By K. VAITHEESWARAN ADVOCATE & TAX CONSULTANT. Indirect tax proposals are estimated to generate...

42

2010 Analysis of Indirect Tax Proposals by K. VAITHEESWARAN ADVOCATE & TAX CONSULTANT BUDGET

-

date post

19-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of By K. VAITHEESWARAN ADVOCATE & TAX CONSULTANT. Indirect tax proposals are estimated to generate...

2010

Analysis of Indirect Tax Proposals

by

K. VAITHEESWARANADVOCATE & TAX CONSULTANT

BUDGET

GENERAL

Indirect tax proposals are estimated to generate Rs.46,500 crores.

Significant number of changes in rate, exemption structure, etc.

No attempt to address pending issues raised by chambers of commerce.

Usual dosage of retrospective amendments.

EXCISE DUTY

RATE STRUCTURE

Excise duty rates for non-petroleum products increased from 8% to 10%.

Cement attracts duty of 10% if the RSP exceeds Rs.190/- per 50 kg bag or Rs.3800/- per tonne.

Increase of duty by 2% for large cars, multi-utility vehicles and sports utility vehicles and tobacco products.

Clean energy cess on coal lignite and peat produced in India.

RATE STRUCTURE

Exemption for supari, menthol by-products, toy balloons, articles of bedding made of quilt.

Goods supplied to mega power products exempted.

Re.1 per litre on petrol and diesel. 4% duty on corrugated boxes and

cottons. Amendments to SSI notifications. 4% on umbrellas, umbrella parts.

THE UMBRELLA STORY

Umbrella exempted in Budget 1989 Exemption withdrawn in Budget 1994 Umbrellas exempted in Budget 1997 Umbrellas taxed through Budget 2002 Umbrellas were exempt from excise duty

Budget 2003. Umbrellas attracted 16% duty in Budget

2006. Duty on umbrellas reduced to 8% in Budget

2007. Duty reduced to 4% in Budget 2010.

DEEMED MANUFACTURE

In relation to products of headings 6802 and 6810, the process of cutting or sawing or sizing or polishing or any other process, for converting of stone blocks into slabs or tiles, shall amount to “manufacture”.’;

Amendment nullifies decision of the Tribunal at the stage of stay in the case of Oriental Trimex Ltd.

MRP BASED TAXATION

Parts, components and assemblies of automobiles is replaced with parts, components and assemblies of vehicles including chassis fitted with engines falling under Chapter 87 excluding vehicles under 8712, 8713, 8715 and 8716.

Rates of abatements revised for certain products.

FINANCE BILL PROPOSALS

Settlement commission scope to be widened.

No penalty if excise duty and interest paid before issue of Show Cause Notice in cases which do not involve fraud, etc.

CUSTOMS

RATE

Peak rate unchanged 5% basic customs duty on crude petroleum. Increase from 2.5% to 7.5% in respect of

petrol and high speed diesel. Increase from 5% to 10% in respect of other

specified petroleum products. Fueling inflation ? Exemptions in respect of certain products from

4% duty under Sec. 3(5) of the Customs Tariff Act.

Project import status for monorail, coal storage, mechanised handling systems in warehouses.

RATE

CVD on MRP basis for goods falling under Medicinal and Toilet Preparations (Excise Duty) Act.

Increase in rate of duty in respect of precious metals.

Electrical energy supplied from SEZ to DTA and non-processing areas of DTA would attract duty of 16% with retrospective effect from 26.06.2009.

EXEMPTION

Goods imported in pre-packaged form and intended for re-sale exempt from 4% duty subject to law requiring declaration of MRP.

Exemption also extended to mobile phones, watches and readymade garments from 4% duty.

For all other goods exemption in the form of refund in terms of Notification No.1/2007 is retained.

SERVICE TAX

GENERAL

Service tax rates unchanged FM had the option of covering all

other services and chose not to exercise the option.

Service tax proposals are expected to generate Rs.3,000 crores.

8 new services proposed.

