C HAPTER 12 MONEY, BANKING, AND THE FINANCIAL SYSTEM.

26

CHAPTER 12 MONEY, BANKING, AND THE FINANCIAL SYSTEM

-

Upload

barrie-franklin -

Category

Documents

-

view

221 -

download

0

Transcript of C HAPTER 12 MONEY, BANKING, AND THE FINANCIAL SYSTEM.

CHAPTER 12

MONEY, BANKING, AND THE FINANCIAL SYSTEM

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

FISCAL POLICY

There are two types of government policies meant to affect prices and short term output. Monetary Policy-control over the money supply

Determined by the Federal Reserve Discuss later

Fiscal Policy. Determined by congress and the president.

The Federal Government (not including the Federal Reserve) using fiscal policy has two ways to affect economic activity. Government Spending.

Simultaneously raising taxes and spending. Deficit Spending- simultaneous increase in

government spending and borrowing. Taxes.

Raising or lowering taxes.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

THE IMPORTANCE OF MONEY

Money

Money performs a crucial role in facilitating the process of exchange by reducing transaction costs.

Money can be used by the government as an alternative to raising taxes as a method of taking individual/business wealth. More common among 3rd world countries where tracking a

person’s economic life is difficult.

In the U.S., printing money is not used much as a revenue raising device.

CTR?

Structuring

Money can theoretically be used as a tool, in certain limited circumstances, to temporarily increase economic activity. Monetary Policy

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Mercedes S500:

U.S. Price: $94, 500Thailand Price: 11,900,000 baht = $397,000 USDCommunist China: 2188000 RMB = $342. 142 USD

Hublot Big Bang – King Power 48mm. - $15,000 USD

Big Bang Tutti Frutti 38mm. - $14,000 USD

Gold Rolex Daytona 40mm. - $14,000 USD

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

$15 USD

Poor countries tend to not issue large denomination bills.

Make it difficult to conduct transactions in cash.

$703 USD

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

MEANING OF MONEY What is it?

Money (or the “money supply”): anything that is generally accepted in payment for goods or services or in the repayment of debts.

A rather broad definition

Money (a stock concept) is different from: Wealth: the total collection of pieces of property

that serve to store value

Income: flow of earnings per unit of time (a flow concept)

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

FUNCTIONS OF MONEY Medium of Exchange:

Eliminates the trouble of finding a double coincidence of needs (reduces transaction costs)

Promotes specialization A medium of exchange must

be easily standardized, widely accepted, be divisible, be easy to carry, not deteriorate quickly.

Unit of Account: used to measure value in the economy reduces transaction costs

Store of Value: used to save purchasing power over time. other assets also serve this function Money is the most liquid of all assets but loses value during inflation

By far the most important function money performs is a medium of exchange that reduces transaction costs and facilitates exchange which is the bedrock of a market economy.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

EVOLUTION OF THE PAYMENTS SYSTEM

Commodity Money: valuable, easily standardized and divisible commodities (e.g. precious metals, cigarettes).

Fiat Money: paper money decreed by governments as legal tender.

Checks: an instruction to your bank to transfer money from your account

Electronic Payment (e.g. online bill pay). E-Money (electronic money):

Debit card Stored-value card (smart card) E-cash

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

MEASURING MONEY

How do we measure money? Which particular assets can be called “money”?

Construct monetary aggregates using the concept of liquidity:

M1 (most liquid assets) = currency + traveler’s checks + demand deposits + other checkable deposits.

M2 (adds to M1 other assets that are not so liquid) = M1 + small denomination time deposits + savings deposits and money market deposit accounts + money market mutual fund shares.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 1 MEASURES OF THE MONETARY AGGREGATES

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

MONETARY AGGREGATES

Currency

Traveler’s Checks

Demand Deposits

Other Check. Dep

M1 (4)M2 (4+3)

M3 (4+3+4)

Small Den. Dep.

Savings and MM

Money Market Mutual Funds Shares

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

M1 VS. M2

Does it matter which measure of money is considered?

M1 and M2 can move in different directions in the short run (see figure).

Conclusion: the choice of monetary aggregate is important for policymakers.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

FIGURE 1 GROWTH RATES OF THE M1 AND M2 AGGREGATES, 1960–2008

Sources: Federal Reserve Bulletin, p. A4, Table 1.10, various issues; Citibase databank; www.federalreserve.gov/releases/h6/hist/h6hist1.txt.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

