Business Optimism Index Kuwait Q4 2009 Presented by Dun & Bradstreet South Asia Middle East Ltd...

16

Business Optimism Index Kuwait Q4 2009 Presented by Presented by Dun & Bradstreet South Asia Middle East Dun & Bradstreet South Asia Middle East Ltd (D&B) Muthanna Investment Company Ltd (D&B) Muthanna Investment Company (MIC) (MIC)

-

Upload

raegan-tibbett -

Category

Documents

-

view

218 -

download

3

Transcript of Business Optimism Index Kuwait Q4 2009 Presented by Dun & Bradstreet South Asia Middle East Ltd...

Business Optimism Index Kuwait Q4 2009

Presented by Presented by Dun & Bradstreet South Asia Middle East Ltd (D&B) Dun & Bradstreet South Asia Middle East Ltd (D&B) Muthanna Investment Company (MIC) Muthanna Investment Company (MIC)

Business Optimism Index

• The D&B Business Optimism Index is recognized world over

as an indicator which ascertains the pulse of the business

community

• Provides insight into the short-term outlook of businesses

on sales, profit growth, investment etc

• Provides analysis of major trends, outlook and issues

concerning businesses

Survey

• Sample of business units representing Kuwait’s economy was

selected

• 500 business owners and senior executives across business

units were surveyed

• Survey conducted during September 2009 for the 4th quarter of

2009

• Respondents were questioned about their expectations on

relevant business parameters

• Survey also captured respondent feedback on current business

conditions

World Economic Outlook

• IMF revises world economic growth to -1.06% in 2009, recovery expected in 2010

with 3.1% growth

• Advanced economies are expected to contract by 3.4% in year 2009, growth in 2010

projected at 1.3%

• World trade volumes set to expand in 2010 by 2.5%

• GCC growth to rebound to 5.2% in 2010

World Stock Markets

Kuwait’s economy

Source: IMF

Source: IMF

• Kuwait’s GDP to register a growth rate of 3.3% after contracting by 1.5% in 2009; Non-oil GDP to grow at 4.1% in 2010

• Drop in trade volumes, lower hydrocarbon prices and productions will lead to a contraction in exports by 32.59% in 2009, sharp recovery expected in 2010.

• Kuwait has posted a preliminary budget surplus of KWD 4.25 bn in first five months of the current fiscal on the back of firm oil prices

Business Optimism Indices : Q4 2009

• All parameters in the non-hydrocarbon sector register improvement in Q4 2009 as

compared to the previous quarter

• No improvement in the selling price outlook for Q4 2009 in the hydrocarbon sector;

Net Profits and Number of Employees optimism modest

All parameters in the hydrocarbon for Q4 2009 improve, Level of Selling Prices turns positives

Business Optimism Indices Trend

Manufacturing sector

• The Global Manufacturing Purchasing Managers’ Index stands at 53 in September

• Improvement in outlook for Q4 as compared to Q3

• 54% expect an increase in sales volumes, 51% foresee a better order book status and

54% of companies expect higher profits in Q4 2009

• A substantial 83% expect no change in selling prices in Q4 2009

Source: J P Morgan and market economics in association with ISM and IFPSM

Construction sector

• Construction sector worldwide is expected to be mainly driven by policy measures and

some stability in demand conditions

• Kuwait’s construction sector has displayed a strong rebound in outlook for all

parameters due to boost from government spending

• 58% of the respondents expect higher sales and a same number of respondents expect

higher profits in Q4 2009

Infrastructure construction growth 2008-13 compound annual growth (%)

Trade, restaurants & hotels sector

• Global trade & hospitality sector has been impacted due to rising

unemployment and falling consumer spending

• Expectations of higher sales boost profitability expectations despite a

bleak selling price outlook

• Level of Selling Prices parameter weakest among all sectors; 32%

foresee a drop in selling prices in Q4

• Drop in trade volumes has impacted the transport and logistics sector across the world

