C O V E R S H E E T - petron.com · securities and exchange commission sec form 17-q quarterly...

39

3 1 1 7 1 P E T R O N C O R P O R A T I O N S M C H E A D O F F I C E 4 0 S A N M I G U E L A V E. M A N D A L U Y O N G C I T Y 1 2- 1 0 0 7 1 2 Dept. Requiring this Doc. Total No. of Stockholders Remarks = pls. use black ink for scanning purposes C O V E R S H E E T S. E. C. Registration Number (Company's Full Name) Fiscal Year Month ( Business Adress: No. Street City / Town / Province ) ATTY. JOEL ANGELO C. CRUZ 886-3888 Contact Person Company Telephone Number SEC Form 17-Q (2nd Quarter) FORM TYPE Month Day N/A Secondary License Type, if Applicable N/A Day Annual Meeting Domestic Foreign To be accomplished by SEC Personnel concerned Amended Articles Number/Section N/A Total Amount of Borrowings S T A M P S Fiscal Numer LCU Document I. D. Cashier

Transcript of C O V E R S H E E T - petron.com · securities and exchange commission sec form 17-q quarterly...

3 1 1 7 1

P E T R O N C O R P O R A T I O N

S M C H E A D O F F I C E 4 0 S A N M I G U E L

A V E. M A N D A L U Y O N G C I T Y

1 2 - 1 0 0 7 1 2

Dept. Requiring this Doc.

Total No. of Stockholders

Remarks = pls. use black ink for scanning purposes

C O V E R S H E E T

S. E. C. Registration Number

(Company's Full Name)

Fiscal Year

Month

( Business Adress: No. Street City / Town / Province )

ATTY. JOEL ANGELO C. CRUZ 886-3888

Contact Person Company Telephone Number

SEC Form 17-Q (2nd Quarter)

FORM TYPEMonth Day

N/A

Secondary License Type, if Applicable

N/A

Day

Annual Meeting

Domestic Foreign

To be accomplished by SEC Personnel concerned

Amended Articles Number/Section

N/A

Total Amount of Borrowings

S T A M P S

Fiscal Numer LCU

Document I. D. Cashier

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THE SECURITIES

REGULATION CODE AND SRC RULE 17 (2)(b) THEREUNDER

1. For the quarterly period ended June 30, 2010.

2. SEC Identification Number 31171 3. BIR Tax Identification No. 000-168-801 4. Exact name of registrant as specified in its charter PETRON CORPORATION 5. Philippines 6. (SEC Use Only)

Province, Country or other jurisdiction

of incorporation or organization

Industry Classification Code:

7. SMC Head Office Complex, 40 San Miguel Avenue, Mandaluyong City, 1550 Address of principal office Postal Code 8. (0632) 886-3888 Registrant's telephone number, including area code 9. Petron MegaPlaza, 358 Sen. Gil J. Puyat Avenue, Makati City 1200 (Former name, former address, and former fiscal year, if changed since last report.) 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA

Title of Each Class Number of Shares of Common Stock

Outstanding and Amount of Debt Outstanding Common Stock 9,375,104,497 Shares Preferred Stock 100,000,000 Shares ............................................................................................................................. .. ...............................................................................................................................

11. Are any or all of these securities listed on the Philippine Stock Exchange. Yes [X ] No [ ] If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange Common and Preferred Stocks

12. Indicate by check mark whether the Registrant:

(a) has filed all reports required to be filed by Section 17 of the Code and SRC Rule 17 thereunder or Sections 11 of the RSA and RSA Rule 11 (a)-1 thereunder, and Sectons 26 and 141 of the Corporation Code of the Philippines, during the preceding 12 months (or for such shorter period the registrant was required to file such reports).

Yes [X ] No [ ]

(b) has been subject to such filing requirements for the past 90 days. Yes [ ] No [ X ]

TABLE OF CONTENTS

Page No.

PART I - FINANCIAL INFORMATION Item 1 Financial Statements

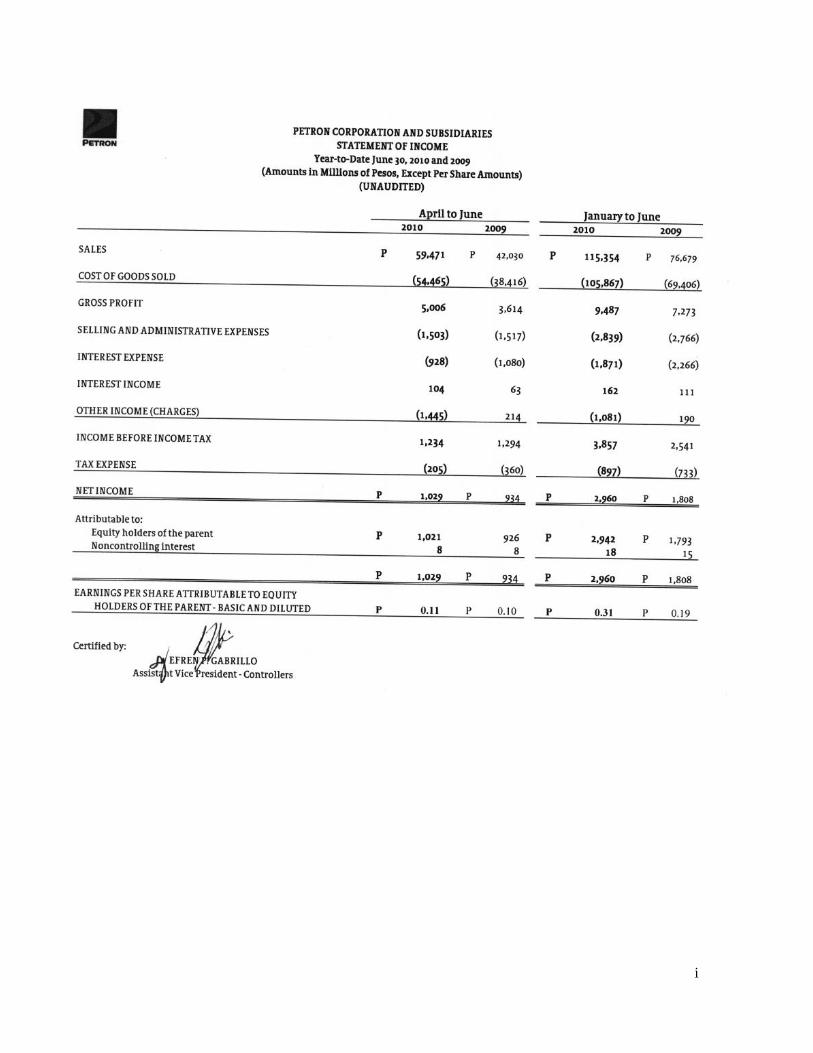

Petron Corporation & Subsidiaries Statements of Income

i

Petron Corporation & Subsidiaries Consolidated Statement of Cash Flows

ii

Petron Corporation & Subsidiaries Consolidated Statement of Comprehensive Income

iii

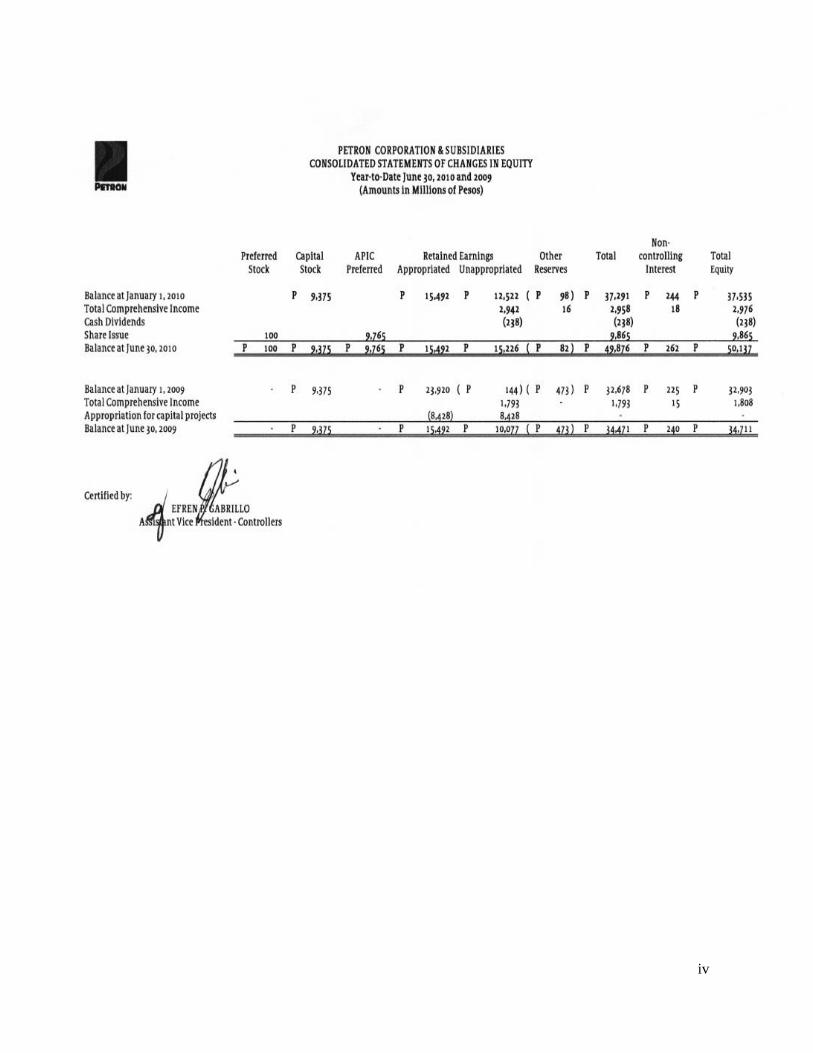

Petron Corporation & Subsidiaries Consolidated Statement of Changes in Equity

iv

Petron Corporation & Subsidiaries Consolidated Statement of Financial Position

v

Selected Notes to Consolidated Financial Statements

1-16

Details of Accounts Receivables 17

Item 2 Management’s Discussion and Analysis of Financial Conditions and Results of Operations

