Bilateral effects of non-tariff measures on international ...

World TrAde reporT 2012

94

This section reviews available sources of information on non-tariff measures (NTMs) and services measures, evaluating their relative strengths and weaknesses. It uses available information to establish a number of “stylized facts” regarding the incidence of NTMs and services measures in general. It looks in particular at technical barriers to trade, sanitary and phytosanitary measures and domestic regulation in services.

C. An inventory of non-tariff measures and services measures

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

95

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

Some key facts and findings

• Progress is being made on improving the quality and availability

of data on non-tariff measures and services measures, but much

remains to be done.

• Availabledatadonotshowanyclearincreasingtrendin

the overall use of non-tariff measures in the last decade.

• Technicalbarrierstotradeandsanitaryandphytosanitary

measures appear to have become prominent, according to official

WTO information. This is confirmed by survey data from both

developing and developed economies.

• Proceduralobstaclesareaparticularsourceofconcernfor

exporters from developing countries.

• Althoughthereissomeevidencethatmeasuresrestrictingtrade

in services have decreased over time in developed economies,

a serious limitation of available data on applied regimes in

the services area makes it difficult to distinguish between market

access, national treatment and domestic regulation.

Contents 1 SourcesofinformationonNTMsandservicesmeasures 96

2 StylizedfactsaboutNTMsrelatedtotradeingoods 105

3 Servicesmeasures 122

4 Conclusions 126

AppendixC.1:DatahandlingmethodologyintheUNCTAD’sTradeAnalysisInformationSystem(TRAINS) 131

AppendixC.2:Regressionresults 133

World TrAde reporT 2012

96

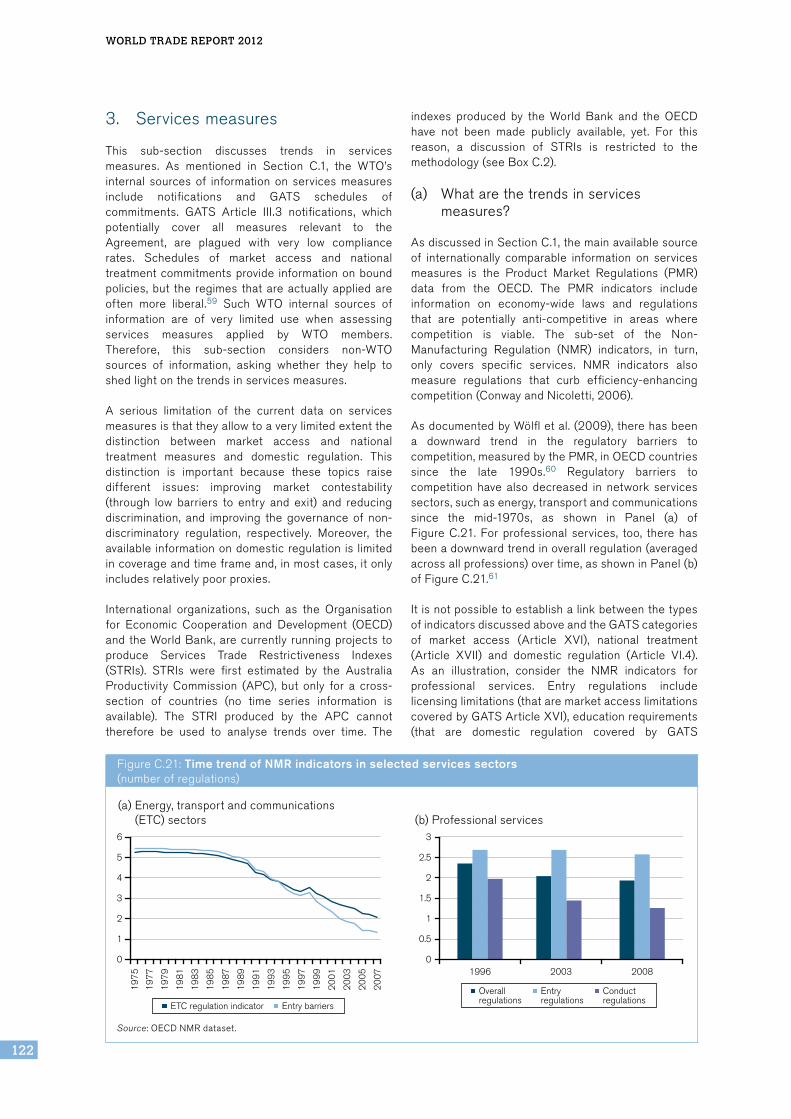

Thissectionsurveysavailablesourcesofinformationonnon-tariff measures (NTMs) and services measures,evaluates their relative strengths and weaknesses,summarizesthecontentoftheprincipaldatabases,andusesthisinformationtoestablishanumberof“stylizedfacts” about these types of measures. This last taskturnedout tobesurprisinglydifficultduetosignificantgapsindataandtonumerousshortcomingsinthedatathat do exist. Despite these limitations, the followingdiscussionattemptstocapturemanykeyfeaturesofthecurrentNTM landscapeand todocumentanumberoftrends in their use over time. As far as servicesmeasuresareconcerned,thedatalimitationsappeartobe even more severe than in the case of NTMs. Inparticular,thecurrentdataonservicesmeasuresdonotallow clear distinctions to be drawn between marketaccess, national treatment (i.e. the principle of givingothersthesametreatmentasone’sownnationals)anddomesticregulationissues.

The scarcity of data on non-tariff measures andservicesmeasuresstemsinlargepartfromthenatureofthesemeasures,whichfindtheirultimateexpressionin complex legal documents rather than in easilyquantifiable tariff schedules. The universe of NTMsencompassesallmeasuresthataffecttradeotherthantariffs,butsincemostregulatoryactionundertakenbygovernments can at least potentially influence trade,the set of possible NTMs is huge and its bordersindistinct. Similar considerations apply to servicesmeasures. On the goods side, this section examinesthe available evidence, with a particular attention totechnical barriers to trade (TBT) and sanitary andphytosanitary (SPS) measures (covering food safetyand animal and plant health). Traditional quantitativeandprice-basedmeasuresarealsodiscussed,butthefact that TBT/SPS measures are among the mostfrequently encountered NTMs and raise some of themostdifficult challenges from theWTO’sperspectivejustifiestheadditionalattentionpaidtothesekindsofmeasures. On the services side, the section takesstock of all measures affecting trade in services, tothe extent possible, before focusing on domesticregulation.

Statistics on non-tariff measures and servicesmeasuresare collectedbymanydifferent institutionsfor a variety of purposes. As a result, data are oftenpresented in formats that are not amenable toquantitativeanalysis,withsignificantgapsincoverageforparticularcountriesandtimeperiods.Whenreliableinformation isavailable, itmaystillprovidenoclueastohowstrictlymeasuresareapplied,orwhether theyareapplied inadiscriminatorymanner.Mostdatasetssimply present counts of the number of measures ineffectataparticularplaceandtime,butthesecountshave no natural economic interpretation and saynothing about the restrictiveness of individualmeasures.Forthesereasonsandothers,theavailabledata on NTMs and services measures can only becharacterizedassparseandincomplete.

The remainderof the section is organizedas follows.Section C.1 reviews the main sources of statisticalinformation on non-tariff measures and servicesmeasures, paying particular attention to areas wherethedataaredeficient.SectionC.2extractsanumberofstylized factsonNTMs ingoods fromtheprincipaldatabases. Section C.3 provides a similar account ofstylized facts about services measures. Section C.4containsconcludingremarks.

1. SourcesofinformationonNTMsandservicesmeasures

This sub-section presents the main sources ofinformation on non-tariff measures and assesses thecoverage and quality of the data they provide. BothinternalWTOsourcesandexternalnon-WTOsourcesare examined. The following overview highlights thediversityofthesourcesandofthemodesinwhichthedata are collected, distinguishing betweennotifications, monitoring, specific trade concerns,official data collection or business surveys. AdistinctionismadebetweeninformationonNTMsandinformationonimpedimentstotraderelatedtoNTMs.It also shows that despite this diversity, the data arepatchyatbest.Eachdatasourceshedslightonasmallpartoftheuniverse.Thelightitshedsdependsonthespecific purpose for which the data have beencollectedaswellasonhowtheyhavebeencollected,i.e. whether a measure is simply reported/notified orwhether there isacomplaint relating to themeasure.In any case, considerable caution is warranted ininterpretingtheavailableevidence.

(a) WTOinternalsourcesofinformation

One important source of information on WTOmembers’ trade policies are their schedules ofconcessions/commitments.Theseschedules,however,provide useful information on the policies thatmembershavecommitted toapply rather thanon thepolicies they actually apply. WTO agreements alsoinclude multiple provisions aimed at improving thetransparency of policy measures affecting trade.These provisions can be grouped into the followingfour categories: (a) publication requirements;(b) notification requirements; (c) the Trade PolicyReviewMechanismandthemonitoringreports;(d)thepossibility of raising specific trade concerns in theSPS and TBT committees and in the disputesettlementmechanism(DSM).

(i) Schedules of concessions/commitments

Theschedulesofconcessionsforgoodsmostlycontaininformation on members’ tariff commitments but theyalso cover their commitments regarding the use of anumber of non-tariff measures that affect trade inagricultural products as well as their so-called “non-tariffconcessions”.TheagriculturalNTMcommitments

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

97

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

includetariffquotas(wherebyquantitiesinsideaquotaarechargedlowerimportdutyratesthanthoseoutside)as well as commitments limiting subsidization inagriculture (total Aggregate Measurement of Support(AMS)commitmentfordomesticsupport,andbudgetaryoutlaysandquantityreductioncommitmentsforexportsubsidies). As for the non-tariff concessions (Part III),theywereeither addedaspart of theUruguayRoundnegotiations (but only by a few members) or after theUruguayRoundaspartofacountry’sWTOaccessionprocess.1 Both tariff and non-tariff commitments arealso available electronically in the Consolidated TariffSchedules database. Note that the commitments ascompiled in the database are not easily comparableacrossproductsandmembers.2

The schedules of commitments for services set outmarket access and national treatment commitments.Foreachserviceonwhichacommitmentismade,theschedule indicates, under each of the four modes ofsupply, any limitations on market access or nationaltreatment which the member is allowed to maintain.Limitations not recorded in the schedules in this wayareillegal.Theschedulesthuscombinea“positivelist”ofcoveredserviceswitha“negativelist”oflimitations.They guarantee a minimum standard of access;members are always free to grant more favourablelevels of market access and national treatment thanare specified in their schedules, on a most-favourednation(MFN)orequaltreatmentbasis,andmanydoso(seeSectionD.3).

