Business Overview - The Hong Kong Mortgage Corporation …The Hong Kong Mortgage Corporation Limited...

24

Business Overview

Transcript of Business Overview - The Hong Kong Mortgage Corporation …The Hong Kong Mortgage Corporation Limited...

Business Overview

Business Overview

The Hong Kong Mortgage Corporation Limited Annual Report 2016 33

Performance Highlights

Themajorachievementsof theCorporation for theyearincluded:

• purchasingaboutHK$206millionofloanassets

• helpinghomebuyersborrowa totalofHK$24.6billionmortgage loans through theMortgage InsuranceProgramme(MIP)

• approving1,525applicationssince the launchof theReverseMortgageProgramme(RMP),withanaveragepropertyvalueofaroundHK$5.1million

• approving 11 applications since the launch of thePremiumLoanInsuranceScheme(PLIS),withanaveragepropertyvalueofaroundHK$3.9million

• approving loans totallingHK$45.8millionunder theMicrofinanceScheme(MFS)since its inceptionanduptotheendof2016tobusinessstarters,self-employedpeoplefromdifferentbackgroundsandprofessionsandthosewanting toachieveself-improvement througheducationandtraining

• withthesupportof theGovernment, furtherextendingtheapplicationperiod for the80%guaranteeproductundertheSMEFinancingGuaranteeScheme(SFGS) foroneyear to28February2017.Sincethe launchof theSFGS in January2011, theCorporationhadapprovedmorethan11,700applicationsforatotalloanamountofapproximatelyHK$46.5billion,ofwhichmorethan11,400applications fora total loanamountofaboutHK$45.6billionwereapprovedwith80%guaranteeprotection.More than7,200 localsmallandmediumenterprises(SMEs) andnearly190,000 relatedemployeeshavebenefitedundertheSFGS

• issuingHK$16.2billionofdebtsecurities (withmaturityof1-yearandabove) inacost-effectivemanner, thuspromoting thedevelopmentof the localdebtmarketandmaintainingtheHKMC’spositionasoneofthemostactiveissuersinHongKong

• safeguardingexcellent credit quality,withover-90-day delinquency ratios of 0.01% for themortgageinsuranceportfolio,0%fortheSMEguaranteeportfolio(excludingthe80%productundertheSFGS),0.03%fortheHongKongresidentialmortgageportfolio (industryaverageof 0.03%), 2.20% for themicrofinance loanportfolioand0.04%acrossallassetclassesasat31December2016

• maintaining theHKMC’s long-term foreignand localcurrencyratingsofAAAbyStandard&Poor’s(S&P)andAa1byMoody’sInvestorsService,Inc.(Moody’s).

TheCorporationmaintainedasolid financialposition for2016:

• profitattributabletoshareholdersofHK$604million

• netinterestmarginof1.0%

• returnonassetsof1.1%

• returnonshareholders’equityof6.8%

• cost-to-incomeratioof30.8%

• capitaladequacyratioof21.3%,wellabovetheminimumrequirementof8%stipulatedbytheFinancialSecretary.

The Hong Kong Mortgage Corporation Limited Annual Report 201634

Business Overview

Market Overview

General Economic ConditionsIn2016,globaleconomicgrowthremainedmodest.TheUSreportedgooddomesticgrowthwhilerecovery inEuropeandJapanremainedsluggish.GlobalmonetarydivergenceagainwidenedwhiletheUSFederalReservecontinuedtograduallynormaliseitsmonetarypolicybutthequantitativeeasingprogrammes in theeuroareawereextendedandanewmonetarypolicy framework foradditionaleasingwasintroducedinJapantofendoffdeflationrisks.MarketvolatilitiesheightenedasaresultofthesurprisingoutcomeofBrexitand theUSpresidentialelection. In theregion,growth in China had beenmoderatingwith signs ofstabilisation inthesecondhalfoftheyearonacceleratedinfrastructureandinvestmentactivitieswhereasHongKongeconomysawmodestgrowthon improveddomesticandexternaldemands.Against thisbackdrop,theHongKongeconomygrewmodestlyduring theyearat1.9%year-on-year in real terms,underpinnedbyastrengtheningindomesticdemandand improvement in theexternaldemand.

Property MarketHongKong’spropertymarketcooledoffatthestartoftheyear,withprices fallingonaslowbutsteadybasisandtransactionvolumedroppingtoanall-timelow.Thepropertymarketrecordedarebound innumberof transactions inthesecondquarter followingan improvement inmarketsentiments.Thiswas followedbyan increaseof31% insalesvolumeinthethirdquarter,bringinganaccumulativegrowth of 8.9% for the sixth consecutivemonth inSeptember.DespitetheGovernment’s introductionofnewprudentialmeasures inNovembertocoolpropertyprices,by raising thestampduty to15%forsecond-timehomebuyers, itdidnot leadtosignificantadjustmentpressureonpropertyprices.Thenumberofproperty transactionsin2016slightlydecreasedbyabout2.3%year-on-yearto54,701,whiletheconsiderationof transactionsgainedanalmost2.8%year-on-yearincrement(Figure 1).

Figure 1

Agreements for Sale and Purchase of Residential Building Units

200,000

150,000

100,000

50,000

0

800,000

600,000

400,000

200,000

096 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 16151413

Number

Number Consideration (HK$ million)

HK$ million

Consideration

Source:LandRegistry

Despitethedeclineinthefirstquarterof2016,thevolumeof transactions inbothprimaryandsecondarymarketshas increasedsinceApril. Ingeneral, residentialpropertyprices1recordedanabout7.6%cumulativeincreasein2016,comparedwiththe2.4%increasein2015,andhadsurpassedthe1997peakbyaround79%asattheendof2016(Figure 2).

320

300

280

260

240

220

200

180

160

140

120

100

80

40

60

300

320

280

260

240

220

200

180

160

140

120

100

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 161514

Jan-13

Apr-14

Apr-13

Jul-1

4

Jan-15

Jul-1

5

Oct-14

Oct-15

Jan-14

Apr-15

Jan-16

Jul-1

6

Apr-16

Oct-16

Oct-13

Jul-1

3

Source:RatingandValuationDepartment

Figure 2

Private Domestic Price Index (1999 = 100)

1 Source:ThePrivateDomesticPrice Indexpublishedby theRatingandValuationDepartment

The Hong Kong Mortgage Corporation Limited Annual Report 2016 35

Mortgage MarketOverall,themortgagerateinHongKongstayedlowin2016.TheBestLendingRates(BLRs)remainedunchangedat5%and5.25%throughouttheyear.TheHongKong InterbankOfferedRates(HIBORs)remainedlowwiththeone-monthHIBORfloatingintherangeof0.21%–0.29%fromJanuarytoOctoberintermsofperiodaverage2.HIBORroseto0.37%inNovemberandsurgedtoahighof0.61%inDecember.

During the year,mortgage lending growth showed aslowing trend,with the total outstanding valueof allresidentialmortgage loans risingmoderatelyby4.1%toHK$1,165.2billion.Thegrossvalueofnew loansdrawndown3decreasedby10.8%year-on-yearin2016,comparedwiththegrowthrateof14%in2015(Figure 3).

Figure 3

New Residential Mortgage Loans Drawn Down

100,000

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

04030201 0805 0906 1007 11 12 1613 14 15

HK$ million

Q1 Q2 Q3 Q4

Source:HongKongMonetaryAuthority

AsHIBOR remainedat a low level formostmonthsoftheyear,HIBOR-basedmortgagesturnedout tobemorereceptivetoborrowers.94.9%ofnewmortgageloanswerepricedwith reference toHIBOR inDecember2016.TheproportionofBLR-basedmortgagesdeclineddrasticallyfrom11.4% in January to2.5% inDecember (Figure 4).Theshareoffixed-ratemortgageloansalsoexperiencedasignificantdrop,from7.5%inJanuaryto0.8%bytheendof2016.

Figure 4

Pricing of New Residential Mortgage Loans Approved

60%40%20%0% 80% 100%90%70%50%30%10%

With reference to BLROthersFixed rate

With reference to HIBOR

Dec-16Nov-16Oct-16Sep-16Aug-16

Jul-16Jun-16

May-16Apr-16Mar-16Feb-16Jan-16

Dec-15Nov-15Oct-15Sep-15Aug-15

Jul-15Jun-15

May-15Apr-15Mar-15Feb-15Jan-15

Source:HongKongMonetaryAuthority

2 Source:HKMAMonthlyStatisticalBulletin3 Source:HKMA’sMonthlyResidentialMortgageSurvey(HKMA Survey)

The Hong Kong Mortgage Corporation Limited Annual Report 201636

Business Overview

Underastable labourmarketandtheprudentsupervisionofthemortgagelendingsectorbytheHongKongMonetaryAuthority (HKMA ) , the asset quality of residentialmortgage loans remainedexcellent in2016. Theover-90-day delinquency ratio ofmortgage loans stayedbetween0.03%–0.04%throughout theyear,reflectingtheprudentunderwritingstandardsadoptedbybanks.Thecombinedratio,whichtakes intoaccountbothdelinquentand rescheduled loans,also remained low in the rangeof0.03%–0.04%during thesameperiod (Figure 5).AsresidentialpropertypriceshadbeenontherisesinceApril,thenumberofmortgageloans innegativeequitydroppedto4atend-December2016,withanaggregatevalueofHK$11millionrecorded4.

Figure 5

Delinquency Ratio of Residential Mortgage Loans

(%)

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 16151413

Combined Ratio (with Rescheduled Loans)Delinquency Ratio (Overdue > 90 days)

Source:HongKongMonetaryAuthority

Banking-Sector ExposureThetotaloutstandingvalueofmortgage loansforprivateresidentialproperties increased toHK$1,122.3billionattheendof2016(end-2015:HK$1,077.9billion),accountingfor one-fifth of total loans inHong Kong (Figure 6).Adding to this the lending forbuildingandconstruction,alongwithpropertydevelopmentand investment, thevalueofproperty-relatedloanstotalledHK$2,383.1billion,representingabout42%of the total loanbookofbanks.Theoutstandingvalueofmortgage loansforthepurchaseof flats in theHomeOwnershipScheme,PrivateSectorParticipation Scheme and Tenants Purchase SchemeincreasedtoHK$43billionbytheendof2016 (end-2015:HK$41.4billion).