18-29

PART II - OTHER INFORMATION

SIGNATURES 30

i

ii

iii

iv

v

1

PETRON CORPORATION AND SUBSIDIARIES SELECTED NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS (Amounts in Million Pesos, Except Par Value, Share and Per Share Amounts, Exchange Rates, and Commodity Volumes) (Amounts Unaudited, Except Comparative Amounts for December 31, 2009 Statement of Financial Position)

1. Corporate Information

Petron Corporation (the Parent Company or Petron) was incorporated under the laws of the Republic of the Philippines and registered with the Philippine Securities and Exchange Commission (SEC) on December 15, 1966. Petron is the largest oil refining and marketing company in the Philippines, supplying nearly 40% of the country‟s fuel requirements. The Company‟s vision is to be the leading provider of total customer solutions in the energy sector and its derivative businesses. Petron operates a refinery in Limay, Bataan, with a rated capacity of 180,000 barrels a day. Petron‟s International Standards Organization (ISO) 14001 – certified refinery processes crude oil into a full range of petroleum products including liquefied petroleum gas (LPG), gasoline, diesel, jet fuel, kerosene, industrial fuel oil, solvents, asphalts, mixed xylene and propylene. From the refinery, Petron moves its products mainly by sea to Petron‟s 31 depots and terminals situated all over the country. Through this nationwide network, Petron supplies fuel oil, diesel, and LPG to various industrial customers. The power sector is Petron‟s largest customer. Petron also supplies jet fuel at key airports to international and domestic carriers. Through its 1,565 service stations, Petron remains the leader in all the major segments of the market. Petron retails gasoline, diesel, and kerosene to motorists and public transport operators. Petron also sells its LPG brands “Gasul” and “Fiesta” to households and other industrial consumers through an extensive dealership network. To broaden its market base and further strengthen its leadership in the LPG business, Petron launched a second LPG brand called “Fiesta Gas” early in 2008. Petron operates a lube oil blending plant at Pandacan Oil Terminal, where it manufactures lubes and greases. These are also sold through Petron‟s service stations and sales centers. In July 2008, Petron completed the construction of a Fuel Additives Blending facility at the Subic Bay Freeport. This plant, which has started commercial operations in October 2008, serves the needs of Innospec, a leading global fuel additive company, in the Asia-Pacific region. Petron is expanding its non-fuel businesses which include its convenience store brand “Treats.” Petron has partnered with major fast-food chains, coffee shops, and other consumer services to give its customers a one-stop full service experience. Petron is also putting up additional company-owned and company-operated (COCO) service stations in strategic locations. In addition, Micro-Filling Stations (MFS) were built across the country in 2009. In line with Petron‟s efforts to increase its presence in the regional market, it exports various petroleum and non-fuel products to Asia-Pacific countries such as South Korea, China, Indonesia, Taiwan, Singapore, Thailand and Cambodia.

2

Petron‟s shares of stock or securities are listed for trading at the Philippine Stock Exchange (PSE). Prior to the entry of Ashmore, the Philippine National Oil Company (PNOC) and the Aramco Overseas Company B.V. (AOC) each owned a 40% share of equity. The remaining 20% was then held by more than 180,000 stockholders. On March 13, 2008, AOC, entered into a share purchase agreement with Ashmore Investment Management Limited and subsequently issued a Transfer Notice to PNOC to signify its intent to sell its 40% equity stake in Petron. PNOC eventually waived its right of first offer to purchase AOC's interest in Petron. A total of 990,979,040 common shares were tendered representing 10.57% of the total outstanding common shares of Petron. Together with the private sale of AOC's 40% interest in Petron, the Ashmore Group, thru its corporate nominee SEA Refinery Holdings B.V. (SEA BV), a company incorporated in The Netherlands, acquired 50.57% of the outstanding common shares in Petron in the latter part of July 2008. SEA BV is a company owned by funds managed by the Ashmore Group.

On October 6, 2008, the PNOC informed SEA BV and Petron of its intent to dispose of its 40% stake in Petron. In December 2008, the 40% interest of PNOC in Petron was finally purchased by SEA Refinery Corporation (SRC), a domestic corporation wholly-owned by SEA BV. In a related development, SEA BV sold a portion of its interest in Petron, equivalent to 10.1% of the issued shares, to SRC. Thus, at the turn of the year, the capital structure of Petron is as follows: SRC – 50.1%; SEA BV – 40.47%; and the general public – 9.43%, making SEA BV‟s direct and indirect ownership interest in Petron at 90.57%; hence, SEA BV is the Company‟s parent company as of December 31, 2008 and 2009 . On December 24, 2008, San Miguel Corporation (SMC) and SEA BV entered into an Option Agreement granting SMC the option to buy the entire ownership interest of SEA BV in its local subsidiary, SRC. The option may be exercised by SMC within a period of two years from December 24, 2008. Under the Option Agreement, it was provided that SMC will have representation in the Petron Board and Management. In the implementation of the Option Agreement between SMC and SEA BV, SMC representatives were elected to the Petron Board and appointed as senior officers last January 8 and February 27, 2009. In the February 27, 2009 Board meeting, the Board approved the amendment of the Articles of Incorporation to include the generation and sale of electric power in its primary purpose. The objective is principally to lower the refinery power cost thru self-generation and, in the event there is excess power, to sell the same to third parties. The Board also approved an increase of the capital stock from the current P10 billion to P25 billion through the issuance of preferred shares aimed at raising funds for capital expenditures related to expansion programs as well as to possibly reduce some of the Company‟s debts. Both items , including a waiver to subscribe to the preferred shares to be issued as a result of the increase in capital stock, were approved by the stockholders last May 12, 2009 annual stockholders meeting. On October 21, 2009, the Board approved the amendment of Petron‟s Articles of Incorporation to reclassify a total of 624,895,503 unissued common shares to preferred shares with a par value of P= 1.00 per share, which also includes a waiver of the stockholders‟ pre-emptive rights on the issuance of preferred shares. Features of said shares were approved by the Executive Committee on November 25, 2009. In November 2009, the requirements for the registration statement of Petron‟s preferred shares, the Preliminary Prospectus, were submitted to the SEC. The application for listing of preferred shares was also subsequently filed with the PSE. By written assent, majority of the stockholders voted for the amendment of the reclassification of unissued common shares to preferred shares. In the meantime, on January 21, 2010, the SEC approved Petron‟s amendment to its Articles of Incorporation to include preferred shares in the composition of its authorized capital stock. On January 22, 2010, the SEC favorably considered the Final Prospectus and the Issue Management and Underwriting Agreement. The SEC subsequently issued an Order permitting the sale of securities

3

on February 12, 2010. Similarly, the PSE also approved the issuance of 100,000,000 preferred shares, which was offered to the public from February 15 to February 26, 2010. The shares were listed at the Philippine Stock Exchange on March 5, 2010. In connection with the inclusion of the generation and sale of electric power in the Company‟s Primary Purpose, the Company received from the Department of Energy the agency‟s endorsement dated January 15, 2010 of the corresponding amendment of Petron‟s Articles of Incorporation. The Company has submitted all the requirements to the SEC in February 2010 and is now awaiting approval. At the April 29, 2010 Meeting, the Board endorsed the amendment of the Company‟s Articles of Incorporation and the By-Laws increasing the number of directors from ten (10) to fifteen (15) and quorum from six (6) to eight (8). The same was approved by the stockholders during their annual meeting last July 12, 2010. The amendment has been filed with the SEC and is now awaiting approval. By end of April 2010, SMC informed Petron of its intention to exercise forty percent of SRC‟s outstanding capital stock, with the remaining sixty percent to be exercised by SMC up to December 23, 2010. SMC submitted its Tender Offer Report with the SEC, offering to acquire the common shares owned by the public. The tender offer period was opened from May 5 to June 2, 2010. The registered office address of Petron and its Philippine-based subsidiaries (except Petron Freeport Corporation which has its principal offices in the Subic Special Economic Zone) is SMC Head Office Complex, 40 San Miguel Avenue, Mandaluyong City. The registered office of SEA BV is located at Prins Bernhardplein 200, 1097 JB, Amsterdam, The Netherlands.

2. Basis of Preparation The condensed consolidated interim financial statements have been prepared in accordance with Philippine Accounting Standard (PAS) 34, Interim Financial Reporting. They do not include all the information required for full annual financial statements in accordance with Philippine Financial Reporting Standards (PFRS), and should be read in conjunction with the audited consolidated financial statements of Petron Corporation and subsidiaries (collectively referred to as “the Company”) for the year ended December 31, 2009.

