Social Media – The Journey Part 1 by Shashwat Sood & Sumair Sethna

C.A. No.437/13 in Co.P. No.122/12

and connected cases

1

IN THE HIGH COURT OF KARNATAKA, BANGALORE

DATED THIS THE 24th DAY OF MAY, 2013

BEFORE

THE HON'BLE MR.JUSTICE RAM MOHAN REDDY

COMPANY APPLICATION NOS.437, 441, 440, 439 AND 438 OF 2013

IN COMPANY PETITION NOS.122, 121, 248, 185 AND 57

OF 2012 CA 437/2013 IN CO.P. No.122/2012 BETWEEN: UNITED BREWERIES (HOLDINGS) LIMITED, REGD. OFFICE AT UB CITY, LEVEL 12, UB TOWER, 24, VITTAL MALLYA ROAD, BANGALORE- 560 001.

… APPLICANT

(BY SRI. UDAYA HOLLA, SENIOR ADVOCATE FOR M/S. HOLLA AND HOLLA, ADVOCATES ) AND: ROLLS-ROYCE & PARTNERS FINANCE LIMITED, REGD. OFFICE AT 65, BUCKINGHAM GATE, LONDON SW1E 6AT ENGLAND REP. BY ITS AUTHORISED SIGNATORY MR.JITENDRA PANDA RESPONDENT (BY SRI N.N. HARISH, ADVOCATE )

C.A. No.437/13 in Co.P. No.122/12

and connected cases

2

THIS APPLICATION IS FILED UNDER SECTION 536(2) R/W SECTION 537(1) OF THE COMPANIES ACT, 1956 R/W RULES 6 AND 9 OF THE COMPANIES (COURT) RULES, 1959 PRAYING TO PERMIT THE APPLICANT UNDER SECTIONS 536(2) AND 537(1) TO SELL TO DIAGEO PLC AND/OR RELAY B.V. UPTO 13,612,591 EQUITY SHARES OF UNITED SPIRITS LIMITED HELD BY THE APPLICANT.

CA 441/2013 IN CO.P. No.121/2012 BETWEEN: UNITED BREWERIES (HOLDINGS) LIMITED, REGD. OFFICE AT UB CITY, LEVEL 12, UB TOWER, 24, VITTAL MALLYA ROAD, BANGALORE- 560 001.

… APPLICANT

(BY SRI. UDAYA HOLLA, SENIOR ADVOCATE FOR M/S. HOLLA AND HOLLA, ADVOCATES ) AND: RRPF ENGINE LEASING LIMITED, REGD OFFICE AT 65, BUCKINGHAM GATE, LONDON SW1E 6AT ENGLAND REP. BY ITS AUTHORISED SIGNATORY MR.JITENDRA PANDA ..RESPONDENT (BY SRI. N.N. HARISH, ADVOCATE ) THIS APPLICATION IS FILED UNDER SECTION 536(2) R/W SECTION 537(1)(b) OF THE COMPANIES ACT, 1956 R/W RULES 6 AND 9 OF THE COMPANIES (COURT) RULES, 1959 PRAYING TO PERMIT THE APPLICANT UNDER SECTIONS 536(2) AND 537(1) TO SELL TO DIAGEO PLC AND/OR RELAY B.V. UPTO

C.A. No.437/13 in Co.P. No.122/12

and connected cases

3

13,612,591 EQUITY SHARES OF UNITED SPIRITS LIMITED HELD BY THE APPLICANT.

C.A. No.440/2013 IN CO.P. No.248/2012 BETWEEN: UNITED BREWERIES (HOLDINGS) LIMITED, REGD. OFFICE AT UB CITY, LEVEL 12, UB TOWER, 24, VITTAL MALLYA ROAD, BANGALORE-560 001. APPLICANT (BY SRI UDAYA HOLLA, SENIOR ADVOCATE FOR M/S. HOLLA AND HOLLA, ADVOCATES) AND BNP PARIBAS, REGD. OFFICE AT 16, BOULEVARD DES ITALIENS, 75009, PARIS, FRANCE, REPRESENTED BY ITS CONSTITUTED ATTORNEY Mr. SABESAN ANANTHANATAYANAN RESPONDENT.

(BY Ms.FERESHTE SETHNA & PRASHANTH G., ADVOCATES) This application is filed under Section 536(2) read with Section 537(1)(b) of the Companies Act, 1956 read with Rules 6 and 9 of the Companies (Court) Rules, 1959, praying to permit the applicant under Sections 536(2) and 537(1)(b) to sell 13,612,591 equity shares of United Spirits Limited held by the applicant in the interests of justice.

CA NO.439/2013 IN CO.P. NO.185/2012

C.A. No.437/13 in Co.P. No.122/12

and connected cases

4

BETWEEN: UNITED BREWERIES (HOLDINGS) LIMITED, REGD. OFFICE AT UB CITY, LEVEL 12, UB TOWER, 24, VITTAL MALLYA ROAD, BANGALORE-560 001.

… APPLICANT.

(BY SRI UDAYA HOLLA, SR. ADVOCATE FOR M/s. HOLLA AND HOLLA, ADVOCATES) AND : AVIONS DE TRANSPORT REGIONAL G.I.E., 1, ALLE PIERRE NADOT, 31172 BLAGNAC, FRANCE, REP., BY ITS ATTORNEY SRI SUDARSHAN PRADHAN.

… RESPONDENT

(BY SRI. C. MURALIDHAR, ADVOCATE FOR M/S. MURALI AND CO., ADVOCATES)

THIS APPLICATION IS FILED UNDER SECTION 536(2) READ WITH SECTION 537(1)(b) OF THE COMPANIES ACT, 1956 READ WITH RULES 6 AND 9 OF THE COMPANIES (COURT) RULES, 1959 PRAYING TO PERMIT THE APPLICANT UNDER SECTIONS 536(2) AND 537(1)(b) TO SELL 13,612,591 EQUITY SHARES OF UNITED SPIRITS LIMITED HELD BY THE APPLICANT IN THE INTERESTS OF JUSTICE.

CA 438/2013 IN COP 57/2012 BETWEEN: UNITED BREWERIES (HOLDINGS) LIMITED,

C.A. No.437/13 in Co.P. No.122/12

and connected cases

5

REGD. OFFICE AT UB CITY, LEVEL 12, UB TOWER, 24, VITTAL MALLYA ROAD, BANGALORE- 560 001.

… APPLICANT

(BY SRI. UDAYA HOLLA, SENIOR ADVOCATE FOR M/S. HOLLA AND HOLLA, ADVOCATES) AND : IAE INTERNATIONAL AERO ENGINES AG, 628 HEBRON AVENUE, SUITE 400, GLASTONBURY, CONNECTICUIT 06033, USA REP. BY ITS ATTORNEY MR.PARAMINDER SINGH DADHWAL.

… RESPONDENT

(BY SRI. SHREYAS JAYASIMHA, ADV., FOR M/S. AZB & PARTNERS, ADVOCATES) THIS APPLICATION IS FILED UNDER SECTION 536(2) R/W SECTION 537(1)(b) OF THE COMPANIES ACT, 1956 R/W RULES 6 AND 9 OF THE COMPANIES (COURT) RULES, 1959 PRAYING TO PERMIT THE APPLICANT UNDER SECTIONS 536(2) AND 537(1)(b) TO SELL 13,612,591 EQUITY SHARES OF UNITED SPIRITS LIMITED HELD BY THE APPLICANT. THESE APPLICATIONS HAVING BEEN HEARD AND COMING ON FOR ORDERS THIS DAY, THE COURT MADE THE FOLLOWING:

C.A. No.437/13 in Co.P. No.122/12

and connected cases

6

ORDER

The respondent-company common in the company

petitions has presented these applications under

Section 536(2) and 537(1) of the Companies Act, 1956

for short ‘Act’ read with Rules 6 and 9 of the Companies

(Court) Rules, 1959, for short ‘Rules’ seeking leave of

the Court to permit it to sell, dispose of and/or procure

sale or disposal of upto 13,612,591 equity shares of

United Spirits Limited (USL) under DIAGEO transaction

referred to in the affidavit dt. 15.3.2013.

2. The applicant is said to own 25,577,293 equity

shares of USL equivalent to 18.03% as disclosed in the

Annual report for the financial year ended 31st March

2012.