Figure 6

Total Loans and Private Residential Mortgage Loans ofAll Authorized Institutions

Source:HongKongMonetaryAuthority

6,000

5,000

4,000

3,000

2,000

1,000

0

%

40%

35%

30%

25%

20%

15%

10%

5%

09897 99 00 01 02 03 04 05 06 07 08 09 10 11 12 16151413

Total LoansPrivate Residential Mortgage Loans Share of Private Residential Mortgage Loans

HK$ billion

4 Source:HKMASurvey

The Hong Kong Mortgage Corporation Limited Annual Report 2016 37

Asset Acquisition

While theample liquidity in themarkethas led toweakincentivesforbankstooffloadtheirassets,theCorporationispreparedtoprovideliquiditytothemarketasandwhenrequired. In2016,theCorporationacquiredaboutHK$206millionofassets,whichincludedresidentialmortgageloansandotherassets.

Extension of the time-limited 80% guarantee product under the SME Financing Guarantee Scheme (80% SFGS)

Beingpartandparcelofthepackageofsupportmeasuresannounced in the2012–13Budget for localSMEs to tideover theuncertain global economicenvironment, theCorporationpromulgatedthetime-limited80%SFGSbackedby theGovernment’s totalguaranteecommitmentofuptoHK$100billion.The80%SFGSprovides80%guaranteeoneligible loanfacilitiesapprovedbyparticipating lendersatasubstantially loweredguaranteefeerate,whichhelpsSMEsobtain loans forgeneralworkingcapitalorbuyingequipment or assets to support business operations.TheCorporationadministers the80%SFGSonprudentcommercialprinciples.Theguaranteefeesaresetasidetopaydefaultclaimsfromparticipating lendersandout-of-pocketexpensestobeincurredunderthearrangement.Atotalof30authorizedinstitutions(AIs)haveparticipatedintheSFGSaslenders.

In lightof theuncertainexternaleconomicenvironmentandtradeperformance,the80%SFGSwasextendedforatotaloffouryearstotheendofFebruary2017.Inaddition,inabidtoalleviatethefinancingburdenofborrowers,theFinancialSecretaryannounced inthe2016–17Budgetthereductionof theannualguarantee feerates for the80%SFGSby10%.TheFinancialSecretaryalsoannouncedtheremovaloftheminimumannualguaranteefeerateof0.5%forguaranteefeesdueandpayableonorafter1June2016.

The80%SFGShasbeenwell receivedby themarket.Asat31December2016, theCorporationhadapprovedmorethan11,700applications fora total loanamountofapproximatelyHK$46.5billionundertheSFGS.Morethan11,400of theapplications for loansamounting toaboutHK$45.6billionwereapprovedunderthe80%SFGS.Morethan7,200 localSMEsemployingnearly190,000peoplehavebenefitedundertheSFGS.

TheCorporationhasmaintainedongoingdialoguewiththeHongKongGovernment,participating lendersandmarketparticipants inorderto further improvepublicawarenessandrecognitionof theSFGS, inparticular the80%SFGS.Aspartof theongoingSFGScommunicationcampaignand inresponsetotheconstraints facedby localSMEs inaccessingbankcredit, theCorporationhasbeenactivelymeetingwithparticipating lenders, SMEassociations,chambers of commerce andmembers of LegislativeCouncil since the secondquarter of 2016 toenhancetheunderstandingand transparencyof theSFGSand topromotemoreactiveuseofthe80%SFGS.

To broaden the understanding of the SFGS amongpractitioners,theCorporationarrangedaseriesofseminarsformore than 20participating lenders. The seminarsweretofamiliarise lenders’staffmemberswiththeSFGS,coveringboththeapplicationandclaimstages.

TheCorporationhastakenonboardlenders’viewscollectedduring thecommunicationcampaign tosmoothout theSFGSclaimprocess.Amongotherthings, theCorporationhasintroducedadigitaldocumentdepositorywhichallowsparticipating lenders tosubmitclaim-relatedsupportingdocumentsatapplicationstage.Theenhancementhelpsexpedite theSFGSclaimprocessby reducing the timeparticipatinglendersspentoncollectionofdocumentsfromvariousinternaldepartmentsatclaimstage.

The Hong Kong Mortgage Corporation Limited Annual Report 201638

Business Overview

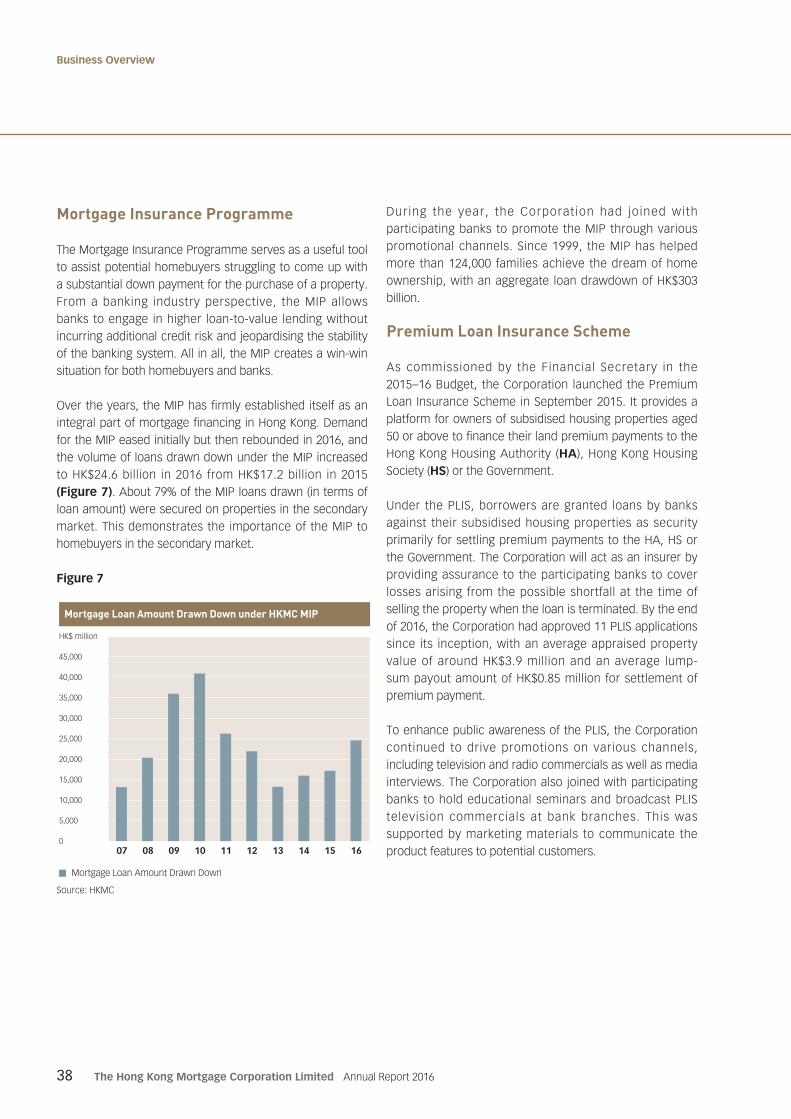

Mortgage Insurance Programme

TheMortgageInsuranceProgrammeservesasausefultooltoassistpotentialhomebuyersstrugglingtocomeupwithasubstantialdownpaymentforthepurchaseofaproperty.Froma banking industry perspective, theMIP allowsbanks toengage inhigher loan-to-value lendingwithoutincurringadditionalcreditriskandjeopardisingthestabilityofthebankingsystem.Allinall,theMIPcreatesawin-winsituationforbothhomebuyersandbanks.

Overtheyears,theMIPhasfirmlyestablisheditselfasanintegralpartofmortgagefinancinginHongKong.DemandfortheMIPeasedinitiallybutthenreboundedin2016,andthevolumeof loansdrawndownundertheMIPincreasedtoHK$24.6billion in2016 fromHK$17.2billion in2015(Figure 7).About79%oftheMIPloansdrawn(intermsofloanamount)weresecuredonpropertiesinthesecondarymarket.Thisdemonstrates the importanceof theMIP tohomebuyersinthesecondarymarket.

Figure 7

Mortgage Loan Amount Drawn Down under HKMC MIP

1607 08 09 10 11 14 151312

45,000

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

Mortgage Loan Amount Drawn Down

HK$ million

Source:HKMC

During the year, the Corporat ion had joined withparticipatingbanks topromote theMIP throughvariouspromotionalchannels.Since1999, theMIPhashelpedmore than124,000 familiesachieve thedreamofhomeownership,withanaggregate loandrawdownofHK$303billion.

Premium Loan Insurance Scheme

As commissioned by the Financial Secretary in the2015–16Budget, theCorporation launchedthePremiumLoan InsuranceScheme inSeptember2015. Itprovidesaplatformforownersofsubsidisedhousingpropertiesaged50orabovetofinancetheirlandpremiumpaymentstotheHongKongHousingAuthority (HA),HongKongHousingSociety(HS)ortheGovernment.

Under thePLIS,borrowersaregranted loansbybanksagainst their subsidisedhousingpropertiesassecurityprimarily forsettlingpremiumpaymentstotheHA,HSortheGovernment.TheCorporationwillactasaninsurerbyprovidingassurance to theparticipatingbanks tocoverlossesarising from thepossibleshortfall at the timeofsellingthepropertywhentheloanisterminated.Bytheendof2016,theCorporationhadapproved11PLISapplicationssince its inception,withanaverageappraisedpropertyvalueof aroundHK$3.9millionandanaverage lump-sumpayoutamountofHK$0.85million forsettlementofpremiumpayment.

