C197 to the Planning - City of Greater Geelong · Amendment C197 to the Greater Geelong Planning...

24

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz 14 March 2011 Prepared for Costa 151 Pty Ltd

Transcript of C197 to the Planning - City of Greater Geelong · Amendment C197 to the Greater Geelong Planning...

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

14 March 2011

Prepared for Costa 151 Pty Ltd

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

Contents 1 Statement of Evidence ................................................................................................. 3

1.1 Introduction and Qualification ............................................................................................ 3

1.2 Information Sources ............................................................................................................ 3

1.3 Abbreviations ....................................................................................................................... 4

1.4 Amendment C197 Overview ............................................................................................... 4

1.5 Subject Site Background ...................................................................................................... 5

1.6 Socio‐Economic Profile ........................................................................................................ 6

2 Demand Assessment .................................................................................................... 8

2.1 Main Trade Area .................................................................................................................. 8

2.2 Competitive Retail Network .............................................................................................. 11

2.3 Retail Demand ................................................................................................................... 12

2.3.1 Specialty Capacity .............................................................................................................. 15

2.4 Specialty Retail Provision ................................................................................................... 16

3 Community Benefits .................................................................................................. 18

3.1 Competition Benefits ......................................................................................................... 18

3.2 Employment ...................................................................................................................... 18

4 Response to Submissions ........................................................................................... 19

4.1 Conclusion ......................................................................................................................... 19

Appendix A ‐ Curriculum Vitae ........................................................................................................... 21

Appendix B ‐ Key Centre Expansion Potential ..................................................................................... 22

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

List of Figures Figure 1. Amendment C197 subject land, Newcomb ......................................................................... 5

Figure 2. Car parking location map, subject site (2010) ..................................................................... 6

Figure 3. Bellarine‐Inner SLA Map ...................................................................................................... 7

Figure 4. Tasman Meats sources of trade by value (2011) ................................................................ 9

Figure 5. Main trade area map ......................................................................................................... 10

Figure 6. Main Trade Area retail expenditure per capita (2010) ...................................................... 13

Figure 7. Retail expenditure snapshot, main trade area (2011‐2021) ............................................. 14

Figure 8. Demand for supermarket, specialty and core retail floorspace (2011, 2016, 2021) ........ 15

Figure 9. Specialty retail floorspace market gap, Newcomb trade area (2010‐2021) ..................... 16

Figure 10. Under provision of specialty floorspace, main trade area (2010) ..................................... 17

Figure 11. Employment potential ....................................................................................................... 18

Figure 12. Provision of specialty floorspace, main trade area (2010) ................................................ 20

List of Tables Table 1. Key Socio‐Economic Statistics, Bellarine Inner SLA (2006 ‐2010) ....................................... 7

Table 2. Retail floorspace of surrounding shopping centres (2010) ............................................... 11

Table 3. Main trade area population forecast, subject site (2010‐2021) ....................................... 12

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

3

1 Statement of Evidence 1.1 Introduction and Qualification

1 I, Justin Malkiewicz, am the Manager of Economics and Research (Retail) at MacroPlan Australia Pty Ltd, Economists and Planners. I practice from level 4, 356 Collins Street, Melbourne Victoria.

2 I hold the qualifications of Bachelor of Business (Economics & Finance). I am currently undertaking a Masters of Urban Planning degree at the University of Melbourne.

3 I have practiced as an Economist for more than 7 years, working with local, State and Commonwealth Governments as well as with the private sector.

4 My area of expertise covers retail economics including activity centres, planning and policy, economic forecasting, population forecasting and strategic activity centre direction.

5 I have been retained as an economic expert to provide a Statement of Evidence on this matter by the owners of the property at 151 Bellarine Highway in Newcomb, which is occupied by Tasman Meats (Unit 1), Conga Foods (Unit 2) and a vacant site (Unit 3 owned by Costa 151 Pty Ltd).

6 I have inspected the site and surrounding area included into the amendment to Mixed Use zoning. I have also conducted visits of the local retail hierarchy to assist with my understanding of potential impacts.

7 I have made all the enquiries that I believe are desirable and appropriate and no matters of significance which I regard as relevant have to my knowledge been withheld from the Panel.