3. The application, it is said is necessitated since:

(a) the petitioners in COP 248/12 and connected

petitions opposed the affidavit dt. 15.3.2013 of the

C.A. No.437/13 in Co.P. No.122/12

and connected cases

7

applicant undertaking to deposit before Court Rs.100

crores from out of the surplus sale proceeds it received

following completion of the DIAGEO transaction;

(b) on 15.1.2013 when COP 248/12 was listed for

admission, the applicant company, through its counsel

submitted that applicant would not alienate its

investments other than those (i) already secured to

various institutions and Banks by way of

pledging/mortgaging/securitizing, being Body

Corporates; (ii) specifically those of USL already

contracted to be sold in terms of the concluded deal

with DIAGEO, which when recorded this Court did not

pass interim orders in the petitions;

(c) at the hearing of COP 122/12 and CA 1130/12

on 15.3.2013, the applicant filed an affidavit disclosing

that shares of USL held by the applicant since

mortgaged/pledged/hypothecated in favour of various

financial institutions and Banks are agreed to be sold to

DIAGEO Group at a price of Rs.1,440/- per equity share

C.A. No.437/13 in Co.P. No.122/12

and connected cases

8

under a concluded contract and obtained requisite

permissions from Competitive Commission of India

(CCI), Securities and Exchange Board of India (SEBI);

(d) subsequently on 21.3.2013 Reserve Bank of

India (RBI) extended permission for the DIAGEO

transaction;

(e) that on 2.4.2013 in COP 122/12 and connected

petitions, this Court directed the applicant to make a

proposal for repayment of dues; and

(f) the Learned counsel for the applicant made a

submission on 08.04.2013, that pending final hearing of

the company petitions filed against the applicant before

this court, without admitting the liabilities, but to

demonstrate bonafides and subject to this Court

permitting the sale of equity shares of USL to DIAGEO

is willing to deposit Rs.200/- crores i.e. 119 crores from

DIAGEO and Rs.81 crores from sale of certain

immovable properties owned by it.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

9

4. According to the applicant in the usual course

of its business, to raise funds, pledged equity shares of

USL, owned by it, in favour of the following financial

institutions which have agreed to release the pledges for

the purpose of DIAGEO transaction, subject to payment

of their dues together with interest until settlement:

Rs. In

Crores

HDFC 75.00

Motilal 40.73

LKP 71.53

SICOM 193.66

Future 161.59

ILFS 155.47

IFCI 160.00

Religare 110.00

Edelweiss 200.00

HDFC Bank 23.00

Yes Bank 219.65

SREI 35.00

Narayan

Shriram

5.00

ICICI 145.00

C.A. No.437/13 in Co.P. No.122/12

and connected cases

10

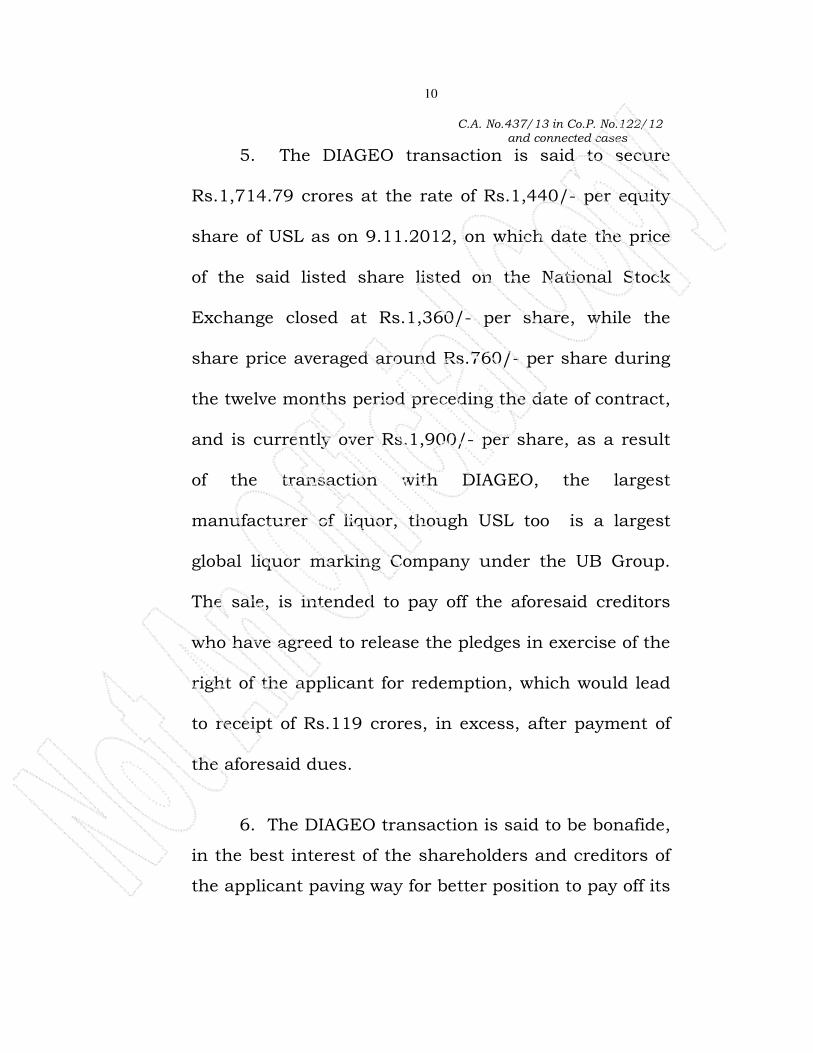

5. The DIAGEO transaction is said to secure

Rs.1,714.79 crores at the rate of Rs.1,440/- per equity

share of USL as on 9.11.2012, on which date the price

of the said listed share listed on the National Stock

Exchange closed at Rs.1,360/- per share, while the

share price averaged around Rs.760/- per share during

the twelve months period preceding the date of contract,

and is currently over Rs.1,900/- per share, as a result

of the transaction with DIAGEO, the largest

manufacturer of liquor, though USL too is a largest

global liquor marking Company under the UB Group.

The sale, is intended to pay off the aforesaid creditors

who have agreed to release the pledges in exercise of the

right of the applicant for redemption, which would lead

to receipt of Rs.119 crores, in excess, after payment of

the aforesaid dues.

6. The DIAGEO transaction is said to be bonafide,

in the best interest of the shareholders and creditors of

the applicant paving way for better position to pay off its

C.A. No.437/13 in Co.P. No.122/12

and connected cases

11

creditors and to preserve its business, as also increase

its net worth as opined by M/s Grant Thorton Group, a

leading international accounting firm. In the event the

transaction does not come through, the applicant

envisages a fall in the price of shares, severely affecting

its net worth to the detriment of its shareholders and

creditors.

7. On 18.4.2013, the applicant filed a memo in

COP 248/12, disclosing particulars of share holding

pattern, details of secured and unsecured loans, shares

pledged/non-disposal undertakings, details of

investments as on 31.3.2013 and copies of pledgees of

shares, as also the annual report 2011-12 of USL.

8. On 24.4.2013 the applicant filed a memo

stating that 87,94,000 equity shares of USL owned by

the applicant and held by M/s YES Bank, subject to

non-disposal undertaking, the said Bank exercised its

right and created a pledge on 10.4.2013.

9. On 26.4.2013 the applicant filed an affidavit

enclosing copies of documents relating to convening of

the meeting of secured creditors on 24.4.2013, whence

the petitioner-creditor in COP 248/12 was represented

C.A. No.437/13 in Co.P. No.122/12

and connected cases

12

and a unanimous decision taken to sell the pledged

13,612,591 equity shares of USL, to DIAGEO PLc in

terms of the agreements dt. 9.11.2012.

10. On 2.5.2013 applicant filed a memo enclosing

documents relating to pledge of USL shares as also

clarification over the same and details of encumbered

and unencumbered immovable properties of the

applicant.

11. On 9.5.2013 applicant filed an affidavit of

even date of its Corporate Vice President-Legal and

Company Secretary, stating that the applicant is willing

to offer its immovable property as security to Court to

secure an amount of Rs.250 crores to demonstrate its

bonafides (without admitting its liability) on the

following terms:

“(i) This Hon`ble Court may be pleased to grant leave in each of the Company Applications under Section 536(2) read with Section 537(1) of the Companies Act, 1956 permitting UBHL to sell, dispose of and / or procure the sale or disposal of upto 13,612,591 equity shares in USL held by UBHL to relay B.V/Diageo Plc;

C.A. No.437/13 in Co.P. No.122/12

and connected cases

13

(ii) UBHL shall be at liberty to deposit upto Rs.250 crores or any part thereof in this Hon`ble Court from time to time, provided that against each such deposit the aforesaid security in favour of this Hon`ble Court in respect of the aforesaid immovable property shall prorata stand released to the extent of each such deposit; and (iii) subject to the aforesaid charges created in favour of HDFC Ltd., and ICICI Ltd., and leases in favour of various third parties, UBHL shall not create any further charge in respect of the aforesaid immovable property, without the prior permission of this Hon`ble Court. “

12. The petitioning creditor in COP 57/12 filed

objections to CA 438/12 inter alia denying the claim

over the alleged DIAGEO transaction dated 09.11.2012

after the commencement of winding up proceeding,

much less, guarantee/pledge of shares of USL, in the

absence of material particulars and copies of

documents. Though in the absence of particulars along

with list of Secured and unsecured creditors of the

applicant, the admission of the Chairman of UB Group

over the execution of the Corporate Guarantees, the

application, it is said, is a ruse to thwart the attempt of

C.A. No.437/13 in Co.P. No.122/12

and connected cases

14

the petitioning creditor to secure an order of winding

up.