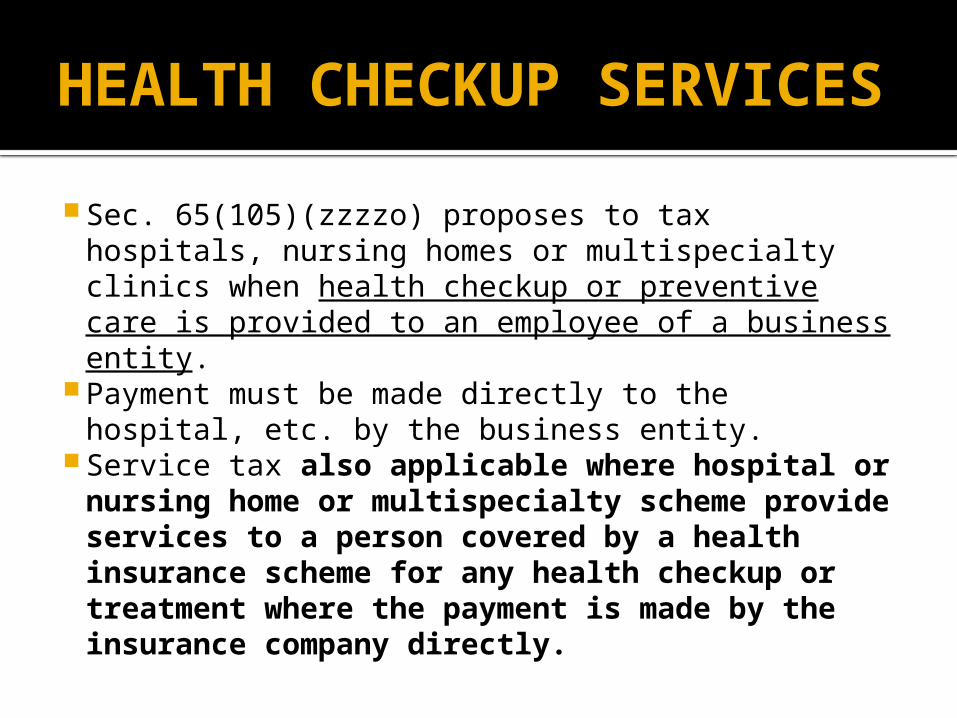

HEALTH CHECKUP SERVICES Sec. 65(105)(zzzzo) proposes to tax hospitals,

nursing homes or multispecialty clinics when health checkup or preventive care is provided to an employee of a business entity.

Payment must be made directly to the hospital, etc. by the business entity.

Service tax also applicable where hospital or nursing home or multispecialty scheme provide services to a person covered by a health insurance scheme for any health checkup or treatment where the payment is made by the insurance company directly.