Significant Accounting Policies The accompanying consolidated interim financial statements of the Company was prepared on the historical cost basis, except for financial assets at fair value through profit or loss (FVPL), available-for-sale (AFS) investments and derivative financial instruments, which are at fair value. The same accounting policies and methods of computation as mentioned in the audited financial statements for the year 2009, were followed in the preparation of the consolidated interim financial statements.

3. Significant Accounting Judgments, Estimates and Assumptions The preparation of the consolidated interim financial statements in accordance with PFRS requires the Company to make estimates and assumptions that affect the reported amounts of assets, liabilities, income and expenses and disclosure of contingent assets and contingent liabilities. Future events may occur which will cause the assumptions used in arriving at the estimates to change. The effects of any change in estimates are reflected in the consolidated interim financial statements as they become reasonably determinable.

4

Judgments and estimates are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

4. Issuances, repurchases, and repayments of debt and equity securities During the second quarter of 2010, the Company entered into a US$355 million Term Facility Agreement with Norddeutsche Landesbank Girozentrale, Singapore Branch as Lender. The full amount was drawn in June 2010

5. Segment Information

Management identifies segments based on business and geographical locations. These operating segments are monitored and strategic decisions are made on the basis of adjusted segment operating results.

Petron‟s major sources of revenues are as follows:

a. Sales from petroleum and other related products which include gasoline, diesel, kerosene, fuel oil, jet fuel and LPG offered to motorists and public transport operators through its service station network around the country as well as to industrial accounts, international and domestic carriers;

b. Insurance premiums from the business and operation of all kinds of insurance and reinsurance, on sea as well as on land, of properties, goods and merchandise, of transportation or conveyance, against fire, earthquake, marine perils, accidents and all other forms and lines of insurance authorized by law, except life insurance;

c. Lease of acquired real estate properties for petroleum, refining, storage and distribution facilities, gasoline service stations and other related structures;

d. Sales on wholesale or retail, and operation of service stations, retail outlets, restaurants, convenience stores and the like; and,

e. Exports sales of various petroleum and non-fuel products to Asia-Pacific countries such as Cambodia, South Korea, China, Australia and Indonesia.

The following tables present revenue and income information and certain asset and liability information regarding the business segments as of June 30, 2010 and December 31, 2009 and for the six-month periods ended June 30, 2010 and 2009. Segment assets and liabilities exclude deferred tax assets and deferred tax liabilities.

Petroleum Insurance Leasing Marketing Elimination Total

Period Ended June 30, 2010

Revenue

External Sales P=113,090 P= 2,264 - P=115,354

Inter-segment Sales 1,544 P=69 P=163 - (P=1,776) -

Segment results 6,374 56 78 85 55 6,648

Net income 2,750 91 29

84 5 2,960

5

As of June 30, 2010

Assets and liabilities

Segment assets 135,551 2,220 2,941 1,413

(3,124) 139,000

Segment liabilities 87,052 427 2,053 605

(2,440) 87,697

Other segment information Property, plant and

equipment

31,542 - 1 643 3,565 35,751 Depreciation and

amortization 1,613 - - 39

- 1,652

Period Ended June 30, 2009

Revenue

External Sales P=75,103 P=1,577 P=76,679

Inter-segment Sales 1,023 P=70 P=95 - (P=1,188) -

Segment results 4,190 57 76 47 136 4,507

Net income 1,654 81 25 46 3 1,808 As of December 31, 2009

Assets and liabilities

Segment assets 110,272 1,966 2,840 1,262 (3,154) 113,186

Segment liabilities 74,811 277 1,981 537 (2,462) 75,144

Other segment information Property, plant and equipment 31,351 - - 661 2,772 34,784 Depreciation and amortization 3,505 - - 81 - 3,586

The following tables present additional information on the petroleum business segment of the Company as of June 30, 2010 and December 31, 2009 and for the six-month periods ended June 30, 2010 and 2009:

Retail Lube Gasul Industrial Others Total

Property, plant and equipment

As of June 30, 2010 P=4,935 P=377 P=263 P=43 P=25,924 P=31,542

As of December 31, 2009 4,296 427 268 63 26,297 31,351

Capital Expenditures

As of June 30, 2010 P=756 P=5 P=82 P=1 P=2,306 P=3,150

As of December 31, 2009 575 5 74 11 785 1,450

Revenue

Period ended June 30, 2010 P=45,789 P=1,054 P=7,325 P=48,239 P=12,227 P=114,634

Period ended June 30, 2009 33,706 1,077 5,381 28,910 7,053 76,126

6

Geographical Segments

The following table presents revenue information regarding the geographical segments of the Company for the six-month periods ended June 30, 2010 and 2009.

Petroleum Insurance Leasing Marketing Elimination Total

Period ended June 30, 2010

Revenue

Local P=105,313 P=40 P=163 P=2,264 (P=1,776) P=106,005

Export/International 9,321 28 – – – 9,349

Period ended June 30, 2009

Revenue

Local P=71,835 P=33 P=95 P=1,577 (P=1,190) P=72,350

Export/International 4,292 37 – – – 4,329

6. Fuel Supply Contract The Company entered into various fuel supply contracts with NPC. Under the agreement, the Company supplies the bunker fuel oil requirements to NPC, its Independent Power Producers (IPP) and Small Power Utility Groups (SPUG) power plants/barges. For of the second quarter of 2010, the following are the fuel supply contracts granted to Petron:

Bid Date Date of Award

Contract Duration IFO (in KL)

IFO (in MP)

Jun 15, „10 Jun 23, „10 Jul. to Aug. „10 17,150 482,999

Jun 28, „10 Jul 5, „10 Jul. to Dec. „10 110,017 3,055780

7. Issuance of Preferred Shares/Amendment in Primary Purpose

On February 27, 2009, the Petron Board approved the amendment of the Company‟s Articles of Incorporation to include the generation and sale of electric power in its Primary Purpose. The objective is principally to lower the refinery power cost thru self-generation and, in the event there is excess power, to sell the same to third parties. The Board also approved an increase in the authorized capital stock of the Company from the current P=10,000 to P=25,000 through the issuance of preferred shares which is intended to raise funds for capital expenditures related to expansion programs, and possibly, to reduce some of the Company‟s debts. Both items were approved by the stockholders during its meeting on May 12, 2009. However, the approved increase in authorized capital stock to P=25,000 was not pursued and instead a reclassification from the unissued authorized common shares to preferred shares was put through. On October 21, 2009, the Board approved the amendment of Petron‟s Articles of Incorporation to reclassify a total of 624,895,503 unissued common shares to preferred shares with par value of P=1.00 per share, which also includes a waiver of the stockholders‟ pre-emptive rights on the issuance of preferred shares. The said amendment and waiver were approved by written assent of the stockholders on January 6, 2010. Features of the preferred shares were approved by the Executive Committee on November 25, 2009. In November 2009, the requirements for the registration statement of Petron‟s preferred shares, the Preliminary Prospectus, were submitted to the SEC. The application for listing of preferred

7

shares was also subsequently filed with the PSE. In the meantime, on January 21, 2010, the SEC approved Petron‟s amendment to its Articles of Incorporation to include preferred shares in the composition of its authorized capital stock. On January 22, 2010, the SEC favorably considered the Final Prospectus and the Issue Management and Underwriting Agreement. The SEC subsequently issued an Order permitting the sale of securities on February 12, 2010. Similarly, the PSE also approved the issuance of 100,000,000 preferred shares, which was offered to the public from February 15 to February 26, 2010. On March 5, 2010, Petron‟s preferred shares became officially traded at the PSE. In connection with the inclusion of the generation and sale of electric power in the Company‟s Primary Purpose, the Company received from the Department of Energy the agency‟s endorsement dated January 15, 2010 of the corresponding amendment of Petron‟s Articles of Incorporation. The Company has submitted all the requirements to the SEC in February 2010 and is now awaiting approval of the amendment.

8. Related Party Transactions Saudi Aramco is the ultimate parent of AOC, the Company‟s major stockholder until July 29, 2008 while PNOC was also a major stockholder until December 24, 2008. Thus, as of March, 2010, PNOC and Saudi Aramco are no longer considered as related parties of the Company (see Note 1).

Petron and Saudi Aramco have a term contract to purchase and supply, respectively, 90% of Petron‟s monthly crude oil requirements at Saudi Aramco‟s standard Far East selling prices. The contract is for a period of one year from October 28, 2008 to October 27, 2009 with automatic one-year extensions thereafter unless terminated at the option of either party, within 60 days written notice. Outstanding liabilities of Petron for such purchases are shown as part of “Liabilities for Crude Oil and Petroleum Product Importation” account in the consolidated interim statements of financial position. Petron has long-term lease agreements with PNOC until August 2018 covering certain lots where the Company‟s refinery and other facilities are located. Lease charges on refinery facilities escalate at 2% a year, subject to increase upon re-appraisal.

