BUSINESS DEVELOPMENTS NOVEMBER 10, 2010 -...

177

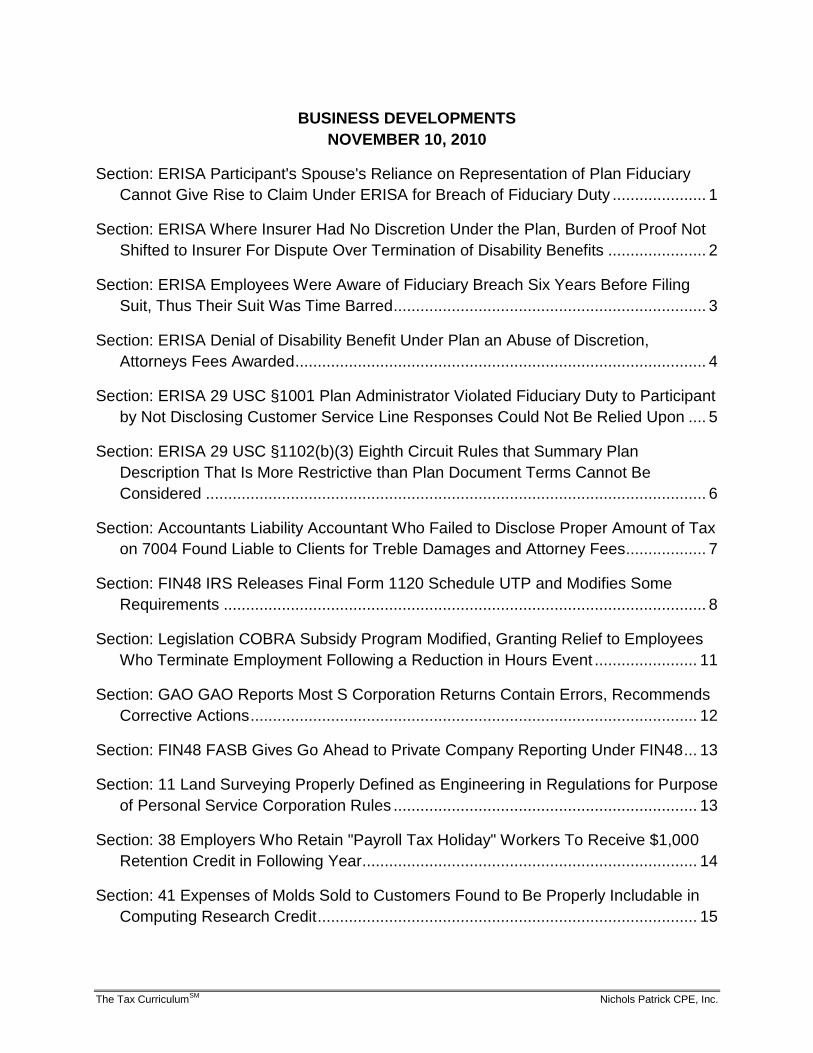

The Tax Curriculum SM Nichols Patrick CPE, Inc. BUSINESS DEVELOPMENTS NOVEMBER 10, 2010 Section: ERISA Participant's Spouse's Reliance on Representation of Plan Fiduciary Cannot Give Rise to Claim Under ERISA for Breach of Fiduciary Duty ..................... 1 Section: ERISA Where Insurer Had No Discretion Under the Plan, Burden of Proof Not Shifted to Insurer For Dispute Over Termination of Disability Benefits ...................... 2 Section: ERISA Employees Were Aware of Fiduciary Breach Six Years Before Filing Suit, Thus Their Suit Was Time Barred...................................................................... 3 Section: ERISA Denial of Disability Benefit Under Plan an Abuse of Discretion, Attorneys Fees Awarded............................................................................................ 4 Section: ERISA 29 USC §1001 Plan Administrator Violated Fiduciary Duty to Participant by Not Disclosing Customer Service Line Responses Could Not Be Relied Upon .... 5 Section: ERISA 29 USC §1102(b)(3) Eighth Circuit Rules that Summary Plan Description That Is More Restrictive than Plan Document Terms Cannot Be Considered ................................................................................................................ 6 Section: Accountants Liability Accountant Who Failed to Disclose Proper Amount of Tax on 7004 Found Liable to Clients for Treble Damages and Attorney Fees.................. 7 Section: FIN48 IRS Releases Final Form 1120 Schedule UTP and Modifies Some Requirements ............................................................................................................ 8 Section: Legislation COBRA Subsidy Program Modified, Granting Relief to Employees Who Terminate Employment Following a Reduction in Hours Event ....................... 11 Section: GAO GAO Reports Most S Corporation Returns Contain Errors, Recommends Corrective Actions .................................................................................................... 12 Section: FIN48 FASB Gives Go Ahead to Private Company Reporting Under FIN48 ... 13 Section: 11 Land Surveying Properly Defined as Engineering in Regulations for Purpose of Personal Service Corporation Rules .................................................................... 13 Section: 38 Employers Who Retain "Payroll Tax Holiday" Workers To Receive $1,000 Retention Credit in Following Year........................................................................... 14 Section: 41 Expenses of Molds Sold to Customers Found to Be Properly Includable in Computing Research Credit ..................................................................................... 15

Transcript of BUSINESS DEVELOPMENTS NOVEMBER 10, 2010 -...

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

BUSINESS DEVELOPMENTS

NOVEMBER 10, 2010

Section: ERISA Participant's Spouse's Reliance on Representation of Plan Fiduciary

Cannot Give Rise to Claim Under ERISA for Breach of Fiduciary Duty ..................... 1

Section: ERISA Where Insurer Had No Discretion Under the Plan, Burden of Proof Not

Shifted to Insurer For Dispute Over Termination of Disability Benefits ...................... 2

Section: ERISA Employees Were Aware of Fiduciary Breach Six Years Before Filing

Suit, Thus Their Suit Was Time Barred ...................................................................... 3

Section: ERISA Denial of Disability Benefit Under Plan an Abuse of Discretion,

Attorneys Fees Awarded ............................................................................................ 4

Section: ERISA 29 USC §1001 Plan Administrator Violated Fiduciary Duty to Participant

by Not Disclosing Customer Service Line Responses Could Not Be Relied Upon .... 5

Section: ERISA 29 USC §1102(b)(3) Eighth Circuit Rules that Summary Plan

Description That Is More Restrictive than Plan Document Terms Cannot Be

Considered ................................................................................................................ 6

Section: Accountants Liability Accountant Who Failed to Disclose Proper Amount of Tax

on 7004 Found Liable to Clients for Treble Damages and Attorney Fees .................. 7

Section: FIN48 IRS Releases Final Form 1120 Schedule UTP and Modifies Some

Requirements ............................................................................................................ 8

Section: Legislation COBRA Subsidy Program Modified, Granting Relief to Employees

Who Terminate Employment Following a Reduction in Hours Event ....................... 11

Section: GAO GAO Reports Most S Corporation Returns Contain Errors, Recommends

Corrective Actions .................................................................................................... 12

Section: FIN48 FASB Gives Go Ahead to Private Company Reporting Under FIN48 ... 13

Section: 11 Land Surveying Properly Defined as Engineering in Regulations for Purpose

of Personal Service Corporation Rules .................................................................... 13

Section: 38 Employers Who Retain "Payroll Tax Holiday" Workers To Receive $1,000

Retention Credit in Following Year ........................................................................... 14

Section: 41 Expenses of Molds Sold to Customers Found to Be Properly Includable in

Computing Research Credit ..................................................................................... 15

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 45R IRS Issues Explanations and Guidance for Small Employer Health

Insurance Credit....................................................................................................... 15

