Business outlook presentation

36

Nigeria: Economic & Business Outlook for 2012 Implications for SMEs By Dr. ‘Doyin Salami

-

Upload

edc-pan-atlantic-university -

Category

Business

-

view

541 -

download

5

Transcript of Business outlook presentation

Nigeria: Economic & Business Outlook for

2012

Implications for SMEs

By Dr. ‘Doyin Salami

Data Sources

• International Monetary Fund (IMF);

• World Bank;

• Central Bank of Nigeria;

• Bank of England

• Economist Intelligence Unit (EIU)

• National Bureau of Statistics

• Financial Derivatives

Competitiveness of the Nigerian Economy

Nigeria remains one of the least competitive economies globally. • Ranks 125th out of 142 countries in

Global Competitiveness 2011/2012. • Ranks 11th out of the N11

economies in 2011/12. Nigeria ranked above Bangladesh and Pakistan in the 2009/2010 rating.

The 2011 Ease of Doing Business Report shows that In the last 5years, 85% of Economies made it easier to do business • Nigeria included amongst countries

where it became easier to do business. Nigeria Ranks 133rd out of 183 countries in Ease of Doing Business Report 2011.

• Ranks 15th easiest economy to do business in Sub-Saharan Africa.

0 50 100 150

NigeriaIndia

BrazilRussia

IndonesiaEgypt

PakistanGhanaTurkeyMexico

South AfricaGermany

South KoreaUSA

UKChina

2011

2010

EASE OF DOING BUSINESS REFORMS - Ranking

0 20 40 60 80 100 120 140

NigeriaPakistan

GhanaEgypt

RussiaTurkeyMexico

IndiaBrazil

South AfricaIndonesia

South KoreaChina

UKGermany

USA

2011

2010

GLOBAL COMPETITIVENESS INDEX RANKING

…Competitiveness of the Nigerian Economy

Nigeria remains the least amidst comparator countries and the N11 economies . Ranks 11th out of the N11 economies in 2011/12 Doing business remains easiest in OECD high-income economies 0 50 100 150

NigeriaPakistan

EgyptIndia

South AfricaBrazil

TurkeyMexicoRussia

IndonesiaTunisia

USAUK

South KoreaChina

Germany

2011

2010

Basic Requirements – (Rankings)

0 25 50 75 100

PakistanEgypt

NigeriaKenya

IndonesiaRussia

MexicoTurkeyBrazil

South AfricaIndia

South KoreaChina

GermanyUK

USA

2011

2010

Efficiency Enhancers – (Rankings)

0 25 50 75 100

RussiaEgypt

PakistanNigeriaTurkeyMexico

KenyaIndia

IndonesiaSouth Africa

BrazilSouth Korea

UKChina

USAGermany

2011

2010

Innovation & Sophistication Factors – (Rankings)

World Bank/IMF Ease of Doing Business

Topic Rankings 2012 Rank 2011 Rank Change in Rank

Ease of Doing Business 133 133 -

Starting a Business 116 108 -8

Dealing with Construction Permits 84 83 -1

Getting Electricity 176 176 -

Registering Property 180 180 -

Getting Credit 78 75 -3

Protecting Investors 65 60 -5

Paying Taxes 138 109 -29

Trading Across Borders 149 149 -

Enforcing Contracts 97 98 +1

Resolving Insolvency 99 105 +6

• Nigeria

Corporate Performance

• Performance of the Top 20 companies shows – the volatility of sales and PAT

growth. In 2008, both sales and PAT growth declined and by 2009, PAT growth was negative reflecting the effect of global recession.

– Q3-2011, nominal GDP growth scaled above both PAT growth and sales growth and the likelihood of a convergence is seen

-40

-20

0

20

40

60

80

100

120

140

160

-10

0

10

20

30

40

50

60

Q1-

2007

Q2-

2007

Q3-

2007

Q4-

2007

Q1-

2008

Q2-

2008

Q3-

2008

Q4-

2008

Q1-

200

9

Q2-

2009

Q3-

2009

Q4-

2009

Q1-

201

0

Q2-

2010

Q3-

2010

Q4-

2010

Q1-

2011

Q2-

2011

Q3-

2011

Per

cen

tage

s (%

)

Sales growth

Nominal GDP growth

PAT growth

Top 20 Corporate Performance

NSE Monthly Reports, EKA Research

-20

-10

0

10

20

30

40

50

20

06

20

07

20

08

20

09

20

10

20

11

(Q

3)P

erc

en

tage

s (%

)

Sales growth (%) PAT growth (%) Nominal GDP growth

Annual Reports - Various issues, EKA Research

Top 20 Corporate Performance

Corporate Performance

• A negative inflation rate is seen in the year 2009 where PAT growth was also negative although rising inflation rate has been the case since then.

• Both depict the effect of rising cost –as shown by the GDP deflator- that resulted to declining demand in the

economy.