ToenhancepublicawarenessofthePLIS,theCorporationcontinued to drive promotions on various channels,includingtelevisionandradiocommercialsaswellasmediainterviews.TheCorporationalso joinedwithparticipatingbanks toholdeducationalseminarsandbroadcastPLIStelevision commercials at bank branches. Thiswassupportedbymarketingmaterials tocommunicate theproductfeaturestopotentialcustomers.

The Hong Kong Mortgage Corporation Limited Annual Report 2016 39

Apart fromcollaboratingwith itsbusinesscounterparts,theCorporation increasedmarket receptivenessof thePLIS throughdown-to-earthpromotionalefforts.Aseriesof16-dayrovingexhibitionswereheldatshoppingcentresclosetosubsidisedhousingestates,duringwhichcreativeandinteractivegameswereconductedtoenrichcustomerexperienceanddeepenpublicunderstandingof thePLIS.Moreover, theCorporationactivelyestablishedcontactswith themanagement offices of subsidised housingproperties to reachout toownersofsubsidisedhousingproperties.

Reverse Mortgage Programme

TheReverseMortgageProgrammewas launchedtogiveelderly people an additional financial planningoptiontoenhance theirqualityof life.By theendof2016, theCorporationhadapprovedatotalof1,525RMPapplicationssince its inception,with anaverageproperty valueofaroundHK$5.1millionandanaveragemonthlypayoutamountofHK$14,900.

In response to the 2016–17 Budget, theCorporationintroducedanewenhancement inOctobertoextendtheRMPtocoversubsidisedsale flatswithunpaidpremium(The Enhancement). It has received a positive andencouragingmarket response since the launch. Twoapplicationswereapprovedon the launchdayof TheEnhancement.AsattheendofDecember2016,morethan110applicationsandmorethan1,200enquiries inrelationtoTheEnhancementwerereceived.

Amulti-facetedpublicity campaignwas rolled out topromoteTheEnhancement.Advertisementswereplacedin localnewspapers.TheRMPcommercialwasbroadcastonmajortelevisionandradiochannels,andputononlinemediaplatformssuchasYouTube, to reach thewider

public.TheCorporationalsousedpublic transportationto promote The Enhancement , inc lud ing p lac ingadvertisementsonbusbodiesandbroadcastingtheRMPcommercial on in-train televisionsof theMassTransitRailway.ThispromotionaltoolwasusedbytheCorporationfor the first time. Itaimedtoeffectively reach the targetsegmentsalongtherouteslargelysurroundedbysubsidisedhousingestates.

TheCorporationorganiseddistrict-levelpromotions tocommunicate TheEnhancement to target customers.A total of seven rovingexhibitionswereconductedatmajor shoppingmallsnear subsidisedhousingestatesindifferentdistrictscoveringHongKong Island,KowloonandtheNewTerritories.TheCorporation’sstaffandbankrepresentativeswereavailableattherovingexhibitionstopromotetheRMPandaddresspublicenquiries.Responsetotherovingexhibitionshasbeenoverwhelminglypositiveandencouraging, inwhichcrowdsassembledandpeopleenquired about the product. Long queues of peopleappearedtoparticipate inthegames.BoththeexhibitionandgameswereeffectiveinenhancingtheawarenessandunderstandingoftheRMPamongthetargetcustomers.

Aside from themarketing initiatives driven by TheEnhancement, theCorporationundertook joint initiativeswith itsbusinesspartners includingbanks,professionalbodies and non-governmental organisations (NGOs)topromote theRMP. In2016,nearly50seminarswerearrangedandtheRMPtelevisioncommercialwasbroadcastat the branches of participating banks. In addition,management of the Corporation has supported thedevelopmentof theRMP.Apart fromgivingtalksathigh-levelconferencesonretirementplanningformembersofprofessionalbodies,potentialcustomersandtheinterestedpublic, theChiefExecutiveOfficeralso reachedout topeople in thedistrictsbyhostingasharingsessionatarovingexhibitionwhichwaswellattendedbymorethan100participants.

The Hong Kong Mortgage Corporation Limited Annual Report 201640

Business Overview

Microfinance Scheme

UndertheMicrofinanceScheme,theCorporationcontinuedto takeup theroleofaschemeoperator. It liaisedwithparticipatingbanksandNGOstoofferloansatanaffordablerateandsupportservicestopeoplewantingtostart theirownbusiness, becomeself-employedor achieve self-enhancement through training, upgrading of skills orobtainingprofessionalcertification.

TosupporttheHongKongFoodTruckPilotScheme(Food Truck Scheme) introducedbytheGovernment inMarch2016, theCorporation collaboratedwith the TourismCommission to rendersupport, including loan financing,mentorshipandentrepreneurial training, toapplicantsof theFoodTruckScheme.TherelevantentrepreneurialtrainingcoursesfortheFoodTruckSchemeorganisedbytheparticipatingNGOsattractedmorethan50enrolments.TheCorporationalsostreamlinedtheapplicationprocessforthoseapplicantsapplyingfortheMFStodeveloptheirfood truckbusiness.By theendofDecember2016,oneapplicationhadbeenapproved.

TheMFShasoperatedsmoothlysince its launch in June2012.Bytheendof2016,theMFShadapprovedatotalof183loanswithatotalloanamountofHK$45.8million.

TheMFShas a goodmix of borrowers fromdifferentbackgroundsandprofessions,suchasyoungbeauticians,makeupartists, apetgroomingawardwinner, fashionandwatchdesigners, IT graduates,Chinesemedicinepractitioners,rehabilitatedoffenders,aclownperformanceentertainer,nativeEnglishspeakingteachers,dessertsandpastrychefs,atesting laboratoryspecialistanduniversityundergraduates.

TheCorporation launchedaseriesofmarketingactivitiestopromotetheMFSbrandamongthelocalentrepreneurialcommunity.Anadvertisingcampaignwasconducted toreachouttothemasspublic,includingprintadvertisementsinmagazines,bannersononlinemediaplatforms,andtelevisioncommercialsonmajorbroadcastingchannels.TheCorporationparticipated in theStartmeupHKFestival2016organisedby InvestHKandpresentedonthe Incu-LabICEDays.TheCorporationadoptedafocusedstrategytopromotetheMFS, includingparticipating in tradefairs

andconductingseminarsatuniversitiestoapproachtargetcustomers.

TheMFSBookletentitled “Tips forSuccessfulBusinessStart-up”wasmadeavailable inmore than250 spots,includingbanks,NGOs,businesscentres,youthcentres,secondaryschools,tertiary institutionsandpublic libraries.Moreover, the Corporation sponsored the NGOs inorganisingpromotionalactivities.

Funding

Theglobal financialmarkets remainedvolatile in2016andwereaffectedby theuneveneconomicgrowthanddivergingmonetarypolicypaths in themajoreconomies,aswellas thesurprisingoutcomeofBrexitand theUSpresidential election.Despite the challengingmarketconditions, theHKMCmanaged tosecureprudentpre-funding for loanpurchases and refinancing activities.Given theCorporation’sstrongbackgroundasawhollygovernment-ownedentityand itssolidcredit rating, theCorporation raiseddebt totallingHK$16.2billion (withmaturityof1-yearandabove) in2016.At theendof theyear,theCorporation’stotaloutstandingdebtamountedtoHK$34.2billion.

TheCorporationiscommittedtodevelopingthelocaldebtmarketthroughregulardebtissuancesandtheintroductionofnewdebtproducts.Asoneof themostactivebondissuers inHongKong, theCorporationwill continue toissuedebtinbothlocalinstitutionalandretailmarkets,anddiversifyitsfundingsourcesandinvestorbasetooverseasinstitutionalmarkets.ThiswillnotonlyhelpbroadentheCorporation’s fundingbase,butalsoprovide institutionaland retail investorswithhighqualitydebt instrumentstosatisfy theirneedforportfoliodiversificationandyieldenhancement.

TheCorporationhas threedebt issuanceprogrammes,whichallowthe issuanceofdebtsecurities inanefficientand effectivemanner.With its strong credit rating,theCorporation’sdebt issuesarewell receivedby theinvestmentcommunity,suchaspensionfunds, insurancecompanies,investmentfunds,charities,government-relatedfundsand retail investors.TheCorporationundertakesproactive investorcommunications tomeetandupdateinvestorsregularly.

The Hong Kong Mortgage Corporation Limited Annual Report 2016 41

Medium Term Note ProgrammeTheCorporationestablished themulti-currencyMediumTermNote (MTN)Programme in June2007 tobroadenits investorbaseandfundingsources in the internationalmarket. Itwassetupwithan initialsizeofUS$3billion,whichwassubsequently increasedtoUS$6billion in July2011 tomeetgrowingdemand fromoverseas investors.Themulti-currencyfeatureoftheprogrammeenablestheCorporationto issuenotes inmajorcurrencies, includingHongKongdollars,USdollars,renminbi,Australiandollars,Britishpounds,euroandJapaneseyen, tomeetdemandfrombothlocalandoverseasinvestors.Allforeigncurrency-denominatedMTNdebt is fully hedged intoeitherUSdollarsorHongKongdollars.Theprogrammeincorporatesflexibleproductfeaturesandofferingmechanismsforbothpublic issuancesandprivateplacements to increase itsappealto investorswithdifferent investmenthorizonsandrequirements.Asat theendof2016,anextensivedealergroup comprising 10major international and regionalfinancial institutionshadbeenappointedtosupportfutureMTNissuanceandprovidesecondarymarketliquidity.

In2016, theCorporation launched33MTNprivatedebtissues, totallinganequivalentofHK$16.2billion (withmaturityof1-yearandabove).

Debt Issuance ProgrammeTheDebt IssuanceProgramme (DIP)wasestablished inJuly1998totarget institutional investorsintheHongKongdollardebtmarket.ItwassetupwithaninitialprogrammesizeofHK$20billion,whichwassubsequentlyincreasedtoHK$40billionin2003.TheDIPhassinceprovidedaflexibleandefficientplatform for theCorporation to issuedebtandtransferable loancertificateswithatenorofupto15years.AtotalofsixPrimaryDealersand16SellingGroupMembershavebeenappointedunder theDIP toprovidewidedistributionchannelsforbothpublicandprivatedebtissues.