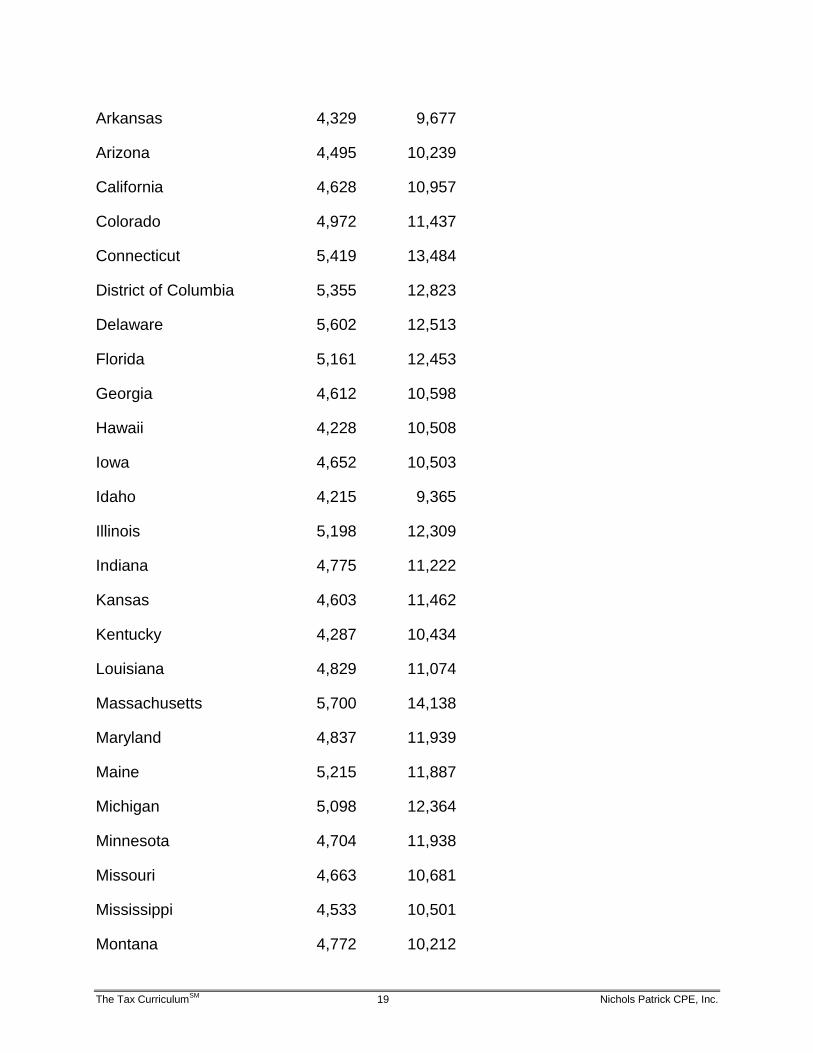

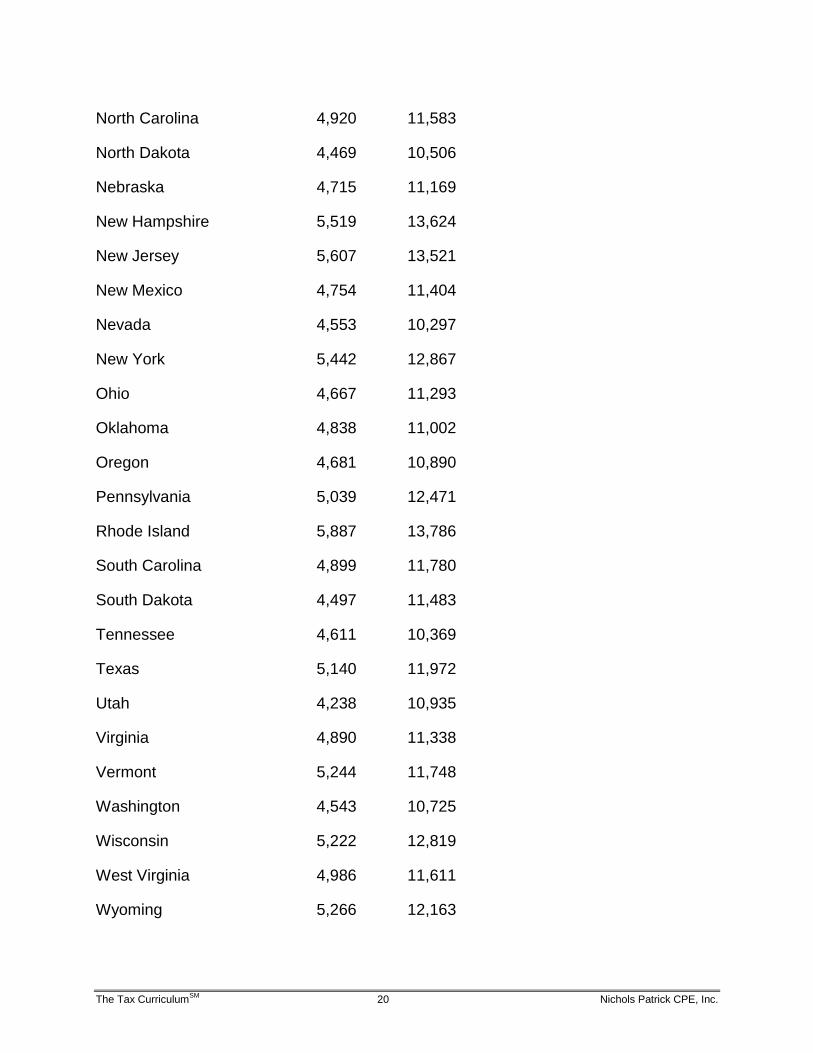

Section: 45R IRS Releases List of Average Premiums for Small Group Market for 2010

................................................................................................................................. 18

Section: 48 Covering Incorporated into Exterior Windows of High Rise Building Qualifies

for Energy Credit ...................................................................................................... 21

Section: 61 IRS Publishes Terminal Charge and SIFL Mileage Rates for July-December

2010 ......................................................................................................................... 21

Section: 61 IRS Sets Annual Limits On Value of Vehicles for Cents Per Mile Valuation

Rule ......................................................................................................................... 22

Section: 62 IRS Finds a Tool Reimbursement Plan They Like ...................................... 22

Section: 105 Spouse Was Participant in "Shared Enterprise" Rather than Employee,

Medical Reimbursement Deduction Denied ............................................................. 23

Section: 106 Guidance Issued Regarding Removal of Over-the-Counter Drugs Obtained

Without a Prescription from Eligible Expenses for HSAs, MSAs, HRAs and medical

FSAs ........................................................................................................................ 24

Section: 106 Current Employer's Payment of Employee's Premiums for COBRA

Coverage from Prior Employer Generally Excludable From Income. ....................... 25

Section: 108 Treatment of §108(i) Debt Issues for S Corporations and Partnership

Issued by IRS .......................................................................................................... 25

Section: 108 C Corporation Treatment of §108(i) Acceleration Rule Addressed in

Temporary and Final Regulations ............................................................................ 27

Section: 108 Debt Secured by Single Member LLC Holding Only Real Estate Can

Qualify for Qualified Real Property Business Indebtedness ..................................... 29

Section: 108 IRS Finalizes S Corporation Reduction of Attributes Regulations When

Debt Discharge Excluded from Income Under §108 ................................................ 30

Section: 108 Deferral of Cancellation of Indebtedness Rules Explained ....................... 31

Section: 125 Medical FSA Full Reimbursement Available During Employment Period

Even if Employee Discharged Before Year End ...................................................... 32

Section: 132 Taxpayer Allowed to Exclude Value of Clothing and Accessories Provided

to Employee as De Minimus Fringe-But the Facts of the Case Matter ..................... 33

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 132 IRS Delays Effective Date of Debit Card and Smartcard Revenue

Procedure Used for Transportation Benefit .............................................................. 34

Section: 162 Payments to Investors to Not Redeem Shares Were Deductible Until Clear

Agreements Were Reasonably Expected to Be Renewed at Termination ............... 34

Section: 162 Owner's Compensation Found Reasonable in Profitable Year, But

Unreasonably High in Loss Year.............................................................................. 35

Section: 162 Taxpayer Not Allowed to Treat Reserve Arrangement With One Subsidiary

of AIG as Part of Insurance Policy with Other Subsidiary and Claim Full Current

Deduction ................................................................................................................. 37

Section: 162 No Deduction Allowed for Payments to Purported 419 Plan Far in Excess

of Annual Benefit Promised Under the Plan ............................................................. 38

Section: 162 Payments to Purported Management Corporation Disallowed ................. 39

Section: 165 Utility Should be Allowed Casualty Loss Deduction Currently Even Though

State Granted Rate Increase to Allow Recovery of Loss ......................................... 40

Section: 165 Lots That Could Not Be Accessed Not Properly Treated as Worthless Due

to Reasonable Prospect of Recovery ....................................................................... 40

Section: 167 SILO Transaction Lacked Any Economic Substance Apart from Tax

Benefits .................................................................................................................... 41

Section: 168 Street Lights Properly Classified by Electric Utility as Seven Year Property

................................................................................................................................. 42

Section: 168 Coordinate Issue Paper Holds That Proper Recovery Period for Open Air

Parking Structures is 39.5 Years, Not 15 Years ....................................................... 43

Section: 172 IRS Adds to Guidance for ARRA and WHBAA Net Operating Loss

Elections .................................................................................................................. 43

Section: 172 Options for Five Year Net Operating Losses for Consolidated Groups

Explained ................................................................................................................. 45

Section: 172 Dentists Repayments of Amounts Received from Insurance Fraud

Committed by Spouse Gave Rise to Business Expenses and Net Operating Loss . 45

Section: 172 Revised Elective 5 Year Net Operating Loss Added By Congress ........... 46

Section: 179 Truck Lease Not Equivalent to Sale, No Section 179 Deduction Allowed 47

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 179 $250,000 §179 Amount Extended Through End of 2010 ......................... 48

Section: 197 Designation of Vineyard as an American Viticultural Area Can Give Rise to

a §197 Intangible ..................................................................................................... 48

Section: 197 Taxpayer's Income from Sale of Customer Relationships That Could Be

Shown to Be Self-Created Not Subject to §1245 Recapture .................................... 49

Section: 197 15 Year Amortization of Agreement Not to Compete Required for

Acquisition of Any Sized Interest in a Trade or Business ......................................... 50

Section: 199 Production of Genetically Modified Material Qualifies for §199 Treatment,

But Only Minor Amount of Licensing Arrangement Would ....................................... 51

Section: 263 IRS Defines Safe Harbor Accounting Methods for Inventory for Auto

Dealers .................................................................................................................... 52

Section: 263 Manufacturer Required to Capitalize Incentive Payments Paid to

Customers Only for Contracts with Minimum Purchase Clause ............................... 53

Section: 263A Packaging Material Costs Must Be Capitalized, But Taxpayer Only Has

to Adjust Prospectively Due to Prior Letter Ruling ................................................... 54

