Www.cabi.org KNOWLEDGE FOR LIFE CABI product training CAB Abstracts - Advanced searching Tom Corser.

CAB

Advanced Financial

Management

Unit : I - V

UNIT I - SYLLABUS

Definition, scope and functions of Financial Management-

Objectives of firm

An outline of Financial System in India

Regulation of SEBI regarding Capital issues and stock

exchanges.

CAB – Advanced Financial Management 2

TM

CAB – Advanced Financial Management

ENVIRONMENT OF CORPORATE FINANCE

Corporate finance consists of the financial activities related to

running a corporation, usually with a division or department set

up to oversee the financial activities. Corporate finance is

primarily concerned with maximizing shareholder value through

long-term and short-term financial planning and the

implementation of various strategies. Everything from capital

investment decisions to investment banking falls under the

domain of corporate finance.

https://www.youtube.com/watch?v=Tdu0QPfoYZQ

3

What is Advanced

Financial Management?

Concerns the acquisition, financing, and

management of assets with some overall goal

in mind.

CAB – Advanced Financial Management

Definitions

Finance management

J.F. Bradlery :-“financial business finance

can be broadly defined as the activity

concerned with the planning, raising,

controlling and administering the funds used

in the business”.

4

“Advanced Financial Management is concerned with the

efficient use of an important economic resource, namely

capital funds”. – Solomon

“Advanced Financial Management is the application of the

planning and control function to the finance function”.- Archer

and Ambrosio

Meaning of Advanced Financial Management

Advanced Financial Management is application of principles of

management to the subject called finance , it involves planning,

controlling decision making with respect to finance activity of the

business .

Video link: https://www.youtube.com/watch?v=jr_Njrgajb0

Definition of Advanced

Financial Management

CAB – Advanced Financial Management 5

Objectives of Advanced

Financial Management

Video link: https://www.youtube.com/watch?v=75dPbNemehk

CAB – Advanced Financial Management 6

Scope of Advanced Financial

Management

(i) Traditional Approach:

a) The traditional approach to scope of Advanced Financial Management refers to its subject matter in the academic literature in the initial stage of its evolution as a separate branch of study confined to raising of funds.

b) The subject was called Corporate finance till the mid 1950‟s and covered discussion on financial instruments, institutions and practices through which funds are obtained.

c) The problem of raising funds is more intensely felt at certain episodic events such as merger, liquidation, consolidation, reorganisation and so on.

CAB – Advanced Financial Management 7

(ii) Modern approach

• The approach and utility of Advanced Financial Managementhas started changing in a revolutionary manner, after 1950.

• The emphasis was shifted from raising of funds to effective andjudicious utilisation of funds.

• Financial decisions have a great impact on all other businessactivities, the finance manager should be concerned aboutdetermining the size and nature of technology, setting thedirection and growth of the business, shaping the profitability,capital structure etc.

• The modern approach is thus an analytical way of viewing the

financial problems of a firm.

• The modern financial manager has to take financial decisions in

the most rational way. These decisions are to be made in such a

way that the funds of the firm are used optimally.

CAB – Advanced Financial Management 8

Nature of Advanced

Financial Management

• FM is an area of decision making in finance function of the business.

• It is descriptive/ theoretical/ statistical/ historical and analytical in nature.

• It involves application of management principles to the finance function.

• It is applicable to every organization irrespective of its size, nature, place.

• It deals with accumulation and utilization of financial resources (business resources).

• It is directed towards achieving business objectives.

CAB – Advanced Financial Management 9

Scope of Advanced

Financial Management.

1.Estimating financial requirements

2.Deciding capital structure

3.Selecting source of finance

4.Selecting pattern of investment

5.Cash management

6.Profit management

7.Ensuring liquidity

8. Meeting statuary requirement.

CAB – Advanced Financial Management 10

CAB – Advanced Financial Management

Indian Financial System

https://www.slideshare.net/divyaactive/indian-financial-system-ppt

Financial system of a country consists of a network of inter connected

system of markets, institutions and services

It connects the savings-surplus and savings-deficit institutions and

establishes a regular flow of funds in the capital market of a country.

11

CAB – Advanced Financial Management

REGULATION OF SEBI

REGARDING CAPITAL ISSUES &

STOCK EXCHANGESSEBI Guidelines for issue of fresh share capital

1. All applications should be submitted to SEBI in the prescribed form.

2. Applications should be accompanied by true copies of industrial license.

3. Cost of the project should be furnished with scheme of finance.

4. Company should have the shares issued to the public and listed in one or

more recognized stock exchanges.

5. Where the issue of equity share capital involves offer for subscription by the

public for the first time, the value of equity capital, subscribed capital privately

held by promoters, and their friends shall be not less than 15% of the total

issued equity capital.

12

CAB – Advanced Financial Management

Contd…

6. An equity-preference ratio of 3:1 is allowed.

7. Capital Cost of the projects should be as per the standard set with a

reasonable debt-equity ratio.

8. New company cannot issue shares at a premium. The dividend on

preference shares should be within the prescribed list.