-20

-10

0

10

20

30

40

50

20

06

20

07

20

08

20

09

20

10

20

11

(Q

3)P

erc

en

tage

s (%

)

Inflation- GDP Deflator Sales growth (%)PAT growth (%)

Top 20 Corporate Performance

Annual Reports - Various issues, EKA Research

-40

-20

0

20

40

60

80

100

120

140

160

-20

-10

0

10

20

30

40

50

60

Q1-

2007

Q2-

2007

Q3-

200

7

Q4-

2007

Q1-

2008

Q2-

2008

Q3-

2008

Q4-

2008

Q1-

2009

Q2-

200

9

Q3-

2009

Q4-

2009

Q1-

2010

Q2-

2010

Q3-

2010

Q4-

2010

Q1-

201

1

Q2-

2011

Q3-

2011

Pe

rce

nta

ges

(%)

Sales growth Inflation GDP-Deflator

PAT growth

Top 20 Corporate Performance

Annual Reports - Various issues, EKA Research

• Aggregate credit to the economy grew on YTD by 42.8% in Dec.2011

– While Credit to the private sector grew YTD by 37.4% in Dec. 2011

– However, credit to FG declined by almost 28% on YTD in Dec. 2011

• Banks are now risk averse in lending

Credit

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

-20.00-10.00

0.0010.0020.0030.0040.0050.0060.0070.0080.00

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Pe

rce

nt

Aggregate Credit (RHS) ∆(YTD)

Credit to the Economy

N'b

n

CBN, EKA Research

-4,500.00-4,000.00-3,500.00-3,000.00-2,500.00-2,000.00-1,500.00-1,000.00-500.000.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Per

cen

t

Credit to Government Sector (RHS) ∆(YTD)

Credit to the Government

N'b

n

CBN, EKA Research

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Per

cen

t

Credit to Private Sector ∆(YTD)

Credit to the Private Sector

N'b

n

CBN, EKA Research

Fuel Subsidy Reduction

• Unsuccessful attempt to introduce deregulation – Price raised from N65/litre to N141/litre – National Strike leading to ‘reduction’ to N97/litre

• Higher prices will produce ‘savings’ of US$3.2bn annually instead of US$8bn if full deregulation had been introduced

• Transfer of US$3.2bn from consumers and business to government – Approximately 3% of spending by business and consumers will transfer to

government Exp. Pre-reduction Exp. Post-reduction Households Business US$158.8 US$ 155.6 Government 34.3 37.5 External Trade 46.4 46.4bn Total Expenditure US$239.5bn US$239.5bn Private spending is (78% of combined private and business spending)

This ignores the multiplier effect – private spending multiplier higher than government spending

Subsidy Reduction - Effect

Cost push inflation: Impact 2-3% on CPI Approximately the same as if fuel price was N141 per litre

Prices already adjusted on basis of N141/litre

Downward sticky prices

Lower household expenditure Effect is same as higher taxes – lower household consumption as

disposable and discretionary income fall

Government revenue will increase by $3.2bn

External Sector Import bill will fall from 15% of total imports to 12% of total

Trade surplus will increase and stabilise Naira at N160/$

Higher price of Forex, resulting in reduced REAL demand and fewer ‘scams’ will lead to possible 10% reduction in it’s demand

Pressure on exchange rate to ease not exceeding N160 in official market

Outlook Drivers

Outlook Drivers

• International Environment

– Indebtedness

– Commodity – especially, Oil – Prices

• Domestic Policies and Characteristics

– Political Environment

• Potential for unruly conversation around succession

– Policy Issues

• Fiscal Profile

• Monetary Policy – Interest & Exchange rates

– Liquidity Management

– Implicit inflation targeting

– Reducing exchange rate disequilibrium

…..Outlook Drivers

• Reform Agenda – Economic Competitiveness

– Energy: Petroleum Industry Bill (PIB); Deregulation of Fuel Prices; Progress on electricity availability

– PPP Framework

– Modernizing and de-risking the Agric Sector

– Inadequate framework for Human Capacity development

– Completion of the Financial Sector Reform

• Characteristics – Terms of trade deteriorating

– Population pressure –

» Difference between population growth and GDP growth narrows

– Income inequality increased

– Increasing competition

– Low capital formation

International Environment

• The Global economic environment has been good to Nigeria – thick dark clouds overhead – – Challenge of managing govt. indebtedness - witness the crisis in the

Euro-zone area; • Resulting in Bank recapitalisation; and restricted private access to credit

– Rising costs in Asia; – Delay in managing US Deficit as elections approach; – Political uncertainty as Middle East continues to pose threat to global

security

• These ‘dark clouds’ likely to result in – Slower global growth; – Lower demand for crude oil – see IEA; – Weaker commodity prices; – Greater uncertainty – Likelihood of protectionist sentiments

World GDP Growth 2012 Forecast (%)