13. The petitioning creditor in COP 248/12 filed

objections to CA 248/12 on 9.5.2013 inter alia denying

the assertions in the application, in addition to

submitting that the application is to subvert orders on

the application for appointment of a provisional

liquidator while concedes the inevitability of winding up.

It is submitted that the applications are not

maintainable without an adjudication of the right of the

petitioner to seek admission of the petition. According

to the respondent, the application is to negate the

retrospective invalidation of the DIAGEO transaction

notwithstanding the applicant’s commercial insolvency.

14. It is stated that despite the undertaking

extended to the court on 15.1.2013, nevertheless,

caused prejudice to the petitioner, by admittedly dealing

C.A. No.437/13 in Co.P. No.122/12

and connected cases

15

with USL shares to the extent of Rs.55 crores as set out

in paragraph 8 of the statement of objections.

15. The alleged re-creation of pledge of 51500

shares (from 7,00,000 to 7,50,000) between 8.2.2013 to

22.2.2013 amounts to gross willful violation of the

undertaking. Even otherwise, 7,51,000 equity shares of

USL valued at more than 108 crores, regard being had

to its price on the relevant date, raises a doubt, in the

absence of valid explanation for the purpose for which

such sums were raised, leading to securing a fraudulent

preference of creditors.

16. The application is opposed on several grounds

including that of liquidation of assets through sale of

share in view of discrepancies in the disclosure of

number of shares of USL held by the applicant in the

public announcement dt. 9.11.2012. According to the

respondent, the number of shares contracted to be sold

C.A. No.437/13 in Co.P. No.122/12

and connected cases

16

to DIAGEO, the reduction in its numbers held by the

applicant as disclosed in the Bombay Stock Exchange

from December 2012 and that reflected during March

2013, as also the conversion from unsecured to

secured, the pledge of shares to LKP finance Limited

valued at Rs.71.53 crores occasioning suspicion. It is

submitted that the non-disposal undertaking extended

to EDELWEISS capital to the extent of 1,50,000 shares

is also suspect. The pledge forms, it is said, appear to

be unauthentic, while illegal pledges after 16.1.2012 (to

be read as 26.3.2012 as submitted by the learned

counsel), the date on which COP 5/12 was filed, require

to be held void, are in respect of the following:

(a) Yes Bank : 12.85 lakh equity shares of USL;

(b) Capital First : 12.79 lakh equity shares of USL;

(c) ECL : 22.15 lakh equity shares of USL;

(d) Religare : 20.52 lakh equity shares of USL;

(e) IFCI : 12.37 lakh equity shares of USL;

(f) IL&FS : 23.91 lakh equity shares of USL;

(g) HDFC : 15.85 lakh equity shares of USL.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

17

17. The annual report for the financial year ended

31.3.2012 of the applicant, it is submitted, does not

disclose pledges in respect of the following:

i) Motilal Oswal: who is claimed to be entitled

to receive Rs. 40.73 crores;

ii) LKP Finance: who is claimed to be entitled to

receive Rs.71.53 crores;

iii) SICOM: who is claimed to be entitled to

receive Rs.193.66 crores;

iv) SREI: who is claimed to be entitled to receive

Rs.35 crores;

v) Naryan Shriram: who is claimed to be

entitled to receive Rs.5 crores.

18. It is the further objection of the respondent

that the application suffers from non-disclosure of

statutory filings, consents, etc, regarding pledges, non-

disclosure of legal proceedings relating to pledge of

shares (suit instituted in Bombay High Court by the

C.A. No.437/13 in Co.P. No.122/12

and connected cases

18

applicant seeking reliefs against sale of pledged shares

by Banks and Financial Institutions), material

suppression of secured and unsecured creditor details,

requisition for share purchase agreement and ancillary

documents not complied with by the applicant, price

valuation by DIEGO sale wholly unsustainable, hence

the need to secure the funds in court. It is next stated

that under the Preferential Allotment Agreement dt.

9.11.2012 DEIGO PLc is entitled to preferential

allotment of 1,45,32,775 shares equivalent to 10% of

the enlarged capital, while under the Share Purchase

Agreement of even date, applicant agreed to sell

9,070,595 equivalent to 6.24% equity shares of USL

while King Fisher (subsidiary of the applicant) agreed to

sell 7,64,63,092 shares equivalent to 5.26% of USL

shares, amongst other shareholders, who have agreed to

sell USL Share owned by them, totaling to 2,52,26,839

equity shares, representing 17.4% of the enlarged

capital, while, the public offer is for 3,77,85,214 shares

C.A. No.437/13 in Co.P. No.122/12

and connected cases

19

representing 26%. Thus in all DIAGEO transaction it is

said, entitles the purchaser to 7,75,44,827 representing

53.4% of equity shares in USL.

19. According to the respondent if USL does not

receive the cash infusion through the preferential

allotment then the deal with DIAGEO cannot fructify. It

is the submission of the respondent that since the

applicant has freely dealt with the shares of USL owned

by its subsidiaries, in the first event be held liable to

discharge any outstanding liability to the lenders from

such pledged shares rather than from the shares of USL

held by the applicant. Yet again, it is submitted, that

after 26.3.2012 sale of any shares of USL owned by the

applicant’s subsidiaries cannot but be void.

20. It is next submitted that the claim to validate

the sale of shares, in view of pledges and the pledgees

C.A. No.437/13 in Co.P. No.122/12

and connected cases

20

consent to the sale, is impermissible, since the pledges

rights are questionable.

21. The valuation report of the immovable

properties belonging to the applicant are said to be

unreliable for several reasons one of which being that

the value could be achieved only “after completion”. The

assessment made by the valuer over the valuation, it is

submitted, is unrealistic and not supported by relevant

material.

22. Applicant filed a rejoinder on 14.5.2013 to

clarify certain facts such as the filing of the company

petition No.5/12 by M/s Micro Dynamics Pvt Ltd. on

16.1.2012 against a company which is not the applicant

and that the respondent is fully aware of the filing of the

O.S.No.263/2013 by the applicant before the Bombay

High court and that State Bank of India and Jammu

and Kashmir Bank invoked the pledged shares of USL,

thus reducing the applicant’s holding of USL shares to

C.A. No.437/13 in Co.P. No.122/12

and connected cases

21

2,05,73,768 and further that M/s Motilal Oswal

Financial Services Limited addressed a letter dated

21.12.2012 to LKP Finance Limited regarding disclosure

in Form-W of even date, the pledge of 1,22,000 shares of

USL as a security trustee on behalf of LKP Finance

Limited and therefore there is no conversion from

unsecured to secured creditor, unsupported by pledge

forms.

23. The letter dated 6.5.2013 of the learned

counsel for the respondent, it is said, in the rejoinder,

seeks unlimited access to records, documents, books of

account, etc. over which the respondent cannot claim as

a matter of right. It is further stated that the applicant

is entitled to seek the reliefs in the application while

pointing out that it holds 2,25,99,890 equity shares of

USL as on 15.1.2013 from out of which 4,70,233 are

unencumbered as on that date, while 5,90,272 equity

shares held by the applicant are unencumbered as on

C.A. No.437/13 in Co.P. No.122/12

and connected cases

22

29.4.2013. The allegation of the applicant having raised

108 crores against pledge of 7,51,500 equity shares of

USL is countered by stating that security cover

demanded by lenders ranges between 1.75 to 2.5 times

the amounts advanced. It is further stated that the

summary of utilization of proceeds submitted by the

applicant as on 8.4.2013 discloses amounts payable to

pledges of the shares created for raising loans in the

usual course of business of the applicant, which are

bonafide. As regards the allegation that another

secured creditor M/s United Bank of India has filed a

company petition before this court, it is stated, that the

applicant is not served with a copy of the petition and

therefore, unaware of its filing and hence unable to

respond to the allegation. That USL’s U.K. based

subsidiary USL Holdings (UK) Limited obtained financial

assistance from City Bank, London to remit funds for

operations of WHYTE and MACKAY Limited, Scotland, a

C.A. No.437/13 in Co.P. No.122/12

and connected cases

23

wholly owned subsidiary of USL and one of the largest

scotch whisky distilleries in the world.

I Re: JURISDICTION UNDER SECTION 536(2) OF THE ACT DURING THE PENDENCY OF COMPANY PETITION FOR WINDING-UP.

24. The contention of the respondent that the

jurisdiction of the company court under Section 536 of

the Act arises only after winding up of the applicant

company, by placing reliance upon the opinion of this

court in Mandya National Paper Mills Limited –v- Rai

Bahadur Shreeram Durgaprasad Private Limited1 is

without merit since it does not fully support the said

proposition, in view of the following observation:

“It may be that the suggestion that the court

has no jurisdiction whatever to deal with

situations arising between the date of

presentation of the winding –up petition and the

order of winding-up is not sound, because on the 1 1967(37) Comp.cases 201 (Mysore High Court)

C.A. No.437/13 in Co.P. No.122/12

and connected cases

24

passing of a winding-up order, the date of

commencement of winding-up is related back to

the date of presentation of the petition, and,

secondly, even before an order for winding up is

passed, the court may find it necessary to make

appropriate interim orders either for the protection

of the company or for the protection of any of the

creditors of the company.”