9. Earnings per share

Basic and diluted earnings per share amounts for the six-month period ending June 30, 2010 and June 30, 2009 are as follows:

Period ended Jun 30, 2010

Period ended Jun 30, 2009

Net income after tax attributable to equity holders of the parent

P= 2,960

P= 1,808

Weighted average number of shares 9,375,104,497 9,375,104,497

Basic and diluted earnings per share P= 0.31 P= 0.19

10. Dividends On June 7, 2010, the Company paid cash dividends of P=2.382 per share totaling P=238 to its preferred stockholders as of May 19, 2010. In addition, the company approved a P=0.10 per share cash dividends to its common shareholders on record as of July 30, 2010 to be given on August 16, 2010.

8

11. Seasonal Fluctuations

There were no seasonal aspects that had a material effect on the financial condition or results of operations of the Company

12. Commitments and Contingencies Unused Letters of Credit and Outstanding Standby Letters of Credit Petron has approximately unused documentary letters of credit amounting to P= 6 as of June 30, 2010 and P= 5 as of December 31, 2009. On the other hand, outstanding standby letters of credit for crude importations amounted to P= 9,261 and P= 10,685 as of June 30, 2010 and December 31, 2009, respectively. TCC-Related Matters

In 1998, the Company contested before the Court of Tax Appeals (CTA) the collection by the Bureau of Internal Revenue (BIR) of deficiency excise taxes arising from the Company‟s acceptance and use of Tax Credit Certificates (TCCs) worth P=659 million from 1993 to 1997. In July 1999, the CTA ruled that, as a fuel supplier of BOI-registered companies, the Company was a qualified transferee for the TCCs and that the collection by the BIR of the alleged deficiency excise taxes was contrary to law. The BIR appealed the ruling to the Court of Appeals where the case is still pending. In November 1999, BIR issued an assessment against the Company for deficiency excise taxes of P=284 million plus interest and charges for the years 1995 to 1997, as a result of the cancellation by the Department of Finance (DOF) Center ExCom of Tax Debit Memos (TDMs), the related TCCs and their assignments. The Company contested on the grounds that the assessment has no factual and legal bases and that the cancellation of the TDMs was void. The Company elevated this protest to the CTA on July 10, 2000. On August 23, 2006, the Second Division of the CTA rendered its Decision denying the Company‟s petition and ordered it to pay the BIR P=580 million representing deficiency excise taxes for 1995 to 1997 plus 20% interest per annum from December 4, 1999. The Company‟s motion for reconsideration was denied on November 23, 2006. The Company appealed the Division‟s Decision to the CTA En Banc. On October 30, 2007, the CTA En Banc dismissed the Company‟s appeal, with two of four justices dissenting. The Company filed its appeal on November 21, 2007 with the Supreme Court. On December 21, 2007, in the substantially identical case of Pilipinas Shell, the Supreme Court decided to nullify the assessment of the deficiency excise taxes and declared as valid Pilipinas Shell‟s use of Tax Credit Certificates for payment of its tax liabilities. On November 7, 2008, the Supreme Court gave due course to the Company‟s appeal. After the parties filed their respective memoranda, the case is now submitted for resolution.

In May 2002, the BIR issued a collection letter for deficiency taxes of P=254 million plus interest and charges for the years 1995 to 1998, as a result of the cancellation of TCCs and TDMs by the DOF Center ExCom. The Company protested this assessment on the same legal grounds used against the tax assessment issued by the BIR in 1999. The Company elevated the protest to the CTA. The 2nd Division of the CTA promulgated a decision on May 4, 2007 denying our Petition for Review for lack of merit. The Company was ordered to pay the respondent the reduced amount of P=601 million representing the Company‟s deficiency excise taxes for the taxable years 1995 to 1998. In addition, the Company was ordered to pay the BIR 25% late payment surcharge and 20% delinquency interest per annum computed from June 27, 2002. On appeal, the CTA En Banc on December 3, 2008,

9

promulgated a decision reversing the unfavorable decision of the CTA 2nd Division. The CIR filed a Petition for Review with the Supreme Court. Petron‟s Comment was filed on April 20, 2009.

It should be noted that there are duplications in the TCCs subject of the three assessments. Excluding these duplications, the basic tax involved in all three assessments represented by the face value of the related TCCs is P=911 million.

The Company does not believe these tax assessments and legal claims will have an adverse effect on its consolidated financial position and results of operations. The Company‟s external counsel‟s analysis of potential results of these cases was subsequently supported by the Decision of the Supreme Court in the case of Pilipinas Shell and in the Decision of the CTA En Banc on December 3, 2008. Pandacan Terminal Operations

The City Council of Manila, citing concerns of safety, security and health, passed City Ordinance No. 8027 reclassifying the areas occupied by the Oil Terminals of Petron, Shell and Chevron from Industrial to Commercial, making the operation of the Terminals therein unlawful. Simultaneous with efforts to address the concerns of the City Council with the implementation of a scale down program to reduce tankage capacities and joint operation of facilities with Shell and Chevron, the Company filed a petition to annul city Ordinance No. 8027 and enjoin the City Council of Manila, as well as Mayor Joselito Atienza from implementing the same.

Thereafter, the City of Manila approved the Comprehensive Land Use Plan and Zoning Ordinance (CLUPZO) (Ordinance No. 8119) that allows the Company a seven-year grace period. The passage of Ordinance No. 8119 was thought to effectively repeal Manila Ordinance No. 8027. However, on March 7, 2007, the Supreme Court rendered a Decision in the case of SJS Society vs. Atienza, directing the Mayor of Manila to immediately enforce Ordinance No. 8027. On March 12, 2007, the Company, together with Shell and Chevron, filed an Urgent Motion for Leave to Intervene and Urgent Motion to Admit Motion for Reconsideration of the decision dated March 7, 2007, citing that the Supreme Court failed to consider supervening events, notably (i) the passage of Ordinance No. 8119 which supersedes Ordinance No. 8027, as well as (ii) the writs of injunction from the RTC presenting the implementation of Ordinance No. 8027, the Supreme Court‟s decision and the enforcement of Ordinance No. 8027 improper. Further, the Company, Shell, and Chevron noted the ill-effects of the sudden closure of the Pandacan Terminals on the entire country.

On February 13, 2008, the Supreme Court allowed the oil companies‟ intervention but denied their motion for reconsideration, declaring Manila City Ordinance No. 8027 valid and applicable to the oil terminals at Pandacan. The Court dissolved all existing injunctions against the implementation of the ordinance and directed the oil companies to submit their relocation plans to the Regional Trial Court within 90 days to determine, among others, the reasonableness of the time frame for relocation. On February 28, 2008, the Company, jointly with Chevron and Shell, filed its motion for reconsideration of the Resolution. On May 13, 2008, the three oil companies submitted their Comprehensive Relocation Plans in compliance with the February 13 Resolution of the Supreme Court. In a Resolution dated April 21, 2009, the Supreme Court 1st Division referred the case to the Court En Banc. However, in its April 28, 2009 Resolution, the Supreme Court En Banc denied the Motion for Reconsideration. The Court declared that no further pleadings or motions will be entertained. As a result, the ruling of the Court that Manila Zoning Ordinance No. 8027 is applicable to the oil depots at Pandacan becomes final and binding on the oil companies.

10

Social Justice Society (SJS), Vladimir Cabigao and Bonifacio Tumbokon filed before the Supreme Court a Motion to stop the City Council of Manila from further hearing the amending ordinance to Ordinance No. 8027. Petitioners alleged that the proposed amendment is "a brazen and malicious attempt by the City of Manila to thwart the Supreme Court's 7 March 2007 decision and 13 February 2008 resolution on the case". To date, the Supreme Court has not issued any TRO or Order granting the motion filed by the petitioners. On May 28, 2009, Mayor Alfredo Lim of Manila approved and signed proposed Ordinance 7177 (which became Ordinance No. 8187) repealing Ordinance No. 8027 and 8119 and allowing the continued stay of the oil depots at Pandacan. On June 1, 2009, SJS officers filed a petition for prohibition against Mayor Lim before the Supreme Court, seeking the nullification of Ordinance 8187. On June 5, 2009, former Manila Mayor Lito Atienza filed his own petition with the Supreme Court seeking to stop the implementation of Ordinance 8187. The Court has ordered the City to file its comment but the Court did not issue a temporary restraining order. The City filed its Comment on August 13, 2009. Petron received a Notice of Entry of Judgment from the Clerk of Court stating that the March 7, 2007 decision of the Supreme Court had on February 27, 2008 become final and executory and has therefore been recorded in the Book of Entries of Judgment. Executive Order No. 839 On October 2, 2009, President Gloria Macapagal-Arroyo, under Proclamation No. 1898, declared a state of national calamity in view of the devastations caused by typhoon “Ondoy” and “Pepeng”. Allegedly in line with this proclamation, the President subsequently issued E.O. 839, mandating that prices of petroleum products being sold in Luzon be kept at October 15, 2009 levels. The oil companies, including the Petron, in compliance with E.O. 839, rolled back prices to October 15, 2009 levels. Pilipinas Shell filed its Petition on November 9, 2009 seeking prohibition, mandamus and injunction with prayer for the issuance of a temporary restraining order and/or writ of preliminary injunction. On November 13, 2009, the Regional Trial Court of Makati issued a temporary restraining order for a period of 20 days and scheduled further hearings for the writ of injunction. On November 16, 2009, thru E.O. 845, the President lifted the price freeze under E.O. 839 and directed a task force to implement proposals promised by oil firms, including discounts and staggered-price adjustments. Oil Spill Incident in Guimaras

M/T Solar I sunk 13 nautical miles southwest of Guimaras in rough seas on August 11, 2006 en route to Zamboanga, loaded with about 2 million liters of industrial fuel oil.

