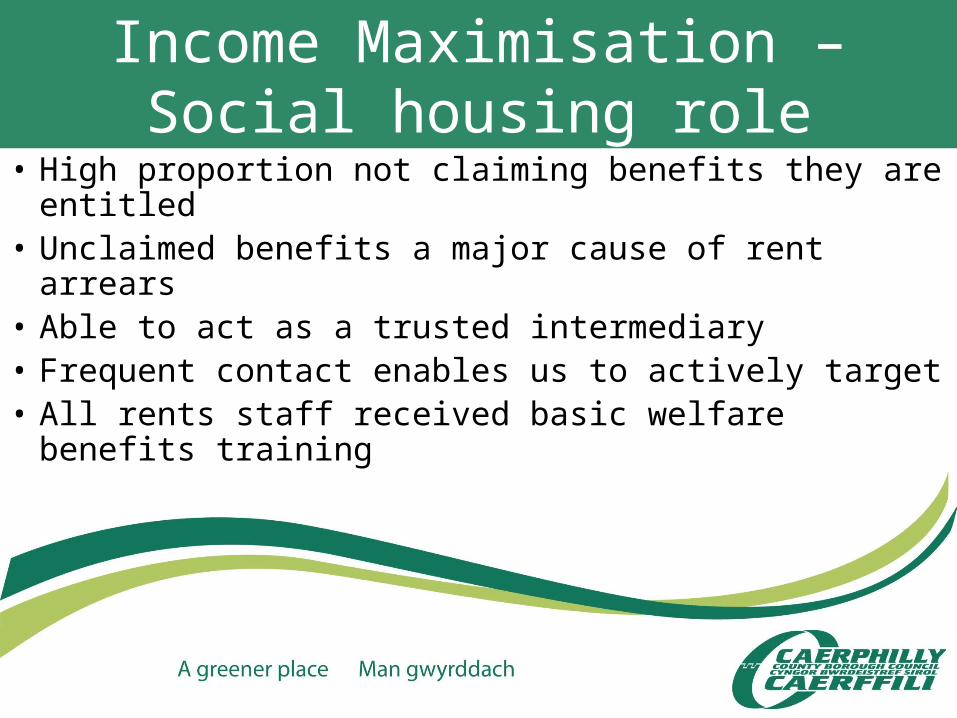

Income Maximisation – Social housing role

• High proportion not claiming benefits they are entitled

• Unclaimed benefits a major cause of rent arrears• Able to act as a trusted intermediary• Frequent contact enables us to actively target • All rents staff received basic welfare benefits