25. There is force in the submission of the learned

senior counsel for the applicant that an order under

Section 536(2) of the Act is permissible even before the

winding up of the company, in the light of the

observations in the opinion of this court in Smt.Usha

R.Shetty and others –v- M/s Radeesh Rubber Private

Limited, Bangalore and another2, that at the stage of

entertaining a winding up petition the court has

inherent power to do that which is necessary to advance

the cause of justice or make such orders which are 2 1992(3) Kar.L.J 604

C.A. No.437/13 in Co.P. No.122/12

and connected cases

25

necessary to meet the ends of justice and such inherent

power is neither taken away nor restricted by Section

443(1) of the Act, while negating the plea that court

cannot exercise jurisdiction under Section 536(2) of the

Act before the winding up order is passed, following the

observations of the Apex Court in N.S.Mills –v- Union

of India3 and Hind Overseas Private Limited –v-

R.P.Jhunjhunwala4.

26. In Kamani Metallic Oxides Limited –v-

Kamani Tubes Limited5 the Division Bench of the

Bombay High Court followed the observations in re

Miles Aircraft Limited6 that “firstly the opening clause

of Section 536(2) “ in the case of winding up” does not

mean “ after the winding up order is passed” or “ upon

passing such order”. It means “ during winding up

proceeding” which admittedly commence on the date on

3 AIR 1976 SC 1152

4 1976(46) Comp.cases 91(SC)

5 1984 (56) Comp.cases 19

6 (1948) 1 All.ER 225 # 18 Comp.cases 250 (Ch.D)

C.A. No.437/13 in Co.P. No.122/12

and connected cases

26

which the petition for winding up is filed. This

interpretation which we are putting does not leave

bonafide dispositions of assets of the company, open to

challenge at the hands of the liquidator, in the event of

winding up order being passed. Sometimes dispositions

would be necessary in the interest of the company and

thus in the ultimate interest of the creditors of the

company, during the pendency of the application for

winding up. But the Directors would be reluctant to enter

into transactions on their own for fear of the transactions

being declared invalid on the passing of the winding up

order. The company Court must have jurisdiction to

protect such transactions. We, therefore, feel that the

rule of harmonious construction supports the view that

the Court can exercise jurisdiction under Section 536(2)

even before the winding up order is made. The fact that

the order would become otiose if the application for

winding up is ultimately rejected, does not take away the

jurisdiction.”

C.A. No.437/13 in Co.P. No.122/12

and connected cases

27

27. The Division Bench in addition followed the

observations In re A.I.Levy (Holdings) Limited7 :

“ It appears to me that the object of the Section

is to protect the interest of the creditors from the

possible unfortunate results which would ensue

from the presentation of a petition, and to protect

the interests as much during the period while the

petition was pending as after an order has been

made on it. What the section provides in its

present terms is that any disposition of the

property of the company made after the

commencement of the winding up shall be void in

the winding up of the company unless the court

otherwise orders; that is to say, if and when the

company comes to be put into liquidation the

transaction is to be as if it had never taken place.”

28. So also is the view of the Kerala High court

in Travancore Rayons Limited –v- Registrar of

Companies8.

7 (1964) 1 Ch 19 # 34 Comp.cases 720 (Ch.D) at page 727

8 1988(64) Comp.cases 819

C.A. No.437/13 in Co.P. No.122/12

and connected cases

28

II Re: ALLEGATIONS OF VIOLATION OF LAWS IN

THE MATTER OF PLEADGE OF SHARES

29. The next submission of the learned counsel

for the respondent that the alleged pledges of USL

shares owned by the applicant are in violation of Section

12(3) of the Depositories Act, 1996 and Regulation 58 of

the Securities and Exchange Board of India

(Depositories and Participants) Regulations, 1996, for

short ‘Regulations’ framed under The Securities and

Exchange Board of India Act, 1992 (Act 15 of 1992),

exfacie, is untenable. Section 12 of the Depositories

Act, 1996 reads thus:

12. Pledge or hypothecation of securities held

in a depository.-(1) Subject to such regulations

and bye-laws, as may be made in this behalf, a

beneficial owner may with the previous approval

of the depository create a pledge or

hypothecation in respect of a security owned by

him through a depository.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

29

(2) Every beneficial owner shall give intimation of

such pledge of hypothecation to the depository

and such depository shall thereupon make

entries in its records accordingly.

(3) Any entry in the records of a depository

under sub-section (2) shall be evidence of a

pledge or hypothecation

Regulation 58 of the Regulations reads thus:

Manner of creating pledge or hypothecation.

58. (1) If a beneficial owner intends to create a

pledge on a security owned by him, he shall

make an application to the depository through

the participant who has his account in respect of

such securities.

2) The participant after satisfaction that the

securities are available for pledge shall make a

note in its records of the notice of pledge and

forward the application to the depository.

(3) The depository after confirmation from the

pledgee that the securities are available for

pledge with the pledger shall within fifteen days

C.A. No.437/13 in Co.P. No.122/12

and connected cases

30

of the receipt of the application create and

record the pledge and

send an intimation of the same to the

participants of the pledger and the pledgees.

(4) On receipt of the intimation under sub-

regulation (3) the participants of both the

pledger and the pledgee shall inform the pledger

and the pledgee respectively of the entry of

creation of the pledge.

(5) If the depository does not create the pledge, it

shall send along with the reasons an intimation

to the participants of the pledgor and the

pledgee.

(6) The entry of pledge made under sub-

regulation (3) may be cancelled by the depository

if the pledger or the pledgee makes an

application to the depository through its

participant:

Provided that no entry of pledge shall be

cancelled by the depository without prior

concurrence of the pledgee.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

31

(7) The depository on the cancellation of the

entry of pledge shall inform the participant of

the pledger.

(8) Subject to the provisions of the pledge

document, the pledgee may invoke the pledge

and on such invocation, the depository shall

register the pledgee as beneficial owner of such

securities and amend its records accordingly.

(9) After amending its records under sub-

regulation (8) the depository shall immediately

inform the participants of the pledger and

pledgee of the change who in turn shall make

the necessary changes in their records and

inform the pledger and pledgee respectively.

(10) (a) If a beneficial owner intends to create a

hypothecation on a security owned by him he

may do so in accordance with the provisions of

sub-regulations (1) to (9).

(b) The provisions of sub–regulations (1) to (9)

shall mutatis mutandis apply in such cases of

hypothecation:

Provided that the depository before

registering the hypothecatee as a

C.A. No.437/13 in Co.P. No.122/12

and connected cases

32

beneficial owner shall obtain the prior

concurrence of the hypothecator.

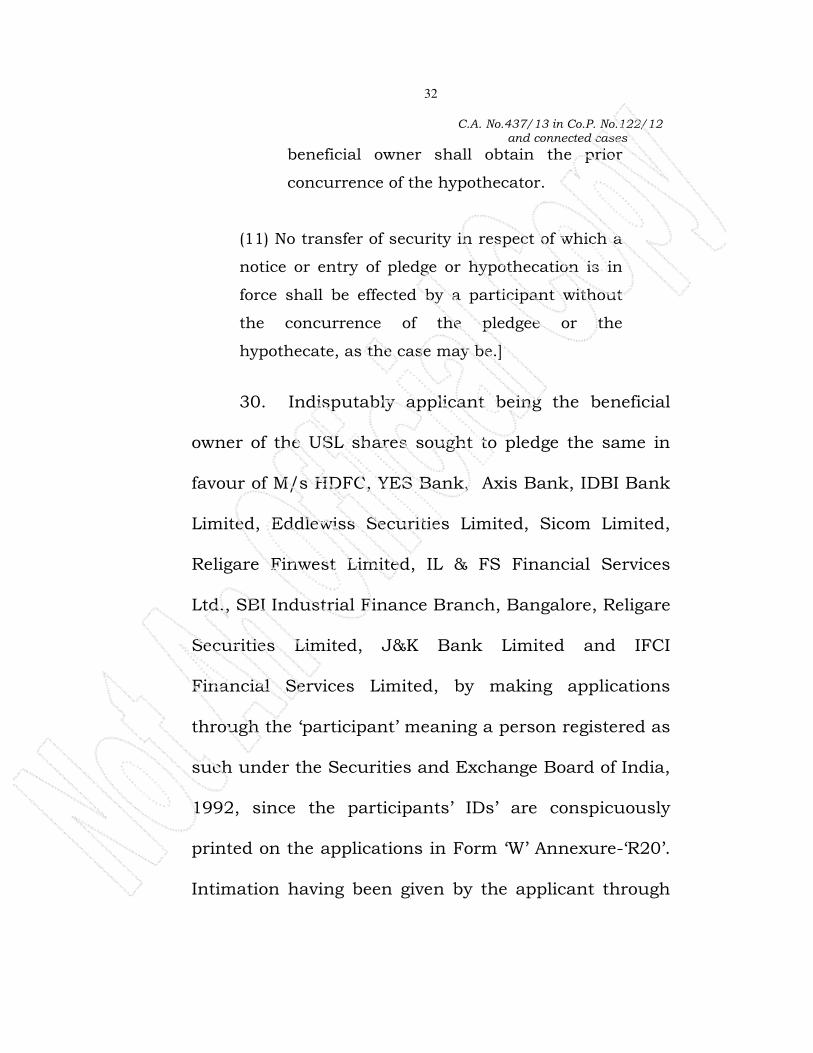

(11) No transfer of security in respect of which a

notice or entry of pledge or hypothecation is in

force shall be effected by a participant without

the concurrence of the pledgee or the

hypothecate, as the case may be.]