(ii) Publication requirements and enquiry points

Article X.1 of the General Agreement on Tariffs andTrade (GATT) requires the prompt publication of alltrade regulations “in such a manner as to enablegovernments and traders to become acquainted withthem”. Several other WTO agreements contain morespecific publication requirements. In the TBTAgreement, for instance, Article 2.9.1 requires thepublicationofanoticewhenthegovernmentenvisagesintroducing a technical regulation which is not basedon internationalstandardsandmayhaveasignificanteffect on trade. Similarly, Article 2.11 requires thepublication of all technical regulations which havebeen adopted. Identical provisions also apply toconformity assessment procedures. Besides thosepublication requirements, the TBT Agreement alsoincludes provisions requiring the establishment ofenquiry points able to answer enquiries and providerelevant documents regarding technical regulations,standardsandconformityassessmentprocedures.

The purpose of publication requirements and enquirypoints is to contribute to transparency by informingothermembersingeneral,andproducersinexportingmembers in particular (see Article X as well as, forinstance, Articles 1, 2 and 3 of Annex B of the SPSAgreement).Publicationrequirementsandnotifications

(seebelow)tendtocomplementeachother.TheSPSand TBT agreements require the notification of draftregulationstotheWTOSecretariatandthepublicationof the adopted regulations. An important differencebetween notification and publication requirements isthat the former is centralized in the WTO Secretariatwhile the latter merely involves making informationpublicly available. Another difference is that whilenotificationsmustbetransmittedtotheWTOinoneofthe three official languages (English, French orSpanish),publicationsareinthenationallanguage.

(iii) Notifications

TheWTOframeworkcontainsmorethan200differentlegal notification requirements, the large majority ofwhich relate to non-tariff measures. NotificationrequirementsundertheWTOarehighlydiverse.3First,whileavastmajorityofrequirementsobligememberstoprovideinformationontheirownpolicies,someare“reverse”notifications,whichallowmemberstoidentifymeasures imposed by other members. Secondly,notificationsdifferfromeachotherwithregardtohowfrequently they are required. Most of those coveringlawsandregulationsareone-off requirements,withaseparate obligation to notify any changes thereafter.The notifications that provide information on themeasures themselves typically take two differentforms:theyareeitheradhocor(semi-)annual.Thirdly,abouthalfofthenotificationrequirementscoverNTMsthattypicallyapplytospecificproducts.Inthosecases,notification templates generally require members toindicate which products are covered. The other halfrelates to measures (e.g. laws and regulations) thataffect, or could potentially affect, all products(e.g.pre-shipmentinspectionorcustomsvaluation).

A comparison of the list of notifications with the2010versionoftheInternationalClassificationofNon-tariffMeasures suggests that notifications covermostof the categories (see Table C.2). The internationalclassification comprises 16 broad categories ofmeasures, of which only three do not seem to becoveredatallbyWTOnotificationrequirements.Thoseare finance measures, distribution restrictions andrestrictions on post-sales services. All the othercategoriesareat leastpartlycovered(i.e.anumberofsub-categoriesarecoveredwhileothersarenot).

Where notification requirements broadly match NTMcategories, however, they do not necessarily cover themeasuresthatcouldbeclassifiedtherein.Inthecaseofsanitary and phytosanitary measures, for example,Article 7 and Annex B of the SPS Agreement requiregovernmentstonotifynewSPSregulationswhicharenotbasedon internationalstandardsandhaveasignificanteffectonthetradeofothermembers,andtonotifythoseat an early stage, i.e. when amendments can still beintroduced.Measuresthatwereinplacebeforetheentryinto force of the SPS Agreement need not be notified,nor is there an obligation to notify the final measures

World TrAde reporT 2012

98

whentheyenterintoforce.Thismeansthatsomeofthemeasures in place were not notified and that some ofthose notified may have been amended before beingimplementedorevennotimplementedatall.

Notifications provide an incomplete and sometimesmisleading account of the incidence of non-tariffmeasures.4 First, WTO members do not necessarilycomplywith theirnotification requirements.While thelevel of compliance is not easy to measure, a simplecount of notifications for selected requirementssuggeststhatatleastinsomeareas,itisrelativelylow.AsdiscussedinmoredetailinSectionE.4,difficultiesfacedbymembersinmakingtheirnotificationsmaybepartofthereasonforthelowcompliance,butthemainexplanation is certainly that governments have noincentivetonotify,or,worse,mayhaveanincentivenotto notify. Secondly, notifications serve variouspurposes (Bacchetta et al., 2012). Some of themclearlydonotaimatprovidinganexhaustiveinventoryofallthemeasuresintheareatheycover. IntheSPSandTBTagreements, forexample,notificationsservetoallowothermemberstoparticipateintheformationof new regulations. This explains why there is norequirement tonotifymeasures inplacebefore1995(when the agreements came into effect) or finalmeasures. Thirdly, the “quality” of the informationprovided varies significantly among notifications.5Again, the quality criteria may be debatable, but inmany cases, notifications fail to provide preciseinformationonimportantdimensionsofthemeasures,such as product coverage or the time period duringwhichthemeasureremainsinplace.

Only a sub-set of the information collected throughnotifications is stored in searchable databases.6 TheWTO Secretariat has developed informationmanagement systems to facilitate access to all theinformation on SPS and TBT measures provided bymembers through the various existing transparency

mechanisms. The TBT Information ManagementSystemandtheSPSInformationManagementSystemare “one-stop” systems that allow users to accessinformation on TBT or SPS measures that membergovernments have notified to the WTO as specifictradeconcernsraisedintheSPSorTBTCommitteeorthroughmembergovernments’enquirypoints.ThetwoinformationmanagementsystemsarenotexactlyNTMdatabases.Theyaredocumentdatabaseswhichmakeit possible to search relevant documents by code,bynotifyingmember,bydate,byproductorbykeyword.

Access to all information from notifications will besubstantially improved with the new Integrated TradeIntelligence Portal (I-TIP) which is currently beingdeveloped by the WTO Secretariat to provide unifiedaccess to all information on trade and trade policymeasuresavailableattheWTO.

In services, the transparency-related notificationobligation is contained in Article III:3 of theGeneral Agreement on Trade in Services (GATS). Itrequires WTO members to notify measures that“significantlyaffecttrade”inservicescoveredbytheirspecific commitments. As of end-2011, just over400 notifications in total had been received.7FigureC.1showsthenumberofnotificationsreceivedperyearsince2000.

Considering the high number of sectors withcommitments by the 153 WTO members as of end-2011 (on average, developing countries havecommitments inmorethan50sectorsanddevelopedcountries nearly 110 sectors), it seems apparent thatthenumberofnotificationsreceivedinanygivenyearcannot account for the entire set of measures thatshouldhavebeennotifiedbymembers.OnedifficultyformembersregardingtheGATS is that thescopeofmeasurestobenotifiedisnotnecessarilyclear,astheGATS provides no further guidance on the

FigureC.1:GATS Article III:3 notifications received, 2000-2011 (numberofnotifications)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

50

25

30

35

40

45

20

15

10

5

0

Source:WTOSecretariat.

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

99

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

interpretationoftheterm“significantlyaffecting”tradein services. However, as already mentioned, lowcompliancewiththenotificationrequirementsismostlyan incentive issue. In committed sectors, memberswouldhavenoincentiveto“incriminate”themselvesbynotifying measures that somehow violated theircommitments. They might also have an interest inbeing non-transparent about measures that“significantly”liberalizedaccesstocommittedsectors,astheymightbefacedwithrequeststobindanysuch,notnecessarilyknown,liberalization.

(iv) Trade policy reviews and monitoring reports

Trade policy reviews

ThetradepoliciesandpracticesofallWTOmembersaresubjecttoperiodicreview:everytwoyearsforthefour countries with the largest share of world trade,every four years for the next 16 countries and everysix years for the others. The review is carried out bythe WTO’s Trade Policy Review Body (TPRB) on thebasisoftworeports:onebythememberunderreviewand another by the WTO Secretariat on its ownresponsibility.Inadditiontothetworeports,thereviewprocessincludesaquestionsandanswersmechanism.Twomonthsbeforethereviewmeeting,thereportsarecirculatedamongallmemberswhohaveonemonthtosubmitwrittenquestionstothememberunderreview.Thelattermustrespondinwritingbeforethemeeting.

The report by the WTO Secretariat reviews a broadrange of non-tariff measures and is typically in fiveparts:8 economic environment, trade and investmentregimes,tradepoliciesandpracticesbymeasure,tradepolicies by sector and Aid for Trade. The chapter ontrade policies and practices by measure distinguishesbetweenmeasuresdirectlyaffectingimportsandthosedirectlyaffectingexportsorthoseaffectingproductionandtrade.TableC.1liststhemeasuresexaminedundereach of the three headings in the 2011 Trade PolicyReview for Cambodia, which has been used forillustrativepurposes.Policiesaffectingtradeinservicesareexaminedsectorbysector.

Toprepare itsreport, theWTOSecretariatusesvarioussourcesof information.Thestartingpoint isusually thepreviousreport,whichcanbeupdatedusinginformationfrom notifications. The Secretariat also sends aquestionnaire to the government of the member underreview. This questionnaire, which addresses all areascovered in the report, followsageneral templatebut isoften customized. To complement the informationcollected through these institutional channels, otherpublicsourcesofinformationareusedtoidentifyissuesworthy of investigation. Despite considerable efforts,trade policy reviews (TPRs) do not and cannot provideexhaustive coverage of all non-tariff measures in allareas.Forexample,asalreadysuggestedinWorldTradeOrganization (WTO) (2006), informationonsubsidies in

TPRs is highly variable. Similarly, only a sub-set ofservices sectors is covered and, in the best possiblecase,selecteddomesticregulationisexamined.