9. All the details of the underwriting agreement

10. Allotment of shares to NRIs is not allowed without the approval of RBI.

11. Details of any firm allotment in favor of any financial institutions.

12. Declaration by secretary or director of the company.

13

CAB – Advanced Financial Management

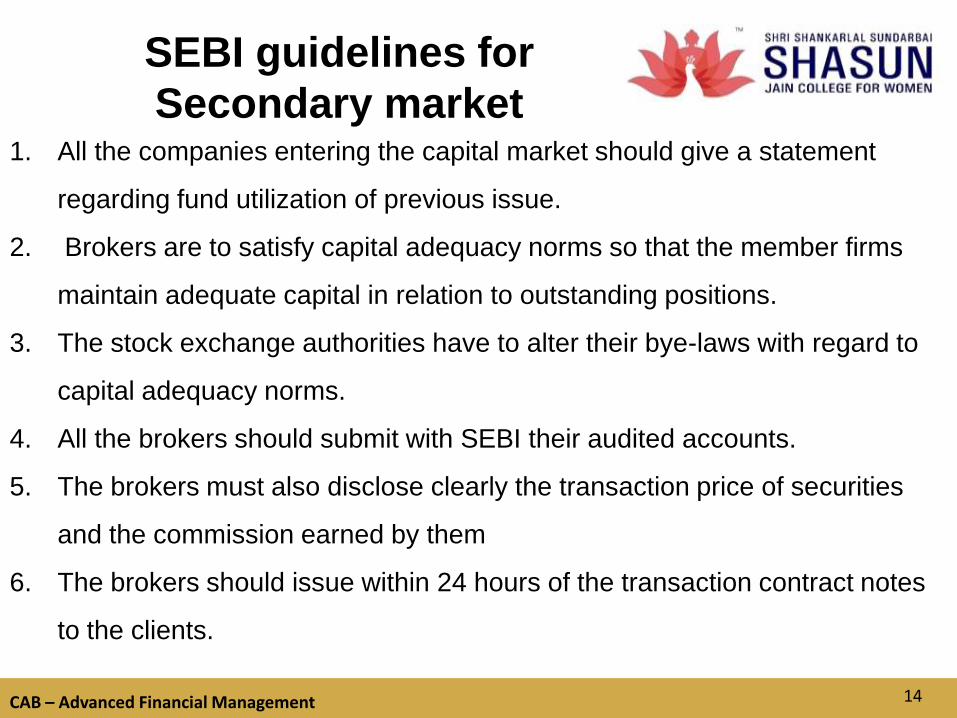

SEBI guidelines for

Secondary market1. All the companies entering the capital market should give a statement

regarding fund utilization of previous issue.

2. Brokers are to satisfy capital adequacy norms so that the member firms

maintain adequate capital in relation to outstanding positions.

3. The stock exchange authorities have to alter their bye-laws with regard to

capital adequacy norms.

4. All the brokers should submit with SEBI their audited accounts.

5. The brokers must also disclose clearly the transaction price of securities

and the commission earned by them

6. The brokers should issue within 24 hours of the transaction contract notes

to the clients.

14

CAB – Advanced Financial Management

SEBI guidelines for

Secondary market

7. Margin money on certain securities has to be paid by claims so

that speculative investments are prevented.

8. Market makers are introduced for certain scrips by which brokers become

responsible for the supply and demand of the securities and the price of the

securities is maintained.

9. A broker cannot underwrite more than 5% of the public issue.

10. All transactions in the market must be reported within 24 hours to SEBI.

11. The brokers of Bombay and Calcutta must have a capital adequacy of Rs. 5

lakhs and for Delhi and Ahmadabad it is Rs. 2 lakhs.

12. Members who are brokers have to pay security deposit and this is fixed by

SEBI.

15

CAB – Advanced Financial Management

SEBI Guidelines for first

issue by new companies in

Primary Market

• A new company which has not completed 12 months of commercial

operations will not be allowed to issue shares at a premium

• If an existing company with a 5-year track record of consistent

profitability, is promoting a new company, then it is allowed to price its

issue.

• A draft of the prospectus has to be given to the SEBI before public issue.

• The shares of the new companies have to be listed either withOTCEI or

any other stock exchange.

16

CAB – Advanced Financial Management

UNIT II - SYLLABUS

Firm‟s Investment Decisions Practical application of

Capital Budgeting

Project Appraisal and evaluation methods

Risk Analysis in Investment Appraisal

17

TM

CAB – Advanced Financial Management

18

In the terminology of Advanced Financial Management, the

investment decision means capital budgeting. Investment decision

and capital budgeting are not considered different acts in

business world. In investment decision, the word „Capital‟ is

exclusively understood to refer to real assets which may assume

any shape viz. building, plant and machinery, raw material and so

on and so forth, whereas investment refers to any such real

assets.

Investment decisions

TM

CAB – Advanced Financial Management 19

Capital investment appraisal, also known as capital budgeting is primarily

a planning process which facilitates the determination of the concerned

firm's investments, both long term and short term. The components of the

firm that come under this kind of capital investment appraisal include

property, equipment, R & D projects, advertising campaigns, new plants,

new machinery etc. Thus in simple words, capital investment appraisal is

the budgeting of major capital and investment to company expenditure.