On separate investigations by the Special Task Force on Guimaras by the Department of Justice and the Special Board of Marine Inquiry (SBMI), both found the owners of M/T Solar I, Sunshine Marine Development Corporation (SMDC) liable. The DOJ found no criminal liability on the part of The Company. However, the SBMI found the Company to have overloaded the vessel. The Company has appealed the findings of the SBMI to the Department of Transportation and Communication (DOTC) and is awaiting its resolution.

The Company implemented a “Cash for Work” program involving residents of the affected areas in the clean-up operations and mobilized its employees to assist in the operations. By the middle of November 2006, the Company had cleaned up all affected shorelines and was affirmed by the inspections made by Taskforce Solar 1 Oil Spill (SOS), a multi-agency group composed of officials

11

from the Local Government Units, Departments of Health, Environment and Natural Resources, Social Welfare and Development, and the Philippine Coast Guard.

The Company collected a total 6,000 metric tons of debris which were brought to the Holcim Cement facility in Lugait, Misamis Oriental for processing/treatment of waste. On November 20, 2006, one of the last barge shipments of oil debris unfortunately sunk en route to the same plant[1].

The Company worked closely with the provincial government, Department of Welfare and Social Development (DSWD), Department of Agriculture (DA), Technical Education and Skills Development Authority (TESDA), the Philippine Business for Social Progress (PBSP), in developing livelihood programs for the local community. Last November 27, 2006, the Company held a scientific conference in cooperation with the University of the Philippines - Visayas, the National Disaster Coordinating Council (NDCC), the World Wildlife Fund (WWF) and the Guimaras Provincial Government with the objective of developing an integrated assessment and protocol for the rehabilitation of the province. On top of providing alternative livelihood for affected Guimarasnons, the company has established programs and facilities aimed at helping improve basic education in the province. The Company also established a mari-culture park at the Southeast Asian Fisheries Development Center (SEAFDEC) area in the town of Nueva Valencia in August 2007. Several representatives from nearby barangays received hands-on training including the construction of fish cages, stocking of fingerlings, feeding, maintenance work on the fish cages, harvesting and packaging for shipment to ensure that the program is sustainable. With regard to the retrieval of the remaining oil still trapped in M/T Solar I, the P & I contracted a sub-sea systems technology provider (Sonsub) to recover the oil from the sunken vessel. Oil recovery operation was technically completed on April 1, 2007. A total of 9,000 liters of oil was recovered. Representatives from the IOPC met with the claimants from various affected areas of Guimaras to give an orientation on the requirements of the claim as well as the documents required to be submitted in support of the claim. The Company has filed a total of P= 220 million against the IOPC as of September 2008. A total of P= 129 million has been paid to the Company. Out of the total outstanding claims on the International Oil Pollution Compensation Fund (IOPC) of P= 91 million, the Company collected P= 14 million on July 27, 2009 as final settlement. On June 17, 2009, a certain Emily Dalida, whose child Remelo M. Dalida died on August 16, 2006 at Brgy. Cabalagnan, Nueva Valencia, Guimaras, and Marcelino Gacho who was hospitalized for seventeen (17) days due to parapneumonic effusion, filed formal complaints for Homicide for the death of Remelo Dalida and for Less Serious Physical Injuries suffered by Gacho allegedly due to exposure to the oil spill along the shores of Cabalagnan against the respondents Sunshine Maritime Development Corp., Petron and Capt. Norberto Aguro, Master of M/T Solar I. Petron, through its legal counsel, submitted its counter-affidavit on August 4, 2009. On the basis of the statement in Petron‟s counter-affidavit, Dalida and Gacho amended their complaint, changing the offense alleged to violations of Sec 28, par. 5 in relation to Sec 4 of the Phil. Clean Water Act of 2004, and dropping current Petron President Eric O. Recto, the Vice President and Board of Directors as respondents.

1 To dispel fear of contamination in the area, personnel and equipment were brought to the sink site. In separate

statements made by the Philippine Coast Guard (PCG), DENR and the Bureau of Fisheries and Aquatic Resources

(BFAR), they found no traces of oil in the water. The Company engaged the services of Mindanao State University

and Dr. Angel Alcala of the Silliman University to conduct an impact assessment of the sunken debris on the

environment. Both studies concluded that the sinking of the ship had no effect on the environment.

12

On August 4, 2009, the Provincial Prosecutor served a subpoena with a complaint-affidavit from Oliver Chavez, supposedly the Municipal Agriculturist of Nueva Valencia who claims to be suffering from PTB due to his exposure to and close contact with waters along the shoreline and mangroves affected by the oil spill. The respondents are being charged of Violation of the Philippine Clean Water Act of 2004 (RA 9275). On or about August 24, 2009, Chavez filed a Manifestation and Motion to Amend Complaint, changing the offense alleged to violations of Sec 28, par. 5 in relation to Sec 4 of the Phil. Clean Water Act of 2004, and dropping current Petron President Eric O. Recto as respondent. The Provincial Prosecutor issued a Subphoena in both cases directing Petron to file their Counter-Affidavit and other controvertible evidence. Petron filed its Counter-Affidavits. The cases are now deemed submitted for resolution. Bataan Real Property Tax Cases

On August 21, 2007, Bataan Provincial Treasurer issued a Final Notice of Delinquent Real Property Tax requiring the Company to settle the amount of P=2,168 million allegedly in delinquent real property taxes as of September 30, 2007.

The Company had previously contested the assessments subject of the Notice of Delinquent Real Property Taxes, appealed the same to the Local Board of Assessment Appeals (LBAA), and posted the necessary surety bonds to stop collection of the assessed amount. The Company contested a first assessment covering the Isomerization and Gas Oil Hydrotreater (GOHT3) Facilities of the Company which enjoy, among others, a 5-year real property tax exemption under the Oil Deregulation Law (RA 8479) per Board of Investments (BOI) Certificates of Registration. The second assessment is based on alleged non-declaration by the Company of machineries and equipment in its Bataan refinery for real property tax purposes and/or paid the proper taxes thereon since 1994. The Company questioned this second assessment on the ground among others that: there was no non-declaration; back taxes can be assessed only for a maximum of 10 years, even assuming fraud; erroneous valuations were used; some adjustments like asset retirement and non-use were not considered; some assets were taken up twice in the assessments; and some assets enjoyed real property tax exemptions. Notwithstanding the appeal to the LBAA and the posting of the surety bond, the Provincial Treasurer proceeded with the publication of the Public Auction of the assets of the Company, which she set for October 17, 2007.

The Company exerted all efforts to explain to the Treasurer that the scheduled auction sale was illegal considering the Company‟s appeal to the LBAA and the posting of the surety bond. Considering the Treasurer‟s refusal to cancel the auction sale, the Company filed a complaint for injunction on October 8, 2007 before the Regional Trial Court to stop the auction sale. A writ of injunction stopping the holding of the public auction until the case is finally decided was issued by the RTC on November 5, 2007.

A motion to dismiss filed by the Provincial Treasurer on the ground of forum-shopping was denied by the RTC. However, a similar motion based on the same ground of forum shopping was filed before the LBAA by the respondents and the motion was granted by the LBAA on December 10, 2007.

On January 4, 2008, the respondents appealed the RTC‟s grant of a writ of injunction to the Supreme Court. Last January 17, 2008, the Company appealed from the LBAA‟s dismissal of its appeal by filing a Notice of Appeal with the CBAA. In an Order dated August 13, 2008, the CBAA reversed the LBAA‟s

13

dismissal of appeal and ordered that the case be remanded to the LBAA of the Province of Bataan to be proceeded "solely for the purpose of ascertaining the facts."

On June 27, 2008, the Supreme Court dismissed the petition filed by Talento on the Order granting the writ of injunction. All five Justices concurred that Talento‟s appeal was procedurally defective and/or was filed out of time. The Court ruled that the issues raised by the Company against the assessment should be resolved before any auction sale is conducted; that the auction sale will have serious repercussions on the operations of the Company; and that a surety bond may be filed in lieu of payment of the taxes under protest to stop collection. Motions for reconsideration filed by Provincial Treasurer and the League of Provinces of the Philippines (LPP) were denied. On June 25, 2010, the RTC Presiding Judge, upheld the position of Petron and declared null and void the Notice of Delinquent Taxes, the Final Notice of Delinquent Real Property Tax, the Notice of Sale of Real Property for Unpaid Real Property Tax, and the levy on the properties of Petron based on said notices, for the reason that these acts of the Provincial Treasurer deprived Petron of its right to due process and were done whimsically and arbitrarily.

13. Financial Risk Management Objectives and Policies

Foreign Exchange Risk The Company‟s functional currency is the Philippine peso, which is the denomination of the bulk of the Company‟s revenues. The Company‟s exposures to foreign exchange risk arise mainly from US dollar-denominated sales as well as purchases principally of crude oil and petroleum products. As a result of this, the Company maintains a level of US dollar-denominated assets and liabilities during the period. Foreign exchange risk occurs due to differences in the levels of US dollar-denominated assets and liabilities.