• WEO September 2011

• WEO update January 2012

MENA

(+4.0) 3.2

Latin America

(+4.0) +3.6

SSA (+5.8) +5.5

Japan (+2.2) +1.7

Cen.& East. Europe

(+2.7) +1.1

Developing Asia (+8) +7.3

China (+9) +8.2

USA

(+1.8) +1.8

Western Europe

(-2.1) – 0.5 Canada

(+1.9) +1.7

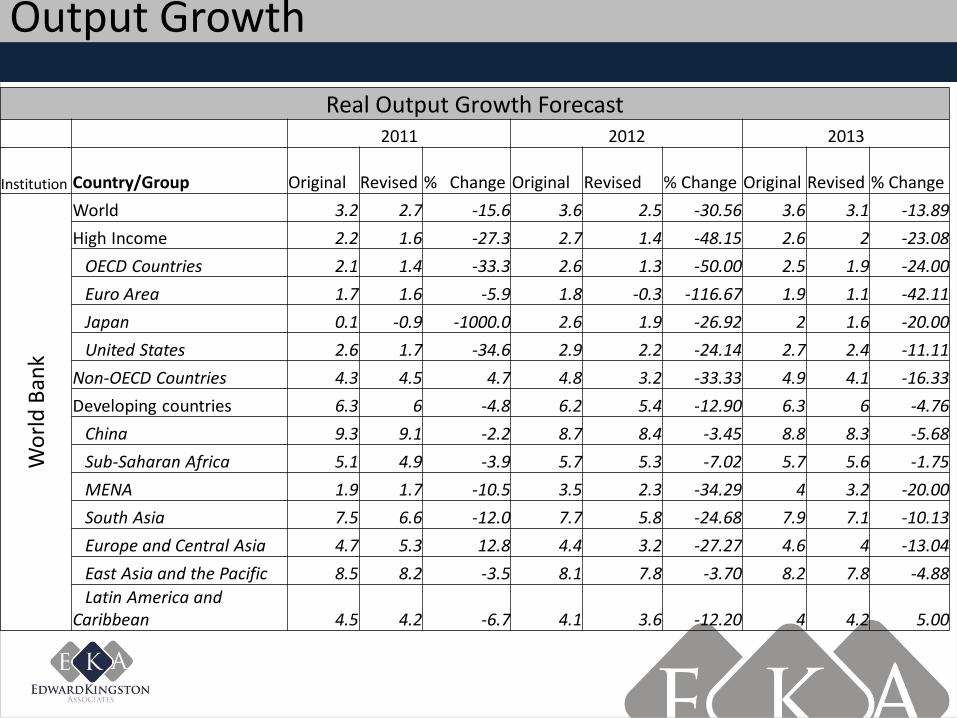

Output Growth

Real Output Growth Forecast 2011 2012 2013

Institution Country/Group Original Revised % Change Original Revised % Change Original Revised % Change

Wo

rld

Ban

k

World 3.2 2.7 -15.6 3.6 2.5 -30.56 3.6 3.1 -13.89

High Income 2.2 1.6 -27.3 2.7 1.4 -48.15 2.6 2 -23.08

OECD Countries 2.1 1.4 -33.3 2.6 1.3 -50.00 2.5 1.9 -24.00

Euro Area 1.7 1.6 -5.9 1.8 -0.3 -116.67 1.9 1.1 -42.11

Japan 0.1 -0.9 -1000.0 2.6 1.9 -26.92 2 1.6 -20.00

United States 2.6 1.7 -34.6 2.9 2.2 -24.14 2.7 2.4 -11.11

Non-OECD Countries 4.3 4.5 4.7 4.8 3.2 -33.33 4.9 4.1 -16.33

Developing countries 6.3 6 -4.8 6.2 5.4 -12.90 6.3 6 -4.76

China 9.3 9.1 -2.2 8.7 8.4 -3.45 8.8 8.3 -5.68

Sub-Saharan Africa 5.1 4.9 -3.9 5.7 5.3 -7.02 5.7 5.6 -1.75

MENA 1.9 1.7 -10.5 3.5 2.3 -34.29 4 3.2 -20.00

South Asia 7.5 6.6 -12.0 7.7 5.8 -24.68 7.9 7.1 -10.13

Europe and Central Asia 4.7 5.3 12.8 4.4 3.2 -27.27 4.6 4 -13.04

East Asia and the Pacific 8.5 8.2 -3.5 8.1 7.8 -3.70 8.2 7.8 -4.88

Latin America and Caribbean 4.5 4.2 -6.7 4.1 3.6 -12.20 4 4.2 5.00

….Output Growth

IMF Real Output Forecast

Institution

2011 2012 2013

Real Output Original Revised % change Original Revised % change Original Revised % change