WhiletheinformationontariffsandtradeusedforthereportsfeedsintotheWTO’sIntegratedDatabaseandis thus accessible electronically, information on non-tariff measures and on measures affecting trade inservices is not stored systematically in electronicformat and thus is neither easily comparable acrossWTO members, nor readily usable for quantitativeanalysis. Similarly, the questions asked and answersreceived as part of the review process are publishedasanannex to theminutesof theTPRBmeetingbutthey are not systematically coded and stored in adatabase. This may change with the new IntegratedTrade Intelligence Portal (I-TIP) which will provideaccess to all information from TPRs. Efforts will bemade to codify this information and thereby facilitatequantitativeanalysis.

Monitoring reports

The WTO publishes two types of monitoring reports.The first type is published twice a year by the WTOSecretariat for the Trade Policy Review Body.9 Thereportscovertradeandtrade-relateddevelopmentsingoods and services of all WTO members as well asobservers. They monitor changes in both tariffs and

TableC.1:Measures covered by trade policy reviews

Measures directly affecting imports

(i) Customsprocedures

(ii) Tariffsandothertaxesandchargesaffectingimports

(iii) Customsvaluation

(iv) Pre-shipmentinspection

(v) Rulesoforigin

(vi) Importprohibitions,quotas,andlicensing

(vii) Anti-dumping,countervailingduties,safeguardregimes

(viii)Governmentprocurement

(ix) Statetradingenterprises

(x) Othermeasures

Measures directly affecting exports

(i) Procedures

(ii) Exporttaxes

(iii) Exportrestrictions

(iv) Exportsubsidies

(v) Exportpromotion

(vi) Specialeconomiczones

Measures affecting production and trade

(i) Regulatoryframework

(ii) Technicalbarrierstotrade

(iii) Sanitaryandphytosanitarymeasures

(iv) Trade-relatedintellectualpropertyrights

Source:WorldTradeOrganization(WTO)(2011a)

World TrAde reporT 2012

100

non-tariff measures as well as in a broad range ofmeasuresaffectingtradeinservices.ThesecondtypeofreportispublishedbytheWTOSecretariattogetherwith the secretariats of the OECD and UNCTADfollowing a request by the G20 to monitor trade andinvestment measures.10 These reports, which onlycoverG20countries,arealsoissuedtwiceayear.

Thesourcesof informationused for the two typesofreportsaresimilar.Bothreportsmostlyuseinformationcollected through a request for information sent toWTOmembers, informal reversenotificationsand thepress. This information is then submitted to therespective members for verification. The data aremadeavailableinpublicreportsandstoredinspread-sheets, but not in a database. Like all the otherinformationontradeandtradepolicycollectedbytheWTO, however, it will be made available through thenewIntegratedTradeIntelligencePortal(I-TIP)portal.

WTOmembershaverecognizedtheusefulnessofthetrade monitoring exercise. There is broad consensusfor its continuation and strengthening as well as forthe related briefings by the Director-General ininternationalforasuchastheG20.11

(v) Specific trade concerns and disputes

Specific trade concerns

WTOmembershaveusedboth theTBTand theSPScommittees as fora to discuss issues related tospecificmeasurestakenbyothermembers.Thesearereferred to as “specific trade concerns” and relatevariouslytoproposedmeasuresnotifiedtotheTBTorSPS committees in accordance with the notificationrequirements in the relevant agreement, or tomeasures currently in force. Committee meetings, orinformal discussions between members held on themargins of such meetings, afford members theopportunity to review trade concerns in a bilateral ormultilateralsettingandtoseekfurtherclarification.

Specific trade concerns raised by members are asource of potentially interesting information on theeffectsofnon-tariffmeasures.Specifictradeconcernspointoutparticularobstaclesfacedbyexportersfromthe country raising the concern in a given exportmarket.TheinformationtheyprovideontheeffectsofNTMs is thus similar to that provided by businesssurveys. The main difference is that specific tradeconcerns are channelled through governments.Exporters facing an obstacle may complain to thegovernment, which may or may not raise the issue attheWTO.Thismeansthatspecifictradeconcernsmayprovide a distorted picture of the trade-restrictive ortrade-distortiveeffectsofTBTandSPSmeasures.Anumberofconcernsmayneverbe raised.12Moreover,therearenoreasonstobelievethattheonesthatgetraised are statistically representative of all theTBT/SPSrelatedtradedistortionsfacedbymembers.

As already mentioned, the TBT InformationManagement System and the SPS InformationManagementSystemallowuserstotrack,andperformsearcheson,specifictradeconcernsraisedintheTBTor SPS committees but they are not suitable forquantitative analysis. The WTO Secretariat has thuscoded all the relevant information on specific tradeconcerns and created two databases: one on TBTmeasures and one on SPS measures. The TBTSpecific Trade Concerns (STC) Database providesinformation on the 317 concerns raised in the TBTCommittee between January 1995 and June 2011.13The SPS STC Database provides information on the312 concerns raised between January 1995 andDecember 2010. Each of these corresponds to aconcernraisedbyoneormoremembersinrelationtoameasuretakenbyoneoftheirtradingpartners.Sincesome of these measures might have been notified tothe WTO, the concern might be related to one orseveral notifications of the member taking themeasure.Themaindifficultywiththecodificationwasto attribute product codes from the HarmonizedSystem(thesystemusedbyparticipatingcountriestoclassifytradedgoodsonacommonbasis).14

Disputes

Disputes initiatedbymembersunder theWTOdisputemechanismareanothersourceofpotentiallyinterestinginformationon theeffectsofnon-tariffmeasures.TheWTOSecretariatmaintainsadatabaseon“requestsforconsultations”, the first step in formally initiating adispute in the WTO. As of 31 December 2011, thedatabase had information on 427 such requests.15These data do not indicate the type of non-tariffmeasure at issue in the disputes, but the WTOagreement(s)andprovision(s)citedineachdisputearelisted. Using the latter, it is possible to obtain anestimateofthenumberofcasesinvolvingeachtypeofnon-tariff measure. When doing this, however, it isimportanttobearinmindthatforeconomicandpoliticalreasons,anumberofNTM-relatedtradedistortionsmaygounchallenged.Aswithspecifictradeconcerns,thereis no reason to believe that the measures challengedwerestatistically representativeofall theNTM-relatedtradedistortionsfacedbymembers.16

Another problem with this approach is that for anydispute, complainants tend to cite a large number ofprovisionswhichhaveallegedlybeenbreached,whilein fact some of the provisions are duplicates orintimately related to other provisions. The GATT, forexample,iscitedinmostdisputesbecauseitincludesthebasicrulesthatapplytotradeingoods.Moreover,even when a complainant brings a dispute under amorespecificagreement,suchastheTBTAgreement,it may also include claims under the GATT, such asunder Article III:4. This means that a simple count ofthenumberofprovisionscitedinthecaseswouldleadtoanover-estimationofthenumberofNTMsthathavebeenchallenged.

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

101

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

Santana and Jackson (2012) proposea methodologytoobtainamorepreciseviewofthetypesofmeasuresthat are the subject of WTO dispute settlement byadjusting for the citation to the GATT in disputeswhere that agreement may have played a secondaryrole. Using this methodology, they have compiled adataset on WTO disputes based largely on thedatabaseof requests for consultationsmaintainedbythe WTO legal division.17 This dataset is not publiclyavailable,butit isconsistentwithadatabaseonWTOdisputes accessible on the World Bank’s website(seebelow). Intheirdataset,JacksonandSantanadonot“doublecount”requestsforconsultationsthatreferto the GATT when the reference is likely to be ofsecondary importance to the main claim of violation(i.e.aspecializedagreementoranotherGATTarticle).Theyhavealsorestrictedcoveragetodisputesrelatedtotrade ingoods.Thiscoversa totalof393disputesout of the 427 filed under the Dispute SettlementUnderstanding(DSU)asof31December2011.

(b) Non-WTOsourcesofinformation

(i) Data collected from official sources

TRAINS and Market Access Map

The most complete collection of publicly availableinformation on non-tariff measures is the TradeAnalysisandInformationSystem(TRAINS)developedby the United Nations Conference on Trade andDevelopment (UNCTAD). UNCTAD started collectingNTM information in 1994 and simultaneouslydeveloped the TRAINS database.18 TRAINS providesinformationontrade,tariffsandNTMsbyHarmonizedSystem(HS)tariffline.NTMswereclassifiedaccordingto a customized Coding System of Trade ControlMeasures, which distinguished six core categories ofNTMs.Thedatabaseincludesbetweenoneandsevenyears of NTM information for 86 countries over theperiod 1992 to 2010. For some countries/years, inparticular after 2001, data were collected only for asub-setofNTMcategories.Varioussourceswereusedto provide data, including, where available, WTOsources such as notifications.19 Overall, the coverageis patchy, resulting in blank cells which are difficultto interpret.Theycansignifymissingdataor indicatethat a particular NTM is not applied to a particulartariffline.

In the early 2000s, it became clear that the TRAINSdatabase required substantial improvement and thatthe Coding System needed an update to reflect newpractices.In2005,theSecretaryGeneralofUNCTADlaunchedaprojectaimedat revamping thedefinition,classification, collection and quantification of non-tariff measures.20 Under the guidance of a Group ofEminent Persons, a multi-agency team composed ofexperts from all international agencies active in theNTM area started working on the project. In 2009,the multi-agency team proposed an updated and

modified version of the old Coding System including16 categories (see Table C.2) which brought theclassification closer to the regulatory framework.21A pilot project on the collection and quantification ofNTMs was carried out by UNCTAD and theInternationalTradeCentre(ITC),withaviewtotestingthe new classification. With the support of two UNregional commissions, UNCTAD and ITC collectedNTM information in seven developing countries.22Basedon the lessons learned in thepilotproject, theupdatedNTMclassificationwasfinalizedandadopted.