Investment Appraisal Methods

https://www.youtube.com/watch?v=4arxW7nO8zc

TM

CAB – Advanced Financial Management 20

RISK & UNCERTAINITY IN INVESTMENT

DECISION

Risks and uncertainties are inevitable in engineering projects and

infrastructure investments. Decisions about investment in infrastructure

such as for maintenance, rehabilitation and construction works can pose

risks, and may generate significant impacts on social, cultural,

environmental and other related issues. This report presents the results of

a literature review of current practice in identifying, quantifying and

managing risks and predicting impacts as part of the planning and

assessment process for infrastructure investment proposals.

TM

CAB – Advanced Financial Management 21

Capital rationingis a common practice in most of the companies as they

have more profitable projects available for investment as compared to the

capital available. In theory, there is no place for capital rationing as

companies should invest in all the profitable projects. However, a majority

of companies follow capital rationing as a way to isolate and pick up the

best projects under the existing capital restrictions.

Capital Rationing

CAB – Advanced Financial Management

Capital Budgeting

Capital budgeting (or investment appraisal) is the process of determining

the viability to long-term investments on purchase or replacement of

property plant and equipment, new product line or other projects.

22

CAB – Advanced Financial Management

Techniques of Capital

Budgeting

Payback Period measures the time in which the initial cash flow is

returned by the project. Cash flows are not discounted. Lower payback

period is preferred.

Net Present Value (NPV) is equal to initial cash outflow less sum of

discounted cash inflows. Higher NPV is preferred and an investment is

only viable if its NPV is positive.

Accounting Rate of Return (ARR) is the profitability of the project

calculated as projected total net income divided by initial or average

investment. Net income is not discounted.

Internal Rate of Return (IRR) is the discount rate at which net present

value of the project becomes zero. Higher IRR should be preferred.

Profitability Index (PI) is the ratio of present value of future cash flows of

a project to initial investment required for the project.

23

CAB – Advanced Financial Management

Risk Analysis in

Investment Appraisal

https://www.slideshare.net/himanshujaiswal/risk-analysis-in-investment

24

*

*

18-25CAB – Advanced Financial Management

Project Appraisal

25

*

*

18-26CAB – Advanced Financial Management

Risk Analysis

26

CAB - Advanced Financial Management

UNIT III- SYLLABUS

Firm‟s Decision and Capital Structure

Sources of long term and short term Finance

Designing Capital Structure

Practical consideration in determining capital

structure

Capital Structure theories

27

Capital Structure

Definition : Capital Structure is the mix of financial securities used to

finance the firm.

• The value of a firm is defined to be the sum of the value of the

firm‟s debt and the firm‟s equity.

• V = B + S

• If the goal of the management of the firm is to make the firm as

valuable as possible, then the firm should pick the debt-equity ratio

that makes the pie as big as possible.

Capital structure

CAB – Advanced Financial Management

Value of the Firm

28

FACTOR INFLUENCING

CAPITAL STRUCTURE

Business Risk

Company Tax exposure

Financial Flexibility

Management Style

Growth Rate

Market Condition

Cost of Fixed Assets

Size of Business Organization

Nature of business Organization

Elasticity of Capital Structure

CAB – Advanced Financial Management 29

Sources of Short term and

Long Term Finance

CAB – Advanced Financial Management 30

CAB – Advanced Financial Management

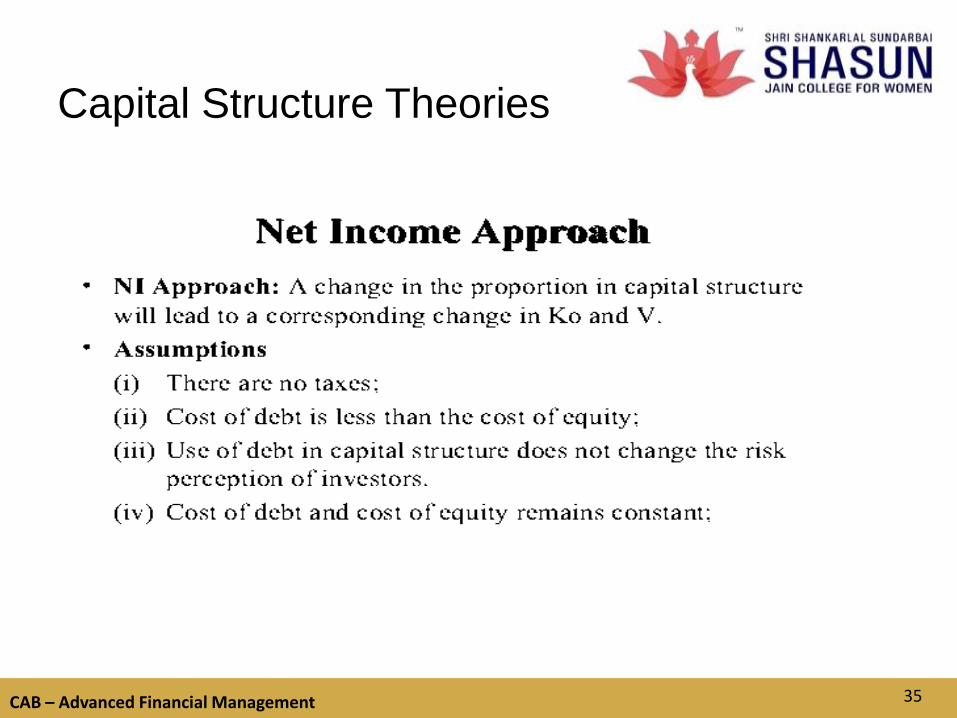

Theories of Capital Structure

Net Operating Income

Approach

Traditional Approach

Modigliani and Miller Approach

Net Income Approach

31

Assumption of Capital

Structure Theories

There are only two sources of funds i.e.: debt and equity.