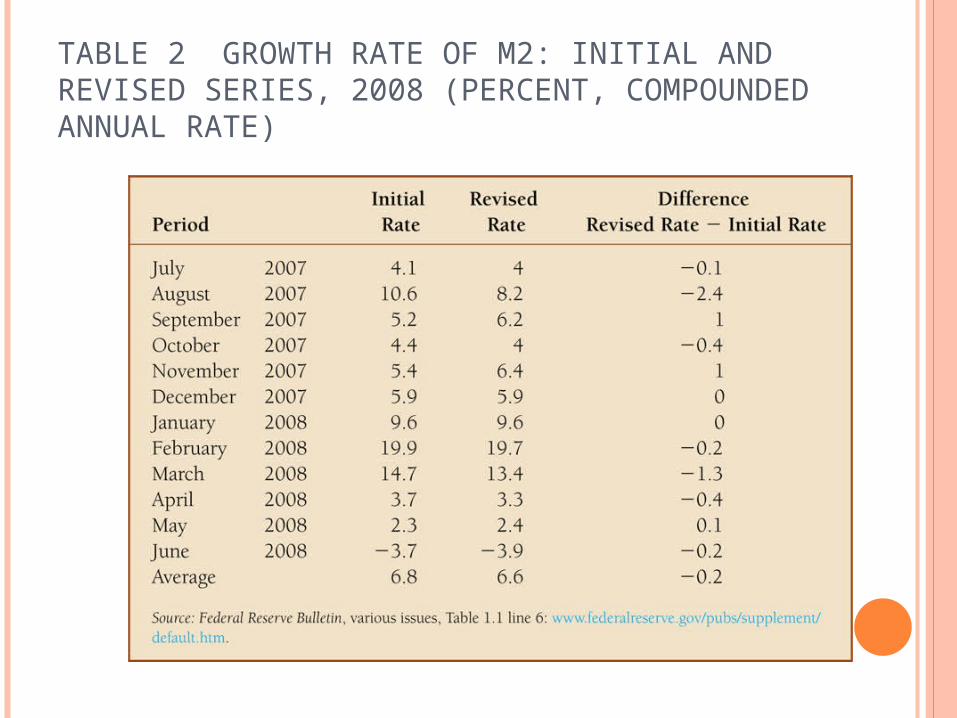

HOW RELIABLE ARE THE MONEY DATA?

Revisions are issued because: Small depository institutions report infrequently Adjustments must be made for seasonal

variation

We probably should not pay much attention to short-run movements in the money supply numbers, but should be concerned only with longer-run movements

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 2 GROWTH RATE OF M2: INITIAL AND REVISED SERIES, 2008 (PERCENT, COMPOUNDED ANNUAL RATE)

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

FUNCTION OF FINANCIAL MARKETS

Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage of funds

Promotes economic efficiency by producing an efficient allocation of capital, which increases production

Directly improve the well-being of consumers by allowing them to time purchases better

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

FIGURE 1 FLOWS OF FUNDS THROUGH THE FINANCIAL SYSTEM

Direct Finance

• Debt and Equity Markets

• Debt instruments (maturity)

• Equities (dividends)

• Primary and Secondary Markets• Investment Banks

underwrite securities in primary markets

• Brokers and dealers work in secondary markets

Exchanges and Over-the-Counter (OTC) Markets

Exchanges: NYSE, Chicago Board of Trade

OTC Markets: Foreign exchange, Federal funds.

Money and Capital MarketsMoney markets deal in short-

term debt instrumentsCapital markets deal in longer-

term debt and equity instruments.

•Indirect Finance involving Financial Intermediaries

•Banks, Insurance Companies, etc.

•Lower transaction costs (time and money spent in carrying out financial transactions).

•Economies of scale•Liquidity services

•Reduce the exposure of investors to risk•Risk Sharing (Asset Transformation)•Diversification

Deal with asymmetric information problems

(before the transaction) Adverse Selection: try to avoid selecting the risky borrower.

Gather information about potential borrower.

(after the transaction) Moral Hazard: ensure borrower will not engage in activities that will prevent him/her to repay the loan.

Sign a contract with restrictive covenants.

The crucial difference between direct and indirect finance is that an agent makes the allocation in direct finance not the principle – Principle Agent Problem

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 1 PRINCIPAL MONEY MARKET INSTRUMENTS

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 2 PRINCIPAL CAPITAL MARKET INSTRUMENTS

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 3 PRIMARY ASSETS AND LIABILITIES OF FINANCIAL INTERMEDIARIES

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 4 PRINCIPAL FINANCIAL INTERMEDIARIES AND VALUE OF THEIR ASSETS

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Exhibit 1: A Bank’s Balance Sheet

Here we show a bank’s balance sheet.

1.On the left-hand side are assets (what others owe to the bank): reserves (equal to bank deposits at the Fed plus vault cash), any loans it has made to others (e.g., a car loan the bank gave to someone), and any securities it owns. 2.On the right-hand side are liabilities (what the bank owes to others): checkable deposits (held for its customers), non-transaction deposits (e.g., small-denomination time deposits), and borrowings of the banks (i.e., any loans the banks may have taken out). 3.Also, it is customary to show bank capital (or net worth) -- which is the difference between assets and liabilities -- on the right-hand side of the balance sheet. In this balance sheet, assets are $110 million and liabilities are $100 million; so bank capital (or net worth) is $10 million.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

REGULATION OF THE FINANCIAL SYSTEM

To increase the information available to investors: Reduce adverse selection and moral hazard problems Reduce insider trading (SEC).

To ensure the soundness of financial intermediaries: Restrictions on entry (chartering process). Disclosure of information. Restrictions on Assets and Activities (control holding of

risky assets). Deposit Insurance (avoid bank runs). Limits on Competition (mostly in the past):

Branching Restrictions on Interest Rates

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TABLE 5 PRINCIPAL REGULATORY AGENCIES OF THE U.S. FINANCIAL SYSTEM

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

GOVERNMENT REGULATION -1 The naïve high school version of government

is that government, both politicians and bureaucrats, do what is in “the public good”.

Rarely does the question of what is “the public good” have a definitive answer. Predominantly, government spending involves

taking from one group (taxes) and providing a free or reduced price good or service to another group (spending) – redistribution of income.

Government regulation predominantly involves imposing costs on one group (the regulated) and providing a benefit to another group.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

GOVERNMENT REGULATION -2 A more realistic view of government is that

politicians and bureaucrats do what is their own self interest. In the case of politicians, the requirements that

they face re-election and avoid going to jail restrain the extent to which they can use their power to benefit themselves.

In the case of government bureaucrats, a more realistic view is that bureaucrats act and use their power to benefit themselves. Promotion to better jobs. Maximizing personal income and satisfaction. All while avoiding running afoul of the law and/or

getting fired.