Theupdatedclassificationalsointroducedtheconceptof“proceduralobstacles”,definedas“issuesrelatedtothe process of application of an NTM, rather than tothe measure itself” (United Nations Conference onTrade and Development (UNCTAD), 2010: xvii). Aninitiallistofproceduralobstacleswasestablishedandtested in a series of interviews with exportingcompaniescarriedoutaspartofthepilotproject(seethe discussion of business surveys below).23 On thebasisof lessonslearnedinthepilotproject,theinitiallistofproceduralobstacleswasrevisedandexpanded.

Table C.3 presents the ten broad categories ofproceduralobstacles in the listcurrentlyusedby ITC.The distinction between a non-tariff measure and aprocedural obstacle can sometimes be very subtle,and is best illustrated with an example. To import aproduct, it may be necessary to have a specificcertification (an NTM); however, the certification

TableC.2:International classification of non-tariff measuresA Sanitaryandphytosanitarymeasures

B Technicalbarrierstotrade

C Pre-shipmentinspectionandotherformalities

D Pricecontrolmeasures

E Licences,quotas,prohibitionsandotherquantity controlmeasures

F Charges,taxesandotherpara-tariffmeasures

G Financemeasures

H Anti-competitivemeasures

I Trade-relatedinvestmentmeasures

J Distributionrestrictions*

K Restrictionsonpost-salesservices*

L Subsidies(excludingexportsubsidies)*

M Governmentprocurementrestrictions*

N Intellectualproperty*

O Rulesoforigin*

P Exportrelatedmeasures*

Source: United Nations Conference on Trade and Development(UNCTAD)(2010).

Note: *indicatesthatnoofficial information iscollectedbyUNCTADfor this category which is only used to collect information from theprivatesectorthroughsurveysandwebportals.

World TrAde reporT 2012

102

authority or testing laboratory can be excessivelycostly,slowinresponseorbelocatedinaremotearea(proceduralobstaclesrelatedtotheNTM).Informationonproceduralobstaclescanonlybecollectedthroughsurveysorothermechanismsthatrecordcomplaints.

Following the pilot project phase, ITC, UNCTAD andtheWorldBankstartedtocollectofficialdataonnon-tariff measures.24 Their strategy consisted of hiringlocalconsultants(universities,thinktanksorconsultingfirms) and giving them assistance and guidelines todraw up NTM inventories in collaboration with theministriesandagenciesconcerned.Relyingonoutsideconsultantsisintendedtoaddresstwooftheproblemsthat plague self-notification: (i) the wide variety ofbodies involved in initiating NTMs; and (ii) theincentivesforauthoritiesnottonotifyinordertoavoidexposure. The data collected by consultants areformatted according to international classification byproduct(ateitherthetariff-lineorHS6level),togetherwith information on legal sources and enforcingagency, in order to ensure verifiability of theinformation. The inventories are then approved bynational authorities during validation workshops.Finally, the data are verified and added to both theTRAINSandMarketAccessMap,adatabaseoftariffsandNTMsdevelopedbyITC.

To consolidate cooperation and expand the recentcollection efforts, an ambitious multi-agencypartnership, Transparency in Trade (TNT), waslaunched in 2011 by the African Development Bank,ITC, UNCTAD and the World Bank. Using donorfinancing,theTNTinitiativeaimsatgivinga“bigpush”to data collection, creating a one-stop globalinformation source. It provides a framework throughwhich the four agencies coordinate their datacollection efforts to fill key data gaps and worktogether to strengthen the capacity of institutions indevelopingcountriestocollectandreport informationon trade policies. TNT has four major components:(i)tools(theMarketAccessMapandtheWorldBank’sWorldIntegratedTradeSolutionportalsprovideaccessto the data); (ii) tariff data collection; (iii) non-tariffmeasures data collection; and (iv) policies affecting

tradeinservices.Oncethefirstwaveofdatacollectioniscompleted,thechallengefacingtheTNTpartnershipwill be to move to a more sustainable structure thanthatprovidedbydonorfinancingalone.

World Bank Temporary Trade Barriers Database (TTBD)

The World Bank’s Trade Barriers Database (TTBD)website hosts detailed and freely available data onmore than 30 different national governments’ use ofanti-dumping and countervailing duties since 1980and of global safeguards since 1995 as well as onChina’suseofitsspecifictransitionalsafeguard.25TheGlobal Anti-Dumping Database, developed by ChadBown,withfundingfromtheWorldBank,usesoriginalnational government documentation to organizeinformation on affected countries, product category(at theHS8 level), typeofmeasure,dateof initiation,final imposition of duties, and revocation dates, andeveninformationonthecompaniesinvolved.

TheTTBD website also hosts a public database withinformation on WTO disputes developed by HenrikHorn and Petros Mavroidis.26 It contains informationonallstagesofWTOdisputesettlementproceedings(e.g.panelreports,appeals,compliancepanelreports)forallWTOdisputesupto11August2011.

OECD product market regulation

The OECD Economics Department has developed adatabase consisting of indicators of product marketregulation for member states. The aim is to turnqualitativedataonlawsandregulationsthatmayaffectcompetition into quantitative indicators. The indicatorsmostly measure regulations that are potentially anti-competitive in areas where competition is viable. Withthe exception of the foreign direct investment (FDI)restrictiveness index, they do not distinguish betweendiscriminatory and non-discriminatory measures (seeSectionC.3). Themain sourceof informationused forthis database is official government responses to theOECDRegulatoryIndicatorsQuestionnaire,withonlyasmallfractionofinformationbeingdrawnfromexternaldatasets, thereby guaranteeing a high level ofcomparability across countries. The indicators aresubjecttopeerreviewbythenationaladministrationsofOECDmembercountries.

The database proposes several different indicatorswhich have been calculated for various years. First,there is the economy-wide product market regulation(PMR) indicator, which covers domestic regulationsboth in the manufacturing and services sectors. Thishasbeenestimatedfor1998and2003for30OECDcountries (Conway et al., 2005). The economy-widePMR indicator was subsequently replaced with theintegrated PMR indicator, which has been estimatedmostly for 2008 for 34 OECD countries (the fouradditional countries are Chile, Estonia, Israel and

TableC.3:ITC list of procedural obstaclesA Administrativeburdens

B Information/transparencyissues

C Inconsistentordiscriminatorybehaviourofofficials

D Timeconstraints

E Payment

F Infrastructuralchallenges

G Security

H Legalconstraints

I Other

Source:InternationalTradeCentre(ITC)(2011).

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

103

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

Slovenia)aswellasforBrazil,China, India, Indonesia,Russia and South Africa (Wölfl et al., 2009). Theintegrated PMR indicator covers general regulatoryissues in fields such as public control and pricecontrols, legal and administrative barriers to marketentry, and barriers to trade and investment. It alsocovers some industry-specific regulatory policies,notably in air and rail passenger transport, rail androadfreight,telecommunicationsandretaildistribution.

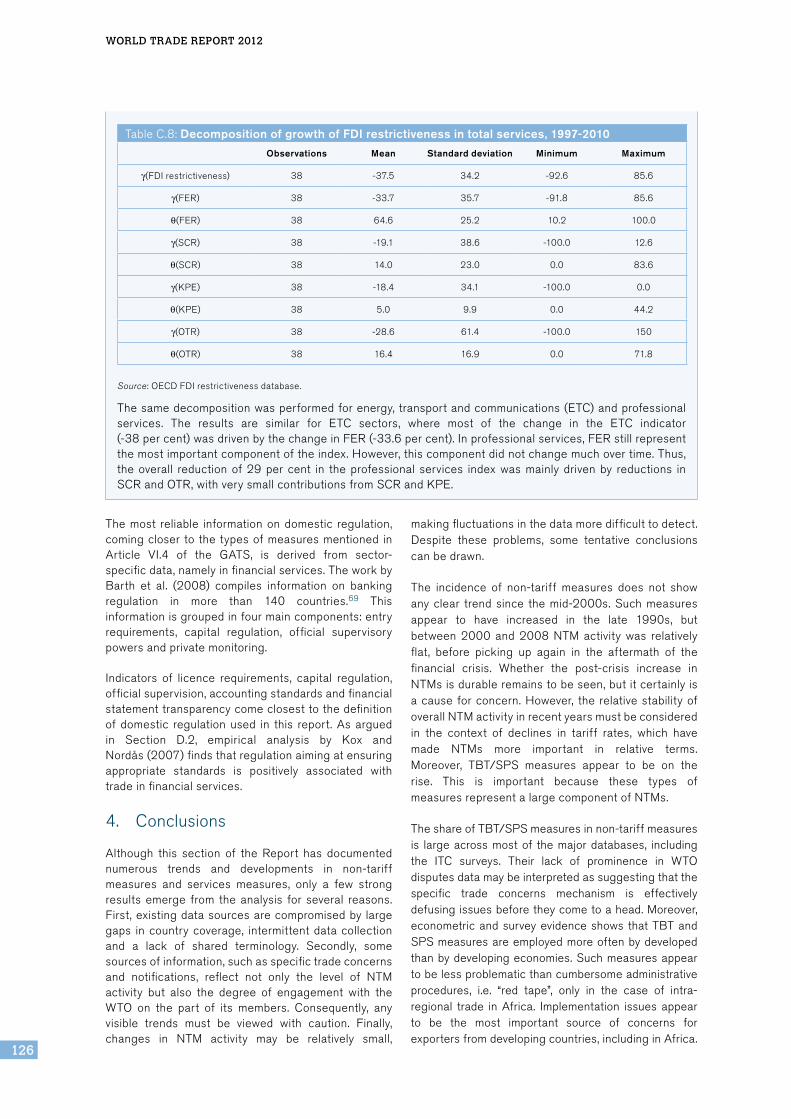

Secondly,inparallelwiththePMRindicator,theOECDhas developed a set of indicators covering regulationin specific sectors or specific aspects of regulation.Thesectoralindicatorscoverthreenon-manufacturingsectors, and in particular network industries such asenergy(electricityandgas),transport(air,railandroadtransport), and communication (post andtelecommunications) as well as retail trade andprofessional services (Conway and Nicoletti, 2006).The energy, transport and communications (ETC)regulationindicatorcoversmeasuresaffectingmarketentry and public ownership plus vertical integrationandmarketstructure,butonlyinasubsetofthesevenindustries.The retaildistribution indicatorcovers fourentry regulations (registration, licences and permits,largeoutletrestrictions,andprotectionofincumbents)andtwoconductregulations(shopopeninghoursandprice controls). Finally, the professional servicesindicator covers three market entry and four conductregulations.TheFDI (regulatory) restrictiveness indexcovers four types of measures: (i) foreign equityrestrictions; (ii) screening and prior approvalrequirements; (iii) rules for key personnel; and(iv) other restrictions on the operation of foreignenterprises (Kalinovaetal.,2010).The latest revisionof the index covers these four typesofmeasures forall primary sectors (agriculture, forestry, fishing andmining),investmentsinrealestate,fivemanufacturingsub-sectors and eight services sectors. The FDIrestrictiveness indicator is available for 1997, 2003,2006and2010for48countries.