• The total assets of the company are given and do no change.

• The total financing remains constant. The firm can change the

degree of leverage either by selling the shares and retiring debt or by

issuing debt and redeeming equity.

• Operating profits (EBIT) are not expected to grow.

• All the investors are assumed to have the same expectation about

the future profits.

• Business risk is constant over time and assumed to be independent

of its capital structure and financial risk.

• Corporate tax does not exit. The company has infinite life. Dividend

payout ratio = 100%.

CAB – Advanced Financial Management 32

CAB – Advanced Financial Management 33

Capital Structure Theories

CAB – Advanced Financial Management 34

Capital Structure Theories

CAB – Advanced Financial Management 35

Capital Structure Theories

CAB – Advanced Financial Management 36

Capital Structure Theories

CAB – Advanced Financial Management 37

Capital Structure Theories

CAB – Advanced Financial Management 38

MM APPROACH

CAB – Advanced Financial Management

MM APPROACH

FORMULA

39

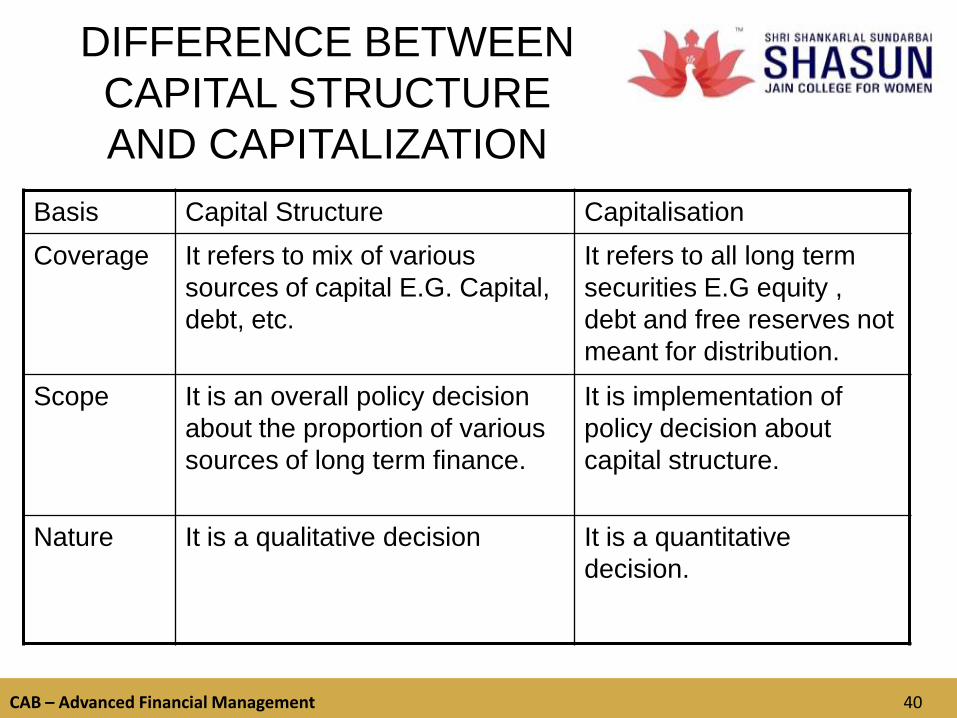

DIFFERENCE BETWEEN

CAPITAL STRUCTURE

AND CAPITALIZATION

Basis Capital Structure Capitalisation

Coverage It refers to mix of various

sources of capital E.G. Capital,

debt, etc.

It refers to all long term

securities E.G equity ,

debt and free reserves not

meant for distribution.

Scope It is an overall policy decision

about the proportion of various

sources of long term finance.

It is implementation of

policy decision about

capital structure.

Nature It is a qualitative decision It is a quantitative

decision.

CAB – Advanced Financial Management 40

Cost of Capital – Meaning, significance and concept of

cost retained earnings

Weighted Average cost of Capital

Leverages – Operating, Financial and Combined

Leverages

CAB – Advanced Financial Management

UNIT IV - SYLLABUS

41

Cost of capital

The rate of return that a firm must earn on the projects in which it invests

to maintain its market value and attract funds.

DEFINITION

COST OF CAPITAL IS THE MINIMUM RATE OF RETURN WHICH A

FIRM REQUIRES AS A CONDITION FOR UNRERTAKING AN

INVESTMENT.