The Company pursues a policy of hedging foreign exchange risk by purchasing currency forwards or by substituting US dollar-denominated liabilities with peso-based debt. The natural hedge provided by US dollar-denominated assets is also factored in hedging decisions. As a matter of policy, currency hedging is limited to the extent of 100% of the underlying exposure.

The Company is allowed to engage in active risk management strategies for a portion of its foreign exchange risk exposure. Loss limits are in place, monitored daily and regularly reviewed by management.

The following is the summation of the Company‟s foreign currency-denominated financial assets and liabilities as of June 30, 2010, June 30, 2009 and December 31, 2009:

Jun 30, 2010 Jun 30, 2009 Dec. 31, 2009

In USD In USD In USD

Financial assets 468 97 250 Financial liabilities (676) (345) (128)

Net foreign exposure (208) (248) 122

The exchange rates used to restate the US dollar denominated financial assets and liabilities stated above are P=46.37 (2Q2010), P=48.13 (2Q2009) and P=46.20 (4Q2009), respectively.

The succeeding table shows the effect of the percentage changes in the Philippine peso to US dollar exchange rate on the Company‟s income before tax. These percentages have been determined based on the market volatility in exchange rates in the previous three months for the

14

quarter period ended June 30, 2010, June 30, 2009, and full year 2009 estimated at 95% level of confidence. The sensitivity analysis is based on the Company‟s foreign currency financial instruments held at each statement of financial position date, with effect estimated from beginning of the year. Had the Philippine peso strengthened/weakened against the US dollar then these would have the following impact: Jun 30, 2010 Jun 30, 2009 Dec. 31, 2009

Increase/Decrease in exchange rates 8.63% 9.73% 12.72% Increase/Decrease in pre-tax income P832 P1,161 (P=717)

Interest Rate Risk The Company‟s exposure to interest rate risk is mainly related to its cash and cash equivalent and debt instruments. Currently, the Company has achieved a balanced mix of cash balances with various deposit rates and fixed and floating rates on its various debts.

Future hedging decisions for floating deposit/interest rates will continue to be guided by an assessment of the overall deposit and interest rate risk profiles of the Parent Company considering the net effect of possible deposit and interest rate movements.

The succeeding table illustrates the sensitivity of income before tax for the year, given the assumed increases/decreases in deposit rates and interest rates for Philippine peso loans and US dollar term loans, all of which at 95% level of confidence, with effect from the beginning of the quarter periods ending June 2010, June 2009 and December 2009. These changes are considered to be reasonably possible given the observation of prevailing market conditions in those periods. The calculations are based on the Company‟s financial instruments held at each of those statements of financial position dates. All other variables are held constant.

Effect of changes in interest rates on Philippine peso and US dollar-denominated loans with floating interest rates:

Jun 30, 2010 Jun 30, 2009 Dec. 31, 2009

PHP USD PHP USD PHP USD

Increase/decrease interest rates for deposits (19.27%) (23.71%) (33.52%) (8.38%)

(44.35%)

(12.80%)

Increase/decrease interest rates for short term loans 15.46% - 30.73%

33.17%

-

Increase/decrease interest rates for long term loans 8.06% 2.33% 28.89% -

35.06%

-

Increase/decrease in pretax income P158 (P11) P458 (P3)

P723

(P13)

The following table sets out the carrying amount of the Company‟s financial instruments exposed to interest rate risk:

Jun 30, 2010 Jun 30, 2009 Dec. 31, 2009

Cash in bank and cash equivalent P25,102 P10,943 P9,884 Short-term loans 31,003 37,971 42,744 Long-term loans 17,461 1,667 1,333

15

Sensitivity to interest rates varies during the year considering the volume of cash and loan transactions. The analysis above is considered to be a representative of the Company‟s interest rate risk.

Credit Risk In effectively managing credit risk, the Company regulates and extends credit only to qualified and credit-worthy customers and counterparties, consistent with established Company credit policies, guidelines and credit verification procedures. Requests for credit facilities from trade customers undergo stages of review by Marketing and Finance Divisions. Approvals, which are based on amounts of credit lines requested, are vested among line managers and top management that include the President and the Chairman.

Generally, the maximum credit risk exposure of financial assets is the total carrying amount of the financial assets as shown on the face of the consolidated statement of financial position or in the notes to the consolidated financial statements, as summarized below.

Jun 30, 2010 Jun 30, 2009

Cash in bank and cash equivalents P=25,102 P=10,943 Receivables 29,565 27,402

Total P=54,667 P=38,345

The credit risk for cash and cash equivalents and derivative financial instruments is considered negligible, since the counterparties are reputable entities with high quality external credit ratings. The credit quality of this other financial assets is therefore considered to be high grade.

In monitoring trade receivables and credit lines, the Company maintains up-to-date records where daily sales and collection transactions of all customers are recorded in real-time and month-end statements of accounts are forwarded to customers as collection medium. Finance Division‟s Credit Department regularly reports to management trade receivables balances (monthly) and credit utilization efficiency (semi-annually). Collaterals. To the extent practicable, the Company also requires collateral as security for a credit facility to mitigate credit risk in trade receivables. Among the collaterals held are real estate mortgages, bank guarantees, letters of credit and cash bonds. These securities may only be called on or applied upon default of customers. Credit Risk Concentration. The Company‟s exposure to credit risk arises from default of counterparty. Generally, the maximum credit risk exposure of trade receivable assets is its carrying amount without considering collaterals or credit enhancements, if any. The Company has no significant concentration of credit risk since the Company deals with a large number of homogenous trade customers. The Company does it execute any credit guarantee in favor of any counterparty. Credit Quality. In monitoring and controlling credit extended to counterparty, the Company adopts a comprehensive credit rating system based on financial and non-financial assessments of its customers. Financial factors being considered comprised of the financial standing of the customer while the non-financial aspects include but are not limited to the assessment of the customer‟s nature of business, management profile, industry background, payment habit and both present and potential business dealings with the Company. Class A “High Grade” are accounts with strong financial capacity and business performance and with the lowest default risk.

16

Class B “Moderate Grade” refer to accounts of satisfactory financial capability and credit standing but with some elements of risks where certain measure of control is necessary in order to mitigate risk of default. Class C “Low Grade” are accounts with high probability of delinquency and default. Liquidity Risk The Company is exposed to the possibility that adverse changes in the business environment and/or its operations could result to substantially higher working capital requirements and consequently, a difficulty in financing additional working capital. The Company manages liquidity risk by keenly monitoring its cash position as well as maintaining a pool of credit lines from financial institutions that exceeds projected financing requirements for working capital. The Company, likewise, regularly evaluates other financing instruments and arrangements to broaden the Company‟s range of sources of financing.

Commodity Price Risk

To minimize the Company‟s risk of potential losses due to volatility of international crude and product prices, the Company implemented commodity hedging for petroleum products. The hedging authority approved by the BOD is intended to (a) protect margins of MOPS (Mean of Platts of Singapore)-based sales and (b) protect product inventories from downward price risk. Hedging policy (including the use of commodity price swaps, buying of put options, and use of collars and three-way options; with collars and 3-way options starting in March 2008) developed by the Commodity Risk Management Committee is in place. Decisions are guided by the conditions set and approved by the Company‟s management. Other Market Price Risk The Company‟s market price risk arises from its investments carried at fair value (FVPL and AFS financial assets). It manages its risk arising from changes in market price by monitoring the changes in the market price of the investments.

17

Petron Corporation and Subsidiaries

Receivables

June 30, 2010

(Amounts in Millions)

Breakdown:

Accounts Receivable - Trade 15,081

Accounts Receivable - Non-Trade 14,484

Total Accounts Receivable 29,565

AGING OF TRADE ACCOUNTS RECEIVABLES

Receivables 1-30 days 7,833

31-60 days 4,560

61-90 days 2,491

Over 90 days 976

Total 15,859

Allowance for doubtful accounts 778

Accounts Receivable - Trade 15,081

18

Interim Financial Report as of June 30, 2010 Management Discussion and Analysis of Financial Condition and Results of Operations

Operating Revenues and Expenses

Petron posted a consolidated net income of P= 2.96 billion for the first half of the year, 64% higher than the year-ago profit of P= 1.8 billion. The significant improvement in the Company‟s bottom line was fueled by higher domestic sales and better margins from petrochemical feedstocks coupled with the reduction in interest expense and translation gains on dollar-denominated transactions. Comparative summary follows:

Variance- Fav (Unfav)

(In Million Pesos) 2010 2009 Amt

%

Sales 115,354 76,679 38,675 50

Cost of Goods Sold 105,867 69,406 (36,461) (53)

Gross Margin 9,487 7,273 2,214 30

Selling and Administrative Expenses 2,839 2,766 73

3

Non-operating Charges 2,791 1,966 (825) 42

Net Income 2,960 1,808 1,731 96

EBITDA 7,218 6,399 820 13

Sales Volume (MB) 23,979 21,414 2,565 12

Earnings per Share 0.31 0.19 0.12 64

Return on Sales (%) 2.6 2.4 0.2 9

During the second quarter, Petron registered net earnings of P= 1.03 billion, up by 10% from P= 934 million profit for the same period last year. Stable crude oil and finished products prices resulted in better margins this year compared last year as most of the products sold came from expensive crude in 2008 after the total plant shutdown (TPS) in the first quarter. Consequently, earnings before interest, taxes, depreciation and amortization (EBITDA) reached P= 7.22 billion, 13% more than the year ago total of P= 6.4 billion. Earnings per share escalated to P= 0.31 from P= 0.19 a year earlier while return on sales almost matched last year‟s 2.4%. Major contributory factors are the following: Gross margin (GM), in terms of amount, rose by 30% to P= 9.49 billion from previous year‟s P= 7.27 billion owing largely to increased sales volume and better returns on exports of petrochemicals. With the full commercial operations of the BTX unit, sales of propylene more than tripled to 486MMB from 146MMB while benzene and toluene contributed a total turnover of 591MMB versus NIL last year. However, GM rate dropped to 8% from 9% in the first half 2009 on account mainly of negative margins on fuel (Naphtha) exports.