Section: 263A Tax Court Ruling Requiring Capitalization of Royalty Payments Triggered

on Sale under §263A Reversed by Second Circuit .................................................. 54

Section: 274 IRS Adds "Public Safety Officer Vehicle" to List of Qualified Nonpersonal

Use Vehicles ............................................................................................................ 55

Section: 274 IRS Announces Auto Mileage Rates for 2010 .......................................... 56

Section: 274 IRS Updates Per Diem Rates for New Fiscal Year ................................... 56

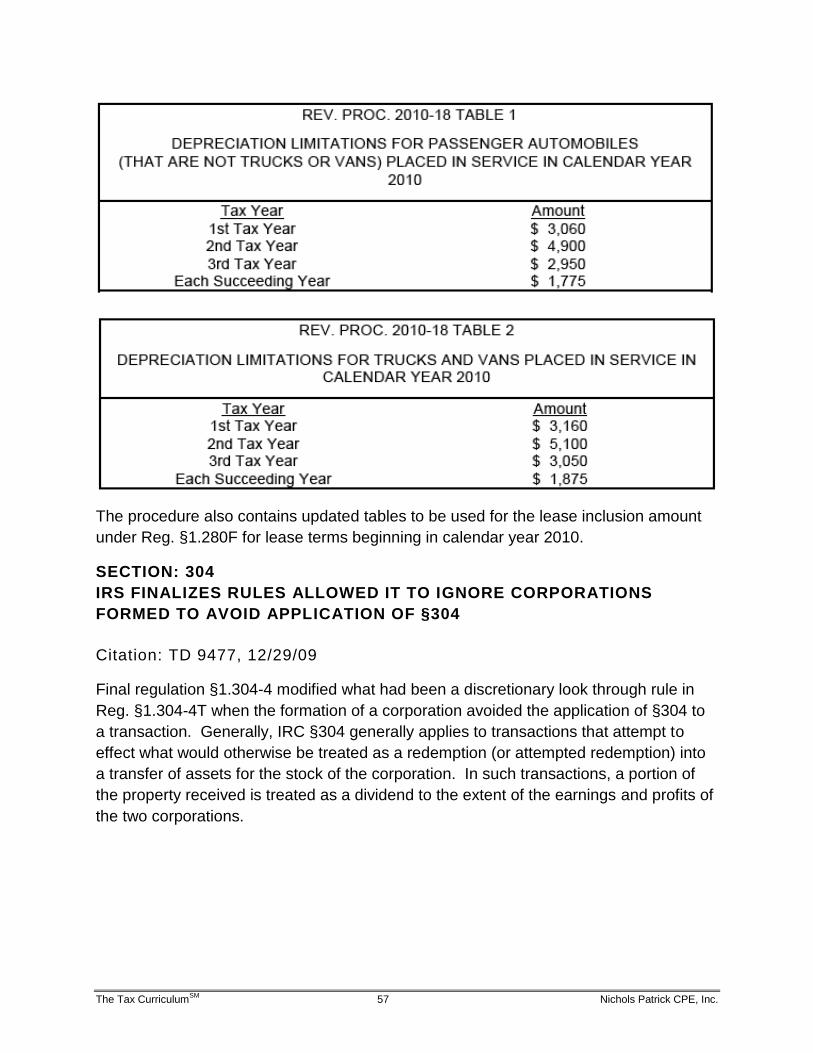

Section: 280F IRS Announcing Depreciation and Lease Inclusion Amounts on Vehicles

for 2010 .................................................................................................................... 56

Section: 304 IRS Finalizes Rules Allowed It to Ignore Corporations Formed to Avoid

Application of §304 .................................................................................................. 57

Section: 316 Auto Titled in Shareholder Name Treated as Corporate Asset, and Date of

Check Determined by Date on Check Not Date Deposited by Shareholder ............ 58

Section: 351 Taxpayers Did Not Transfer Farming Activity to New Corporation, Income

Taxable to Shareholders Directly ............................................................................. 59

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 368 Revised Regulations Provide for Issuance of Deemed Share of Stock in D

Reorganization Where No Stock is Issued ............................................................... 59

Section: 401 IRS Announces Pension Plan Limitations for 2011 .................................. 60

Section: 401 Sixth Circuit Reverses Previous Position, Now Holds Equitable Estoppel

Can Apply to ERISA Pension Cases ........................................................................ 61

Section: 401 Department of Labor Relents, Allows Third Service Providers to Complete

and Electronically File Electronic 5500s for Clients.................................................. 62

Section: 401 Plan Administrator's Revised Interpretation of Plan Terms Still Must be

Granted Deference by Court Even if Initial Interpretation Found to Be Unreasonable

................................................................................................................................. 63

Section: 401 Adopters of Pre-Approved Defined Benefit Plans Will Have Until April 30,

2012 to Adopt Restated Version of Plans ................................................................ 64

Section: 401 IRS Releases Question and Answer Guidance on Implementing Provisions

of the 2008 HEART Act ............................................................................................ 64

Section: 402 Value of Life Insurance Policy Distributed from Qualified Plan Is Not

Reduced by Surrender Charges .............................................................................. 65

Section: 404 Eighth Circuit Again Denies Deduction to Corporation for Amounts Paid to

ESOP to Redeem Stock .......................................................................................... 66

Section: 409A IRS Analyzes Requests for Distributions to Determine If They Were

Unforeseeable Emergencies .................................................................................... 67

Section: 409A Relief Granted for Certain Documentation Issues Related to Nonqualified

Deferred Compensation Plans ................................................................................. 67

Section: 411 Modifications to Welfare Plan Held to Be Constructive Amendment to

Pension Plan that Violated Anti-Cutback Rule ......................................................... 69

Section: 415 IRS Announces 2010 Qualified Plan Inflation Adjusted Limits .................. 70

Section: 419 §419A(f)(6) Plan Revised to Eliminate Attempt at Qualification as 10 or

More Employer Plan Ruled No Longer Similar to Listed Transaction ...................... 70

Section: 446 IRS Announces Release of New Form 3115 That Will Generally Be

Required to Be Used for Requests After May 30, 2010. .......................................... 71

Section: 446 Change in Timing of Reporting Advance Payments on Applicable Financial

Statements is an Accounting Method Change for §446 ........................................... 72

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 451 Taxpayer Who Received Check in 2006 Could Not Show Substantial

Restrictions Existed and Had To Include in 2006 Income Though Not Cashed Until

2007 ......................................................................................................................... 72

Section: 451 Taxpayer Can Use Deferral Method of Revenue Procedure 2004-34 for

Prepaid Royalties Received in Lawsuit Settlement .................................................. 73

Section: 453 Taxpayer Granted Permission by IRS to Accelerate Recovery of Basis

Under Contingent Sales Price Installment Agreement ............................................. 74

Section: 460 Extended Maintenance Period on Road Paving Job Not Eligible for

Percentage of Completion Treatment for Tax Purposes .......................................... 75

Section: 461 Amounts Due Under Bonus Plan That Required Employees Remain

Employed Until Date of Payment Could Not Be Accrued Despite Requirement That

Amounts Not Paid to Employees Be Paid to Charity................................................ 76

Section: 465 At Risk Amount for Leasing Activity Did Not Include Amount Due on

Promissory Note for RV Not Owned by LLC or Used in LLC's Leasing Activity ....... 76

Section: 469 Participation by Trustee of Trust, and Not of Beneficiaries, Is Measured to

Determine Material Participation by Trust ................................................................ 77

Section: 472 Method of Properly Identifying Items for Creation of LIFO Pools for a

Vineyard Detailed ..................................................................................................... 78

Section: 481 Taxpayer Not Allowed to Submit Request to Change Accounting Method in

Current Year When IRS on Exam Disputed Whether Taxpayer Had File for

Permission in Prior Year .......................................................................................... 78

Section: 481 IRS Updates List of Automatic Accounting Method Changes ................... 79

Section: 481 Auto Dealers Losing a Franchise May Elect to Terminate LIFO and Spread

Adjustment Over Four Years ................................................................................... 79

Section: 482 IRS Chastised for Poorly Supported Position on Value of Intangibles

Transferred and Use of Temporary Regulations Issued 10 Years After the

Transaction .............................................................................................................. 80

Section: 501 Virtual Congregation Not Sufficient For Religious Organization to Qualify

as a Church Under the IRC ...................................................................................... 81

Section: 501 Bluetooth Certification Group Did Not Qualify as Tax Exempt Business

League ..................................................................................................................... 82

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 501 Foundation to Provide Single Donor's Sperm Free of Charge to Selected

Applicants Properly Denied Tax Exempt Status ...................................................... 83

Section: 512 Operation of Beach House and Parking Lot Were Unrelated-Business

Income for Homeowners Association ....................................................................... 84

Section: 512 Computer Software Intellectual Property Developed for Internal Use by

Church Was Not Unrelated Business Income When Sold ....................................... 85

Section: 512 VEBA Cannot Avoid Limit on Exempt Function Income By Claiming

Investment Income Used to Pay Benefits ................................................................ 85

Section: 565 IRS Allows Corporation to Make Late Consent Dividend Election for PHC

When Finally Advised of the Option Two Years Later .............................................. 86

Section: 704 §704(c) Anti-Abuse Rules Added by IRS to Regulations .......................... 87

Section: 705 Taxpayer's Initial Victory on Option Loss Generating Partnership Reversed

by Tenth Circuit ........................................................................................................ 88

Section: 705 Basis Calculation is a Cumulative and Not Year by Year Calculation When

Applying "Not Below Zero" Limit Found in §705(b) .................................................. 89

Section: 707 Transfer of Subsidiary to Partnership Was a Disguised Sale ................... 89

Section: 707 Investors Were Actually Partners, and There Was Not a Disguised Sale of

State Tax Credits ..................................................................................................... 90

Section: 707 Transfer of Assets to Partnership Followed by Pledge of Interest to

Receive Nonrecourse Loan and Related Put Held to Be Disguised Sale ................ 91

Section: 752 Son-of-BOSS Transaction Found to Lack Economic Substance, so Issue

of Retroactive Application of Reg. §1.752-6 Not Relevant. ...................................... 92

Section: 851 Discharge of Indebtedness Income From Requiring Debt by Regulated

Investment Company Held to Be Qualifying Income ................................................ 93

Section: 864 Worldwide Allocation of Interest Delayed Yet Again ................................. 93

Section: 881 Guarantee Fees Paid to Foreign Parent Corporation Held Not to Be U.S.