Comparedwithotherindicatorsofservicesmeasures,thefamilyofOECDregulationindicatorshasanumberof advantages. First, the information summarized bythe indicators is “objective”, in the sense that it isbased on rules, regulations and market conditionsrather thanonperceptionscaptured throughsurveys.Secondly, these indicators provide the broadestcoverage of sectors and areas, and the longest timeseries currently available to compare product marketregulation across countries. As discussed in moredetailinSectionC.3,thePMRindicatorscoverawidearrayofmeasures relevant to theservicessectorbutthey do not match the GATS categories of measures(marketaccessandnationaltreatmentlimitations;anddomesticregulation).Moreover,theyareonlyavailableforarelativelysmallgroupofmostlyrichcountries.27

(ii) Business concerns

Most of the sources discussed so far are sources ofofficial information, whether notified to the WTO orcollected from governmental sources. Officialinformationhasanumberofdistinctadvantages.First,it isgenerallyreliable. Itcanbelinkedbacktoa legaltextand,at least for theWTOsources, it isapprovedbygovernments.Secondly,inmostcasesitiscollectedin a systematic way.28 However, it also has a fewdisadvantages,foremostamongthemthatthedataaregenerated/reported by the countries imposing thenon-tariff measures. Some of these countries maywant toavoidattractingattention to theiradoptionofnewNTMs,ortheymaysimplynotdeemthemworthyofreporting, inwhichcasethe incidenceofNTMsforindividualcountriesand inaggregatemeasurescouldbeunderstated.Furthermore,whileevidencesuggeststhat how NTMs are applied or administered canbecome a “procedural barrier to trade”, governmentshave absolutely no incentive to document obstaclesrelating to the specific way in which measures areapplied.

Questions relating to procedural obstacles may bebetteraddressedusingbusinesssurveysorinformationonfirms’ownperceptionsof thedifficulties they facedoing business in various markets. Data on exporterperceptions provide a valuable complement to datafromofficialsourcesbecausetheyhelpidentifythosemeasuresthatareperceivedasimpedimentstotrade.Thesesortsofdata,however,reflectfirms’ judgmentsandmaybesubjecttovariousbiases.Businessesmayexaggerateproceduralobstacles–or,onthecontrary,minimize them – depending on the circumstances.They may also be unable to identify the specificpoliciesofconcern,ormaymisidentifythem.Moreover,surveys, because of problems related to sample sizeand self-selection of respondents, do not alwaysguaranteerigorousandsignificantresults.29Similarly,with websites where exporters can file complaints,self-selectionleadstoabiasedstatisticalsample.

Two sources of business data are presented in thissub-section and used in the next sub-section sincetheydealdirectlywithnon-tariffmeasures.Thefirstisa set of 11 business surveys conducted by ITC indeveloping countries. The second is the CoRe NTMs(compilationofreportedNTMs)DatabasecompiledbyMartinezetal.(2009),whichincorporatesinformationfrom the United States Trade Representative’sNational Trade Estimate Reports on Foreign TradeBarriers and the European Union’s Market Access –Trade Barriers database. These two sources give anoverview of barriers faced by firms from two of thelargestdevelopedeconomies.Otherbusinesssurveysfocusingon“easeofdoingbusiness”indicatorsarenotdiscussedhere(eventhoughtheymaycontainrelevantinformation)sincetheyrequiremoreattentiontomakesurethecorrectmeasuresareidentified.30

World TrAde reporT 2012

104

ITC business surveys

Since the end of the pilot project in 2009 (see sub-section 1(b)(i) above), the ITC has carried out large-scalecompanysurveysonnon-tariffmeasuresinmorethanadozendevelopingandleast-developedcountriesonallcontinents.31Thesurveyscoverat least90percent of the total export value of each participatingcountry(excludingmineralsandarms).32Theeconomyis divided into 13 sectors, and all sectors accountingformorethan2percentoftotalexportsareincludedinthesurvey.Bothexportingandimportingcompaniesare covered. The survey methodology involves atwo-stepapproach.

Inthefirststep,companiesthatexperienceburdensomenon-tariff measures are identified through phoneconversationswithallthecompaniesinthesample.Thesecond step then consists of face-to-face interviewswiththecompaniesthatreporteddifficultieswithNTMsinthephoneconversations.Atrainedinterviewerhelpsrespondentsidentifytherelevantregulation,thenatureoftheproblem,theaffectedproducts(six-digit leveloftheHarmonizedSystem),thepartnercountryexportingor importing the product and the country applying theregulation (partner, transit or home country). The ITCdoesnotimplementthesurvey,butguidesandsupportsalocalsurveycompanyandexpertsindoingthis.Uponfinalizing the survey, its results are presented anddiscussed at a dissemination workshop, which bringstogetherallnationalstakeholdersandfostersadialogueonNTMissues.

Compilation of NTMs reported by US and EU exporters

Over the lastdecade, theOfficeofEconomicsof theUnitedStatesInternationalTradeCommission(USITC)has been engaged in compiling a unified databaseusing the EU’s Market Access – Trade BarriersDatabaseand theNationalTradeEstimateReportonForeign Trade Barriers issued by the United StatesTrade Representative (USTR), as well as the WTO’strade policy reviews. The first version of the USITCNTMdatabasedatesbackto2002andisdescribedinManifold (2002) and Donnelly and Manifold (2005).ItwaslaterupdatedbyMartinezetal.(2009).

The EU’s Market Access – Trade Barriers Databaseprovidesasnapshotofnon-tariffbarriersfacedoutsideoftheEUbyexportersfromEUmembers.ItisbasedoncomplaintsregisteredbyEUexportersandprocessedbytheEuropeanCommission.Thedatabasehas32sectorsand seven main categories of measures: tariffs andduties, trade defence instruments, non-tariff barriers,investment-relatedbarriers, intellectual property rights-related barriers, other (export-related) measures andservices-specificmeasures.Eachofthosecategoriesisfurther divided into a number of sub-categories. Non-tariff barriers, for instance, are sub-divided into:registration, documentation and customs; quantitative

restrictions and related measures; competition issues;standards, sanitary and other technical measures;government procurement; subsidies; other non-tariffmeasures; and sanitary and phytosanitary measures.TheUSITCdatabasedoesnot includetariffsandtradedefence instruments and EU data are reclassifiedaccordingtotheUSITCclassification.

TheNationalTradeEstimate(NTE)ReportonForeignTrade Barriers is issued annually by the USTR. ItsprimaryfocusisonforeignbarrierstoUSexports.TheNTE isnotasimplebusinesssurvey. It isbaseduponinformationcompiledwithintheUSTR,theDepartmentofCommerceand theDepartmentofAgricultureandother US government agencies. It is supplementedwith information provided in response to a noticepublished in the Federal Register (the official journalof the US Government), and with information frommembers of the private sector trade advisorycommittees and US embassies abroad. While eachcountry is reviewed in a different way, the discussiontypicallyfocusesonindividualmeasuresbysector.

Global Trade Alert

In 2009, the Centre for Economic Policy Research(CEPR) teamed up with independent researchinstitutes from around the world to create the GlobalTrade Alert (GTA) initiative.33 Their objective was toincrease the information available on state measuresthatmayaffecttradingpartners’commercialinterests,broadly defined as imports, exports, foreigninvestments (including intellectual property), andforeignemployees.CEPRbelievedthatacombinationof peer pressure plus up-to-date, comprehensiveinformation would help avoid the historic mistakes ofprotectionismofpreviouseras. Inaddition to trackinggovernmentmeasurestakenduringthecurrentglobaleconomicdownturn,theGTAprovidesresearchersandgovernmentofficialswithinformationonnewpatternsof state intervention that are problematic from theperspectiveofmaintainingopenborders.

Regional nodes, a network of independent researchinstitutesandtradeexpertsfromallovertheglobe,areresponsible formonitoringstatemeasures introducedintheirownregion(andelsewhere).TheGTAinitiativealsoencourages thirdparties to submitmeasures forscrutiny, and welcomes dialogue with implementingjurisdictions concerning the measures they haveintroduced. The Evaluation Group, consisting of theleaders of the regional nodes and chaired by therepresentative of the network hub (CEPR), isresponsibleforassessingthisinformationanddecidingwhether to publish it on the GTA website. The GTAdoes not confine itself to the measures that arecoveredbytheexistingbodyofWTOagreements.NordoestheinitiativepronounceontheWTOlegalityofameasureorwhetherameasureis“protectionist”.

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

105

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

2. StylizedfactsaboutNTMsrelatedtotradeingoods

Currently available databases on non-tariff measures,despitetheshortcomingsdiscussedabove,canbeusedto address important questions about trade in goods,includingwhether such measures have increased overtime, how important SPS and TBT measures arecompared with other types of NTMs, and how firmsperceive the obstacles they face in internationalmarkets.Thissub-sectionposesseveralsuchquestionsabout NTMs and provides answers in the form ofdescriptive statistics inorder toestablish anumberofstylized facts about NTMs. Only with a reliable setof facts can researchers hope to make progress inaddressingmorefundamentalquestionsaboutNTMs.

(a) Isthereevidenceofanincreasingmedium-tolong-termtrendinNTMs?