HOSPITALS

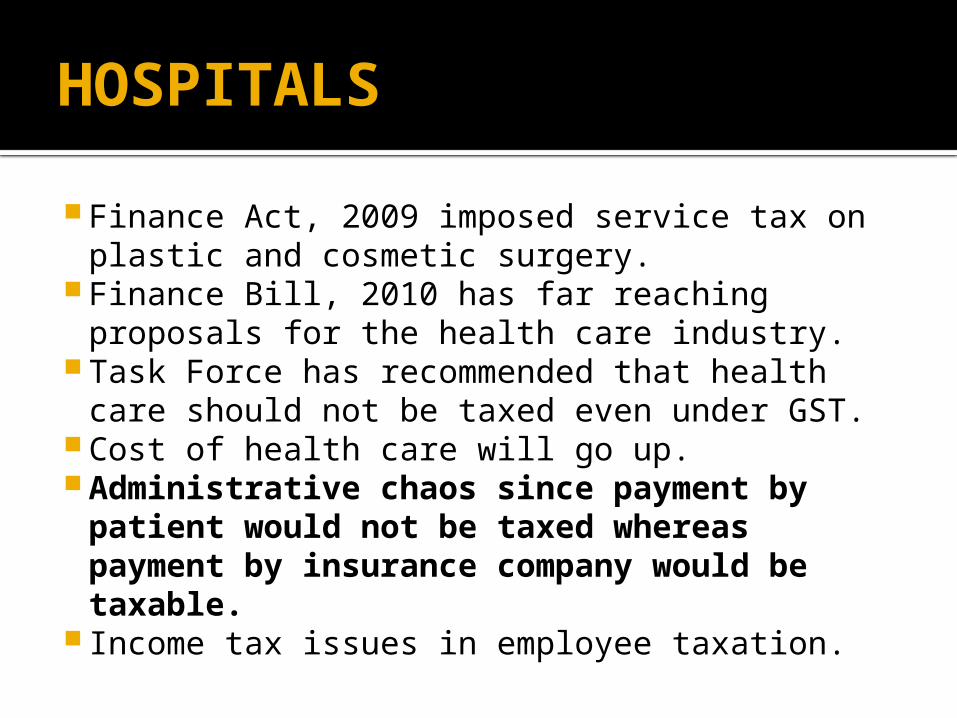

Finance Act, 2009 imposed service tax on plastic and cosmetic surgery.

Finance Bill, 2010 has far reaching proposals for the health care industry.

Task Force has recommended that health care should not be taxed even under GST.

Cost of health care will go up. Administrative chaos since payment by

patient would not be taxed whereas payment by insurance company would be taxable.

Income tax issues in employee taxation.

GAMES OF CHANCE

Sec. 65(105)(zzzzn) proposes to tax services for promotion, organizing or in any other manner assisting in-organizing games of chance, including lottery, bingo or lotto whether or not conducted through internet or other electronic networks.

Explanation to BAS definition inserted by Finance Act, 2008 deleted.

MEDICAL RECORDS

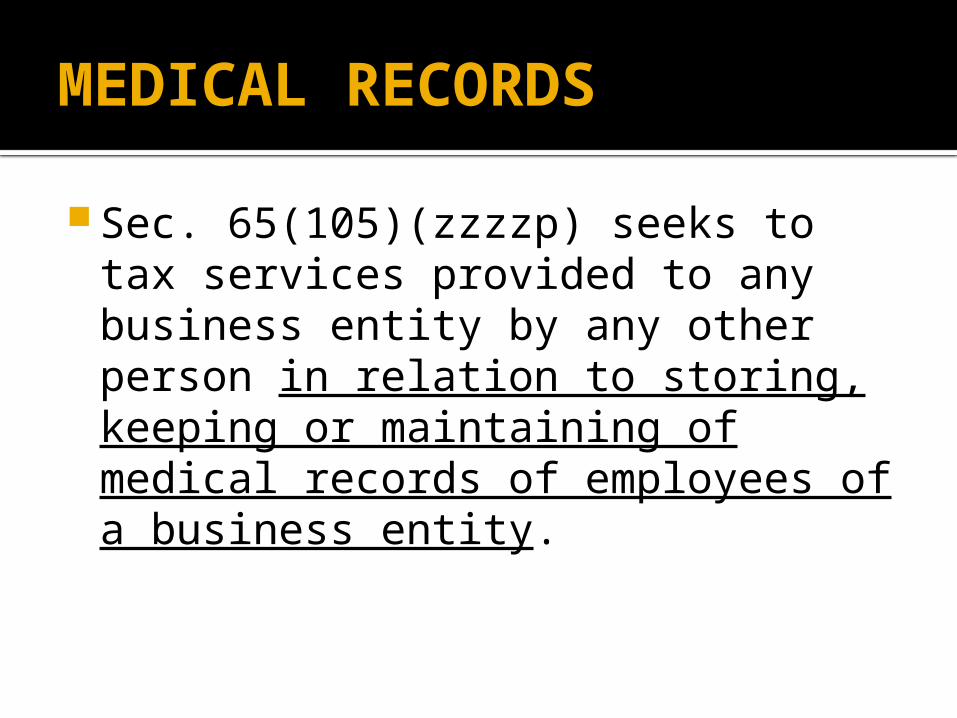

Sec. 65(105)(zzzzp) seeks to tax services provided to any business entity by any other person in relation to storing, keeping or maintaining of medical records of employees of a business entity.

BRAND PROMOTION

Sec. 65(105)(zzzzq) seeks to tax promotion or marketing of a brand of goods, service, event or endorsement of name including a trade name, logo or house mark of a business entity by appearing in advertisement and promotional events or carrying out promotional activity.

Service is taxable whether provided to a business entity or otherwise under a contract.