The following accounted for the variance in gross margin:

19

Sales volume went up by 12% to 24.0MMB from prior year‟s 21.4MMB primarily from higher diesel and petrochemical sales. Demand for diesel grew due to increased operations of independent power producers during the election period combined with the effect of new service station builds. Last year, the refinery was on TPS in the first quarter while the BTX unit started commercial operations only in April limiting production and sales of petrochemicals as well as of fuel products in the first semester.

Net sales totaled P= 115.35 billion, almost twice the 2009 level of P= 76.68 billion traceable mainly to higher average selling price per liter (2010: P= 29.61 vs. 2009:P= 21.97) complemented by the 2.6MMB incremental sales volume. Year-on-year, regional MOPS prices escalated to an average US$81.55/bbl this year from US$55.75/bbl in first half of 2009.

Cost of Goods Sold (CGS) surged to P= 105.87 billion from P= 69.41 billion in the same period the previous year brought about by more expensive crude purchases that went into CGS (2010: US$77.88 vs. 2009: US$53.31). Since the refinery was on TPS for the first few months of 2009, only 58% of CGS was sourced from crude compared to 84% this year. As against last year, average importation costs per liter were cheaper vis-à-vis in 2010 (2010: P= 19.70 vs. 2009: P= 16.50).

Refinery Operating Expenses, which formed part of CGS, declined by 6% to P= 2.47 billion as maintenance and repairs (M&R) were trimmed down by half. The bulk of last year‟s M&R were related to the restoration of the electrical facilities damaged by the 2008 fire incident plus turnaround activities of some units.

Selling & Administrative Expenses of P= 2.84 billion for the year matched 2009 level as increased

expenses related to service station network expansion projects were offset by lower advertising expenses. However, on a peso per liter basis, actual OPEX was lower at P= 0.72 versus P= 0.81 a year ago as volume sold grew from 21.4MMB to 24.0MMB

Net Financing Costs & Other Charges of P= 2.79 billion moved up by 42% from last year‟s total. Interest expense was lower this year by P= 710 million which can be attributed to the decline in short-term borrowing level (2010 average: P= 35.2B vs. 2009 average: P= 42.9B) and rates (2010: 4.3% vs. 2009: 6.7%). This was slightly tempered by the rise in long-term interest payments (by P= 357 million) mostly related to the P= 10 billlion FXCN loan availed in June 2009. However, lower interest expense was fully offset by higher forex and commodity hedging losses recorded this year.

Capital Resources and Liquidity At the close of the first half of the year, Petron‟s total resources stood atP= 139.0 billion, up 23% or P= 25.8 billion from end-December 2009 level of P= 113.19 billion. Loan availments to finance capital expenditures augmented cash and cash equivalents by 118% or P= 15.34 billion to P= 28.32 billion. Financial assets at fair value through profit or loss climbed by 15% or P= 26.0 million from P= 169 million to P= 195 million brought about by higher market values of investments in marketable equity securities and proprietary memberships. Inventories-net rose to P= 37.66 billion from P= 28.17 billion as of December 31, 2009. This was attributed to higher volume of crude and finished products equivalent to P= 12.76 billion partly offset by the drop in prices (2010 per liter: P= 24.33 vs. 2009: P= 26.97) from year-end level valued at P= 3.42 billion. There were minimal purchases in December in anticipation of the impact of the ASEAN Trade in Goods Agreement (ATIGA).

20

Other current assets dropped by 40% or P= 1.8 billion from P= 4.47 billion to P= 2.67 billion essentially on account of filing input VAT claims on zero-rated sales. Deferred tax assets declined this period to P= 6.0 million from end-December 2009‟s P= 7 million due mainly to the effect of translation adjustment for the foreign insurance subsidiary. Other non-current assets were higher at P= 3.25 billion this year from P= 1.33 billion in year-end 2009 primarily traced to advances to the retirement fund. Short-term loans and liabilities for crude oil and petroleum product importations slipped by 6% (P= 3.09 billion) from P= 50.27 billion to P= 47.18 billion due essentially to settlements made partly tempered by higher crude/finished products importations.. Long-term debt inclusive of current portion escalated by 81% or P= 15.39 billion from P= 18.89 billion to P= 34.28 billion traceable to the newly-availed foreign loan amounting to US$355 million partly reduced by amortizations on outstanding loans.

Income tax payable increased to P= 14 million from P= 10 million as at December 31, 2009 owing to higher tax liabilities reported by the subsidiaries. Deferred tax liabilities-net at P= 1.17 billion more than doubled the P= 514 million level at end-December 2009 traceable to the impact of NOLCO as well as temporary differences reflected under parent and subsidiaries‟ accounts. Other non-current liabilities moved up by 6% or P= 64 million to P= 1.12 billion this period from P= 1.05 billion as of December 2009 mainly because of the increments in provision for Asset Retirement Obligation and cylinder/cash bond deposits. Total equity attributable to equity holders of the parent closed at P= 50.14 billion at the end of the first semester showing a 34% or P= 12.60 growth over the end-December 2009 level attributable mainly to the following:

P= 9.86 billion additional paid-in capital from the issuance of preferred shares; P= 2.96 billion first half net income partly reduced by the P= 238.2 million dividend on

preferred shares; and, Cash Flow Operating activities of the Company generated net cash inflows amounting to P= 4.45 billion, 73% lower than a year earlier due mainly to incremental requirements for working capital.

In Million Pesos

June 30, 2010

June 30, 2009

Change

Operating Inflows 4,450 16,475 (12,025)

Investing Outflows (2,573) (9,440) (6,867)

Financing Inflows (Outflows) 13,309 (6,645) 19,954

21

Discussion of the company’s key performance indicators:

Ratio June 30, 2010 Dec 31, 2009

Current Ratio 1.8 1.3

Debt to Equity Ratio 1.8 2.0

Return on Equity (%) 13.7 12.1

Debt Service Coverage 5.3 4.2

Tangible Net worth 50.1B 37.5B

Current Ratio: Total current assets divided by total current liabilities. This ratio is a rough indication of a company's ability to service its current obligations. Generally, the higher the current ratio is, the greater the "cushion" between current obligations and a company's ability to pay them. Debt Equity Ratio: Total liabilities divided by tangible net worth. This ratio expresses the relationship between capital contributed by creditors and that contributed by owners. It expresses the degree of protection provided by the owners for the creditors. The higher the ratio, the greater the risk being assumed by creditors. A lower ratio generally indicates greater long-term financial safety. Return on Equity: Net income divided by average total stockholders‟ equity. This ratio reveals how much profit a company earned in comparison to the total amount of shareholders equity found on the balance sheet. A business that has a high return on equity is more likely to be one that is capable of generating cash internally. For the most part, the higher a company‟s return on equity compared to its industry, the better. Debt Service Coverage: The sum of free cash flows and available closing cash balance divided by projected debt service. This ratio shows the cash flow available to pay for debts to the total amount of debt payments to be made. It also measures the company‟s ability to settle dividends, interests and other financing charges. Tangible Net Worth: Net worth minus intangible assets. This figure gives a more immediately realizable value of the company. Known trends, demands, commitments, events or uncertainties that will have a material impact on the issuer’s liquidity Gross Domestic Product (GDP) The Philippine economy strongly rebounded from its sluggish growth of 1.1% in 2009. During the first quarter, GDP surged 7.3% as the economy benefitted from strong remittance inflows, robust recovery of trade activity, higher government and personal consumption, stable peso, prices and interest rates, and hefty election spending. This is despite the challenges faced by the economy like the El Niño crisis which hurt the agricultural sector, and the power crisis experienced during the period. 91-Day Treasury Bill/Philippine Dealing System Treasury Reference(PDST-F) Rates 91-day T-bill rates as of the first half 2010 stood at an average of 3.9%, lower than 2009‟s 4.9% FY average. Interest rates in 2010 were kept low as liquidity in the financial markets remained sufficient. Stable inflation also allowed the Bangko Sentral ng Pilipinas (BSP) to maintain its interest rates at