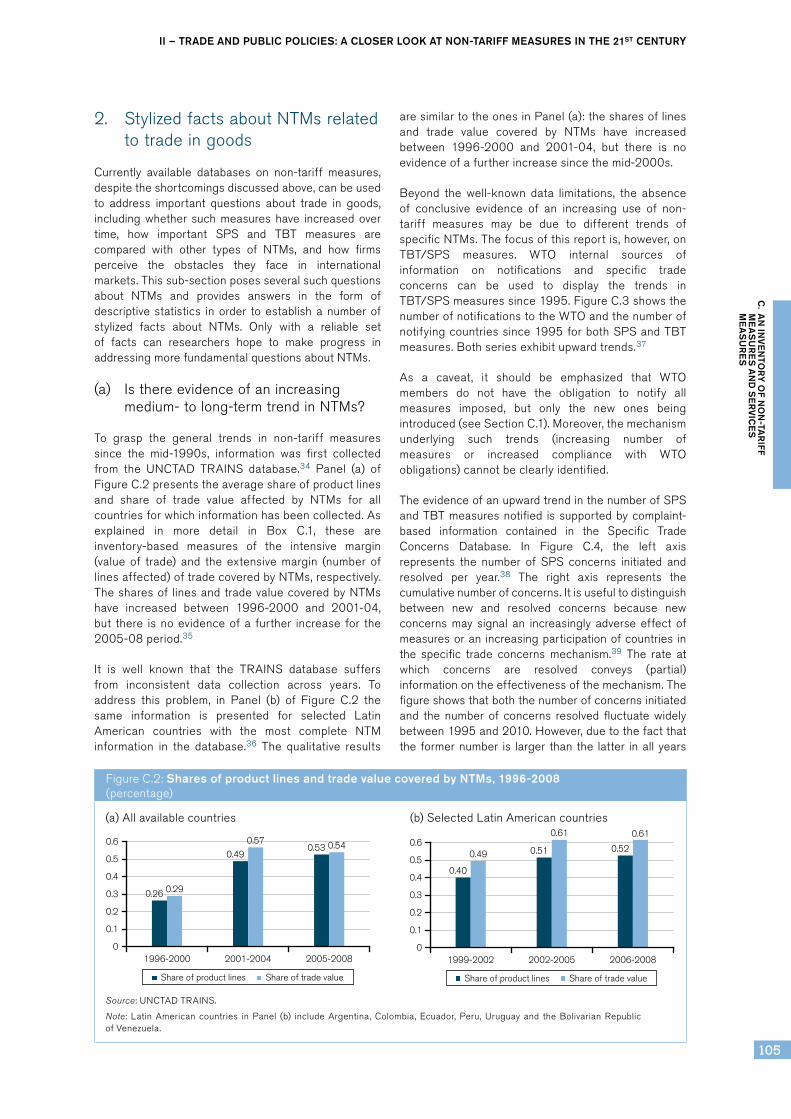

To grasp the general trends in non-tariff measuressince the mid-1990s, information was first collectedfrom the UNCTAD TRAINS database.34 Panel (a) ofFigureC.2presentstheaverageshareofproductlinesand share of trade value affected by NTMs for allcountriesforwhichinformationhasbeencollected.Asexplained in more detail in Box C.1, these areinventory-based measures of the intensive margin(value of trade) and the extensive margin (number oflinesaffected)oftradecoveredbyNTMs,respectively.Thesharesof linesandtradevaluecoveredbyNTMshave increased between 1996-2000 and 2001-04,but there isnoevidenceofa further increase for the2005-08period.35

It is well known that the TRAINS database suffersfrom inconsistent data collection across years. Toaddress this problem, in Panel (b) of Figure C.2 thesame information is presented for selected LatinAmerican countries with the most complete NTMinformation in the database.36 The qualitative results

aresimilartotheonesinPanel(a):thesharesoflinesand trade value covered by NTMs have increasedbetween 1996-2000 and 2001-04, but there is noevidenceofafurtherincreasesincethemid-2000s.

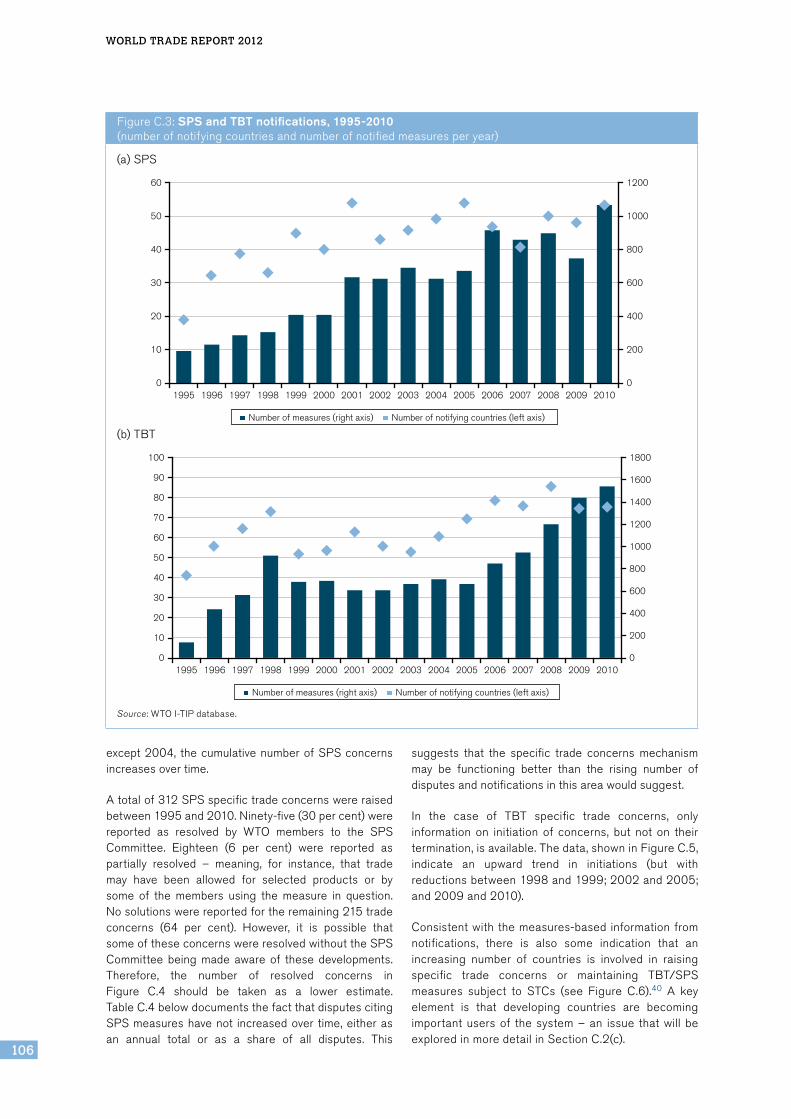

Beyond the well-known data limitations, the absenceof conclusive evidence of an increasing use of non-tariff measures may be due to different trends ofspecificNTMs.Thefocusofthisreportis,however,onTBT/SPS measures. WTO internal sources ofinformation on notifications and specific tradeconcerns can be used to display the trends inTBT/SPSmeasuressince1995.FigureC.3showsthenumberofnotificationstotheWTOandthenumberofnotifyingcountriessince1995forbothSPSandTBTmeasures.Bothseriesexhibitupwardtrends.37

As a caveat, it should be emphasized that WTOmembers do not have the obligation to notify allmeasures imposed, but only the new ones beingintroduced(seeSectionC.1).Moreover,themechanismunderlying such trends (increasing number ofmeasures or increased compliance with WTOobligations)cannotbeclearlyidentified.

TheevidenceofanupwardtrendinthenumberofSPSandTBTmeasuresnotified issupportedbycomplaint-based information contained in the Specific TradeConcerns Database. In Figure C.4, the left axisrepresents the number of SPS concerns initiated andresolved per year.38 The right axis represents thecumulativenumberofconcerns.Itisusefultodistinguishbetween new and resolved concerns because newconcerns may signal an increasingly adverse effect ofmeasuresoran increasingparticipationofcountries inthe specific trade concerns mechanism.39 The rate atwhich concerns are resolved conveys (partial)informationontheeffectivenessofthemechanism.Thefigureshowsthatboththenumberofconcernsinitiatedand the number of concerns resolved fluctuate widelybetween1995and2010.However,duetothefactthatthe formernumber is larger than the latter inall years

FigureC.2:Shares of product lines and trade value covered by NTMs, 1996-2008 (percentage)

1999-2002

0.40

0.49 0.51

0.61

0.52

0.61

2002-2005 2006-2008

0.5

0.6

0.4

0.3

0.2

0.1

0

Share of product lines Share of trade value

1996-2000 2001-2004 2005-2008

0.5

0.6

0.4

0.3

0.2

0.1

0

Share of product lines Share of trade value

0.26 0.29

0.49

0.570.53 0.54

Source:UNCTADTRAINS.

Note: Latin American countries in Panel (b) include Argentina, Colombia, Ecuador, Peru, Uruguay and the Bolivarian RepublicofVenezuela.

(a)Allavailablecountries (b)SelectedLatinAmericancountries

World TrAde reporT 2012

106

FigureC.3:SPS and TBT notifications, 1995-2010 (numberofnotifyingcountriesandnumberofnotifiedmeasuresperyear)

1995 1996 1997 19991998 2000 20022001 2003 2004 20062005 2007 20092008 2010

60

30

40

50

20

10

1200

600

800

1000

400

200

00

Number of notifying countries (left axis)Number of measures (right axis)

1995 1996 1997 19991998 2000 20022001 2003 2004 20062005 2007 20092008 2010

100 1800

601200

70

1400

40800

30600

501000

90

80

1600

20 400

10 200

00

Number of notifying countries (left axis)Number of measures (right axis)

Source:WTOI-TIPdatabase.

(a)SPS

(b)TBT

except2004, thecumulativenumberofSPSconcernsincreasesovertime.

Atotalof312SPSspecifictradeconcernswereraisedbetween1995and2010.Ninety-five(30percent)werereported as resolved by WTO members to the SPSCommittee. Eighteen (6 per cent) were reported aspartially resolved – meaning, for instance, that trademay have been allowed for selected products or bysome of the members using the measure in question.Nosolutionswerereportedfortheremaining215tradeconcerns (64 per cent). However, it is possible thatsomeoftheseconcernswereresolvedwithouttheSPSCommittee being made aware of these developments.Therefore, the number of resolved concerns inFigure C.4 should be taken as a lower estimate.TableC.4belowdocumentsthefactthatdisputescitingSPSmeasureshavenot increasedover time,eitherasan annual total or as a share of all disputes. This

suggests that the specific trade concerns mechanismmay be functioning better than the rising number ofdisputesandnotificationsinthisareawouldsuggest.