Source Income ......................................................................................................... 94

Section: 1001 Transfers of Building on Owned Land Were Sales, Those on Leased

Land Were Not ......................................................................................................... 94

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 1031 Exchange Had Principal Purpose of Tax Avoidance, Deferral of Gain Not

Allowed .................................................................................................................... 95

Section: 1031 Pollution Control Credits Treated As Like Kind Property ........................ 96

Section: 1031 Leasing Company Could Not Avoid Recognizing Gain on Exchange Via

Qualified Intermediary to Acquire Equipment from Related Dealer .......................... 97

Section: 1221 Taxpayer's Ignorance of Need to Specifically Identify Hedging

Transactions Not "Inadverent Error" Allowing Treatment as Ordinary Losses ......... 98

Section: 1361 Stockholder Agreement Providing for Distributions to Pay Tax in

Accordance With Interest for Year Tax Arises Does Not Create Second Class of

Stock ........................................................................................................................ 98

Section: 1361 Merger of Parent into QSUB Was an F Reorganization, S Election Not

Terminated ............................................................................................................... 99

Section: 1361 Roth IRA Account is Not an Eligible S Corporation Shareholder .......... 100

Section: 1362 Corporation Removal of Guarantee of Return of Principal to Single

Shareholder Was Treated by IRS as Reason to Treat Termination as Inadvertant 100

Section: 1362 IRS Allows Late Election When Individuals Who Signed S Election Only

Believed They Were Shareholders ........................................................................ 101

Section: 1362 IRS Rules That Termination of S Election Due to Excess Passive Income

Was Inadvertent ..................................................................................................... 101

Section: 1362 S Corporation Shareholder Agreement Served to Preserve S Status

Despite Attempt to Transfer Shares to Ineligible Shareholder ............................... 102

Section: 1362 Trust That Erroneously Elected QSST Rather than ESBT Status Allowed

to Correct Error and Corporation Remained an S Corporation .............................. 103

Section: 1363 Section 291 Does Not Apply to Limit Deduction for Interest Paid on Debt

to Acquire Qualified Tax Exempt Securities for QSUB With S Status More than 3

Years ..................................................................................................................... 103

Section: 1363 LIFO Recapture Tax Does Not Apply to Proprietorship Electing S Status

Immediately Following §351 Incorporation ............................................................. 104

Section: 1366 Taxpayer's Inability to Show Basis, Combined with Fact that Debt

Guarantee Doesn't Create Basis, Means No S Corporation Loss Deduction......... 105

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 1367 Contribution of Capital Not Treated As Either Tax Exempt Income for S

Corporation Debt Basis Or Loss Under §165 ......................................................... 106

Section: 1374 Linked Prepaid Variable Forward Contract and Share Lending Agreement

Triggered Immediate Gain Recognition in Built In Gain Measurement Period ....... 107

Section: 1374 Price Paid Nine Months After S Election Was a Factor, But Did Not By

Itself, Establish Value at S Election Date for Built In Gain Tax .............................. 108

Section: 1402 IRS Protective Assertion of FICA Tax Due From S Corporation Did Not

Prohibit IRS From Later Arguments Payments Were Personal Self-Employment

Income ................................................................................................................... 109

Section: 3101 IRS Not Limited to Assessing Payroll Taxes Only Against Designated as

Compensation in Corporate Minutes for S Corporation ......................................... 110

Section: 3102 Owner of Company Held Liable for Payroll Taxes on Individuals He

Claimed Were Independent Contractors ................................................................ 110

Section: 3111 Qualified Employees Must Sign New Form W-11 or a Similar Affidavit For

Employer to Claim HIRE Act FICA Relief ............................................................... 111

Section: 3111 Employers Hiring Certain Individuals Not Responsible for Employer

Social Security for That Employee Through End of 2010 ...................................... 112

Section: 3121 Service Providers Working at Spa Held Not To Be Employees ............ 113

Section: 3121 IRS No Longer to Contest Claims for Refunds of FICA Taxes Paid to

Medical Residents Prior to April 1, 2005 ................................................................ 114

Section: 3121 Disagreeing with Federal Circuit Court of Appeals, Michigan District Court

Holds that Severance Payments Not Subject to FICA ........................................... 114

Section: 3121(b)(20) Performance of Repair Services for Boat Owner Did Not Render

Crew Member an Employee .................................................................................. 115

Section: 3302 Taxpayer Who Relied On Payroll Service Unable to Show State

Unemployment Taxes Actually Paid, Therefore Loses FUTA Credit...................... 116

Section: 3401 Public Officials Paid a Salary Are Employees Regardless of Status Under

Traditional Common Law Employee Test .............................................................. 117

Section: 4965 Final Regulations for Tax Exempt Entities That Participate in Prohibited

Tax Shelter Transactions Issued, 7/2/10 ................................................................ 117

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 4975 Disclosures of Fees Required by Service Providers to Qualified Plans,

Including Accountants and Auditors ....................................................................... 118

Section: 4980B COBRA Subsidy Period Extended and Expanded ............................. 120

Section: 6001 IRS Begins Accepting (and Potentially Demanding) Taxpayer Records in

Electronic Format ................................................................................................... 121

Section: 6011 IRS Updates List of "Transactions of Interest" and "Listed Transactions"

............................................................................................................................... 122

Section: 6031 IRS Adds New Inquiries and New Schedule B-1 to 2009 Form 1065 ... 122

Section: 6039 IRS Publishes Final Regulations on Reporting ISOs and ESPP Options

with First Reports Required for Calendar Year 2010 ............................................. 123

Section: 6050N Website that Keeps Percent of Charge Established by Artist When

Selling Music Must Report Net Paid to Artist on Form 1099 .................................. 123

Section: 6051 IRS Will Not Penalize Employers For Failing to Report Cost of Employer

Paid Health Care on 2011 Forms W-2 ................................................................... 124

Section: 6053 IRS Extends Attributed Tip Income Program Through December 31, 2011

............................................................................................................................... 125

Section: 6109 IRS Adds Requirement to List Name and Identifying Number of

Responsible Party When Applying for EIN ............................................................. 125

Section: 6205 Procedures for Correcting Employment Tax Errors In Various Situations

Explained by IRS ................................................................................................... 126

Section: 6226 Tax Court Had Jurisdiction to Determine Partnership a Sham, But Not to

Determine Affect on Individual Partners' Basis ...................................................... 127

Section: 6229 Fees Paid Related to Son of BOSS Partnership Transaction Transaction

Billed to S Corporation Nevertheless Is An Affected Item ...................................... 127

Section: 6231 Items Affecting Nonpartners Not Affected Items Nor Properly Handled Via

TEFRA Procedures ................................................................................................ 128

Section: 6231 Designation of a Tax Matters Partners on a 1065 By Partnership

Otherwise Exempt from Unified TEFRA Procedures Does Not Serve As Election to

Have Procedures Apply ......................................................................................... 128

Section: 6231 IRS Required to Issue Notice of Deficiency if No Partnership Item is

Changed, but Error Was Harmless ........................................................................ 129

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 6302 Paper Federal Tax Deposit Coupons To Be Eliminated Effective in 2011,

Businesses Must Deposit Virtually All Federal Taxes Electronically ...................... 130

Section: 6330 Appeals Officer's Admitted Lack of Understanding of Transcript Relied

Upon to Verify Tax Assessment Found Sufficient to Overturn CDP Hearing Holding

Against Taxpayer ................................................................................................... 130

Section: 6331 California Stop Notice To Be Treated as Superior to Federal Tax Lien 131

Section: 6331 Failure to Immediately Honor Levy Makes Medical Clinic Liable for

Amounts Not Paid Over ......................................................................................... 132

Section: 6501 Gross Receipts Not Reduced By Returns or Allowances for Purposes of

25% Test for Six Year Statute ................................................................................ 132

Section: 6501 Credits Carried Back After Release of Credit from Net Operating Loss

Carryback to Later Year Do Open Year to Assessment ......................................... 133

Section: 6501 IRS, After Losing in Court, Revises Regulations to Redefine an

Overstatement of Basis as Creating an Understatement of Income Under

§6501(e)(1)(A) ....................................................................................................... 134