Inte

rnat

ion

al M

on

etar

y Fu

nd

World 4.0 3.8 -3.9 4.0 3.3 -17.4 4.5 3.9 -12.7

Advanced economies 1.6 1.6 -0.8 1.9 1.2 -37.6 2.4 1.9 -20.2

USA 1.5 1.8 17.9 1.8 1.8 1.0 2.5 2.2 -13.3

Japan -0.5 -0.9 92.3 2.3 1.7 -26.2 2.0 1.6 -21.6 France 1.7 1.6 -3.1 1.4 0.2 -85.7 1.9 1.0 -46.4

Germany 2.7 3 10.1 1.3 0.3 -76.4 1.5 1.5 -0.1 UK 1.1 0.9 -20.8 1.6 0.6 -61.9 2.4 2.0 -15.6

Euro area 1.6 1.6 -1.2 1.1 -0.5 -146.0 1.5 0.8 -47.7

Greece -3.0 -5.0 65.0 1.08 -2.0 -285.4 2.1 1.5 -27.5 Emerging and developing economies 6.4 6.2 -3.0 6.1 5.4 -11.1 6.5 5.9 -8.9 Brazil 3.8 2.9 -23.1 3.6 3.0 -17.2 4.2 4.0 -3.7 China 9.5 9.2 -2.9 9.0 8.2 -9.3 9.5 8.8 -7.2 India 7.8 7.4 -5.6 7.5 7.0 -7.1 9.5 7.3 -23.1 Latin America and the Caribbean 4.5 4.6 1.5 4.0 3.6 -9.3 4.1 3.9 -4.2 MENA 4.0 3.1 -22.5 3.6 3.2 -11.3 4.3 3.6 -15.8

Sub-Saharan Africa 5.2 4.9 -5.3 5.8 5.5 -5.5 5.5 5.3 -3.8 Nigeria 6.9 6.9 -0.2 6.6 6.6 0.0 6.3 6.3 0.7

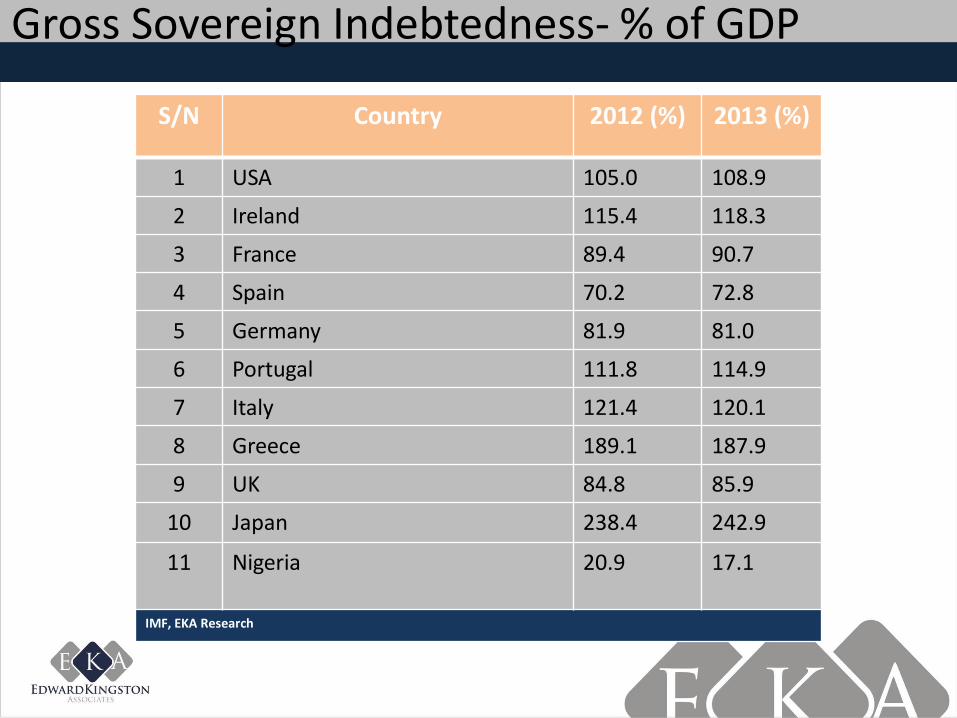

Gross Sovereign Indebtedness- % of GDP

S/N Country 2012 (%) 2013 (%)