1.2 Information Sources This report draws on a wide range of information sources including, but not limited to:

• Australian Bureau of Statistics

o Census of Population and Households (2006)

o Regional Population Cat # 3218.0 (2009)

o Retail Trade Cat #6501.0 (July 2009)

• MarketInfo (July 2009)

• Victoria in Future population estimates (2007)

• The Greater Geelong Planning Scheme (2010)

• Amendment C197 to the Greater Geelong Planning Scheme (2010)

• Geelong Eastern Boundary Review (January 2009)

• Retail Strategy, City of Greater Geelong (June 2006)

• Correspondence between local landholders and City of Greater Geelong (2010‐2011)

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

4

1.3 Abbreviations The following abbreviations are used in this report.

ABS Australian Bureau of Statistics

B4Z Business 4 Zone

CCD Census Collection District

EIA Economic Impact Assessment

GLAR Gross Leasable Area (Retail)

LDRZ Low Density Residential Zone

m2 Square metre

MTA Main Trade Area

MUZ Mixed Use Zone

PTA Primary Trade Area

SLA Statistical Local Area

STA Secondary Trade Area

1.4 Amendment C197 Overview 8 Amendment C197 to the Greater Geelong Planning Scheme seeks to rezone approximately

5.3 hectares of land to the Mixed Use Zone (MUZ).

9 According to the City of Greater Geelong's Explanatory Report, the proposed rezoning will provide for the economic revitalisation of the area, and will allow for an increased mix of uses on the site providing a greater range of commercial tenancies in the area.

10 Specifically, Amendment C197 proposes the following:

a The rezoning of all the land in the existing B4Z north of the Bellarine Highway, Moolap between Coppards Road and Twitt Street to the MUZ.

b The rezoning of the rear portion of 191‐209 Bellarine Highway, Moolap from Low Density Residential (LDRZ) to the MUZ.

11 I note that there is currently no schedule to the MUZ proposed that will limit the amount of "shop" floorspace allowed on the subject land. However, the majority of commercial/retail uses allowable under the MUZ are subject to the issue of a planning permit.

12 Figure 1 indicates the land to be rezoned to MUZ. The existing B4Z land to the south of the Bellarine Highway will remain as currently zoned.

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

5

Figure 1. Amendment C197 subject land, Newcomb

Source: MapInfo (2010), MacroPlan Australia (2010)

1.5 Subject Site Background 13 Existing uses at 151 Bellarine Highway include Tasman Market Fresh Meats, Conga Foods

UCG Wholesale and one vacant tenancy (Unit 3 owned by Costa 151 Pty Ltd) The vacant tenancy at Unit 3 comprises a floorspace of approximately 1,400m2.

14 There are also a number of smaller tenants (within the proposed amendment area) including Video Easy, Subway and Pizza Hut (all located at 181‐183 Bellarine Highway). Surrounding tenants within the amendment area include Thriftway Furniture and Bedding, Mobil Service Station, Peninsula Receptions (food and accommodation), and Bellarine Veterinary Practice.

15 151 Bellarine Highway includes 94 car parks located to the front of the three tenancies and 16 employee parking spaces to the rear of the building. Additional parking is also available within 181‐183 Bellarine Highway. The car parks are accessible from Bellarine Highway and Coppards Road and are generally shared between the existing tenancies and convenience restaurants. Number 151 Bellarine Highway is outlined within the red boundary in the figure below.

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

6

Figure 2. Car parking location map, subject site (2010)

Source: O'Brien Traffic Rezoning Report (2010)

16 The site is surrounded by predominantly residential land to the north (LDRZ) and business (B4Z) land to the south.

1.6 Socio‐Economic Profile 17 The following table provides a number of economic indicators which point to the welfare

of residents surrounding the subject site. Key points to note are:

a Household income is 22% lower than the Victorian average, reflecting a generally lower socio‐economic profile of residents in the Bellarine ‐ Inner SLA (refer figure overleaf). Hence, flexibility to provide a discount food and grocery offer could be considered attractive for residents within the SLA.

b A generally higher level of unemployment, with a higher number of blue collar jobs.

18 These indicators provide a basis that further allowance for a discount offer in the area could be considered beneficial for residents.