training

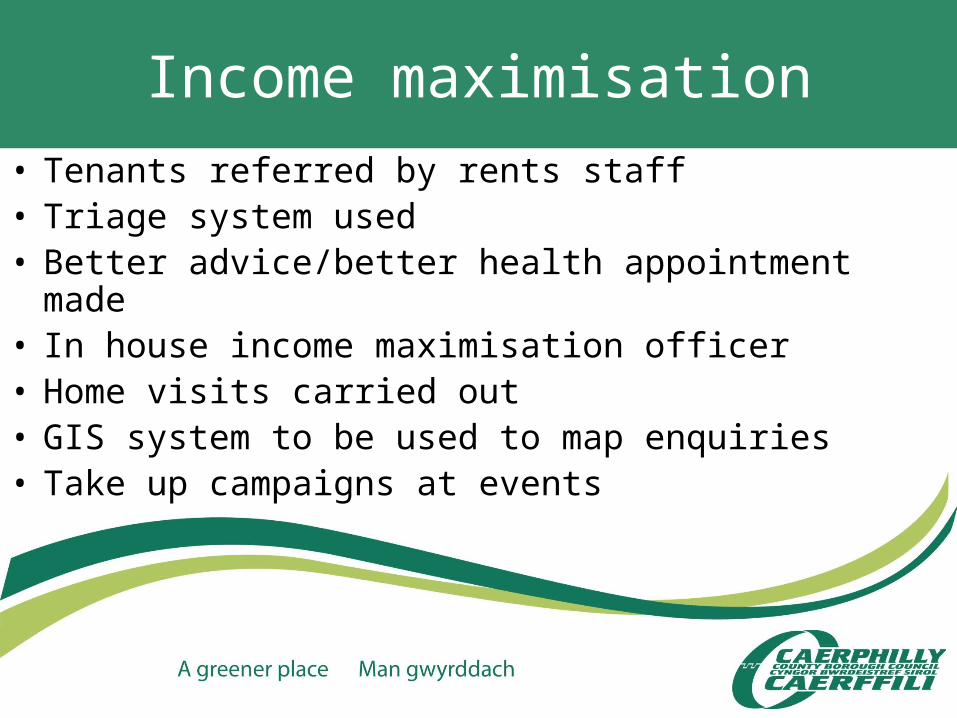

Income maximisation

• Tenants referred by rents staff • Triage system used• Better advice/better health appointment made• In house income maximisation officer • Home visits carried out• GIS system to be used to map enquiries• Take up campaigns at events

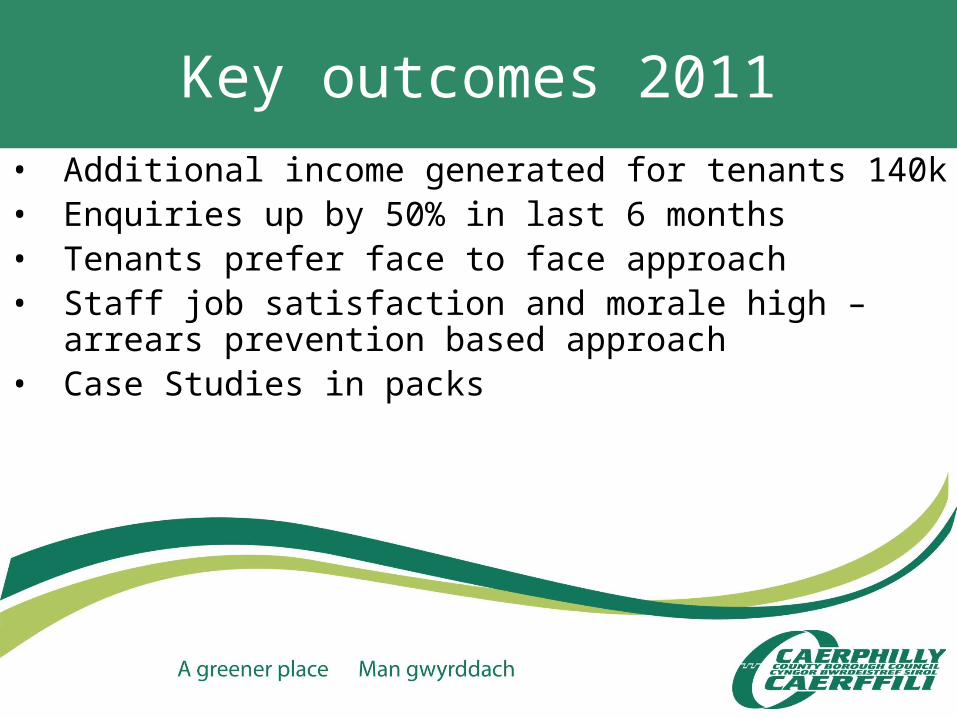

Key outcomes 2011

• Additional income generated for tenants 140k• Enquiries up by 50% in last 6 months• Tenants prefer face to face approach• Staff job satisfaction and morale high – arrears