Retail Bond Issuance ProgrammeTheCorporation isdedicatedtopromotingthe localretailbondmarket.TheCorporationpioneeredanewofferingmechanism for the retailbondmarket inHongKong inNovember2001andestablished theHK$20BillionRetailBond Issuance Programme inMay 2004. Under this

programme,placingbanksusetheirretailbranchnetworks,telephoneandelectronicbanking facilities toplacedebtsecurities issuedbytheCorporationwithretail investors.Toensuretheliquidityoftheaforementionedretailbonds,theplacingbanksarecommittedtomakingfirmbidpricesfor thebonds in thesecondarymarket.Since2001, theCorporationhas issued retail bonds totallingHK$13.7billion.When themarketenvironment isconducive, theCorporationaimsto issueretailbondsregularlytoprovidean additional investment tool for Hong Kong’s retailinvestors.

Revolving Credit Facility Provided by the Exchange FundIn January1998,during theAsianFinancialCrisis, theExchangeFundextendedaHK$10billionRevolvingCreditFacilitytotheCorporationthroughtheHKMA.ThisFacilityenables theCorporation tomaintain smoothoperationunderexceptionalcircumstances,so it canbetter fulfilitsmandate topromotebankingand financial stabilityinHongKong.While theCorporationobtains long-termfundingfromlocaland internationaldebtmarketstofunditsoperations,theFacilityalsoprovidesa liquidityfallbackfortheCorporation. In lightoftheglobal financialcrisis in2008,thesizeoftheFacilitywassubsequentlyincreasedtoHK$30billioninDecember2008,demonstratingtheHKSARGovernment’srecognitionoftheimportanceof,andfurthersupportfor,theCorporation.

TheCorporationusedtheRevolvingCreditFacilityduringtimesofmarketstressin1998and2008topartiallyfundtheacquisitionofHongKongresidentialmortgageassetsfromlocalbanks.Atbothtimes,theRevolvingCreditFacilitywasfullyrepaidwithfundsraisedfromtheCorporation’scost-effectivedebt issuancewhen themarketsstabilised. In2016,therewerenodrawdownsundertheRevolvingCreditFacility.

Credit RatingTheCorporation’sability toattract investment in itsdebtsecurities is underpinned by its strong credit rating,equivalenttothatoftheHKSARGovernment,accordingtoS&PandMoody’s.

The Hong Kong Mortgage Corporation Limited Annual Report 201642

Business Overview

Credit Ratings of the HKMC

S&P Moody’sShort-term Long-term Short-term Long-term

LocalCurrency A-1+ AAA(Negative) P-1 Aa1(Negative)

ForeignCurrency A-1+ AAA(Negative) P-1 Aa1(Negative)

The credit rating agencies havemade very positivecommentsontheCorporation’screditstanding.

ThefollowingcommentsareextractsfromthecreditratingreportsofS&PandMoody’sinJune2016:

S&P“Weequalize the ratingsonHKMCwith the ratingsonHongKong,thecorporation’ssoleowner.Thisreflectsourviewofanalmostcertainlikelihoodoftimelyandsufficientextraordinarysupport from theHongKonggovernmentin theunlikelyevent thatHKMCneeds it…WeconsiderHKMC’sundertakingofadditionalpolicyinitiativesoverthepastseveralyearsashavingamildsolidifyingeffectonitstieswiththeHongKonggovernment,andreinforcingtheintegrallinkbetweenthetwoentities.”

“Inour view,HKMC’svery strongmarketpositionandits strongmanagement and governance underpin itsstrongbusinessposition.HKMC isunique in its roleofaddressing localHongKongbanks’ liquidityandbalance-sheetmanagementneedsbypurchasingmortgageandloanportfolios,especially intimesofstress…AvarietyofstressfulmarketconditionshavetestedHKMC’sbusinessmodel.When theglobal financialmarketand the localeconomywereunderstress in late2008andearly2009,HKMCenlarged itsmortgageacquisitions in response tobanks’ requests,andenhanced itsmortgage insuranceprogram.InmorerecentyearswhenHongKong’spropertypriceswereshowingtheirsustainedgrowthtrendpriortothefall in late2015,HKMCtightenedtheeligibilitycriteriaforitsmortgageinsuranceprogram.ThemovewaspartofajointeffortwiththegovernmentandtomitigateapossibleoverheatingofpropertypricesinHongKong.”

“WebelievethatHKMCmanagesmarketriskseffectively.The companymaintains a simple asset and liabilitystructure,withmainlyvanillaproductsmanagedwithinwhatweregardassoundmarketriskpolicies.Thecorporation’sexposure tomarket risk is principally to interest ratemovements,withexposure to interest ratemismatchesappearingtobewellmanaged.”

“WeexpectHKMC tocontinue toprudentlymanage itsfundingand liquidity.Weassess thecompany’s fundingprofileasadequate,consideringits lackofretail funding…WeexpectHKMCtomaintainabufferofhighlyliquidassets,whichismorethansufficienttocoveritsshort-termfundingneeds…Further,aHK$30billion revolvingcredit facilitymorethanadequatelycoversall liabilitiesofHKMCwithinthenextyearandprovidesasignificantcushionagainstanyunexpectedliquiditystress.”

Moody’s“HKMCisfullyownedbythegovernment,andcarriesoutpublicpolicy functions through itsdailyoperations.Thecompany’spolicymandatesincludeenhancingfinancialandbankingstabilityinHongKong,promotinghomeownership,andfacilitatingthedevelopmentof the localdebtcapitalmarket.Aspartofitsmandatetopromotebankingstability,thecompanyactsasanalternative ‘lenderof lastresort’bystandingreadytopurchaseresidentialmortgagesfromHongKongbanks,particularlyduringtimesofstress.”

“ThegovernmentprovidestheHKMCwithaHK$30billionrevolvingcredit facilityandHK$1billionofequitycapitalcallablewhenneeded. In theevent thecompany’screditprofile isweakened inastressscenario,weexpect thegovernmenttoprovidetimelyextraordinarysupport.”

“TheHKMChasmaintainedverysoundassetqualitymetricsthroughmultiplehousingcyclessince itsestablishment…Hong Kong residentialmortgages have historicallyperformedverywellthrougheconomiccycles.Evenwhenpropertypricefellbyupto70%between1997and2003,overallmortgagedelinquenciesneverexceeded2%.ThecurrentaverageLTVratioon thecompany’sHongKongmortgagesisbelow40%.”

The Hong Kong Mortgage Corporation Limited Annual Report 2016 43

“Asawholesalefundedentitywithnocustomerdeposits,theHKMC reliesonongoingaccess to thedebtcapitalmarket to fund itsoperation.Nevertheless, thecompanyhasapolicyofpre-funding itsexpectedassetpurchasesandmaintainsaverystrongliquidityprofileduringnormaleconomicconditions. Ithasverygoodaccess tocapitalmarkets due to its strong financial fundamentals andgovernmentaffiliation…ItalsohasaHK$30billionrevolvingcredit facility fromthegovernment’sExchangeFund.Thecompanyhas sufficient liquid assets andgovernmentrevolvingcreditfacilitytorepayallof itsoutstandingdebtsasofend-2015.”

Mortgage-Backed Securitisation

TheCorporationstrivestopromotethedevelopmentofthemortgage-backedsecurities (MBS)market inHongKong.MBS isaneffective financial instrumentthatcanchannellong-termfundingfromthedebtmarkettosupplementtheneedforlong-termfinancinggeneratedbymortgageloans.Banksand financial institutionscanmakeuseofMBStomanagerisks inherent inmortgage loans,suchascreditrisks, liquidity risks, interest rate risksandasset-liabilitymaturitymismatchrisks.AdeepandliquidMBSmarketcanhelpenhancethedevelopmentofanefficientsecondarymortgagemarketand furtherpromoteHongKongasaninternationalfinancialcentre.

TheCorporationhas issuedatotalofHK$13.2billionMBSsince1999.TheUS$3billionBauhiniaMortgage-BackedSecuritisationProgrammewasestablished in 2001 toprovideaconvenient, flexibleandcost-efficientplatformfor theCorporation to issueMBSwithvariousproductstructures,creditenhancementsanddistributionmethods.

Risk Management

TheCorporation operates under prudent commercialpr inciples, and the principle of “prudence beforeprofitabi l i ty” guides the design of the overal l r iskmanagementframeworkanddisciplinesitsusesinitsday-to-daybusinessexecution.Overtheyears,theCorporationhascontinuouslymaderefinementstoitswell-established,robustand time-tested riskmanagement framework toreflectchangesinthemarketsanditsbusinessstrategies.

Corporate Risk Management CommitteeTheBoard is thehighestdecision-makingauthorityoftheCorporationandholds theultimateresponsibility forriskmanagement.TheBoard,with theassistanceof theCorporateRiskManagementCommittee (CRC),has theprimary responsibility for formulating riskmanagementstrategies intheriskappetitestatementandforensuringthat theCorporationhasaneffective riskmanagementsystemto implement thesestrategies.The riskappetitestatementdefinestheconstraintsforallrisk-takingactivitiesandtheseconstraintsare incorporatedintorisk limits,riskpoliciesandcontrolproceduresthattheCorporationfollowstoensurerisksareproperlymanaged.

TheCRC is responsible foroverseeingtheCorporation’svarioustypesofrisks, reviewingandapprovinghigh-levelrisk-relatedpolicies,overseeingtheir implementation,andmonitoring improvementefforts ingovernance,policiesandtools.RegularstresstestsarereviewedbytheCRCtoevaluatetheCorporation’s financialcapability toweatherextremestressscenarios.