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

7

Figure 3. Bellarine‐Inner SLA Map

Source: MapInfo (2010), MacroPlan Australia (2011)

Table 1. Key Socio‐Economic Statistics, Bellarine Inner SLA (2006 ‐2010)

Source: ABS Census (2006), MacroPlan Australia (2006)

Bellarine Inner SLA Regional Victoria VictoriaPopulation and Households (2009)Persons 25,169 1,447,691 5,443,228Households 8,642 498,387 1,781,666Age Distribution (2009)0‐24 years 33% 33% 33%25‐64 years 52% 51% 54%65+ years 16% 16% 14%Income and Wealth (2008)Average Individual Income $36,879 $35,712 $42,727Variation from Victoria ‐13.7% ‐16.4%Average Household Income $58,517 $57,931 $75,031Variation from Victoria ‐22.0% ‐22.8%Employment Labour Force (2010) 13,077 750,400 2,953,600Unemployment Rate (2010) 6.1% 6.0% 5.4%Businesses (2007) 1,335 139,995 502,668Occupation by Sector (2008)White Collar 31% 35% 42%Blue Collar 39% 36% 29%Service Sector 30% 28% 29%

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

8

2 Demand Assessment 19 To understand the demand for food and convenience retailing, I have analysed the area for

which I understand the centre draws the majority of its trade. This analysis includes the profile of consumers within this trade area (including their spending habits), and the current provision of retail and shop floorspace in and around the Main Trade Area (MTA).

20 The MTA is the area where a centre is likely to gain the majority of its trade and it made up by a core 'Primary Trade Area' (PTA) and an area where lower, but still relatively significant amount of market share are attained, known as the 'Secondary Trade Area' (STA).

21 In forming the MTA, I have also used primary quantitative data obtained by an in‐centre survey of customers to understand the residential location of customers and the average amount spent.

2.1 Main Trade Area 22 My MTA has been influenced by a number of key factors including:

a Competitive framework of existing supply;

b Road networks and traffic flows;

c Natural and man‐made physical boundaries such as rivers, rail, freeways etc;

d Ease of parking;

e Food and convenience role the centre may play for surrounding residents;

f Other competing centres anchored by a supermarket (noting that no supermarket is contemplated within the amendment area);

g The location on Bellarine Highway, directly in between the Geelong CBD and Bellarine Peninsula with easy regional access; and,

h Population distribution and proximity to the proposed premises.

Customer Survey Data

Survey #1

23 The survey information received from 664 customers to the Tasman Meats store (located on the subject site) to provide information as to the MTA of the site.

24 The survey was conducted over a three day period from 6th July to 9th July 2010 ‐ yielding 664 results on residential postcodes of customers. The results indicated that patronage from a wide area is attracted to the centre with many patrons coming from beyond the trade area (BTA) originally defined by MacroPlan.

25 The survey revealed where customers to the subject site currently reside:

a 35% from Newcomb;

b 35% from the Bellarine Peninsula including suburbs like St Leonards, Portarlington, Indented Head and Ocean Grove;

c 11% from Leopold suburb; and,

d 7% from Moolap and Whittington suburbs.

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

9

26 The survey results highlight that up to 35% of trade is being sourced from surrounding towns outside the MTA, such as Portarlington. Other sources of trade include North Geelong and to a less extent western Geelong suburbs.

Survey #2

27 The second survey was conducted in January 2011 and included 2,496 transactions which have been assessed by dollar value in each postcode to Tasman Meats.

28 This survey provides a strong assessment as to the trade areas as it is indicative of where the store receives the majority of its trade.

Figure 4. Tasman Meats sources of trade by value (2011)

Source: MapInfo (2010), MacroPlan Australia (2011)

Some key findings include:

• 57% of transactions (by value) were sourced from Newcomb

• 21% from the Bellarine Peninsula including suburbs such as St Leonards, Portarlington and Ocean Grove

This data has been used to assist in forming the trade area below.

Trade Area Delineation

29 Subject to the findings of the survey of trade sources and in consideration of existing competition, I have defined a trade area for existing and potential retailers at the subject site. Key features of the trade area are as follows:

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

10

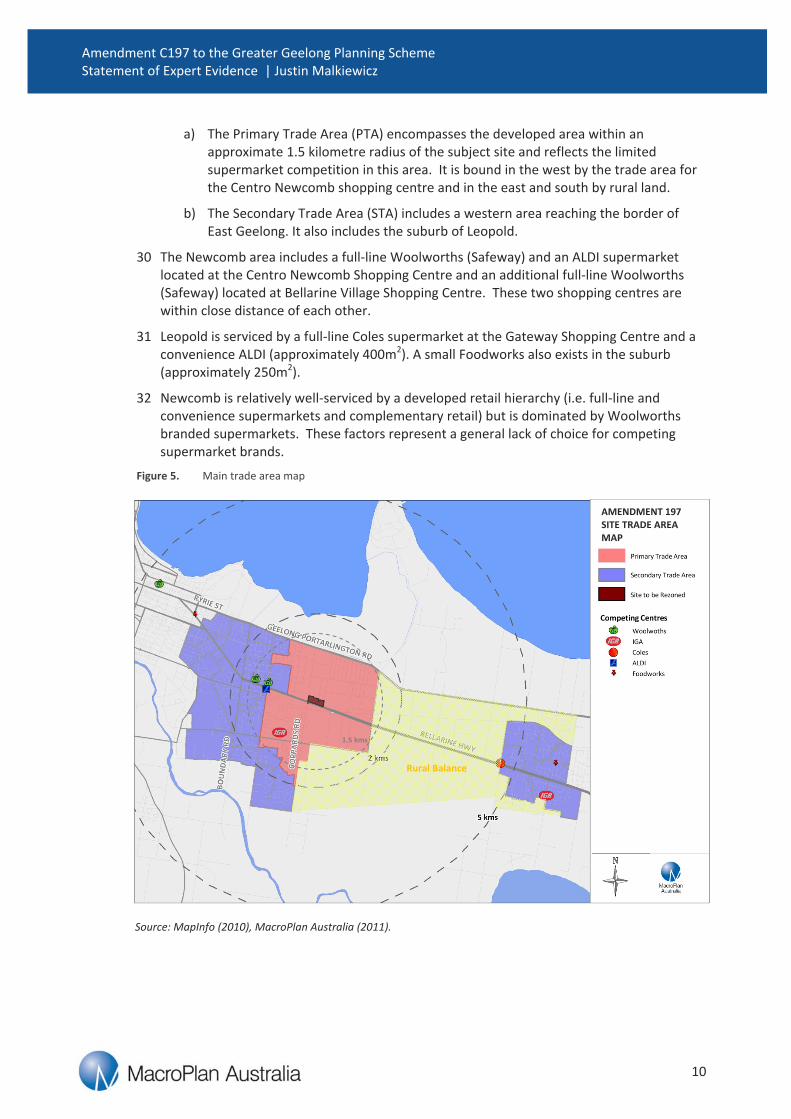

a) The Primary Trade Area (PTA) encompasses the developed area within an approximate 1.5 kilometre radius of the subject site and reflects the limited supermarket competition in this area. It is bound in the west by the trade area for the Centro Newcomb shopping centre and in the east and south by rural land.

b) The Secondary Trade Area (STA) includes a western area reaching the border of East Geelong. It also includes the suburb of Leopold.

30 The Newcomb area includes a full‐line Woolworths (Safeway) and an ALDI supermarket located at the Centro Newcomb Shopping Centre and an additional full‐line Woolworths (Safeway) located at Bellarine Village Shopping Centre. These two shopping centres are within close distance of each other.

31 Leopold is serviced by a full‐line Coles supermarket at the Gateway Shopping Centre and a convenience ALDI (approximately 400m2). A small Foodworks also exists in the suburb (approximately 250m2).

32 Newcomb is relatively well‐serviced by a developed retail hierarchy (i.e. full‐line and convenience supermarkets and complementary retail) but is dominated by Woolworths branded supermarkets. These factors represent a general lack of choice for competing supermarket brands.

Figure 5. Main trade area map

Source: MapInfo (2010), MacroPlan Australia (2011).

Rural Balance

1.5 kms

AMENDMENT 197 SITE TRADE AREA MAP

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

11

2.2 Competitive Retail Network 33 I have reviewed the competitive retail network in the MTA and consider it predominately

comprised of neighbourhood shopping centres which cater for basic day‐to‐day retail and weekly shopping needs.

Table 2. Retail floorspace of surrounding shopping centres (2010)

Source: MacroPlan Australia (2011) *MacroPlan estimate

Bellarine Village

34 Comprised of 6,170m2 GLAR with one full‐line supermarket and 17 specialty shops spread over one level, Bellarine Village is classified as a neighbourhood centre. Regarding the food components, the speciality shops include a Baker’s Delight and a Butcher. These food specialities add up to 110m2 and the Woolworth provides 3,877m2 of floorspace.