1 USA 105.0 108.9

2 Ireland 115.4 118.3

3 France 89.4 90.7

4 Spain 70.2 72.8

5 Germany 81.9 81.0

6 Portugal 111.8 114.9

7 Italy 121.4 120.1

8 Greece 189.1 187.9

9 UK 84.8 85.9

10 Japan 238.4 242.9

11 Nigeria

20.9 17.1

IMF, EKA Research

Prices- Inflation

Institution

Average CPI, Inflation Forecasts

2011 2012 2013

Inte

rnat

ion

al M

on

etar

y Fu

nd

Original Revised % change Original Revised % change Original Revised % change

World 4.458 4.958 11.2 3.441 3.663 6.5 3.006 3.241 7.8

Advanced economies 2.23 2.613 17.2 1.671 1.44 -13.8 1.605 1.373 -14.5

USA 2.173 2.987 37.5 1.605 1.209 -24.7 1.403 0.903 -35.6

Japan 0.156 -0.37 -337.2 0.244 -0.48 -296.7 0.436 0.041 -90.6

France 2.143 2.146 0.1 1.724 1.4 -21.7 1.788 1.66 -7.2

Germany 2.186 2.236 2.3 1.527 1.3 -14.9 1.8 3.8 111.1

UK 4.2 4.513 7.5 1.997 2.439 22.1 2 2 0.0

Euro area 2.26 2.515 11.3 1.726 1.507 -12.7 1.762 1.652 -6.2

Greece 2.54 2.883 13.5 0.5 1.0 105.6 0.657 1 52.2

Emerging and developing economies 6.87 7.468 8.7 5.278 5.944 12.6 4.399 5.077 15.4

Brazil 6.268 6.589 5.1 4.777 5.2 7.8 4.498 4.152 -7.7

China 4.985 5.498 10.3 2.5 3.3 32.0 2 3 50.0

India 7.519 10.551 40.3 6.852 8.6 25.3 4.865 7.071 45.3

Latin America and the Caribbean 6.669 6.733 1.0 6.013 5.976 -0.6 5.602 5.395 -3.7

MENA 9.966 9.912 -0.5 7.302 7.599 4.1 6.069 6.509 7.2

Sub-Saharan Africa 7.796 8.432 8.2 7.311 8.329 13.9 6.411 6.35 -1.0

Nigeria 11.086 10.559 -4.8 9.45 8.977 -5.0 8.5 8.5 0.0

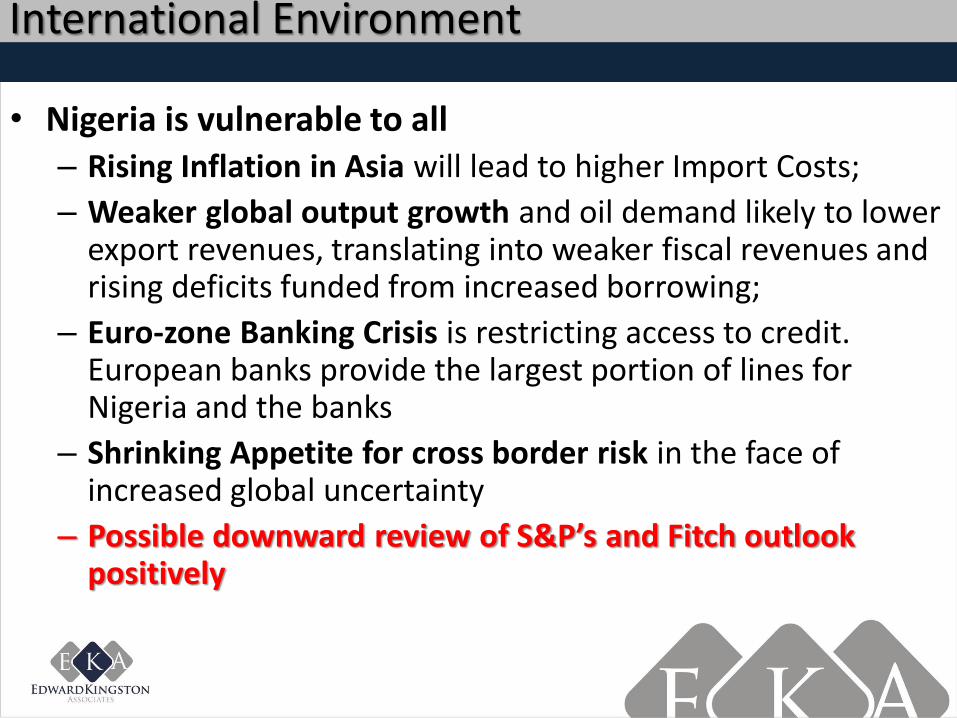

International Environment

• Nigeria is vulnerable to all – Rising Inflation in Asia will lead to higher Import Costs;

– Weaker global output growth and oil demand likely to lower export revenues, translating into weaker fiscal revenues and rising deficits funded from increased borrowing;

– Euro-zone Banking Crisis is restricting access to credit. European banks provide the largest portion of lines for Nigeria and the banks

– Shrinking Appetite for cross border risk in the face of increased global uncertainty