22

record low. Since December 2008, BSP has cut its policy rates by a total of 200 basis points to 4% for overnight borrowing rate and 6% for overnight lending rate and this has been maintained to date. For the first half of 2010, the three month PDST-F stood at 4.0924%, lower than 2009‟s full year average of 4.116%. Interest rate stayed at the low end in view of the strong liquidity in the market and the inflation rate which remained at 3.9%. In spite of the forecasted slow economic growth for the second-half of the year, BSP‟s policy rate settings remain unchanged. Yields will move sideways as inflation rate stays at the 4% level. Peso - US dollar Exchange Rate

The local currency sustained its strength towards the 2nd quarter. From 2009 average of P47.6/$, the peso gained 3.9% to average P45.8/$ in the first half. The strong growth of OFW remittances, heavy rebound of exports, improved investor appetite with the global economic recovery, and market optimism on the new administration‟s good governance and policies, contributed to the peso‟s appreciation. Inflation Inflation averaged 4.3% in the 1st half, up from the 2009‟s 3.2% average. Uptick in prices of commodities like fuels, light, and water, and services contributed to the rise in inflation. However, although prices went up, inflation remained relatively stable and manageable staying within the government‟s target inflation of 3.5-5.5% in FY 2010. Dubai Price Dubai crude averaged $77/bbl in the first six months of 2010, a strong recovery from the $61.9/bbl average in FY 2009. The uptrend of crude prices was supported by optimism arising from signs of economic recovery. Outlook for world oil demand has also improved with agencies like OPEC, Energy Information Administration, and International Energy Agency revising their 2010 forecasts upward. The weakness of the dollar also diverted investment funds to the oil market.

Industry Oil Demand Data from DOE shows that as of May 2010, total oil industry demand surged by 6% to 308.4 MBD this year from 291.1 MBD in the same period last year. Election spending and economic rebound supported fuel consumption. Sustained OFW remittances, strong vehicle sales, and heavy rebound in the trade, air transport and power sectors during the period boosted demand for oil. Tight Industry Competition Competition remains stiff with the new players implementing different marketing strategies and aggressively expanding. As of YTD May 2010, the new players have collectively cornered around 20.7% of the total oil market. Collectively, the new players are leading the LPG market segment with 49.6%

market share. Updates on Capital Program The 2010 capital program endorsed last December 2009 is P= 15.1 billion. Of this amount P= 13.9 billion has already been approved and includes the refinery‟s power plant, service station and non-fuels business expansion, additional tankage at the depots and at the refinery, maintenance projects and the

23

relocation of the Makati head office to San Miguel Head Office Compound. The remaining projects totaling P= 1.2 billion will be further evaluated within the year.

Known trends, events or uncertainties that have had or that are reasonably expected to have a material favorable or unfavorable impact on net sales/revenues/income from continuing operations

Illegal Trade Practices Cases of smuggling and illegal trading (e.g. “bote-bote” retailing, illegal refilling) continue to be a concern. These illegal practices have resulted in unfair competition among players. Existing or Probable Governmental Regulations EO 890: Removing Import Duties on All Crude and Refined Petroleum Products. After the ASEAN Trade in Goods Agreement (ATIGA) was implemented starting 2010, tariff rate structure in the oil industry was distorted with crude and product imports from ASEAN countries enjoying zero tariff while crude and product imports from outside the ASEAN are levied 3%. To level the playing field, Petron filed a petition with the Tariff Commission to apply the same tariff duty on crude and petroleum product imports, regardless of source. In June 2010, the government approved Petron‟s petition and issued Executive Order 890 which eliminates import duties on all crude and petroleum products regardless of source. The reduction of duties took effect on July 4, 2010 and was then considered in the implementation of rollbacks in the pump prices of fuels. Biofuels Act of 2006. Currently, the Biofuels Act of 2006 mandates that ethanol comprise 5% of total gasoline volumes, and diesels contain 2% CME (cocomethyl ester). By 2011, all gasoline grades should contain 10% ethanol. Moving forward, the National Biofuels Board will review and recommend further increases in ethanol and CME content. At the moment, however, the Department of Energy is considering making amendments to the Biofuels Act amidst the shortage of locally-produced ethanol. To produce compliant fuels, the Company invested in CME (coco methyl esther) injection systems at the refinery and depots. Prior to the mandatory blending of ethanol into gasoline by 2009, the Company already started selling ethanol blended gasoline in selected service stations in Metro Manila in May 2008. Renewable Energy Act of 2008. The Renewable Energy Act signed in December 2008 aims to promote development and commercialization of renewable and environment-friendly energy resources (e.g. biomass, solar, wind) through various tax incentives. Renewable energy developers will be given 7-year income tax holiday, power generated from these sources will be VAT-exempt, and facilities to be used or imported will also have tax incentives. Laws on Oil Pollution. To address issues on marine pollution and oil spillage, the MARINA mandated the use of double-hull vessels for transporting black products beginning end-2008 and by 2011 for white products. Petron has been using double-hull vessels in transporting all black products and some white products already. Clean Air Act. Petron invested in a Gasoil Hydrotreater Plant and in an Isomerization Plant to enable it to produce diesel and gasoline compliant with the standards set by law.

24

Liquefied Petroleum Gas (LPG) Bill. The LPG Act of 2009 aims to ensure safe practices and quality standards and mitigate unfair competition in the LPG sector. LPG cylinder seal suppliers must obtain a license and certification of quality, health and safety from the Department of Energy before they are allowed to operate. LPG cylinder requalifiers, repairers and scrapping centers, will also have to obtain a license from the Department of Trade and Industry. The Bill also imposes penalties on underfilling, underdelivering, illegal refilling and storage, sale or distribution of LPG-filled cylinders without seals, illegal possession of LPG cylinder seal, hoarding, and importation of used or second-hand LPG cylinders, refusal of inspection, and non-compliance to standards. Significant elements of income or loss that did not arise from the issuer’s continuing operations

There are no elements of income or loss that did not arise from the Registrant‟s continuing operations.

Any events that will trigger direct or contingent financial obligation that is material to the company, including any default or acceleration of an obligation

TCC-Related Matters

In 1998, the Company contested before the Court of Tax Appeals (CTA) the collection by the Bureau of Internal Revenue (BIR) of deficiency excise taxes arising from the Company‟s acceptance and use of Tax Credit Certificates (TCCs) worth P=659 million from 1993 to 1997. In July 1999, the CTA ruled that, as a fuel supplier of BOI-registered companies, the Company was a qualified transferee for the TCCs and that the collection by the BIR of the alleged deficiency excise taxes was contrary to law. The BIR appealed the ruling to the Court of Appeals where the case is still pending. In November 1999, BIR issued an assessment against the Company for deficiency excise taxes of P=284 million plus interest and charges for the years 1995 to 1997, as a result of the cancellation by the Department of Finance (DOF) Center ExCom of Tax Debit Memos (TDMs), the related TCCs and their assignments. The Company contested on the grounds that the assessment has no factual and legal bases and that the cancellation of the TDMs was void. The Company elevated this protest to the CTA on July 10, 2000. On August 23, 2006, the Second Division of the CTA rendered its Decision denying the Company‟s petition and ordered it to pay the BIR P=580 million representing deficiency excise taxes for 1995 to 1997 plus 20% interest per annum from December 4, 1999. The Company‟s motion for reconsideration was denied on November 23, 2006. The Company appealed the Division‟s Decision to the CTA En Banc. On October 30, 2007, the CTA En Banc dismissed the Company‟s appeal, with two of four justices dissenting. The Company filed its appeal on November 21, 2007 with the Supreme Court. On December 21, 2007, in the substantially identical case of Pilipinas Shell, the Supreme Court decided to nullify the assessment of the deficiency excise taxes and declared as valid Pilipinas Shell‟s use of Tax Credit Certificates for payment of its tax liabilities. On November 7, 2008, the Supreme Court gave due course to the Company‟s appeal. After the parties filed their respective memoranda, the case is now submitted for resolution.

In May 2002, the BIR issued a collection letter for deficiency taxes of P=254 million plus interest and charges for the years 1995 to 1998, as a result of the cancellation of TCCs and TDMs by the DOF Center ExCom. The Company protested this assessment on the same legal grounds used against the tax assessment issued by the BIR in 1999. The Company elevated the protest to the CTA. The 2nd Division of the CTA promulgated a decision on May 4, 2007 denying our Petition for Review for lack of merit. The Company was ordered to pay the respondent the reduced amount of P=601 million representing the Company‟s deficiency excise taxes for the taxable years 1995 to 1998. In addition, the Company was ordered to pay the BIR 25% late payment surcharge and 20% delinquency interest per annum computed from June 27, 2002. On appeal, the CTA En Banc on December 3, 2008, promulgated a decision reversing the unfavorable decision of the CTA 2nd Division. The CIR filed a Petition for Review with the Supreme Court. Petron‟s Comment was filed on April 20, 2009.

25

It should be noted that there are duplications in the TCCs subject of the three assessments. Excluding these duplications, the basic tax involved in all three assessments represented by the face value of the related TCCs is P=911 million. The Company does not believe these tax assessments and legal claims will have an adverse effect on its consolidated financial position and results of operations. The Company‟s external counsel‟s analysis of potential results of these cases was subsequently supported by the Decision of the Supreme Court in the case of Pilipinas Shell and in the Decision of the CTA En Banc on December 3, 2008.