30. Indisputably applicant being the beneficial

owner of the USL shares sought to pledge the same in

favour of M/s HDFC, YES Bank, Axis Bank, IDBI Bank

Limited, Eddlewiss Securities Limited, Sicom Limited,

Religare Finwest Limited, IL & FS Financial Services

Ltd., SBI Industrial Finance Branch, Bangalore, Religare

Securities Limited, J&K Bank Limited and IFCI

Financial Services Limited, by making applications

through the ‘participant’ meaning a person registered as

such under the Securities and Exchange Board of India,

1992, since the participants’ IDs’ are conspicuously

printed on the applications in Form ‘W’ Annexure-‘R20’.

Intimation having been given by the applicant through

C.A. No.437/13 in Co.P. No.122/12

and connected cases

33

the ‘participant’, duly acknowledged, is compliance with

Regulation 58(1) of the Regulations, while under sub-

regulation (2) it is for the ‘participant’ to make note in

its record the notice of the pledge and thereafter forward

the application to the depository. Thus the applicant

has, primafacie, disclosed compliance with the notice of

pledge.

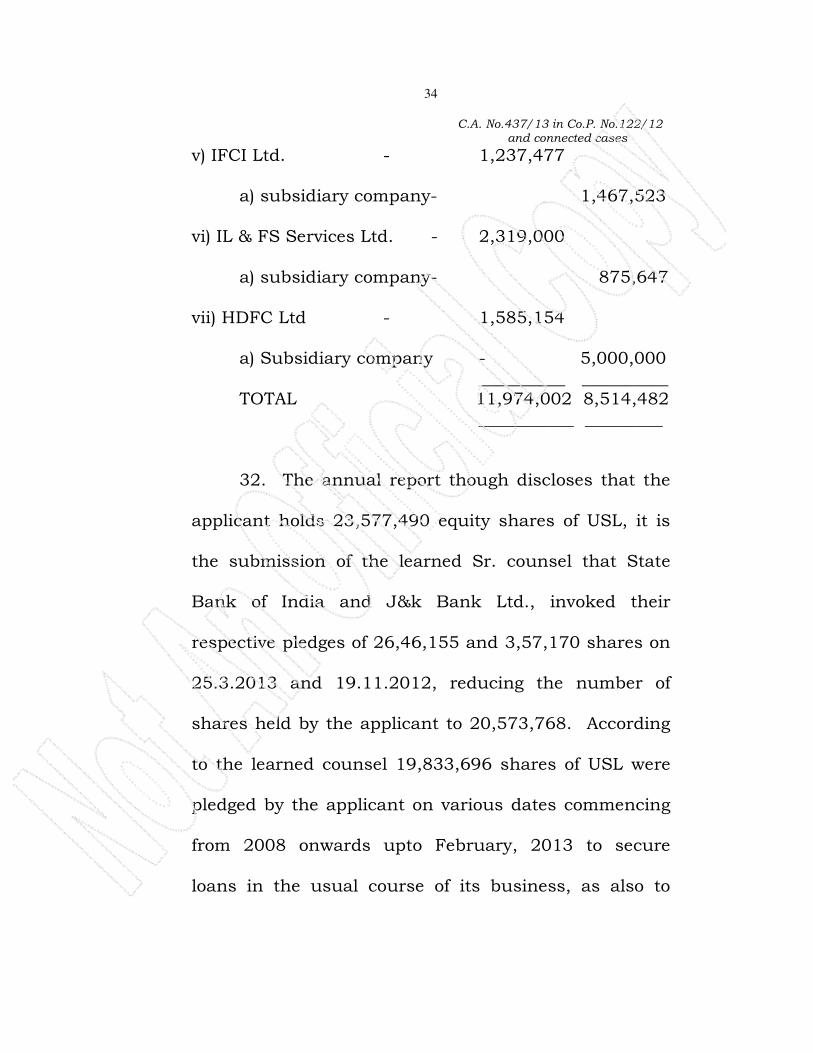

31. Moreover, in the Notes to the financial

statement under the nomenclature ‘ Nature of Security

and terms of repayment of secured borrowings’, at page

33 of the Annual report 2011-12 of the applicant,

discloses the creation of following pledges:

Name No. of shares of USL

i) YES Bank Ltd - 1,285,000

ii) Future Capital Holdings Ltd- 1,279,688

a) Subsidiary company- 1,171,312

iii) ELC Finance Ltd. - 2,215,000

iv) Religare Finvest Ltd. - 2,052,683

C.A. No.437/13 in Co.P. No.122/12

and connected cases

34

v) IFCI Ltd. - 1,237,477

a) subsidiary company- 1,467,523

vi) IL & FS Services Ltd. - 2,319,000

a) subsidiary company- 875,647

vii) HDFC Ltd - 1,585,154

a) Subsidiary company - 5,000,000

__________ __________ TOTAL 11,974,002 8,514,482 ___________ _________

32. The annual report though discloses that the

applicant holds 23,577,490 equity shares of USL, it is

the submission of the learned Sr. counsel that State

Bank of India and J&k Bank Ltd., invoked their

respective pledges of 26,46,155 and 3,57,170 shares on

25.3.2013 and 19.11.2012, reducing the number of

shares held by the applicant to 20,573,768. According

to the learned counsel 19,833,696 shares of USL were

pledged by the applicant on various dates commencing

from 2008 onwards upto February, 2013 to secure

loans in the usual course of its business, as also to

C.A. No.437/13 in Co.P. No.122/12

and connected cases

35

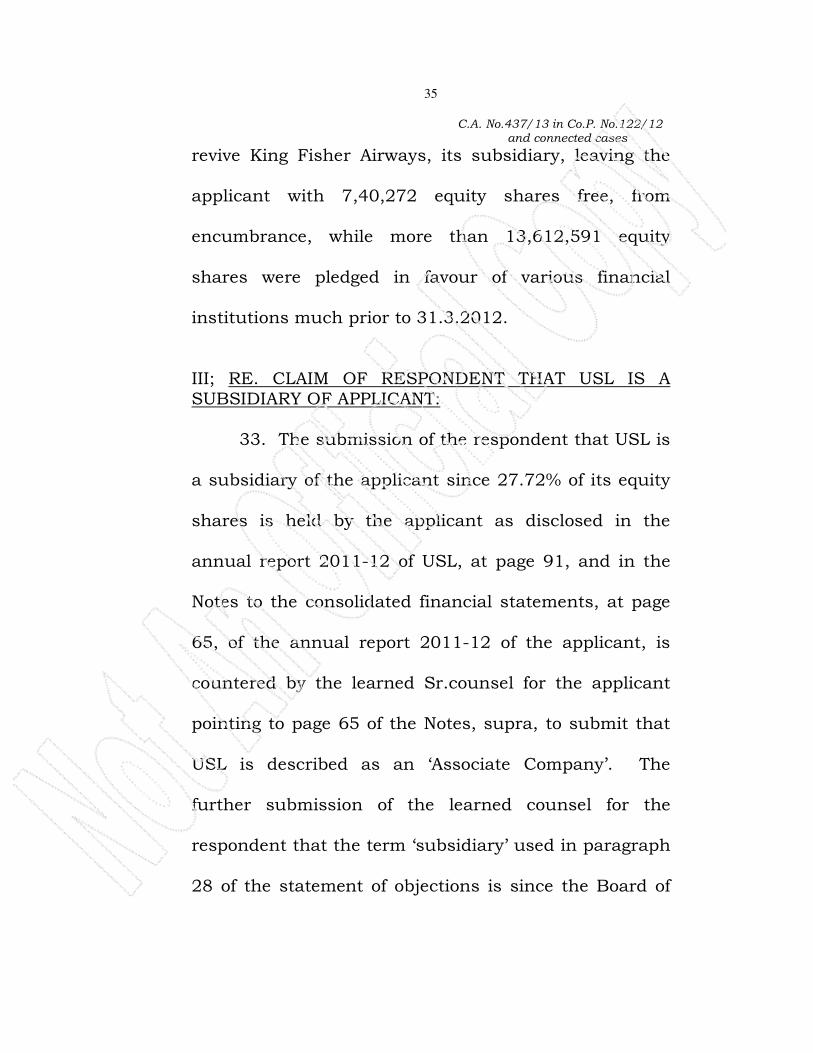

revive King Fisher Airways, its subsidiary, leaving the

applicant with 7,40,272 equity shares free, from

encumbrance, while more than 13,612,591 equity

shares were pledged in favour of various financial

institutions much prior to 31.3.2012.

