Business Considerations for A&E Firms From Cradle … › Documents › Architects and...Business...

36

Business Considerations for A&E Firms From Cradle to Grave Colleen M. Palmer, Esq. Beazley Group David E. Barker, Esq. Collins Collins Muir + Stewart LLP Lionel Béjean Beazley Group

Transcript of Business Considerations for A&E Firms From Cradle … › Documents › Architects and...Business...

Business Considerations for A&E Firms From Cradle to Grave

Colleen M. Palmer, Esq.

Beazley Group

David E. Barker, Esq.

Collins Collins Muir + Stewart LLP

Lionel Béjean

Beazley Group

This Presentation is protected by US and International Copyright laws. The reuse, duplication or reproduction in whole or in part, other than distribution for informational purposes within your own firm, is prohibited without the written approval of Beazley Group.

This material is intended for informational purposes on the subject and should not be taken as legal advice. Please consult appropriate advisors for guidance applicable to your individual circumstances and/or state requirements.

Copyright & Legal Disclaimer

Starting a business

Sole Proprietorship

You as you. No corporate

entity.

All income and losses straight to your taxes.

All liability straight to

you.

Can enter contracts, hire employees, take loans, incur

debts.

Can operate under a fictitious

business name (“dba”).

Normally handled on a local (city or county) level.

Partnership

Two or more people (or entities)

combining for a business purpose.

All income and losses flow

straight to the partners taxes.

Written partnership

agreement not required, but

strongly suggested.

All liability straight to the

partners.

*CPAs frequently say they like partnerships because it allows greater flexibility on the distribution of income and losses.

Limited Partnership

• Big brother/little brother arrangement

• Must have at least one general partner.

o General Partner has unlimited liability and generally runs the business.

• Can have multiple limited partners.

o Should not have management responsibilities.

o Limited Partners have limited liability (a liability shield).

• Income and losses all go through to the partners (general and limited).

Limited Liability Partnership (LLP)

• A partnership just for professionals.

• Each Partner is responsible for their own professional obligations, but has a shield from partnership liabilities.

• Pass through of income and losses.

• Normally have specific insurance requirements.

Limited Liability Company (LLC)

• Not allowed in all states for professionals. o Can create an issue for multi-state practice that chooses this form.

• Owners are called members.

• Considered a separate legal entity.

• Members have a liability shield for actions of the LLC. o Note as professionals – still personal liability for professional

services.

• Pass through treatment of income and losses.

• Some states have additional tax burden on LLCs.

• Some states have specific insurance requirements for LLCs.

Professional Limited Liability Company (PLLC)

• Most states that do not allow professionals to form an LLC allow a PLLC.

• Formation normally requires an additional step of approval by the state licensing board.

• Limited Liability o But individual may still face

personal liability for professional acts they perform.

• Key document is the operating agreement.

o Similar to a partnership agreement, it sets out the rules for operation.

• Flow through taxation.

• Otherwise generally operates like a normal LLC.

Corporation

• Separate Legal Entity

• Owners are shareholders. o Liability is limited to the amount of shareholders investment.

As a professional – may still have personal liability for professional services you provide.

• Annual election for the board of directors.

• Board of directors run the big picture. They appoint the officers that run the day to day.

• Double taxation.

S- Corporation • Technically a regular corporation with a subchapter S election.

o File a form with the IRS.

• Allows flow through taxation (avoid double taxation).

• Limited to 100 shareholders.

• Stockholders cannot be: o Another corporation (with certain limited exceptions) o Non-resident aliens o Partnership o LLC (with certain limited exceptions) o Business Trust

• Otherwise works like a regular corporation (C-Corporation).

Professional Corporation

A Corporation just for

professionals.

Rendering professional services in a

single profession.

Shareholders must all be licensed in

the profession.

Otherwise operates

like a normal

corporation in other respects.

*Can be licensed in different states.

Joint Venture

• A business venture for a specific purpose.

• Can be any form of business that a professional can form.

• Oral agreement is allowable but not recommended.

• Important to address issues such as: oManagement decisions o Accounting o Liability o How insurance will work

Insurance Needs

Starting up – what do you

need

Higher limits

Deductible – keeping up with

growth

Being purchased? – tail, roll

coverage, etc.