Section: 6601 Taxpayer Cannot Elect to "Redesignate" Application of Overpayment

After Return is Filed ............................................................................................... 135

Section: 6621 Consolidated Group Not Eligible for Interest Netting With Overpayments

from Subsidiaries Acquired After Year of Underpayment ....................................... 135

Section: 6652 Exempt Organization Late Filing Penalty Is To Be Either Completely

Abated Due to Reasonable Cause or Applies in Full ............................................. 136

Section: 6656 Taxpayer Reasonably Relied on Erroneous Advice from CPA Regarding

Payroll Issues, Penalties Waived ........................................................................... 137

Section: 6662 Taxpayer Could Not Reasonably Rely on Advice from Two Accountants

When Taxpayers Provided Neither With All Relevant Facts .................................. 137

Section: 6662 Corporation's Reliance on Opinion Letter From CPA Firm Involved In

Structuring Transaction Not Reasonable, Penalties Applied .................................. 139

Section: 6662 Executor Reasonably Relied Upon Preparer, Was Unaware Preparer Had

Been Disbarred by OPR ........................................................................................ 140

Section: 6662A Penalties Apply to Reportable Transaction, Did Not Violate Due Process

............................................................................................................................... 141

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 6665 Large Corporate Estimated Taxes Due in July, August and September of

Three Years Accelerated ....................................................................................... 142

Section: 6672 Owner Who Lacked Signature Authority Over Checking Account Held

Liable for Responsible Person Penalty .................................................................. 142

Section: 6698 & 6699 Penalties Increased Dramatically for Late Filed Partnership or S

Corporation Returns ............................................................................................... 143

Section: 6901 Buyer of Corporate Assets Found Not Liable for Tax of Seller Under

Transferee Liability Theory .................................................................................... 143

Section: 7206 Taxpayer Who Admitted He and Preparer Had "Agreed to Cover Each

Other's Backs" Properly Convicted of Filing False Returns and Conspiracy .......... 145

Section: 7422 Characterization of Transaction as Sham a Partnership Item, Statute of

Limitations Defense Not Available to the Individual Partners in Refund Action ...... 146

Section: 7422 IRS Settlement Did Not Amount to Concession on Sham Transaction

Doctrine or That Sham Transaction Issue Not a Partnership Item ......................... 147

Section: 7430 Attorneys Fees Awarded for Initial IRS Postion, But Not for Second

Position Taken Following Rejection of First ........................................................... 148

Section: 7602 DC Circuit Rules Disclosures to Auditors Did Not Remove Work Product

Privilege ................................................................................................................. 149

Section: 7602 Supreme Court Declines to Review Holding that Tax Accrual Workpapers

Not Protected by Work Product Privilege ............................................................... 150

Section: 7701 Late Request For Automatic Relief Under Rev. Proc. 2009-41 Should

Result in Change Effective Exactly 3 Years and 75 Days Prior to Date of Request

............................................................................................................................... 151

Section: 7701 IRS Liberalizes Relief for Late Entity Elections Under Check the Box

Rules ...................................................................................................................... 152

Section: 7805 Failure to Properly Answer Question About Controlled Entities Allowed

IRS to Retroactively Revoke Plan's Determination Letter ...................................... 152

Section: 9100 Taxpayer That Accidentally Neglected to Scan Required 3115 to Submit

with Efiled Return Granted Reprieve ...................................................................... 153

Section: 9100 IRS Grants Taxpayer Permission to File Copy of 3115 with National

Office After Due Date ............................................................................................. 154

The Tax CurriculumSM

Nichols Patrick CPE, Inc.

Section: 9815 Preventive Care Must Be Provided Without Cost Sharing in Group Health

Plans ...................................................................................................................... 155

Section: 9815 Temporary Regulations Give Requirements for Preexisting Conditions,

Benefit Limits and Rescissions Following Patient Protection and Affordable Care Act

............................................................................................................................... 156

Section: 9815 Temporary Regulations Outline Requirements for Grandfathered Health

Care Plans and Policies ......................................................................................... 159

Section: 9815 Temporary Regulations Outline Requirements for Meeting Age 26 Test

for Group Health Plans that Offer Dependent Coverage ........................................ 163

The Tax CurriculumSM

1 Nichols Patrick CPE, Inc.

SECTION: ERISA

PARTICIPANT'S SPOUSE'S RELIANCE ON REPRESENTATION OF PLAN

FIDUCIARY CANNOT GIVE RISE TO CLAIM UNDER ERISA FOR BREACH

OF FIDUCIARY DUTY

Citation: Shook v. Avaya, Inc, CA3 No. 09-4043, 11/2/10`

The Third Circuit Court of Appeals ruled that there could not be an action for breach of

fiduciary duty under ERISA when a participant claimed he had been damaged by a

misrepresentation that caused he and his wife to decide that she should retire from her

job. The case in question involved an employer that had been subject to an acquisition.

The key question became how many years of service the participant would have credit

for under the plan, and to what extent his service to the predecessor employer would

count under the successor employer's plan.

Based on answers the participant had received to inquiries regarding his start date for

various benefits the participant had computed his expected retirement benefit. The

benefit he computed presumed that he would be able to obtain a full retirement benefits

even if he were to be, as it turns out he was, laid off in a force reduction in the near

future. Based on that expected benefit, it was decided that his wife could go ahead and

retire from her job with a different employer. Unfortunately, the actual benefit he

qualified for when he was laid off was substantially less than what he had computed.

Even worse, his wife had retired before he had been laid off.

The Court held that the actions of a non-participant, that is the wife in this case, could

not be the source of a claim for breach of fiduciary duty due to detrimental reliance on a

fiduciary's representation. Rather, the Court held that it was required to show action on

the part of the participant that led to the damages.

The Court noted that the wife's decision to retire had no impact on the participant's

benefits, nor did it have any effect on benefits potentially payable to her as a beneficiary

of her spouse under the plan. The Court found that this was not a reasonably

foreseeable consequence to the fiduciary.

The Tax CurriculumSM

2 Nichols Patrick CPE, Inc.

SECTION: ERISA

WHERE INSURER HAD NO DISCRETION UNDER THE PLAN, BURDEN OF

PROOF NOT SHIFTED TO INSURER FOR DISPUTE OVER TERMINATION

OF DISABILITY BENEFITS

Citation: Muniz v. Amec Construction Management, No. 09-55689, 10/27/10

The Ninth Circuit Court of Appeals sustained a District Court ruling holding an individual

did not qualify for disability benefits under the terms of an employer plan, and that the

plan was justified in terminating the individuals disability benefits.

The individual in question was diagnosed with HIV in 1989, and stopped working in

1991. He began receiving disability benefits under the plan in 1992. In 2005 his claim

came up for periodic review.

After examining medical records submitted by the employee, the insurer determined

that he could perform sedentary employment which rendered him no longer disabled

under the terms of the plan. Eventually the employee filed an appeal with the United

States District Court. The court reviewed the insurer's decision using a de novo

standard of review after finding the plan did not grant discretion to the insurer in this

area.

An expert appointed by the court to perform this review determined that the employee

was no longer disabled under the terms of the plan and the court sustained the denial of

benefits.

The employee argued that because he had presented his own physicians statements

regarding proof of disability, the burden of proof should have shifted to the insurer to

clearly show he was no longer disabled.

The Ninth Circuit declined to follow this result. The Court noted that the employee was

citing cases on the burden of proof under situations where the administrator had

discretion and the test was for an abuse of discretion. In this case, the administrator did

not have discretion and the prior burden decisions did not apply to the District Court's de

novo review.

The Court also found that while the fact the employee had previously been paid

disability benefits may be relevant to the question of whether he remained disabled, that

fact itself did not shift the burden of proof to the plan.

The Tax CurriculumSM

3 Nichols Patrick CPE, Inc.

The key factor in this case was the lack of discretion on the part of the plan

administrator. Where the plan administrator has discretion under the plan, the Courts

have expressed concern that a conflict may exist where the funds to pay the benefit will

come from the organization which is exercising the discretion. However, in this case the

plan did not grant discretion and the District Court conducted its own independent de

novo review of the determination of disability. Thus it appears the Ninth Circuit panel

concluded that the risk inherent when there is discretion did not exist here, and

therefore no special burden rested upon the plan administrator.

SECTION: ERISA

EMPLOYEES WERE AWARE OF FIDUCIARY BREACH SIX YEARS

BEFORE FILING SUIT, THUS THEIR SUIT WAS TIME BARRED

Citation: Brown, et al v. Owens Corning Investment Review Committee, et al,

CA6 No. 09-3692, 9/27/10

Better late than never did not apply to participants in a plan who were alleging the plan’s

fiduciaries should have acted to remove from the plan an investment option in employer

securities for an employer who ended up filing bankruptcy, causing the value of the

stock of the employer to plunge dramatically. The company filed bankruptcy after facing

numerous lawsuits related to asbestos in an industrial insulating product the company

had produced prior to 1972.

Prior to 2000 all employer matching contributions and ½ of the employer’s discretionary

profit sharing contribution was required to be invested in employer stock. The

requirement was dropped via a plan amendment in the year the employer eventually

filed bankruptcy.