• Optimism about improvement in order books and rise in sales volumes lifts profitability expectations

• 29% of respondents foresee increase in Level of Selling Prices; BOI improves to 13

Transport & communication sector

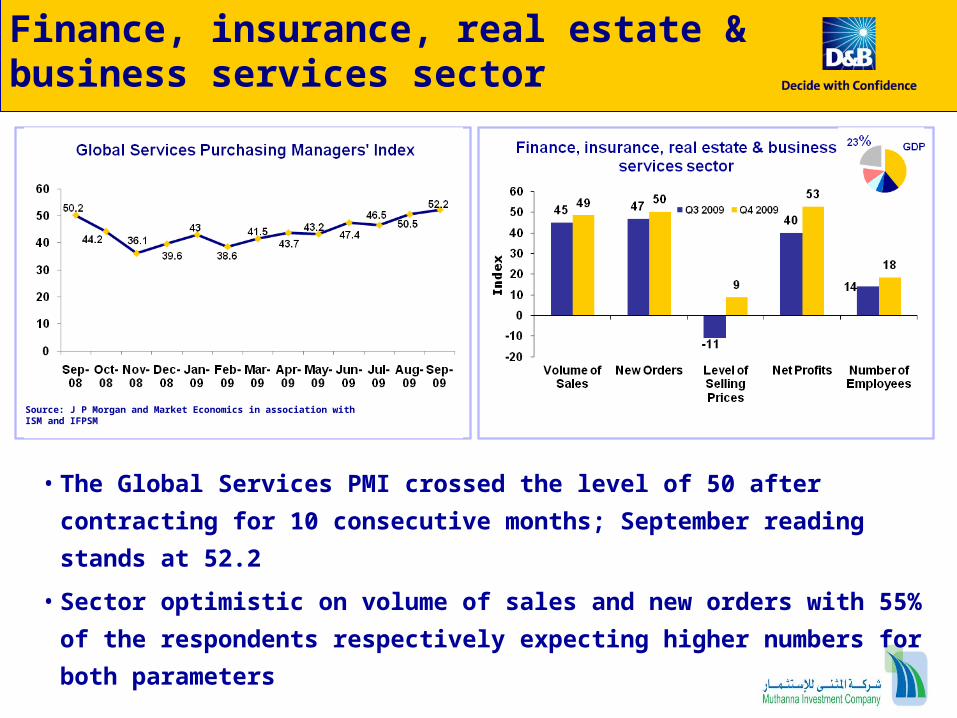

Finance, insurance, real estate & business services sector

• The Global Services PMI crossed the level of 50 after contracting for 10

consecutive months; September reading stands at 52.2

• Sector optimistic on volume of sales and new orders with 55% of the

respondents respectively expecting higher numbers for both parameters

Source: J P Morgan and Market Economics in association with ISM and IFPSM

Business Optimism Indices Trends : Hydrocarbon sector

• 84% of the firms expect selling prices to remain unchanged, 58% anticipate a rise in employee count

• 73% foresee higher profitability in Q4 2009

Other Key Highlights

• Availability of finance and raw material costs cited as leading

business concerns by the non-hydrocarbon sector

• 54% of the business units freeze investment outlays while

only 35% to invest in business expansion

• 43% of the business units in the non-hydrocarbon sector

expect borrowing conditions to improve

• Discovery & development cost identified as the chief concern

by 38% of the units in the hydrocarbon sector

Conclusion

• Business outlook for Q4 improves across sectors with emerging signs of global economic revival and government support through expansionary fiscal policy

• Activity in finance, insurance, real estate & business services sector is expected to improve with signs of increased liquidity in the international markets

• Optimism in the trade, restaurants & hotels sector gains traction as global trade improves

• Hydrocarbon sector uncertain on recent crude price rally amid weak fundamentals

THANK YOUTHANK YOU