In the case of TBT specific trade concerns, onlyinformation on initiation of concerns, but not on theirtermination,isavailable.Thedata,showninFigureC.5,indicate an upward trend in initiations (but withreductionsbetween1998and1999;2002and2005;and2009and2010).

Consistentwiththemeasures-basedinformationfromnotifications, there is also some indication that anincreasing number of countries is involved in raisingspecific trade concerns or maintaining TBT/SPSmeasures subject to STCs (see Figure C.6).40 A keyelement is that developing countries are becomingimportantusersof thesystem–an issue thatwill beexploredinmoredetailinSectionC.2(c).

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

107

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

Because thenumber of “resolved” concerns is basedonanassumption in the caseofTBT, thedescriptivestatistics on TBT are to be interpreted with somecaution.Moreover,nodirectcomparisoncanbemadebetween SPS concerns (upper panel) and TBTconcerns(lowerpanel).

The specific trade concerns data can also provideinformation on the amount of trade affected byTBT/SPS concerns. Firstly, Figure C.7 shows theaverage amount of trade per concern initiated. Thefigure shows that, onaverage, the import valueof aninitiated trade concern has been quite stable since1995, with the exception of two peaks at the end ofeachdecade.InthecaseofSPSconcerns,thepeaksoccurred in 1997-98 and in 2008. As for TBTconcerns,therewasapeakin1999-2000andanothersmalleronein2010.41

Thesepeaksareduetothefilingofconcernsinvolvinga wide set of HS2 lines between two or more majortrading countries. In the case of the SPS peaks,the first is mainly due to two separate concerns, oneon pharmaceutical products raised by the UnitedStates, Switzerland, Brazil, Canada, Australia andothers against the European Union in 1997, andanother on dairy products raised by the EuropeanUnionagainstPolandin1998.TheSPSpeakin2008ismainlyduetoacomplaintbytheUnitedStatesandChina,amongothercountries,againstJapanonmeat,dairyandmostvegetableproducts.

For TBT concerns, the earlier peak is also a “doublepeak” spanning the years 1999 and 2000. In 1999,aTBTconcernwasraisedagainsttheEuropeanUnionbyalargesetofcountries includingtheUnitedStates,China and Japan, involving a wide range of sectors

FigureC.4:New and resolved SPS specific trade concerns, 1995-2010 (numberofconcerns)

FigureC.5:New TBT specific trade concerns, 1995-2010 (numberofconcerns)

1995

Num

ber o

f new

and

reso

lved

con

cern

s

Cum

ulat

ive

num

ber o

f act

ive

conc

erns

1996 1997 19991998 2000 20022001 2003 2004 20062005 2007 20092008 2010

45

25

35

40

30

15

20

10

5

250

150

200

100

50

00

Number of resolved concernsNumber of new concerns Cumulative

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

50

25

30

35

40

45

20

15

10

5

0

Source:WTOSTCDatabase.

Source:WTOSTCDatabase.

World TrAde reporT 2012

108

including miscellaneous chemical products, variousmetals,electricalmachineryandtoys.Anotherconcernwas raised in 2000 by the United States, Canada,Japan and others against the European Union onelectrical machinery and instruments. Finally, a TBTpeakin2010wasmainlyduetoaconcernraisedbytheEuropeanUnionagainst theUnitedStates, involvingawidesetofsectors,includingchemicalsandplastics.

Secondly, inventory-based measures of the incidenceofnon-tariffmeasures,namely frequencyandcoverageratios, have been calculated (see Box C.1 formethodology). In this case, too, a specific tradeconcern inTBT is assumed tobe “resolved” if, after itsinitiation, it is not raised again for two years; no directcomparison can be made between SPS concerns (seeFigure C.8(a)) and TBT concerns (see Figure C.8(b)),especiallyontheabsoluteamountoftradecovered.The

general message is, however, that frequency andcoverage ratios are increasing (although not evenly),indicatingthatSPSandTBTmeasuressubjecttospecifictrade concerns are affecting an increasing number ofproductlinesandanincreasingamountoftrade.42

Evidence from disputes on trends in TBT/SPSmeasures is inconclusive. According to Santana andJackson(2012),thenumberofdisputescitingtheSPSandTBTagreementsfellbetween1995and2011,butthedropwasconsistentwiththeoveralldeclineinthenumberofdisputesduringthisperiod(seeTableC.4).Requests for consultations related to SPS measuresfellfrom18in1995-2000tosevenin2007-11,buttheshare of SPS cases in the total number of disputesincreased to 11 per cent from 9 per cent betweenthesetwoperiods.DisputescitingtheTBTAgreementnumbered24intheearlierperiodandjusteightinthe

FigureC.6:Maintaining and raising countries in specific trade concerns, 1995-2010 (numberofcountries)

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

40

50

60

30

20

10

0

Raising countriesMaintaining countries

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

40

50

60

30

20

10

0

Raising countriesMaintaining countries

Source:WTOI-TIPdatabase.

Note:IntheTBTdataset,aconcernisassumedtobe“resolved”ifnotraisedagainfortwoormoreyears.A“raising”countryistheonewhichcomplainsaboutaTBT/SPSmeasureimposedbya“maintaining”countryintherelevantWTOcommittee.

(a)SPS

(b)TBT

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

109

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

FigureC.7:Average value of initiated SPS and TBT concerns, 1995-2010 (US$billion)

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

1.5

2 40

35

30

25

20

15

10

5

0

1

0.5

0

Average import value per new TBT concern (right axis)

Average import value per new SPS concern (left axis)

Source:WTOSTCDatabase.

FigureC.8:Coverage ratio and frequency index of STCs aggregated by year, 1995-2010

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

0.07

0.09

0.08

0.05

0.06

0.02

0.03

0.1

0.04

0.01

0

Frequency indexCoverage ratio

20

00

19

99

19

98

19

97

19

96

19

95

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

0.02

0.01

0.015

0.025

0.005

0

Frequency indexCoverage ratio

Source:WTOI-TIPdatabase.

Note:IntheTBTdataset,aconcernisassumedtobe“resolved”ifnotraisedagainfortwoormoreyears.

(a)SPS

(b)TBT

World TrAde reporT 2012

110

BoxC.1: Methodology for constructing indices from UNCTAD TRAINS and STC databases

TheUNCTADTRAINSdatabase,asdescribedinAppendixC.1,containsinformationonnon-tariffmeasuresbycountryandsectorforHS6productlines(asix-digitsub-headingintheHarmonizedSystemclassification)andyear.FollowingBoraetal.(2002),foragivencountrycinagivenyeart,theshareofimportlinesthataresubjecttoNTMsisdefinedasfollows:

19

(a) SPS (b) TBT Source: WTO STC Database. Note: In the TBT dataset, a concern is assumed to be “resolved” if not raised again for two or more years. Box C.1: Methodology for constructing indices from UNCTAD TRAINS and STC databases The UNCTAD TRAINS database, as described in Appendix C.1, contains information on non-tariff measures by country and sector for HS6 product lines (a six-digit sub-heading in the Harmonized System classification) and year. Following Bora et al. (2002), for a given country c in a given year t, the share of import lines that are subject to NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑀𝑀!!

𝑀𝑀!!

In the formula, i indexes HS6 products, Di is a dummy variable taking value equal to one if an NTM is in place and Mi is a dummy variable equal to one if there are imports of product i.43 The share of import values affected by NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑉𝑉!!

𝑉𝑉!!

where Vi is the value of imports at the HS6 level and tariff line level and Di is as above. Simple averages over countries for each of the years are used. Thus, each year’s share of import lines and share of trade value represents the average of a different sample of countries. However, the results with Latin American countries in Figure C.2 are based on a set of countries with information on the same years. Information on the countries to which the NTMs apply was not included. Therefore, the trade partner was chosen to be the world. The STC Database contains bilateral information at the HS4 sector disaggregation (a four-digit heading in the Harmonized System classification level). The coverage ratio and the frequency index were computed using the following formulae:

𝐶𝐶𝐶𝐶!,!"!,! =𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 !,!,!,!"!!"!∈!"!

𝐹𝐹𝐹𝐹!,!"!,! =𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑡𝑡𝑜𝑜𝑜𝑜𝑜𝑜𝑜𝑜 𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓!,!,!,!"!!"!∈!"!

where c indexes maintaining countries, j indexes raising countries, i indexes HS4 sectors and t indexes time. In other words, CR is the share of trade under a complaint over total trade for country c, in sector HS2 (a two-digit chapter in the Harmonized System classification level) at time t. This is an inventory-based measure of the intensive margin of trade covered by NTMs. FI is the share of the number of product codes covered by a certain NTM over the total number of product codes for which import flows are positive. It is an inventory-based measure of the extensive margin of trade under NTMs. Note that the set of j countries is not the world, but rather the set of raising countries per specific trade concern. This is very different from the TRAINS data. Given this difference, it is not

43 Subscripts c and t are omitted for expositional simplicity.

Intheformula,iindexesHS6products,DiisadummyvariabletakingvalueequaltooneifanNTMisinplaceand Mi is a dummy variable equal to one if there are imports of product i.43 The share of import valuesaffectedbyNTMsisdefinedasfollows:

19

(a) SPS (b) TBT Source: WTO STC Database. Note: In the TBT dataset, a concern is assumed to be “resolved” if not raised again for two or more years. Box C.1: Methodology for constructing indices from UNCTAD TRAINS and STC databases The UNCTAD TRAINS database, as described in Appendix C.1, contains information on non-tariff measures by country and sector for HS6 product lines (a six-digit sub-heading in the Harmonized System classification) and year. Following Bora et al. (2002), for a given country c in a given year t, the share of import lines that are subject to NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑀𝑀!!

𝑀𝑀!!