The participants did not initiate their suit until six years after the bankruptcy. ERISA

generally limits suits for breach of fiduciary duty to the earlier of six years following the

alleged breach or three years after the participant becomes aware of the alleged

breach. In the view of the Sixth Circuit, which heard this case, such knowledge does

not require that the participant be aware that the matter could qualify as breach under

ERISA, only that the participants be aware of the breach. The court noted that other

circuits do require that the participants be aware of the potential ERISA action,

specifically citing the Third Circuit’s 1992 decision in Int’l Union v. Murata Erie N. Am.,

Inc. The Sixth Circuit indicated that it clearly disagrees with that view.

The Tax CurriculumSM

4 Nichols Patrick CPE, Inc.

The Sixth Circuit ruled that the participants were aware of key facts at the date of the

bankruptcy filing—that the investment had dropped dramatically in value and that

fiduciaries for the plan existed in the area of investment selection. The panel rejected

the claim that they were only aware that the plan could have been amended and not

that fiduciaries existed that could have selected plan investments. The Court indicated

that the receipt of the amendment in 2000 that changed the requirements to invest in

the company stock fund made clear that someone had the authority to select the

investments, knowledge sufficient to trigger the beginning of the statute of limitations.

In a concurring opinion, Judge Helene White took some issue with the majority’s finding

that the making available a summary plan description electronically should be held

against a participant who failed to read the document. Judge White complained that

ERISA imposes a high standard on employers to insure employees actually receive the

SPD, and that the sponsor’s action of simply posting the SPD online did not, in her view,

meet the standard expected for the employer to be able to rely on the disclosures in that

SPD even if an employee did not actually read it.

She concluded that, in this case, this finding did not ultimately change the view that the

participants (including one who failed to read the document) had waited too long, but

the discussion does raise some questions about what is adequate disclosure for such

documents.

SECTION: ERISA

DENIAL OF DISABILITY BENEFIT UNDER PLAN AN ABUSE OF

DISCRETION, ATTORNEYS FEES AWARDED

Citation: Rote v. Titan Tire, CA8 Nos. 09-2510/2890, 7/28/10

While ERISA plan administrators' discretion in interpreting a plan are generally given

deference by the courts, there is a limit—and in this case the administrator was found to

have abused that discretion. The case came at the end of what was a long strike for the

union that the participant was a member in. The participant had surgery to replace the

joints in both of her thumbs. While recovering from the surgery in April 1998, the strike

began—a strike that did not end until October 2001.

When the strike ended, she asked to return to work and was evaluated by a physician

that the administrator selected to determine if she could return to work. The physician

determined there were substantial restrictions on her abilities, and the company

informed her that no jobs existed at the plant that were compatible with the required

restrictions.

The Tax CurriculumSM

5 Nichols Patrick CPE, Inc.

The employer maintained a long term disability plan that covered participants who were

permanently and totally disabled so as to be unable to perform the work of any

classification at the plant. The employee, after much difficulty in obtaining the

paperwork, filed for the long term benefits. The physician who performed her surgery

noted that her restrictions had not changed and in his opinion. However, the employer

summarily dismissed her claim, saying only she was not disabled under the plan.

The employee filed suit, and the District Court found the decision purely conclusory and

lacked the explanation of a denial required under ERISA, and remanded the case for

further consideration. On remand, additional evidence was submitted on the question of

whether her disabilities were permanent. The sponsor focused on a technical reading

that since her attorney initially only asked if these restrictions would continue

indefinitely, that wasn't permanent under the plan. She asked for a review, and her

doctor clarified that when he said indefinitely, he meant that he intended the restrictions

to be permanent.

The District Court and the Eighth Circuit found that the sponsor had abused its

discretion in denying the benefits, finding the case ―wasn't a close matter‖ and ordered

the benefits to be paid. As well, the sponsor was ordered to pay the participant's

attorney fees for both cases and the administrative claim.

SECTION: ERISA 29 USC §1001

PLAN ADMINISTRATOR VIOLATED FIDUCIARY DUTY TO PARTICIPANT

BY NOT DISCLOSING CUSTOMER SERVICE LINE RESPONSES COULD

NOT BE RELIED UPON

Citation: Kenseth v. Dean Health Plan, Inc., CA7 No. 08-3219, 6/30/10

Under ERISA the Seventh Circuit ruled a plan administrator had a fiduciary duty to warn

participants in the health plan it administered that calls to its customer service

department, which participants were directed in documents given to the participants to

call if they had questions about covered procedures, could not be relied upon and the

existence of a second method to obtain a binding ruling had to be disclosed to those

individuals.

The Tax CurriculumSM

6 Nichols Patrick CPE, Inc.

In the case in question a participant who had undergone gastric surgery years earlier

(prior to working for the plan sponsor) to treat morbid obesity developed problems

related to the surgery. The plan Certificate provided that it would not pay for any

surgical treatment for morbid obesity, and on another page of the document it provided

wording that the plan would deny treatment for procedures related to noncovered items.

However the plan had paid for one prior procedure to treat her complications, and when

she faced a more extensive surgery she called the customer service line and was told

the procedure would be covered. But once her surgery was completed, the plan ruled

that the procedure was not covered under the plan and refuse to pay.

The Seventh Circuit ruled that due to the fact that the document was not clear to an

average reader, and it directed the reader to call the customer service line to resolve

issues of coverage the plan violated its fiduciary duty to the participant by failing to

disclose the limits of the customer service representative and the existence of another

means that would be binding. However, the Court found that because the participant

was suing as an individual, and not on behalf of participants as a whole, she could only

seek an equitable remedy—and it wasn't clear if any such remedy would do her any

good. The case was remanded to District Court to determine if, in fact, there was any

equitable remedy being requested, or whether there was no remedy available.

SECTION: ERISA 29 USC §1102(B)(3)

EIGHTH CIRCUIT RULES THAT SUMMARY PLAN DESCRIPTION THAT IS

MORE RESTRICTIVE THAN PLAN DOCUMENT TERMS CANNOT BE

CONSIDERED

Citation: Ringwald v. Prudential, CA8, No. 09-1933, 6/21/10

The Eighth Circuit Court of Appeals, clarifying a previously holding that the District Court

had attempted to rely upon in its decision, held that a Summary Plan Description would

not be considered where it provided for discretion to the plan administrator not granted

in the plan document. The Circuit held that while it had previously ruled an SPD

provision in conflict with the plan that was in the participant's favor would generally

control, that would not be true of SPD provisions that conflicted and granted more

favorable positions for the administrator.

The Tax CurriculumSM

7 Nichols Patrick CPE, Inc.

In this case the participant had been denied disability benefits under an ERISA plan that

limited benefits to 24 months if the disability was due to mental illness. In this case,

there was both a physical ailment (HIV) along with depression, and the plan

administrator (who was also the insurer under the plan) found that the participant was

not disabled based solely on his HIV condition. The District Court, relying on a

provisions in the SPD, but not in the plan document, that granted full discretion to the

administrator refused to review the determination from scratch, and rather only

conducted an abuse-of-discretion analysis, after which it dismissed the participant's

claim.

The Eighth Circuit sent the case back to the District Court to be reviewed de novo. The

Court held that the plan must have provisions to allow the plan itself to be amended,

and no provision allowed for such an amendment to be made informally via the SPD.

As well, the plan contained language that specifically disclaimed the power of the

summary plan description to amend the plan. Thus, the Eighth Circuit panel ruled, the

District Court should not have granted the level of deference that it did to the plan

administrator's decision and sent the case down for a new decision under the standard

it outlined.

SECTION: ACCOUNTANTS LIABILITY

ACCOUNTANT WHO FAILED TO DISCLOSE PROPER AMOUNT OF TAX

ON 7004 FOUND LIABLE TO CLIENTS FOR TREBLE DAMAGES AND

ATTORNEY FEES

Citation: Haddad Motor Group v. Karp, Ackerman, CA1 Nos. 06-2206, 09-

1479, 4/20/10

An accounting firm found that even though it was found not liable for the major claim of

damages against it, its actions were enough to trigger an award of treble damages

under Massachusetts law and, as well, a complete award of attorney fees and costs

incurred by the plaintiffs—amounts that were far in excess of the actual damages found.

The CPA firm in question acquired a client in December of 1997 that was already a

party to a ―margin-against-the-box‖ transaction that gave the corporation access to the

funds represented by appreciated stock it held, but delayed the payment of tax on that

transaction until the position was closed out. The corporation continued with the

accountant, and in December of 1998 met to discuss whether to close out the ―margin-

against-the-box‖ transaction (which incurred fees each year it was kept open) and

whether the corporation should make an S election.

The Tax CurriculumSM

8 Nichols Patrick CPE, Inc.

On February 11, 1999 the corporation closed out the transaction, triggering the gain.

On March 15, 1999 the corporation filed an S election retroactive to the beginning of the

year—and causing the February transaction to be subject to built-in gains tax. In

December of 1999 the accounting firm informed the corporation it was subject to the

built in gains tax, and suggested the corporation file an extension at March 15 due to

the ongoing audit of the corporation’s 1997 return.

An extension was prepared, but no amount was shown as being due with the extension.

When the return was filed on the extended due date, the tax due, plus penalties for

underpayment of estimated taxes, late payment of taxes and interest were imposed.

The client sued the CPA firm asking for damages from the BIG tax and the penalties

and interest. The trial court found no damages from the BIG tax itself, but did find that

the penalties and interest were related to the CPA firm’s failure to advise the client to

make payment earlier.