III; RE. CLAIM OF RESPONDENT THAT USL IS A SUBSIDIARY OF APPLICANT: 33. The submission of the respondent that USL is

a subsidiary of the applicant since 27.72% of its equity

shares is held by the applicant as disclosed in the

annual report 2011-12 of USL, at page 91, and in the

Notes to the consolidated financial statements, at page

65, of the annual report 2011-12 of the applicant, is

countered by the learned Sr.counsel for the applicant

pointing to page 65 of the Notes, supra, to submit that

USL is described as an ‘Associate Company’. The

further submission of the learned counsel for the

respondent that the term ‘subsidiary’ used in paragraph

28 of the statement of objections is since the Board of

C.A. No.437/13 in Co.P. No.122/12

and connected cases

36

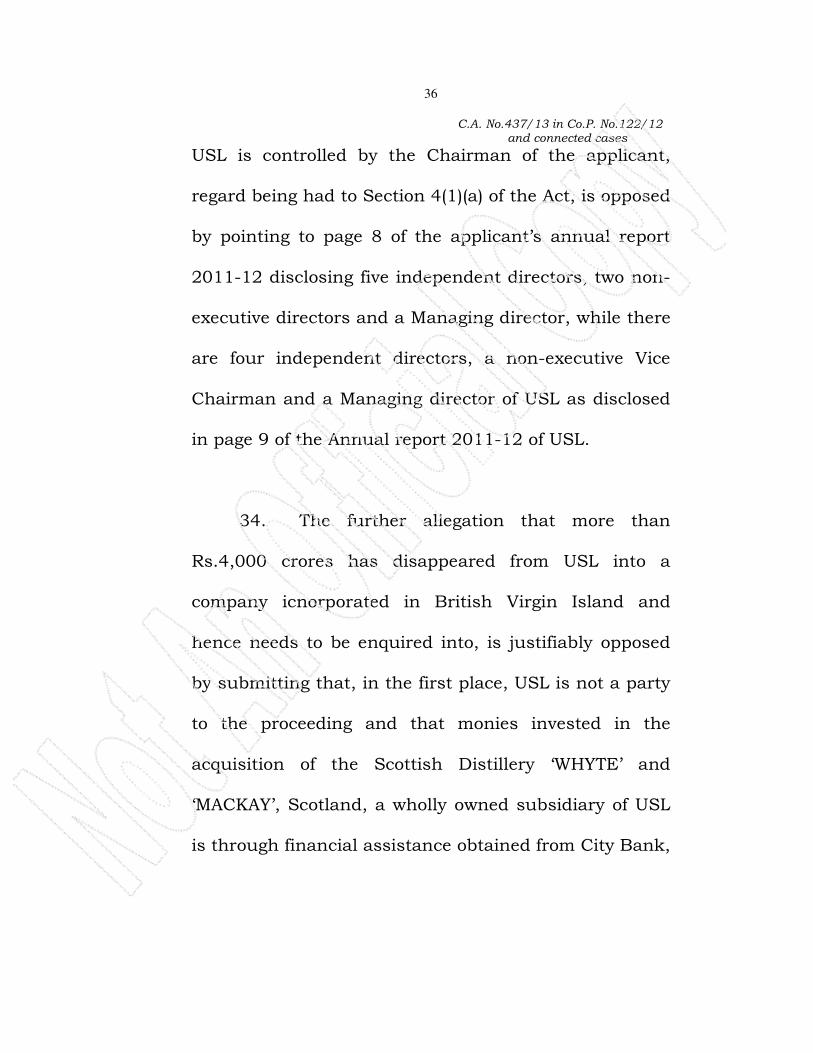

USL is controlled by the Chairman of the applicant,

regard being had to Section 4(1)(a) of the Act, is opposed

by pointing to page 8 of the applicant’s annual report

2011-12 disclosing five independent directors, two non-

executive directors and a Managing director, while there

are four independent directors, a non-executive Vice

Chairman and a Managing director of USL as disclosed

in page 9 of the Annual report 2011-12 of USL.

34. The further allegation that more than

Rs.4,000 crores has disappeared from USL into a

company icnorporated in British Virgin Island and

hence needs to be enquired into, is justifiably opposed

by submitting that, in the first place, USL is not a party

to the proceeding and that monies invested in the

acquisition of the Scottish Distillery ‘WHYTE’ and

‘MACKAY’, Scotland, a wholly owned subsidiary of USL

is through financial assistance obtained from City Bank,

C.A. No.437/13 in Co.P. No.122/12

and connected cases

37

London, in full compliance with the Foreign Exchange

Regulations.

35. In the circumstances, truly, an investigation

into the aforesaid allegations at this stage of the

proceeding in the company petition is neither desirable

nor called for.

IV. Re: PRINCIPLES GOVERNING EXERCISE OF JURISDICTION OF COURTS UNDER SECTION 536(2) OF THE ACT:

36. It is useful to make reference to the

observations of the Court of Chancery Division in

Burton and Deakin Ltd., In re9 :

“ If on an application under Section 227

relating to a solvent company, it s directors

placed before the Court evidence that they

considered that a particular disposition falling

within their powers was necessary or expedient

in the interest of the company, and if the court

considered that the reasons given were such as

9(1977) 1 All ER 631 (Ch.D)

C.A. No.437/13 in Co.P. No.122/12

and connected cases

38

an intelligent and honest man could reasonably

hold, the Court would normally sanction the

disposition notwithstanding the opposition of a

contributory, unless the contributory had

adduced compelling evidence which proved that

the disposition is likely to injure the company.

The court would not, except in the case of proven

bad faith or other exceptional circumstances,

interfere with the discretion conferred on the

directors by a company’s articles of association at

the instance of the contributory, even if a

winding-up petition had been presented.

According to Slade J, the animus of the

subsection is to forbid malapropos and

objectionable disposition or dissipation of

property which would ultimately fall to a low ebb

or tale off the assets otherwise available for

distribution among the creditors of the company

in the event of winding-up. But the section

leaves a reserve power of discretion to justify and

uphold all genuine and proper transactions,

exercising a sound discretion normally validating

transactions which are benign and honest;

transactions which have been done in the best

C.A. No.437/13 in Co.P. No.122/12

and connected cases

39

interest of the company and in the ordinary

course of the company’s business. The legislative

intent is plainly manifested by the use of the

select expression ‘unless the court otherwise

orders’ which mandates silently but eloquently a

duty on the Judge to examine each case on its

peculiarities, facts, and circumstances, special

bearing being given to the question of good faith

and honest intention aimed at the best interest of

the company. The omission to indicate any

special guiding principles in the matter of

discretion to be exercised by the Court, makes it

clear that it is not left entirely at large, but

controlled by the general principles which apply

to every kind of judicial discretion.”

37. In re Gray’s Inn Construction Company

Limited10 the Court of appeals observed thus:

“ In considering whether to make a

validating order the court must always, in

my opinion, do its best to ensure that the

interests of the unsecured creditors will not

be prejudiced. Where the application relates

10

(1980) 1 WLR.711

C.A. No.437/13 in Co.P. No.122/12

and connected cases

40

to specific transaction this may be

susceptible of possible proof. In a case of

completion of a contract or project the proof

may perhaps be less positive but

nevertheless be cogent enough to satisfy the

court that in the interest of the creditors the

company should be enabled to proceed, or at

any rate that proceeding in the manner

proposed would not prejudice them in any

respect. The desirability of the company

being enabled to carry on its business

generally is likely to be more speculative and

will be likely to depend on whether a sale of

the business as a going concern will be more

beneficial than a break-up realization of the

companies assets. In each case, I think, the

court must necessarily carry out a balancing

exercise of the kind envisaged by

Templeman J., in his Judgment. Each case

must depend on its own particular of facts.

Since the policy of the law is to procure

as far as practicable ratable payments of the

unsecured creditors’ claims, it is, in my

opinion, clear that the court should not

validate any transaction or series of

C.A. No.437/13 in Co.P. No.122/12

and connected cases

41

transactions which might result in one or

more preliquidation creditors being paid in

full at the expense of other creditors, who

will only receive a dividend, in the absence of

special circumstances making such a course

desirable in the interests of the unsecured

creditors as a body. If for example, it were in

the interest of the creditors generally that

the company’s business should be carried on

and this could only be achieved by paying for

goods already supplied to the company when

the petition is presented but not yet paid for,

the court might think fit in the exercise of its

discretion to validate payment for those

goods.”