MILTON H.SPENCER

CAB – Advanced Financial Management 42

COMPONENTS OF COST

OF CAPITAL

i) RETURN AT ZERO RISK

ii) PREMIUM FOR BUSINESS RISK

iii) PREMIUM FOR FINANCIAL RISK

IMPORTANCE

1.CAPITAL BUDGETING DECISION

2.DESIGNING THE CAPITAL STRUCTURE

3.DECIDING ABOUT THE METHOD OF FINANCING

4.PERFORMANCE OF TOP MANAGEMENT

CAB – Advanced Financial Management 43

FACTORS DETERMINING

THE COST OF CAPITAL

1.General economic conditions

2.Market conditions

3. Operating and financing decisions

4. Amount of financing

TYPES OF COST OF CAPITAL

Historical cost and future cost

Explicit cost and implicit cost

Specific cost and composite cost

Average cost and marginal cost

CAB – Advanced Financial Management 44

COMPUTATION OF COST

OF CAPITAL

1.COST OF DEBT

Video link: http://study.com/academy/lesson/capital-structure-the-

cost-of-capital.html

THE COST OF DEBT IS OF TWO TYPES

a. COST OF IRREDEEMABLE DEBT

b. COST OF REDMEEABLE DEBT

CAB – Advanced Financial Management 45

COMPUTATION OF COST

OF CAPITAL

CAB – Advanced Financial Management 46

COMPUTATION OF COST

OF CAPITAL

CAB – Advanced Financial Management 47

COMPUTATION OF COST

OF CAPITAL

CAB – Advanced Financial Management 48

COMPUTATION OF COST

OF CAPITAL

CAB – Advanced Financial Management 49

COMPUTATION OF

PREFERENCE SHARE

CAPITALVIDEO LINK:

https://www.slideshare.net/akankshagupta963871/new-

microsoft-office-power-point-presentation-32612359

CAB – Advanced Financial Management 50

CAB – Advanced Financial Management

COMPUTATION OF

PREFERENCE SHARE

CAPITAL

51

CAB – Advanced Financial Management

COMPUTATION OF

WEIGHTED AVERAGE

COST OF CAPITAL

52

CAB – Advanced Financial Management

Leverages

• James Horne defines “Leverage is the employment of an asset or

funds for which the firm pays a fixed cost or fixed return”.

• Leverage is the result of employment of an asset or funds having a

fixed cost of return .

• VIDEO LINK: http://study.com/academy/lesson/leverage-ratios-

types-formula.html

53

CAB – Advanced Financial Management

Types of Leverage

Operating

Financial

Combined

54

CAB – Advanced Financial Management

Operating Leverage

• OL =Contribution / EBIT

• DOL=Percent change in EBIT

Percent change in Sales

Financial Leverage

• FL=EBIT/EBT

• DFL=Percent change in EPS

Percent change in EBIT

55

CAB – Advanced Financial Management

Combined Leverage

OPERATING LEVERAGE X FINANCIAL LEVERAGE

CONTRIBUTION EBIT CONTRIBUTION----------------------- X -------- = ----------------------

EBIT EBT EBIT

56

UNIT V- SYLLABUS

Dividend Policy: Behavioural models of

dividend policy

Factors affecting dividend policy

Theories of dividend

CAB – Advanced Financial Management 57

Dividend

Dividend policy is the set of guidelines a company uses to decide how

much of its earnings it will pay out to shareholders. Some evidence

suggests that investors are not concerned with a company'sdividend

policy since they can sell a portion of their portfolio of equities if they

want cash

Definition

“A dividend is a distribution to shareholders out of profit or reserve

available for this purpose”.

-Institute of Chartered Accountants of India

-VIDEO LINK : http://study.com/academy/lesson/dividend-definition-

lesson-quiz.html

CAB – Advanced Financial Management 58

TYPES OF DIVIDEND

1.Regular dividend

2. Interim dividend

3.Stock dividend

4.Bond dividend

5.Property dividend

CAB – Advanced Financial Management 59

Determinants of dividend

policy

CAB – Advanced Financial Management

i. Dividend Pay-out Ratio:It indicates the proportion of earnings

distributed as dividend. Lower dividend pay-out ratio indicates

conservative dividend policy.

ii. Stability of Dividend: Stable dividend policy which means they

require a certain minimum percentage of dividends to be paid

regularly to them.

iii. Liquidity: Payment of dividend requires availability of cash

resources. Future investment opportunities should also be taken

into consideration. iv. Divisible Profit: This means dividend can

be declared out of divisible profit, i.e. the profit which is legally

available for distribution as dividend to the shareholders.

v. Legal Constraints: All requirements of The Company‟s Act and

SEBI guidelines must be kept in mind before declaring dividend.

60

• vi. Owner’s Consideration: Tax statuses of shareholders,

availability of investment opportunities, ownership dilutions, etc.,

are the different factors that affect shareholders.

• vii. Capital Market Conditions and Inflation: Capital market

conditions and inflation play a dominant role in developing the

dividend policy.

Objectives of Dividend Policy:i. Wealth Maximization: Dividend policy should be developed

keeping in mind the wealth maximization objective of the firm.

ii. Future Prospects: Dividend policy is a financing decision and

leads to cash outflows and also leads to decrease in availability of

cash for financing of profitable projects.

CAB – Advanced Financial Management

Determinants of dividend

policy

61

CAB – Advanced Financial Management

Objectives of Dividend

Policy

iii. Stable Rate of Dividend: Fluctuation in the rate ofreturn adversely affects the market price of shares.iv. Degree of Control: Issue of new shares or dependenceon external financing will dilute the degree of control of theexisting shareholders.