More troubling, the court found that the firm acted willfully, rather than merely

negligently, based on the fact that the Form 7004 the firm prepared showed a very small

tax liability when the firm at that point knew a substantial liability for the built in gain tax

on this transaction was due. The willful action triggered an automatic trebling of the

$12,345 of damages to $37,035. But that wasn’t the worst of it—the finding also

triggered an award of attorney’s fees and costs in the case that amounted to over

$250,000, which included costs incurred on the portion of the claim for which the

plaintiffs did not prevail (in fact, that appears to have made up the vast majority of such

costs).

On appeal the First Circuit Court of Appeals sustained the result. The Court found it

plausible that the accounting firm had failed to discuss the payments due largely to

avoid having to admit the large amount of tax due that they had failed to warn the client

about, and found very damaging the preparation of the Form 7004 that failed to include

taxes the firm knew were due.

SECTION: FIN48

IRS RELEASES FINAL FORM 1120 SCHEDULE UTP AND MODIFIES SOME

REQUIREMENTS

Citation: Announcement 2010-75 and 2010-76, 9/25/10

The IRS has issued the final Form 1120 Schedule UTP for tax year 2010. In issuing

the final version of the form, the IRS also made modifications from the original proposal

that affects which entities will be required to file the return and the types of items that

will be reported.

The Tax CurriculumSM

9 Nichols Patrick CPE, Inc.

Corporations that file Forms 1120, 1120-F, 1120-L or 1120-PC and issue or are

included in audited financial statements that have total assets exceeding $100 million

must file the schedule for their 2010 tax year. The total asset threshold will be reduced

over five years to include a larger number of corporations. The threshold for filing will

drop to entities with total assets of more than $50 million for 2012 tax years, and down

to total assets of $10 million for tax years beginning in 2014. The IRS indicated that it

will consider whether to extend these requirements to other taxpayers, such as

passthrough entities and tax exempt organizations, for 2011 and later years.

The final schedule dropped the requirement that taxpayers report the maximum tax

adjustment for each tax position listed on the schedule. Rather, taxpayers will required

to rank the positions in order based on the United States federal income tax reserve,

including interest and penalties, recorded for each position on the return. The taxpayer

must also specifically identify those tax positions for which the reserve exceeds 10% of

the aggregate amount of reserves.

The final version of the schedule no longer includes the requirement that a taxpayer

must disclose the rationale and nature of the uncertainty, replacing that with a

requirement that the taxpayer include a concise description of the tax position, including

a description of the relevant facts affecting the tax treatment of the position and

information that reasonably can be expected to apprise the Service of the identity of the

tax position and the nature of the issue.

The IRS has also eliminated the requirement that taxpayers report

tax positions for which no reserve was created due to a widely-understood

administrative practice, but indicated they would ―continue to explore‖ ways to

determine the impact of such positions on overall tax compliance.

The IRS clarified the instructions to indicate that the schedule looks for reporting of tax

positions consistent with the reserve decisions made by the entity for purposes of the

audited financial statements. As well, the unit of account for purposes of the form

should be applied consistent with the treatment in FIN 48. If a corporation uses IFRS or

another comprehensive basis of accounting other than GAAP for financial reporting

must identify a unit of account based on FIN 48 or any other level of detail that is

consistently applied if that identification is ―reasonably expected to apprise the Service

of the identity and nature of the issue underlying a tax

position taken in the tax return.‖

The Tax CurriculumSM

10 Nichols Patrick CPE, Inc.

A number of other clarifications were made to the instructions based on the comments

received. The instructions were clarified to make clear that Schedule UTP requires the

reporting of U.S. income tax positions, but not foreign or state tax positions. As well, a

UTP must be filed once 1) a reserve for a tax position is recorded and 2) a tax position

is taken on the return, regardless of the order of those two events. As well, a

corporation reports only its own tax positions and not those of a related party.

Taxpayers also will not be required to report on tax positions taken in years before 2010

even if a reserve is recorded in audited statements issued for 2010 or later years. The

form is not required to be attached to returns for short tax years ended in 2010. As well,

worldwide assets is used to determine if a corporation meets the filing requirements.

The instructions define an audited financial statement as ―one on which an independent

auditor

expresses an opinion‖ and specifically excludes audited or compiled statements. The

definition of a reserve was clarified to indicate that it includes a reserve for United

States federal income taxes, interest and penalties, and that differences that are

temporary must still be reported on Schedule UTP.

If a corporation's information is included in multiple financial statements, the existence

of a reserve in any of those audited financial statements that relates to a position of the

taxpayer triggers the requirement to file the Schedule UTP.

The IRS did not adopt suggestions that taxpayers not be required to report positions for

which no reserve was recorded because the taxpayer expects to litigate the position,

litigation for which the taxpayer expects to prevail. No guidance is provided on how to

determine such ―expected to litigate‖ positions except to indicate that it ―expects that a

corporation would continue to document its

decision in the same way as it substantiates any decision not to record a reserve in its

financial statements.‖

The IRS also provided that disclosure of a position for other than a reportable

transaction on Schedule UTP will be considered a disclosed position for the purposes of

the penalty under §6662(i) for undisclosed positions lacking economic substance. As

well, complete and adequate disclosure of a position on the Schedule UTP will be

treated as if the corporation had filed a Form 8275 or 8275-R for the position in

question. For the moment such disclosure will not satisfy the requirement to file Form

8886 for listed and reportable transactions, but the IRS is studying whether it may be

possible to eliminate this filing as well for disclosed positions.

The Tax CurriculumSM

11 Nichols Patrick CPE, Inc.

Along with the announcement for the final Schedule UTP, the IRS released

Announcement 2010-76 that modified the IRS's ―policy of restraint‖ of seeking

documents in certain situations. The revised procedure provides that generally the IRS

will not seek to assert that disclosure to the outside auditor of items authorized subject

to privilege amounts to a waiver of the privilege unless the taxpayer has engaged in

other activities that would waive the privilege or it relates to a listed transaction for which

a request is made under IRM 4.10.20.3.

As well taxpayers may redact from any tax reconciliation workpapers related the

preparation of Schedule UTP requested by the IRS during exam that are ―(a) working

drafts, revisions, or comments concerning the concise description of tax positions

reported on Schedule UTP; 3 (b) the amount of any reserve related to a tax position

reported on Schedule UTP; and (c) computations determining the ranking of tax

positions to be reported on Schedule UTP or the designation of a tax position as a

Major Tax Position.‖ The revisions in the notice are to be incorporated in IRM 4.10.20.

SECTION: LEGISLATION

COBRA SUBSIDY PROGRAM MODIFIED, GRANTING RELIEF TO

EMPLOYEES WHO TERMINATE EMPLOYMENT FOLLOWING A

REDUCTION IN HOURS EVENT

Citation: Temporary Extension Act of 2009, 3/3/10

The Temporary Extension Act of 2010 extended the COBRA subsidy qualification

period for one month, from its scheduled February 28, 2010 termination date to March

31, 2010. But in addition it contains a couple of additional provisions that modified the

COBRA subsidy program.

The bill retroactively modified the program to allow individuals whose initial COBRA

event was a reduction of hours to qualify for the subsidy if they later were involuntarily

terminated. Such a person is eligible to elect COBRA coverage at the date of

involuntary termination even if the person had declined coverage at the initial loss of

coverage due to a reduction of hours.

The bill also grants protection to employers who reasonably determine that an

employee was involuntarily terminated. In such a case the employee will be deemed to

be involuntarily terminated for purposes of qualifying for the COBRA subsidy. Without

that protection, it was possible the employer might find upon an IRS examination that

the IRS might decide the termination did not qualify as involuntary and seek to recover

the Form 941 credit.

The Tax CurriculumSM

12 Nichols Patrick CPE, Inc.

These provisions are effective as if they had been originally in the American Recovery

and Reinvestment Act of 2009. For employees that were involuntarily terminated

following a reduction of hours prior to the passage of this bill, a special 60 day election

period is created from the date of enactment of the bill, March 3, 2010.

After the expiration of this provision, Congress yet again extended the program towards

what became a May 31 ending date in the Continuing Extension Act of 2010. When

May 31 comes and goes, we’ll see if Congress yet again gives us a short term

extension of the COBRA subsidy.

SECTION: GAO

GAO REPORTS MOST S CORPORATION RETURNS CONTAIN ERRORS,

RECOMMENDS CORRECTIVE ACTIONS

Citation: Tax Gap: Actions Needed to Address Noncompliance with S

Corporation Rules, GAO-10-195, 12/15/09

In a report to the Senate Finance Committee, the GAO discussed the results of the

IRS’s National Research Project on S Corporations. The GAO found that, per the NRP,

68 percent of S corporation returns filed for tax years 2003 and 2004 had at least one

item misreported that affected net income, resulting in a net underreporting of income of

$85 billion. The GAO also found that returns prepared by paid preparers actually had a

higher error rate of 71 percent.

The GAO also noted significant problems for taxpayers in the computation of basis in

their S corporation shares, resulting in taxpayers claiming losses beyond those allowed

under the law. The GAO suggests that S Corporations be required to prepare a

computation of basis to be given to each shareholder.

The largest median adjustment was for shareholder compensation, amounting to

$20,127. The GAO noted that the largest adjustments in total for compensation took

place on S corporations with a single shareholder, decreasing as the number of

shareholders increased—and for S corporations with 4 or more shareholder there was

actually a negative adjustment.