– Possible downward review of S&P’s and Fitch outlook positively

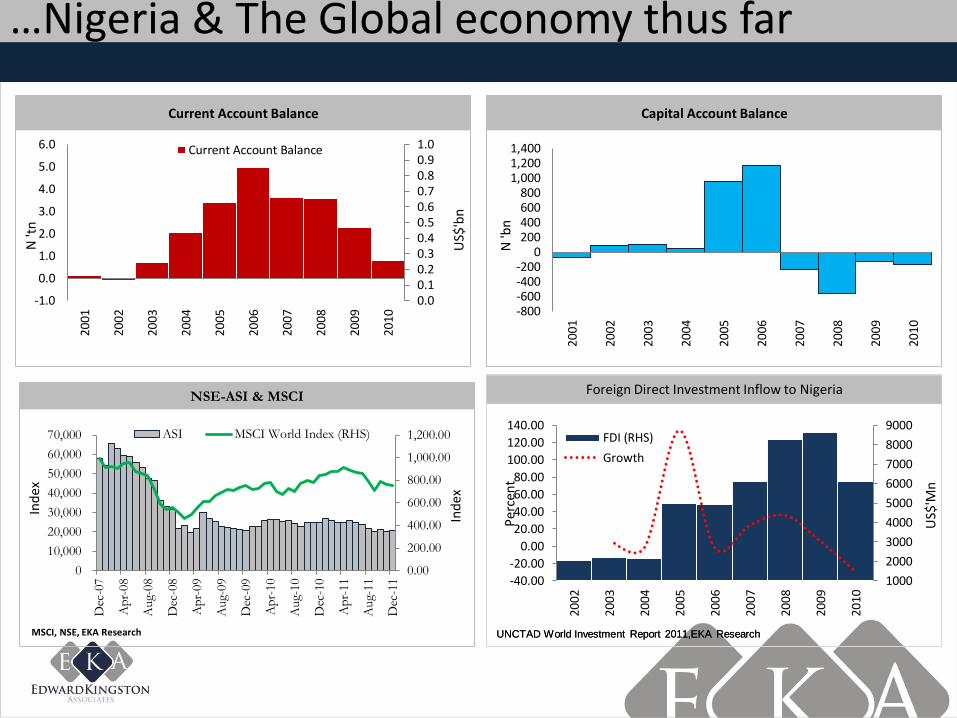

UNCTAD World Investment Report 2011,EKA Research

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

-800-600-400-200

0200400600800

1,0001,2001,400

Capital Account Balance

N 'b

n

0.00.10.20.30.40.50.60.70.80.91.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0 Current Account Balance

Current Account Balance

US$

'bn

N 't

n

1000

2000

3000

4000

5000

6000

7000

8000

9000

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

2002

2003

2004

2005

2006

2007

2008

2009

2010

FDI (RHS)

Growth

Foreign Direct Investment Inflow to Nigeria

US$

'Mn

Per

cen

t

…Nigeria & The Global economy thus far

UNCTAD World Investment Report 2011,EKA Research

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Dec

-07

Ap

r-08

Aug-

08

Dec

-08

Ap

r-09

Aug-

09

Dec

-09

Ap

r-10

Aug-

10

Dec

-10

Ap

r-11

Aug-

11

Dec

-11

ASI MSCI World Index (RHS)

NSE-ASI & MSCI

Ind

ex

Ind

ex

MSCI, NSE, EKA Research

Domestic Overview

• Domestic Overview – 2012 is the 1st full year for the GEJ Administration. – This is the best time to take the hard decisions

• Expect to see ‘hard’ measures pushed through – Is the reaction to petrol price deregulation going to be the standard

response?

• Preparations for 2015 elections ,which should begin mid-2013.,may already have begun.

– Key challenges revolve around • budget consolidation • Policy Changes • economic competitiveness

– infrastructure expansion and upgrade; – Human Capital Development; – Local Content

2012 Federal Govt. Budget Proposal

• President Jonathan proposes N4.749trn for 2012 – – 6% higher than 2011 amended budget.

• The budget assumes –

– Oil production of 2.48 mbpd up from 2.3mbpd for 2011;

– Benchmark oil price of US$75/bl

– Exchange rate of NGN155/US$;

– Projected GDP growth rate of 7.2%; and

– Projected single digit inflation rate of 9.5%.

– In 2012, Capital spending intended to grow faster than recurrent spending

– The Gross federally collectible revenue is projected at N9.406trn

• Of which FGN revenue is forecast at N3.644trn - 9% higher than 2011 estimate

• Non-oil revenue is expected to grow significantly in 2012 - Resulting from reform in revenue collecting agencies and initiative to further develop non-oil sectors

Budget Amendment

• FG revises 2012 budget to include fuel subsidy

– Total of N888.1bn to be expended on PMS and Kerosene in 2012, net addition of N733.1bn an increase of N25bn on proposed PMS subsidy.

– FG share of the projected expenditure stands at 43% while the states & LGs take 57%

• IGR increases by 13.6% to N446.78bn

…..2012 Federal Govt. Budget Proposal

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Per

cen

t

Total FGN Expenditure

Recurrent Expenditure

Capital Expenditure

Federal Government Budget Growth P

erce

nt

FMF, EKA Research

18.31

26.49

30.84

39

45.57

49.23

54.83

54.83

59.66

59.72

78.98

161.42

180.8

282.77

282.77

400.15

921.91

Communications Technology

Land & Housing

Science & Technology

Water Resources

FCTA

Aviation

Transport

Transport

Petroleum Resources

Niger Delta

Agriculture & Rural Development

Power

Works

Health

PTDF

Education

Security

Allocation to Critical Sectors

N'bn

…Policy Reforms- PHCN Liquidation

• Roadmap to power sector focuses on unbundling, to attracting private sector investment, increase job creation and promoting transparency.