NATURE OF DIVIDEND POLICY

1.Stability of earnings

2.Age of firm

3. Regularity and stability in dividend

payment

4. Time for payment of dividend

5. Liquidity of funds

62

NATURE OF DIVIDEND

POLICY

6. Policy of control

7. Repayment of loan

8. Government policies

9. Legal requirements

10. Trade cycles

11. Need for additional capital

12. Ability to borrow

13. Extent of share distribution

14. Past dividend rates

CAB – Advanced Financial Management 63

CAB – Advanced Financial Management

Dividend Theories

Relevance Theories

(i.e. which considerdividend decision to berelevant as it affects thevalue of the firm)

Walter‟s Model

Gordon‟s Model

Irrelevance Theories

(i.e. which consider dividend decision to be irrelevant as it does not affects the value of the

firm)

Modigliani andMiller‟s Model

Traditional Approach

64

CAB – Advanced Financial Management

Prof. James E Walter argued that in the long- run the share prices

reflect only the present value of expected dividends. Retentions

influence stock price only through their effect on future dividends.

Walter has formulated this and used the dividend to optimize the

wealth of the equity shareholders.

Assumptions of Walter‟s Model:

Internal Financing

constant Return in Cost of Capital

100% payout or Retention

Constant EPS and DPS

Infinite time

Walter’s Model

65

CAB – Advanced Financial Management 66

Walter‟s Model

CAB – Advanced Financial Management

Criticisms of Walter‟s Model

No External Financing

Firm‟s internal rate of return does not always remain

constant. In fact, r decreases as more and more

investment in made.

Firm‟s cost of capital does not always remain constant. In

fact, k changes directly with the firm‟s risk.

67

CAB – Advanced Financial Management

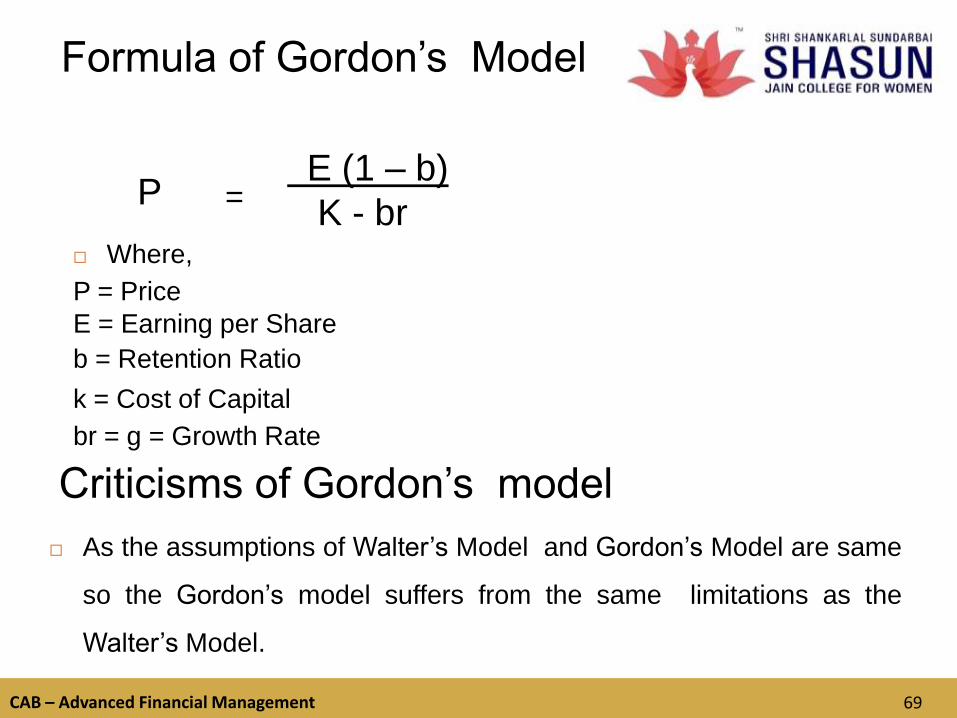

Gordon‟s Model

According to Prof. Gordon, Dividend Policy almost always affectsthe value of the firm. He Showed how dividend policy can beused to maximize the wealth of the shareholders.

Assumptions:

All equity firm

No external Financing

Constant Returns

Constant Cost of Capital

Perpetual Earnings

No taxes

Constant Retention

Cost of Capital is greater then growth rate (k>br=g)

68

CAB – Advanced Financial Management

Formula of Gordon‟s Model

Where,

P = Price

E = Earning per Share

b = Retention Ratio

k = Cost of Capital

br = g = Growth Rate

P =E (1 – b)

K - br

Criticisms of Gordon‟s model

As the assumptions of Walter‟s Model and Gordon‟s Model are same

so the Gordon‟s model suffers from the same limitations as the

Walter‟s Model.