TheCRCischairedbyanExecutiveDirector,withmembersincludingChiefExecutiveOfficer,SeniorVicePresident(Operations), SeniorVicePresident (Finance),GeneralCounsel,SeniorVicePresident(Risk),andseniorstafffromtheRiskManagementDepartment.

ThemajortypesofrisktheCorporationmanagesarecreditrisk,marketrisk,operationalrisk,legalandcompliancerisk,leveragingrisk,longevityriskandpropertyrisk.

The Hong Kong Mortgage Corporation Limited Annual Report 201644

Business Overview

Credit RiskCredit risk is theCorporation’sprimary riskexposure. Itrepresents thedefault riskpresentedby loanborrowersandcounterparties.

(a) Default riskToaddressdefault riskeffectively, theCorporationadoptsa four-prongedapproach tosafeguardandmaintain the quality of its assets,MIP and SMEguaranteeportfolios:

• carefulselectionofApprovedSellers,Servicers,ReinsurersandLenders

• prudent eligibility criteria for asset purchase,insuranceandguaranteeapplication

• effective duediligenceprocess formortgagepurchase,default loss, insuranceandguaranteeclaims

• enhancedprotectionforhigher-risktransactions.

LossesmayariseifthereareshortfallsintherecoveryamountreceivedfordefaultedloansthatfallundertheMortgagePurchaseProgramme (MPP).Tomitigatethisdefaultrisk,theCorporationestablishesprudentloanpurchasingcriteria;andconductseffectiveduediligencereviewsaspartoftheloanpurchaseprocessinorder tomaintain thecreditqualityof loans. Inaddition,dependingontheprojectedriskexposureofeachunderlying loanportfolio,creditenhancementarrangementsareagreeduponwithApprovedSellersonadeal-by-dealbasis to reduce thecredit lossesthatcouldarisefromtheborrower’sdefault.

Lossesmayalsoarise fromdefaulton loansundertheMIP’s insurancecoverage.EachMIPapplicationisunderwrittenby theCorporation inaccordancewithasetofeligibilitycriteriaandeachclaimfromaparticipatingbank isreviewedbytheCorporationtoensurethefulfilmentofallMIPcoverageconditions.As a result, the default risk for loanswithMIP

coveragehasbeengreatly reduced.Toreducetheriskofpossibleconcentrationof thisdefault risk,theCorporation transfersaportionof the risk-in-force toApprovedReinsurers throughreinsurancearrangements.

Similarly, lossesmay arise from a borrower’sdefaulton loans intheSMEguaranteeportfolio.Theborrower’sdefaultriskofeachguaranteeapplicationisassessedby the lender inaccordancewith theircreditpolicies. Inaddition, theCorporationadoptsprudenteligibilitycriteria,conductsadministrativevettingandcredit reviewstobetterunderstandthecreditqualityoftheapplications,andcarriesoutduediligencereviewoneachdefaultclaimtoensuretheloan’scompliancewith theCorporation’seligibilitycriteriaaswellasthelenders’internalcreditpolicies.

Inaddition, theCorporationadoptsathree-prongedapproach tomanage the default risk under theMFS,which includes: (a) prudent assessment ofborrowers’repaymentcapability; (b)avettingpaneltoconsiderbusinessviabilityandapprovalof theloanapplications;and (c)provisionof trainingandmentoringsupporttoborrowers.

Credit performances of the loan and guaranteeportfoliosaretrackedandreportedonaregularbasistoprovidemanagementwithupdatedcreditprofiletocloselymonitor theoperatingenvironment foranyemerging risks to theCorporation,and timelyimplementriskmitigatingmeasures.

(b) Seller/Servicer counterparty riskCounterparty risksmayarise from the failureofaSeller/Servicerofanacquiredportfolio to remitscheduledpayments to theCorporation ina timelyandaccuratemanner.

TheApprovedSellers/Servicersaresubjecttoarisk-basedeligibility reviewandongoingmonitoringontheirloanservicingqualityandcreditstanding.

The Hong Kong Mortgage Corporation Limited Annual Report 2016 45

(c) Reinsurer counterparty riskReinsurercounterparty risk refers to the failureofanApprovedReinsurer tomakeclaimpaymentsto theCorporation. Inorder tomitigate reinsurercounterparty riskeffectively, theCorporationhasestablished a framework for the assessment ofmortgagereinsurer’seligibility.

TheCorporationperformsannualandad-hocreviewsof each Approved Reinsurer to determine theeligibilityfortheongoingbusinessallocationandrisk-sharingportions.

(d) Treasury counterparty riskTreasury counterparty risk ariseswhen there isadelayor failure from treasurycounterparties tomakepaymentswithrespecttotreasuryinstrumentst ransac ted w i th the Corpora t ion . T reasurycounterparties aremanagedby a ratings-basedcounterparty assessment framework and a risk-basedcounterparty limitmechanism.The treasurycounterpartiesarecontinuallymonitoredand thecounterparty limits are adjusted based on theassessmentresults.

Furthermore, theCorporationhassetupbilateralco l l a t e r a l a r r angemen t s w i t h ma jo r swapcounterpartiestomitigatethecounterpartyrisk.

(e) Lender riskTheCorporation isexposed to lender risk inSMElendingthatarises from: (a)a lender’sunderwritingbeingnon-compliantwith its credit policy; (b) alender’s loosely formulatedcreditpolicy that isnotspecificenoughorsufficientlydefinedforcompliance;and (c) themoral hazard of a lender being lessprudent in underwriting a guarantee-protectedapplication.TheCorporationmanages lender riskthroughthereviewofthelenders’creditpoliciesandtheduediligencereviewsonclaims.

At the heart of the Corporat ion’s credit r iskmanagement frameworkare twocommittees: theCreditCommittee and the TransactionApprovalCommittee.

Credit CommitteeTheCreditCommittee(CC) isresponsibleforsettingtheCorporation’soverallcreditpoliciesandeligibilitycriteria,particularly forassetacquisition,mortgageinsurance,SMEguaranteebusinessandMFS.TheCCoperatesundera frameworkapprovedby theBoard.TheCCistheapprovalauthorityforacceptingapplications tobecomeApprovedSellers/Servicersunder theMPP,ApprovedReinsurers under theMIP,ApprovedLendersundertheSFGSandeligibletreasurycounterparties. It is also responsible forsettingriskexposurelimitsforthecounterparties.TheCCalsocloselymonitorstheoperatingenvironment,andputs inplacetimelyriskmitigatingmeasurestomanagethecreditrisk.

Transaction Approval CommitteeTheTransactionApprovalCommittee(TAC)conductsan in-depth analysis of pricing economics andassociatedcreditrisksforbusinesstransactions,whiletakingintoconsiderationthelatestmarketconditionsandbusinessstrategiesapprovedbytheBoard.Majortransactionsendorsedby theTACare subject toapprovalbyanExecutiveDirector.

TheCCandtheTACarebothchairedby theChiefExecutiveOfficer,withmembers includingSeniorVicePresident (Operations),SeniorVicePresident(Finance),GeneralCounsel,SeniorVicePresident(Risk)andseniorstaff fromthe relevant functionaldepartments.

The Hong Kong Mortgage Corporation Limited Annual Report 201646

Business Overview

Market RiskMarketriskariseswhentheCorporation’s incomeor thevalueofitsportfoliosdecreasesduetoadversemovementsinmarketprices.Marketriskconsistsof interestraterisk,asset-liabilitymaturitymismatch risk, liquidity riskandcurrencyrisk.

(a) Interest rate riskNet interest income is thepredominant sourceofearningsfortheCorporation.Itrepresentstheexcessof interest income (from theCorporation’s loanportfolio,cashanddebt investments)over interestexpenses(fromdebtissuanceandotherborrowings).Interest rate riskariseswhenchanges inmarketinterest ratesaffect the interest incomeassociatedwiththeassetsand/or interestexpensesassociatedwiththeliabilities.

Theprimaryobjectiveofinterestrateriskmanagementis thereforeto limit thepotentialadverseeffectsofinterestratemovementsoninterestincome/expense,whilemaintainingstableearningsgrowth.TheinterestrateriskfacedbytheCorporationistwo-fold,namelyinterestratemismatchriskandbasisrisk.Interestratemismatchrisk is themostsubstantial riskaffectingtheCorporation’snetinterestincome.Itarisesmainlyasaresultofthedifferencesinthetimingofinterestratere-pricingfortheCorporation’s interest-earningassetsand interest-bearing liabilities. Interest ratemismatchrisk ismostevident in the loanportfolioswhere themajority of the loansare floating-rateassets(benchmarkedagainstthePrimeRateorHIBORRate),whilstthemajorityoftheCorporation’sliabilitiesare fixed-rate debt securities. TheCorporationthereforemakesprudentuseofarangeof financialinstruments,suchasinterestrateswaps,interestrateswaptions,basisswaps,forwardrateagreementsandissuancesofMBS,tomanageinterestratemismatchrisk.Theproceedsof the fixed-ratedebtsecuritiesaregenerallyswapped intoHIBOR-based fundsviainterest rate swaps inorder tobettermatch thefloating-rateincomesfrommortgageassets.

TheCorporationalsousesdurationgapasanindicatortomonitor,measure andmanage interest ratemismatchrisk.Durationgapmeasuresthedifferencein interest rate re-pricing intervalsbetweenassetsandliabilities.Thewiderthedurationgap,thehigherthe interest ratemismatchrisk.Apositivedurationgapmeansthedurationofassets is longerthanthatoftheliabilities,andtherefore,representsgreaterriskexposuretorisinginterestrates.Anegativedurationgap, incontrast, indicatesgreater riskexposure todeclininginterestrates.

Dependingontheprevailinginterestrateoutlookandmarketconditions, theCorporationproactively re-balancesthedurationgapofitsasset-liabilityportfolioundertheguidanceandsupervisionoftheAssetandLiabilityCommittee(ALCO).