prevention based approach• Case Studies in packs

Tenant contents insurance

• Since 1996 tenants contents scheme offered to tenants

• Scheme provided through AVIVA

• Annual insurance premiums collected 10/11 170k

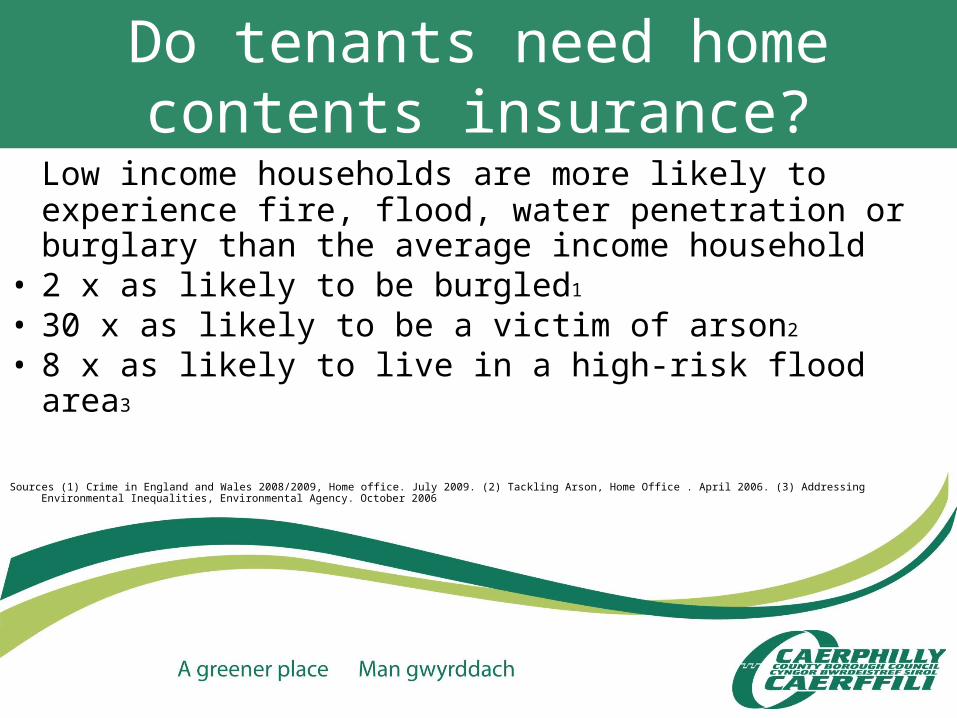

Do tenants need home contents insurance?

Low income households are more likely to experience fire, flood, water penetration or burglary than the average income household

• 2 x as likely to be burgled1

• 30 x as likely to be a victim of arson2

• 8 x as likely to live in a high-risk flood area3

Sources (1) Crime in England and Wales 2008/2009, Home office. July 2009. (2) Tackling Arson, Home Office . April 2006. (3) Addressing Environmental Inequalities, Environmental Agency. October 2006

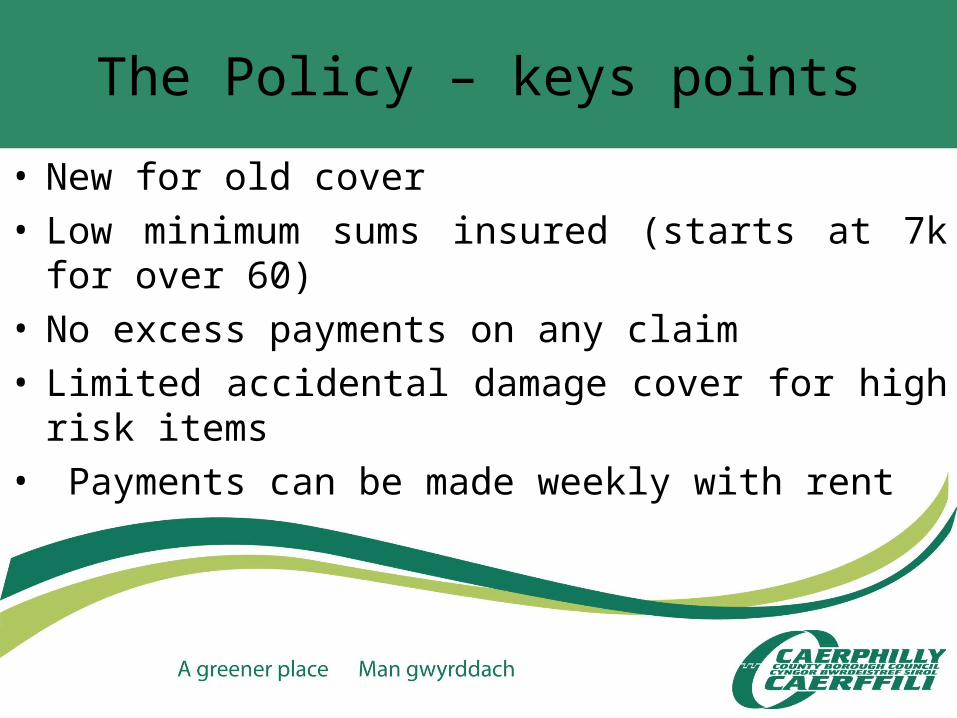

The Policy – keys points

• New for old cover• Low minimum sums insured (starts at 7k for over 60)• No excess payments on any claim• Limited accidental damage cover for high risk items• Payments can be made weekly with rent