Buying another firm?

– tail, roll coverage, etc.

Retiring?

Starting up

Risk management

Deductible

Limits

Claims

Higher limits

Higher limits

Client requests

Types of projects

Size of your firm

Claims

Deductible

Client requests

Size of your firm

Claims

Being purchased

• Think about insurance at the beginning of the talks

• Tail

• Roll into the acquiring firm’s program

• Retro coverage

Buying another firm

• Think about insurance at the beginning of the talks

• Tail

• Roll into the acquiring firm’s program

• Retro coverage

Retiring

• Tail

• Travel plans

• Golf clubs…

Insurance

• Professional Liability

• General Liability

• Automobile Liability

• Workers Compensation

• Employment Practices Liability (EPLI)

• OCIP/CCIP

Professional Liability

• Also known as errors and omissions

• Covers professional services o Does not cover obligations incurred by contract

Unless you would have that obligation in the absence of the contract.

• Typically on a “claims made” or “claims made and reported” basis

• Limits are per claim and in the aggregate

• No “additional insured” endorsements

General Liability

• Also known as CGL – Commercial General Liability, or an older term, Comprehensive General Liability

• Does not cover professional acts

• Would cover non-professional liability

• Typically on an occurrence basis

• Can have an additional insured endorsement

Automobile Liability

• Basically the same as your personal auto policy

• Covers liability and damages for property damage and bodily injury

• May cover owned (vehicles your company owns) and non-owned vehicles (your employees driving their cars)

Worker’s Compensation

• Covers your employees for injuries they get while on the job

• This works as a trade off:

o You, the employer, get a “cap” on the damages. For a broken arm the employee gets a fixed amount of money.

o The employee gets an easier lawsuit in that they don’t have to file a normal lawsuit – they go through worker’s compensation and they don’t have to prove all of the elements of a normal lawsuit.

• This is required by law.

o If you have employees, you have to have worker’s compensation insurance.

• There are different forms this can take: actual insurance, group funds (self insured group)

Employment Practices Liability (EPLI)

• Covers various employment related claims such as: o Sexual Harassment oWrongful Termination o Discrimination (religion, age, race, gender)

• Covers claims by current, past, and prospective employees.

• In addition to claims history, pricing is generally based on the size of the business, the industry of the business, and may involve reviewing aspects such as the company’s policies for hiring and firing as well as written policies and procedures (employee handbook)

OCIP/CCIP

• Owner Controlled Insurance Policy • Contractor Controlled Insurance Policy

• Larger policy typically for larger projects

• Normally each participant in the project contributes to the payment of the premiums (e.g., 1% of your fee is held back and goes to the payment of insurance)

• Be very careful about what is covered and not covered.

o Typically do not cover professional acts, or have significant limitations on the professional coverage that they provide.

Intellectual Property • Architectural Copyrights: protects the overall layout, design, and

composition of spaces – but not individual elements.

oYou own what you create. A business owns what its employees create in the course and

scope of their employment.

oBuilding your plans is making a copy of those plans. oIf someone builds your plans without your permission, you may be able to get a court order to stop them, or you may be able to get damages for their infringement. oContracts may have provisions for ownership of plans, assignment of copyright, or the license of the copyright.

Employees • Classification of employees: exempt vs. non-exempt

• State laws on overtime/meal and rest breaks • Required postings • Benefits: insurance, vacation, sick leave, medical leave • Independent contractors • At will employment • Interns

Succession Planning

• When it is time to retire there are generally three options:

• Planning for any of the above takes time. o Can’t start this process 6 months before you want out.

Acquisition Internal Dissolution/ Wind Down

Succession Planning - Acquisition • Generally three forms: stock sale, asset sale, merger

o Stock sale: you sell the stock (or membership) to the buyer. They get the good, bad, and ugly – assets and liabilities.

o Asset sale: Buyer takes only the assets and leaves you with the liabilities.

•Your existing business still exists and you will need to address the continued existence.

oMerger: Governed by state and potentially federal law.

•Two companies become one. •Assets and liabilities both go with the new/surviving company.