38. In RBI –V- CRYSTAL CREDIT

CORPORATION LIMITED11 at paragraph 5 it is

observed thus:

“ …. The purpose behind subsection (2)

of Section 536 is to prevent improper

disposition or dissipation of property so as to

affect the assets otherwise available for

11

(2006) 132 COMP.cases 363 (Delhi)

C.A. No.437/13 in Co.P. No.122/12

and connected cases

42

distribution among the creditors of the

company in winding up. But the court is,

however, given the discretion to uphold all

proper transactions which otherwise appear

to be proper transactions. What is to be

borne in mind, while examining such a

transaction, is that the assets of the

company should be made available for

distribution pari passu amongst the

creditors of the company and that no

creditor should obtain an advantage over his

fellow creditor. In Andhra Bank Ltd. –v-

Provisional Liquidator, Godavari sugars

and Refineries Ltd.12, after scanning

through the case law on the point culled out

the following principles which are to be kept

in mind in such cases:

i) transactions bonafide entered

into and completed in the

ordinary course of trade must be

protected.

ii) if the disposition is made for the

purpose of preserving the

business as a going concern,

12

(1954) 24 Comp.cases 149

C.A. No.437/13 in Co.P. No.122/12

and connected cases

43

then also the discretion of a court

must be exercised.

iii) A disposition must not be

validated merely because the

party bonafide entered into the

transaction.

iv) Knowledge of the presentation of

the winding up is immaterial.”

V. RE.PLEDGE OF SHARES FOR RAISING LOANS NOT FORTHCOMING FROM THE APPLICANT’S ANNUAL REPORT 2011-12:

39. From out of the names of the pledgees

(Secured Creditors) and the amounts due to them said

to be Rs.1,595.63 crores, as extracted in paragraph 4

supra, pledge of shares of USL by the applicant for

securing loans from the following are not disclosed in

the Annual report 2011-12 of the applicant, so as to, at

this stage, be treated as secured creditors, more so after

the institution of the company petition 5/12 on

26.3.2012:

C.A. No.437/13 in Co.P. No.122/12

and connected cases

44

Names Rs. in crores

i) Motilal 40.73

ii) L.K.P. 71.53

iii) SICOM 193.66

iv) SREI 35.00

v) Narayan Shreeram 5.00

vi) ICICI 145.00

Total 490.92

40. There is force in the submission of the learned

counsel for the respondent that the pledge of USL

shares by the applicant in respect of the aforesaid

pledges, not disclosed to be accounted for in the Books

of account of the applicant for the financial year 2011-

12 and in the absence of relevant material as well as

accounts post 31.3.2012 or after the undertaking

extended to the court on 15.1.2013 for having taken

loans by the applicant as against the pledges, in the

usual course of business of the applicant, prima facie,

do not qualify for repayment. In order to effect

repayment to the pledgees, it is required of the

applicant, who admits to have made pledge of shares

C.A. No.437/13 in Co.P. No.122/12

and connected cases

45

after 31.3.2012, to establish transaction bonafide

entered into and completed in the ordinary course of

trade, to be protected and that the disposition is made

for the purpose of preserving the business as a going

concern. Regard being had to the nature of business of

the applicant and the ongoing projects of construction

activity over its immovable properties, it is possible that

the Applicant may have bonafide, for preserving the

business, pledged shares in USL with reputed financial

institution. But merely because pledge of shares of USL

is made by the applicant in favour of the aforesaid

institutions, a bonafide transaction, does not mean that

the disposition during the pendency of the Company

Petition calls for validation. Had records of accounts

been made available, the Court could have appreciated

such material and if warranted protected the said

transactions, even if the transactions are made during

the pendency of petition for winding-up, being its

jurisdiction under Sec 536(2) of the Act. It is open for

C.A. No.437/13 in Co.P. No.122/12

and connected cases

46

the Applicant to make necessary application in that

regard.

VI) RE – ADJUDICATION OVER PLEDGES OF SHARES IN FAVOUR OF S.B.I & J & K BANK LTD.

41. The submission that the pledge of 26,46,155

shares of USL by the applicant in favour of SBI and

3,57,170 shares in favour of J & K Bank made

apparently after 31.3.2012 (since not accounted for in

the balance sheet for the financial year 2011-12) and

since invoked, while the High court of Bombay did not

grant any interim relief to the applicant over the

disposal of the shares by the pledgees, ought to be

declared void, is unavailable to the respondent as it

does not arise for decision making, at this stage of the

proceeding, and more so, when the said financial

institutions are not parties to the proceeding. This

aspect of the matter may arise for decision making on

C.A. No.437/13 in Co.P. No.122/12

and connected cases

47

the winding-up of the company, after an investigation

by the Official Liquidator.

VII) RE – PUBLIC ANNOUNCEMENT:

42. The public announcement, for short ‘PA’

under Regulation 15(1) of the SEBI (substantial

acquisition of shares and take overs) Regulations, 2011,

dated 9.11.2012 Annexure-P1 to the statement of

objections, is an open offer to the public shareholders

for acquisition of upto 37,785,214 equity shares of USL

constituting 26% of the share capital, for short ‘Target

company’, by Relay B.V. together with DIAGEO PLc and

others, acting in concert, at a price of Rs.1,440/- per

equity share. The underlining transaction for the open

offer, it is said, is:

(A) the Share Purchase Agreement (SPA) of even date

between relay B.V. and DIAGEO with the applicant,

amongst others for acquisition of 25,226,839 equity

shares constituting 17.4% shares in USL, whereunder

C.A. No.437/13 in Co.P. No.122/12

and connected cases

48

applicant together with its subsidiary King Fisher

Finvest India Limited for short ‘KFL’ have agreed to sell

19,536,648 equity shares from out of 23,577,293

representing 18% of equity shares in USL held by the

applicant and 12,676,342 being 9.7% of equity shares

held by KFL. However, the footnote therein reads thus:

“NOTES-

1) xxxxx

2) In terms of the SPA, United Breweries (Holdings)

Limited and King Fisher Finwest India Limited

have agreed to sell an aggregate of 16,716,987

equity shares of USL to the acquirer and the split

between them shall be determined closer to the

completion of the SPA. Currently, United

breweries (Holdings) Limited intends to sell

9,070,595 equity shares and Kingfisher FinWest

India Limited intends to sell 7,646,392 equity

shares.”

C.A. No.437/13 in Co.P. No.122/12

and connected cases

49

B) The preferential allotment agreement (PAA) of even

date between relay B.V. and DIAGEO with USL is to

subscribe to 14,532,775 equity shares (preferential

shares) being 10% of the shares in USL on a preferential

basis at Rs.10/- per share on payment in cash.

C) The Share Holders Agreement (SHA) of even date is

between the same parties, whereunder, the applicant

and its wholly owned subsidiary KFL have agreed,

conditionally, to sell additional shares of USL to Relay

B.V. at the price of Rs.1,440/- per equity shares in the

event preferential allotment does not complete and

Relay holds less than 25.1% of the shares in USL after

taking into account equity shares of USL acquired

under the open offer, under SPA or in any other manner

and accordingly the public announcement would stand

modified.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

50

43. The PA further discloses that after the

acquisition of shares the proposed share holding would

be 77,544,828 equity shares representing 53.4% of USL

shares on emerging voting capital.

44. The share holding pattern of USL as disclosed

in Annexure-P2 to the statement of objections discloses

that from out of 20,573,968 shares representing 15.73%

held by the applicant, 20,005,235 shares representing

15.30% are encumbered, while KFL though holds

1,26,76,342 shares representing 9.69%, nevertheless

1,23,12,892 shares representing 9.41% are

encumbered.

45. Indeed the public offer is said to have failed

since none of the public shareholders offered to sell

their shares in USL at 1,440/- per equity shares, which,

apparently does not necessarily mean that the SPA, the

PPA and SHA are rendered void, as submitted by the

C.A. No.437/13 in Co.P. No.122/12

and connected cases

51

learned counsel for the respondents, more so, in the

light of the said agreements being independent of the

outcome of the public offer, as discernable from the PA.

46. Having scrutinized the terms and conditions

of the SPA, a copy of which is placed before court,

material particulars as set out therein are reflected in

the PA and regard being had to the term of

confidentiality, the imprimatur of the competition

Commission of India on 26.2.2013 Annexure-A, the

Securities and Exchange Board of India on 31.1.2013

Annexure-B and the Reserve Bank of India on

21.3.2013 Annexure-C, it cannot but be said that no

prejudice is caused to the respondent by not being

furnished with a copy of the SPA. The contention to the

contrary is without merit. What merits consideration is

the fact that permission for sale of shares numbering

13,612,591 of USL are encumbered/pledged in favour of

reputed financial institutions, for securing loans to

C.A. No.437/13 in Co.P. No.122/12

and connected cases

52

carry on the applicant’s business, as indicated in the

Annual report for the financial year 2011-12.