Centro Newcomb

35 Centro Newcomb includes 8,216m2 of retail floor space and is a neighbourhood centre anchored by two supermarkets. A total of 22 specialty stores currently operate and include a Baker’s Delight, Leonard’s Poultry and Tender Cut Meat as food tenants. The total food retail floorspace in the centre is 5,418m2.

Gateway Plaza Leopold

36 Gateway Plaza is comprised of approximately 5,430m2, according to MacroPlan estimates, and is anchored by a full‐line Coles. In total an estimated 3,130m2 of food retail are offered in this centre.

37 These centres are comprised of retail tenancies that serve the day to day convenience needs of their immediate surrounding population. Similar to the subject site, these centres have the potential to capture passing trade from residents across the wider Bellarine Peninsula.

Bellarine Village 1.7 Woolworths 3,877 110 3,987Woolworths

ALDIGateway Shopping Centre 4.6 Coles 3,000* 130* 3,130

Other Local CentresIGA Whittington 1.2 IGA 525 - 525IGA Leopold 5.1 IGA 500 - 500Foodworks Leopold 6.3 Foodworks 500 - 500Other Food Speci l i t ies

Wattlepark Av Bakery 0.5 - - - 90Ramsay's Bakery 0.5 - - - 100Newcomb Village Food Sp. 0.1 - - - 150Watsons Rd Fruit and Veg. 1.5 - - - 70St Albans Park Gral Store 4.6 - - - 60Leopold Bakery 5.1 - - - 100Leopold Butcher 5.2 - - - 100Total Food Supply 14,730

CentreDistance from the Site (km)

Anchor(s)Food

Special i ty (sqm)

Total Food and Grocery

(sqm)

Centro Newcomb 1.2 5,238180 5,418

Supermarket (sqm)

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

12

2.3 Retail Demand 38 I have assessed the retail and 'shop' floorspace demand at the subject site. This analysis

has involved the following:

a Analysing current population levels within the MTA and projected into the future;

b the average expenditure per capita for MTA residents; and,

c the amount of floorspace expected to be demanded at the subject site given the market share that site would be expected to capture from the expenditure pool.

Population Assessment

39 The total population in the MTA has been based on historical population statistics utilising data from the 2006 ABS Census and projected forward using Department of Health and Ageing forecasts. These population forecasts have been prepared at a small area level (Census Collection District (CCD)).

40 The current MTA population is estimated at 27,300 people, including 6,390 people within the PTA. The growth in population of the MTA is similar to the Victorian state average, with the MTA growing by around 2,400 people in the 10 years to 2021. This additional residential population will increase demand for retail floorspace.

Table 3. Main trade area population forecast, subject site (2010‐2021)

Source: ABS 2006 Census (2006), Department of Health and Ageing (2007)

Retail Expenditure Pool

41 I have used the population projections detailed above and data on the per capita retail expenditure to estimate the level of retail expenditure for the MTA below.

42 The level of retail expenditure per person for the MTA population is currently estimated at $11,500 which is generally in line with regional Victorian averages.

43 The figure below shows the per capita expenditure levels within the MTA by retail category, including food and groceries, total food retail and non food retail.

Trade Area 2010 2011 2016 2021

PTA 6,340 6,394 6,677 6,952

STA 20,734 20,911 21,837 22,736

MTA 27,074 27,305 28,514 29,688

PTA 0.9% 0.9% 0.8% 0.8%

STA 0.9% 0.9% 0.8% 0.8%

MTA 0.9% 0.9% 0.8% 0.8%

Average Annual Change (%)

Estimated Population

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

13

Figure 6. Main Trade Area retail expenditure per capita (2010)

Source: MacroPlan Australia (2010)

44 The tables below summarise the retail spending capacity of residents within the defined MTA over the forecast period to 2021. Spending forecasts presented in this report are expressed in constant 2009/10 dollar terms excluding inflation.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Food and Grocery Total Food (incl. catering, bottle shop)

Non Food Total Retail

Retail expe

nditure pe

r capita

PTA STA Regional Victoria

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

14

Figure 7. Retail expenditure snapshot, main trade area (2011‐2021)

Retail Expenditure Snapshot

The surrounding tables provide an insight into the retail expenditure pool of the C197 main trade area.