Basisriskrepresentsthedifferenceinthebenchmarkrates between the Corporation’s Prime-basedinterest-earningassetsanditsHIBOR-basedinterest-bearing liabilities.However, thereareonly limitedfinancialinstrumentscurrentlyavailableinthemarkettofullyhedgethePrime-HIBORbasisrisk. Ingeneral,basis riskcanbeeffectivelyaddressedonlywhenassetsarebasedonHIBOR tomatch the fundingbase,orwhenrelatedriskmanagement instrumentsbecomemoreprevalentoreconomical.Overthepastfewyears,theCorporationhasconsciouslyadoptedastrategythatacquiresmoreHIBOR-basedassets.Asaresult,thePrime-HIBORbasisriskfortheCorporationhas been substantially reduced. In addition, theCorporationhad issuedPrime-basedMBSandusedhedgingderivativesinthepasttomitigatesuchbasisrisk.

(b) Asset-liability maturity mismatch riskTheactualaverage lifeofaportfolioofmortgageloans,whichisusuallyshorterthantheircontractualmaturity, depends on the speed of scheduledmortgagerepaymentsandunscheduledprepayments.Higherprepayment ratesshorten theaverage life

The Hong Kong Mortgage Corporation Limited Annual Report 2016 47

of a portfolio ofmortgage loans. InHong Kong,prepaymentoccursfortwomainreasons:(i)housingturnover—borrowersrepayingtheirmortgageloansuponthesalesof theunderlyingproperties,and (ii)refinancing—borrowersrefinancingtheirmortgageloanstoobtainlowermortgagerates.

Asset-liabilitymaturitymismatch riskcanbemorespecificallycharacterisedas reinvestment riskandrefinancingrisk.Reinvestmentriskreferstotheriskofa lowerreturnfromthereinvestmentofproceedsthat theCorporation receives fromprepaymentsandrepaymentsof its loanportfolio.Refinancingriskis the riskof refinancing liabilitiesatahigher levelof interest rateorcreditspread.TheCorporation isexposedtorefinancingrisk (inbothfundingamountandcostof funds)whenitusesshort-termliabilitiesto finance long-term, floating-rate loanportfolios.Reinvestmentrisk ismanagedthroughtheongoingpurchaseofnew loanstoreplenish therundown intheretainedportfoliosandthroughthe investmentofsurpluscashindebtsecuritiesorcashdepositstofine-tunetheaveragelifeoftheoverallassetspool.Inaddition,theCorporationmakesuseofthe issuanceofcallablebondsandtransferableloancertificatestomitigatereinvestmentrisk.Thecalloptionembeddedincallablebondsand transferable loancertificatesallowstheCorporation toadjust theaverage lifeofits liabilities tomatchmorecloselywith thatof theoverallpoolofassets.

TheCorporationmanagesitsrefinancingriskthroughflexible debt securities issuancewith a broadspectrumofmaturities.Thisagainserves toadjusttheaverage lifeof theoverall liabilityportfolio inadynamicfashion. Inaddition,refinancingriskcanbemitigatedbyadjustingthematuritiesofassets inthe

investmentportfoliooroff-loadingmortgageassetsthroughsecuritisationofmortgage loans intoMBS.TheCorporationusestheasset-liabilitymaturitygapratiotomeasure,monitorandmanageasset-liabilitymaturitymismatchrisk, toensureaproperbalancebetweentheaveragelifeoftheCorporation’sassetsandliabilities.

(c) Liquidity riskLiquidity riskrepresents theriskof theCorporationnotbeingable torepay itsobligations,suchas theredemptionofmaturingdebt,ortofundthecommittedpurchases of loan portfolios. The Corporationimplements its liquidityriskmanagementframeworkin response tochanges inmarketconditions.TheCorporationhascontinuouslymonitoredthe impactofrecentmarketeventson its liquidityposition,andhaspursuedaprudentpre-fundingstrategytohelpcontainthe impactofanyglobalfinancialturmoilonitsliquidity.Liquidityriskismanagedbymonitoringthedaily inflowandoutflowof funds,andbyprojectingthelonger-terminflowsandoutflowsoffundsacrossthefullmaturityspectrum.TheCorporationusestheliquidasset ratio tomeasure,monitorandmanageliquidityrisk.

Givenitsstrongbackgroundasawhollygovernment-ownedentityandsolidcreditrating,theCorporationisefficientinraisingfundsfromdebtmarketswithbothinstitutionalandretail fundingbases.Thisadvantageis supplementedby theCorporation’sportfolioofhighly liquid investments,which isheld toenableaswiftandsmooth response tounforeseen liquidityrequirements. TheHK$30billionRevolvingCreditFacilityfromtheExchangeFundfurtherprovidestheCorporationwithaliquidityfallbackevenifexceptionalmarketstrainslastforaprolongedperiod.

The Hong Kong Mortgage Corporation Limited Annual Report 201648

Business Overview

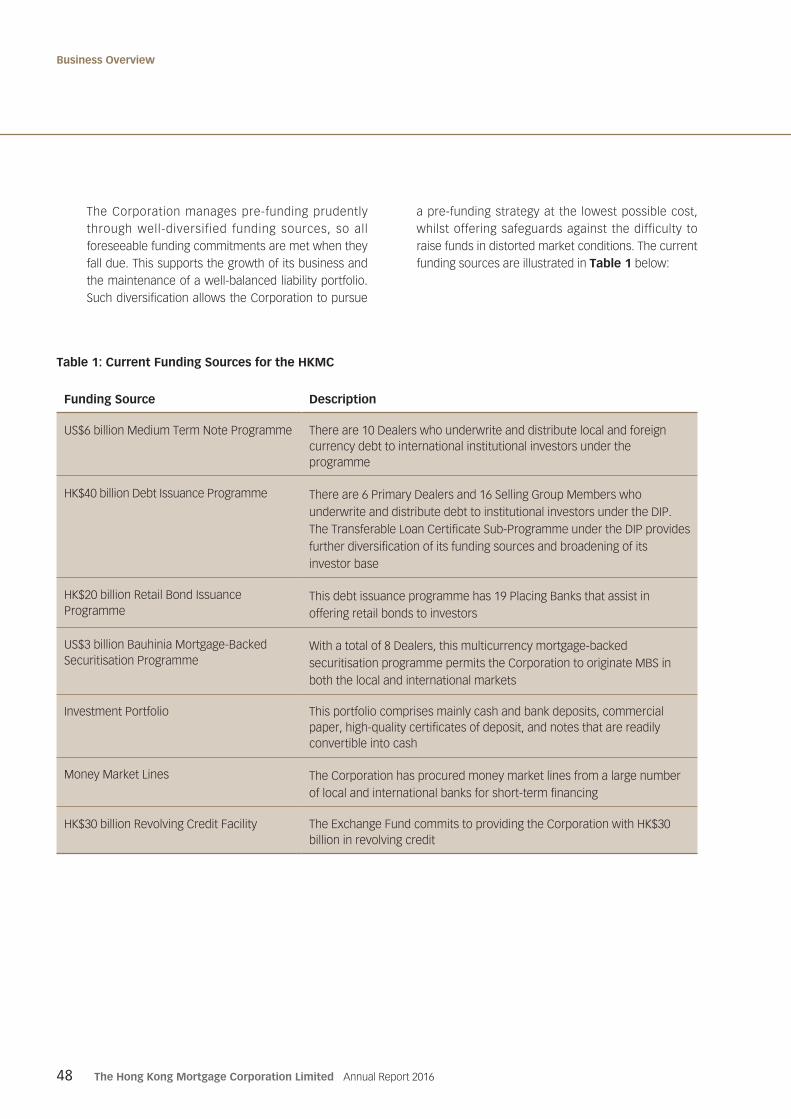

TheCorporationmanagespre-fundingprudentlythroughwell-diversified funding sources, so allforeseeablefundingcommitmentsaremetwhentheyfalldue.Thissupportsthegrowthofitsbusinessandthemaintenanceofawell-balancedliabilityportfolio.SuchdiversificationallowstheCorporationtopursue

apre-fundingstrategyat the lowestpossiblecost,whilstofferingsafeguardsagainst thedifficulty toraisefundsindistortedmarketconditions.ThecurrentfundingsourcesareillustratedinTable 1below:

Table 1: Current Funding Sources for the HKMC

Funding Source Description

US$6billionMediumTermNoteProgramme Thereare10Dealerswhounderwriteanddistributelocalandforeigncurrencydebttointernationalinstitutionalinvestorsundertheprogramme

HK$40billionDebtIssuanceProgramme Thereare6PrimaryDealersand16SellingGroupMemberswhounderwriteanddistributedebttoinstitutionalinvestorsundertheDIP.TheTransferableLoanCertificateSub-ProgrammeundertheDIPprovidesfurtherdiversificationofitsfundingsourcesandbroadeningofitsinvestorbase

HK$20billionRetailBondIssuanceProgramme

Thisdebtissuanceprogrammehas19PlacingBanksthatassistinofferingretailbondstoinvestors

US$3billionBauhiniaMortgage-BackedSecuritisationProgramme

Withatotalof8Dealers,thismulticurrencymortgage-backedsecuritisationprogrammepermitstheCorporationtooriginateMBSinboththelocalandinternationalmarkets

InvestmentPortfolio Thisportfoliocomprisesmainlycashandbankdeposits,commercialpaper,high-qualitycertificatesofdeposit,andnotesthatarereadilyconvertibleintocash

MoneyMarketLines TheCorporationhasprocuredmoneymarketlinesfromalargenumberoflocalandinternationalbanksforshort-termfinancing

HK$30billionRevolvingCreditFacility TheExchangeFundcommitstoprovidingtheCorporationwithHK$30billioninrevolvingcredit

The Hong Kong Mortgage Corporation Limited Annual Report 2016 49

(d) Currency riskCurrency risk arises from the impact of foreignexchange rate fluctuations on theCorporation’sfinancialpositionandforeigncurrency-denominatedcashflows.TheCorporationmanagesitscurrencyriskstrictly inaccordancewiththeinvestmentguidelinesapprovedby theBoardandunder thesupervisionof theALCO,whichsetsdailymonitoring limitsoncurrencyexposure.