• Current installed capacity to generate 6,000 MW of electricity of which only 3,600 is actually generated. 6852 MW

• Finally, 17 out of 18 companies were successfully privatised in Jan. 2012

– Workers redeployed from headquarters to successor companies of PHCN

Nigeria on the World Stage

Country Generation Capacity (GW) Watts per capita

S. Africa 40.498 826

Egypt 20.46 259

Nigeria 5.96 40 (25 available)

Ghana 1.49 62

USA 977.06 3,180

Germany 120.83 1468

UK 80.42 1316

Brazil 96.64 486

China 623.56 466

India 143.77 124

Indonesia 24.62 102

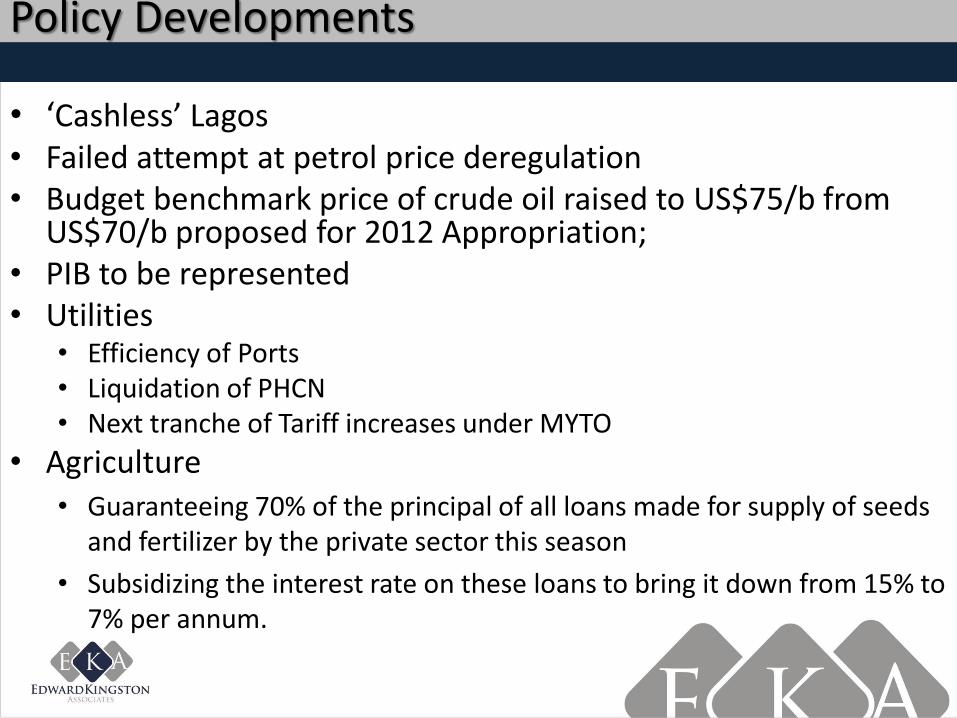

Policy Developments

• ‘Cashless’ Lagos • Failed attempt at petrol price deregulation • Budget benchmark price of crude oil raised to US$75/b from

US$70/b proposed for 2012 Appropriation; • PIB to be represented • Utilities

• Efficiency of Ports • Liquidation of PHCN • Next tranche of Tariff increases under MYTO

• Agriculture • Guaranteeing 70% of the principal of all loans made for supply of seeds

and fertilizer by the private sector this season

• Subsidizing the interest rate on these loans to bring it down from 15% to 7% per annum.