MacroPlan estimate:

Total Food and Grocery expenditure to be over $130 million for the main trade area in 2011, and is forecast to grow to nearly $28 million by 2021.

Non‐Food retail spending is currently around $119 million, excluding bulky goods.

Source: MarketInfo (2009), MacroPlan Australia (2011)

Primary Sector

Secondary Sector

Main Trade Area

2011 $30.4 $100.4 $130.72012 $31.0 $102.3 $133.32013 $31.6 $104.4 $135.92014 $32.2 $106.4 $138.62015 $32.8 $108.5 $141.42016 $33.5 $110.7 $144.22017 $34.1 $112.8 $147.02018 $34.8 $115.0 $149.82019 $35.5 $117.2 $152.72020 $36.1 $119.5 $155.62021 $36.8 $121.7 $158.6

2011-16 $3.1 $10.3 $13.52011-21 $6.5 $21.4 $27.8

Retai l Expendi ture ($m) - Food and Grocery

Expendi ture Growth ($m) - Food and Grocery

Primary Sector

Secondary Sector

Main Trade Area

2011 $27.1 $91.8 $118.92012 $27.7 $93.6 $121.22013 $28.2 $95.4 $123.62014 $28.8 $97.3 $126.12015 $29.3 $99.2 $128.62016 $29.9 $101.2 $131.12017 $30.5 $103.2 $133.62018 $31.1 $105.1 $136.22019 $31.7 $107.2 $138.82020 $32.3 $109.2 $141.52021 $32.9 $111.3 $144.2

2011-16 $2.8 $9.5 $12.22011-21 $5.8 $19.5 $25.3

Retai l Expend i ture ($m) - Non Food Retai l

Expendi ture Growth ($m) - Non-Food Retai l

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

15

2.3.1 Specialty Capacity 45 The methodology I adopted for assessing specialty floorspace capacity takes account the

food and grocery (F&G) and non‐food retail specialty floorspace to estimate the amount of floorspace that should be supported by this market over time, assuming a sustainable average trading level for all retailers.

46 The Table below provides an analysis of demand for specialty floorspace in the trade area based on a number of steps as follows:

• Expenditure available within the MTA for Food and Grocery and Non‐Food retailing, showing the total level of convenience retail spending (excluding bulky goods) generated by MTA residents.

• Share of spending to Specialty retail. Not all expenditure is directed to specialty retailers, a proportion is directed to major anchor stores such as supermarkets. In the case of the defined MTA I have assumed a rate of 30% across food and grocery retail, and 40% for other forms of retail. This is then presented in spending ($) terms.

• Estimate the Level of Supportable Floorspace. Using an assumed supportable average trading level, the estimated level of floorspace that can be sustained within the MTA is calculated to reflect a floorspace provision.

47 The outcome of the analysis is that the MTA has a strong capacity to support specialty retail and over time expansions in retail specialty floorspace will be required.

Figure 8. Demand for supermarket, specialty and core retail floorspace (2011, 2016, 2021)

Source: MacroPlan Australia (2011)

48 Demand for specialty floorspace within the MTA is currently around 14,300m2 while the level of supply within the MTA is estimated at 10,800m2.

49 The total demand for these centres does not account for people who reside outside the MTA who are spending at the centre. It is estimated that due to many of these centres being on the Bellarine Highway heading to the tourism and employment areas of Greater Geelong, the market gap is even greater than that outlined above.

Expenditure ($m) 2011 2016 2021

Food and Grocery Retail $130.7 $144.2 $158.6Non‐Food Retail $119 $131 $144% directed to specialty retail

Food and Grocery Retail 30% 30% 30%Non‐Food Retail 45% 45% 45%Specialty Retail PoolFood and Grocery Retail $39.2 $43.3 $47.6

Non‐Food Retail $53.5 $59.0 $64.9Retail Turnover DensityFood and Grocery Retail $8,500 $8,715 $8,935Non‐Food Retail $5,500 $5,639 $5,781Floorspace RequirementFood and Grocery Retail 4,614 4,964 5,324Non‐Food Retail 9,726 10,463 11,223Total Specialty Requirement 14,339 15,427 16,547

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

16

Figure 9. Specialty retail floorspace market gap, Newcomb trade area (2010‐2021)

Source: MarketInfo (2009), Property Council of Australia (2010), MacroPlan Australia (2011)

2.4 Specialty Retail Provision 50 The delivery of specialty floorspace in and around activity centres is important for a

number of reasons including:

a delivery of a wider range of product mixes for convenience needs of the local community;

b allowance for an additional niche/discount offers for the local community;

c increased range of jobs for residents for the local community.