Inaccordancewith thisprudent risk-managementprinciple, thenetexposureof the foreigncurrencydenominateddebtsissuedundertheMTNProgrammeisfullyhedgedbytheuseofcross-currencyswaps.

Transactionexecutionissegregatedamongthefront,middleandbackofficestoensureadequatechecksandbalances.TheTreasuryDepartment,actingasthefrontoffice,isresponsibleformonitoringfinancialmarketmovementsandexecutingtransactionsinthecash,derivatives,debtandsecuritisationmarkets,inaccordancewith thestrategies laiddownby theALCO.TheRiskManagementDepartment,assumingthemiddle-office role,monitors compliancewithtreasurycounterpartyandmarket risk limits. TheOperationsDepartment,actingas thebackoffice,is responsible fordeal verification, confirmation,settlementandthepaymentprocess.

Asset and Liability CommitteeTheALCOisresponsiblefortheoverallmanagementofmarket risk of theCorporation. It follows theprudent r iskmanagement principles and theinvestmentguidelinesapprovedby theBoard. It isresponsible forreviewingandmanagingthemarketriskincludinginterestraterisk,asset-liabilitymaturitymismatchrisk,liquidityandfundingrisk,andcurrencyriskof theCorporation.Regularmeetingsareheldto reviewthe latest financialmarketdevelopmentsand formulate relevantasset-liabilitymanagementstrategiesfortheCorporation.

TheALCO ischairedbytheChiefExecutiveOfficer,withmembers including Senior Vice President(Finance),SeniorVicePresident (Operations),SeniorVicePresident(Risk)andseniorstafffromtherelevantfunctionaldepartments.

Operational RiskOperational riskrepresents theriskof lossesarisingfrominadequaciesorthefailureofinternalprocesses,peopleorsystemsorexternalinterruptions.

TheCorporationadoptsabottom-upapproachto identifyoperational risk by carrying out in-depth analyses ofnewproducts, business activities, processes, systemenhancements and due di l igence reviews of newoperational flows. Comprehensive validation rules,management informationsystemreportsandaudit trailsareinplacetotrackandreportanyerrorsordeficiencies.

TheCorporationactivelymanagesoperationalriskwith itscomprehensivesystemofwell-establishedinternalcontrols,authentication structuresandoperationalprocedures.Theoperational infrastructure iswelldesignedtosupportthe launchofnewproducts indifferentbusinessareas.Rigorousreviewsareconductedbeforetheimplementationofoperationalorsysteminfrastructuretoensureadequateinternalcontrolsareinplacetomitigateoperationalrisks.

Toensureanefficient andeffectivedischargeofdailyoperations,theCorporationpursuesadvancedtechnologicalsolutionsalongsiderobustbusinesslogisticsandcontrolstocarryout itsoperationalactivitiesandbusinessprocesses.Stepshavebeentakentoensuretheaccuracy,availabilityandsecurityof thesesystems.TheCorporationhasalsotakencautioussteps to instituteadequatechecksandbalancestoensure itsoperationsareproperlycontrolled.Effective internalcontrolsalsohelpminimisefinancialriskandsafeguardassetsagainst inappropriateuseor loss,includingthepreventionanddetectionoffraud.

Information System Security PolicyTheCorporation’s Information SystemSecurity Policydocuments the requirementsofsecuritystandardsandestablishescontrolsover theconfidentiality, integrityandavailabilityofinformationassetsforobservancebyallstaff.TheCorporation implementsvarious informationsecuritymeasures tominimise itsexposure toexternalattacks.Internally, theCorporationhasalso implementedsecuritycontrolsonitsLocalAreaNetworktoreducedamageintheeventofamalicious intrusion.TheCorporationengagesexternalconsultantswhenappropriatetoconductintrusionvulnerability tests toenhancesystemsecurity.Toensureahighdegreeofcompliance, theCorporation’smissioncriticalsystemsandprocessesaresubjecttoregularreviewbyinternalauditors.

The Hong Kong Mortgage Corporation Limited Annual Report 201650

Business Overview

Business Continuity PlanThe Corporation’s business recovery plan ensuresmaximumpossibleservicelevelsaremaintainedatallunitstosupportbusinesscontinuityandminimisetheimpactofbusinessdisruptionfromdifferentdisasterscenarios.Eachbusinessunit regularlyassesses the impactofdisasterscenariosandupdates recoveryprocedures.Toensurebusiness recoveryproceduresarepractical, anannualcorporate-widebusinesscontinuitydrill isconducted.Dailyback-upsandoffsitestorageofback-uptapesare inplacetoprotecttheCorporationfromITdisasters.

Product Sign-off MechanismToensureall risk factorsareconsideredwhendesigningand implementinganewproduct, theCorporationhasdevelopedaproductdevelopmentmanagementframework,underwhichpropersign-offofproductspecification isconductedprior to the launchofanynewproduct.Theproductdriverisclearlyassignedatthestartoftheproductdevelopmentprocessand is responsible for institutingthesign-offprocess.Productscanonlybe launchedafterall functionaldepartmentshavesignedoffandconfirmedfunctionalreadiness.

Complaint-Handling MechanismTheCorporationmakesacontinuouseffort to improveitscoreprocesses toensure itsproductsandservicesmeetcustomers’expectations.Tomakesurecustomers’feedbackistimelyandproperlyattendedto,theCorporationhasaformalcomplaint-handlingmechanismtotrack,reportandhandlecomplaints.

Operational Risk CommitteeTheOperationalRiskCommittee (ORC) is responsible forensuringall line functions in theCorporationmaintainaneffectiveoperational riskand internalcontrol framework.TheORCestablisheskey risk indicators to track thekeyoperationalriskitemsandmonitortheeffectivenessoftheriskmitigatingmeasures.Operational risk incidents thatmaypotentially indicateacontrolweakness,a failureornon-compliancein internalprocessesare logged,reportedandhandled foroperational riskmanagement.TheORCisalsoresponsible forprovidingdirectionsandresolving

issues related to policies, controls andmanagementofoperational issues, aswell asensuringpromptandappropriatecorrectiveactionsinresponsetoauditfindingsrelatedtooperationalrisksorinternalcontrols.

TheORC ischairedby theChiefExecutiveOfficer,withmembers includingSeniorVicePresident (Operations),SeniorVicePresident (Finance),GeneralCounsel,SeniorVicePresident (Risk)andsenior staff from the relevantfunctionaldepartments.

Legal and Compliance RisksLegal riskarises fromuncertainty in theapplicationorinterpretationoflaws,regulations,andanyunenforceabilityor ineffectivenessof legaldocuments insafeguardingtheinterestsoftheCorporation.Complianceriskarisesfromthefailuretocomplywith laws,regulations,codesofpracticeandindustrypracticesapplicabletotheCorporation.

TheLegalOffice,headedbytheGeneralCounsel (who isalsotheCompanySecretary),advisestheCorporationonlegalmatterswithaviewtocontrolling legal risk.Whennewproductsorbusinessactivitiesareconsidered, theLegalOfficewill advise on the relevant laws and theregulatoryenvironment.Itwillalsoadviseonthenecessarylegaldocumentation,and identifypossible legalpitfallswithaviewtoprotectingthe interestsoftheCorporation.Whereappropriateexternalcounselwillbeengaged toassist theLegalOffice inproviding legal support to theCorporation.TheLegalOfficeworkscloselywiththeotherdepartmentsof theCorporationtoadviseon legal issuesanddocumentation.

TheComplianceFunction ispartof theLegalOfficeandis ledbytheChiefComplianceOfficerwhoreportstotheChiefExecutiveOfficerthroughtheGeneralCounsel.WhereappropriatetheComplianceFunctionwillengageexternalcounsel toadviseoncompliancematters. For amoredetaileddescriptionof theComplianceFunctionand itswork,pleaserefertotheComplianceReportingSectionoftheCorporateGovernanceReport.

TheORC is the governance committee for legal andcompliancerisks.

The Hong Kong Mortgage Corporation Limited Annual Report 2016 51

Leveraging RiskInorder toensure that theCorporationwouldnot incurexcessiveriskwhenexpanding itsbusinessandbalancesheet in relation to itsowncapitalbase, theFinancialSecretary,inhiscapacityastheFinancialSecretaryandnottheshareholder,actedastheregulatoroftheCorporation,by issuingasetofguidelinesbyreferenceprincipally totheBasel II risk-basedcapitaladequacy framework, theGuidelinesonCapitalAdequacyRatio (CAR),with theminimumCARsetat8%.Asat31December2016, theCorporation’sCARwas21.3%.

Theprudentuseofregulatorycapital ismonitoredcloselyin accordancewith the capital guidelines. TheChiefExecutiveOfficerreportstheCARandthedailyminimumratiototheBoardofDirectorsonaquarterlybasis.Anearlywarningsystem isalso inplace. If theCARdrops to thethresholdlevelof14%,theChiefExecutiveOfficerwillalerttheExecutiveDirectors. If theCARfalls to12%orbelow,theBoardofDirectorswillbe informedandappropriateremedialactionswillbetaken.

Longevity RiskLongevity risk refers to theheightening risk of largerpayoutsundertheRMPandPLIS.Thelongerthepayoutandloanperiodis,thelargertheloanbalancewillaccrueovertime,andthelessbuffertherewillbefromthesaleofthepropertytocovertheoutstandingloanbalance.Alossmayariseifthereisashortfallintherecoveryamountafterthedisposaloftheproperty.Theterminationrateofthe loansdependslargelyonthemortalityrate(i.e.lifeexpectancy)oftheborrowers.

Annual riskanalysis isconducted inorder toassess thepotential financial impactof longevityrisk,aswellas theinteractionamongthevariousriskfactorsundertheRMPandPLIS.Themortalityassumptionsare reviewedonaregularbasisbytheTAC.