69

CAB – Advanced Financial Management

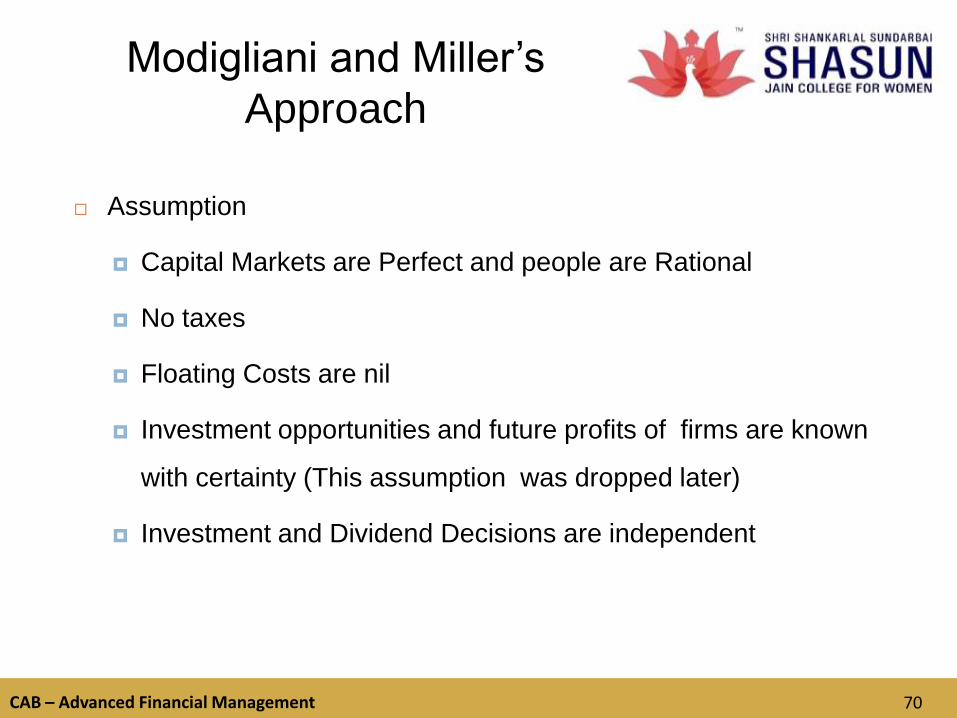

Modigliani and Miller‟s

Approach

Assumption

Capital Markets are Perfect and people are Rational

No taxes

Floating Costs are nil

Investment opportunities and future profits of firms are known

with certainty (This assumption was dropped later)

Investment and Dividend Decisions are independent

70

CAB – Advanced Financial Management

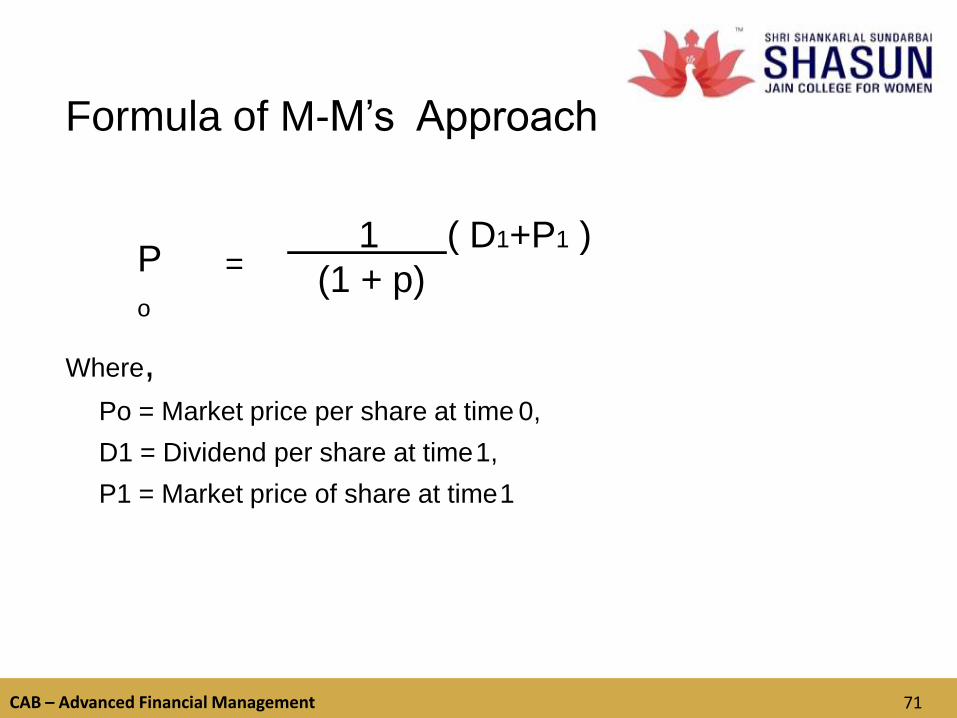

Formula of M-M‟s Approach

=1 ( D1+P1 )

(1 + p)P

o

Where,Po = Market price per share at time 0,

D1 = Dividend per share at time1,

P1 = Market price of share at time1

71

CAB – Advanced Financial Management

Criticism of M-M

Model

No perfect Capital Market

Existence of Transaction Cost

Existence of Floatation Cost

Lack of Relevant Information

Differential rates of Taxes

No fixed investment Policy

Investor‟s desire to obtain income

72

UNIT VI - SYLLABUS

Working Capital Management

Theories Vs Practice – principles of working capital

Working Capital forecast

Individual Current Asset Management

CAB – Advanced Financial Management 73

What is working capital?