51 Generally, neighbourhood and supermarket anchored centres would provide an average of around 50% of floorspace allocated to specialty and other small tenancy uses. The remaining 50% would be accommodated within major anchor floorspace such as a supermarket.

52 I have undertaken a detailed review of key competing centres to the proposed uses and consider there to be a severe lack of specialty floorspace for the local community delivered through the surrounding supermarket based centres.

53 The chart below indicates the level of specialty floorspace in centres within the MTA as a portion of the whole centre.

0

5,000

10,000

15,000

20,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Demand Supply with potential additional Current supply

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

17

Figure 10. Under provision of specialty floorspace, main trade area (2010)

Source: Property Council of Australia (2010), MacroPlan Australia (2010)

54 Based on my review, the surrounding retail centres are highly weighted towards the key anchor and supermarket tenants and are not providing a full or comprehensive range of specialty retailers.

55 This severe lack of specialty retail offer is more prominent in the following centres

o Bellarine Shopping Centre, 27% specialty provision.

o Centro Newcomb, 26% specialty provision, and

o Leopold Gateway Plaza, 23% specialty provision.

56 It must be noted that the only centres within the MTA which are above national average are very small centres with a limited supermarket offer.

57 The consequences of an under‐supply of retail specialty floorspace results in residents being required to travel to centres outside the MTA to undertake convenience shopping needs such as the Geelong CBD.

58 The proposed development would only fulfil a small proportion of the current gap in local and specialty retailing, with a requirement for other larger centres to expand their retail offer to serve the community appropriately.

0%10%20%30%40%50%60%70%

Surrounding centres Surrounding centres average National Average

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

18

3 Community Benefits 59 The proposed rezoning is likely to generate a number of wider economic and social

benefits to the community. These benefits are detailed in the following section and include:

• Competition; and,

• Employment.

3.1 Competition Benefits 60 The potential uses at the subject site (such as those currently trading) have significant

competitive benefits to the resident population. While competition that threatens the viability of the surrounding retail network is a cause for concern, by and large competition brings significant positive outcomes to the local community.

61 Without a supermarket anchor, the proposed rezoning would have limited opportunity to compete strongly with, or challenge the viability of centres supported by supermarkets, however, there is one vacant tenancy of approximately 1,400m2.

3.2 Employment 62 The employment benefits will include the potential for a more diverse range of

employment forms and an increased number of jobs relative to uses that could are allowed under the current planning zone.

63 The table below presents an estimate of the difference in employment that will be created by allowing a mixed use zone in comparison to the current B4Z.

64 I have estimated the differences in employment numbers based on employment density ratios per square metre of floorspace. On average, specialty and retail floorspace employs one employee per 25m2. Larger retail formats such as bulky goods showrooms average around one employee per 50m2.

65 If the 3,500m2 earmarked as 'shop' floorspace was occupied by food and grocery and specialty uses (as currently provided), then there would be an estimated 140 jobs for that land area.

Figure 11. Employment potential

Source: MacroPlan Australia (2011)

66 If the subject site was able to secure a tenant permissible under existing zonings, I estimated there would be only 70 jobs for the land area based on the averages. Hence, the proposed development sustains a significantly higher level of employment generation for the local community than other potential uses.

Employment differential BZ4 MUZ

A) Examination area (m2) 3,500 3,500

B) Employment density (m2/empl) 50 25C) Job estimation for examination area (A÷B)

70 140

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

19

4 Response to Submissions 67 I am aware that some points raised by objectors to Amendment C197 have been

responded to by the City of Greater Geelong through reports raised in the council meeting of 23 November 2010. As part of this I would like to further provide economic considerations to some of the specific details of the City of Greater Geelong's policies and procedures.