Property RiskProperty riskarises from the fluctuation in thevalueofpropertywhichactsascollateralfortheCorporation’sloanandguaranteeportfoliosunder theMPP,MIP,RMPandPLIS.TheCorporationmanagespropertyriskbyconductingexternalpropertyvaluations foreach loanpurchaseorapplication,settingprudentassumptionsintherecoverablevalueof thecollateralisedproperty, restrictingmaximumloan-to-valueratiosoftheloansundertheprogrammesandconductingstressteststoexaminethe impactofadversemarketconditions.

Process Management and Information Technology

Sinceitsinception,theCorporationhasdevotedsubstantialresourcesandefforttocontinuously improve itsbusinessoperations,strengthenitsinternalcontrolsandenhanceitsapplicationsystems.Thepastyearisnoexception.

To furtherstrengthen theprocessesandsystemsat theCorporation in respectof informationsecurityanddataprotection,theCorporationappointeda leadingconsultingfirmwithexpertiseintheareatoreviewexistinginformationsystemsecuritymanualsandpolicies.Recommendationsfromthereviewwillbeimplementedaccordingly.

TheCorporationcontinuedtoimproveprocessautomation,data integrity,systemresilienceand informationsecuritythrough systemsdevelopment and enhancements tosupportvariouscorporateandbusinessinitiatives,suchastheSFGS,theRMP,thePLIS,theMFS,theMIP,thetreasuryoperations,andstrengthenriskmanagement.Suchstepsarevital toensureefficiency,accuracyandrobustness inbusinessoperationsthattranslateintobetterservicestothecommunity.Forexample, thereportingdatarequirementundertheMPPhasbeenfurthersimplifiedtostreamlinethepurchaseprocess.

Inaddition,oursystemenhancementsandprocess re-engineeringmeasuresaimtoachievepaperlessoperationsthathelpcontributetoabetterandgreenerenvironment.

The Hong Kong Mortgage Corporation Limited Annual Report 201652

Business Overview

Corporate Social Responsibility

In recognitionof theCorporation’scontribution to thecommunity and its commitment to corporate socialresponsibility(CSR)inpastyears,theCorporationhasbeenawardedtheCaringOrganisationLogobytheHongKongCouncilofSocialServicesince2008andhasnowsteppedinto itsninthyearofCSRparticipation. Inappreciationofemployerswhoplacehighvalueon theiremployee’sretirementneeds,theCorporationreceivedtheGoodMPFEmployerAward foreachof theassessmentperiodsof2014/2015and2015/2016bytheMandatoryProvidentFundSchemesAuthority. In recognitionofbeinganemployerattaching importance to the family-friendly spirit, theCorporationalso received theFamily-FriendlyEmployerAwardandtheAwardforBreastfeedingSupportunderthe2015/16Family-FriendlyEmployersAwardSchemeof theFamilyCouncilsupportedbytheHomeAffairsBureau.

Asasocially responsibleorganisation, theCorporationcares forboth itsemployeesand thecommunity. TheCorporationhasunderlined its commitment toCSRbycaringforitsemployees’well-being,participatingincharityactivities and implementingenvironmental protectionmeasures.

Care for EmployeesStaffing and RemunerationTheCorporationattractsandgroomstalenttoensuretheefficientperformanceof itscoremissionsofenhancingstability in thebanking sector, promotingwiderhomeownership and facilitating development of the debtsecuritiesmarket.Employeesareprovidedwithcompetitiveremunerationpackagesand fringebenefits,apromisingcareerpathanddevelopmentopportunities,andahealthyandsafeworkingenvironment.TheCorporationhasalsoadopted family-friendlypracticesbyofferinga five-dayweektohelpemployeesmaintainagoodwork-lifebalance,aswellascomprehensivemedicalanddental insuranceplansthatcoverbothemployeesandtheirfamilymembers.

Throughsystemautomationandprocessre-engineering,theCorporation hasmaintained a lean and efficientworkforce,despitean increase inthescopeofoperationsandthecomplexityof theproducts itoffers. In2016, thepermanentstaffestablishmentoftheCorporationwas202,andthestaffturnoverratewas4.96%.

Training and DevelopmentTheCorporation recognises the importanceofongoingtrainingandhasdevotedconsiderable resources to thecontinuousenhancementof itsemployees’professionalknowledgeandskills. In2016, theCorporationarrangeddifferentprogrammesandworkshopstohelpemployeesenhance theirproductknowledge,andstrengthen theirmanagerialandtechnicalcompetenceandsoftskills.

The in-house trainingworkshopscoveredawide rangeof topicssuchasnegotiationand influencingskills, teamcollaboration,conflictmanagement,crisismanagementandoccupationalsafetyandhealth.Duringtheyear,seminarsonPersonalData(Privacy)Ordinance,Anti-briberyLawandAnti-MoneyLaunderingwerealsoheld.

TeamBuildingTraining

The Hong Kong Mortgage Corporation Limited Annual Report 2016 53

TrainingonOccupationalSafetyandHealth

TrainingonNegotiationandInfluencingSkills

TrainingonCrisisManagement

TheCorporationalsosponsoredemployees forexternaljob-related traininganddevelopmentcoursescoveringawide rangeof topics frommortgage-related issues,riskmanagement, corporategovernance, financeandaccounting to information technology and leadershiptraining.

Inaddition, all newemployeeswereprovidedwithaninductionsession toprovide themwitha foundationofknowledgeabouttheCorporation’sorganisationalstructure,functionsandpolicies.

Employee Relations and Staff ActivitiesTopromoteahealthywork-lifebalanceandfosterafamily-friendlyworkingenvironment,theHKMCStaffClubregularlyorganisesstaffactivities tocultivatebetter relationshipsandcommunicationamongemployees. In2016, theseactivitiesincludedinterestclasses,Work-LifeBalanceWeek,outingsandotherstaffgatherings,allofwhichwerewellreceivedbyemployeesand their families.The in-housestaffpublication“HKMConnection”recapssnapshotsoftheHKMCstaffactivities.

Work-lifeBalanceWeek

To fac i l i tate ef fect ive communicat ion wi th in theCorporation, the intranetStaffHomepage is frequentlyupdated so useful information can be shared amongdifferentdepartments.There isalso theStaffSuggestionScheme,whichencouragesstafftosuggest improvementsinworkflowandtheworkplace.

Health and SafetyAsacaringorganisation, theCorporation isdedicatedto lookingafterboth thephysicalandmentalhealthofitsemployees.AnEmployeeSupportProgramme is inplacetoprovideconfidentialexternalcounsellingservicestoemployeesand their familymembers, if needed.Avaccinationprogrammeforthepreventionofinfluenzaandhealth-checkprogrammesatprivileged rateswerealsoofferedtoemployees.

The Hong Kong Mortgage Corporation Limited Annual Report 201654

Business Overview

TheCorporationhas, from time to time, reviewedandstrengtheneditscontingencyplanswhichaimtominimiseany unexpected or sudden disruption to businessoperations,suchas fromanoutbreakofcommunicablediseaseamongemployees.Periodicdrillsareorganisedtomakesureemployeesareconversantwiththeactivationofback-up facilities,contingencyplansandcommunicationarrangementsincaseofemergency.

Care for the CommunityCharities and Social ActivitiesThe Corporation promotes various charitable andcommunityfunctions,suchasfundraisingevents,donationcampaigns and voluntary services. Employees areencouragedtosupportcharityactivitiesandjoinvoluntaryworkorganisedby theHKMCVolunteersTeam,CaringLeague.

In2016, theCorporationorganiseddonationcampaigns,suchasDressCasualDay2016fortheCommunityChest,andhelditsannualBloodDonationDayeventfortheHongKongRedCross.

BloodDonationDay

DressCasualDay

Employeeshavebeenkeen toparticipate in voluntaryservices, demonstrating their concern for the needyby dedicating time and effort to various causes. TheCaringLeaguehaspartneredwithseveralsocialserviceorganisations to participate in a number of voluntaryservices,includingthefollowing:

• care for theenvironment—a recyclingcampaign inpartnershipwith theSalvationArmy tocollectbooks,stationeryandtoys,etc

• carefortheelderly—organisedbytheHOPEWorldwideandHongKongPlaygroundAssociation, involvingourvolunteersvisitingelderlypeople,andbringing them“luckybags”withdaily necessities towelcome theChineseNewYearandMid-AutumnFestival

• care for thechildren—organisedby theH.K.S.K.H.LadyMacLehoseCentreServicesforEthnicMinorities,involvingourvolunteershavingaChristmaspartywithethicminoritychildren.

The Hong Kong Mortgage Corporation Limited Annual Report 2016 55

Internship and Manager Trainee ProgrammesTohelpnurture talent for the future, theCorporationprovides a number of internship programmes forundergraduatestogivethematasteof therealbusinessworldandhelpthembetterpreparefortheirfuturecareers.Thestudentswho joined theprogrammesappreciatedthe learningexperienceandworkopportunitiestheywereexposedto.

During the year, the Corporation has continued theManager Trainee Programmewith the objective ofidentifyinghigh-calibreyoungexecutives forgroomingtomeet theCorporation’s long-termstaffdevelopmentplan.Throughoutthethree-yearprogramme,theManagerTraineeswill undergoon-the-job training in differentdepartments, takepart incorporateprojectsandattendstructuredlearninganddevelopmentprogrammes.

Environmental ProtectionTheCorporationcontinuouslysupportsand implementsvariousgreenmeasurestocreateamoreenvironmentallyfriendlyofficeandraiseemployees’awarenessofmethodsofwastereductionandenergyconservation.Employeesareencouraged to adoptpaperlessworkingpracticesby usingmore electronic communication. They arealsoencouraged tocollectwastepaperandused tonercartridges for recycling.Since2006, theCorporationhasadoptedvariousmeasures,includingbettercontrolofofficetemperatureandtheuseofLEDlighting, inthe interestofenergyefficiency.TheCorporationwelcomessuggestionsfromemployeesongreenoffice ideasandencourages itssuppliers touseandoffermoreenvironmentally friendlyproductswheneverpossible.