47. Keeping in mind the fact that more than

13,612,591 equity shares of USL were pledged to raise

loans to carry on business of the applicant as disclosed

in the annual report 2011-12 and extracted at

paragraph 31 supra, the submission of the learned

Counsel for the respondent that the shares of USL held

by the subsidiaries of the Applicant and not that

belonging to the applicant be sold to wipe out the

secured liabilities, though the split between them is to

be determined closer to the completion of the ‘SPA’,

pales into insignificance. The applicant is the holding

company while KFL is its subsidiary and in the

circumstances, more appropriately the permission to

sell 13,612,591 equity shares and the pledge of the

shares as set out in the Annual report 2011-12 it does

not matter much over the number of shares of USL held

C.A. No.437/13 in Co.P. No.122/12

and connected cases

53

by the applicant required to be sold in terms of the

DIAGEO transaction under the SPA. The further

submission of the learned counsel that three million

equity shares of USL held by KFL is encumbrance free

and therefore, may be put to sale under the SPA is

without merit, since as noticed supra out of 1,26,76,342

equity shares of USL held by KFL 1,23,12,892 equity

shares are encumbered (as disclosed in Annexure-P2 to

the statement of objections).

VIII. RE-PRICE PER EQUITY SHARE:

The price of Rs.1,440/- per equity share of USL on

9.11.2012 the date of SPA, PPA and SHA and the issue

of PA, it is submitted, is far less than the true value of

the share which is presently hovering around

Rs.2,200/- is without merit. A copy of the historical

price data for the equity share of USL as quoted on the

National Stock Exchange Limited for India for the period

from 25.4.2012 to 30.4.2013, furnished by the learned

C.A. No.437/13 in Co.P. No.122/12

and connected cases

54

senior counsel for the applicant, discloses that as on

25.4.2012 one equity shares of USL closed at Rs.737.60

and on 9.11.2012 closed at Rs.1,360.50 and thereafter

on the increasing trend closed at Rs.2210.95 on

30.4.2013, while on 8.5.2013 it closed at Rs.2324.10.

Therefore, the DIAGEO transaction entered into on

9.11.2012 for sale of equity shares of USL at a price of

Rs.1440/- per equity share was higher than

Rs.1360.50 per equity share as closed on the National

Stock Market on the said date.

IX. RE.IMMOVABLE PROPERTY VALUATION REPORT:

48. There is considerable force in the submission

of the learned Counsel for the respondent that the

valuation report of H.S.Nagaraja and Assts over

immovable properties belonging to the applicant suffers

from inadequacies of relevant material constituting

substantial legal evidence in support of valuation. It is

not known as to what is the basis or foundation to

C.A. No.437/13 in Co.P. No.122/12

and connected cases

55

arrive at the value of the properties. Hence the report is

rejected.

X. RE-ALLEGATION THAT APPLICANT IS COMMERCIALLY INSOLVENT:

49. It is lastly pointed out that the contingent

liabilities of the applicant, more appropriately

guarantees extended by the applicant on behalf of

subsidiaries, Banks, financial institutions and others

and the long terms borrowings, both secured and

unsecured is around Rs.10,000/- crores as disclosed in

the annual report 2011-12, to submit that the applicant

is not in a position to repay its debts and therefore

allowing the application and permitting the sale

transaction of shares is detrimental to the interest of

the respondents. Regard being had to the fact that

undisputedly applicant has immovable properties,

which are secured against loans extended by reputed

financial institutions and on their clearance would

C.A. No.437/13 in Co.P. No.122/12

and connected cases

56

become freehold properties, while though the report of

M/s Grant Thorton is, in my opinion, an exaggeration,

nevertheless, it cannot be presumed that the applicant

is commercially insolvent, so as to disentitle the

Applicant to a permission to sell 13,612,591 shares.

XI. RE-ALLEGATION THAT SPA, PPA & SHA ARE DETRIMENTAL TO THE INTEREST OF CREDITORS:

50. Regard being had to the annual report 2011-

12 of the applicant and keeping in mind that loans were

raised by pledging excess of 13,612,591 equity shares of

USL much before the filing of the company petitions for

winding up and that the monies secured as loans are

disclosed to be put to use for carrying on the business

of the applicant, coupled with the secured creditors

having extended their consent for the sale, as also the

permission of the concerned authorities, it cannot be

said that the SPA, PPA and SHA are detrimental to the

interest of the respondents. In my opinion, paying off

C.A. No.437/13 in Co.P. No.122/12

and connected cases

57

the debts of the secured creditors from out of the sale

proceeds of the sale of shares under the DIAGEO

transaction is in the best interest of the secured

creditors in particular to those set out in the annual

report 2011-12 and as extracted supra at paragraph

No.31 supra.

51. Keeping in mind the principles of law in the

matter of exercise of discretion under Section 536(2) of

the Act as extracted supra, and applying the same to

the facts and circumstances of this case, the DIAGEO

transaction, in my opinion is genuine and bonafide and

for the purpose of promoting the interest of the

company, its creditors, as also the respondents who

have come up in the winding-up petitions. The fall and

ebb in the share price are on account of several factors

and in this case the run up in the share price from

Rs.737.80 as on 25.4.2012 and its fall till about

12.7.2012 whereafterwards a steady increase in the

C.A. No.437/13 in Co.P. No.122/12

and connected cases

58

price to Rs.1,360.50 as on 9.11.2012 the date of the

DIAGEO transaction, thereafter, has left a value

enhancement to Rs.2324.10 per share as on 8.5.2013.

This price run up is attributable to the DIAGEO

transaction, regard being had to, the said company

being also one of the distillery having joined hands with

the applicant also commanding global leadership as the

worlds largest Distilled Spirit marketer. The

transaction, it appears is likely to enhance the business

opportunities of the applicant. The apprehension of the

applicant that if the DIAGEO transaction is frustrated

there is a strong possibility that the price of USL share

would crash, possibly below Rs.737/- per equity share

causing enormous loss of value to the detriment of the

applicant and its creditors, is well founded.

XII. RE-UTILIZATION SUMMARY:

52. The summary of utilization of proceeds from

DIAGEO transaction is perse unacceptable in the

C.A. No.437/13 in Co.P. No.122/12

and connected cases

59

absence of actual amounts received as loans, interest

applied and the amounts due on the date of payment

and therefore, it is too far fetched for the applicant to

expect the court to conclude that out of Rs.1960.21

crores there would be a net in-flow of Rs.1,714.79

crores from out of which loans to an extent of

Rs.1595.63 crores are to be repaid leaving a net surplus

of Rs. 119.16 crore. Therefore, there is a need to direct

the applicant to place on record the audited accounts

relating to amounts due and payable to the secured

creditors, more fully mentioned at paragraph No.31

supra and as disclosed in the annual returns 2011-12.

As regards the payment of dues to such of those

persons/institutions mentioned in paragraph 39 supra,

who do not find place in the disclosure in the annual

report 2011-12 of the applicant, no payments can be

made from out of sale proceeds until after filing

necessary application, an investigation thereto and an

order of this court.

C.A. No.437/13 in Co.P. No.122/12

and connected cases

60

53. Company petition 57/12 filed by IAE

International Aero Limited is for recovery of Rs.168

crores; COP 121/12 filed by RRPF Engine Leasing

Limited, is for recovery of Rs.2.92 crores: cop 122/12

filed Rolls-Royce & Partners Finance Limited is for

recovery of Rs.57.18 crore; 185/12 filed by Avions De

Transport Regional G.I.E., is for recovery of Rs.92.58

crores and COP 248/12 filed by B.N.P. Paribas is for

recovery of Rs.145.91 cores.

Regard being had to the totality of circumstances,

ends of justice would be met by the following:

ORDER

I) The applications are allowed in part.

II) The applicant is permitted to:

a) sell 13,612,591 equity shares of USL held by it, to Relay B.V., and DIAGEO PLc and others acting in concert, at a sale price of Rs.1,440/- per equity share;

b) from out of the sale proceeds:

C.A. No.437/13 in Co.P. No.122/12

and connected cases

61

i) to make payment of dues to the secured

creditors disclosed in its annual report 2011-12 as extracted at paragraph 31 supra;

ii) to expend reasonable sums of money towards legal expenses; iii) to pay taxes incidental to the sale transaction;

III) to submit to court the audited statement of accounts over repayments, expenses and taxes, incurred as directed supra, by the 22nd July, 2013;

IV) The applicant is directed to:

a) deposit Rs.250/- crores (rupees Two

Hundred and Fifty crores only) in this

court immediately on the conclusion of the transaction and receipt of sale consideration which the registry is directed to keep in a term deposit in a Nationalised Bank for an initial period of one year;

b) retain the balance of the sale

consideration without deploying the same for its business activity, subject to further orders;

c) refrain from creating

pledge/hypothecation/charge/

C.A. No.437/13 in Co.P. No.122/12

and connected cases

62

encumbrance over its movable and immovable properties pending disposal of the company petitions.

Sd/-

JUDGE ln/sma