• All of them, but particularly asset sales, have significant insurance

considerations.

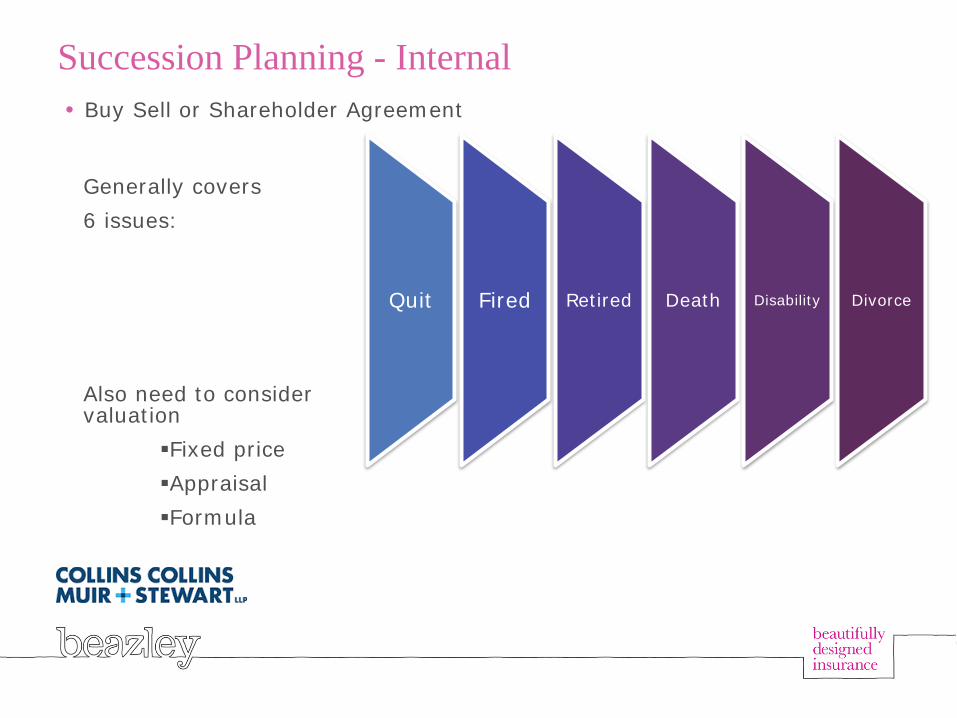

Succession Planning - Internal • Buy Sell or Shareholder Agreement

Generally covers 6 issues:

Also need to consider valuation

Fixed price Appraisal Formula

Quit Fired Retired Death Disability Divorce

Succession Planning – Dissolution/Wind Down

• Considerations: o Existing contracts

Terminate Assign them

o Employees o Pay off liabilities/debts o Sell off assets o Distribute any remaining money

Overall Considerations For Your Business

• Three key partners for your business:

• Expect the unexpected

• Don’t rush too fast – enjoy the ride.

CPA Insurance Broker Attorney

Questions David E. Barker, Esq. Collins Collins Muir + Stewart LLP 10681 Foothill Blvd. Suite 260Rancho Cucamonga CA 91730 [email protected] Lionel Béjean Beazley Group 15305 Dallas Parkway, Suite 1060 Addison TX 75001 [email protected] Colleen M. Palmer, Esq. Beazley Group 1270 Avenue of the Americas New York NY 10020 [email protected]

Thank you for participating in the Beazley webinar,

Site coordinators For premium and CE credit, you must complete an attendance form online (deadline tomorrow) at http://bit.ly/BZ1809a All attendees Please complete an evaluation form at http://bit.ly/BZ1809ev Engineers registered in Florida or North Carolina For CE credit in Florida and North Carolina, engineers (not architects) must complete a 10-question quiz at http://bit.ly/BZ1809q (deadline tomorrow) Engineers registered in North Carolina Please complete a separate evaluation form at http://bit.ly/BZ1809evnc Certificate of Attendance We will issue certificates of attendance to site coordinators by email in about three weeks. Questions? If you have any questions, please contact [email protected]

Webinar managed and hosted by Synthesis Partnership www.synthesispartnership.com

Business Considerations for A&E Firms From Cradle to Grave