The GAO also recommended the IRS take action to improve preparer compliance in this

area. The recommendations include licensing of paid preparers, including consideration

of special licensing for S corporation preparers and increased penalties imposed on

paid preparers.

The Tax CurriculumSM

13 Nichols Patrick CPE, Inc.

SECTION: FIN48

FASB GIVES GO AHEAD TO PRIVATE COMPANY REPORTING UNDER

FIN48

Citation: ASU 2009-06, Income Taxes, 9/2/09

After a couple of delays, the Financial Accounting Standards Board gave the go ahead

for the implementation of the measurement and disclosure requirements of FIN48 to

private companies (or ―nonissuers‖ in the current parlance) and passthrough entities,

effective for annual statements with an ending date after December 31, 2009. The

FASB did make some modifications found in Accounting Standards Update 2009-06 in

the final requirements.

The ASU did remove some disclosure requirements for nonpublic entities. Such entities

will not be required to disclose a tabular reconciliation of uncertain return positions, nor

would they prepare a summary of exposures that would change the effective tax rates.

However the other measurement and disclosure requirements of FIN48 will apply to

such entities.

Firms should be readying procedures to handle FIN48 compliance for clients that

require GAAP compliant statements. Firms should also consider the potential impact on

their independence of any assistance tax practitioners render to the client’s accounting

staff in assembling the information necessary to comply with FIN48, specifically

considering issues related to nonattest work covered by Ethics Interpretation 101-3.

SECTION: 11

LAND SURVEYING PROPERLY DEFINED AS ENGINEERING IN

REGULATIONS FOR PURPOSE OF PERSONAL SERVICE CORPORATION

RULES

Citation: Kraatz & Craig Surveying, Inc. v. Commissioner, 134 TC No. 9,

4/13/10

The Tax Court had, in the case of Rainbow Tax Serv. vs. Commissioner, 128 TC

42, had ruled that the definition of accounting for purposes of determining if a C

corporation is a personal service corporation, the field was not limited to those licensed

as accountants under state law. Rather, the court held that we had to test that field

based on its normal meaning.

The Tax CurriculumSM

14 Nichols Patrick CPE, Inc.

Now the Tax Court turns to another of the defined fields for personal service

corporations, engineering. In the current case, the taxpayer argued that land surveying

should not be treated as engineering because state law did not treat land surveying as

engineering, required separate licensing, and the firm had no licensed engineers on its

staff. However, the Tax Court held that the IRS had included surveying in the definition

of engineering in Temporary Reg. §1.448-T(e)(4)(i), and that the definition conformed to

both the legislative record of what Congress saw as engineering and general dictionary

definitions of engineering.

The Tax Court specifically held yet again that state licensing laws do not

determine whether an activity falls into one of the affected categories, noting that due to

lack of consistency among the laws making use of those laws would end up with

taxpayers performing identical services being taxed differently.

Thus, the land surveying firm was subject to the flat 35 percent tax rate on its

taxable income.

SECTION: 38

EMPLOYERS WHO RETAIN "PAYROLL TAX HOLIDAY" WORKERS TO

RECEIVE $1,000 RETENTION CREDIT IN FOLLOWING YEAR

Citation: Section 102, Hiring Incentives to Restore Employment Act, 3/18/10

As a companion to the payroll tax exemption provision of the HIRE Act, the law at Act

Section 102 grants an addition to the general business credit in the following year

(which will generally be 2011) of the lesser of $1,000 per qualified individual who first

meets the following criteria during the tax year in question or 6.2% of the wages paid

during the 52 week measuring period.

The employee must be employed by the taxpayer on any date during the tax year in

question, must be so employed for a period of not less than 52 consecutive weeks and

whose wages for the last 26 weeks of the period equaled at least 80 percent of the

wages paid to the employee for the first 26 weeks of that period. The 52 week period

mentioned above is the ―measuring period‖ for purposes of determining the credit.

Amounts paid to domestic workers and workers eligible for the foreign earned income

exclusion do not qualify as wages for purposes of this credit.

The credit is implemented as a part of the general business credit of §38, but this part of

the credit cannot be carried back to any taxable year beginning before the date of

enactment of HIRE (March 18, 2010).

The Tax CurriculumSM

15 Nichols Patrick CPE, Inc.

SECTION: 41

EXPENSES OF MOLDS SOLD TO CUSTOMERS FOUND TO BE PROPERLY

INCLUDABLE IN COMPUTING RESEARCH CREDIT

Citation: TG Missouri Corporation v. Commissioner, 133 TC No. 13, 11/12/09

The Tax Court held that molds a taxpayer commissioned to be made by a third party

and were later sold to their customers were not ―assets subject to depreciation‖ and

qualified as supplies for purposes of computing the research credit under §41. The

taxpayer manufactured custom molds for customers in the auto industry, outsourcing

much of the work to outside entities. When a mold was complete, the mold would either

be sold to the customer or held by the taxpayer as equipment and depreciated.

In either case the taxpayer used the molds to manufacture parts. If a customer bought

the mold, the charge per unit was lower than if the customer did not do that. However, if

the customer bought the mold it took on the risks of ownership, while otherwise the

taxpayer had those risks. The IRS argued that because molds that weren’t purchased

were depreciated by the taxpayer, the property were ―assets subject to depreciation‖

and their cost did not count currently in computing the research credit.

The Tax Court held that because the sold molds were properly not depreciated by the

taxpayer, they were not such property and the expense did count currently in computing

the research credit.

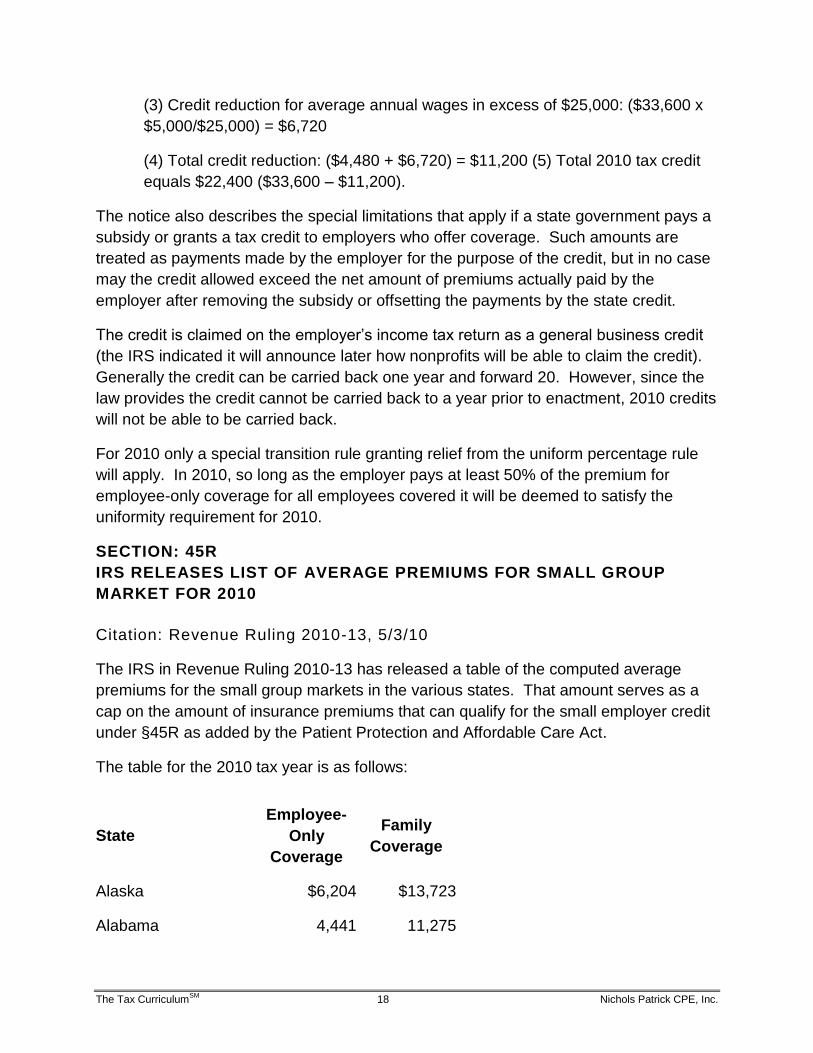

SECTION: 45R

IRS ISSUES EXPLANATIONS AND GUIDANCE FOR SMALL EMPLOYER

HEALTH INSURANCE CREDIT

Citation: Notice 2010-44, 5/17/10

The IRS has provided additional guidance and a general explanation of the application

of the new tax credit for health insurance expenses of small employers. In the notice,

the IRS outlines employer eligible for the credit, the calculation of the credit, and how

the credit is claimed on the return, along with its interaction with estimated taxes and the

alternative minimum tax. The notice goes on to provide transition rules for 2010 that the

IRS had originally committed to provide in the explanation of the credit that was posted

to the IRS website.

The IRS outlines the following steps that are necessary to determine if an employer is

eligible to claim the credit:

Determine the employees who are taken into account for purposes of the credit.

Determine the number of hours of service performed by those employees.

The Tax CurriculumSM

16 Nichols Patrick CPE, Inc.

Calculate the number of the employer’s FTEs.

Determine the average annual wages paid per FTE.

Determine the premiums paid by the employer that are taken into account for purposes

of the credit.