Taxation of brand ambassadors.

BRAND PROMOTION

Celebrity endorsements Team endorsements Applicability of Business Auxiliary Service Payments to celebrities who are based outside

India. Endorsements in films ? Brand ambassadors used by Governments ? What is the difference between ‘mere acting’

and ‘endorsement’ ? Asin acting in Hayagriva and Asin appearing in

Miranda advertisements.

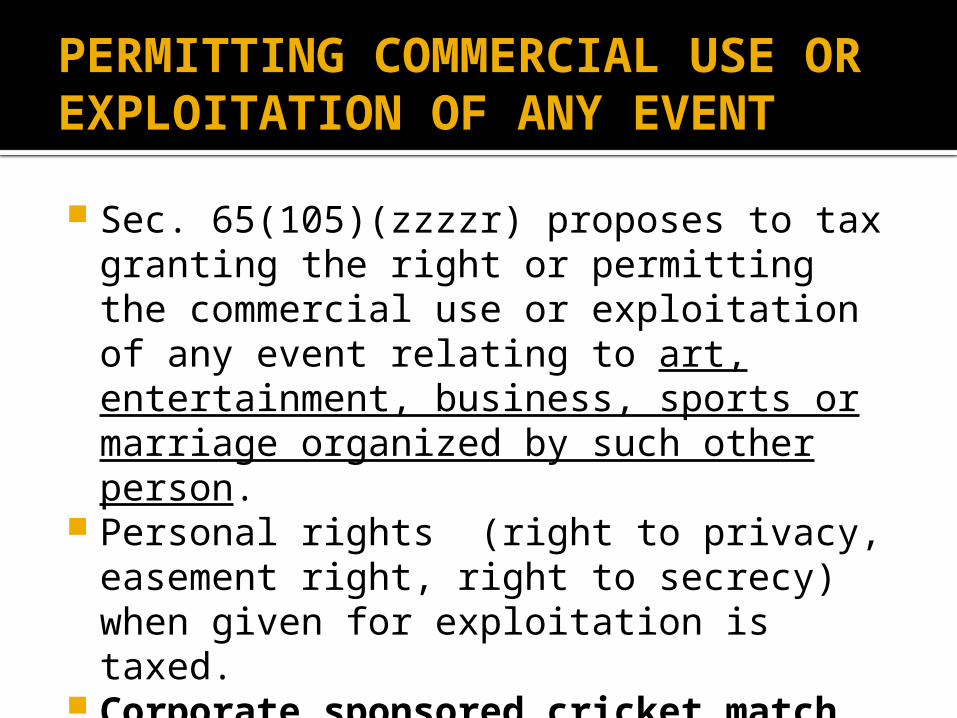

PERMITTING COMMERCIAL USE OR EXPLOITATION OF ANY EVENT Sec. 65(105)(zzzzr) proposes to tax

granting the right or permitting the commercial use or exploitation of any event relating to art, entertainment, business, sports or marriage organized by such other person.

Personal rights (right to privacy, easement right, right to secrecy) when given for exploitation is taxed.

Corporate sponsored cricket match or concert; film award events, celebrity marriages, beauty contests.

PERMITTING COMMERCIAL USE OR EXPLOITATION OF ANY EVENT Generally these rights are given to

companies or broadcasting agencies and video producers.

‘Parattu Vizha’ Film release functions or preview shows

or audio release IPL Vijay TV telecasting celebrity marriages Endiran audio release function ?

ELECTRICITY EXCHANGES Sec. 65(105)(zzzzs) seeks to tax an

electricity exchange by whatever name called approved by the Central Electricity Regulatory Commission under the Electricity Act, 2003 in relation to trading, processing, clearing or settlement of spot contracts, term ahead contracts, seasonal contracts or any other electricity related contracts.

Assessee is the electricity exchange

COPYRIGHTS

Sec. 65(105)(zzzzt) seeks to tax temporary transfer or permitting use or enjoyment of any copyright other than original literary dramatic, musical and artistic work.

Copyrights of cinematographic films and sound recordings are getting taxed.

Film producers who give this rights temporarily for a consideration is taxable.

Royalty payments on imported and indigenously produced films given by the producer to the distributor is taxable.