In the formula, i indexes HS6 products, Di is a dummy variable taking value equal to one if an NTM is in place and Mi is a dummy variable equal to one if there are imports of product i.43 The share of import values affected by NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑉𝑉!!

𝑉𝑉!!

where Vi is the value of imports at the HS6 level and tariff line level and Di is as above. Simple averages over countries for each of the years are used. Thus, each year’s share of import lines and share of trade value represents the average of a different sample of countries. However, the results with Latin American countries in Figure C.2 are based on a set of countries with information on the same years. Information on the countries to which the NTMs apply was not included. Therefore, the trade partner was chosen to be the world. The STC Database contains bilateral information at the HS4 sector disaggregation (a four-digit heading in the Harmonized System classification level). The coverage ratio and the frequency index were computed using the following formulae:

𝐶𝐶𝐶𝐶!,!"!,! =𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 !,!,!,!"!!"!∈!"!

𝐹𝐹𝐹𝐹!,!"!,! =𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑡𝑡𝑜𝑜𝑜𝑜𝑜𝑜𝑜𝑜 𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓!,!,!,!"!!"!∈!"!

where c indexes maintaining countries, j indexes raising countries, i indexes HS4 sectors and t indexes time. In other words, CR is the share of trade under a complaint over total trade for country c, in sector HS2 (a two-digit chapter in the Harmonized System classification level) at time t. This is an inventory-based measure of the intensive margin of trade covered by NTMs. FI is the share of the number of product codes covered by a certain NTM over the total number of product codes for which import flows are positive. It is an inventory-based measure of the extensive margin of trade under NTMs. Note that the set of j countries is not the world, but rather the set of raising countries per specific trade concern. This is very different from the TRAINS data. Given this difference, it is not

43 Subscripts c and t are omitted for expositional simplicity.

whereViisthevalueofimportsattheHS6levelandtarifflinelevelandDiisasabove.

Simpleaveragesovercountriesforeachoftheyearsareused.Thus,eachyear’sshareofimportlinesandshare of trade value represents the average of a different sample of countries. However, the results withLatinAmericancountriesinFigureC.2arebasedonasetofcountrieswithinformationonthesameyears.Informationon thecountries towhich theNTMsapplywasnot included.Therefore, the tradepartnerwaschosentobetheworld.

TheSTCDatabasecontainsbilateral informationattheHS4sectordisaggregation(afour-digitheading inthe Harmonized System classification level). The coverage ratio and the frequency index were computedusingthefollowingformulae:

19

(a) SPS (b) TBT Source: WTO STC Database. Note: In the TBT dataset, a concern is assumed to be “resolved” if not raised again for two or more years. Box C.1: Methodology for constructing indices from UNCTAD TRAINS and STC databases The UNCTAD TRAINS database, as described in Appendix C.1, contains information on non-tariff measures by country and sector for HS6 product lines (a six-digit sub-heading in the Harmonized System classification) and year. Following Bora et al. (2002), for a given country c in a given year t, the share of import lines that are subject to NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑀𝑀!!

𝑀𝑀!!

In the formula, i indexes HS6 products, Di is a dummy variable taking value equal to one if an NTM is in place and Mi is a dummy variable equal to one if there are imports of product i.43 The share of import values affected by NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑉𝑉!!

𝑉𝑉!!

where Vi is the value of imports at the HS6 level and tariff line level and Di is as above. Simple averages over countries for each of the years are used. Thus, each year’s share of import lines and share of trade value represents the average of a different sample of countries. However, the results with Latin American countries in Figure C.2 are based on a set of countries with information on the same years. Information on the countries to which the NTMs apply was not included. Therefore, the trade partner was chosen to be the world. The STC Database contains bilateral information at the HS4 sector disaggregation (a four-digit heading in the Harmonized System classification level). The coverage ratio and the frequency index were computed using the following formulae:

𝐶𝐶𝐶𝐶!,!"!,! =𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 !,!,!,!"!!"!∈!"!

𝐹𝐹𝐹𝐹!,!"!,! =𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑡𝑡𝑜𝑜𝑜𝑜𝑜𝑜𝑜𝑜 𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓!,!,!,!"!!"!∈!"!

where c indexes maintaining countries, j indexes raising countries, i indexes HS4 sectors and t indexes time. In other words, CR is the share of trade under a complaint over total trade for country c, in sector HS2 (a two-digit chapter in the Harmonized System classification level) at time t. This is an inventory-based measure of the intensive margin of trade covered by NTMs. FI is the share of the number of product codes covered by a certain NTM over the total number of product codes for which import flows are positive. It is an inventory-based measure of the extensive margin of trade under NTMs. Note that the set of j countries is not the world, but rather the set of raising countries per specific trade concern. This is very different from the TRAINS data. Given this difference, it is not

43 Subscripts c and t are omitted for expositional simplicity.

19

(a) SPS (b) TBT Source: WTO STC Database. Note: In the TBT dataset, a concern is assumed to be “resolved” if not raised again for two or more years. Box C.1: Methodology for constructing indices from UNCTAD TRAINS and STC databases The UNCTAD TRAINS database, as described in Appendix C.1, contains information on non-tariff measures by country and sector for HS6 product lines (a six-digit sub-heading in the Harmonized System classification) and year. Following Bora et al. (2002), for a given country c in a given year t, the share of import lines that are subject to NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑀𝑀!!

𝑀𝑀!!

In the formula, i indexes HS6 products, Di is a dummy variable taking value equal to one if an NTM is in place and Mi is a dummy variable equal to one if there are imports of product i.43 The share of import values affected by NTMs is defined as follows:

𝑆𝑆𝑆𝑆𝑆𝑆 =𝐷𝐷!𝑉𝑉!!

𝑉𝑉!!

where Vi is the value of imports at the HS6 level and tariff line level and Di is as above. Simple averages over countries for each of the years are used. Thus, each year’s share of import lines and share of trade value represents the average of a different sample of countries. However, the results with Latin American countries in Figure C.2 are based on a set of countries with information on the same years. Information on the countries to which the NTMs apply was not included. Therefore, the trade partner was chosen to be the world. The STC Database contains bilateral information at the HS4 sector disaggregation (a four-digit heading in the Harmonized System classification level). The coverage ratio and the frequency index were computed using the following formulae:

𝐶𝐶𝐶𝐶!,!"!,! =𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 !,!,!,!"!!"!∈!"!

𝐹𝐹𝐹𝐹!,!"!,! =𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓 𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢𝑢 𝑁𝑁𝑁𝑁𝑁𝑁!,!,!,!"!!"!∈!"!!

𝑡𝑡𝑜𝑜𝑜𝑜𝑜𝑜𝑜𝑜 𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛𝑛 𝑜𝑜𝑜𝑜 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝 𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖𝑖 𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓𝑓!,!,!,!"!!"!∈!"!

where c indexes maintaining countries, j indexes raising countries, i indexes HS4 sectors and t indexes time. In other words, CR is the share of trade under a complaint over total trade for country c, in sector HS2 (a two-digit chapter in the Harmonized System classification level) at time t. This is an inventory-based measure of the intensive margin of trade covered by NTMs. FI is the share of the number of product codes covered by a certain NTM over the total number of product codes for which import flows are positive. It is an inventory-based measure of the extensive margin of trade under NTMs. Note that the set of j countries is not the world, but rather the set of raising countries per specific trade concern. This is very different from the TRAINS data. Given this difference, it is not

43 Subscripts c and t are omitted for expositional simplicity.

wherecindexesmaintainingcountries,jindexesraisingcountriesand tindexestime.Inotherwords,CRistheshare of trade under a complaint over total trade for country c, in sector HS2 (a two-digit chapter in theHarmonizedSystemclassificationlevel)attimet.Thisisaninventory-basedmeasureoftheintensivemarginoftradecoveredbyNTMs.FIistheshareofthenumberofproductcodescoveredbyacertainNTMoverthetotalnumberofproductcodesforwhichimportflowsarepositive.Itisaninventory-basedmeasureoftheextensivemargin of trade under NTMs. Note that the set of j countries is not the world, but rather the set of raisingcountriesperspecifictradeconcern.ThisisverydifferentfromtheTRAINSdata.Giventhisdifference,itisnotsurprising that the shares of trade and lines covered computed from the TRAINS data is larger than thecoverageratiosandfrequencyindexescomputedfromtheSTCsdata.44

ForthedescriptivestatisticsusedinSectionC.2,weaverageCRandFIacrosssectorswithinmaintainingcountrycandtimet,andthenoverallmaintainingcountriesinyeart.TheformeraverageisweightedbytheHS2sectorimportshareintotalimportsofc.Thelatterisasimpleaverage.Theendresultisatime-varyingcoverageratioandfrequencyindex.45

Itshouldbeemphasized that these indexesare inventory-basedmeasures thatdonotnecessarilycapturethetraderestrictivenessofameasure,but justhowmuchtradeisaffectedbyit(SectionD.1isconcernedwiththemethodsusedtocomputethetraderestrictivenessofNTMs).Wheninterpretingthem,onehastotakeintoaccounttheissueofendogeneity.Forthecoverageratio(ortheshareofimportvaluesaffected),theproblemisthatthevalueofimportsinagivenproductlineisnegativelyaffectedbytheNTMsimposedonit.Forthefrequencyindex(ortheshareofimportlinesaffected),thisendogeneityproblemisattenuated,unlessthemeasureeliminatestradealtogether.However, thismeasure is less indicativeof theoverallandrelativeimportanceoftheNTM.

latterone,buttheirshareintotaldisputeswasroughlythe same in both periods, at 12 per cent. ThepercentageofdisputesmentioningTBTmeasuresfellto 4.5 per cent during the 2001-06 period before

returningto12percent,sowhiletherearesomesignsofarecentriseinthisarea,thereisnoindicationofalonger-termtrend.

II – TRADE AND PUBLIC POLICIES: A CLOSER LOOk AT NON-TARIFF MEASURES IN THE 21ST CENTURY

111

C. A

N IN

VE

NTO

RY

OF N

ON

-TAR

IFF

ME

AS

UR

ES

AN

D S

ER

VIC

ES

ME

AS

UR

ES

(b) AreTBT/SPSmeasuresmoreprevalentthanothertypesofnon-tariffmeasures?

(i) Evidence from official sources