68 The Geelong Retail Strategy raises some relevant policies with regards to activity centre planning and zoning. A few of these include:

a Section 4.2 (2) states there should be facilitation of "additional retail facilities where they meet the needs of residents and visitors" and that local government should "ensure that activity centres evolve to meet the changing needs and preferences of the community"

b Section 4.2 (8) recommends to "closely monitor out‐of‐centre development, and allow such development at appropriate locations"

c "The Strategy includes measures which guide the development of out‐of‐centre activities, while ensuring that the integrity of the retail activity centre hierarchy and the goals relating to activity centre policy are not compromised... Council will encourage an appropriate balance between the interests of shoppers and retailers, and the need to achieve orderly and sustainable planning outcomes" ‐ Pg 18 Greater Geelong Retail Strategy (2006)

69 If it is determined that this is an out‐of‐centre location, the above statements point to support where necessary for out‐of‐centre development of new retail floorspace. However, I must reaffirm that the rezoning to MUZ will not be creating additional retail floorspace, but the potential for flexibility within the current floorspace.

70 Furthermore, from my study of the area, it appears that there is an undersupply of MUZ land when compared to the large amounts of B4Z land, including the large B4Z precinct at Waurn Ponds which is located less than 9km from the subject site.

Adverse impacts on designated Activity Centres

71 Arguments were raised as to the economic impacts on tenancies in designated activity centres, in particular if there was to be unrestricted retail floorspace allowance at the rezoned site.

72 I consider that without a major anchor such as a supermarket, the amount of retail floorspace sustainable at the site is limited and in line with a 3,500m2 'cap' on 'shop' floorspace. A centre without a major retail anchor is unlikely to have direct economic impacts on existing centres and is likely to result in a stronger retail outcome for residents.

73 I consider that the proposed uses (including the existing uses on site) allow for an exciting and unique retail offer.

4.1 Conclusion 74 It remains my view that there is now, and into the foreseeable future, the need for

additional convenience specialty retail within the defined MTA, which is currently not being provided for within existing supermarket anchored centres.

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

20

75 In my view there is sufficient for the proposed rezoning and no economic obstacle to it.

76 In my view there is good economic reason to justify an allowance for some shop floorspace at the proposed site:

a I consider the current trading performance of centres within the MTA to be strong. However, the centres within the MTA are generally dominated by supermarkets and there is an under‐provision of specialty floorspace.

b It is important to provide consumers with a range of products, prices and competing retail forms. This is important in light of limited convenience retail offered within surrounding centres such as Bellarine Village and Centro Newcomb. The proposed uses introduce a new and exciting retail offer to residents of the area.

c I have found there to be a severe lack of specialty ('shop') floorspace for the local community delivered through the surrounding supermarket based centres. This lack of shop floorspace is leading to residents travelling to areas beyond the MTA for these retail offers.

Figure 12. Provision of specialty floorspace, main trade area (2010)

Source: Property Council of Australia (2010), MacroPlan Australia (2010)

d I consider there to be a large lack of specialty "shop" floorspace within the MTA (refer Appendix B for further consideration).

0%10%20%30%40%50%60%70%

Surrounding centres Surrounding centres average National Average

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

21

Appendix A ‐ Curriculum Vitae

Amendment C197 to the Greater Geelong Planning Scheme Statement of Expert Evidence | Justin Malkiewicz

22

Appendix B ‐ Key Centre Expansion Potential

Bellarine Village

Constrained from expansion by residential to the north and west, Bellarine Hwy to the south, and with limited expansion possibility into car parking

areas.

Centro Newcomb

Constrained by residential and Bellarine Hwy to the south. There are limited expansion possibilities

into car parking areas.

Leopold Plaza

Potential for significant expansion based on growth in the Leopold market.

Wider Geelong Hierarchy

From the Greater Geelong Retail Strategy. The 3 centres surrounding the site are currently

neighbourhood centre which are servicing areas to the east of Geelong.

Source: Google Maps (2010), Greater Geelong Retail Strategy (2006)

MacroPlan Australia National Offices Sydney

Suite 1.02, Level 1 34 Hunter Street Sydney NSW 2000

t 02 9221 5211 f 02 9221 1284

Melbourne

Level 4, 356 Collins Street, Melbourne VIC 3000

t 03 9600 0500 f 03 9600 1477

Brisbane

Suite 6, Level 2 320 Adelaide Street Brisbane QLD 4000

t 07 3010 9249 f 07 3010 9640

Perth

Ground Floor 12 St Georges Terrace Perth WA 6000

t 08 9225 7200 f 08 9225 7299

www.macroplan.com.au