Companies distributing music, owners of copyrights and films would be taxable.

COPYRIGHTS

Individual artists, composers and performers will not be taxable as their copyrights falls under Sec. 13(a) of the Copyright Act.

The Madras High Court in the case of A.V.Meiyappan Vs. Commissioner of Commercial Taxes (1967) 20 STC 115 has held that the term ‘goods’ include copyright and upheld by Supreme Court in Joint Commercial Tax Officer Vs. Smt. Pankajammal (1991) 80 STC 391.

In terms of G.O.No.Ms No. 61 dated 31.03.2000 – Notification No.II(1)/CT/22(e-2)/2000, exemption is available in respect of tax payable by any dealer under Section 3 A of the TNGST Act on the right to use exposed cinematograph films (feature films).

PREFERRED LOCATION SERVICES

Sec. 65(105)(zzzzu) proposes to tax services provided or to be provided to a buyer of a residential or a commercial complex or any other person authorised by such builder for providing preferential location or development of such complex.

Charges for ‘next to mall, beach facing, east facing, vastu enabled, preferred floor, preferred door number’ will be taxable.

Charges for development charges for parks, pipelines, access, common lighting, backup power, fire fighting, etc. taxable.

Parking space specifically excluded.

AMENDMENT OF EXISTING SERVICES

AIRPORT SERVICES & PORT SERVICES

Amendment to specifically provide that all services provides entirely within the port or airport would fall under the respective port services or airport services.

Sec. 65A has no application to any service when the same is rendered wholly within the port or airport.

Litigation in the past.

AIRTRAVEL

Sec. 65(105)(zzzo) is proposed to be amended to expand the levy to all types of air travel in scheduled or non-scheduled air transport.

Tax is on the air craft operator. Originally only international journey and that too

business class or first class was taxed. Possible exemptions and abatements after enactment

of law. Air travel to become costlier. Cenvat credit for passenger ? Cenvat credit for aircraft operator ? Airlines is a loss making business world over and Indian

companies are going through a very rough patch.

OTHER AMENDMENTS

Sec. 65(105)(zzzze) being amended in order to provide for tax on software services whether or not used in the course or furtherance of business or commerce.

Definition of Sponsorship Services amended. Sports sponsorship is also taxable. Auctioneer services amended to provide that there will

not be any tax only when Government property is auctioned.

Amendment to ULIP service to provide that value shall be actual amount charged by insurer for management of funds or maximum amount of fund management charges fixed by IRDA whichever is higher.

CONSTRUCTION SERVICES The word ‘service’ stands omitted from

Sec.65(105)(zzq) – commercial or industrial construction.

Construction / construction of a complex intended for sale by the builder before or during or after construction or shall be deemed to be a service provided by the builder to the buyer

Concept of ‘self-service’, legislatively nullified. No service tax if entire payment for the

property is paid by the buyer only after completion of the construction including certification by the local authorities.

CONSTRUCTION SERVICES Amendment in the form of an insertion

of explanation to the definition of taxable service pertaining to construction of complex /commercial construction.

No amendment to works contract service.

Circular No.108. Amendment is prospective. Impact for the past period ?

EXEMPTIONS

Taxes charged by Governments on air passenger. Commissioning installation of mechanized food grain

handling systems, equipment for coal storage, machinery equipment for processing of agricultural, apiary, horticultural, diary, poultry, aquatic, marine or meat products.

Packaged IT software, pre-packed in retail packages for single use provided excise duty or customs duty has been paid on the entire amount received from the buyer.

GTA exemption to food grains and pulses. Indian News Agencies under BAS and online database

services. Central and State seed testing laboratories and agencies. Transmission of electricity – Notification No.11/2010.

EXPORT OF SERVICES – Notification No.6/2010 w.e.f. 27.02.2010 Mandap services shifted to first category. Chartered Accountant, Cost Accountant, Company

Secretary services shifted to third category. Rule 3(2)(a) is deleted. (This condition provided

that service must be provided from India and used outside India)

India includes the installations, structures and vessels located in the Continental Shelf of India and Exclusive Economic Zone of India for the purposes of prospecting or extraction or production of mineral oil and natural gas and supply thereof.