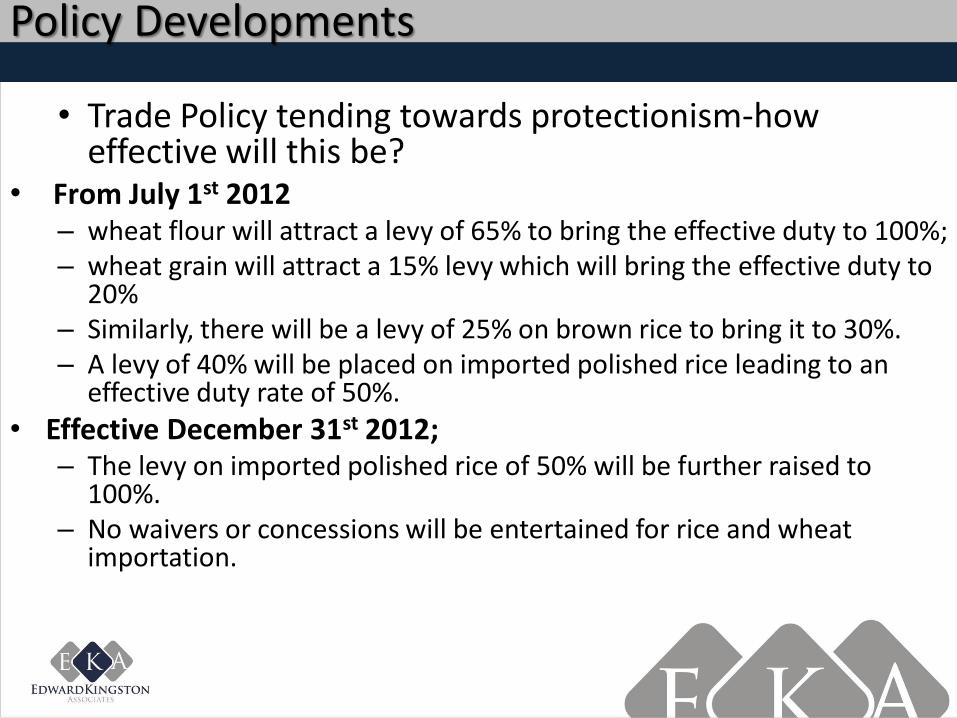

Policy Developments

• Trade Policy tending towards protectionism-how effective will this be?

• From July 1st 2012 – wheat flour will attract a levy of 65% to bring the effective duty to 100%; – wheat grain will attract a 15% levy which will bring the effective duty to

20% – Similarly, there will be a levy of 25% on brown rice to bring it to 30%. – A levy of 40% will be placed on imported polished rice leading to an

effective duty rate of 50%.

• Effective December 31st 2012; – The levy on imported polished rice of 50% will be further raised to

100%. – No waivers or concessions will be entertained for rice and wheat

importation.

Policy Developments

Import Substitution

• Bread-baking input substitution (Cassava flour to replace wheat flour),tax incentive of 12% if they attain 40% blending in 18months and prohibition of cassava flour effective from March 31st 2012.

• Importation of agricultural machinery and equipment; equipment and machinery in the power sector shall attract zero percent (%) duty from 31st January, 2012

• All cassava processing equipments shall be duty free with effect from 31st March, 2012

Cashless Lagos – Benefits & Costs

• Transactions • Increased transparency • Higher turnover/sales as the number of transactions rise because

the settlement period declines

• Transaction cost reduction

• Banks • Reduces the frequency of visits to banking halls –

• opportunity for better use of space • Reduction in number of bank employees

• Reduction in overheads as branches shrink • Opportunity for banks to set up terminals in strategic

locations and outlets

• Costs - Short-term • Teething problems occasioned by inadequate infrastructure

Likely Outcomes

• Fiscal Policy

– Likely to be very loose with revenues swelled by:

• Higher budget benchmark price of crude oil

• ‘Savings’ from subsidies; and

• Monetary Policy

– Greater emphasis on exchange rate management

– Likely to show acceptance of the need to recognize structural inflation arising from reform agenda

• Trade & Regulatory

– Tending towards protectionist

…Output - Sectors

• Output – Sectors

– Distribution(Wholesale and Retail) • Short-term slow-down as the expenditure impact of subsidy

reduction works its way through

• Industry to become more competitive

– Telecomms

• Expected to continue growing especially driven by data services

– Construction

• Will benefit for increased spending by government across the 3 tiers

– Financial Services

• Resolution of crisis in banking subsector almost completed-Portfolio Risk needs to be managed

• Insurance sub-sector should now become the focus of attention

... Likely Outcomes

• Income – Continuing to rise – Upward Concentration driven by unemployment and leading to

Greater inequality and creates challenges especially for firms in FMCG

• Expenditure – Short term

• Private sector expenditure likely to remain under pressure as – Unemployment, estimated at almost 24% of labour force, continues to

rise. – Fuel price deregulation will hit the middle class hardest

• Further shift to the government sector

– Medium term • Private expenditure will rise as growth recovers and the middle class

grows

Likely Outcomes - Costs

• Inflation likely to continue to be a challenge in 2012. – Driven by Structural rigidities and Imported costs

• Inflation rate for the Nigerian economy was 12.6% in January

• Inflation is a challenge in Asia which accounts for 33% of non-oil imports to Nigeria

• External value of the Naira likely to be more volatile. – Will remain within the band

– Volatility will depend on • oil sector parameters (price and quantity);

• government spending; and

• reserve strength

– Convergence across market segments

Likely Outcomes -

– Access to borrowing may ease • Removal of NPLs from Bank Balance sheets

• Pressure for performance on banks

• CBN efforts at de-risking the credit environment

• Refinancing windows

– Borrowing costs likely to remain high influenced by a combination of factors

• Removal of CBN guarantees on interbank market transactions at the end of Dec 2011;

• Limitation of NPL to 5% of credit portfolio combined with rising cost of borrowing likely to keep a lid on access to credit whilst raising its cost

• Defence of the Naira’s value

Thank You Q&A