Working capital is calculated by subtracting current liabilities from

current assets. Current assets include cash, marketable securities,

inventory, accounts receivable and other short-term assets to be used

within the year

CAB – Advanced Financial Management 74

CAB – Advanced Financial Management

Estimation of Required Working Capital…

For estimation of working capital, following four step procedure is

applicable:

Estimation of cash cost of the various current assets required

by the firm.

Estimation of current liabilities of the firm.

Calculation of net working capital.

Add percentage of contingency.

http://study.com/academy/lesson/how-to-calculate-net-working-

capital-definition-formula.html

https://www.youtube.com/watch?v=eaGgCJtHxuE

75

CAB – Advanced Financial Management

Cont… Raw Material = Budgeted Production in Units * Raw Material Cost

per unit * Average Raw material Holding Period / 12 months or 365

days.

WIP = Budgeted Production in Units * Estimated WIP Cost per unit *

Average WIP Holding Period / 12 months or 365 days.

Finished Goods Inventory = Budgeted Production in Units * Cost

of Goods produced * finished Goods Holding period / 12 months or

365 days.

Investment in Debtors = Budgeted Credit Sales in Unit * Cost of

Sales per Unit * Average Debt Collection Period / 12 months or 365

days.

76

CAB – Advanced Financial Management

Estimation of Current

Liabilities…

Creditors = Budgeted Production in Units * Raw Material Cost per

unit * Credit period Allowed by Suppliers / 12 months or 365 days.

Direct Wages = Budgeted Production in Units * Direct Wages Cost

per unit * Lag in Payment of Wages / 12 months or 365 days.

Overheads = Budgeted Production in Units * Overhead Cost per

unit * Lag in Payment of Overheads / 12 months or 365 days.

Operating cycle… Operating cycle is the time that elapses to convert raw materials

into cash.

Operating cycle of Manufacturing firm.

Operating cycle of a Non manufacturing firm.

http://study.com/academy/lesson/operating-cycle-cash-cycle-

definition-calculations.html

77

CAB – Advanced Financial Management

Operating cycle…

78

Concepts of Working Capital

1. Gross Working Capital

• Total Current assets

• Where Current assets are the assets that can be converted into

cash within an accounting year & include cash , debtors etc.

• Referred as “Economics Concept” since assets are employed to

derive a rate of return.

2. Net Working Capital

• CA – CL

• Referred as „point of view of an Accountant‟.

• It indicates liquidity position of a firm & suggests the extent to which

working capital needs may be financed by permanent sources of

funds.

CAB – Advanced Financial Management 79

OPERATING CYCLE OF

MANUFACTURING FIRM

RAW

MATERIALS

FINISHED

GOODS

CASH

WORK-IN

PROGRESSDEBTORS

CAB – Advanced Financial Management 80

OPERATING CYCLE OF

TRADING FIRM

FINISHED

GOODS

DEBTORS

CASH

CAB – Advanced Financial Management 81

Sources of working capital

Sources of

Working

capital

Long term

sources

Short term

sources

Internal External

CAB – Advanced Financial Management 82

Determinants of working

capital

• General nature of business

• Production cycle

• Business cycle

• Credit policy

• Production policy

• Growth and expansion

• Profit level

• Operating efficiency

CAB – Advanced Financial Management 83

CAB – Advanced Financial Management

Current Asset Management

https://www.slideshare.net/Jacknickelson/chapter-7-current-asset-management

84

UNIT VII - SYLLABUS

• Capital Asset Pricing: Sharpe‟s CAPM

• Security Analysis and portfolio Selection

• Markowitz Portfolio theory

CAB – Advanced Financial Management 85

TM

KDF4B – Investment Analysis & Portfolio Theory 86

CAPM is a model that describes the relationship

between risk and expected (required) return; in

this model, a security‟s expected (required)

return is the risk-free rate plus a premium based

on the systematic risk of the security.

CAPITAL ASSET PRICING MODEL

TM

KDF4B – Investment Analysis & Portfolio Theory

https://www.youtube.com/watch?v=gzxKd2S2MdU

CAPITAL ASSET PRICING

MODEL

87

TM

KDF4B – Investment Analysis & Portfolio Theory 88

1. Capital markets are efficient.

2. Homogeneous investor expectations over a given period.

3.Risk-free asset return is certain (use short- to intermediate-

term Treasuries as a proxy).

4.Market portfolio contains only systematic risk (use S&P 500

Index or similar as a proxy).

CAPM ASSUMPTIONS

TM

KDF4B – Investment Analysis & Portfolio Theory 89

• An index of systematic risk.

• It measures the sensitivity of a stock‟s returns

to changes in returns on the market portfolio.

• The beta for a portfolio is simply a weighted

average of the individual stock betas in the

portfolio.

WHAT IS BETA?

TM

KDF4B – Investment Analysis & Portfolio Theory 90

https://www.youtube.com/watch?v=kq9T3yWuqR4

Security Analysis and

Portfolio Selection

TM

KDF4B – Investment Analysis & Portfolio Theory 91

MARKOWITZ APPROACH

TM

KDF4B – Investment Analysis & Portfolio Theory 92

MARKOWITZ APPROACH