TRANSPORTATION OF GOODS BY RAIL

Finance Act, 2009 Issue of product oriented exemptions Specific abatement Withdrawal of all Notifications Notification exempting Government Railways –

No.33/2009 dated 01.09.2009. Notification No.7/2010 dated 27.02.2010

has rescinded Notification No.33/2009. Notification No.8/2010 provides for

product oriented exemption. Notification No.9/2010 provides for

abatement.

FM’s SPEECH

While formulating them, I have been guided by the principles of sound tax administration as embodied in the following words of Kautilya – thus a wise collector shall conduct the work of revenue collection in a manner that production and consumption should not be injuriously affected; financial prosperity depends upon public prosperity; abundance of harvest and prosperity or commerce among other things.

Para 117 of the Finance Minister’s speech

RETROSPECTIVE AMENDMENTS

Finance Bill 2010 proposes to amend Sec.65(105)(zzzz) in order to provide the renting or any other services in relation to renting is taxable.

An attempt to nullify Delhi High Court decision when the matter is even pending before the Supreme Court.

Vacant land given for construction where the structure at a latter stage is used for furtherance of business or commerce is also taxable.

Amendment is with retrospective effect from 01.06.2007.

Validation amendment through Sec.76 of the Finance Bill. Also facilitates recovery of interest and penalty or fine or other charges which may not have been collected.

RETROSPECTIVE AMENDMENTS

Sec. 65(105)(zzc) dealing with commercial training or coaching service is proposed to be amended with retrospective effect from 01.07.2003.

The Explanation provides that the commercial training or coaching centre shall include any centre or institute by whatever name called whether training or coaching is imparted for consideration, whether or not it is registered as a trust or society, etc. and carrying on activity with or without profit motive.

A number of Tribunal judgments nullified with retrospective effect.

How will the institute now recover the tax from the students for the past period ?

CENVAT CREDIT

Amendments to Rule 3(5) dealing with removal of capital goods after being used.

SSI can take the entire duty on capital goods as credit in the first year itself.

Jigs, fixtures, etc. can be removed to the location of another manufacturer for production of goods.

Proportionate credit reversal formula can be applied for the past period if case is pending. Retrospective amendments to various Rules to provide relief.

Amendments to Rule 15 as a measure of harmonization.

GST

I have been informed that the Empowered Committee of State Finance Ministers has made considerable progress in preparing the roadmap and the design of the GST. Officials from the Central Government have also been associated in this exercise. I am glad to inform the House that, through their collaborative efforts, they have reached an agreement on the basic structure in keeping with the principles of fiscal federalism enshrined in the Constitution. I compliment the Empowered Committee of State Finance Ministers for their untiring efforts. The broad contour of the GST Model is that it will be a dual GST comprising of a Central GST and a State GST. The Centre and the States will each legislate, levy and administer the Central GST and State GST, respectively. I will reinforce the Central Government’s catalytic role to facilitate the introduction of GST by 1st April, 2010 after due consultations with all stakeholders. (Para 85 of the Finance Minister Shri Pranab Mukherji’s speech on 06.07.2009)

GST

On Goods and Services Tax, we have been focusing on generating a wide consensus on its design. In November, 2009 the Empowered Committee of the State Finance Ministers placed the first discussion paper on GST in the public domain. The Thirteenth Finance Commission has also made a number of significant recommendations relating to GST, which will contribute to the ongoing discussions. We are actively engaged with the Empowered Committee to finalise the structure of GST as well as the modalities of its expeditious implementation. It will be my earnest endeavour to introduce GST along with the DTC in April, 2011. – Para 26 of the Finance Minister Mr. Pranab Mukherji’s speech on 26.02.2010

![[XLS] catalog.xls · Web viewTitles English New Thiraigalukku Appal kzk-0148 1994, 2000 Verppattru kzk-0149 Kaal Mulaiththa Manam S. Vaitheeswaran kzk-0150 Kasthuri Thilagam Baraneedharan](https://static.fdocuments.net/doc/165x107/5afdaf777f8b9a864d8de47b/xls-viewtitles-english-new-thiraigalukku-appal-kzk-0148-1994-2000-verppattru.jpg)