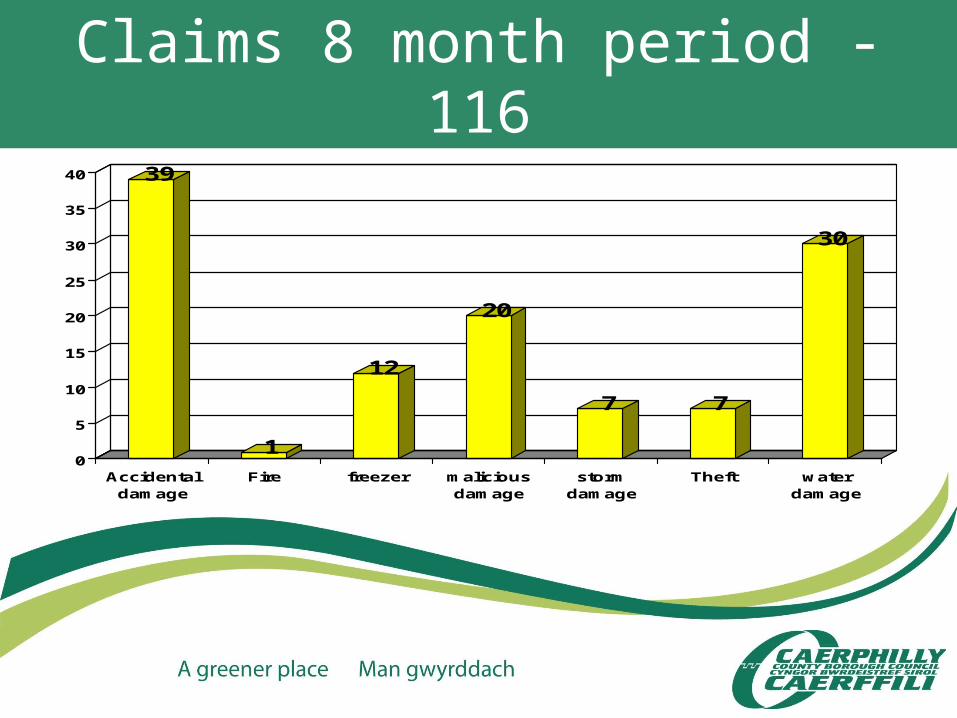

Claims 8 month period - 11639

1

12

20

7 7

30

0

5

10

15

20

25

30

35

40

Accidentaldamage

Fire freezer maliciousdamage

stormdamage

Theft waterdamage

Barriers

• Considered to be too expensive• Self exclusion – people decide there is little point applying as

they believe they would be refused• Carefree – believe insurance is only for those with something to

worry about ie for people with large number of possessions • Confusion – people with poor financial capability can struggle to

decode financial information• Mistrust of insurance companies

The Caerphilly approach to promotion of scheme

• All front line staff trained • Scheme discussed with tenants at initial sign up as part of

financial risk assessment• During one month and 3 month settling in visits• Each time a tenant is contacted i.e. either face to face or over

the phone• Insurance road shows held at sheltered accommodation• GIS mapping used to target areas with low take up of tenants

contents insurance

Why is take up high?

• Tenants trust us as an intermediary rather than a direct relationship with the insurance company

• Our scheme popularity travels by word of mouth, a form of recommendation people trust

• Personal face to face approach• Key training provided to all front line staff

Key Outcomes

• 24% of tenants are in the scheme

• One of the highest percentage in UK

• Tenants trust us as an intermediary rather than a direct relationship with the insurance company

And Finally……Caerphilly Approach – key themes

• Partnership working• Removing barriers• Early intervention• Measuring Outcomes

Future challenge - Welfare Reform Act

• Reduction in HB for tenants under occupying– tenant profiling exercise– GIS mapping of under occupation

• Universal Credit – direct payments– work with credit unions

ANY QUESTIONS?